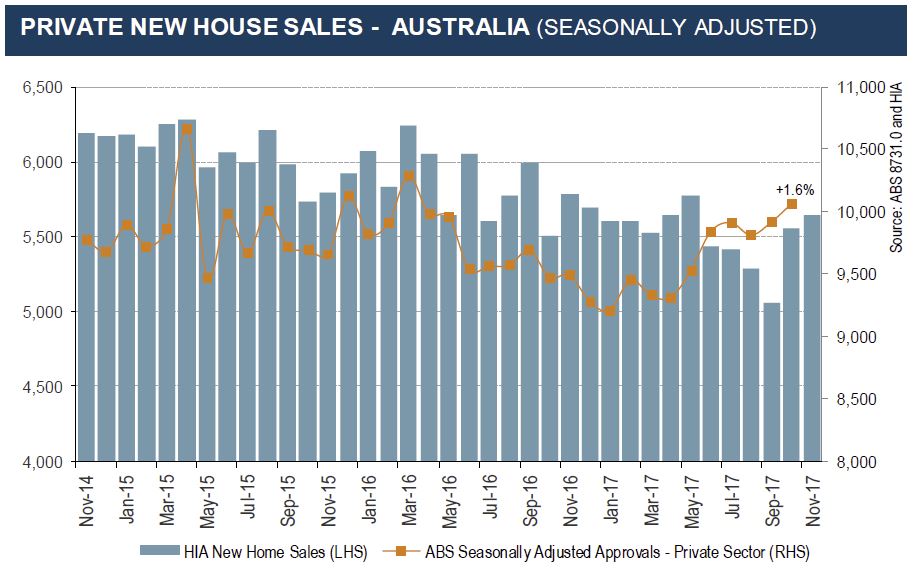

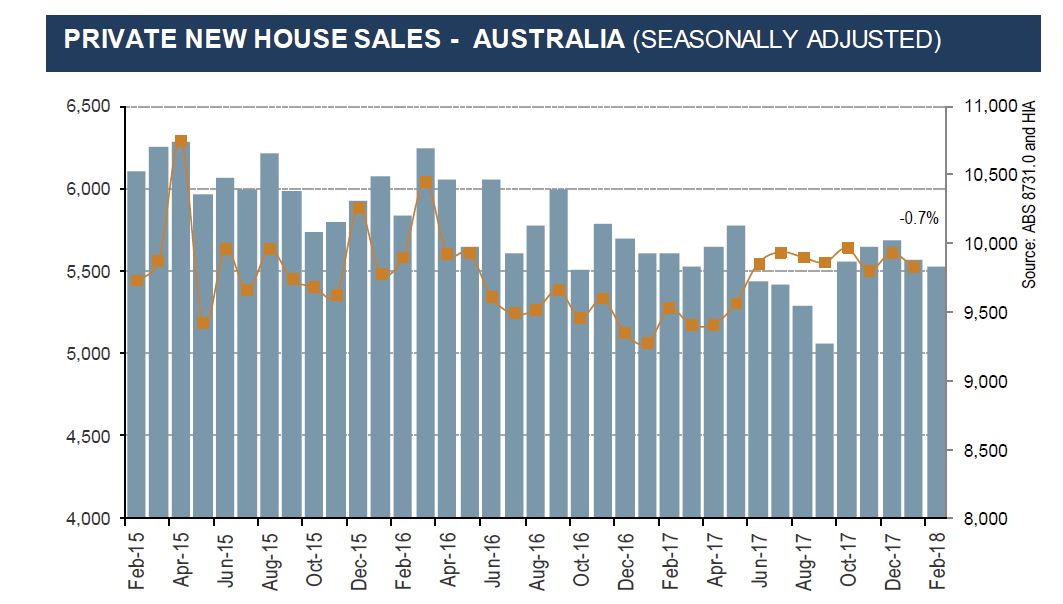

The HIA says sales of new detached houses declined for the second consecutive month during February 2018 overall, but the markets were patchy, based on results contained in the latest edition of their New Home Sales report – a monthly survey of the largest volume home builders in the five largest states.

Despite the fact that the overall volume of sales declined during February, reductions only occurred in two of the five states covered by the HIA New Home Sales Report – the magnitude of these reductions outweighed the increases which took place elsewhere. The largest fall was in Queensland (-16.3 per cent) with a 9.9 per cent contraction recorded in WA. The largest increase in sales was in NSW (+11.7 per cent), followed by SA (+10.3 per cent) and Victoria (+4.8 per cent).

“The decline in new house sales during the first two months of 2018 is consistent with our expectation that residential building activity will move lower over the next 12 months.

“Tighter restrictions around investor lending and heavier obstacles to foreign investor participation are contributing to the weaker conditions in new dwelling construction.

“New house sales in NSW saw decent growth during February. There were several favourable changes made by the NSW government relating to First Home Buyers last year and these have been beneficial to the state’s housing industry.

“Our forecast is that new home sales will trend downwards during 2018 in line with new home building activity. We expect things to bottom out in late 2019 before modest growth resumes,” concluded HIA Senior Economist Shane Garrett.