Moody’s Investors Service says that underwriting discipline and capital are key variables in maintaining the health of bank credit profiles in Australia, in the face of rising housing market imbalances.

“Rapid house appreciation, particularly in Sydney, as well as lending imbalances are increasing the risks of a housing market correction,” says Ilya Serov, a Moody’s Vice President and Senior Credit Officer. “This poses long-term challenges to Australian bank credit profiles”.

“We expect that over time the banks will revise up their mortgage risk weights and capital levels to better recognize the rising tail risks embedded in their housing portfolios,” adds Serov .

Moody’s analysis is contained in its just-released report titled “Rising Housing Market Imbalances Pose Long-Term Challenges for Australian Banks,” and is authored by Serov.

Moody’s report points out that dividend policy initiatives announced recently by major Australian banks — including National Australia Bank’s announcement of a capital raising of AUD5.5 billion — represent the start of a capital accumulation phase that is likely to extend well into 2016.

In Moody’s assessment, the risks in Australia’s housing market risks are skewed towards the downside. While over the short run, stability in the housing market will be supported by low interest rates and the healthy state of bank balance sheets, elevated and rising house prices are intensifying imbalances in the housing market.

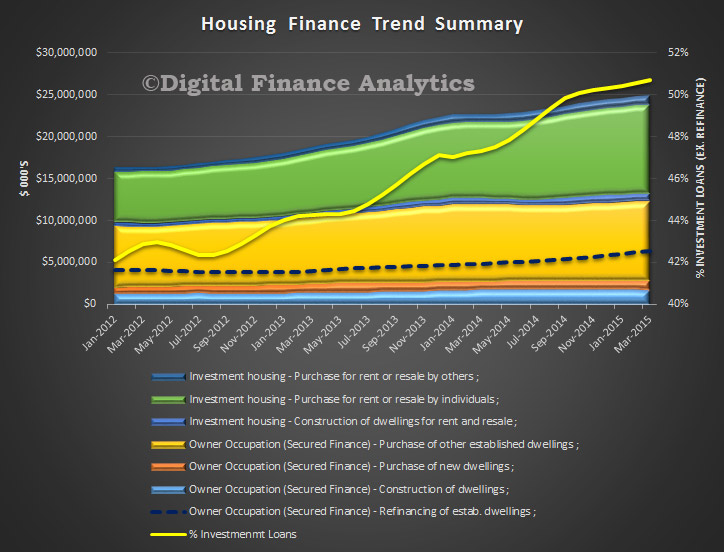

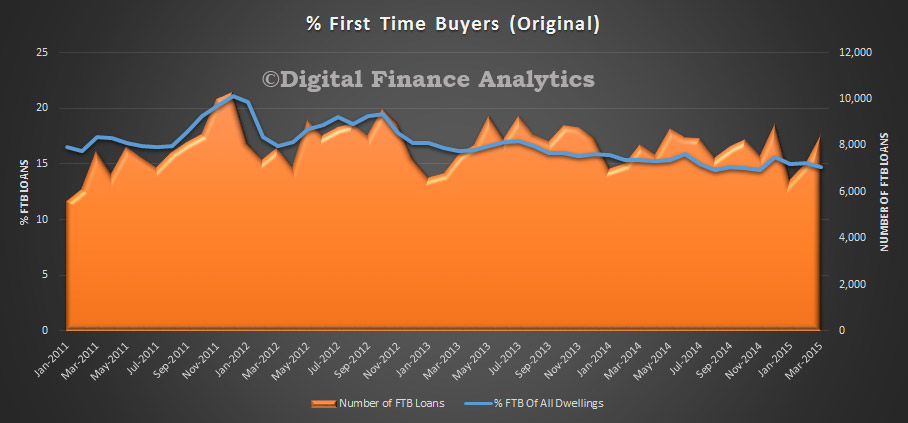

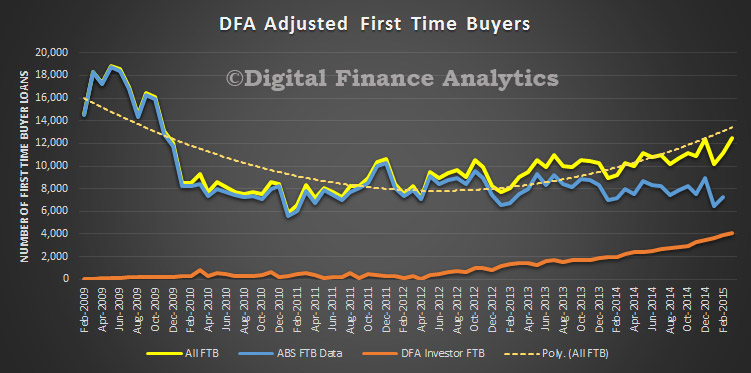

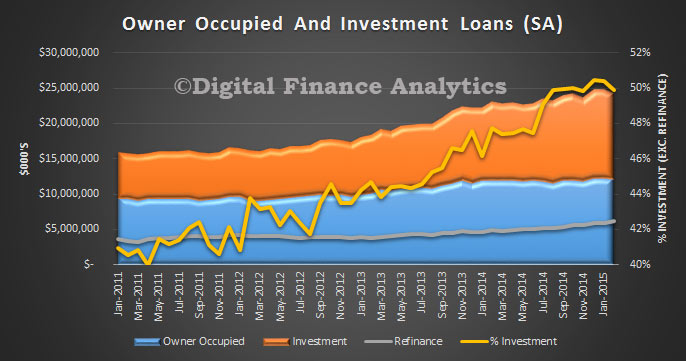

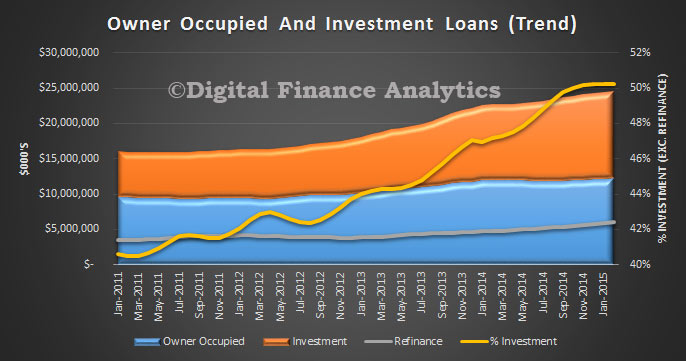

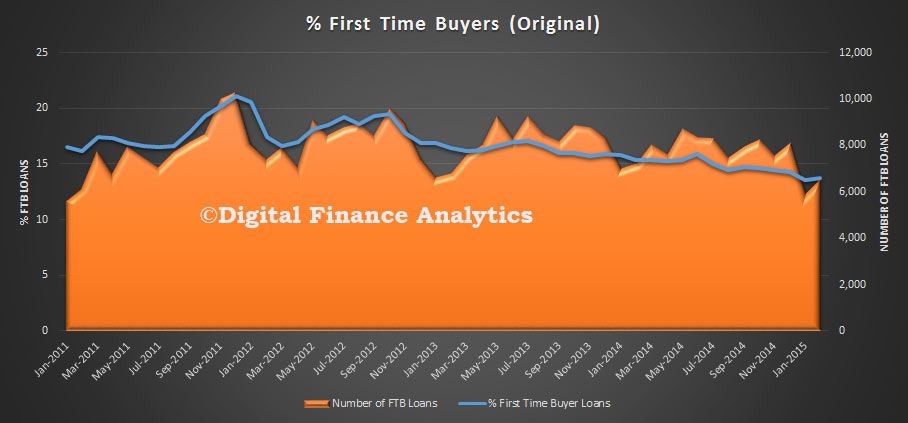

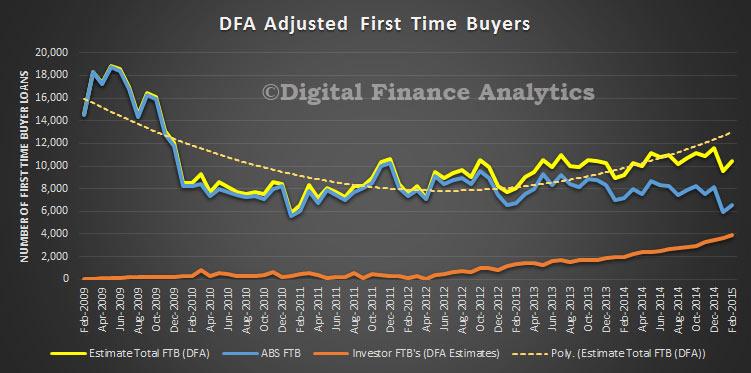

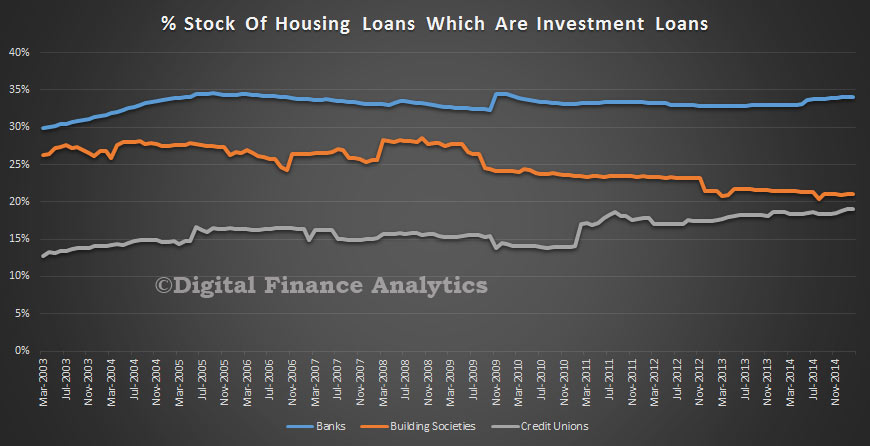

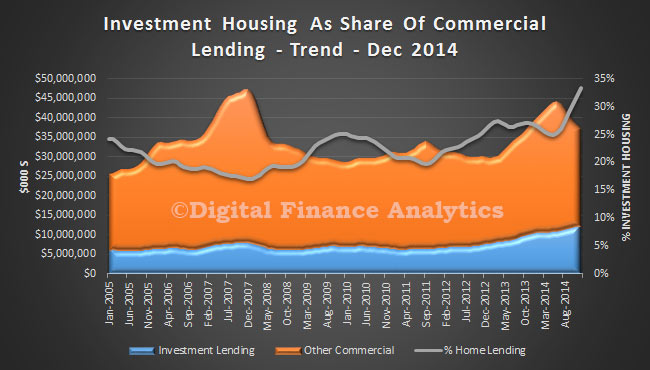

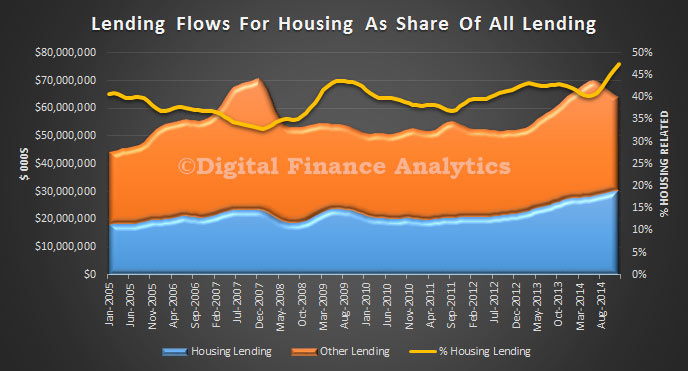

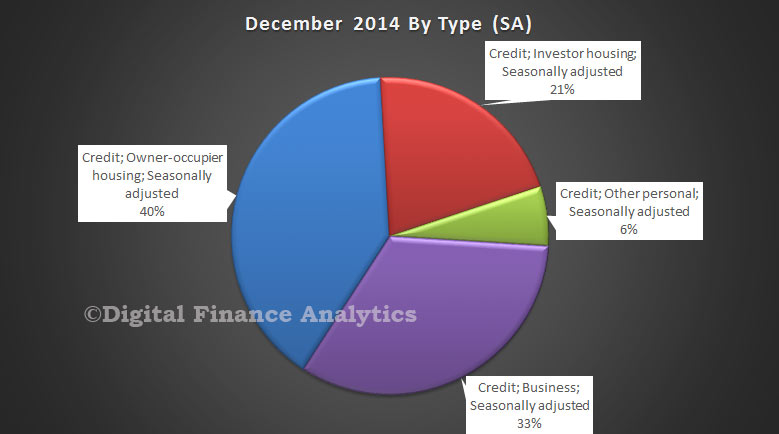

Moody’s evaluation of the Australian housing market suggests that housing affordability is falling, despite the low interest rate environment. Similarly, lending imbalances, including a decline in the proportion of first-time home buyers and a sharp rise in residential investment activity, pose a further source of risk.

In Moody’s view, Australian banks are well-positioned to adjust their origination practices and capital levels to better recognize the rising tail risks embedded in their housing portfolios.

Moody’s report says likely regulatory changes will see average mortgage risk weights for the major banks in Australia increase to the 20%-25% range, up from the current 15%-20%. It estimates that Australia’s four major banks — National Australia Bank Limited (NAB, rated Aa2 stable, a1), Westpac Banking Corporation (Aa2 stable, a1), Australia and New Zealand Banking Group Limited (Aa2 stable, a1) and the Commonwealth Bank of Australia (Aa2 stable, a1) — are well-positioned to absorb such a change.

However, Moody’s also anticipates a broader increase in regulatory capital requirements, in line with the November 2014 recommendation by Australia’s independent Financial System Inquiry that Australian bank capital ratios should be “unquestionably strong” and rank in the top quartile of internationally active banks. This scenario would necessitate deeper adjustments to the banks’ dividend policies, and potentially the raising of new capital.

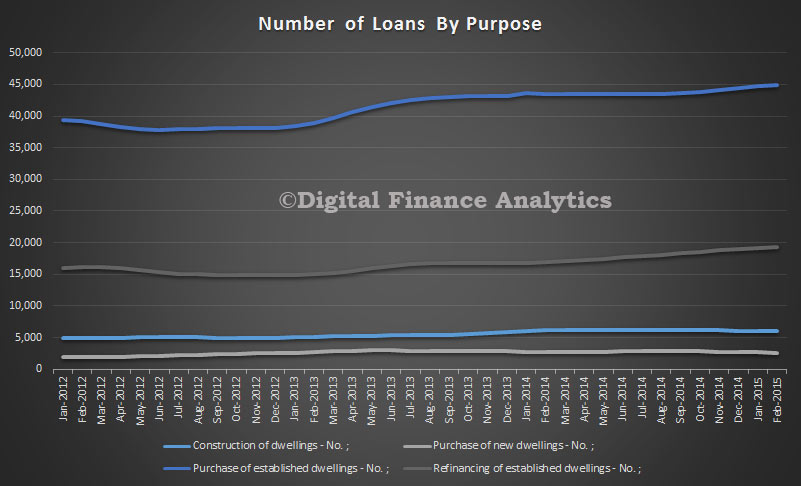

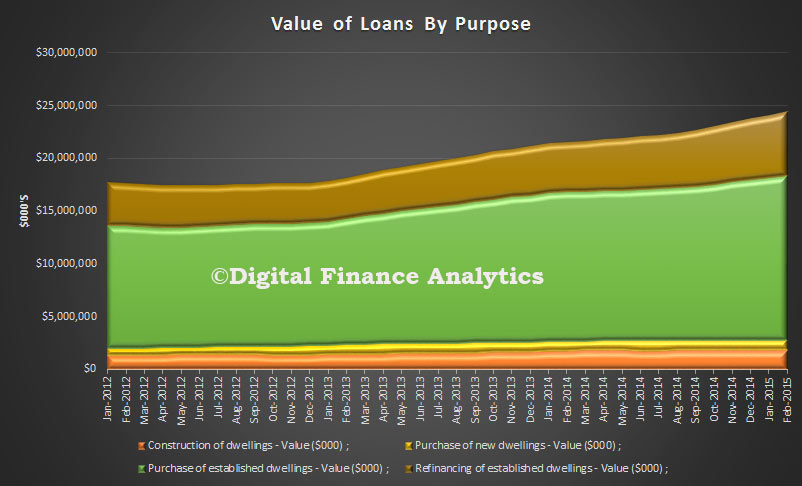

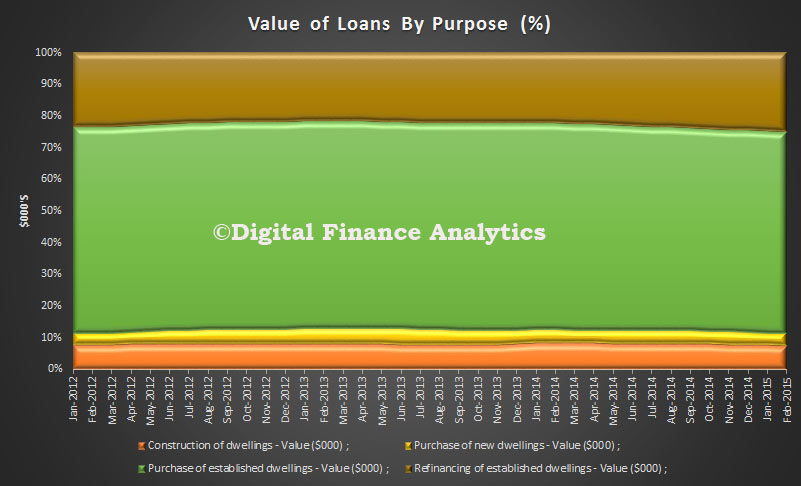

Moody’s report points out that the latest regulatory data suggests that Australian banks have become more conservative in their underwriting, as they have curtailed their exposure to high loan-to-value ratio loans. Such moves would help offset the risks posed by the country’s deepening housing market imbalances.

The rating agency sees ongoing adjustment to banks’ underwriting practices to bring them into line with the guidelines released by the Australian Prudential Regulation Authority in December 2014, which include limiting growth in investor housing loans to 10% per annum and specific guidance around stressed debt-service requirements, as supportive of the banks’ high rating levels.

Moody’s report notes that since May 2014, median home prices have risen by 10% nationwide, and by 16% in the core Sydney market . The report further notes that Australian home prices have risen by 23% since the start of the latest interest rate cutting cycle in November 2011.

Overall, Moody’s says that the banks’ asset quality metrics and portfolio quality will remain strong in calendar 2015, supported by Australia’s low interest-rate environment.