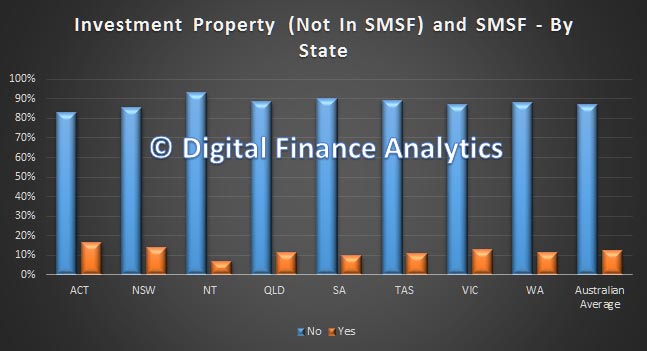

More than one in three portfolios with Sydney property would be at risk, says DFA, compared with Melbourne where one in four properties could be impacted.

“These are investors who would not have income or savings to pay for their investment property mortgages if rent were to stop,” says Martin North, principal of DFA.

His consultancy puts the number of property portfolios that may be affected at 36,000 based on analysis of household surveys, public and private data to model the nation’s property market.

Increasing supply of houses and apartments and falling rents are already creating pressures for many investors, North warns.

About 20 per cent of investors in Brisbane property could be at risk, compared with under 10 per cent in Adelaide, Perth and Canberra, according to the analysis.

Weak cash flows from investment properties, low equity, high gearing and large loan commitments are loud warning bells for investors to review, restructure and roll back debt, say investment advisers, mortgage brokers and analysts.

Reserve Bank of Australia governor Philip Lowe cautions that too many banks are giving owner occupier and investor loans to struggling investors, increasing the risk of defaults if even small shocks hit the economy.

Mario Borg, principal of Mario Borg Strategic Finance, says: “Not having the cash flow to maintain your repayment commitments is where you can run into trouble.”

Borg, who owns a mix of houses and apartments in a personal portfolio worth more than $10 million, adds: “There is no one-size-fits-all when it comes to an optimal portfolio size, as everyone’s financial situation and personal circumstances are different.”

He creates a buffer against potential financial stress caused by falling markets or rising rates via borrowing only 30-40 per cent on investment properties.

“Ask yourself whether you can still maintain your investment loan portfolio if interest rates were 2 per higher,” he recommends for stress testing a portfolio.

For example, a rate rise from 5 per cent to 7 per cent on a $1 million loan for a borrower with an 80 per cent loan to valuation (paying principal and interest) would mean a monthly repayment increase of $1222 to $7,068, according to research house Canstar.

“You should also ask whether there are adequate financial buffers in place should the unforeseen happen and you lose your job, or the business takes a turn and cash flow is reduced all of a sudden,” suggests Borg.

Christopher Foster-Ramsay, principal of Foster Ramsay Finance, says borrowers will need to face up to higher interest, bigger deposits and much closer scrutiny of their finances and ability to repay.

“There is going to be an upheaval for property investors,” he warns. “Obtaining interest-only loans is going to get very hard.”

Daren McDonald, head of property for property consultancy ShineWing Australia, urges investors to review their holdings to ensure they are maximising each property’s potential and investment returns.

“Property is generally an illiquid investment, so good planning is required, forecasting and risk assessment is required,” he says.

McDonald, who has advised on property for more than 20 years, recommends investors look at ways of improving their portfolio’s income and valuations, reconsider financing options to satisfy changing conditions and consider asset protection and taxation implications.

He offers detailed commentary on how to review a property portfolio in the accompanying checklist.

The nation’s trillion-dollar love affair with property has been cemented by historically low interest rates, generous negative gearing allowances and heady property price rises in Melbourne and Sydney.

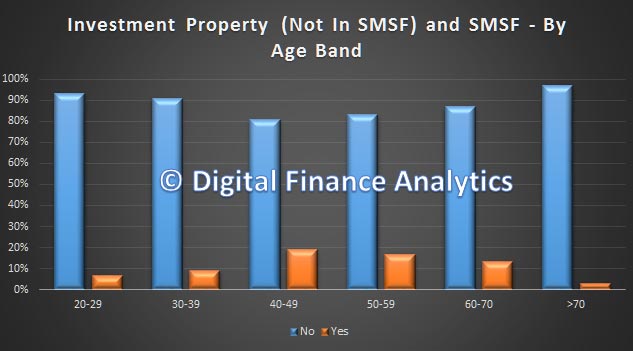

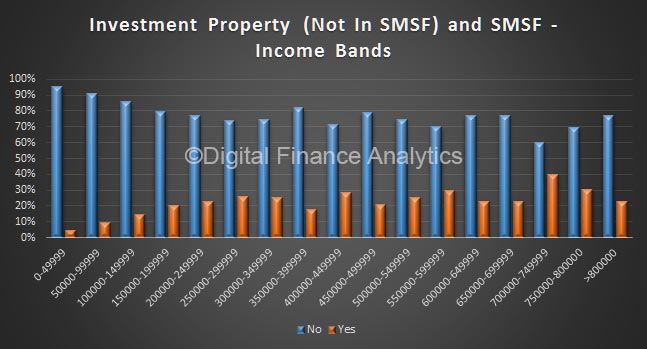

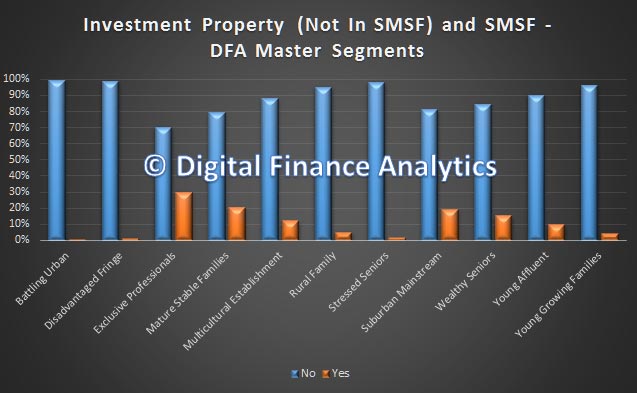

The average Aussie property investor has two properties, says DFA’s North, with the bulk of the remainder having between three and five.

North says the “striking observation” about households with large numbers of investment properties is the size of their debt, preference for interest-only loans and smaller number of quality portfolios.

“That means they are the most vulnerable to a rapid interest rate increase or a downturn in property values, which is likely to impact lower-quality properties first,” says North.

Investors dumping property into the market will trigger bigger falls, analysts warn.

The property market’s outlook, values and returns vary widely between cities and sometimes postcodes.

For example, house prices in Perth and Darwin dropped by up to 7 per cent during the past 12 months. Falls were even bigger for apartments.

Melbourne is the nation’s top performer with houses up by more than 7 per cent and units 5 per cent. Melbourne and Sydney are regularly posting weekend auction clearance rates of 80 per cent or higher.

Since March more than 20 banks have increased the cost of nearly 300 mortgage products by between 5 basis points and 60 basis points, says Canstar,