To prevent its bond yields from rising, Italy needs a bailout now, not later. Specifically, it needs a dedicated firewall of at least €500 billion . This is because if bond yields were to rise too high too quickly, Italian public finances will deteriorate, and Italy will then be increasingly unable to roll over its debt.

The European Central Bank is the only authority with the wherewithal to finance this bailout. But they won’t at the moment.

The bond market has been pricing an implicit ECB guarantee concerning Italian sovereign debt. Thus, should the ECB fail to act this could become another global credit crisis trigger. So the ECB is basically being held hostage by the bond markets.

At present, the ECB only has the authority to purchase an additional €150 billion of Italian debt before it breaches the self-imposed 33% issuer limit. German and Dutch hawks on the ECB governing council have expressed opposition to even contemplating any breach of this ceiling. This impending bailout will test European political unity shortly.

The ECB must ride to the rescue over the objections of the fiscally upright German and Dutch council members, assuming all of the repugnant moral hazard that comes with that. The only alternative is an Italian default and subsequent “Italexit” that would send shockwaves reverberating throughout financial markets worldwide. And it would blow-up the Eurozone in a heart beat.

Reuters is reporting that payments on mortgages will be suspended across the whole of Italy after the coronavirus outbreak, Italy’s deputy economy minister said on Tuesday.

“Yes,

that will be the case, for individuals and households,” Laura Castelli

said in an interview with Radio Anch’io, when asked about the

possibility.

Italy’s banking lobby ABI

said on Monday lenders representing 90% of total banking assets would

offer debt moratoriums to small firms and households grappling with the

economic fallout from Italy’s coronavirus outbreak.

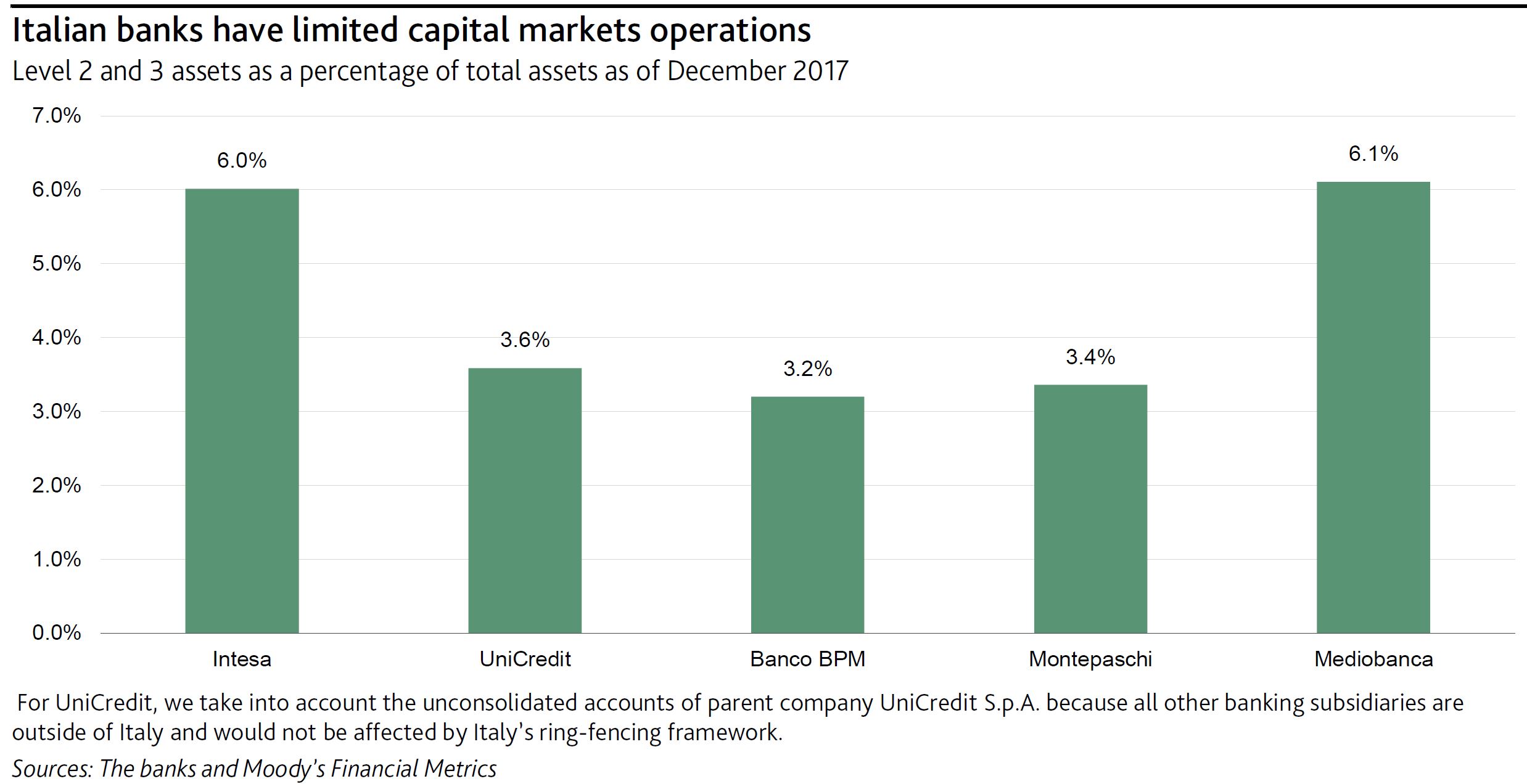

Last Wednesday, Italian Prime Minister Giuseppe Conte announced that the newly formed government will seek to separate investment banking operations from other commercial operations, similar to the recently implemented ring-fencing in the UK.

Although the government’s goal is to protect retail depositors, we believe that ring-fencing, if implemented, would have a limited effect on the operations of Italian banks because only a handful of banks have material capital markets operations that could drive losses to retail clients.

Unlike other European banks, Italian banks’ investment banking operations have not produced large losses because of their focus on more traditional commercial banking activities. Additionally, a large share of Italian banks’ investment banking activities are already booked in separate legal entities, requiring only minor structural changes.

UniCredit S.p.A. already books a large portion of its corporate and investment banking division at its wholly owned German subsidiary UniCredit Bank AG. Intesa Sanpaolo S.p.A. books its capital market operations at its wholly owned subsidiary Banca IMI S.p.A. Banco BPM S.p.A. and Banca Monte dei Paschi di Siena S.p.A. have very limited capital market operations, and conduct most of their capital market activities through fully owned subsidiaries: Banca Akros for Banco BPM and MPS Capital Services S.p.A. for Montepaschi. Mediobanca S.p.A. already carries out its retail and investment banking activities in different legal entities.

We believe the portion of assets that would be transferred to non-ring-fenced banks would be limited for two reasons. The first is that Italy’s ring-fencing regulations will likely follow the UK model of applying only to large banks. The second is based on our calculation using the percentage of so-called Level 2 assets (whose values can be approximated using observable prices as parameters) and Level 3 assets (whose values banks estimate themselves because of a lack of observable prices) as a proxy for capital market operations, which leads us to estimate that Italy’s large banks’ Level 2 and 3 assets comprised less than 7% of their total assets as of December 2017, as shown in the exhibit.

These amounts are close to the 7% of assets that Lloyds Banking Group plc recently transferred to the newly established non-ring-fenced bank Lloyds Bank Corporate Markets plc. For Lloyds, before the implementation of ring-fencing, we had noted that the new framework was unlikely to materially affect the bank’s strong fundamentals; since Italian banks and Lloyds have similar business models focused on retail activities with little capital market operations, we believe that ring-fencing will also not materially affect Italian banks’ fundamentals.

Italy’s proposal to unwind mutual-bank reform is credit negative

In addition, Italy’s Prime Minister Giuseppe Conte announced that the newly formed government would seek to reverse the previous government’s reforms to consolidate the fragmented mutual-bank sector, without providing a specific rationale. If adopted, mutual banks would not be required to become affiliated with a group with shared cross-guarantees — an attempt to consolidate Italy’s highly fragmented banking system. The proposal, if enacted, would be credit negative for mutual banks because these small institutions will remain exposed to a fragile operating environment, with limited product diversification and economies of scale, and will not reap the benefits of being part of a large and cohesive group.

Mutual banks are savings banks in which each shareholder has one vote irrespective of the number of shares held. In December 2017, Italy had 295 mutual banks, which in aggregate comprised a material portion of the Italian banking system, accounting for a 7.8% market share for retail funding (deposits and bonds) and a 7.2% market share for loans. With the reform to consolidate mutual banks, the previous government wanted to improve financial stability in Italy by creating larger and more solid mutual banking groups. Doing so would have created banks with sufficient scale to access the international equity and debt markets and face challenges from the operating environment, reducing the risk of weaker banks failing.

On a standalone basis, single mutual banks are generally small, averaging 14 branches, 100 employees and around €400 million in loans and retail funding. If they were combined into a single group, mutual banks would be the third-largest banking group in Italy, with €131 billion loans after UniCredit S.p.A. and Intesa Sanpaolo S.p.A. And, although some have performed well, several have been put under administration by the Bank of Italy or required rescue by other mutual banks.

Currently, mutual banks have a certain degree of independence and can decide at their discretion the level of integration within Italy’s mutual bank network. This structure leaves them exposed to daunting challenges including competition, low profitability from traditional mortgage and savings business in the low interest rate environment, large investments in digitalisation to meet changing customer behaviour and

Salvini has responded to the refugee crisis by saying that Italy needs “a mass cleaning – home by home, street by street, neighbourhood by neighbourhood”. Grillo, meanwhile, has championed the idea of celebrating “V-Days” – short for the Italian vaffanculo (the various English translations all begin with an expletive and end with either “off” or “you”) – taking aim at the political elite as part of an eccentric grab bag of largely anti-capitalist policy ideals.

Setting aside the bizarre prospect of a coalition between the far right and the loopy left, as a prospective government the pair do not bode well for Italy or Europe. Although officially disavowing any move to exit the Eurozone, they almost surely would have sought to do so. That would have triggered an automatic exit from the European Union, perhaps inevitably nicknamed “Quitaly”.

Italy, and the European experiment with it, might have bled out slowly.

But when Italian President Sergio Mattarella refused to allow the putative coalition to form government in its currently proposed form, all hell broke loose.

With a second election now on the cards, the spread on two-year Italian bonds quickly jumped to around 300 basis points over German bonds. That’s the market suggesting a staggering risk of default.

Yesterday Mattarella tried to calm things down by suggesting that he could appoint an interim technocratic government, giving Salvini and Five Star’s current leader, Luigi Di Maio, more time to produce a list of ministers that he could live with.

That’s probably the right thing to do, but it’s tough to get the toothpaste back in the tube. The markets are spooked. It will take a lot more than the prospect of securing a coalition government between two lunatic-fringe parties bent on getting Italy out of the euro to calm things down.

Greece is the word

Italy is Europe’s third-largest economy and it has public debt of €2.3 trillion. A bank run on the Italian economy, similar to what happened in Greece in 2015, would be a cataclysm that would likely be impossible to stop without Italy exiting the euro.

The seeds of Italian populism were fairly predictable in the wake of the great recession. Italy’s unemployment rate doubled to more than 12% and is still at 10.9%. Youth unemployment peaked at a 42.7% in 2014 and remains around 35%. GDP fell by more than 7% per year at an annualised rate and only turned positive in 2014. Real GDP is still below its 2007 level. Italy’s current GDP growth of 1.5% is the lowest in the Eurozone.

The question is what to do about it. Radical spending promises that can’t possibly be fulfilled without totally blowing the government’s books are not the answer. Having them delivered by an unstable government comprised of a loose coalition of warring tribes is less encouraging still.

On the other hand, fresh elections will just spook the markets even more.

Right now, Mattarella’s proposed technocratic government looks like the least worst option. There is an open question about how long it should govern for, but a reasonable starting point would be three years. That might give it time to get the Italian economic ship back upright. Enough time to take some tough decisions. This, of course, simply cannot be guaranteed under the constitution, so all Mattarella can do is install it and hope that the prospect of stability becomes self-reinforcing.

That is the kind of government that former Greek finance minister Yanis Varoufakis would hate, given his fierce resistance to the austerity imposed on Greece by its creditors. And I’m sure it will take about five seconds for me to be labelled a Washington Consensus, IMF-loving neoliberal for suggesting it. It would certainly attract plenty of criticism in Italy, given the strong anti-establishment sentiment that created this crisis in the first place.

But, to use the language of bankruptcy, the bottom line is that Italy is in political and economic Chapter 11. It is broke. It’s not technically insolvent just yet. But it will be, as they say in debt contracts, “but for the passage of time”.

It’s time to bring in the receivers to restructure. There needs to be serious microeconomic and labour-market reform, of the kind Emmanuel Macron is trying to implement in France. There also needs to be some attempt to get the debt under control. Lowering the interest rate through increased confidence would be a good start.

This would also help the rest of Europe. Perhaps there is some hope that German Chancellor Angela Merkel would be grateful, and thus more amenable to assistance measures for Italy. She certainly could not be less well disposed to help out than at present.

Author: Richard Holden, Professor of Economics and PLuS Alliance Fellow, UNSW

At first blush the news at home and abroad appears to be steering us towards our most risky – scenario 4 outcome, where global financial markets are disrupted and home prices fall by 20-40 percent or more as confidence wains.

Some would call this GFC 2.0. So let’s looks at the evidence.

In Australia, as we predicted, a massive class action lawsuit is being planned on behalf of “Australian bank customers that have entered into mortgage finance agreements with banks since 2012”.

Law firm Chamberlains has been appointed to act in the planned class action lawsuit, which has been instructed by Roger Donald Brown of MortgageDeception.com in the action that aims to represent various Australian bank customers that are “incurring financial losses as a result of entering into mortgage loan contracts with banks since 2012”.

As the AFR put it – Lawyers’ representing up to 300,000 litigants are planning an $80 billion action against mortgage lenders, mortgage brokers and financial regulators in a class action that would dwarf previous actions. Roger Brown, a former Lloyds of London insurance broker, said he already has about 200,000 borrowers ready to join the action and has $75 million backing from UK and European investors. There has been a scam, he said about mortgage lending to Australian property buyers. “But the train has hit the buffers and there needs to be recompense.

As we discussed before, if loans made were “unsuitable” as defined by the credit legislation, there is potential recourse. This could be a significant risk to the major players if it gains momentum. And more will likely join up if home prices fall further and mortgage repayments get more difficult. But we think individuals must take some responsibility too!

Next, we now see a number of the major media outlets starting to blame the Royal Commission for the falls in home prices, tighter lending standards and even damage to the broader economy. Talk about shoot the messenger. The fact is we have had years of poor lending practice, and poor regulation. But the industry and regulators kept stumn preferring to enjoy the fruits of over generous lending. The Royal Commission is doing a great job of exposing what has been going on. In fact, the reaction appears to be that what had been hidden is now in the sunshine, and it is true the sunlight is the best disinfectant. Structural malpractice is being exposed, some of which may be illegal, and some of which certainly falls below community expectations. But let’s be clear, it’s the poor behaviour of the banks and the regulators which have placed us in this difficult position. Hoping bad lending remans hidden is a crazy path to resolution. At least if the issues are in the open they stand a chance of being addressed.

But it is also true that just a lax lending allowed households to get bigger mortgages than they should, and bid home prices higher, to be benefit of the banks, and the GDP out-turn, the reverse is also true. Tighter lending will lead to less credit being available, which in turn will translate to lower home prices, and less book growth for the banks. But do not lay this at the door of the Royal Commission. They are actually doing Australia a great service, in a most professional manner.

But that does not stop the rot. UBS came out today with an update saying that the housing market is slowing, with house prices falling and credit conditions tightening. Given the number of headwinds the market is facing; many investors are now questioning whether the housing correction could become disorderly. We expect credit growth to slow sharply and believe the risk of a Credit Crunch is rising.

They walk through the main areas, including tighter lending, interest only loans and foreign buyers. Specifically, they highlight that approved foreign investment in housing is down -65%. The Foreign Investment Review Board just released data for 16/17. The value of approvals to buy residential housing collapsed 65% y/y to $25bn in 16/17, the lowest level since 12/13, and mostly reversing the prior ‘super boom’. The fall was across both new (-66% to $22bn) and established housing (-59% to $3bn) – led by total falls in NSW (-66% to $7bn) and Victoria (-61% to $11bn.

They say that the collapse in 16/17 may be overstated because of the introduction of application fees in Dec-15 – meaning the fall in transactions is less pronounced. But, there is still likely to have been a drop in transactions, reflecting more structural factors including – the lift in taxes on foreigners; domestic lenders tightening standards for foreign buyers (effectively no longer lending against foreign sources of income or collateral); as well as tighter capital controls especially from China.

Their base case is for a small fall in prices ahead, and assumes house prices fall by 5%+ over the coming year and that bad and doubtful debts increase only modestly given the current very benign credit environment. but they also talk about a downside scenario which reflects a more disorderly correction in the housing market (ie a Credit Crunch) and could result in approximately 40% reduction in major bank share prices. This is likely due to credit growth falling more substantially, by ~2-3% compound and credit impairment charges rising significantly as the credit cycle turns. This scenario would put pressure on bank NIMs. Litigation risk from class actions for mortgage misselling is also a tail risk. Dividends would need to be cut in this scenario. Given the leverage in the banking system, accurately predicting the extent of a downturn is very difficult, as was seen in 2008.

And the reason they still hold to their milder view is the expectation that the Government will step in to assist, and slow the implementation of recommendations from the Royal Commission. To quote Scott Morrison on 2GB radio on 23d March.

If banks stop lending, then what do people think that is going to mean for people starting businesses or getting loans or getting jobs or all of this. In the budget papers, the Treasury have actually highlighted this as a bit of a risk with the process we are going through. We have got to be very careful. These stories are heartbreaking, I agree, but we have to be also very cautious about, well, how do we respond to that. What is the right reaction to that? Is it to just throw more regulation there which basically constipates the banking and financial industry which means that people can’t start businesses and people can’t get jobs, people can’t get home loans. Or do we want to move to a smarter way of how this is all done and I think in the era of financial technology in particular there are some real opportunities there. We are going to continue to listen and carefully respect the royal commission, not prejudge the findings, but be very careful about any responses that are made because this can determine how strong an economy we live in over the next ten years and whether people get jobs and start businesses.

But in essence, expect some unnatural acts from the Government to try to keep the bubble going a little longer. All bets are off the other side of the election.

And the third risk, and the one which takes us closest to GFC 2.0 is what is happening in Italy. I am not going to go back over the history, but after months of wrangling, Italy’s political crisis has a hit an impasse, with new elections now increasingly likely. The country faces an institutional crisis without precedent in the history of the Italian republic. Its implications extend well beyond Italy, to the European Union as a whole.

Since an election on March 4, there have been endless vain attempts to form a government – with the likely outcome changing every 24 hours. By mid-May, the Five Star Movement (M5S) and the League, both populist parties, had come together to draft a programme for government featuring tax cuts and spending plans. But it sent shivers down the spines of those contemplating Italy’s public debt – running at over 130% of GDP – and threatened the stability of the eurozone.

The appointment of Carlo Cottarelli, a former official from the International Monetary Fund, as prime minister on May 28 was merely a stop-gap measure until fresh elections in the autumn. His government will almost certainly fail to win the necessary vote of confidence required of all incoming governments upon taking office. This means that it will be unable to undertake any legislative initiatives that go beyond day-to-day administration.

ITALY’S president, Sergio Mattarella had originally planned to put a former IMF economist, Carlo Cottarelli, at the head of a government of technocrats, tasked with steering the country back to the polls after the summer. But Mr Mattarella was reportedly considering changing tack after meeting Mr Cottarelli on May 29th amid growing evidence of support in parliament for an earlier vote. Not a single big party has declared its readiness to back Mr Cottarelli’s proposed administration in a necessary vote of confidence.

So the president is expected to decide on May 30th whether to call a snap election as early as July in an effort to resolve a rapidly deepening political and economic crisis that has sent tremors through global financial markets. There was also concern that the populist parties could win a bigger parliamentary majority in the new election, creating a bigger risk for the future of the eurozone.

In a sign of investors’ concern, the yield gap between Italian and German benchmark government bonds soared from 190 basis points on May 28th to more than 300. The governor of the Bank of Italy, Ignazio Visco, warned his compatriots not to “forget that we are only ever a few steps away from the very serious risk of losing the irreplaceable asset of trust.”

The yield on two-year debt has risen from below zero to close to 2% and Italy’s 10-year bond yields, which is a measure of the country’s sovereign borrowing costs, breached 3 per cent on Tuesday, the highest in four years. At the start of the month they were just 1.8 per cent. Italy’s sovereign debt pile of €2.3 trillion is the largest in the eurozone

The Italian stock market was also down 3 per cent on Tuesday, and has lost around 13 per cent of its value this month.

But these movements need to be put in some context. The Italian stock market is still only back to its levels of last July, after experiencing a strong bull run since later 2016.

In 2011 and 2012 Italian bond breached 7 per cent and threatened a fiscal crisis for the government in Rome. Yields are still some distance from those extreme distress levels.

George Soros was quoted in the FT:

The EU is in an existential crisis. Everything that could go wrong has gone wrong,” he said. To escape the crisis, “it needs to reinvent itself.” Mr Soros said tackling the European migration crisis “may be the best place to start,” but stressed the importance of not forcing European countries to accept set quotas of refugees. He said the Dublin regulation — which decides which nation is responsible for processing a refugee’s asylum status, largely based on which country the individual first enters — had put an “unfair burden” on Italy and other Mediterranean countries, “with disastrous political implications.” While austerity policies appeared initially to have been working, said Mr Soros, the “addiction to austerity” had harmed the euro and was now worsening the European crisis. US president Donald Trump’s exit from the nuclear arms deal with Iran and the uncertainty over tariffs that threaten transatlantic trade will harm European economies, particularly Germany’s, he said, while a strong dollar was prompting “flight” from emerging market economies. “We may be heading for another major financial crisis,” he said. Meanwhile, years of austerity policies had led working people to feel “excluded and ignored,” sentiment that had been exploited by populist and nationalistic politicians, said Mr Soros. He called for greater emphasis on grassroots organisations to meaningfully engage with citizens.

To play devil’s advocate, if Italy were to leave the Eurozone, the Lira would drop, hard. Most probably Italy would default on debt, and this would hit the Eurozone banks hard, especially those in German and French banks will be hit hard and they are saddled with about half the outstanding debt. Just like in the GFC a decade back, global counter-party bank risk will rise, and this time sovereign are involved, so it may go higher. The US Dollar will run hot, and there will be a flight to quality, tightening the capital markets, lifting rates and causing global stocks and commodities to crash, possibly a recession will follow.

In Australia, the dollar would slide significantly, fuelling stock market falls and a further drop in home prices, leading to higher levels of default, and recession, despite the Reserve Bank cutting rates and even trying QE.

Now the financial situation in Italy at the moment, a far cry from the height of the eurozone crisis in 2012, when it really did look possible that weaker member states would be imminently forced to default and the single currency would collapse. Then, that situation was finally defused when the head of the European Central Bank, Mario Draghi, announced he would do “whatever it takes” to stop this break up happening, unveiling an emergency programme of backstop bond buying by the central bank. This reassured private investor that they would, at least, get their money back and bond yields in countries like Italy and Spain fell back to earth, ending the risk of a destructive debt spiral.

But the latest deadlock in Rome is nevertheless the biggest crisis in the eurozone since Greece last threatened to leave in 2015. And Italy is a much larger economy than Greece. If the third largest country in the bloc exited the euro, it is doubtful the single currency would survive.

Falling bank shares dragged down Europe’s main share markets. At the close the UK’s FTSE 100 fell almost 1.3%, while Germany’s Dax was down 1.5% and France’s Cac 1.3% lower. “It’s a market that is totally in panic”, said a fund manager at Anthilia Capital Partners, who noted “a total lack of confidence in the outlook for Italian public finances”. And the chief economic adviser at Allianz in the US said: “If the political situation in Italy worsens, the longer-term spill overs would be felt in the US via a stronger dollar and lower European growth.”

So whether you look locally or globally its risk on at the moment, and we are it seems to me teetering on the edge of our Scenario 4. This will not be pretty and it will not be quick. I see that slow moving train wreck still grinding down the tracks, with no way out.

The European Central Bank sees Italian lender Banca Monte dei Paschi di Siena SpA needing about 8.8 billion euros ($9.2 billion) of capital to bolster its balance sheet, according to Bloomberg.

The calculation is based on the results of a 2016 stress test, the bank said in a statement late Monday, citing two letters from the ECB that it received via Italy’s Finance Ministry. While the ECB saw worsening liquidity at Monte Paschi in December, it still considers the Italian bank to be solvent because it meets Tier 2 capital requirements. Paschi is seeking further information on the central bank’s calculations, according to the statement.

On Friday, the Italian government said it will plow as much as 20 billion euros into Monte Paschi and other banks after the lender failed in its plan to raise about 5 billion euros from private investors. Chief Executive Officer Marco Morelli had crisscrossed the globe looking for investors to back the bank’s reorganization plan, which included a share sale, a debt-for-equity swap and the sale of 28 billion of soured loans.

Il Sole/24 Ore reported Tuesday that the Italian government will invest 6.3 billion euros n the bank, after the newspaper said Monday that the European Central Bank had called for a 4.5 billion-euro contribution from the Italian state and 4.3 billion euros from bondholders.

Italy has agreed a £17bn bailout for world’s oldest bank Monte dei Paschi di Siena, which was recently judged the weakest of the European Union’s major banks.

According to The Independent, the world’s oldest bank, Monte dei Paschi di Siena, has been granted a multi-billion euro state bailout after it admitted a private rescue plan was unlikely to succeed.

Paolo Gentiloni, the new Italian Prime Minister, said his Government had approved a new €20 billion (£16.8 billion) fund after Cabinet met to discuss the matter into the small hours of Friday.

The Italian parliament had already authorised the Government to step in and save Monte dei Paschi di Siena, recently judged the weakest of the European Union’s major banks.

Italy’s third largest lender had hoped to raise €5bn from investors through the sale of shares in order to avoid being nationalised.

However, the bank admitted on Wednesday night that Qatar’s sovereign wealth fund had not been persuaded to become the “anchor investor” to underpin its recapitalisation plan.

Without private sector capital, Monte dei Paschi was set to miss an end-of-year deadline imposed by the European Central Bank to raise fresh funds.

Shares in Monte dei Paschi were briefly suspended on Thursday after plunging by nearly 7 per cent in early trade as the embattled Italian lender’s bailout crisis continued.

The bank has already lost more than 80 per cent of its value since the start of the year.

Parliamentary approval for the €20bn rescue package was needed to allow the state to take on new debt. Italy’s debt burden, at about 133 per cent of annual output, is already the second highest in the eurozone after Greece.

However, state intervention could also spur further anti-euro feeling among Italian voters at an uncertain time in Italian politics.

The misfortunes of Italy’s banking sector have already spilled over into the political sphere, contributing to the government’s defeat in this month’s constitutional referendum.

The failure of Monte dei Paschi would threaten the savings of thousands of Italians and could undermine confidence in the country’s wider banking sector, saddled with a third of the eurozone’s total bad loans.

In the wake of the Italian constitutional referendum, the country’s banking crisis is going from bad to worse. The European Central Bank (ECB)‘s decision to refuse an extension to Banca Monte dei Paschi di Siena to raise €5 billion (£4.2 billion) has left the country’s third-largest bank facing a government bailout that looks likely to inflict severe pain on many ordinary Italian savers.

As if that were not enough, Italy’s biggest bank, UniCredit, announced a restructuring plan that requires a capital raising of €13 billion in the first three months of next year. Given the torrid time Monte dei Paschi has had trying to find sufficient private backing, will UniCredit need help from the Italian taxpayer, too?

The problems at Monte dei Pashci and UniCredit reflect the parlous state of the country’s banking system. The economy has been struggling for a number of years and borrowers have been defaulting, creating a mountain of bad loans. Around 20% of bank loans are bad, amounting to a staggering €360 billion (about one-third of all bad loans in the eurozone).

More than 70% of these loans are to small and medium-sized businesses. Small firms in Italy tend to have numerous bank relationships, commonly with accounts at four or five banks. Hence their defaults have polluted bank balance sheets across the sector.

I hear critics saying the Bank of Italy, the regulator, was slow to deal with the problem, only intervening within the past 18 months. Individual banks also stand accused of being complicit in rolling over non-performing loans – disguising the true picture. The situation is worse for banks in the south, where economies have been faring even worse. And Matteo Renzi’s defeat in the referendum exacerbates the whole problem by denying the sector reforms to help banks recover bad loans by speeding up insolvency processes, among other things.

The Bank of Italy restructured four small banks last year, but its ability to rapidly resolve problems at bigger banks is hindered by EU bank bailout and state aid rules. These say direct state aid cannot be provided until a bank has looked for private injections of capital, including making investors in a class of bank debts known as bail-in bonds take some pain by converting their bonds into shares.

The logic is that these unsecured bondholders should bear the same risks as shareholders, thus reducing the burden on the taxpayer in the event of a rescue. Investors have nonetheless been lured into these bail-in bonds, including those of Monte dei Paschi and UniCredit, by higher returns than other bank bonds, betting they would not end up being converted.

In most countries institutional investors including pension funds and insurance companies are the main investors in unsecured bank bonds. But in Italy there’s an additional problem: households own about a third of the total – 40,000 retail investors own Monte dei Paschi bonds, for instance.

When the four small Italian banks were restructured, the value of their bonds was wiped out. In addition to political condemnation, there were widespread protests and at least one suicide. Particularly when the country is going through such a politically volatile period, the government will be very wary of another bail-in as part of any Monte dei Paschi rescue. Depositors above around €90,000 are also supposed to lose out, though it is hard to see this being politically possible regardless of the rules.

What comes next

The ECB decided the request from Monte dei Paschi for a deadline extension for its recapitalisation from year-end to January 20 was a delaying tactic. It said the bank had to sort things out faster – together with the new Italian government, headed by Renzi loyalist Paolo Gentiloni. This means the world’s oldest bank, established in 1472, now has barely two weeks to find a private solution and avoid inflicting a bail-in on the country.

The recapitalisation plan has three components. The first is a voluntary bond swap – similar to bail-in bonds, except bondholders choose whether to convert their bonds to shares or not. This has raised around €1 billion from institutional investors, but there has been no take-up from retail investors. They have viewed the exchange as too risky and have been concerned about whether the regulator has fully approved the retail swap transactions.

Second, Monte dei Paschi hopes to get €1 billion from Qatar’s sovereign wealth fund. Finally, a consortium of banks has said it will try to sell the bank’s shares in the open market. They will not be underwritten, however, so there is no guarantee of raising significant funds.

So even if the capital-raising is successful there is likely to be a shortfall of several billion euros. The question then is what happens next. The government will certainly not let this historic institution fail, despite a national debt in excess of 130% of GDP – among the highest in the world.

Failure to resolve the problems would compound financial market jitters surrounding Italian banks. That could lead to widespread failure and the export of similar problems, due to a collapse of confidence, to other fragile eurozone countries.

To unlock an injection of state funds the Bank of Italy would therefore need to decide whether to follow the EU rules and risk the wrath of the retail bondholders with a bail-in – and/or provide guarantees to cover their losses. Ironically, the ECB would then potentially have to provide guarantees, liquidity injections and capital support to maintain confidence in the Italian system.

Meanwhile, all eyes will be on the UniCredit capital-raising to see if it fares any better. It should do: UniCredit’s proposed rights issue requires market credibility that Monte dei Paschi does not have at present. Were it to hit difficulties, however, this crisis will move from major to monumental. Either way, it looks likely to be some time before the problems in Italian banking even begin to look like being resolved.

Author: Philip Molyneux, Professor of Banking and Finance, Bangor University