Moody’s says today’s still underperforming US economy leaves plenty of room for significant improvement in 2017 without the unwanted side effect of significantly faster price inflation. The US economy may be far from realizing its full potential.

January 2017 marks the 91st month of the current economic recovery and yet the US economy’s rates of resource utilization leave considerable room for additional production. In terms of the latest three-month averages, only 75.2% of industrial capacity was in use, while payrolls approximated a relatively low 57.0% of the working-age population. When previous upturns were of similar vintage in October 1998 and June 1990, the industrial capacity utilization rate averaged 82.7% and payrolls averaged 59.9% of the working age population.

Will this be the first economic recovery since the 1930s where the capacity utilization rate’s moving three month average fails to reach the 80% mark, where the latter is typically associated with the sufficient utilization of potential industrial output? Thus far in the current upturn, this version of capacity utilization has risen no higher than the 78.6% of Q4-2014. Figure 1 indicates a good deal of room to grow for industrial capacity utilization and, thus, lends support to the possibility of faster than 3% real GDP growth. By comparison, real GDP has risen by only 1.8% annualized, on average, for the current recovery to date and not since 2005’s 3.3% has growth managed to reach 3% for an entire calendar year. (Figure 1.)

In a similar vein, late 2016’s relatively low ratio of jobs to the working-age population preserves the possibility of a fuller utilization of US labor resources that could supply a noticeably faster rate of economic growth. However, the recent absence of labor productivity growth limits the extent to which faster jobs growth can quicken economic growth. (Figure 2.)

Yes, late 2016’s comparatively low rates of resource utilization hint of considerable upside potential for US business activity. Nevertheless, whether such potential is realized depends on a far from assured quickening of expenditures. For one thing, the recent strengthening of the dollar exchange rate heightens the importance of an acceleration by US household spending, which requires improved prospects for employment income.

The critical role of household expenditures cannot be overemphasized. Regardless of the more favorable tax treatment of capital outlays, businesses are only likely to significantly increase their production capabilities if they are convinced of sufficiently profitable markets for new and existing products.

Thus, businesses are likely to heed the warning of slower household spending growth implicit in the dip by payrolls’ annual increase from Q1-2015’s cycle high of 2.2% to Q4-2016’s 1.6%. The last two times payrolls decelerated in a similar manner, recessions arrived within 18 months.

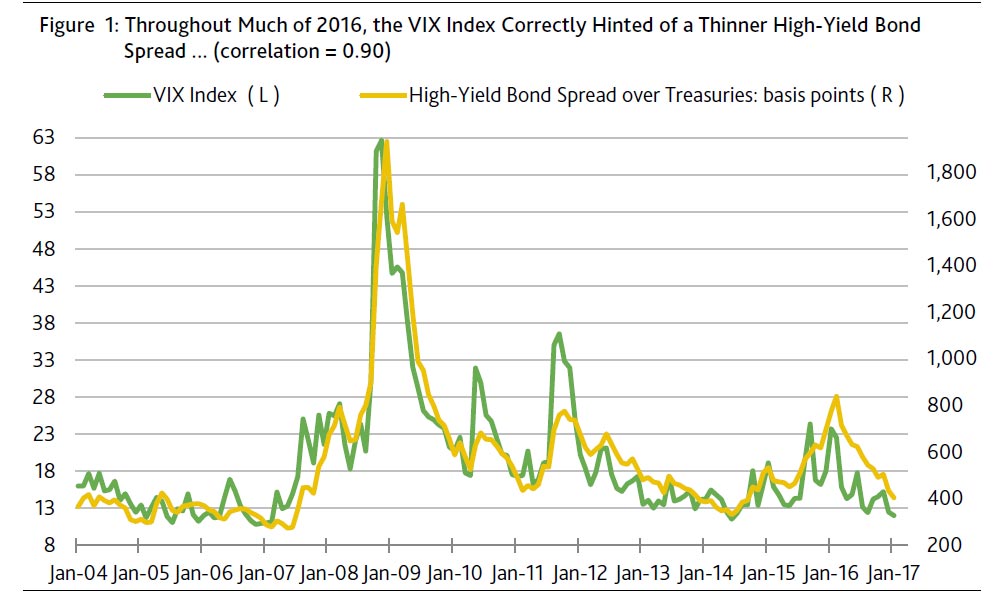

Jobs outlook suggests spreads are too thin

Corporate credit is now very much priced for faster economic growth that will require the fuller utilization of US productive resources. The correlation between the high-yield bond spread and the moving three-month average of payrolls’ monthly percent change is a strong 0.78. Fourth-quarter 2016’s average monthly increase by payrolls of 0.11% predicts a 531 bp midpoint for the high-yield bond spread.

Accordingly, January 11’s far thinner high-yield bond spread of 405 bp implicitly expects faster jobs growth. However, as inferred from the Blue Chip consensus expectation of a drop by payrolls’ average monthly increase from 2016’s 180,000 jobs to 2017’s 161,000 jobs, the high-yield spread may soon be closer to 500 bp than to 400 bp.

Unemployment rate overstates labor market tightness

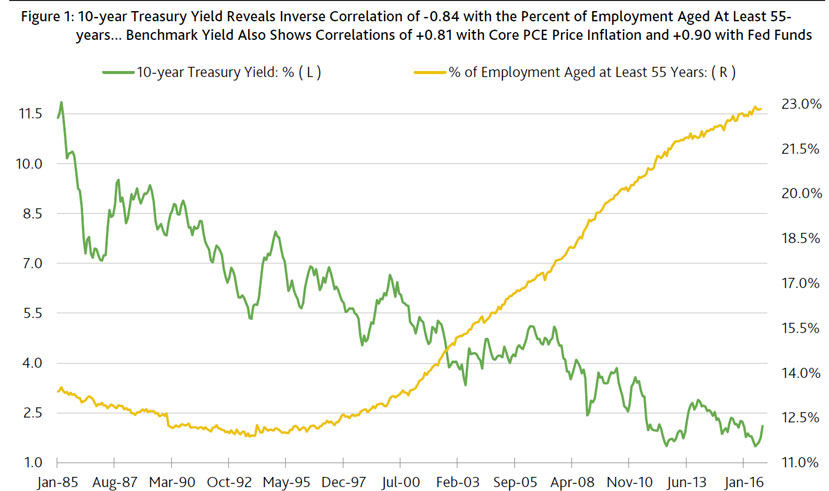

As opposed to the unemployment rate, the ratio of payrolls to the working-age population may now be the better estimate of labor market utilization, owing to the current recovery’s large number of labor force dropouts. For example, when the unemployment rate previously first fell to Q4-2106’s 4.7% in March 2006 and November 1997, payrolls averaged 60.2% of the working age population, which was well above Q4-2016’s 57.0%.

As inferred from the unemployment rate’s statistical relationship with the ratio of payrolls to the working-age population since 1988, Q4-2016’s ratio of 57.0% is ordinarily accompanied by a jobless rate of 6.8%. Even after allowing for how an aging workforce exerts a downward bias to the ratio of payrolls to the working-age population, the 4.7% unemployment rate still probably overstates the degree of labor market tightening. (Figure 3.)

In addition to an atypically low labor force participation rate, the 4.7% unemployment rate overstates labor-market tightness because of a relatively high U6 unemployment, or under-employment, rate. When the jobless rate’s moving three-month average previously first fell to 4.7% in March 2006 and November 1997, the U6 under-employment rate averaged 8.4%, considerably lower than Q4-2016’s 9.3%.

Nevertheless, the US labor market is firming up, as seen in the yearly increase of the average hourly wage from the 2.5% of Q4-2015 to Q4-2016’s 2.7%. However, when the unemployment rate’s three-month average last fell to 4.7% in Q1-2006, average hourly earnings posted a comparable increase of 3.4%. During the previous cycle, the yearly increase of the average wage’s moving three-month average peaked at the 3.8% of Q3-2006. By the time the moving three-month averages of the jobless rate and the U6 under-employment rate bottomed simultaneously in May 2007 (at 4.4% and 8.1%, respectively), the average hourly wage’s annual increase had slowed to 3.4%.

Despite an earlier acceleration by the hourly wage’s moving yearlong average from the 2.0% of the span-ended September 2004 to the 3.7% of the span-ended March 2007, the annual rate of growth for the core PCE price index peaked at a relatively modest 2.4%. By comparison, the core PCE price index rose by 1.7% annually during the three-months-ended November 2016. The possibly unfinished strengthening of the dollar exchange rate will limit the upside for US price inflation and just might intensify the price deflation still afflicting a number of internationally traded goods.

Ratio of jobs to the working-age population outshines other possible inflation indicators

The market’s recent obsession with December’s 2.9% yearly jump by average hourly earnings may have been unwarranted. After all, the annual rate of core PCE price index inflation generated a meaningless correlation of 0.04 with the yearly percent change of the average hourly wage.

By contrast, the ratio of payrolls to the working-age population again offers useful insight regarding labor market tightness and inflation risk. Since 1992, the year-to-year percentage point change for the ratio of payrolls to the working-age population shows a correlation of 0.31 with the annual rate of core PCE price index inflation, where this and forthcoming comparisons employ moving three-month averages.

As far as predicting core PCE price index inflation, the ratio of jobs to the working-age population also outperforms both the unemployment and U6 under-employment rates. For example, the jobless rate and its year-to-year percentage point change showed weaker correlations of -0.22 and -0.24 with the annual rate of core PCE price index inflation, while the U6 under-employment rate posted comparably measured correlations of -0.23 and -0.22, respectively. Thus, expectations of a continued mild rise by the ratio of payrolls to the working-age population suggest only a limited upside for core PCE price index inflation.

Consensus views on employment and industrial production favor a continuation of the Great Underutilization. Unless payrolls zoom ahead of recent forecasts, the midpoint for fed funds may finish 2017 no higher than 1.125%, while the 10-year Treasury yield spends most of the year under 2.5%. Only if the demand for US output delivers a big enough upside surprise might a substantially fuller utilization of resources help make America great again.