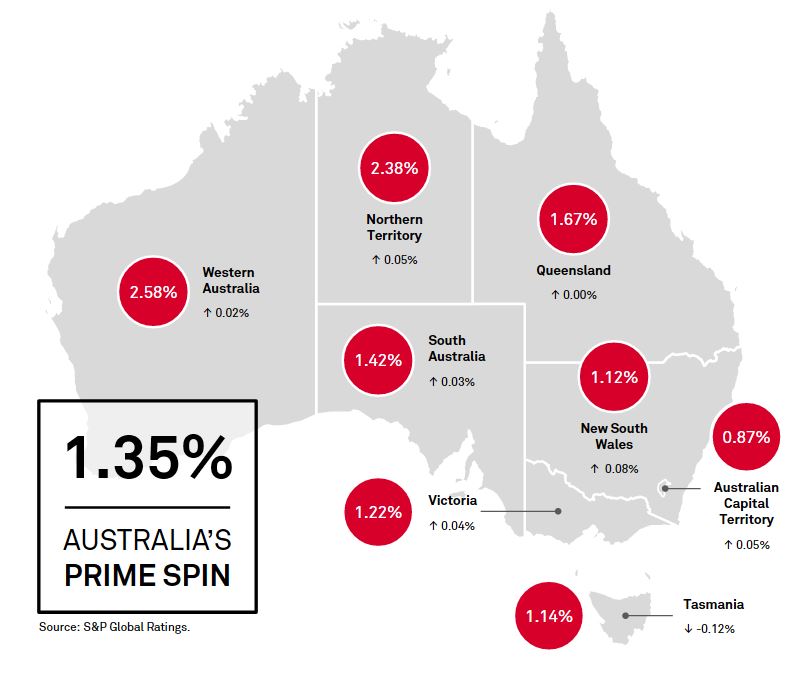

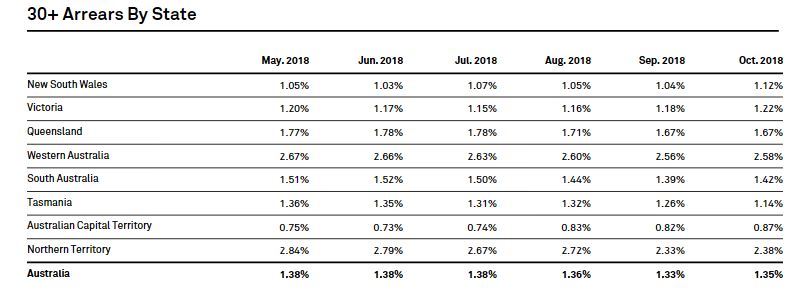

According to data from S&P Global Ratings relating to mortgage backed securities, the arrears rate rose in October 2018 (which is against normal trend).

Total SPIN index rose to 1.35%. The trend was consistent in all states and territories except Tasmania, where arrears fell to 1.14% in October from 1.26% the previous month. New South Wales recorded the largest increase in arrears in October, rising to 1.12% from 1.04% a month earlier. Arrears in New South Wales have been gradually rising throughout 2018, but remain the second lowest in the country, behind Australian Capital Territory.

WA stands out as the highest risk state, no surprise given the flat economy and many years of sliding home prices.

Investor and owner-occupier arrears increased in October. Investor

arrears increased to 1.25% in October from 1.19% in September and

owner-occupier arrears rose to 1.54% from 1.52% a month earlier. In our

opinion, the larger increase in investor arrears during the month partly

reflects the repricing of investor loans and interest-only loans, which

are more common among investors. This is also reflected in the

narrowing of the differential between investor and owner-occupier

arrears, which peaked at 0.61% in January 2017. The differential had

decreased to around 0.30% by October 2018, thanks to the ongoing

repricing of investor loans.

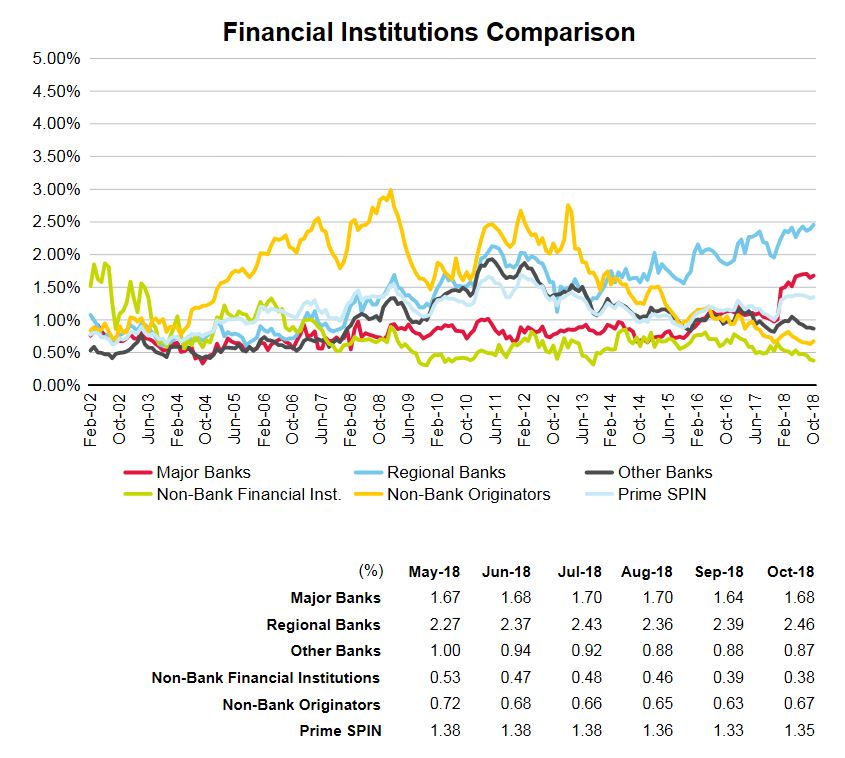

Arrears rose at the major and regional banks, offset by a small fall in the non-bank financial institutions. Defaults with non-bank originators rose.

“Reserve Bank governor Philip Lowe is understood to have met with the big bank chiefs in recent weeks to caution them against an overzealous tightening of credit supply in response to lending rules and the Hayne royal commission”.

The RBA is of the view that lenders are turning good business away, and need to take risk on.

Some SME’s are getting caught in the cross fire, and its clear that business is finding it harder to get funding. This was covered in the RBA’s minutes, released yesterday.

Of course the responsible lending obligations have not changed, but now the meaning and obligations are front of mind. Thus banks need to examine income and expenses etc and cannot necessarily rely on HEM or mortgage brokers. So all this is in direct opposition to the RBA’s wishes, and we suspect the risk of legal action, or worse will continue to limit bank lending.

The ASIC Westpac case will be back before the courts in the new year, though as yet is not clear whether HEM will be tested in court, or whether its more about reaching a settlement. And the royal commission recommendations will be out in February

Is the RBA really condoning the bad behaviour and law breaking exposed in the past year?

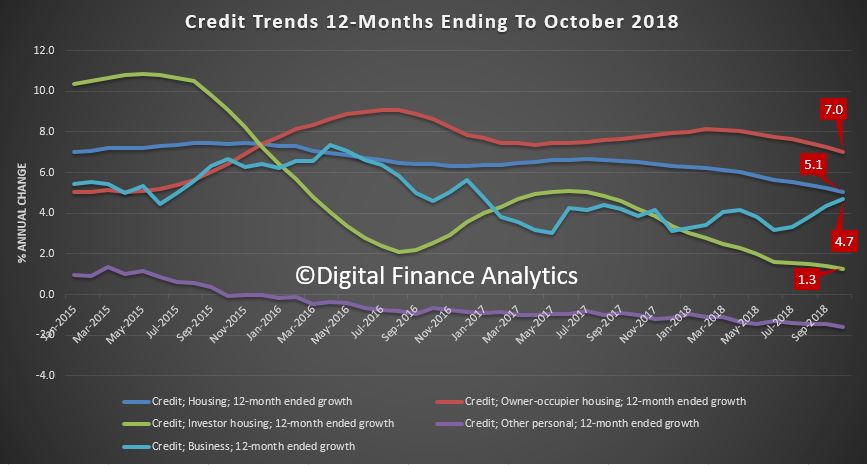

And remember that currently mortgage lending is still running at more than 5% on an annualised basis, according to RBA data.

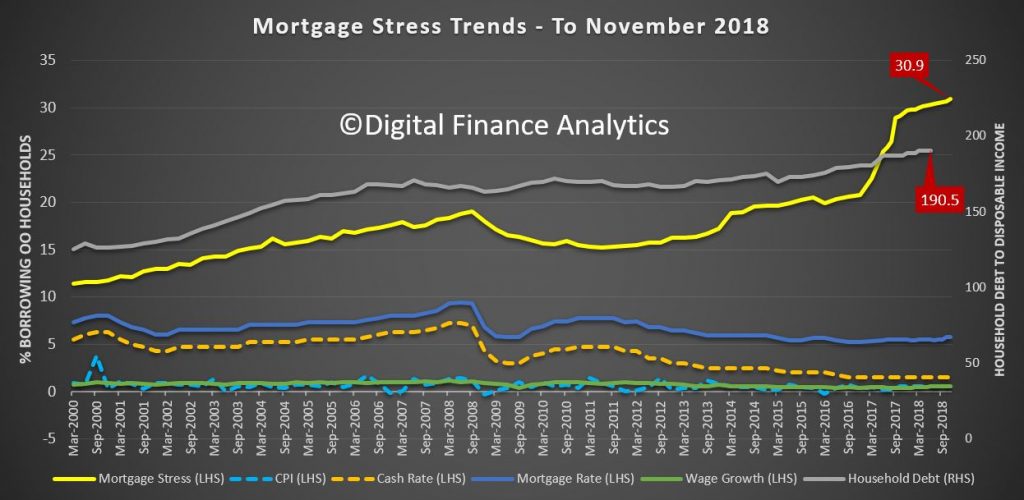

The fundamental problem is the RBA has been responsible for the growth of credit to the point where households in Australia are some of the most leveraged in the world, home prices have exploded and bank balance sheets have inflated. But all this “growth” is illusory. Mortgage stress continues to build and the wealth effect is reversing as home prices slide.

Thus, as we anticipated, we will see a number of “unnatural acts” by the RBA and the Government to try and stop the debt bomb from exploding, by trying to get credit to expand. But this is irresponsible behaviour, in the light of rising global interest rates, high market volatility and building systemic risks.

A class action lawsuit that was being planned on behalf of “Australian bank customers that have entered into mortgage finance agreements with banks since 2012” has been dropped due to a lack of a “clear cause of action”; via The Adviser.

Law

firm Chamberlains has announced that its major class action against

various Australian banks will no longer proceed despite interest in the

matter.

In May of this year, it was announced that law firm

Chamberlains had been appointed to act in the planned class action

lawsuit, which was instructed by Roger Donald Brown of

MortgageDeception.com to represent various Australian bank customers

that had been “incurring financial losses as a result of entering into

mortgage loan contracts with banks since 2012”.

The law firm had

been calling on bank customers to join the class action, led by Stipe

Vuleta, if they had “incurred financial losses due to irresponsible

lending practices”.

In an update to interested parties, seen by

The Adviser, Chamberlains commented: “Over the last few months, we have

been busy investigating the scope of a potential legal claim, which

could be commenced as a class action against various Australian banks.

“During

this process, we have engaged with senior and junior counsel to assist

with the questions of law to be raised if an action were to be commenced

in the Federal Court of Australia.

“Despite

our efforts, we have been unable to identify a clear class of claimants

who have a clear cause of action against a particular Australian bank.”

It continued: “As a result, we are unable to take this process further.”

While

the law firm has said that some may still have “an individual case

arising from [their] dealings with the banks, which may have merit

outside of the framework of a class action”, it would encourage those

people to “seek independent legal advice about [their] claim”.

Class actions in focus

Several

class actions against major lenders have already been initiated

following some of the revelations from the royal commission, including four separate class actions against AMP on

the grounds that the company breached its obligations to customers and

engaged in “misleading and deceptive representations to the market”.

The legal action was announced after senior AMP executives appeared before the royal commission as

witnesses. Some of the executives admitted to a number of potential

crimes and suggested that these were repeatedly mischaracterised to the

Australian Securities and Investments Commission (ASIC) and to its

customers as being “administrative errors”.

These included

providing false and misleading statements to the regulator and charging

customers for services that were not provided.

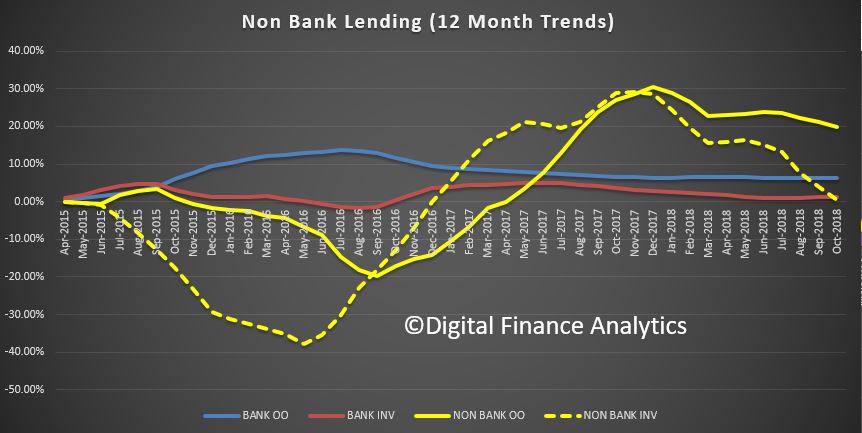

The analysis of the monthly banking stats out last week gives us the opportunity to look across the non-bank sector, relative to the banking sector by comparing the APRA data with the Reserve Bank data series.

We have plotting the rolling 12 month trends, and this chart shows the results.

The striking observation is the relatively stronger growth rate relative to the banks supervised more directly by APRA. Granted APRA does have some responsibilities for the non-bank sector, but appear not to be their main focus.

All lenders have the same obligation with regards to responsible lending, but non-banks are generally more flush with cash, and less constrained by the capital requirements which crimp ADI’s.

Thus we can expect the growth on non-ADI mortgage lending to continue at a faster pace than the bank sector. As a result, we think more risks are building in the financial system.

The use of the Household Expenditure Measure to assess serviceability was initially less common for broker-originated loans, but such is no longer the case, ANZ chief Shayne Elliott has revealed, via The Adviser.

Appearing before the financial services royal commission in its seventh and final round of hearings, ANZ CEO Shayne Elliott was questioned over the bank’s use of the Household Expenditure Measure (HEM) to assess home loan applications.

In round one of the commission’s hearings, ANZ general manager of home loans and retail lending practices William Ranken admitted that the bank did not further investigate a borrower’s capacity to service a broker-originated mortgage.

In his interim report, Commissioner Kenneth Hayne alleged that using HEM as the default measure of household expenditure “does not constitute any verification of a borrower’s expenditure”, adding that “much more often than not, it will mask the fact that no sufficient inquiry has been made about the borrower’s financial position”.

Counsel assisting the commission Rowena Orr QC pointed to a review of ANZ’s HEM use by consultancy firm KPMG upon the Australian Prudential Regulation Authority’s (APRA) request.

The KPMG review found that 73 per cent of ANZ’s loan assessments defaulted to the HEM benchmark.

Mr Elliott noted that since the review, ANZ has taken steps to reduce its reliance on HEM, with the CEO stating that the bank plans to reduce the use of HEM for loan assessments to a third of its overall applications.

When asked if there was a disparity between the use of HEM through the broker channel and branch network, Mr Elliott revealed that prior to the bank’s move to reduce its reliance on the benchmark, the use of HEM was less prevalent for broker-originated loans.

“Perhaps surprisingly, when we did the review, when we were talking about the mid-70s [percentage], the branch channel actually had slightly higher usage or dependency on HEM as opposed to the broker [channel].

“[That] actually is counterintuitive,” he added. “I think it would be reasonable to expect that if [ANZ] knows these customers, one might expect to use HEM less.”

Mr Elliott attributed the disparity to the higher proportion of “top-ups” for existing loans through the branch network, noting that ANZ’s home loan managers would be more likely to “shortcut the process” through the use of the HEM benchmark.

However, the CEO said that according to the latest data that he’s reviewed, the branch network’s reliance on HEM is lower than in the broker channel.

“[It’s] changing as we speak,” he said.

“As in the latest data I saw, the branch network is now lower in terms of its usage or reliance on HEM versus the broker channel. And that’s because we are in, if you will, greater control of that process in terms of our ability to coach and send signals to our branch network.”

However, he added that the use of the benchmark for broker-originated loans is “coming down rapidly” in line with the bank’s overall commitment to reduce its reliance on HEM.

Flat-fee ‘credible alternative’ to commission-based model

Further, as reported on The Adviser’s sister publication, Mortgage Business, Mr Elliott told the commission that a flat fee paid by lenders to brokers is a “credible alternative” to the existing commission-based remuneration model.

When asked by Ms Orr about his view on broker remuneration, Mr Elliott said that a flat fee paid by lenders is a “credible alternative” to the current commission-based model.

In a witness statement provided to the commission, Mr Elliott said that there’s “merit in considering alternative models for broker remuneration to ensure that the current model remains appropriate and better than any alternative”.

Reflecting on his witness statement, Ms Orr asked: “Is that because you accept that there’s an inherent risk that incentives might cause brokers to behave in ways that lead to poor customer outcomes?”

The ANZ CEO replied: “There is always that risk. [The] term incentive is to incent behaviour. Therefore, it can be misused or it can cause unintended outcomes if the broker is apt to be led by their own financial reward.”

Mr Elliott acknowledged that “no system’s perfect” and that a “fixed fee is also capable of being misused and leading to unintended outcomes”.

However, he added: “It is just my observation that there is at least some data on this from other markets, most notably in northern Europe. It seems a model that’s worth looking at.”

Mr Elliott continued: “I’m not suggesting it’s necessarily an improvement. It just feels like a credible alternative.”

The ANZ CEO compared a flat-fee model in the broking industry to the financial planning industry.

“The service is the work you are paying for, and perhaps the fee should not necessarily be tied to the outcome.

“I think that’s not an unreasonable proposition.”

However, the ANZ chief noted the negative implications of a flat-fee model, stating that with lenders ultimately passing on costs to consumers, the model would be a “major advantage” to higher income borrowers.

“The difficulty with the fixed fee, if I may, is it essentially is of major advantage to people who can afford and have the financial position to undertake large mortgages,” he said.

“[A] subsidy would be paid by those least able to afford it, and it runs the risk of making broking a privilege for the wealthy.”

There’s ‘merit’ in a fees-for-service model

Ms Orr also asked Mr Elliott for his view regarding a consumer-pays or “fees-for-service” model.

The QC asked whether such a model would address some of the concerns expressed by Mr Elliott about a flat-fee model.

Mr Elliott said that if a fee is paid by borrowers, it would be “uneconomic” for people seeking a loan to visit a broker, repeating that using a broker would become a “service for the wealthy”.

Ms Orr then asked the CEO for his thoughts on a Netherlands-style fees-for-service model, supported by Commonwealth Bank CEO Matt Comyn, in which both branches and brokers would charge a fee for loan origination.

Mr Elliott replied: “There’s merit in looking at that, [but] it still is an imposition of cost that would otherwise not have been there.”

Mr Elliott added that there would be “new costs” associated with a Netherlands-style model, noting that borrowers seeking a “top-up” for an existing loan would need to pay an additional fee.

In response, Ms Orr alleged that under the current commission-based model, costs are also “filtered back down” to consumers.

To which Mr Elliott replied: “In general terms, yes. Not necessarily in direct terms like that fee I charge you as a borrower, [and] at ANZ, we have, for some time, disclosed [commissions]. So, when you do get a mortgage through a broker, we do advise the customer what we have paid that broker. So, it is disclosed to them.”

The ANZ CEO also said that under a fees-for-service model, consumers could be incentivised to take out larger loans to avoid paying a fee if they wish to top up their loan.

Conversely, Mr Elliott added that if a flat fee is paid by lenders, some brokers may be incentivised to encourage clients to borrow less and “come back for more top-ups so that they get more fees”.

Mr Elliott reported that top-ups on existing loans make up 30 per cent ($17 billion) of total volume settled by ANZ.

The ANZ chief also told Ms Orr that he doesn’t believe a move to introduce an alternative remuneration model would be “hugely successful” without regulatory intervention.

She updated their views on responsible lending, and their new approach to getting better data on the sector. They also to publish a consultation paper on RG 209 revisions and enhancements.

Responsible lending

The National Consumer Credit Protection Act includes an array of obligations designed to protect consumers. Chief among them are the responsible lending provisions – a set of obligations that require lenders and mortgage brokers to do three things before offering a loan to a consumer:

One – the lender or broker must make reasonable inquiries into the requirements, objectives and financial situation of the consumer.

Two – they then need to verify the financial situation of the consumer.

Three – the lender or broker must then make an assessment or preliminary assessment (respectively) of whether the proposed loan is unsuitable for the consumer.

Lenders also have an obligation not to enter into an unsuitable loan contract with the consumer.

The responsible lending provisions are not designed to protect those who invest in residential mortgage-backed securities or other consumer debt securities. However, by protecting consumers in the manner I’ve just described, the provisions necessarily afford investors some secondary protection.

This also means that a failure by a bank that either issues, or sells loans to issuers of, residential mortgage-backed securities to lend responsibly harms both borrowers and investors. As ASIC goes about its responsible lending work, we are cognisant of this fact.

That said, as we all appreciate, compliance with the responsible lending provisions by securitisers alone does not automatically mean a AAA grade rating for a tranche of securities. The provisions set the minimum standard.

ASIC expects and encourages lenders to think about how they can ensure loans provided to consumers are not only ‘not unsuitable’ in accordance with the language of the National Credit Act, but also ‘suitable’ – properly designed and priced to meet the needs of the consumer.

Responsible lending should not be a static, mechanical process devoid of common sense, nor a checkbox exercise. It should be a dynamic, evolving process that looks to continually improve credit quality through the adoption of new practices and new technology, underpinned by basic common sense.

Investors in residential mortgage-backed securities should be looking to those lenders that make this commitment to ongoing improvement.

I should also say something about low-doc loans at this point. As you’ll be aware, many mortgage pools will include some portion of low-doc loans. The definition of a low-doc loan can vary. Nevertheless, it must be said that the idea of a loan provided to a consumer after taking less than reasonable steps to verify the consumer’s financial situation (by obtaining and reviewing reliable documentation) is fundamentallyincompatible with responsible lending.

Investors should be wary of the additional credit and regulatory risks that low-doc loans involve.

There is also a move away from what’s termed ‘low-doc loans’ to the more popular ‘non-confirming loans’. It is fair that all consumers capable of repaying a loan have the opportunity to apply for one, even where the consumer’s circumstances are unusual. But insofar as the phrase ‘non-conforming loans’ could be used as a euphemism for a low-doc or risky consumer loan, our warning remains: lenders and investors face not only higher credit risks, but also the risk of a regulatory response in these situations.

As we begin to see some examples of mortgage stress, particularly as interest rates rise, it becomes more important for investors to be discerning about the securities they invest in. Investors must consider how the mortgage lender goes about lending responsibly.

ASIC’s recent responsible lending initiatives

ASIC’s recent responsible lending initiatives have been informed by three priorities:

Promote responsible lending and appropriate responses to financial difficult

Address the mis-selling of products and promote good consumer outcomes, and

Respond to innovation in financial services and consumer credit and facilitate appropriate reform.

Let me update you on some our initiatives now.

Loan application fraud

ASIC has focused on loan application fraud for some time.

The falsification of loan documents by brokers and lender employees can undermine the integrity of the responsible lending provisions and lead to consumer harm where borrowers obtain loans they can’t afford. It can also harm investors if the loan is securitised.

Insufficient controls to address the risk of loan application fraud and incentive structures that reward poor behaviour jeopardise trust and confidence in the financial sector.

We recognise that lenders have a significant interest (both financial and regulatory) in detecting and responding to loan fraud and ensuring consumers can repay the loans offered to them.

In many cases where we are alerted to alleged loan fraud involving brokers or lender employees, the matters have been brought to our attention by industry, or an industry association, which has already suspended or terminated the individual’s employment, accreditation or aggregator agreement.

We have taken a strategic approach, including civil penalty proceedings against ANZ (Esanda) for breaches of the responsible lending provisions, as they relied on information in falsified payslips submitted by brokers where it had reason to doubt the reliability of that information.

In its judgment, the Court made clear that where unlicensed brokers submit loan applications in reliance on the ‘point of sale’ exemption in regulation 23 of the National Credit Consumer Protection Regulations, lenders have a greater obligation to exercise care. This was the basis for the higher penalties imposed on ANZ relating to the loans submitted by one of the brokers under the point of sale exemption.

In line with our strategic approach, we are undertaking an industry review to better understand the type and level of fraud faced by industry, and how industry goes about preventing, detecting and responding to it.

We are collecting information on industry controls and processes, with a view to promoting best practice. This will help us to improve public confidence in controls for preventing, detecting and responding to loan fraud.

We have met with all of the review participants and have commenced a data collection phase involving selected lenders and aggregators. We expect to release a report next year.

Motor vehicle finance

We are undertaking a review of the car finance industry’s compliance with regulatory obligations relating to responsible lending, collections and hardship.

Our recent work in the car finance industry has identified poor practices such as:

lenders offering loans to consumers that they cannot afford

lenders failing to make reasonable inquiries into, and to verify information about, the consumer’s financial situation, and

consumers being denied important protections under the National Credit Act because of car dealers misrepresenting the loan as a business loan.

We are collecting information from several car financiers to:

understand current trends and practices in the car finance industry

assess the adequacy of their responsible lending, hardship and debt collection processes, and

identify areas of concern or risks that might affect consumers.

We plan to use the findings from the review to drive improved standards of conduct and compliance with regulatory obligations across the industry, including financiers who regularly issue consumer debt securities.

We expect all participants will improve their practices and develop remediation programmes to respond to past instances of poor conduct.

Where we identify concerns, we will be commencing investigations with a view to enforcement action. We have already seen BMW Finance pay $77 million in Australia’s largest consumer credit remediation program. Other financiers engaging in similar conduct can expect a strong response.

We recently issued pilot surveys to participants to obtain feedback on the availability of the data required for the review, with the aim of understanding the systems and methods of data collection and storage. We will use the information provided to further refine our future data requests.

Recurrent data requests

We have also commenced a pilot to obtain home loan data on a recurrent basis.

We will review the results of the pilot in 2019 to assess how to roll out recurrent data requests more broadly.

We will be able to use this data in a number of ways, including to identify potential trends and issues that can help us prioritise regulatory actions and provide feedback to industry. We also envisage releasing the aggregated data to inform consumers and investors more broadly.

We acknowledge that recurrent data collection will have a cost impact on industry, which is why conducting the pilot is so important. We are working with industry and other parts of the government to do this in the most efficient way possible.

By obtaining recurrent granular data, our vision is to reduce the need for ad-hoc and bespoke data collection exercises. This may reduce some costs for the industry in the long run.

Review of Regulatory Guide 209

We are planning to consult on our responsible lending guidance in Regulatory Guide 209 (RG 209).

ASIC first published RG 209 in February 2010 to provide guidance on the processes that we expect licensees to have in place to ensure that consumers are not provided with unsuitable loans.

The Regulatory Guide was last updated in November 2014 following the Cash Store decision.

We believe it’s timely to review the guide, so we can ensure our guidance remains current, addresses emerging issues, and provides a clear indication of what our expectations are.

Since the last revision, there have been a range of developments, including:

thematic ASIC reviews, including ASIC Report 445 and Report 493, which looked at interest-only lending and the conduct of lenders and brokers respectively

law reform in relation to credit cards, with the potential for small amount credit contract and consumer lease reforms

judicial commentary and enforcement outcomes, such as in the Channic, Esanda and Thorn matters, and

commentary from the Royal Commission.

We are still at a reasonably early stage in scoping the kinds of changes or additions that we think would be useful to update.

We intend to engage quite actively about the range of issues that should be addressed, and the approach that we propose to take.

We hope to publish a consultation paper on RG 209 later this year or early next year and will give stakeholders such as the Australian Securitisation Forum the opportunity to make submissions.

Product intervention powers

Treasury recently released draft legislation to introduce design and distribution obligations for persons providing financial services, and a product intervention power for ASIC.

The design and distribution obligations will apply to issuers or distributors of financial products. It is not proposed that these obligations will apply to credit licensees.

However, to complement these obligations, the Government is also introducing a product intervention power for ASIC. This power would enable us to make orders for up to 18 months prohibiting specified conduct in relation to a product, or even ban a product, where we identify a risk of significant consumer detriment. This power is proposed to apply to both financial and credit products.

Under the proposed legislation, this power will only apply prospectively; that is, it will not apply to products that have already been provided. We will need to consult the affected parties prior to making an order.

While the current proposed changes are welcome, we have submitted to the Government that we think the design and distribution obligations should be expanded to cover products regulated by the National Credit Act.

Responsible lending surveillance

Very briefly, I also want to mention a targeted surveillance activity we undertook last year. We reviewed the credit assessment processes of several lenders to assess their compliance with the responsible lending provisions. The participating entities included some issuers of residential mortgage-backed securities.

Following our work, we have seen the participating credit providers improve their processes for the collection and verification of information about the consumers’ financial situation. Industry can expect these kinds of surveillance activities to continue, and regulatory action to follow where breaches of the responsible lending provisions are identified.

Regulatory environment and the future

This is a unique and turbulent time for the financial services industry.

Royal Commission

Three of the rounds of hearings of the Royal Commission have touched on credit matters. Many of the issues raised were already under consideration by ASIC and our work on some of these matters is continuing.

The Royal Commission has produced an interim report that covers the first four rounds of public hearings, including the first round on consumer credit. We have made submissions to the Royal Commission on the content of the interim report.

We look forward to continuing to assist the Government in improving the regulatory framework for financial services in Australia.

ASIC’s enforcement initiatives

ASIC has received additional funding from Government to assist ASIC to accelerate its enforcement in financial services and credit.

Industry should recognise that ASIC will have even greater capacity to pursue breaches of the law we administer and we have very clearly heard the message that the community expects us to utilise court processes as much as possible.

Implementing new supervisory approaches

A key part of our work over the next year will be implementing new supervisory approaches. This work follows additional funding which was recently announced by Government to progress our strategic priorities.

One of our key new initiatives is a Corporate Governance Taskforce, which will undertake targeted reviews of corporate governance practices in large listed entities. This will allow us to shine a light on ‘good’ and ‘poor’ practices observed across these entities. Poor corporate governance practices have led to significant investor and consumer losses as well as a loss of confidence in our markets.

We are also implementing a new and more intensive supervisory approach by regularly placing ASIC staff onsite in major financial institutions to closely monitor their governance and compliance with laws – we call this new programme of work close and continuous monitoring.

These new approaches will help us realise our vision for a fair, strong and efficient financial system for all Australians.

Other initiatives of interest to ASF members

Before I go, there are just a couple of other areas of ASIC work that I want to highlight to you.

Benchmarks Reforms : In July ASIC established a comprehensive regulatory regime for financial benchmarks. This followed on from the work of industry and ASX in May when the new methodology for BBSW came into effect. But it is important for Australian market participants to engage with the changes to LIBOR which will occur at end of 2021. It is critical for all market participants to plan for a post LIBOR world.

Wholesale Market Conduct: We are examining aspects of conduct in the FX Market. We recently reported on High Frequency Trading in the AUD/USD cross rate (Report 597) and we found high frequency trading was 25% of the total, down from a high of 32% in early 2013. We are also examining the practice ‘last look’ and plan to publish our observations and findings in due course.

After plans were originally announced in September, online Australian retail group Kogan.com has launched its home loan offering today (28 November), via Australian Broker.

The website sells everything from technology and homewares to holidays and insurance, and will now begin offering Kogan Money Home Loans.

The products are for a range of borrowers, including first home buyers, refinancers and investors.

Rates for owner-occupiers start from 3.69% per annum, comparison rate 3.70% p.a. or 3.83% p.a. with 100% offset. Investor rates start from 3.89% p.a., comparison rate 3.90% p.a. or 4.03% p.a. with 100% offset.

Kogan lists other benefits as fixed and variable home loans with the option of 100% offset accounts, as well as catering for specialist loans for self-employed, debt consolidation and those with credit issues.

The retailer said it provides a loan calculator to help borrowers get a quicker understanding of how much they can borrow, as well as lending specialists who will call borrowers back “within a few business hours”.

The home loans are funded by Adelaide Bank and Pepper Group.

The Essential Home Loans range, funded by Adelaide Bank, boasts free online redraw, no monthly or ongoing fees on the home loan and $10 per month for the 100% offset account, unlimited extra repayments (up to $20,000 p.a on fixed), interest only options available, and weekly, fortnightly, or monthly repayments (for P&I loans).

The Options Home Loans range funded by Pepper helps those that have unique circumstances, such as having a non-standard income, having suffered previous financial setbacks or are self-employed.

David Shafer, executive director of Kogan.com, said, “Kogan.com delivers products and services that Australians need at some of the most affordable prices in the market, and we’re proud to extend our offerings to the financial services Australians use every day through the launch of Kogan Money Home Loans.

“Digital efficiency continues to be a key driver of our ability to achieve price leadership, and we’ve taken this approach with our Kogan Money Home Loans offering.

“Knowing where to start when getting a home loan can be difficult, especially in a crowded market. Kogan Money Home Loans is making this process easier and more efficient for the many Australians looking to secure a home loan either when purchasing a property or as part of a refinance.

“A large part of Kogan Money Home Loans’ mission is to provide solutions to help people lower the cost of owning homes and investment properties and to achieve property ownership.”

A fintech start-up is celebrating a $25million raise as it continues on its pathway to becoming Australia’s “most innovative home loan provider”; via AustralianBroker.

Athena Home Loans, which is still in its pilot phase, has closed its most recent Series B raise led by Square Peg Capital.

Industry super fund Hostplus and venture firm AirTree also joined the round, taking the group’s total capital raised to date to $45m.

The Series B raise comes six months after the company announced a Series A fund raise led by Macquarie Bank and Square Peg Capital and three months after announcing a strategic partnership with Resimac Group.

Powered by Australia’s first cloud native digital mortgage platform, Athena aims to bypass the banks to connect borrowers to superfund backed loans.

The company was founded by two ex-bankers, Nathan Walsh and Michael Starkey, who said they wanted the journey to home ownership to be faster, cheaper and stress free.

Square Peg Capital invested in Athena in Series A and has further solidified its support of the home loan provider by leading the Series B round.

Venture capitalist and co-founder of Square Peg, Paul Bassat, who also sits on the Athena Board, said investing further into Athena proves the potential they see in the business.

He said, “Having worked with Nathan, Michael and the team over the last year I have enormous admiration for the speed at which they have navigated complex financial systems to develop a robust and customer-centric mortgage service.

“Athena is solving a really important problem for home buyers and is certainly one of the most exciting Fintech companies in Australia.

“We are thrilled to back the team again and look forward to supporting them on this extraordinary journey.”

Industry superannuation fund Hostplus has more than 1.1 million members and $37billion in funds under management.

Hostplus has spearheaded investment in the local start-up ecosystem, with more than $1billion of its fully diversified portfolio committed to Australian venture capital managers.

Hostplus chief investment officer, Sam Sicilia, said that “Athena is a great example of disruptive innovation delivering big savings for home loan borrowers”.

Athena COO Michael Starkey said, “We are delighted to have Hostplus and AirTree joining Athena as investors. Athena’s journey has benefited hugely from the insights and support from some of Australia’s smartest investors. It’s clear the timing has never been better to offer a fairer home loan.”

Athena CEO Nathan Walsh said, “During our pilot, we are already seeing the power of the Athena proposition to save money and change lives.

“A single mum who will be able to pay off her home loan 19 months earlier and save $130,000 over the life of the loan.

“A family with three young kids who will save $40,000 on their home loan can now take the family on the first holiday in years. It’s powerful stuff.”

Commenting on the company’s upcoming launch in Q1 2019, Nathan said, “Our key priorities with the investment will be to continue to innovate our platform, invest in talent and scale the business.

He makes the point that non-banks are picking up the investor slack, as reflected in the composition of the collateral underpinning RMBS. The high volume of RMBS issuance by non-banks is consistent with a sizeable increase in their mortgage lending.

More evidence that this sector of the market needs tighter controls?

Today I’ll provide an update on developments in the markets for housing and housing credit. These markets are closely related and both are of considerable interest to those that issue and those that invest in Australian residential mortgage-backed securities (RMBS).

Along the way, I’ll make use of data on residential mortgages from RMBS that are eligible for repurchase operations with the Reserve Bank.[1] Among other things, these data are a useful source of timely information on interest rates actually paid, loan by loan. As I’ll demonstrate, this allows us to infer something about shifts in the supply of, and demand for, housing credit, thereby shedding some light on the different forces driving these markets.

With this background in mind, I’ll also review some recent developments in the RMBS market. And I’ll finish by taking the opportunity to emphasise that RMBS issuers and investors should be prepared for any future changes in the use and availability of benchmark interest rates.

Interactions between the housing market and the market for housing credit

As highlighted recently in a speech by the Deputy Governor, the markets for housing and housing credit are going through a period of significant adjustment.[2] After years of strong growth, housing prices have been declining nationally, driven by falls in Melbourne and Sydney over the past year. Also, there has been a noticeable decline in investor credit growth and an easing in owner-occupier credit growth. The cycles in the growth of overall housing prices and investor credit have moved together quite closely over the past few years (Graph 1).

Graph 1

Underpinning these changes, there have been shifts in the demand for, and supply of housing, as well as in the demand for, and supply of, housing credit.

Credit supply affecting housing demand

The links between these two markets run in both directions, from housing credit to the housing market, and from the housing market to housing credit. Of late, the story more commonly told, though, is that a tightening in the supply of credit over recent years has impinged on the demand for housing.

This story is certainly the more apparent one in terms of its causes and effects. In particular, the measures implemented by regulators over recent years to address the risks associated with some forms of housing lending have worked to mitigate those risks and they have also led to a noticeable slowing of investor credit. This, in turn, has contributed to a decline in the demand for housing.

Again, these links have been discussed by Guy Debelle and are well-documented in the Bank’s latest Financial Stability Review (FSR).[3] In late 2014, the Australian Prudential Regulation Authority (APRA) set a benchmark for investor lending growth at each bank of no more than 10 per cent per annum (Graph 2).[4] Then in March 2017, APRA announced it would require interest-only loans – which are disproportionately used by investors – to be less than 30 per cent of each bank’s new lending. Over the same period, several other measures were implemented, including to tighten up the ways in which banks assessed the ability of borrowers to service their loans, and to limit the share of loans that constituted a large portion of the value of the property being purchased.

Graph 2

Banks responded to these requirements in two key ways. First, for some years now they have been tightening lending standards, thereby reducing the availability of credit to higher-risk borrowers. Second, banks raised interest rates for new and existing borrowers, first on investor loans from 2015, and then on interest-only loans in 2017 (Graph 3). In other words, the banks tightened the supply of credit, most notably for investors.

Graph 3

The FSR presents estimates of the effect of APRA’s first round of regulatory changes from late 2014. The key conclusions of that analysis are that, with the introduction of the 10 per cent investor credit growth benchmark:

the composition of new lending shifted away from investors and towards owner-occupiers, with little change in overall housing loan growth;

and housing prices have grown more slowly in regions with higher shares of investor-owned properties.

So, that’s the story that emphasises the effect of prudential measures on the supply of credit. And, in turn, the effect of tighter credit supply on the demand for housing.

I now want to draw your attention to the story less often told about the important causal link going in the other direction. In particular, the correction in the housing market over the past year or so appears to have been impinging on the demand for credit.

There are a number of reasons for the ongoing adjustment in housing prices:

the aforementioned reduction in the supply of credit;

the large increase in the supply of new housing associated with the high levels of housing construction in Brisbane, Melbourne and Sydney;

weaker demand from foreign buyers due to stricter enforcement of Chinese capital controls and various policy measures in Australia (many of which were implemented by various state governments) that have made it more costly for foreign residents to purchase and hold housing;

and last, but by no means least, the very substantial growth in housing prices over a long period, which had pushed housing prices to record levels as a share of household incomes and raised the prospects for a correction.

In support of this last point, I note that housing prices in Melbourne and Sydney (which had increased by 55 and 75 per cent respectively since 2012) are currently experiencing larger declines than in Brisbane (where housing prices had risen 20 per cent from 2012 to the recent peak; Graph 4).[5] It is also worth noting that housing prices are currently rising in Adelaide and Hobart. In addition, in Melbourne and Sydney house prices had run up further than apartment prices, and it is now house prices that have declined the most.[6]

Graph 4

While there may have been numerous causal factors, after a period of slowing housing price growth, more recently it is clear that housing prices are in decline in a number of major markets. This dynamic would have weighed heavily on the minds of buyers; particularly investors whose only motivation for buying is the return on the asset. An expectation of even a modest capital loss provides a strong incentive for them to delay buying a property, particularly in an environment of relatively low rental yields.

But how can we assess the role of factors affecting credit supply versus those affecting credit demand? Changes in the price of credit – that is, interest rates – can help. Other things equal, a fall in the supply of credit relative to demand can be expected to be associated with higher interest rates on housing loans. In contrast, a fall in the demand for credit (relative to supply) should be associated with a decline in interest rates. Just to be clear, I’m talking about the credit supply and demand curves shifting inwards. The former, by itself, reduces quantities while prices rise as the equilibrium shifts up along the demand curve. The latter, by itself, reduces quantities but decreases prices as the equilibrium shifts down along the supply curve.

So what’s happened to the interest rates borrowers are actually paying? The Securitisation Dataset provides estimates for both owner-occupiers and investors.

There has been a modest broad-based decline in outstanding mortgage rates in the Securitisation Dataset over the year to August (Graph 5). This suggests that banks were responding to weakness in credit demand by competing more vigorously to provide loans to high-quality borrowers. Indeed, looking just at new loans there is some evidence that average variable interest rates declined by more for investors than owner-occupiers, which is consistent with a noticeable decline in the demand for investor credit.

Graph 5

However, compositional changes might also explain why there was a slight decline in interest rates over this period. In particular, the tightening in lending standards has helped to shift the profile of loans away from higher-risk borrowers. This shift would have contributed to the decline in average interest rates paid as better quality borrowers tend to get loans at lower rates. However, it turns out that rates have declined over this period even within the set of low-risk borrowers – for example, those with low loan-to-valuation ratios (LVRs) (Graph 6). So the decline in average rates paid has been driven by factors other than just compositional changes.[7]

Graph 6

While banks began the process of tightening lending standards from around 2015, over the past year or so they have extended these efforts by applying greater rigour to their assessments of the ability of prospective borrowers to service loans. For example, banks have been assessing borrowers’ expenditures more thoroughly, which is likely to have contributed to reductions in the maximum loan sizes offered to borrowers.[8] Notwithstanding these changes, there are two other pieces of evidence that suggest that factors other than just a tightening in constraints on the supply-side have been affecting housing credit and housing market developments over the past year or so:

First, the majority of borrowers had earlier chosen to borrow much less than the maximum amounts offered by lenders. Hence, reductions in the sizes of maximum loans on offer over the past year does not imply one-for-one reduction in credit actually extended.[9]

Second, given that owner-occupiers have lower incomes on average than investors, they are likely to have faced noticeable reductions in maximum loan sizes as a result of the recent tightening in serviceability practices. However, owner-occupier credit growth has remained notably higher than investor credit growth.

In summary, weakness in credit demand – stemming from the dynamics in the housing market – has been a significant development over the past year or so. This is not to say that ongoing weakness of credit supply has not also been at work since then, but that credit supply is not the only part of the story.

Broader developments in the securitisation market

So far I have focused on the prudentially regulated banks. While the non-banks still only account for a modest share of outstanding mortgages, the sector has experienced very strong growth over recent years and is an important source of competition for the banks.

The RMBS market is a major source of funding for the non-bank providers of residential mortgages, and so RMBS issuance provides an indication of the recent growth in this sector. Last year, RMBS issuance was at its highest level since the global financial crisis. Non-banks’ issuance was in line with the high levels issued by this sector in the mid-2000s (Graph 7). In 2018, RMBS issuance in aggregate has been lower, but this has been largely been driven by decreased issuance by banks. Non-banks, by contrast, are continuing to issue close to $4 billion of RMBS per quarter.

Graph 7

This high volume of RMBS issuance by non-banks is consistent with a sizeable increase in their mortgage lending. This is an unsurprising consequence of the tighter supervision and regulation of mortgage lending by banks. This is not to say that non-banks are unregulated. They operate under a licensing regime managed by the Australian Securities and Investments Commission. And, as my colleague Michele Bullock mentioned recently, the members of the Council of Financial Regulators (which includes the Reserve Bank, APRA and ASIC) are monitoring the growth of the non-bank lenders for possible emerging financial stability risks.[10]

The Reserve Bank’s liaison indicates that non-banks have been lending to some borrowers who may otherwise have obtained credit from banks in the absence of the regulatory measures. Consistent with this, the Securitisation Dataset shows that a rising share of non-bank lending has been to investors. Indeed, there has been at least a five-percentage-point increase in the share of investor loans across all outstanding non-bank deals in the Securitisation Dataset over the past two-and-a-half years (Graph 8).[11] This is in contrast to the share of total bank loans to investors, which has been declining over that period.

Similarly, the share of non-bank loans that are on an interest-only basis has been stable over the past couple of years, whereas the share of bank loans that are interest-only has declined significantly over the same period.

Graph 8

The increase in the share of investor housing in deals issued by non-banks is one of the few noticeable changes in the composition of the collateral underpinning RMBS in the past couple of years. Indeed, for deals by non-banks the share of loans with riskier characteristics such as high LVRs or self-employed borrowers has been little changed.

One of the other changes to loan pools in new deals is a fall in seasoning (i.e. the age of loans when the deal is launched). This has been most pronounced for non-banks (Graph 9). It is consistent with non-banks writing a lot more loans. Hence, warehouses of their loans are reaching desired issuance sizes more quickly.

Graph 9

Despite the pull-back in RMBS issuance by the major banks over recent years, the broader stock of asset-backed securities (ABS) on issue increased by around $20 billion over the past 18 months, after remaining broadly stable for the previous 5 years (Graph 10; in addition to RMBS, ABS cover other assets such as car loans and credit card receivables). Demand for these additional asset-backed securities has been driven by non-residents.

Graph 10

As well as a shift in the composition of investors in ABS, we have observed some changes in deal structures over recent years. Of particular note, the average number of tranches per deal has increased from around four to eight (Graph 11). The increase has been broad-based across different types of issuers. This general trend covers deals with a greater number of tranches with differing levels of subordination, as well as deals where the top tranche is split into a number of individual tranches with different characteristics but equal subordination.

Graph 11

We have also seen what might be termed greater ‘specialisation’ of individual tranches. For instance, in recent years the use of one or more tranches with less common features – such as foreign currency, short term or green features – has increased.[12] This increased specialisation is consistent with issuers addressing the needs of different types of investors.

All of these developments point to the evolution of the Australian securitisation market over the past few years, with non-bank issuers playing an increasingly important role and non-resident investors taking an increasing share of issuance.

Benchmark interest rates, RMBS pricing and funding costs

The increase in bank bill swap (BBSW) rates in early 2018 has led to a modest rise in the funding costs of both banks and non-banks.[13] However, the increase in overall funding costs has been a bit greater for non-bank issuers than for banks. This is because banks have a sizeable proportion of their liabilities – such as retail deposits – that do not reprice in line with BBSW rates. Also, the bulk of non-banks’ loans are funded via RMBS issuance, and the cost of issuance has risen by a bit more than BBSW rates (Graph 12). The premium over the BBSW benchmark rate has risen to the level of two years ago. At the margin, these changes mean that non-bank issuers are not able to compete as aggressively on price for new borrowers as banks than was the case a year ago.

Graph 12

Most lenders have passed through modest increases in their funding costs to borrowers over the past few months. Despite these increases, competition for new loans remains strong, and interest rates for new loans are still well below outstanding rates. So credit supply is available to good quality borrowers on good terms and there is a strong financial incentive to shop around.

Interest Rate Benchmarks for the Securitisation Market

One final point I’d like to make on pricing, is that RMBS issuers and investors should be considering the implications of developments in interest rate benchmarks. In light of the issues around benchmarks such as LIBOR (the London Inter-Bank Offered Rate), substantial efforts have been made to reform these benchmarks to support the smooth functioning of the financial system.

BBSW rates are important Australian dollar interest rate benchmarks, and the 1-month BBSW rate is frequently used in the securitisation market. We have worked closely with the ASX and market participants to ensure that BBSW rates are anchored as much as possible to transactions in the underlying bank bill market. However, the most robust tenors are 6-month and 3-month BBSW, which are the points at which banks frequently issue bills to investors. In contrast, the liquidity of the 1-month BBSW market is lower than it once was. This is mainly due to the introduction of liquidity standards that reduced the incentive for banks to issue very short-term paper.

Given this, RMBS issuers should consider using alternative benchmarks.[14] One option would be to reference 3- or 6-month BBSW rates for new RMBS issues. Another option is the cash rate, which is the (near) risk-free benchmark published by the Reserve Bank.[15] Given the underlying exposure in RMBS is to mortgages rather than banks, it could make more sense to price these securities at a spread to the cash rate rather than to BBSW rates, which incorporate bank credit risk.

Issuers and investors globally, including in Australia, should also be prepared for a scenario where a benchmark they are using ceases to be published. In such an event, users would have to rely on the fall-back provisions in their contracts. However, for many products – including RMBS – the existing fall-back provisions would be cumbersome to apply and could generate significant market disruption. This is most urgent for market participants using LIBOR, since the regulators are only supporting LIBOR until the end of 2021. While we expect that BBSW will remain a robust benchmark, it is prudent for users of BBSW to also have robust fall-backs in place. The International Swaps and Derivatives Association (ISDA) recently conducted a consultation on how to make contracts more robust. We would expect Australian market participants to adopt more robust fall-backs in their contracts following this process.

Conclusion

As the housing market undergoes a period of adjustment, it is useful to have an understanding of some of the drivers at play. Much attention has been given to the effect of prudential measures in dampening the supply of credit and how this has affected the housing market. However, it is also important to acknowledge causation going in the other direction, whereby the softer housing market has led to weakness in credit demand. My assessment is that the slowing in housing credit growth over the past year or so is due to both a tightening in the supply of credit and weaker demand for credit. Within that environment, lenders are competing vigorously for high-quality borrowers.

Developments in the RMBS market are consistent with non-bank lenders providing an extra source of supply. While non-banks remain small as a share of total housing lending, developments over the past couple of years show that the sector continues to evolve. The recent increase in issuance spreads may provide some slight headwinds for the sector; however, spreads remain below their levels in early 2016.

Finally, I would urge both issuers and investors to be responsive to the forces affecting benchmarks used to price RBMS and to focus on preparing for the use of alternative benchmarks.

Australian fintech Tic:Toc – the world’s only fully digital home loan platform – has announced Bendigo Bank will use Tic:Toc’s proprietary technology to power its own instant home loan, Bendigo Bank Express.

The white label partnership will allow Bendigo Bank to be the first Australian lender offering a digital home loan application and assessment process under its own brand, accelerated with Tic:Toc technology.

Tic:Toc launched the World’s first instant home loan™ in July 2017, and is now collaborating with financial institutions to offer their platform as a service; helping bring traditional home loan processes up to speed.

Tic:Toc’s technology offers customers a streamlined digital fulfilment process, while lenders benefit from significant efficiencies in the way they can originate home loan customers. The automated assessment strips cost from the process and delivers higher responsible lending standards via inbuilt reg-tech and digital validation of income and expenses.

Announcing the agreement, Tic:Toc founder and CEO, Anthony Baum, said most importantly, the customer will be the ultimate beneficiary of the collaboration between financial institutions and fintechs.

“Tic:Toc is changing the customer experience when it comes to home loans. It’s no longer necessary to wait weeks for home loan approval, when it can be done digitally and conveniently.

“There’s actually not much difference between home loan options. But there can be a big difference in how that home loan is delivered, and the experience for the customer.

“Our automated assessment and approval technology also creates dramatic cost efficiencies for lenders.

“You only need to look to the United States to see how a digital home loan can change a market: Quicken Loans is now America’s largest home loan lender after launching their online product, Rocket Mortgage.

“Our partner, Bendigo and Adelaide Bank, shares our passion for great customer outcomes, so we’re delighted the Bank has chosen Tic:Toc to offer its customers a truly digital experience, if they want it.”

Bendigo and Adelaide Bank Managing Director, Marnie Baker said, “Our partnership with Tic:Toc is another example of Bendigo and Adelaide Bank investing in innovative technologies to offer Australian consumers more choice, and ultimately, better digital experiences.

“Our strategy means we can provide the best solution to customers by selecting the right partner to offer the right services to meet our customers’ needs and make it easier for them to do business with us. Fintech disruption, combined with banking innovation, is helping us drive better outcomes and we consider relationships with fintechs, such as Tic:Toc, as a mutually beneficial strategy.

“We believe we can grow our business through our vision of being Australia’s bank of choice and we will do this by providing new and existing customers with valued and relevant products and services, all while investing in new capability and innovation,” she said.

Bendigo Bank Express will be available to customers in early 2019.

Since its launch, Tic:Toc has received more than $1.6 billion in value of submitted home loan applications. While the white label product will be available directly from Bendigo Bank, the multi award-winning home loans originated by Tic:Toc are already available throughout Australia at tictochomeloans.com.