Sharp fixed and variable rate home loan reductions are set to trigger a spike in refinancing applications through the broker channel, according to Aussie CEO James Symond. Via The Adviser.

Last week, the Reserve Bank of Australia (RBA) lowered the official cash rate by 25 bps from 0.75 per cent to 0.5 per cent – marking the fourth cut since June 2019 when the easing cycle commenced.

This followed a sharp turnaround in

sentiment ahead of the RBA’s monetary policy board meeting, with

analysts initially expecting the central bank to keep rates on hold.

Developments in the domestic and global

economy are likely to have altered the RBA’s tone, with weak local

market indicators and the coronavirus (COVID-19) outbreak rattling

market confidence.

A host of lenders, including the big four banks announced variable home loan rate reductions in response to the cut.

Bendigo and Adelaide Bank is the latest

lender to announce variable rate reductions, passing on the full 25 bps

to new and existing customers, effective 27 March.

Bendigo Bank has also cut small business and overdraft variable rates by the full 25 bps, also effective 27 March.

“In an environment experiencing

historically low rates, we have carefully evaluated our responsibility

to borrowers and communities with the impact lower rates have on

depositors, our business performance and all other stakeholders,”

Bendigo Bank’s managing director, Marnie Baker said.

“At the same time, many customer and

communities are facing a long recovery from bushfires and drought and

coupled with the still largely unknown economic impacts from COVID-19,

this decision aims to further support our home loan and business

customers and our many communities nationwide.”

Adelaide Bank’s head of third-party

banking, Darren Kasehagen, added: “These changes will have a direct and

positive impact [on] what is a most uncertain time for our home loan

customers.”

“The decision allows customers to take advantage of the lowest variable home loan rates that have been available for some time.

“As always, we carefully considered the

impact on all stakeholders and the overall cost of funding in arriving

at this decision.”

Macquarie Bank and ING, which were among

the lenders to drop variable rates by the full 25 bps, have also

announced sharp reductions to their fixed rate home loans.

Macquarie has dropped two and three-year

fixed rates to as low as 2.64 per cent for owner-occupied borrowers

paying principal and interest (P&I) and with a loan-to-value ratio

(LVR) of less than 70 per cent.

Owner-occupied P&I rates have also

been reduced to 2.74 per cent for four and five-year fixed rates for

borrowers with an LVR of less than 70 per cent.

Meanwhile, ING has slashed its fixed rates

to as low as 2.49 per cent for owner-occupied P&I borrowers with

the Orange Advantage product (3.89 per cent comparison rate).

ING’s investor fixed rates have dropped to as low as 2.74 per cent (4.44 per cent comparison rate).

In light of record-low mortgage rates,

Aussie Home Loans CEO Mr Symond has called on borrowers to consider

refinancing to save on their repayments.

“I expect many fixed and variable mortgage rates will fall below 3 per cent over the next month,” he said.

“Borrowers should be exploring the market for competitive rates and speaking with a reputable mortgage broker.

“A decision to see a mortgage broker could

save borrowers thousands of dollars and years off their repayments over

the life of the mortgage.”

Mr Symond added that he is expecting

refinance rates to spike beyond 30 per cent of new flows – as currently

experienced by Aussie’s broker network.

“Now is a great time to refinance and

exploit the strong competition amongst lenders, but borrowers need to

get sound, well-researched advice from a credible broker or lender

before taking this step,” he concluded.

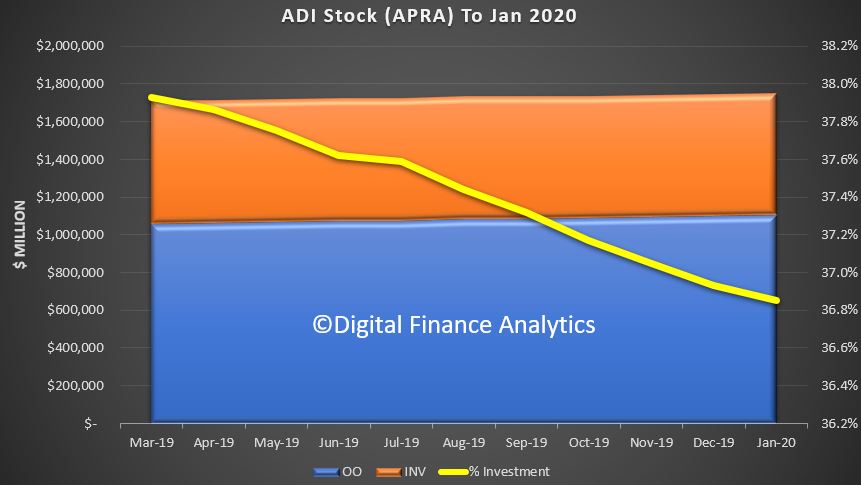

APRA released their monthly stats showing total reported balances for each bank to the end of January 2020.

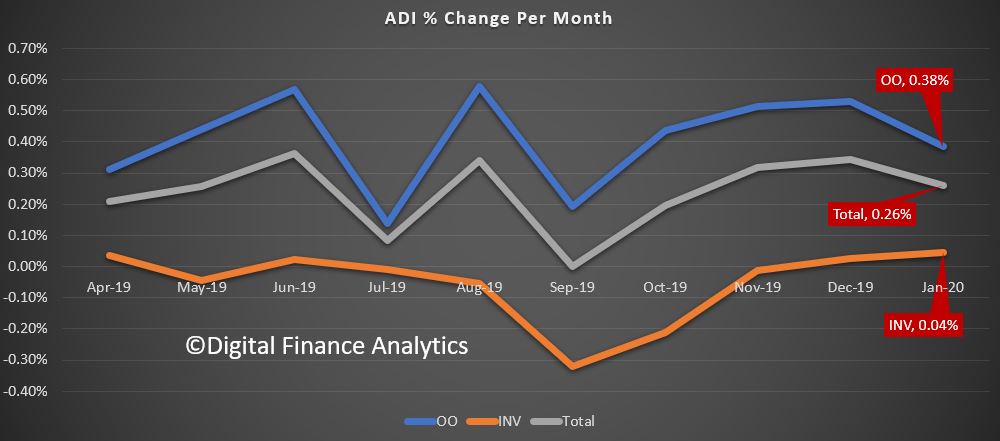

Total balances grew by 0.26%, to $1.75 trillion dollars, with loans for owner occupation up 0.38%, to $1.1 trillion dollars and investment loans up 0.04% to $0.64 trillion dollars. Investment loans made up 36.9% of the portfolio.

These are net balances, after repayments and new loans, and refinancing between banks.

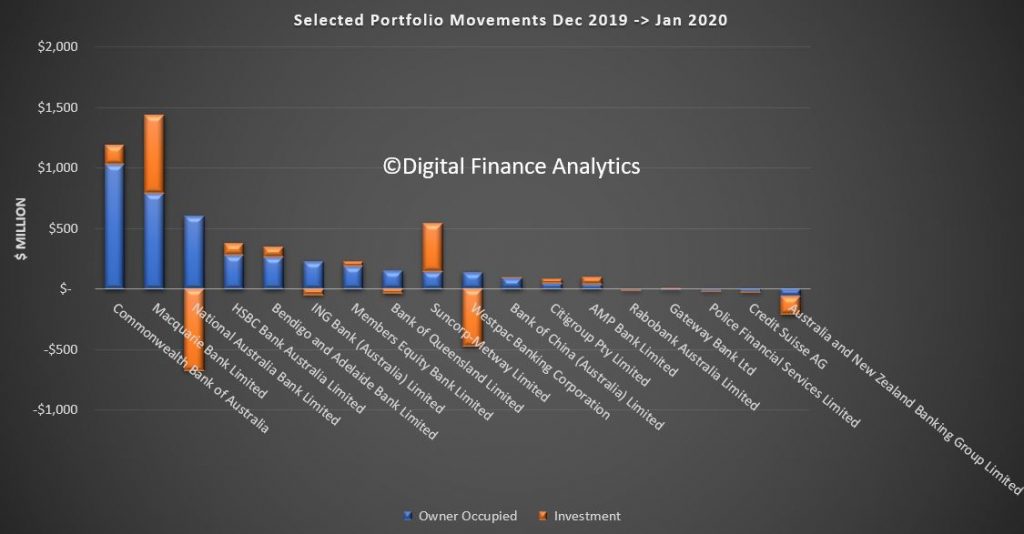

The individual movements between banks shows that CBA and Macquarie Bank are leading the growth, while NAB, and Westpac dropped investment loan balances, ANZ dropped both types, while Suncorp accelerated their investment lending. Macquarie still leads in investment lending however.

This suggests ongoing weakness in credit growth – and we will examine the RBA data shortly, also out today. But clearly individual lenders are executing different strategies, and the portfolio changes highlight the net impact.

ASIC has today started a four week consultation on draft guidance about the new best interests duty for mortgage brokers.

The new obligations were legislated by the Parliament in response to Recommendation 1.2 of the Royal Commission.

From 1 July, the obligations will require mortgage brokers to act in

the best interests of consumers and to prioritise consumers’ interests

when providing credit assistance.

Announcing the

consultation, ASIC Commissioner Sean Hughes said, ‘The obligations

properly align the interests of mortgage brokers with the interests and

expectations of their clients – the borrowers. Consumers should feel

confident that their broker is offering the best loan for their

circumstances and we expect that consumer outcomes will improve as a

result of this reform.’

‘We have released this

draft guidance for consultation as early as possible, to help promote

certainty for mortgage brokers as industry prepares for the new

obligations to commence in July’ Mr Hughes added.

ASIC’s proposed approach to the guidance is outlined in Consultation Paper 327 Implementing the Royal Commission recommendations: Mortgage brokers and the best interests duty

(CP 327). Consistent with the legislation, the draft guidance is

high-level and principles-based, but also incorporates practical

examples. The purpose of the guidance is to explain the obligations

introduced by the Government, it does not prescribe conduct or impose

additional obligations.

The draft guidance is

structured around the key steps common to the credit assistance process

of brokers, such as gathering information, considering the product

options available and presenting options and a recommendation to the

consumer.

ASIC welcomes views from

all interested stakeholders on the proposals in CP 327, as well as the

draft guidance. This will allow ASIC to understand how the guidance can

best assist brokers to meet these new legal obligations. ASIC expects

that the new obligations will also improve competition in the home

lending market.

ASIC seeks public comment on the draft guidance by 20 March 2020.

ASIC intends to publish final guidance before the obligations commence on 1 July 2020.

Download

Consultation Paper 327: Implementing the Royal Commission recommendations: Mortgage brokers and the best interests duty

Background

In February 2019, Parliament passed the Financial Sector Reform (Hayne Royal Commission Response—Protecting Consumers (2019 Measures) Act 2020,

which introduces a best interests duty for mortgage brokers in response

to Recommendation 1.2 of the Royal Commission. The duty is a statement

of principle which seeks to align the interests of the mortgage broker

with the interests and expectations of the consumer.

ASIC’s proposed guidance

will assist mortgage brokers to comply with these new legal obligations

by setting out ASIC’s views on what the best interests duty provisions

require and steps that can minimise the risk of non-compliance.

The best interests duty

introduced by the Government applies in addition to the responsible

lending obligations. ASIC’s draft guidance explains the interaction of

these two obligations, including that information gathered for the

purpose of complying with the responsible lending obligations may help

brokers to comply with the best interests duty.

ASIC’s draft guidance follows research we published last year in Report 628Looking for a mortgage: Consumer experiences and expectations in getting a home loan. Key findings from this research included:

consumers who visit a mortgage broker expect the broker to find them the ‘best’ home loan;

mortgage brokers were inconsistent in the

ways they presented home loan options to consumers, sometimes offering

little (if any) explanation of the options considered or reasons for

their recommendation; and

first home buyers were more likely to take out their loan with a mortgage broker.

AFG and Connective are mortgage aggregators that act as intermediaries between lenders and their affiliated brokers.

“Combining AFG and Connective would create

the largest mortgage aggregator in Australia by a significant margin,

accounting for almost 40 per cent of all mortgage brokers operating in

Australia,” ACCC Chair Rod Sims said.

More than half of all home loans written

each year are initiated through the broker channel, and brokers play an

important role for consumers when seeking a home loan and for lenders in

reaching those consumers.

“AFG and Connective operate in an already

concentrated market, and not many other mortgage aggregators offer a

similar level or type of service. Additionally, potential entrants or

small players may be deterred from expanding by various barriers,

including compliance costs,” Mr Sims said.

“The ACCC is concerned there will be

limited similar alternatives for brokers to switch to. This may

negatively impact the services offered to brokers.”

The ACCC has published a statement of

issues and is seeking further information about the supply of mortgage

aggregation and distribution services, and the supply of home loans in

Australia. The ACCC invites further submissions from interested parties

in by 5 March 2020. The final decision will be announced on 7 May 2020.

AFG and Connective provide brokers with

access to a panel of lenders, and provide panel lenders access to

affiliated brokers to distribute loans. Generally, a broker will be

affiliated with one mortgage aggregator at a time, while lenders tend to

sit on a number of mortgage aggregator panels.

AFG and Connective also offer brokers

various support services to assist them to run their businesses. This

includes customer relationship management software that provides brokers

with the ability to compare products from the lender panel and assist

in the lodgement of loan applications.

AFG and Connective also offer white-label

or own-branded loan products under their respective brands. These

products are mostly funded by third party lenders, however, AFG also

offer loan products funded by its securitisation program.

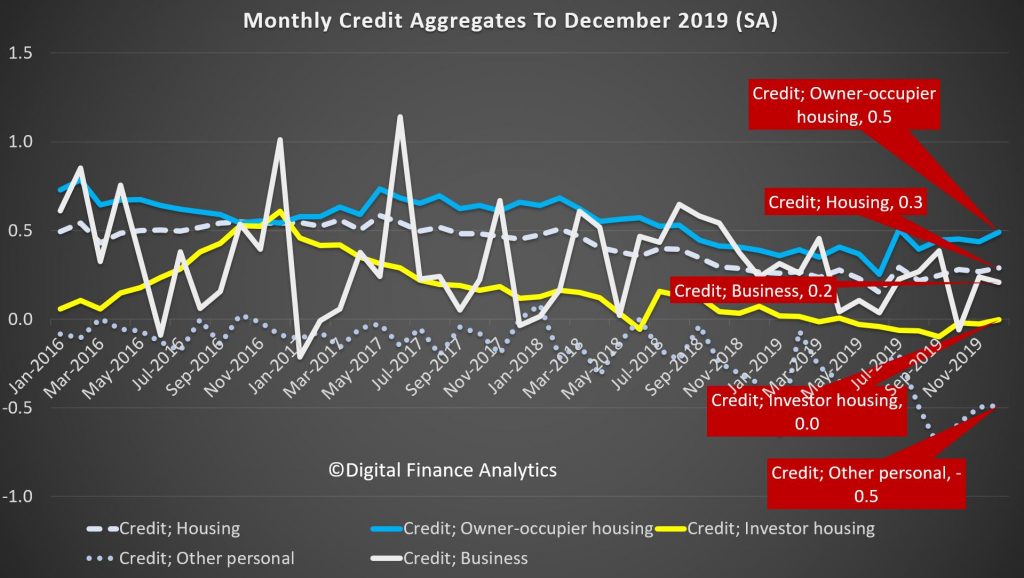

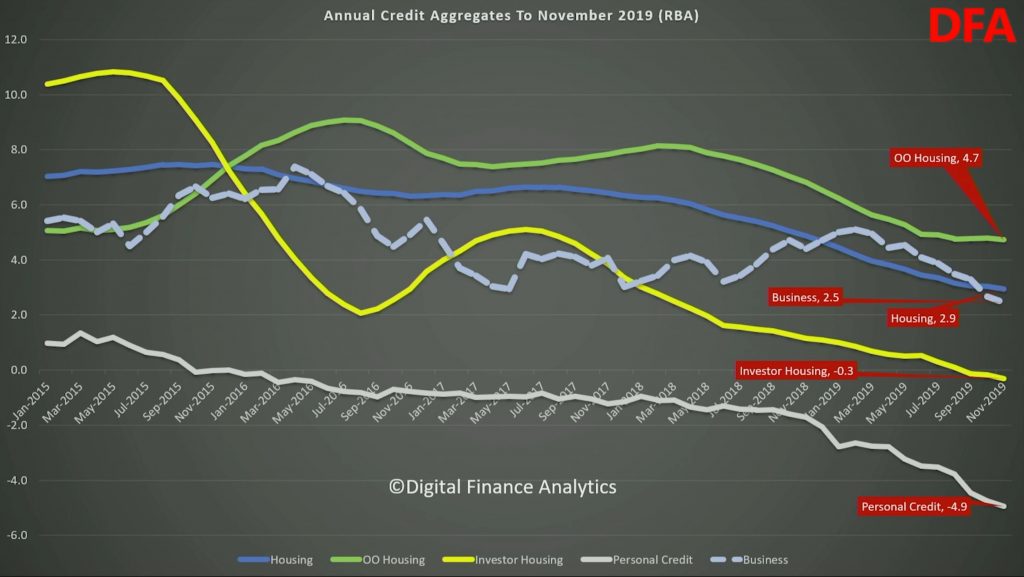

Looking at the RBA data first, over the past month housing credit stock (the net of new loans, repaid loans and existing loans) rose by 0.3%, driven by owner occupied housing up 0.5%, while investment loans slide just a little, but rounded to zero. Personal credit slid another 0.5% while business credit rose 0.2% compared with the previous month. These monthly series are always noisy, and they are also seasonally adjusted by the RBA, so there is plenty of latitude when interpreting them.

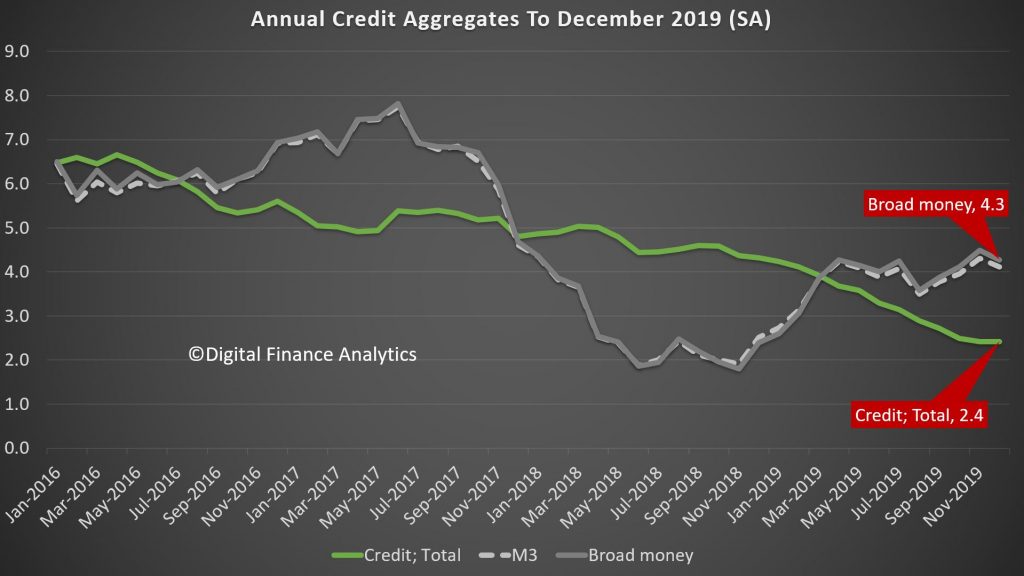

But overall, total credit grew by 0.2% over the month, while the broad measure of money rose just 0.1%.

The three month derived series helps to spotlight the key movements over the past few years. Credit growth for owner occupation rose 1.4%, and it has been rising a little since the May election, and the loosening of lending standards by APRA, and lower rates later. Its low point was a quarterly rise of 1% a few months ago. Investment lending continues to shrink, at 0.1%, but the rate of decline has eased from September, again thanks to loser lending standards. However this also reflects a net loan repayment scheme that many households, in the current tricky environment are on. Personal lending is still shrinking, falling at 1.6%, though the rate of slowing is reversing from a low of minus 1.8%. Business credit is o.4%, but has been falling since October where it stood at 1.8%, reflecting a serious downturn in business confidence and demand for credit. For businesses, the economic backdrop has been a challenging one. The global economy is sluggish and household spending is soft. In this environment business investment in the real economy has lost momentum across the non-mining sectors – weighing on credit demand. Rolling total credit for 3 months is 0.6%, up from a low of 0.5% a couple of months back.

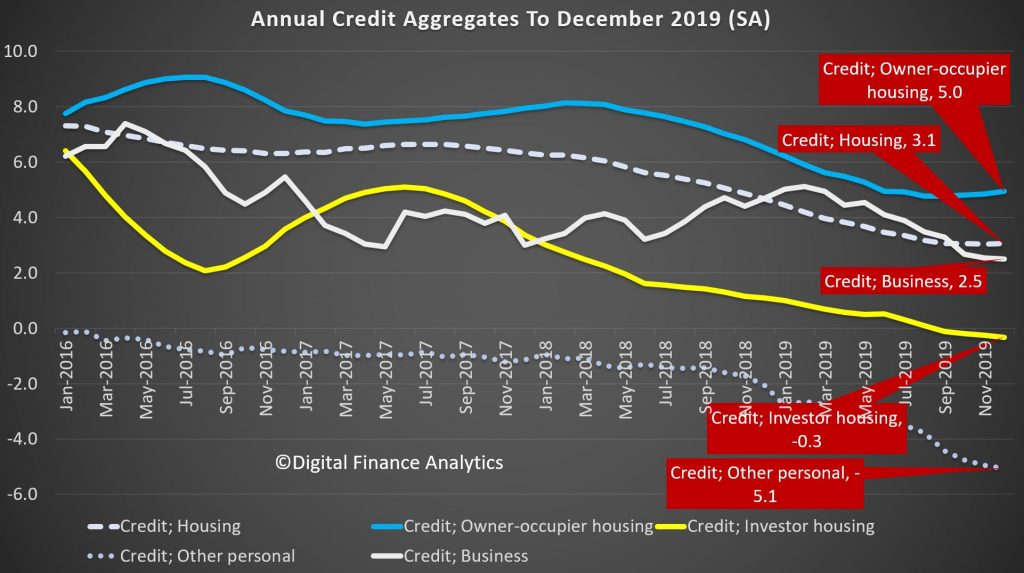

Turning to the annualised data series, housing credit is at 3.1% up from 3.03% last month. Annual owner occupied housing is up 5% from a low of 4.7% in August, while investor loans are down 0.3%, which is the largest fall we have ever seen. Personal credit is 5.1% lower, and that is another record low, while business credit grew by 2.5% on an annual basis, which is the lowest its been for years.

As a result, total credit grew 2.4%, which is the lowest level of growth since 2010, following the global financial crisis. Credit growth has progressively eased after peaking at 6.7% during the 2015/16 financial year. Key to the slowdown was the housing downturn as the cycle matured and lending conditions tightened. On the other hand, broad money is growing at 4.3%, and is significantly higher than last year, which we attribute to the positive terms of trade (thanks to iron ore prices and commodity volumes and RBA open market operations).

So while sentiment bounced after the May Federal election, which removed uncertainty around tax policy for the sector, as the RBA has lowered rates since June by a total of 75bps, with further cuts likely and APRA easing mortgage serviceability assessments; growth is anemaic, and of course sentiment is now in the gutter, thanks to the bushfires, coronavirus, and lack of income growth. While many analysts are predicting a bounce in credit in 2020, and a sentiment turnaround, pressure on global commodity prices and weak international tourism, as well as the drought are likely to take their toll.

We are also seeing more applications for mortgages being received, but also higher rejection rates, so we will see if this will really lead to stronger credit. And given such weak credit, we still question the veracity of the CoreLogic price series, which seems to exist in a different world. Our data supports much weaker average home price growth.

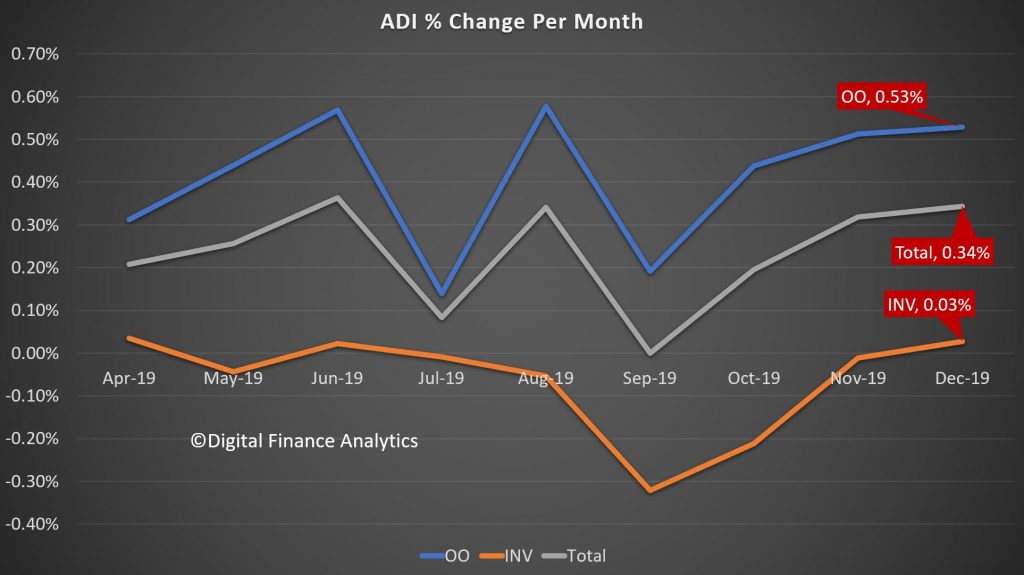

Turning to the APRA Bank series, the total value of mortgages lent (in original terms) grew by 0.34%, which is stronger than the market (0.3%), suggesting that the banks may be clawing back some business from the non-bank lenders, who have been quite active over the past couple of years. Within that owner occupied loans rose by 0.53% in the month, while investment loans grew 0.3%. The rate of growth remains slow.

The total stock of loans did rise, up around $5 billion dollars to $1.09 trillion for owner occupied loans, and up only slightly to $644 billion, giving total exposures of $1.74 trillion, a record. The mix of investment loans fell to a low of 36.9%.

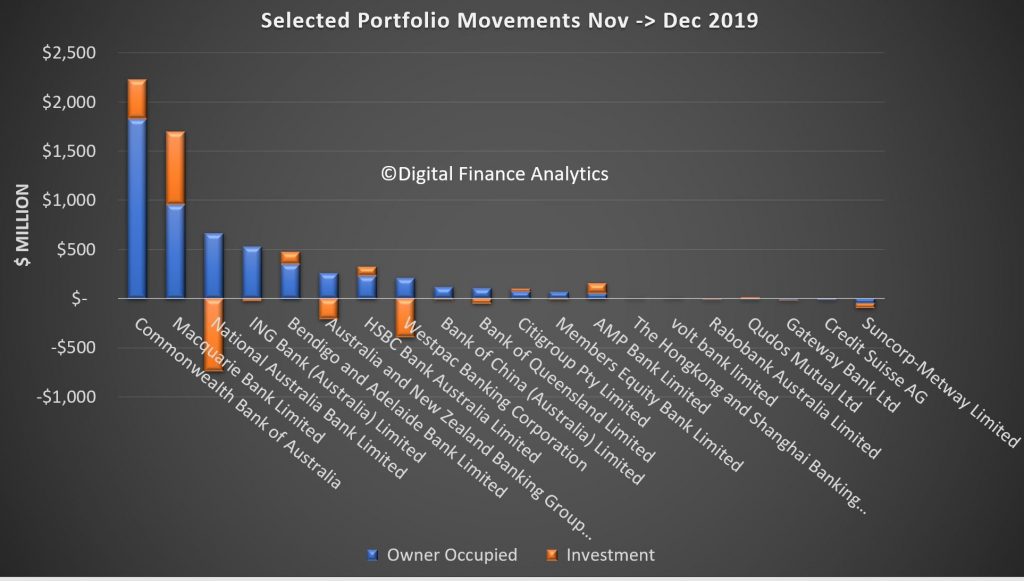

Finally we can examine the portfolio movements by individual lender, which reveals that, according to the data submitted by lenders (which may include some adjustments) CBA grew their portfolio the strongest, up more than $2.2 billion, including both owner occupied and investor loans, followed by Macquarie which continues to drive investor lending very hard, while NAB, Westpac and ANZ grew their owner occupied loans, while dropping their investor lending balances. Bendigo Bank, AMP and HSBC were also active in growing their investor loans. Neo-lender Volt Bank made an appearance in our selected list, while Suncorp dropped the value of both their owner occupied and investor loans. This highlights that lenders are steering quite different paths in their underwriting and marketing strategies. Time will tell whether the new loans being written are more risky.

And in closing, its interesting to note APRA’s release today saying that

The Australian Prudential Regulation Authority (APRA) will expand its quarterly property data publication to include new and more detailed statistics on residential mortgage lending.

In a letter to authorised deposit-taking institutions (ADIs) today, APRA confirmed the next edition of its Quarterly Authorised Deposit-taking Institution Property Exposures (QPEX) publication would include additional aggregate data on residential property exposures and new housing loan approvals.

The decision is part of APRA’s to move towards greater transparency, and will enable more in-depth market analysis by industry analysts, media and other interested parties.

The updated QPEX publication will also feature:

• reporting of additional sector-level statistics for the ‘Mutual ADI’ category; and

• clarified definitions for reported items, specifically for unreported loan-to-value ratios.

APRA Executive Director of Cross-Industry Insights and Data Division, Sean Carmody said: “APRA’s updated Corporate Plan commits us to increasing transparency of both our own operations and the industries we regulate. One of the key ways we can do that is by releasing more of the data we collect.

“With the ADI sector heavily reliant on commercial and residential property lending, enhancing QPEX will translate to greater transparency and sharper insights into one of the most crucial contributors to the economy.”

Consultation is continuing separately on a proposal for quarterly publication data sources to become non-confidential. This would mean that more of the underlying data may be disclosed to the public on a dis-aggregated basis. While this consultation remains open, APRA will continue to publish industry and peer group aggregate data, and mask data in QPEX where an individual entity’s confidential information could be revealed.

The next QPEX will be published on 10 March 2020 for the December 2019 reference period.

We believe that the dis-aggregated data should indeed be released – because sunlight remains the best disinfectant to quote Supreme Court Justice Louis Brandeis. Compared with the disclosures in other markets, Australia is so behind the times, on the pretext of confidentially. So we endorse the need for more granular data to help separate the lending sheep from the lending goats.

I caught up with the founder of Hero Broker, Clint Howen to discuss what he is seeing in the mortgage industry at the moment. The online platform gives an interesting perspective on the changes in the market.

Westpac yesterday announced a number of changes to its credit policy, which have also gone into effect across its subsidiaries: BankSA, Bank of Melbourne, and St George Bank. Via Australian Broker.

Investor lending

Effective 22 October, the maximum loan to value ratio for

interest-only investor loans was raised from 80% to 90% – including any

capitalised mortgage insurance premium.

The update applies to new purchases, refinances within Westpac Group

or externally, and loan variations such as switching from P&I

repayments to interest-only.

However, the current switching policy will continue to apply, with

customers only able to switch to interest-only repayments post 12 months

of loan drawdown.

The changes will not apply to interest-only owner occupier loans, which will maintain their maximum LVR at 80%.

HEM calculations

Also effective yesterday, referral to credit will no longer be

required in instances where expenses are greater than 130% of HEM and no

other reason that requires credit assessment is triggered, a change the

group expects to save brokers time and deliver faster outcomes to

customers.

Updated resources

The group also launched an enhanced version of its Assess calculator,

“developed in response to broker feedback.” It crafted the updated tool

to be more intuitive and streamlined, making the completion of

assessments “much quicker” and saving brokers valuable time.

Westpac plans to remain receptive to feedback moving forward,

inviting brokers to “give it a go” and share their thoughts on their

experience.

The older version of the Assess calculator will not be available for use after 15 November 2019.

Yet another inquiry has been announced into mortgage pricing as the ACCC is tasked to examine the banks failure to pass on in full official interest rate cuts engineered by the central bank. The ACCC’s preliminary report is due by 30 March next year, six months before the final report.

Beyond the crocodile tears, there are important questions here, because as we have highlighted, loyalty is not rewarded as the banks cut rates to attract new customers. In addition, deposit margin compression has reach a floor, and funding costs are under pressure. But nothing has fundamentally changed from recent ACCC and Productivity Commission reports. Yet, having another investigation takes pressure off The Treasurer, conveniently.

Via The Guardian. The treasurer, Josh Frydenberg, has asked the competition watchdog to examine why many mortgage holders are being charged rates well above the cash rate record low of 0.75%.

The higher rates have prompted allegations of price gouging by the banks – Commonwealth Bank,

Westpac, ANZ and National Australia Bank – which have previously cited

funding costs as a reason why not all reductions could be passed on.

“We need information about the cost of the funds of the banks and …

why they’re not passing on these rate cuts in full,” Frydenberg told

ABC television on Monday.

The inquiry, which will also include smaller institutions, comes

after an earlier royal commission into misconduct in the banking sector

uncovered predatory practices and dented market confidence.

But Frydenberg shrugged off suggestions that the new inquiry by the

Australian Competition and Consumer Commission would further affect

confidence in Australia’s banks.

“I actually did call the CEOs of the big four banks yesterday and

told them that this could actually help clear the air,” he said. “But at

the same time, you know, they’re defending their patch and will

continue to do.”

The treasurer said the banks need to explain how they balance the competing needs of shareholders and customers.

The official cash rate is at a record low of 0.75% after the Reserve

Bank of Australia cut interest rates three times this year. But the big

four banks on average passed on only 75% of the total reductions to

their customers.

“There are a number of smaller lenders that have actually wasted no

time in passing on these rate cuts on in full,” Frydenberg said.

“If the big four banks had passed on these 75 basis point rate cuts,

then somebody with a $400,000 mortgage would be more than $500 a year

better off in lower interest payments.”

The ACCC’s preliminary report is due by 30 March next year, six months before the final report.