According to the AFR, Australia’s red-hot jobs market is preventing the country’s most indebted borrowers from falling behind on their home loan, as internal Reserve Bank research reveals nearly one in five borrowers may be in mortgage stress.

While unemployment nationally was 3.7 per cent in August, unemployment among homeowners was likely “almost non-existent”.

But markets ascribe a three-in-five chance the RBA board will deliver one more rate rise by the end of the year, amid concerns about persistently high inflation in the services sector and a stubbornly strong jobs market.

Strong employment growth and nominal wage increases have insulated borrowers from some of the financial pain caused by high interest rates. About 18 per cent of loans across the country have a high repayment burden, defined as spending more than 30 per cent of household income on paying down a mortgage, according to internal RBA research released under Freedom of Information laws.

http://www.martinnorth.com/

Go to the Walk The World Universe at https://walktheworld.com.au/

This is an edit of my latest live show, as I walk through our latest financial stress analysis, to end August. Which post codes are most impacted, and what are the potential outlook for prices and defaults?

Go to the Walk The World Universe at https://walktheworld.com.au/

Digital Finance Analytics (DFA) Blog

DFA Live Q&A HD Replay: Latest Household Financial Stress And Analysis

This is an edit of my latest live show, as I walk through our latest financial stress analysis, to end August. Which post codes are most impacted, and what are the potential outlook for prices and defaults?

Go to the Walk The World Universe at https://walktheworld.com.au/

Almost one in three Australians are struggling to make ends meet, as cost-of-living pressures push more people to renegotiate bills, cut back on groceries and access their superannuation early. And one in five hit up friends or family as times tighten.

About 30 per cent of Australian adults find it difficult or very difficult to get by on their current income, according to a quarterly poll by the Australian National University.

Borrowers have been hit with 12 interest rate rises since May 2022 as the RBA tries to get on top of the most acute inflation outbreak in decades.

Financial stress is on the rise, with two-fifths of renters finding it difficult or very difficult to get by on present income amid a nationwide surge in rents.

But the biggest increase in stress over the past year was among people with a mortgage, who have borne the brunt of the fastest interest rate tightening cycle in a generation. About three in 10 borrowers are finding it tough.

None of this should be a surprise to followers of this channel, as I have been reporting the steady rise in cash flow stress in recent times, to new highs. My latest data to end August will be out in the next few days, and the trends continue to deteriorate.

Go to the Walk The World Universe at https://walktheworld.com.au/

Today’s post is brought to you by Ribbon Property Consultants.

Almost one in three Australians are struggling to make ends meet, as cost-of-living pressures push more people to renegotiate bills, cut back on groceries and access their superannuation early. And one in five hit up friends or family as times tighten.

About 30 per cent of Australian adults find it difficult or very difficult to get by on their current income, according to a quarterly poll by the Australian National University.

Borrowers have been hit with 12 interest rate rises since May 2022 as the RBA tries to get on top of the most acute inflation outbreak in decades.

Financial stress is on the rise, with two-fifths of renters finding it difficult or very difficult to get by on present income amid a nationwide surge in rents.

But the biggest increase in stress over the past year was among people with a mortgage, who have borne the brunt of the fastest interest rate tightening cycle in a generation. About three in 10 borrowers are finding it tough.

None of this should be a surprise to followers of this channel, as I have been reporting the steady rise in cash flow stress in recent times, to new highs. My latest data to end August will be out in the next few days, and the trends continue to deteriorate.

Go to the Walk The World Universe at https://walktheworld.com.au/

Today’s post is brought to you by Ribbon Property Consultants.

If you are buying your home in Sydney’s contentious market, you do not need to stand alone. This is the time you need to have Edwin from Ribbon Property Consultants standing along side you.

Buying property, is both challenging and adversarial. The vendor has a professional on their side.

Emotions run high – price discovery and price transparency are hard to find – then there is the wasted time and financial investment you make.

Edwin understands your needs. So why not engage a licensed professional to stand alongside you. With RPC you know you have: experience, knowledge, and master negotiators, looking after your best interest.

Shoot Ribbon an email on info@ribbonproperty.com.au & use promo code: DFA-WTW/MARTIN to receive your 10% DISCOUNT OFFER.

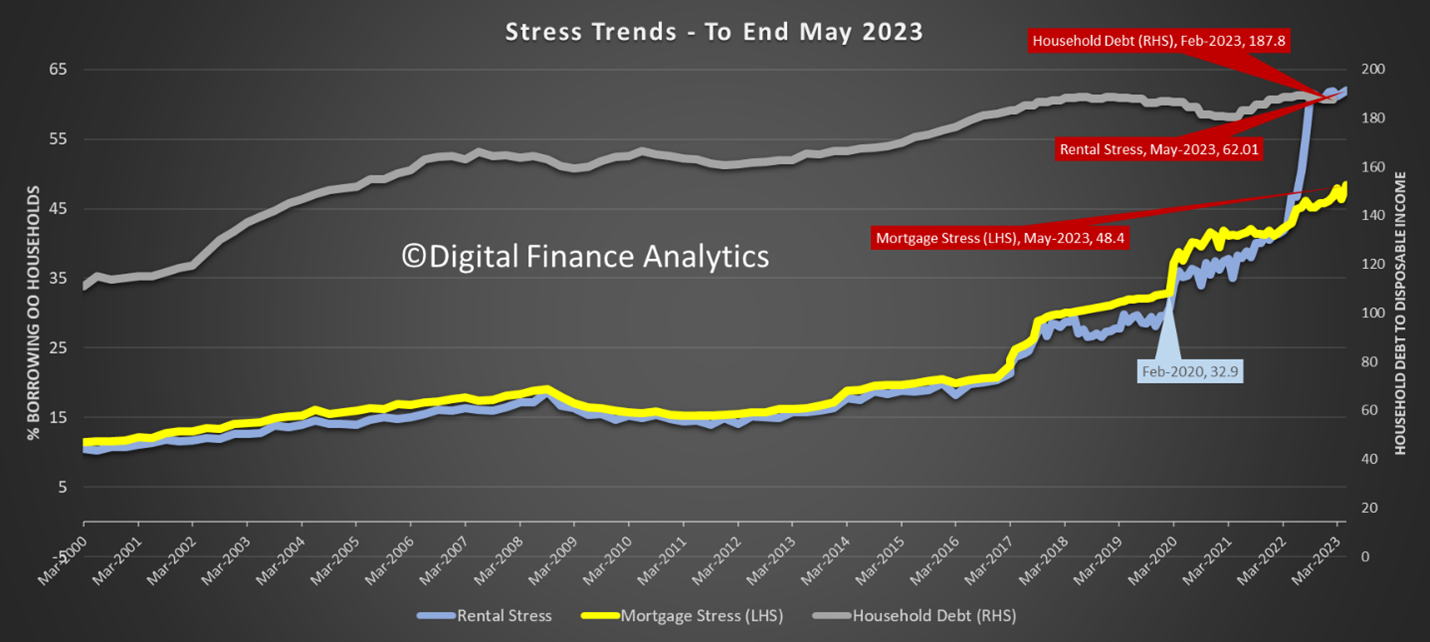

The hot news from our surveys and models is that financial stress, mortgage stress and particularly rental stress has gone higher again, as more households struggle with cash flow issues (our stress definition is based on cash flow status).

We walk though the main results, across the states, households segments and post codes. We also geo-map the results.

Let me know if you would like me to run another live show on this analysis, with post code data available.

The latest edition of the DFA Household surveys (a 0.5% sample across Australia), reveals the creeping mortgage and rental stress which is continuing to reach new highs. We measure stress in cash flow terms – money in and money out, and where there is a deficit, households are identified as “stressed”. Often households will be able to hang on for months by tapping into savings, drawing down more from refinanced loans, or from other forms or credit, or by tightening their spending. Some have been able to gain temporary relief by refinancing to a cheaper loan (even if on extended terms), but as income growth remain below the current inflation rates, incomes continue to lose ground. Data this past week showed more than ever households were now working multiple jobs to get buy.

The rises in stress since before COVID are stark.

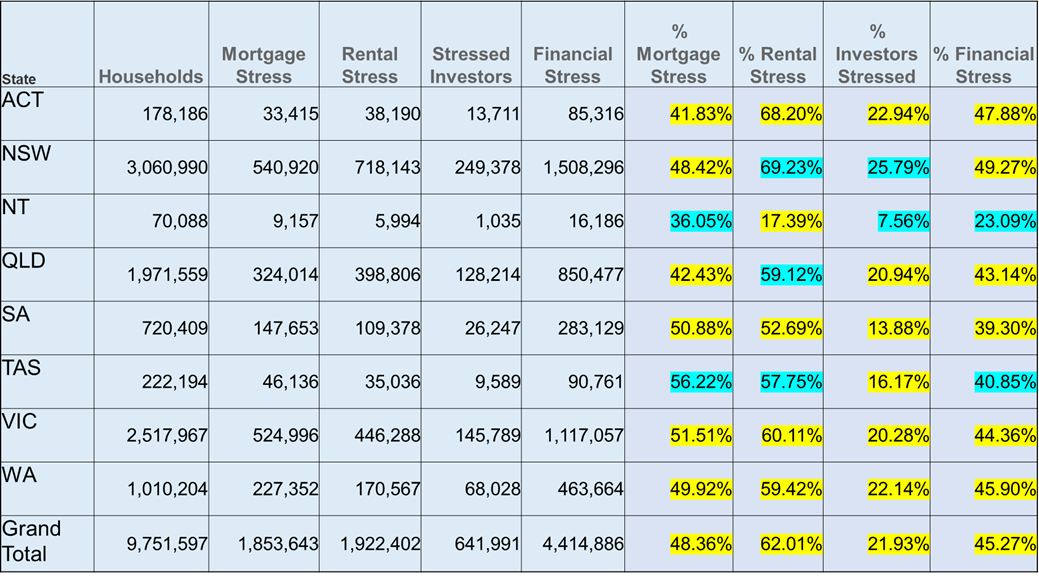

Analysis By State

We display the latest results by state and highlight in yellow where the proportion have rises since last month in yellow. Tasmania continues to experience the highest proportion of mortgage stressed households. But the more populous states of NSW and VIC reported strong increases. Rental stress remained highest in the ACT. Financial Stress, an aggregate measure across all households remained highest in NSW, where the average house price remain most extreme, compared to income.

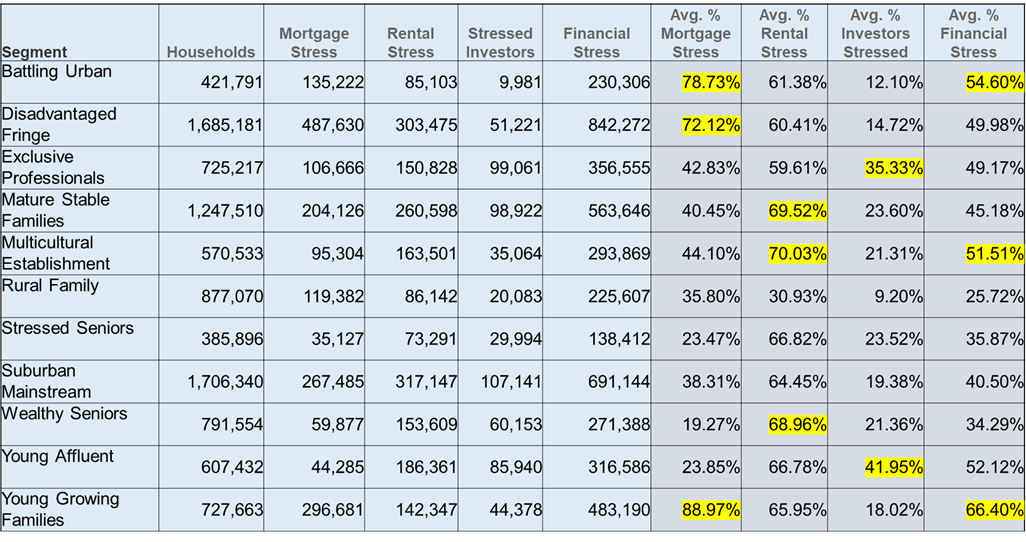

Analysis By Cohort

We can also analyse the data by our segments, or cohorts. This is a critical dimension to understand, given that generally younger households, including first time buyers are the most exposed. But other cohorts, including first generation migrants, and older households continue to drop into stress. Underlying inflation, as well as increasing mortgage rates, and rents explain this.

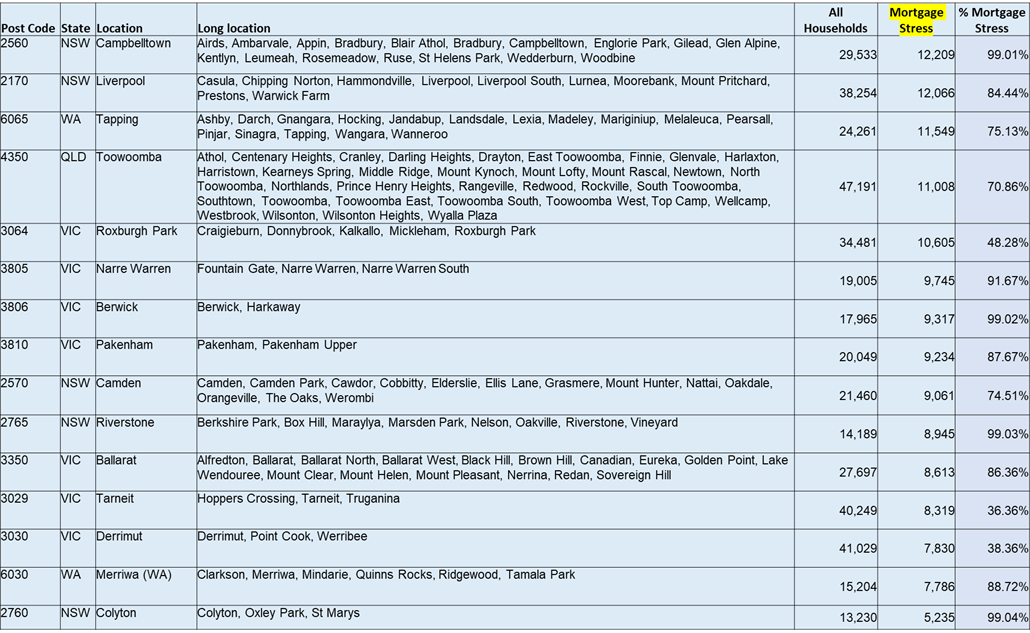

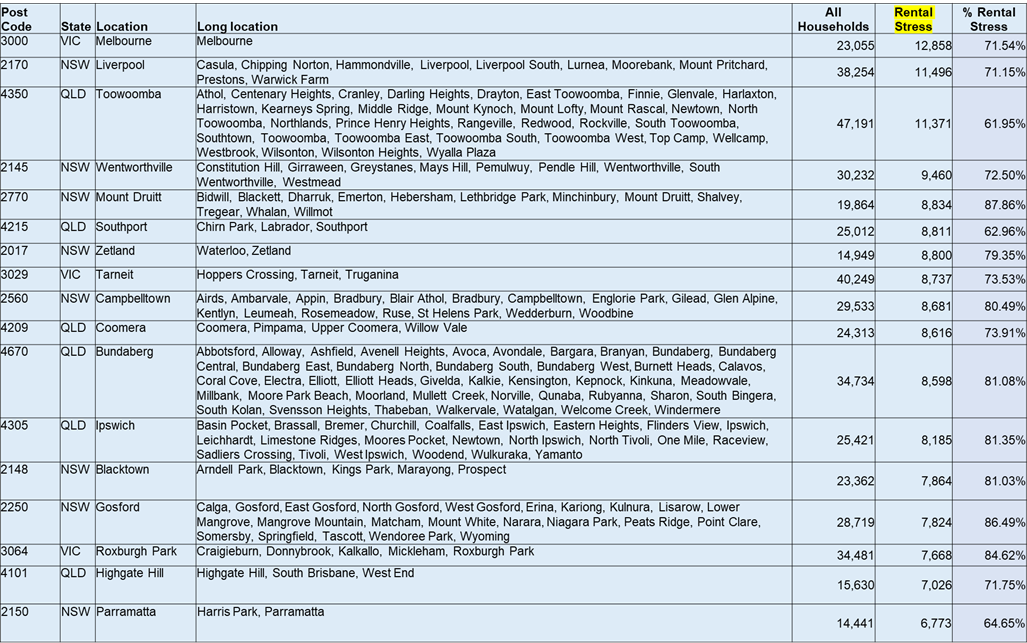

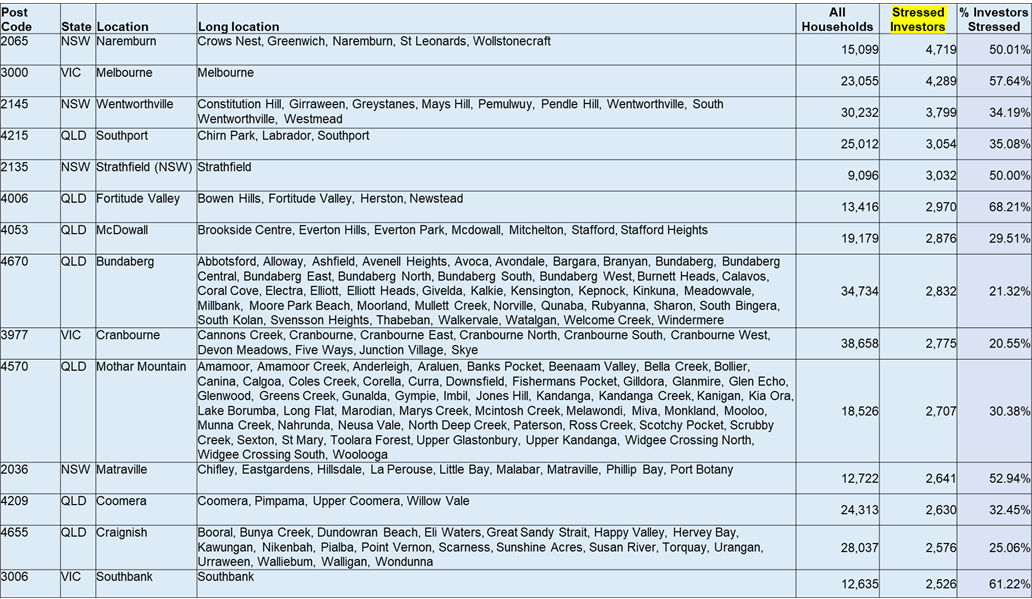

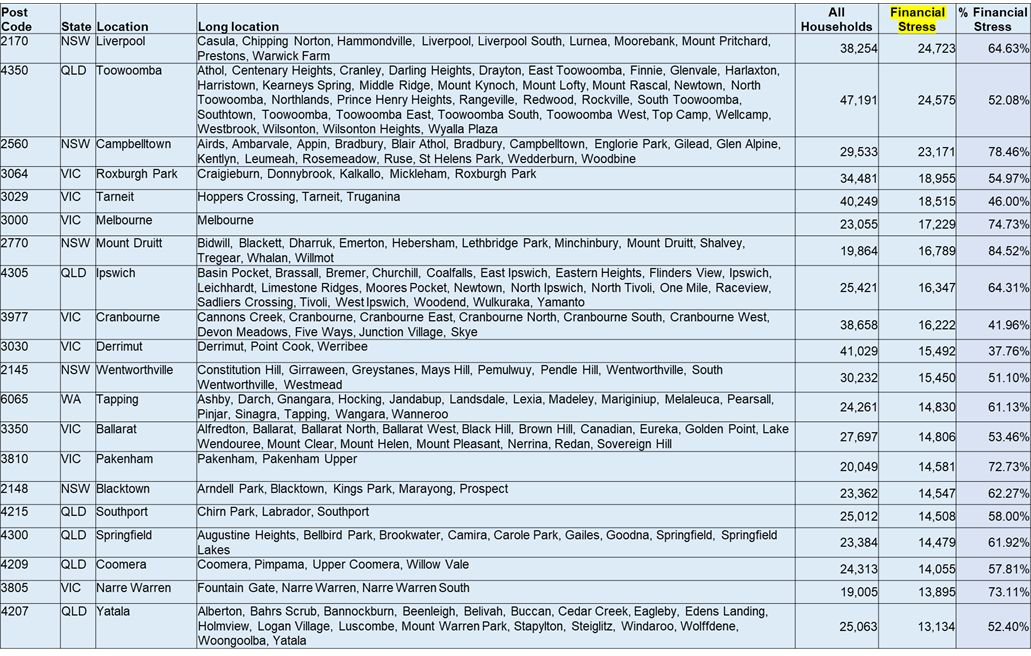

Post Code Analysis

We list the top households – by count – for each post code. We use counts to avoid over-weighting small household post codes.

We find that the focus of high stress remains in the high growth new-development suburbs, where many households purchased ant peak low rates and high home prices. But regional areas, and more developed suburbs are also registering. This is a national issue, not just confirmed to the main cities.

Future Outlook and Conclusions

We expect the RBA to lift rates again, as inflation is still far from being controlled and it is both sticky and embedded. Prices for electricity will rise from 1 July by up to 25% in some east coast states, whilst the mortgage cliff is reaching its heights in the same period.

The recent FWC award will have a small inflationary impact, and we expect more wages rises in the services, as well as more prices rises as businesses seek to support their margins.

Households in cash flow difficulty should discuss their mortgage situation with their bank, build robust cash flows, and prioritise effectively, because this is a crisis years in the making, and it will not abate any time soon. Moreover, hopes of cash rate cuts this year are fading, despite the rising risk of recession and higher unemployment, both of which may amplify stress further. We will update our analysis in a months’ time.

Blog")