ANZ NZ says David Hisco, its CEO of almost 9 years, is leaving due to ‘ongoing health issues’ and ‘the characterisation of certain transactions following an internal review of personal expenses’

This follows the Reserve Banks’ censure of their operations, as we reported recently.

According to a report in interest.co.nz, ANZ NZ is comfortably New Zealand’s biggest bank. As of March 31, it had total assets of $164.952 billion, total liabilities of $153.224 billion, and gross loans of $132.275 billion. Last year the bank’s annual profit was a shade under $2 billion.

The report says David Hisco, ANZ New Zealand’s CEO since 2010, is leaving the bank under a cloud.

In a statement ANZ says Hisco’s departure follows “ongoing health issues as well as Board concern about the characterisation of certain transactions following an internal review of personal expenses.”

“ANZ today confirmed the appointment of Antonia Watson as Acting CEO of ANZ New Zealand, following the departure of David Hisco,” ANZ says.

“While Mr Hisco does not accept all of the concerns raised by the Board, he accepts accountability given his leadership position and agrees the characterisation of the expenses falls short of the standards required.”

ANZ New Zealand Chairman John Key says it’s disappointing Hisco is leaving ANZ under such circumstances after such a long career, his departure is “the right one in these circumstances given the expectations we have of all our people, no matter how senior or junior.”

Monday’s announcement comes after ANZ NZ announced in late May that Hisco had taken extended sick leave with Antonia Watson, the bank’s managing director for retail and business banking, stepping in as acting CEO.

“We are fortunate to have an experienced executive in Antonia Watson to step in while we conduct a search for a replacement. Antonia’s extensive banking career has her well placed to help ANZ manage through this transition,” Key says.

“Mr Hisco will receive his contracted and statutory entitlements to notice and untaken leave, with all unvested equity to forfeit. The Reserve Bank of New Zealand and Australian Prudential Regulation Authority have been notified of the changes and are being provided all requisite filings.”

Key and Watson will hold a press conference later on Monday morning.

ANZ’s 2018 annual report shows (page 54-55) that in the year to September 2018 Hisco was on a A$1,170,703 fixed salary. On top of this he received A$644,397 in cash as ‘variable remuneration’ and A$864,274 of ‘deferred variable remuneration’, which vested during the year, giving a total remuneration received during the year of A$2,679,384. Hisco was paid in New Zealand dollars, with the amounts converted into Australian dollars.

Hisco’s appointment as ANZ NZ CEO was announced in September 2010, with him succeeding Jenny Fagg. An Australian, he had previously been managing director of ANZ NZ subsidiary UDC Finance between 1998 and 2000. Hisco, 55, has also been a member of Australian parent the ANZ Banking Group’s group executive committee with responsibility for Asia wealth, Pacific, and international retail.

An undoubted high-point of Hisco’s time as CEO of ANZ NZ was the successful culling of the National Bank brand, and movingANZ onto National Bank’s core ‘Systematics’ banking platformin 2012. The two moves effectively unified the two banks nine years after the ANZ Banking Group bought the National Bank from Britain’s Lloyds TSB for A$4.915 billionplus a dividend of NZ$575 million paid from National Bank’s retained earnings.

The Reserve Bank of New Zealand has released an important statement on the new approach they are going to adopt in policy setting. The focus will be on improving wellbeing. In addition they are expanding their dna to avoid group think. This follows their recent moves to lift bank capital.

There is so much here the RBA should embrace.

The Reserve Bank has significantly changed the way it makes monetary policy decisions, keeping itself in step with public expectations.

In a panel discussion last week at the Institute for Monetary and Economic Studies (Bank of Japan) in Tokyo, Reserve Bank Assistant Governor and General Manager of Economics, Financial Markets and Banking Christian Hawkesby talked about the importance of good decision making and governance, and of being credible and trusted, in achieving the long-term goal of improving wellbeing.

“We maintain our legitimacy as an institution by serving the public interest and fulfilling our social obligations. Keeping our ‘social licence’ to operate depends on maintaining the public’s trust that we are improving wellbeing,” Mr Hawkesby said.

“Thirty years ago New Zealand was prepared to accept a single expert – the Governor – making decisions about how to fight inflation. People now expect to see how and why decisions are made, expect that decision makers reflect wider society, and that current issues and concerns are factored into the decision making. By meeting these expectations, we can improve public trust in the legitimacy of the Reserve Bank’s work,” he said.

Mr Hawkesby outlined the new committee process that the Reserve Bank uses for deciding the official cash rate, noting that diversity among decision makers improves the pool of knowledge, insures against extreme views, and reduces groupthink.

“This diversity is needed to confront issues such as climate, technological, and other structural and social changes,” he said.

He also said that collaboration with government can be undertaken in a way that maintains the Reserve Bank’s political independence while working on the broader objective of improving wellbeing.

Here is the supporting speech.

Introduction

Tena koutou katoa

Thank you for the opportunity to talk about the Reserve Bank of New

Zealand and the changes we are making to maintain our credibility in

times of change.

I would like to focus on two building blocks of credibility:

renewing a social licence to operate by aligning our objectives with the needs of the public; and

achieving those objectives through good decision making enabled by a framework of good governance.

A common theme is the importance of transparency.

The imperative for change: Central banks in the 21st century

The first building block of credibility is the renewal of a social

licence to operate—by this I mean the legitimacy an institution earns by

serving the public interest. It is granted by the public when an

institution is seen to fulfil its social obligations.1

New Zealand was the first country to officially adopt inflation

targeting in 1989, with a number of central banks around the world

following the example.2

Under a single-decision-maker model, we brought inflation down from

around twenty percent to two percent in five years. In doing so, we

helped build our credibility during the high-inflation environment of

the times.3

Fast-forward to 2019, and monetary policy in New Zealand has

undergone major change. Firstly, we have adopted a dual mandate, focused

on achieving price stability and supporting maximum sustainable

employment. Secondly, we have adopted a committee structure for decision

making, and are delivering greater transparency in our decision making.

Why the change?

The reform of our framework was not merely a simple choice based on

technical performance. As you can see in figure 1, when it comes to

inflation and growth, over the past 30 years inflation-targeting central

banks (e.g. New Zealand and the United Kingdom) have a pretty similar

track record to central banks with a dual mandate (e.g. Australia and

the United States). 4

The imperative for change comes from more than examining our history;

it comes from our expectations of the future, and the present we find

ourselves in. Our policy framework changed because times are changing.

For the Reserve Bank to maintain its credibility and relevance, we must

change too.

Figure 1: Inflation, and GDP growth across monetary policy frameworks5

Wellbeing of our people

Inflation has been low and stable in New Zealand for nearly 30 years.

There is a greater appreciation that low inflation is a means to an

end, and not the end itself. In the fight to lower inflation that was

perhaps easy to forget. The end goal is, of course, improving the

wellbeing of our people.6

For many in the general public, employment is one tangible measure of wellbeing. Employment can provide an opportunity to earn your own wage, contribute to society, and live a fulfilling life.

It is in this light that the Reserve Bank Act (1989) has been amended to include a dual mandate with an employment

objective alongside our price stability goal. Incorporating the

objective of supporting maximum sustainable employment, and equally

weighting it alongside inflation, emphasises our long-term goal of

improving New Zealanders’ wellbeing. This aligns us with the needs of

the public. And it helps us renew our social licence to operate – the

first building block for maintaining our credibility.

But it is not enough for the public to believe in and understand our

objectives. We must also prove to them that they can be achieved. This

brings us to the second building block necessary for maintaining

credibility: establishing modern governance principles for dealing with

modern problems, and translating good governance into good decisions.

Good governance

In preparing for our dual mandate, and a formal Monetary Policy

Committee (MPC), we have updated the principles and processes that form

our governance framework for monetary policy.

In pursuit of greater transparency, we have also published these

principles and processes in a comprehensive Monetary Policy Handbook

(the Handbook). 7 This is an essential document, for everyone from school students to MPC members.

Importantly, it is also a living document that will evolve as our understanding evolves.

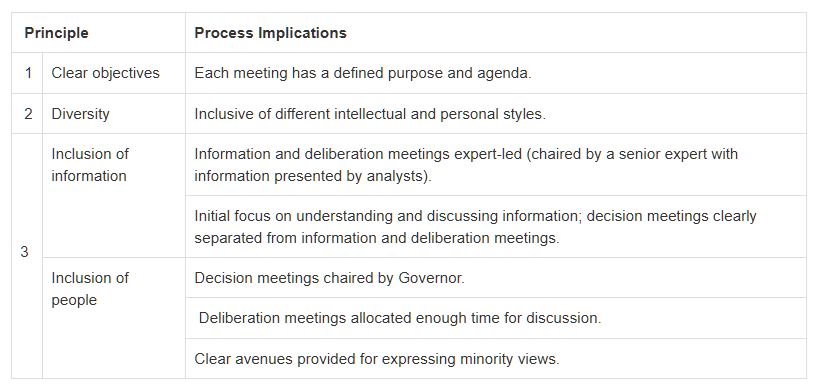

Principles

The first part of the Handbook I would like to cover is the section on MPC deliberation principles. 8

Figure 2: MPC deliberation principles

There are three principles which guide the deliberations within the MPC.

I’ve talked already about providing clarity around our objectives –

the equal weighting of our employment and inflation goals. This is the

first of our three principles.

The second, is diversity – diversity in the skills, experiences, thoughts, and personal characteristics of the MPC members.

The third, is inclusion – inclusion of information and people, ensuring decisions are made on the basis of all the available insights, and reflecting the views of all of the committee members.

Why are diversity and inclusion so important?

The governance literature shows that diversity and inclusion improves

the pool of committee knowledge, insures against extreme views, and

reduces groupthink.9 These principles drive the committee towards an unbiased policy decision – the best that is possible given existing information.

Think about this from a practical perspective. Modern monetary policy

is confronted by diverse issues such as climate, technological, and

other structural and social changes. A sole decision maker or uniform

committee cannot possibly hope to possess the broad range of insights

necessary to consider these issues.

A diverse committee operating in an inclusive environment can. It is

these additional insights that improve collective understanding, and

lead to better monetary policy decisions.

So you see these principles are not simply rhetorical devices. They

are carefully chosen pillars to support our credibility though good

decision making in achieving our dual mandate.

Good decision making

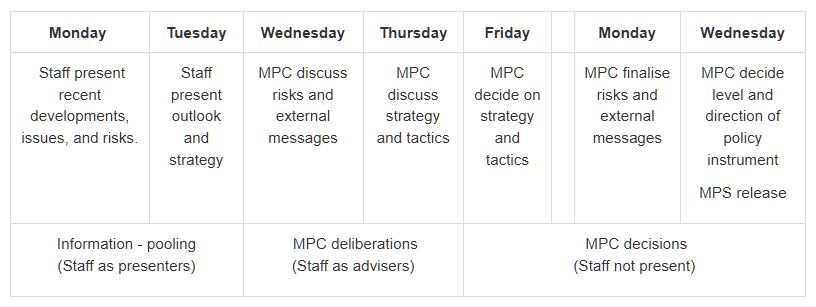

Processes

Our principles of good governance have directly influenced the policy-setting process of the MPC. 10

This is a process that has been designed with consensus-based decision

making front and centre, consistent with the agreement with the Minister

of Finance. 11

Figure 3: The structure of the forecast week for quarterly Monetary Policy Statements

We begin with information pooling, which flows through to MPC

deliberations, and culminates in the final decision making meeting.

As you can see, the policy-setting framework is highly collaborative

and deliberate. Deliberate in the sense that the process inspires lively

debate, giving MPC members every possible chance to challenge

assumptions, critique policy judgements and assess a range of policy

strategies to achieve our dual mandate objectives.

A crucial part of this is that the MPC members hold back their views

on the decision until the final stages, rather than starting with them.

This supports evidence-based decision making and guards against

confirmation bias.

The process begins with open information pooling on recent

developments and the outlook for the economy. Here, the MPC have the

opportunity to investigate and challenge the assumptions made in the

staff’s initial forecasts. This is where the MPC member’s judgement

enters the picture, and where creative tensions improve collective

understanding.

While the MPC members may enter the room with different insights and

questions about the economy, at the end of the information pooling stage

the committee shares a common reference point for the economic outlook.

There are numerous opportunities to discuss and reflect on key

issues, judgements, risks, strategy, and communication throughout the

week. There are also a number of anonymous internal surveys we perform

to gauge collective opinion among staff and MPC members.12

By the end of the week-and-a-half, the final monetary policy decision reflects the greater momentum of the MPC’s discussion.

We publish the final Official Cash Rate (OCR) decision, a Monetary Policy Statement (MPS), and a Summary Record of Meeting at the same time.

The Summary Record of Meeting captures the key judgements

and risks underpinning the central forecasts and decision, as well as

indicating where members of the MPC had different views. We identify any

differing views, and communicate where the most significant

uncertainties lie in our baseline forecasts.13

If consensus cannot be reached, a vote by simple majority would be

carried out, and the reasoning behind different stances disclosed in the

Summary Record of Meeting.

Our desire is that the transparency provided in the Handbook can help

the public understand how the Bank’s collective ‘mind’ works. If the

public can see the analytical rigour in our decision making, they should

have greater confidence in the MPC’s conclusions, and thus more faith

in the Reserve Bank.

Our credibility will be supported in the long run if the decisions

made by the MPC are unbiased and effective ones. Our results will speak

louder than our words.

Monetary policy strategy and our May decision

So far I’ve talked about the principles and processes we follow in

setting policy. Now I’m going to cover how we ‘walk the talk’ in

formulating our monetary policy decisions.14

Sound and effective monetary policy strategy requires more than just

deciding whether the OCR should go up or down on any given day; instead

central banks need to be transparent about their views of the economy

over the medium-term and how monetary policy might respond to a changing

economic landscape.

In this regard, around twenty years ago, the Reserve Bank became a

pioneer in another way. When publishing our interest rate decisions, we

also began to publish a forward (and endogenous) projection of interest

rates in the future. We use this to capture the overall stance of

monetary policy.

This tool remains integral to how the MPC sets monetary policy and understands the potential trade-offs with a dual mandate.

The first monetary policy decision of the new MPC occurred last

month, in May. Our starting point was a New Zealand economy where the

labour market was operating near maximum sustainable employment, and

annual core inflation pressures were within our 1 to 3 percent target

range but below the 2 percent mid-point.

We discussed the slowdown in global growth, and how this might affect

New Zealand. We also addressed the recent loss of domestic economy

momentum since mid-2018, through both tempered household spending and

restrained business investment.

In order to continue achieving our policy objectives, we agreed that

additional monetary stimulus was needed to help bring inflation back to

the 2 percent mid-point and support maximum sustainable employment. We

then turned to the question of the magnitude of stimulus we wanted to

adopt (the stance) and the timing and means by which we would try to

deliver this (the tactics).

Figures 4–6 show how different OCR paths could have been used to

achieve our objectives. While each path was consistent with meeting our

objectives, they each offered different trade-offs.15

Figure 4: Official Cash Rate (OCR) paths to achieve alternative monetary policy stances

Figures 5-6: Inflation, and employment gap under alternative OCR paths

If we kept rates unchanged (the higher OCR path), our projections

suggested that it would have taken a number of years for inflation to

return to target, and employment would have fallen below the maximum

sustainable level.

If we lowered the OCR by around 75 basis points over the next 12 months

(the lower OCR path), our projections suggested it would result is a

situation where both inflation and employment would be overshooting

their targets.

By contrast, the baseline (our final published projection), with the

OCR around 40 basis points lower over the next 12 months, brought

inflation back to target in a reasonable time period, with employment

remaining near the maximum sustainable level. We decided this path

captured our preferred strategy, and was robust to the key risks we had

discussed.

After agreeing on the appropriate stance of monetary policy, MPC

turned to the tactical decision of where to set the OCR at the May

meeting, and decided to cut the OCR by 25 basis points to provide a more

balanced outlook for interest rates.

This brings us to discuss the future.

Maintaining credibility in the future

Our central view is that New Zealand’s interest rates will remain

broadly around current levels for the foreseeable future. However, we

need to be ready to adapt to changing conditions, to meet our objectives

even when confronted with unforeseen developments.

An issue that policymakers and academics are grappling with around

the world is the role of both monetary and fiscal stimulus in a world of

low interest rates.

There is emerging consensus that coordination is necessary for an optimal response of broader macroeconomic policy.16 For central banks, operational independence does not have to mean operational isolation.

Rather, collaboration with government can be done in a way that builds

and reinforces the social licence to operate, by showing a willingness

to work with other partners to do whatever is necessary to achieve the

broader objective—improving public wellbeing.

Even with coordination between monetary and fiscal policy, if further

macroeconomic stimulus is needed quickly, the first line of defence

will still inevitably fall upon central banks.17

In New Zealand, we are in the strong position of having further room to provide conventional monetary stimulus if required (using the OCR).

Having effective unconventional policy options expands the

toolbox of a central bank, which is naturally more relevant in a low

interest rate environment. In this spirit, we published a Bulletin article last year on the practicalities of unconventional monetary tools in a New Zealand context, and we continue to learn from the lessons of our central banking cousins.18

It’s better to have a tool and not need it, than need one and not have it.

Conclusion

In the Handbook, we explore the history of central banking objectives, and see how dramatically they have evolved over time. 19

We haven’t always had a mandate to support maximum sustainable

employment, or to achieve price stability, or even control over interest

rates or the money supply.

Nothing lasts forever, and it is possible that the role of central

banks may change again in the future. Our Handbook will inevitably

change. We need to be ready to adapt when changes beckon.

And it is not enough to grudgingly adapt. In order to

maintain credibility, central banks must embrace change and prove to the

public that they are capable of delivering on their objectives. To

remain credible is to remain relevant. Central banks should keep their

eyes open, and be ready to change tack. Our destination—a world with

improved wellbeing for our citizens—may not change, but the best route

for getting there may.

We must adapt. We must continue to improve the wellbeing of our citizens. We must remain credible.

Property expect Joe Wilkes and I discuss the latest New Zealand data,

and consider the drive to attract first time buyers in both NZ and

Australia. What does the data say?

Property expect Joe Wilkes and I discuss the latest New Zealand data, and consider the drive to attract first time buyers in both NZ and Australia. What does the data say?

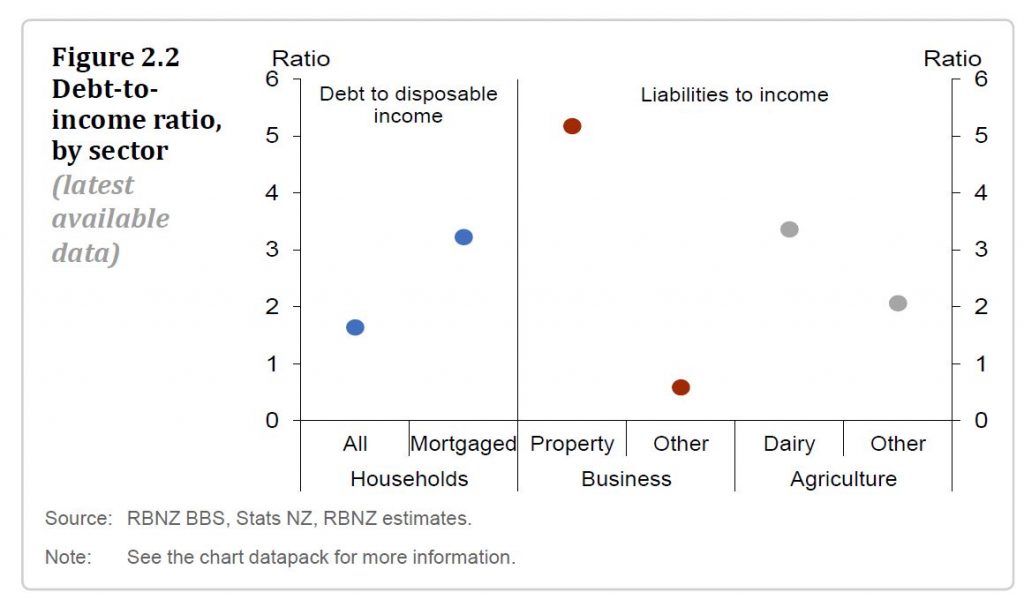

The New Zealand financial system remains resilient to a broad range of economic risks. However, financial system risks remain elevated, and ongoing effort is necessary to bolster system soundness and efficiency.

Domestically,

debt levels are high in the household and dairy sectors, leaving borrowers and

lenders exposed to unanticipated events. Similar challenges exist globally,

given current high public and private debt levels, and stretched asset prices

in many of New Zealand’s trading partners.

Some regions have recently had high house price growth. This is not an immediate financial stability concern as those regions have smaller and less stretched housing markets than Auckland. But if strong price growth continued, the financial system would become more exposed to those regions. The Global Financial Crisis (GFC) showed that house prices can fall dramatically in small regions.

At a national level, the growth of household debt and house prices has slowed, but household debt has still grown faster than income in the past year. Housing market pressures could re-emerge if there is a strong response to the recent decline in mortgage rates, or reduced uncertainty about the future tax treatment of property investments.

Given this environment, the financial system’s vulnerability to risks in the household sector remains elevated, and must continue to be closely monitored and managed.

The capacity for some foreign governments and central banks to respond to unanticipated negative events is also limited by their current high government debt and low nominal interest rates. It is imperative to improve New Zealand’s financial system resilience while conditions are conducive.

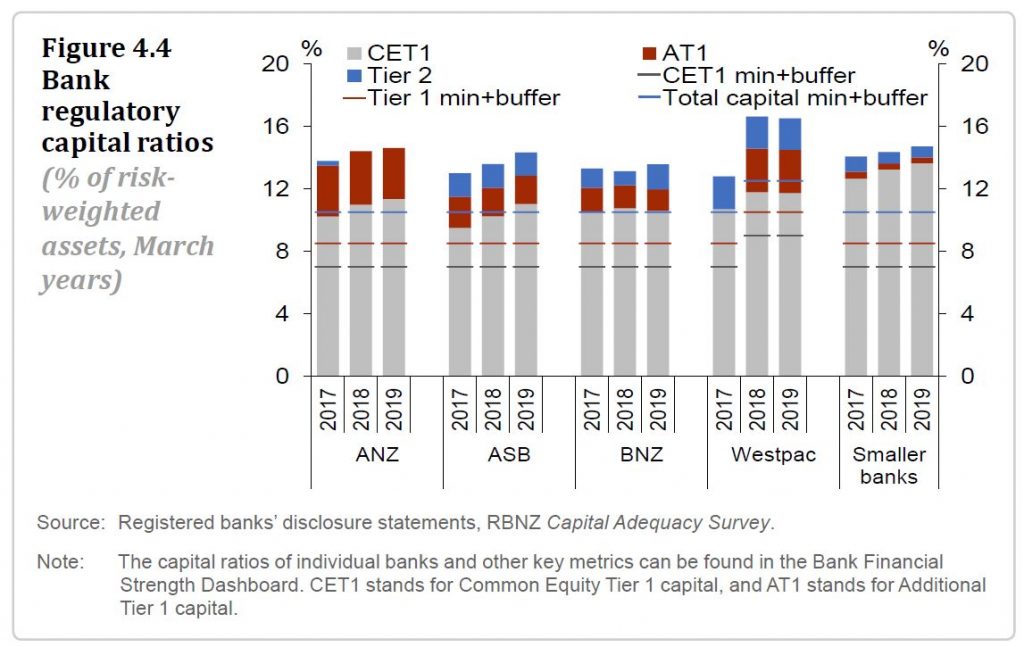

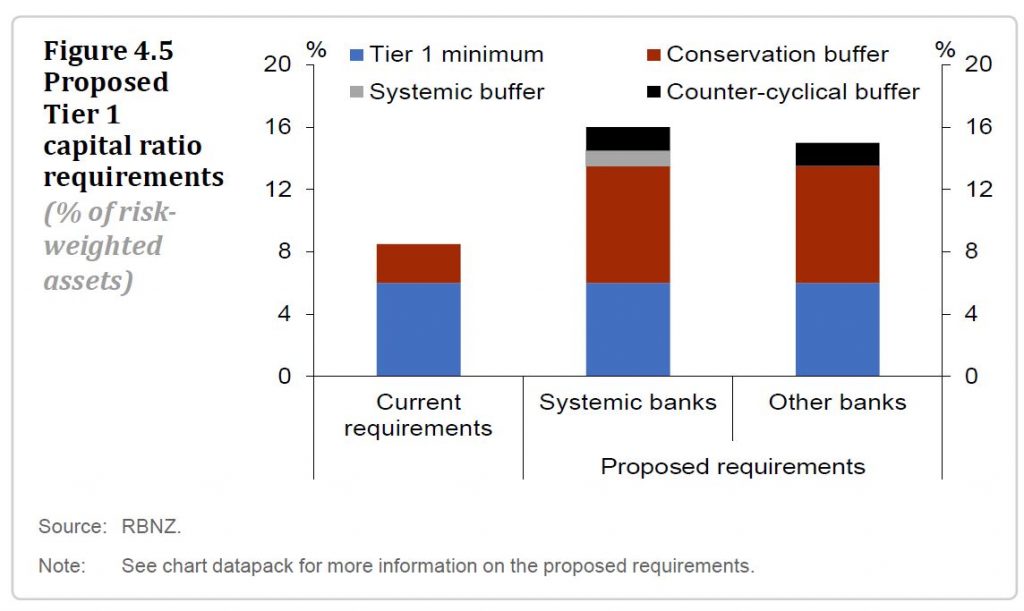

Increasing financial institutions’ capital positions is central to ensuring that they can withstand severe shocks. We have proposed higher capital requirements for banks, and are currently reviewing public submissions on this proposal.

There is also a need for some insurers and non-bank deposit takers to improve their capital buffers. We will be reviewing insurer solvency standards in the months ahead.

Financial

resilience also includes service providers taking a long-term customer outcome

focus, to both maintain confidence and promote sound resource allocation. We

will ensure banks and insurers respond to the issues identified in our recent

review of their conduct and culture.

A longer-term

focus is also necessary for financial firms to adapt to the changing

competitive, regulatory, and natural environment.

Insurers are changing how they manage their exposure to natural disaster events, which is altering affordability. Risks associated with climate change are also impacting on the accessibility of insurance, with potential flow-on effects on bank lending. These risks must be appropriately identified and priced, so as to best ensure a stable transition over coming years.

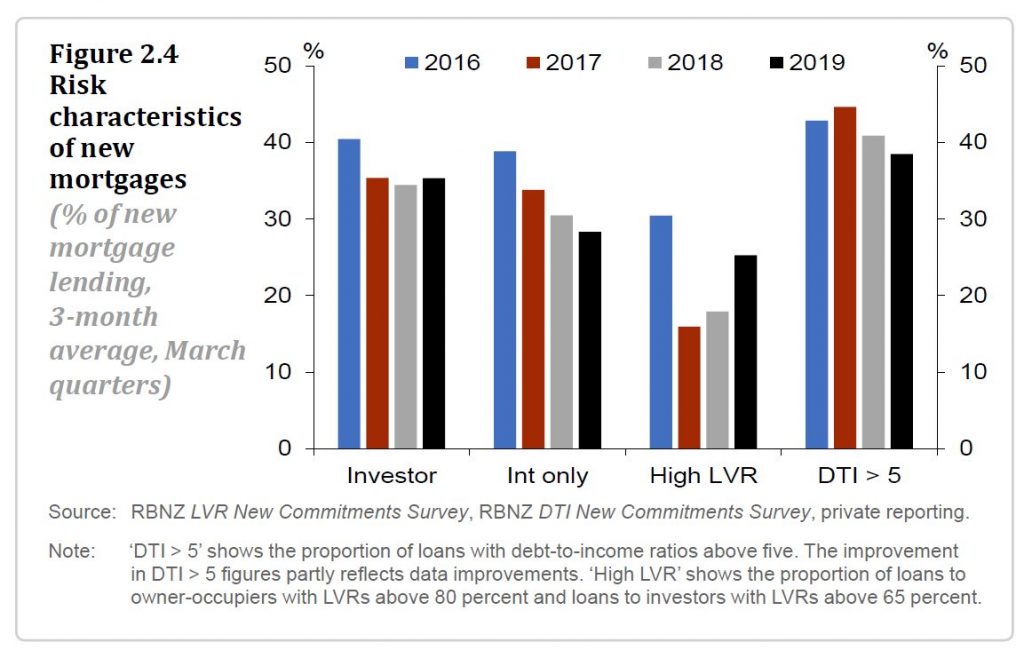

The Reserve Bank’s loan-to-value ratio (LVR) restrictions have been successful in reducing some of the risk associated with high household indebtedness. The current LVR settings remain appropriate for now, with any further easing subject to continuing subdued growth in credit and house prices and banks maintaining prudent lending standards.

The New Zealand Reserve Bank has today announced the next steps in its Capital Review, following the closing of written submissions on Friday last week. An announcement is planned by the end of November, with implementation of any new rules starting from April next year.

The review

proposes changes to regulatory capital requirements for locally incorporated

banks. These include requiring bank shareholders to increase their stake

so that they absorb a greater share of losses should their bank fail, and

ensuring banks more accurately calculate how much capital they have.

Deputy Governor

Geoff Bascand says he is encouraged by the number of, and the effort put into,

submissions received on the proposals to make New Zealand’s banking system

safer.

“It is

important that the public understands how higher levels of capital better

protect their deposits. It is pleasing to see stakeholders’ interest in the

proposals reflected in the 164 responses received as well as in feedback

received through our briefings with banks, industry bodies, investors, the news

media, and social sector groups.

“The proposals

are consistent with steps taken by other banking regulators after the Global

Financial Crisis. There is increasing evidence that the costs of bank failures

– both economic and well-being costs – are higher than previously understood.”

The submissions

will now be collated and published along with a summary in June. The Reserve

Bank will continue its stakeholder outreach programme, which includes

conducting focus groups to understand how New Zealanders feel about risks in

our financial system, how these risks could affect them, and how the risks

should be managed.

An important

part of the consultation process involves seeking relevant information from

industry and broader stakeholders to better understand costs and benefits, Mr

Bascand says.

“The proposals

were designed around a net benefits framework, where more capital was required

up to the point that financial stability gains were matched by increases in

costs.

“Our policy

development process is to develop policy options, lay out our thinking on the

nature of the costs and benefits of the policy being consulted on, seek input

from affected parties, and produce a full cost benefit around any modified

proposals before making final policy decisions.”

The Reserve

Bank is also in the process of appointing external experts to independently

review the analysis and advice underpinning the proposals. Their reports will

be part of the suite of information considered in the final decision-making

process of the review.

An announcement is planned by the end of November, with implementation of any new rules starting from April next year. There will be a transition period of a number of years before banks are required to fully comply with any new rules.

The review

began more than two years ago, when the Reserve Bank published an issues paper

and opened the first of four public consultations.

The Official Cash Rate (OCR) has been reduced to 1.5 percent. They signalled risks from China and Australia, and that lower mortgage rates might help household finances and housing.

The Monetary Policy

Committee decided a lower OCR is necessary to support the outlook for

employment and inflation consistent with its policy remit.

Global economic growth

has slowed since mid-2018, easing demand for New Zealand’s goods and services.

This lower global growth has prompted foreign central banks to ease their

monetary policy stances, supporting growth prospects.

However, there is

uncertainty about the global economic outlook. Trade concerns remain, while

some other indicators suggest trading-partner growth is stabilising.

Domestic growth slowed

from the second half of 2018. Reduced population growth through lower net

immigration, and continuing house price softness in some areas, has tempered

the growth in household spending. Ongoing low business sentiment, tighter

profit margins, and competition for resources has restrained investment.

Employment is near its

maximum sustainable level. However, the outlook for employment growth is more

subdued and capacity pressure is expected to ease slightly in 2019.

Consequently, inflationary pressure is projected to rise only slowly.

Given this employment

and inflation outlook, a lower OCR now is most consistent with achieving our

objectives and provides a more balanced outlook for interest rates.

Summary record of meeting – May 2019 Statement

The Monetary Policy Committee agreed on the economic

projections outlined in the May 2019 Statement in order to provide a

sound basis on which to form its OCR decision.

The Committee noted that inflation is currently

slightly below the mid-point of the inflation target, and that employment is

broadly at the targeted maximum sustainable level. However, the members agreed

that given the recent weaker domestic spending, and projected ongoing growth

and employment headwinds, there was a need for further monetary stimulus to

meet its objectives.

The Committee agreed that the risks to achieving its

consumer price inflation and maximum sustainable employment objectives were

broadly balanced around the projection. Possible alternative outcomes were

noted on the upside and downside.

A key downside risk relating to the growth projections was a larger than anticipated slowdown in global economic growth, particularly in China and Australia, New Zealand’s largest trading partners. The Committee agreed that the projections adequately captured the observed global slowdown and its impact on domestic employment and inflation.

The Committee noted that additional stimulus from

central banks had underpinned growth and reduced the likelihood of a

more-pronounced slowdown. With some indicators of global growth improving in

recent months, a faster recovery in global growth was possible. However, on

balance, the Committee was more concerned about a continued slowdown rather than

a faster recovery.

The Committee discussed other potential risks to

domestic spending. The members acknowledged the importance of additional

spending from households, businesses, and the government, to meet their

inflation and employment targets. However, they noted several important

uncertainties.

The Committee noted upside and downside risks to the

investment outlook. Capacity pressure could see investment increase faster than

assumed. On the downside, if sentiment remained low as profitability remains

squeezed, investment might not increase as anticipated over the medium term. It

was also noted that firms’ ability to invest is constrained by the current

competition for resources.

A potential source of additional demand discussed by

the Committee included government spending being higher than currently

projected, in view of the current strength of the Crown balance sheet. This

view was balanced by the impact of any increase in government investment being

delayed, for example due to timing of the implementation of new initiatives and

current capacity constraints in the construction sector. The implications for

monetary policy remain to be seen.

Some members noted that with lower mortgage rates and easing of loan-to-value requirements, any possible pick-up in the housing market could support household spending growth more than anticipated.

The Committee noted that employment is currently near

its maximum sustainable level. However, it was agreed that the outlook for

employment growth is more subdued and capacity pressure is expected to ease

slightly in 2019.

The Committee agreed that overall risks to the

inflation projection were balanced. The Committee noted the outlook for

inflation is below the target mid-point for longer than projected in the February

Statement.

The recent period of rising domestic inflation was

discussed. The Committee noted that the near-term outlook was more subdued due

to lower capacity pressure. It was also noted that cost pressures remain

elevated, and that there is a risk firms may pass these costs on as higher

consumer prices by more than assumed. However, it was agreed that inflation

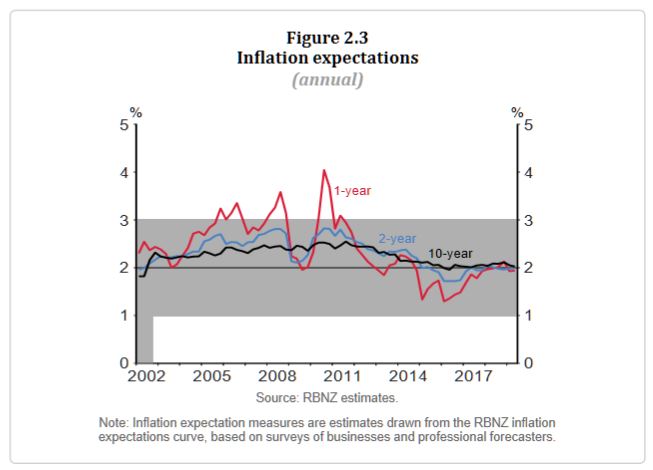

expectations remain well anchored at the mid-point of the target range.

The Committee also noted the relatively subdued

private sector wage growth, despite businesses suggesting that the inability to

find labour is a significant constraint on their growth. The Committee noted

the limited pass-through of the nominal wage growth to consumer price

inflation.

Some members noted slower global growth reducing

imported inflation was a downside risk to the inflation outlook.

The Committee reached a consensus that, relative to

the February Statement, a lower path for the OCR over the projection

period was appropriate. The lower path reflected the economic projections and

the balance of risks discussed, and is consistent with both inflation and

employment remaining near the Committee’s objectives.

After discussing the relative benefits of holding the

OCR and committing to a downward bias, versus cutting the OCR now so as to

establish a more balanced outlook for interest rates, the Committee reached a

consensus to cut the OCR to 1.50 percent.

Blog")