The Productivity Commission (PC) had posed the question in its draft report into competition in the Australian financial system of whether consumers should pay service fees, with the aim of finding out if such a model would ensure consumer interests are being served without any conflicting commercial influence.

In a public hearing on Wednesday (28 February), Travis Crouch, divisional CFO for revenue at Bendigo and Adelaide Bank, contended that a “fee-for-service brokerage [would] remove the inherent conflicts involved in a commission-based structure and ensure fees earned are aligned with the value of the service provider”.

The representative explained that the bank relies less on mortgage brokers than other banks, as its primary focus for the last two decades has been on developing a strong branch network.

“We have been focused on the development of a strong branch network primarily since the advent of our community banking model, some 20 years ago, where communities can open a branch of a Bendigo Bank as a franchisee. That remains a reverse enquiry model… We’re not out there selling to a community that you should open a community bank; rather, [the] community comes to us and [says], ‘We would like to open a branch’,” Mr Crouch told the PC in the hearing.

“There is a significant process including feasibility studies [that] they need to go through to show that they could be successful. But we continue to increase our branch footprint primarily through that community bank model.”

Mr Crouch further explained the difference between the organisation’s Adelaide Bank and Bendigo Bank brands, saying: “Our brand that we use in the broker market is the Adelaide Bank brand. The Bendigo Bank brand is our retail offering through our retail and community bank network. The Adelaide Bank brand is effectively an online brand once you take out the mortgage through a mortgage broker.”

Trail “an absurd option”

In response, a PC representative commented that if Adelaide Bank is ultimately an online brand, paying trail commissions must be an “absurd option”.

“For the average loan, $665 per year in perpetuity for an online-based product seems very expensive,” the PC said.

“You presumably have very little choice about that because, as you say, you have to play in the market.”

The Bendigo and Adelaide Bank representative agreed with the comment, drawing back to why the bank believes that a fee-for-service model is “more appropriate”.

Mr Crouch did not, however, deny the importance of brokers, saying that it would be a “brave decision to not participate in that market”, given that “roughly half of Australians [are] choosing to select a mortgage by going to a broker”.

When asked about whether the bank has had to make “either/or” decisions around opening branches in the same location as brokerages, Mr Crouch noted that it has separate strategies for its retail and broker businesses.

“The reality is both are generally competing in the same market, whether that be a geographic market or anything else, and quite often you’ll find one of our branches in the same shopping strip as an outlet of a major broker. So, it is not an either/or in our organisation,” the CFO explained.

“I can’t think of a time when we made a decision around our branch network based on ‘should we actually use a third party in that particular space’.”

While the bank is in support of consumers paying service fees to brokers, its representative acknowledged that “such a change will have significant and varied implications, which will need to be carefully considered before such a change is implemented”.

The proposed monetisation model has been met with criticism from the aggregator and broker community, with Connective director Mark Haron previously telling The Adviser that if brokers charged a fee for service, the Australian broker population would decline significantly, which, in turn, would negatively impact the non-major banks and non-banks that depend on brokers for business. It was his contention that such a model would decrease competition in the Australian financial system.

The major banks — which already control more than 80 per cent of all owner-occupied housing loans and 85 per cent of investor housing loans, according to the Australian Prudential Regulation Authority — would therefore gain additional market share if consumers chose to go directly to banks for their loans in order to avoid paying broker fees, Mr Haron said.

The Connective director also warned that a fee-for-service model could make financial advice less accessible to customers who need it the most, such as first home buyers, and further noted that, by managing home loan applications, brokers actually reduce the workload for banks.

“[Brokers are doing] the work that the banks would have to do themselves, so it’s only fair that the brokers get remunerated by the banks,” the director said.

The chairman of the Productivity Commission has said that while it may be in the interests of the bank and the broker to limit churn, it is not in the interests of the borrower.

Speaking at the Committee for Economic Development of Australia (CEDA) in Melbourne on Monday, Productivity Commission chairman Peter Harris reiterated some of the questions raised in the commission’s draft report into competition in the Australian financial system, which scrutinised broker remuneration and the purpose of trail commissions.

The PC is also questioning whether consumers should pay brokers a fee for service.

Speaking on Monday, Mr Harris said: “Despite some recently announced industry changes to parts of the commission payment structure, commission earned by brokers remains far from aligned with the interests of the customer.

“Trailing commissions are an example of that. These are only paid while a customer remains with a loan. They are worth $1 billion per annum. There is nothing immaterial about them.

“The industry itself has said that trailing commissions are designed to reduce churn and manage customers on behalf of banks.

“Despite the hint to the contrary, we do actually understand quite well why it might be in a bank’s interest and a broker’s interest to jointly limit churn.

“But not the customer’s interest, who (the data is surprisingly unavailable, as noted earlier) is most probably paying for the service.”

He continued: “Given the unhappy experience with misaligned incentives in wealth management, being able to substantiate the assurance that a broker is acting in the customer’s best interest would seem to be pretty desirable today.”

He said that the commission would “prefer” that banks imposed this interest via contract rather than have the standard introduced via regulation. (However, the commission’s chairman added that as the commission has no power to recommend what banks do, it has instead proposed regulation in the draft report.)

“It would have been valuable to put the cost-benefit side by side”

Once again, the chair highlighted a data gap in the industry, stating that he believes the “default position among data holders in this industry is set against transparency”.

“[W]e were genuinely surprised to find that they either do not hold data at all on some important aspects of decision making, or for another reason could not supply them,” Mr Harris said, stating that “the cost of mortgage brokers is quite high”.

Mr Harris added that brokers cost $2,300 for the average loan of $369,000, plus a trailing commission of $665.

He said: “Other analysts have suggested higher numbers than these in high-priced locations, but we will stick with national averages.

“More than $2.4 billion is now paid annually for these services. Some in the broking industry want to know why there is suddenly attention being paid to commissions.

“The sum I just cited, as a large apparent addition to industry costs since the mid ’90s, by itself suggests a public analysis of why it is so large might be in order.”

He argued that the $2.4 billion figure “becomes problematic when it is also suggested that customers aren’t burdened by this as they don’t pay these costs”, adding that “anyone with a slight amount of common sense knows that somewhere in any product purchase it is only a customer or a shareholder who could be paying this charge, unless offsetting costs have been stripped out”.

Mr Harris continued: “Shareholders returns are pretty constant, so we would have liked to unpack that cost question a little, to see if the price was supported by cost savings. With the data provided by banks, this proved to be near impossible.

“For smaller banks, we were able to develop some estimates of the branch costs they would potentially face, without broker assistance. But we received insufficient information from most (not all) banks, and so could not create a clear picture.

“Thus, we can’t say whether there has been a net improvement in efficiency, even as a large sum in commissions has been added to industry costs. We have also shown in the report that brokers do produce slightly better rates for their clients than going in to the bank branch. But that benefit for consumers has been declining since the GFC. It would have been valuable to put the cost-benefit side by side.”

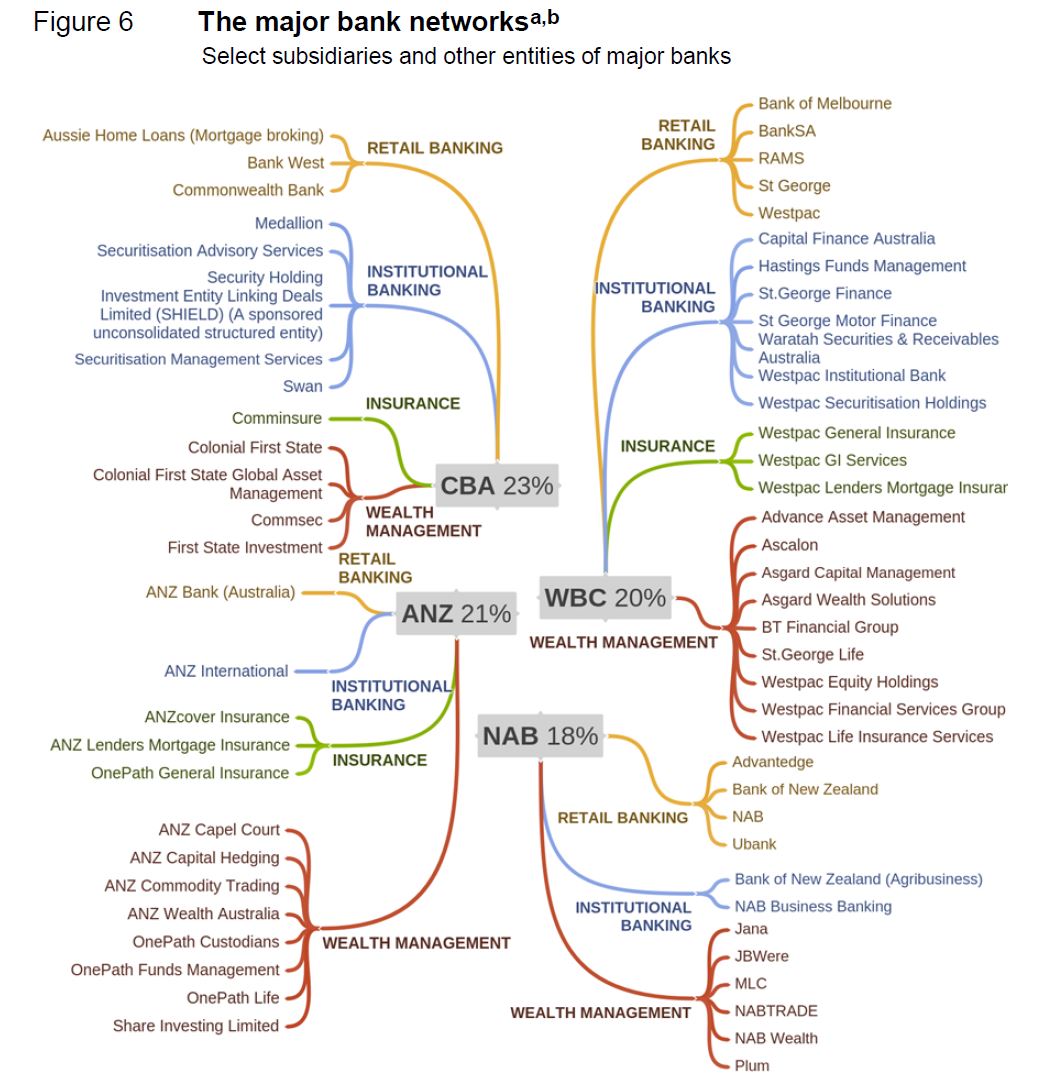

Mr Harris also took aim at vertical integration, suggesting that bank-owned aggregators control about 70 per cent of the mortgage broking market.

He added that in-house products or white label loans appear to “dominate disproportionately” the outcomes for borrowers who use bank-owned aggregators.

The PC chair noted that, in 2015, the Commonwealth Bank had 21 per cent overall market share in the broker channel but a 37 per cent market share via Aussie Home Loans.

However, while it has concerns about vertically integrated groups, the Productivity Commission said that forcing banks to divest of their broking businesses should be “a last resort”.

“Of course, if the necessary solutions prove commercially unpalatable, institutions themselves may then choose to divest,” Mr Harris said.

Many in the industry have spoken out against the Productivity Commission’s draft report, with some suggesting that the remuneration figures cited are “incorrect”, others stating that the recommendation to charge fees would be “anti-competitive”, and both broker associations calling out some findings of the report (which relied heavily on figures from CHOICE consumer group and UBS reports) as “limited”, “amateur” and — in some cases — “nonsense”.

Productivity Commission chairman Peter Harris defended his agency’s criticism of broker commission in its report on competition in financial services, as he highlighted again the high cost of mortgage brokers.

Speaking at a Committee for the Economic Development of Australia event yesterday, Harris said more than $2.4bn is now paid annually for mortgage broker services.

The commission’s draft report released in early February says that based on ASIC’s findings, lenders pay brokers an upfront commission of $2,289 (0.62%) and a trail commission of $665 (0.18%) a year on an average new home loan of $369,000.

“Some in the broking industry want to know why there is suddenly attention being paid to commissions. The sum I just cited, as a large apparent addition to industry costs since the mid-90s, by itself suggests a public analysis of why it is so large might be in order.”

Harris said the amount becomes problematic when some parties suggest that consumers do not bear this burden as they do not pay commission costs.

“Which is a comment surely made for Twitter – since anyone with a slight amount of common sense knows that somewhere in any product purchase, it is only a customer or a shareholder who could be paying this charge, unless offsetting costs have been stripped out,” he said.

Harris also cast doubt on industry changes to broker remuneration structures. He said that despite announced changes to parts of commission payment schemes, broker commission remains far from aligned with consumer interests.

He zeroed in on trailing commissions – which he said are worth $1bn per annum – and questioned their relevance.

“The industry itself has said that trailing commissions are designed to reduce churn and manage customers on behalf of banks. Despite the hint to the contrary, we do actually understand quite well why it might be in a bank’s interest and a broker’s interest to jointly limit churn,” said Harris.

“But not the customer’s interest – who is most probably paying for the service.”

Harris said the Productivity Commission preferred that banks imposed on brokers the duty of ensuring they act in consumers’ best interests, “perhaps via contract”.

“But we have no power to recommend what banks do for themselves, so we have instead a draft report that proposes regulation,” he said.

The commission is moving into the public hearing stage this week, and will submit its final report on 1 July.

Recent events have the potential to create a revolution in Australian Finance. We explore the 72 hours that changed banking forever.

Welcome to the Property Imperative Weekly to 10th February 2018.Watch the video or read the transcript.

In our latest weekly digest, we start with the batch of new reports, all initiated by the current Australian Government – and which combined have the potential to shake up the Financial Services sector, and reduce the excessive market power which the four major incumbents have enjoyed for years.

On Wednesday, the Productivity Commission, Australian Government’s independent research and advisory body released its draft report into Competition in the Australian Financial System. It’s a Doozy, and if the final report, after consultation takes a similar track it could fundamentally change the landscape in Australia. They leave no stone unturned, and yes, customers are at a significant disadvantage. Big Banks, Regulators and Government all cop it, and rightly so. They say, Australia’s financial system is without a champion among the existing regulators — no agency is tasked with overseeing and promoting competition in the financial system. It has also found that competition is weakest in markets for small business credit, lenders’ mortgage insurance, consumer credit insurance and pet insurance. The report demonstrates the inter-linkages between difference financial entities, and their links to the four majors. They criticised mortgage brokers and financial advisers for poor advice (influenced by commission and ownership structures) and the regulatory environment, where the shadowy Council of Finance Regulators (RBA, ASIC, APRA and Treasury) do not even release minutes of the meetings which set policy direction. You can watch our separate video blog on this.

On Thursday, the Treasurer released draft legislation to require the big four banks to participate fully in the credit reporting system by 1 July 2018. They say this measure will give lenders access to a deeper, richer set of data enabling them to better assess a borrower’s true credit position and their ability to pay a loan. This removes the current strategic advantage which the majors have thanks to the credit data asymmetry, and the current negative reporting. We note that there is no explicit consumer protection in this bill, relating to potential inaccuracies of data going into a credit record. This is, in our view a significant gap, especially as the proposed bulk uploading will require large volumes of data to be transferred. It does however smaller lenders to access information which up to now they could not, so creating a more level playing field. Consumers may benefit, but they should also beware of the implications of the proposals.

On Friday, Treasurer Morrison released the report by King & Wood Mallesons partner Scott Farrell in to open banking which aims to give consumers greater access to, and control over, their data and which mirrors developments in the UK. This “open banking” regime mean that customers, including small businesses, can opt to instruct their bank to send data to a competitor, so it can be used to price or offer an alternative product or service. Great news for smaller players and fintechs, and possibly for customers too. Bad news for the major players. The report recommends that the open banking regime should apply to all banks, though with the major banks to join it first. For non-banks and fintechs, the report wants a “graduated, risk-based accreditation standard”. Superannuation funds and insurers are not included for now. In terms of implementation, data holders should be required to allow customers to share information with eligible parties via a dedicated application programming interface, not screen scraping. A period of approximately 12 months between the announcement of a final Government decision on Open Banking and the Commencement Date should be allowed for implementation. From the Commencement Date, the four major Australian banks should be obliged to comply with a direction to share data under Open Banking. The remaining Authorised Deposit-taking Institutions should be obliged to share data from 12 months after the Commencement Date, unless the ACCC determines that a later date is more appropriate.

Then of course the Royal Commission in Financial Services starts this coming week. We discussed this on ABC The Business on Thursday. Lending Practice is on the agenda, highly relevant given the new UBS research (they of liar loans) suggesting that incomes of many more affluent households are significantly overstated on mortgage application forms. And The BEAR – the bank executive behaviour regime legalisation – passed the Senate, and as a result of amendments, Small and medium banking institutions have until 1 July 2019 to prepare for the BEAR while it will commence for the major banks on 1 July 2018.

APRA Chairman Wayne Byers spoke at the A50 Australian Economic Forum, Sydney. Significantly, he says the temporary measures taken to address too-free mortgage lending will morph into the more permanent focus on among other things, further strengthening of borrower serviceability assessments by lenders, strengthened capital requirements for mortgage lending, and the comprehensive credit reporting being mandated by the Government.

Adelaide Bank is ahead of the curve, as it introducing an alert system that will monitor property borrowers that are struggling with their repayments. The bank and its subsidiaries and affiliates will compare monthly mortgage repayments with borrowers’ income ratios. In addition, extra scrutiny will be applied where the loan-to-income ratio exceeds five times or monthly mortgage repayments exceed 35% of a borrower’s income.

But combined, data sharing, positive credit and banking competition and regulation are all up in the air, or are already coming into force and in each case it appears the big four incumbents are the losers, as they are forced to share customer data, and competition begins to put their excessive profitability under pressure. It highlights the dominance which our big banks have had in recent years, and the range of reforms which are in train. The face of Australian Banking is set to change, and we think customers will benefit. But wait for the rear-guard actions and heavy lobbying which will take place ahead.

Of course the RBA left the cash rate on hold this week, and signalled the next move will likely be up, but not for some time. Retail turnover for December fell 0.5% according to the ABS seasonally adjusted. This is the headline which will get all the coverage, but the trend estimate rose 0.2 per cent in December 2017 following a rise of 0.2 per cent in November 2017. Compared to December 2016 the trend estimate rose 2.0 per cent. This is in line with average income growth, but not good news for retailers.

The latest Housing Finance Data from the ABS shows a fall in flows in December. In trend terms, the total value of dwelling finance commitments excluding alterations and additions fell 0.1% or $31 million. Owner occupied housing commitments rose 0.1% while investment housing commitments fell 0.5%. Owner occupied flows were worth $14.8 billion, and down 0.3% last month, while owner occupied refinancing was $6.2 billion, up 1.2% or $73 million. Investment flows were worth 11.9 billion, and fell 0.5% or $62 million. The percentage of loans for investment, excluding refinancing was 45%, down from 49% in Dec 2016. Refinancing was 29.5% of OO transactions, up from 29.2% last month. Momentum fell in NSW and VIC, the two major states. In original terms, the number of first home buyer commitments as a percentage of total owner occupied housing finance commitments fell to 17.9% in December 2017 from 18.0% in November 2017 – the number of transactions fell by 1,300 compared with last month. But the ABS warns that the First Time Buyer data may be revised and users should take care when interpreting recent ABS first home buyer statistics. The ABS plans to release a new publication which will see Housing Finance, Australia (5609.0) and Lending Finance, Australia (5671.0) combined into a single, simpler publication called Lending to Households and Businesses, Australia (5601.0).

We continue to have data issues with mortgage lending, with the RBA in their new Statement on Monetary Policy saying it now appears unnecessary to adjust the published growth rates to undo the effect of regular switching flows between owner occupied and investment loans as they have been doing for the past couple of years. So now investor loan growth on a 6-month basis has been restated to just 2%. More fluff in the numbers! Additionally, the RBA will publish data on aggregate switching flows to assist with the understanding of this switching behaviour.

More data this week highlighting the pressures on households. National Australia Bank’s latest Consumer Behaviour Survey, shows the degree of anxiety being caused by not only cost of living pressures but also health, job security, retirement funding as well as Australian politics. Of all the things bothering Australian households in early 2018, nothing surpasses cost of living pressures. Over 50% of low income earners reported some form of hardship, with almost one in two 18 to 49-year-olds being effected.

Despite improved job conditions and households reporting healthier financial buffers, the overall financial comfort of Australians is not advancing, according to ME’s latest Household Financial Comfort Report. In its latest survey, ME’s Household Financial Comfort Index remained stuck at 5.49 out of 10, with improvements in some measures of financial comfort linked to better employment conditions – e.g. a greater ability to maintain a lifestyle if income was lost for three months – offset by a fall in comfort with living expenses.

We released the January 2018 update of our Household Financial Confidence Index, using data from our rolling 52,000 household surveys. The news is not good, with a further fall in the composite index to 95.1, compared with 95.7 last month. This is below the neutral setting, and is the eighth consecutive monthly fall below 100. Costs of living pressures are very real, with 73% of households recording a rise, up 1.5% from last month, and only 3% a fall in their living costs. A litany of costs, from school fees, child care, fuel, electricity and rates all hit home. You can watch our separate video on this.

We also published updated data on net rental yields this week, using data from our household surveys. Gross yield is the actual rental stream to property value, net rental is rental payments less the costs of funding the mortgage, management fees and other expenses. This is calculated before any tax offsets or rebates. The latest results were featured in an AFR article. The results are pretty stark, and shows that many property investors are underwater in cash flow terms – not good when capital values are also sliding in some places. Looking at rental returns by states – Hobart and Darwin are the winners; Melbourne, and the rest of Victoria, then Sydney and the rest of NSW the losers. The returns vary between units and houses, with units doing somewhat better, and we find some significant variations at a post code level. But we found that more affluent households are doing significantly better in terms of net rental returns, compared with those in more financially pressured household groups. Batting Urban households, those who live in the urban fringe on the edge of our cities are doing the worst. This is explained by the types of properties people are buying, and their ability to select the right proposition. Running an investment property well takes skill and experience, especially in the current rising interest rate and low capital growth environment. Another reason why prospective property investors need to be careful just now.

Finally, we saw market volatility surge, as markets around the world gyrated following the “good news” on US Jobs last week, which signalled higher interest rates. In our recent video blog we discussed whether this is a blip, or something more substantive. We believe it points to structural issues which will take time to play out, so expect more uncertainly, on top of the correction which we have already had. This will put more upward pressure on interest rates, and also on bank funding here.

Overall then, a week which underscores the uncertainly across the finance sector, and households. This will not abate anytime soon, so brace for a bumpy ride. And those managing our large banks will need to adapt to a fundamentally different, more competitive landscape, so they are in for some sleepless nights.

If you found this useful, do like the post, add a comment and subscribe to receive future updates. Many thanks for taking the time to watch.

A Productivity Commission report analysing competition in the financial sector has pointed out that our finance regulators have become enablers of an industry that is an impediment to our economic competitiveness and exploitative of their most loyal customers.

It proves the need for a board to oversee the conduct of our financial regulators, policing the bodies that are supposed to be keeping our financial system in check.

It could not have come at a worse time for our big four banks. Perennially pilloried for their rampant market misconduct (fraudulently manipulating benchmark interest rates) and their equally rampant abuse of upwards of hundreds of thousands of consumers across every one of their retail operations at one stage or another – financial advice, life insurance and credit card insurance, just to name a few.

The Australian Securities and Investments Commission (ASIC) most recently launched a bank-bill swap rate manipulation case against the Commonwealth Bank, but only across a very narrow range of infringements. The bulk of the infringements can’t be prosecuted because ASIC has dithered for so long, the statute of limitations has run out, and the alleged crimes have proscribed.

And what of our other financial regulator – the Australian Prudential Regulation Authority (APRA)? The Productivity Commission reckons that APRA’s ham-fisted use of macro-prudential tools, usually used to reduce risk in our financial system, has benefited the big four banks to the tune of A$1 billion.

APRA has been criticised for pursuing stability in a manner that has killed competition, hurt consumers, and starved small businesses of life-giving capital. The dominance by a few banks, whose profits are based on runaway property prices, is its own systemic threat.

The result is that small banks are squeezed out, big banks raking in higher rates, and investors offsetting higher rates against their taxes and so costing the Australian Taxation Office an estimated A$500 million in deductions. As the old saying goes, when your only tool is a hammer, every problem looks like a nail.

Who will regulate the regulators?

So what to do about ASIC and APRA? Back in 2014, the Financial System Inquiry recommended a board of oversight – a regulator for the regulators – to ensure that the regulators discharge their mandates.

So, for example, to ensure that ASIC acts like a cop, not a co-op; that APRA acts with foresight and finesse, as opposed to damaging competition. APRA and ASIC pushed back at the time, and the Abbott government rejected the recommendation.

Now to add impetus to the Financial System Inquiry recommendation, the Productivity Commission says there is a lack of transparency and accountability exhibited by our regulators. Add to that the implications regarding regulator’s efficacy that comes with the establishment of the Financial Services Royal Commission. The public deserves better than this.

A regulator for the regulators – a Financial Regulator Assessment Board – would conduct ex post analyses of how regulators had discharged their mandates, evaluate their policies and the efficacy of their policy tools. It would be a sober second thought, and a crucial mechanism of double redundancy – to pick up on crucial elements that the regulator may have overlooked.

The idea has form. The British have created something similar, called a Financial Policy Committee, this body’s aim is to review the British regulators, while keeping a look-out for where the next “bombshell” may come from.

That development in turn builds on the work of James Barth, Gerard Caprio and Ross Levine whose research indicates that regulators simply cannot be trusted to perform these crucial functions as the guardians of finance, without oversight. The researchers call their proposed board of oversight the “Sentinel”, and point out that no industry is more adept and more practised at suborning the guardians of finance than banks and insurers. Sound familiar?

Australia’s financial system is increasingly governed by a lawless financial sector, presided over by regulators that are at best misguided, and at worst captured. A board of oversight is the least we can do.

Author: Andrew Schmulow, Senior Lecturer, Faculty of Law, University of Western Australia

The Productivity Commission, Australian Government’s independent research and advisory body has released its draft report into Competition in the Australian Financial System. It’s a Doozy, and if the final report, after consultation takes a similar track it could fundamentally change the landscape in Australia. They leave no stone upturned, and yes, customers are at a significant disadvantage. Big Banks, Regulators and Government all cop it, and rightly so.

Australia’s financial system is without a champion among the existing regulators — no agency is tasked with overseeing and promoting competition in the financial system. The Commission’s draft report into Competition in the Australian Financial System recognises that both competition and financial stability are important to the Australian financial system, and are an uncomfortable mix at times. It has also found that competition is weakest in markets for small business credit, lenders’ mortgage insurance, consumer credit insurance and pet insurance.

Here are some of the key findings.

Whilst there has been significant innovation (enabled by technology), the financial system is highly profitable and concentrated. It lacks strong pricing rivalry – and evidence that it exploits loyal customers.

It questions whether the four pillars policy is still relevant. It is an ad hoc policy that, at best, is now redundant, as it simply duplicates competition and governance protections in other laws. At worst, in this consolidation era it protects some institutions from takeover, the most direct form of market discipline for inefficiency and management failure. All new entrants to the banking system over the past decade have been foreign bank branches, usually targeting important but niche markets (and these entrants have evidenced only limited growth in market share).

Australia’s financial system is dominated by large players — four major banks dominate retail banking, four major insurers dominate general insurance, and some of these same institutions feature prominently in funds and wealth management. A tail of smaller providers operate alongside these institutions, varying by market in length and strength.

Across the financial system, there is a continual flow of new products and a re-packaging of existing products to appeal to specific groups of consumers. As a consequence, there is a very large number of products in financial markets, with sometimes only marginal differences between them: nearly 4000 different residential property loans and 250 different credit cards are on offer, for example. The same situation is apparent in insurance markets: the largest 4 general insurers hold more than 30 brands between them. In the pet insurance market this is particularly pronounced — 20 of the 22 products (with varying premiums) on offer are underwritten by the same insurer.

Banks can price as they want. Little switching occurs — one in two people still bank with their first-ever bank, only one in three have considered switching banks in the past two years, with switching least likely among those who have a home loan with a major bank. ‘Too much hassle’ and a desire to keep most accounts with the same institution are the main reasons given for the lack of switching, with home loans being a particularly difficult product for consumers to switch.

Although financial institutions generally have high customer satisfaction levels, customer loyalty is often unrewarded with existing customers kept on high margin products that boost institution profits. For this to persist, channels for provision of information and advice (such as mortgage brokers) must be failing.

Scope for price rivalry in principal loan products is constrained by a number of external factors: price setting by the Reserve Bank facilitating price coordination by banks; expectations of ratings agencies that large banks are too big to fail; and some prudential regulation (particularly in risk weighting) that favours large institutions over smaller ones.

The growth in mortgage brokers and other advisers does not appear to have increased price competition. The revolution is now part of the establishment. Non-transparent fees and trailing commissions, and clear conflicts of interest created by ownership are inherent. Lender-owned aggregators and brokers working under them should have a clear best interest duty to their clients.

There is also variation between larger and smaller institutions in funding costs (with a large regulatory-determined component). Not all ADIs face the same regulatory arrangements and regulatory effects on their pricing capacity. A source of differential funding costs to banks is a series of regulatory measures and levies that apply (both positively and negatively) to the major Australian-owned banks but not to smaller Australian-owned ADIs or foreign banks operating in Australia.

The net result of these regulatory measures is a funding advantage for the major banks over smaller Australian banks that rises in times of heightened instability. RBA estimated this advantage to have averaged around 20 to 40 basis points from 2000 to 2013 (worth around $1.9 billion annually to the major banks). More recently, the funding cost advantage of major banks has been estimated to have declined to about 10 basis points, due in part to prudential reforms. But it nevertheless persists, and ratings agencies are unlikely to rate institutions’ fund raising such that there is no effective differential between Australia’s major and smaller banks.

Australia’s major banks have delivered substantial profits to their shareholders — over and above many other sectors in the economy and in excess of banks in most other developed countries post GFC. In recent times, regulatory changes have put pressure on bank funding costs, but by passing on cost increases to borrowers, Australia’s large banks in particular have been able to maintain high returns on equity (ROEs).

The ROE on interest-only investor loans doubled, for example, to reach over 40% after APRA’s 2017 intervention to stem the flow of new interest-only lending to 30% of new residential mortgage lending (reported by Morgan Stanley). This ROE was possible largely due to an increase by banks in the interest rate applicable to all interest-only loans on their books, even though the regulator’s primary objective was apparently to slow the growth rate in new loans. Competing smaller banks were unable to pick up dissatisfied customers from this re-pricing of their loan book because of the application of the same lending benchmark to them.

Regulators have focused on a quest for financial stability prudential stability since the Global Financial Crisis, promoting the concept of an unquestionably strong financial system.

The institutional responsibility in the financial system for supporting competition is loosely shared across APRA, the RBA, ASIC and the ACCC. In a system where all are somewhat responsible, it is inevitable that (at important times) none are. Someone should.

The Council of Financial Regulators should be more transparent and publish minutes of their deliberations. Under the current regulatory architecture, promoting competition requires a serious rethink about how the RBA, APRA and ASIC consider competition and whether the Australian Competition and Consumer Commission (ACCC) is well-placed to do more than it currently can for competition in the financial system.

Some of APRA’s interventions in the market — while undertaken in a way that is perceived by the regulators to reflect competitive neutrality — have been excessively blunt and have either ignored or harmed competition. Such consequences for competition were neither stated nor transparently assessed in advance. APRA’s interpretation of Basel guidelines on risk weightings that non-IRB banks use for determining the amount of regulatory capital to hold, puts it among the most conservative countries internationally.

For home loans, the main area in which Australia’s risk weights vary from international risk weightings is for (lower risk) home loans that have a loan to value ratio below 80%.Australian non-IRB lenders are required to use a risk weight of a flat 35%, compared with Basel-proposed guidelines of 25% to 35% for such loans.

For small and medium enterprise (SME) loans, the main area of difference is lending that is not secured by a residence. A single risk weight (of 100%) applies to all SME lendingnot secured by a residence, with no delineation allowed for the size of borrowing, the form of borrowing (term loan, line of credit or overdraft) or the risk profile of the SMEborrowing the funds. In contrast, Basel proposed risk weights for SME lending vary from75% for SME retail lending up to €1 million, to 150% for lending for land acquisition, development and constructions.

The RBA should establish a formal access regime for the new payments platform (NPP). As part of this regime, the RBA should review the fees set by participants of the NPP and transaction fees set by NPPA; and require all transacting participant entities that use an overlay service to share de-identified transaction-level data with the overlay service provider.

Measures that should be prioritised to help consumers become a competitive force in the longer term include:

consumer rights to have their financial data transferred directly from one service provider to another, either facilitated through Open Banking arrangements or as part of a more broadly-based consumer data right

automatic reimbursement of the ‘unused’ portion of lenders mortgage insurance when a consumer terminates the loan

payment system reforms that help detach consumers from their financial providers

provision of information on median home loan interest rates provided in the market over the previous month

inclusion on insurance premium notices, of the previous year’s premium and percentage change.

The Productivity Commission has released the first in a planned series of five-yearly updates on productivity in Australia. The report shows that there is much the Australian government can do to boost productivity and living standards.

These include changing how government delivers or controls education and health, and how it manages infrastructure. Interestingly, for the Commission, policy to improve productivity in the private sector (primarily tax and regulation), while still important, plays second fiddle.

The Commission backs up its recommendations in these huge domains by a compendium of analyses spread over hundreds of pages in 16 supporting papers.

The Productivity Commission’s review comes amid a period of slow productivity growth in Australia and around the developed world. Fifteen years ago, most economists expected that the internet revolution and the rapid shift of manufacturing to China would, for all the disruption they entailed, sustain strong growth in the rich world. But those hopes were dashed.

A wide range of research has identified many possible culprits for the productivity slowdown. These include mismeasurement, that “easy wins” such as universal education have already been used up, ageing, risk aversion, and a hit to investment and innovation from the global financial crisis.

One of the Commission’s background papers covers many of these contributors to slow growth.

Australian productivity has grown faster than in many other high-income economies since the financial crisis, largely thanks to the mining boom and to our having avoided a deep recession.

But productivity growth has not been strong enough to keep wage growth strong in the face of declining export prices and some broader weakness as the mining investment boom comes off. Getting policy settings right is urgent to reduce the risk that Australia slides into the stagnation that other high-income economies have experienced.

The recommendations

The new report identifies five priorities to revitalise productivity: health, education, cities, market competition, and more effective government.

The Commission’s estimates imply that its policies would eventually boost GDP by at least two per cent, with additional non-market benefits in longer lives and quality of life.

In health, the report recommends changing funding arrangements, cutting low-value treatments, putting the person at the centre of health care, shifting to automated pharmacy dispensing in many locations, and moving to tax alcohol content on all drinks. The Commission estimates that the value of these reforms is at least A$8.5 billion over 5 years.

In education, the report makes recommendations to build teacher skills, better measure student and worker proficiency, extend consumer law to cover universities, and improve lifetime learning, including better information about the performance of institutions. The Commission does not put a dollar value on these reforms.

In cities and transport, the report recommends improved governance to stop poor projects being built, budget and planning practices to properly provide for growth and infrastructure, and policies to get more value out of existing and new assets (including road user charges, extending competition policy principles to cover land use regulation, and replacing stamp duties with land tax). The Commission estimates that these reforms would be worth at least A$29 billion per year in time.

To improve market competition, the report suggests a single effective price be placed on carbon, an end to ad-hoc interventions in the energy market, better consumer control of and access to data, and reforms to intellectual property to support innovation. The Commission estimates that these reforms would be worth at least A$3.4 billion per year.

Finally, to improve government, the report recommends that the states and the Commonwealth develop a new formal reform agenda that clarifies who has responsibility for what, tax changes, measures to improve fiscal discipline, and tougher accountability for implementation of agreed initiatives. The Commission does not put a dollar value on these reforms.

What’s missing?

The review’s omissions are informative, and some are glaring.

First, cutting company taxes is conspicuously absent from the proposals. It seems unlikely this omission is an oversight. It would seem, instead, that the Commission does not see a company tax cut as a priority for productivity growth, and is happy for government to make its own case for a tax cut.

Still, the report would have been stronger had it considered the tax mix more fully. There is credible case for a company tax cut, though it is not the only way to stimulate investment, it would take years to pay off, and it would hit the budget without increase in other taxes or spending cuts.

Second, the report gives short shrift to population growth. Governments are racing to keep pace with population growth in Melbourne and Sydney in particular, yet the report does not consider how population contributes to congestion, how it dilutes the value of natural resource rents, and how the challenges it creates for governments make it more difficult for them to deliver reforms that would boost productivity.

Third, the report does not give enough attention to reforms to improve market functioning. Many consumers in retail markets for services like energy and superannuation do not know how to identify good products, and so consumers often bear the costs of excess marketing or an excess of providers.

There are other gaps. The report does not give enough attention to macroeconomic stability, or even note the risks posed by the Australian house price boom. It does not mention the problematic National Broadband Network. It pays too little attention to the role of social safety nets in helping people manage risks and making the economy more flexible.

And finally, the report could have made stronger recommendations for better measurement. It is ironic that it finds the biggest opportunities in the health and education sectors, whose output is not measured with much accuracy.

Overall, the report is something of a landmark, and the Treasurer deserves credit for commissioning it. It condenses much of the policy advice the Productivity Commission has made in recent years, and adds new insights (for example, on land use).

It provides credible, if incomplete recommendations for improving health and education, and cities and transport. It undersells the value of further reforms to private sector regulation and tax. But it underscores how much governments can do on the “home turf” of the things they control most directly.

Now it is up to Commonwealth and state governments to absorb its insights, integrate them into their agendas, and put them into action.

Author: Jim Minifie, Productivity Growth Program Director, Grattan Institute

Australia’s most recognised regional banks have called on a major competition inquiry to level the playing field and put consumers and the economy first.

In a joint submission lodged with the Productivity Commission, AMP Bank, Bank of Queensland, Bendigo and Adelaide Bank, ME Bank and Suncorp highlighted five key areas that require policy reform to achieve sustainable competition and competitive neutrality:

Further policy reform to reduce the artificial funding cost advantages enjoyed by the major banks. While the new Major Bank Levy has reduced this advantage, it only recoups a small proportion of the overall credit rating uplift enjoyed by the majors;

Further reform of risk weights to address the significant gap that still exists between the capital requirements of the major banks and standardised banks. While there has been some risk weight narrowing following the FSI, the gap remains significant, and is particularly stark for loans with the lowest risk;

A review of macro-prudential rules to better balance macro outcomes such as stability, without undermining banking competition. One option would be for APRA to give greater policy weight to minimum capital requirements. Macroprudential rules set by APRA have effectively ‘locked-in’ market share of loan books at current levels, thus leaving smaller banks with no room to challenge the already dominant position of major banks;

Mortgage aggregators and brokers owned by major banks should publicly report on the proportion of loans they direct to their owners. While we do not suggest that major banks should be banned from owning broker networks, we do believe that where this occurs it should be managed in an open and transparent way to ensure customers are able to make fully informed decisions; and

Before any new regulations are introduced, greater consideration should be given to the impacts on smaller banks. The unprecedented pace and volume of new regulation and compliance has a disproportionate impact on smaller banks which stifles sustainable competition.

The banks also support the ABA’s submission calling for more care and attention into the shadow banking sector, which continues to compete free of many regulations and APRA oversight.

The CEOs said while Australia had been well served by a strong and highly regulated banking sector, it was important that stability did not overshadow competition and good consumer outcomes.

Suncorp Banking & Wealth CEO David Carter said: “We believe there can be a balanced and fair framework allowing banks of all sizes to compete on a level playing field, while still meeting all sound, prudential principles. We would like to see more attention on macro-prudential rules to promote customer choice and competitive pricing, as opposed to maintaining the status quo – which is in effect similar to the ‘yellow flag’ being waved at the Grand Prix, where all drivers are then prohibited from overtaking one another.”

ME CEO Jamie McPhee said: “Regulatory imbalances have allowed a small group of banks to dominate the Australian market. Reform is needed if we want to create a fairer banking system so smaller banks can compete. A more competitive banking system is about improving customer choice and promoting economic growth.”

AMP Bank Group Executive Sally Bruce said: “Access to cheaper funding plus lower capital requirements for like-for-like loans gives the big banks a huge advantage over smaller players. Combined with the blanket approach to compliance and macro-prudential limits, we have a system of issues which impede competition and the best outcomes for customers. We are at risk of keeping big banks big and small banks small unless we address.”

The CEOs said improving competitive neutrality will deliver better customer outcomes and drive greater innovation in the sector.

“A strong banking system is good for all Australians and smaller banks bring vital competition and choice to the market,” they said.

“While the market is competitive today, it is vital this competition is fair, productive and sustainable.

“The bottom-line test must be: what is good for customers is good for the economy.”

Macquarie Bank has started a trial, giving customers access to the data the bank has collected on them. These might include the number and types of account held, average balances, regular payments and income and credit score information. This information helps to determine both the need for products and the risk of a customer.

This idea is called open banking and will see customers use their data in a whole range of ways – to ensure they are getting a good deal on their credit cards or mortgages, to see how they are faring financially against people in similar situations, and even to make paying taxes easier. Until recently our banks have had exclusive access to all of this data. The banks used it for marketing and product design. That is, your data was used to increase their profits.

The absence of sharing meant the data was a hurdle to customer switching. But the Productivity Commission has said consumers should be given a “comprehensive right” to their data.

In fact, you can already see some of use cases for your data in services the banks themselves provide. For example, Ubank has a tool that allows customers to work out a budget, and compare themselves to others of similar ages, household types etc. And many banks and credit card companies allow you to dive into your spending habits, to see where your money is going.

Treasury is currently examining how open banking should work in practice, and the Productivity Commission is looking at competition in the financial services sector. So this Macquarie Bank trial is just the beginning of open banking in Australia.

Is it safe?

You might be worried about how these other services will access you data. You don’t have to share your passwords or bank login, rather the data is shared using a standardised application programming interface or API.

An API creates a standard for connecting to a service, similar to how there is a standard for writing down your home address. To mail a letter you write down a street number, street name, suburb, state, postcode. If you write down the latitude and longitude of the person’s house then the letter won’t get there, because it doesn’t abide by the standard.

API’s have security standards as well, with two elements. One is authentication – making sure that the machine seeking access is the machine it says it is – and the other is authorisation – making sure that the machine is permitted to access the API. In practice, the authentication component could be done by a trusted third party, such as Facebook or Google.

An open banking API would need to allow enough information about a customer to be accessed to allow for service comparisons. However, the data must not contain enough information to identify an individual. This is essential under Australian privacy law and proposed standards would also need to comply with the European General Data Protection Regulation (GDPR).

What will I use the data for?

The fact that all this data has largely been held by the banks until now means there aren’t a lot of services for us to connect to immediately.

The most immediate example is to use your data to make sure you are getting the best deal you can on your loans. This is one of the reasons the British Competition and Markets Authority decided that open banking was necessary.

Under this scheme, if you want to compare service providers, you can download your anonymised data in a standard form and then upload it to a bank, a price comparison website or an app. In the case of the app, it would present to you your best options, given your current banking profile. This would include staying with your current bank or changing one or more accounts to a different institution.

This data could also be used to get approval for a new loan. Your anonymous data, in combination with identity information, includes enough material for a lender to decide whether to give you a loan for a specific purpose.

These tools will foster more competition between banks as customers will find it easier to compare services and switch, but it will also mean customers can make sure they are getting the best product available at the bank they are currently at.

But beyond comparison and switching, there are a number of interesting examples of how you can benefit from the data in your bank.

A budgeting app connected to your bank account, for example, can use your anonymous data to help you plan your finances. Using both your banking and “tap and go” payment history, it can help you analyse your spending and set goals. These services can even tap into outside data, such as interest rates, to help you determine what to do if rates go up. It’s that spooky moment when your phone becomes your conscience.

Online accounting software such as Xero or MYOB allows daily reconciliation of business accounts. These software systems already use APIs provided by the major banks to reconcile current accounts, loan accounts and credit card services. One variant on the open banking API could let customers “mark” transactions that are employment related expenses or health related expenses to simplify tax returns.

Going beyond fintech

But beyond these examples there are any number of possibilities for what we can do with this data. For instance, we could see an app that helps you make shopping decisions to increase the amount of loyalty points you earn. That is, using data on prices, goals and financial history to benefit consumers and not just sellers.

There are already limited examples of such schemes. The Coles “Fly Buys” scheme is connected to Virgin Velocity points. Both Coles and Velocity prompt members to earn points. Adding an overlay of which credit card to use at the checkout is currently up to you. However, it would be perfectly feasible for an app in your phone to choose which credit card the phone uses to pay at the supermarket to give you maximum points.

There’s also an opportunity here to connect your stream of financial data to what might seem like unrelated data. For example, what if your smart watch prompted you to walk home if you’ve spent more on eating out than your budget allowed? That is, open banking might actually improve your fitness, or at least make you feel guilty about overspending.

Author: Rob Nicholls, Senior lecturer in Business Law, UNSW

The Australian government is still protecting industries that employ a small number of people. This is while the largest employer, the services sector, is subject to the largest tariffs, a recent Productivity Commission report demonstrates.

As a whole, manufacturing still receives 77% of net assistance, largely due to the remaining small levels of tariff assistance, plus some budget measures, according to the report.

“Input tariffs” increase the costs of imported goods and services that go into making things. This makes a business’ activities more expensive for the consumer. And even though the services sector accounts for around 85% of employment, current government policy is penalising this sector, which has the best prospects for future growth.

However, as the report states, it’s the construction industry that is most affected by input tariffs (A$1.5 billion worse off), followed by property and real estate (A$337 million), then accommodation and food (A$294 million). All of these sectors are labour intensive and employ substantial numbers of people, yet are forced to pay unnecessary tariff costs.

Despite all of this, the government is still protecting primary industries such as horticulture, sheep, beef and grains, and in the manufacturing sector in food and metal production, wood pulp and oil and chemicals. All of these latter industries are basic supply or processing industries, that provide inputs into other industries, but not usually the final products.

Tariffs against foreign goods are reducing and now only provide modest assistance to a few industry sectors. The report says this is worth A$4.6 million to manufacturing, and within that sector food and beverages, metal fabrication, wood and paper petroleum and chemicals enjoy the most protection. Together these industries provide a relatively small proportion of total employment (around 7% or just under 1 million employees).

The popular image of our government protecting the motor vehicle and component industries seems to be less true according to these latest statistics.

In terms of budget assistance from the government, it’s not cars but finance and insurance services that benefit most from the public purse followed by sheep, cattle and grain industries. Vehicle production now receives less than half the budgetary support it received eight years ago – down to approximately A$290 million from A$600 million in 2008-09. The government has given up on the motor vehicle industry and its capacity to provide jobs into the future. More particularly, the Productivity Commission is critical of governmental assistance to the Spencer Gulf industries in South Australia and to the bail-outs for the Arrium steel works in Whyalla, in the same state, which it considers wasteful and distortionary. Arrium went into voluntary administration before an overseas buyer was procured.

The commission is also hostile to green energy production and storage and to the politically sensitive Northern Australian Infrastructure Facility, which it considers a pork-barrelling exercise open to political pressure. It says this facility is likely to fund non-available projects, that will sit on the public books for years, and this is a misapplication of investment resources.

Finally the wrath of the Commission is piqued by the re-regulation of the sugar industry (another declining industry in employment terms) and especially at the granting of charity status to the main marketing arm, Queensland Sugar Ltd. This body must be one of the last remaining marketing monopolies in the primary industries.

Governments will have to look at winding back the remaining (smallish) tariffs affecting domestic service industry sectors – especially those affecting construction supplies, retail and property, accommodation and food.

These impacts flow into local costs that are making Australia a more expensive place to consume or do business both for Australians and overseas visitors.

Author: John Wanna, Sir John Bunting Chair of Public Administration, Australian National University