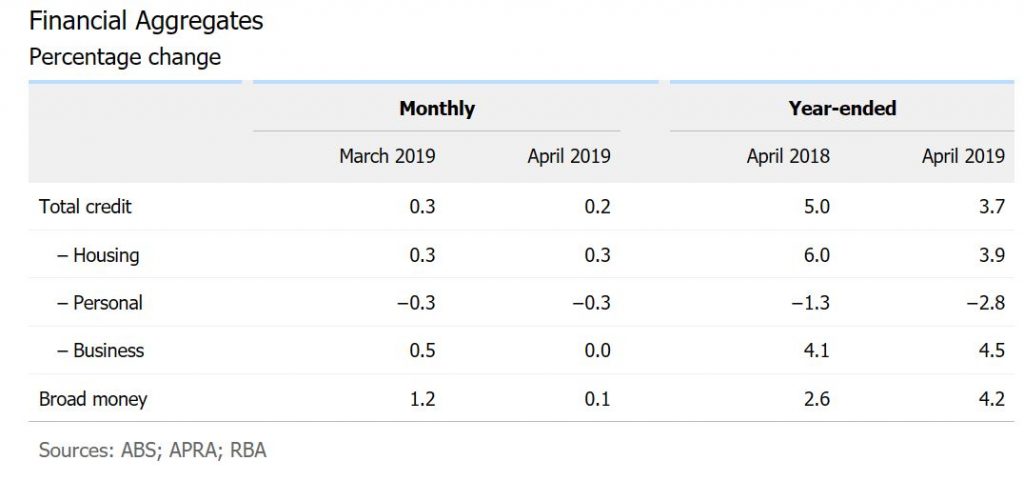

We look at the latest stats from RBA and APRA on credit growth. Home lending is STILL growing at 3.9% per annum – yet we are about to stir up the monster some more – “you cannot be serious!”

Once again on the last working day we get the latest credit

data from both the RBA and APRA. And fair enough, this is before the election,

and the recent spate of “unnatural acts designed to kick start credit growth,

but the trends before this are clearly down.

Here we are talking about the net stock of loans – rather than new loan

flows (so we see the net of old loans closed, refinanced, and new loans written).

We will need to wait for the ABS series in a couple of weeks to get the flow stats.

The RBA provides an overview, and a seasonally adjusted

series, including the non-bank sector. APRA provides data for the banking

sector – ADI’s or authorised depository institutions.

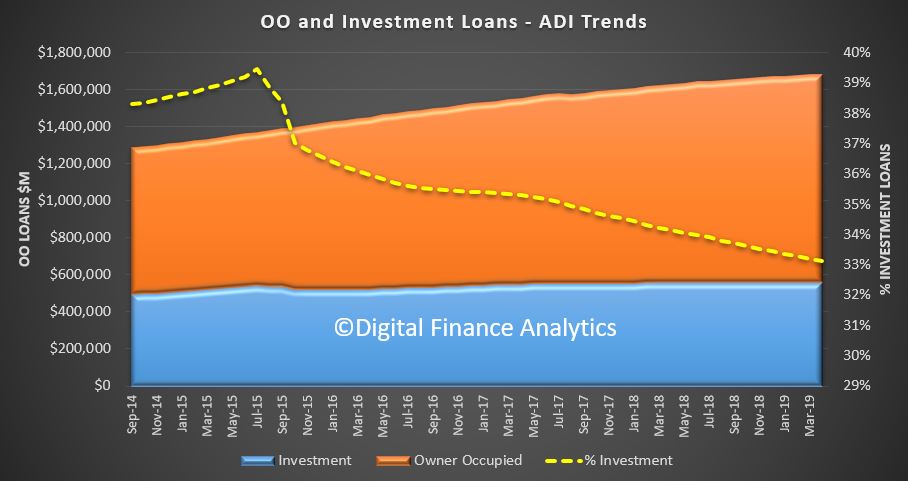

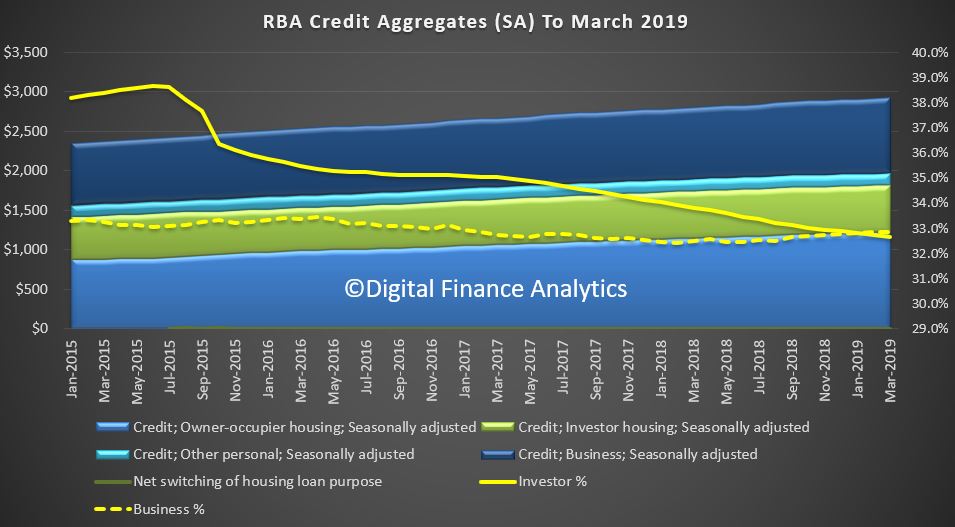

Total credit in the system, is still growing, with housing

lending up to $1.83 trillion dollars, with owner occupied lending accounting

for $1.23 trillion and investor loans 0.59 trillion. Business lending was 0.96

Trillion dollars and personal credit was $146 million dollars. So, you can see

how significant housing credit – and yes, it is STILL growing.

Of that $1.83 trillion dollars for housing, $1.68 trillion

comes from the banks, as reported by APRA.

Of that $1.12 trillion dollars is for owner occupied housing, and 0.55

trillion dollars for investors. The rest is non-banks, institutions who can

lend, but do not fund these loans from holding bank deposits. APRA now have

responsibility for these too but is not that actively engaged. So, to the rate of change of credit growth.

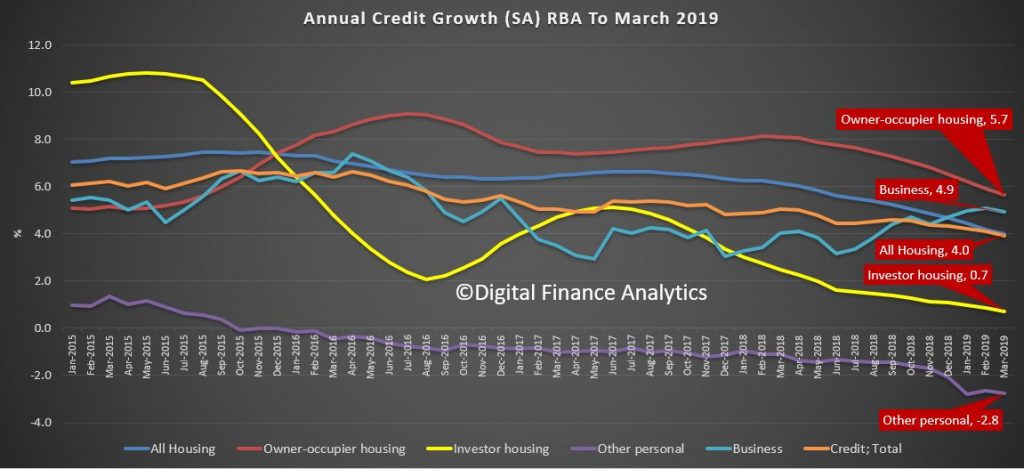

We know that housing credit growth has been slowing as

demand has slowed, and lending standards tightened, in response to APRA’s

interventions and the Royal Commission. But the stark reality is that business

lending is also flat according to the RBA.

In fact, last month, total credit grew by only 0.16% and

this is the weakest since early 2013.

Overall housing credit was up by 0.28% in the month, and personal

credit declined by 0.3%

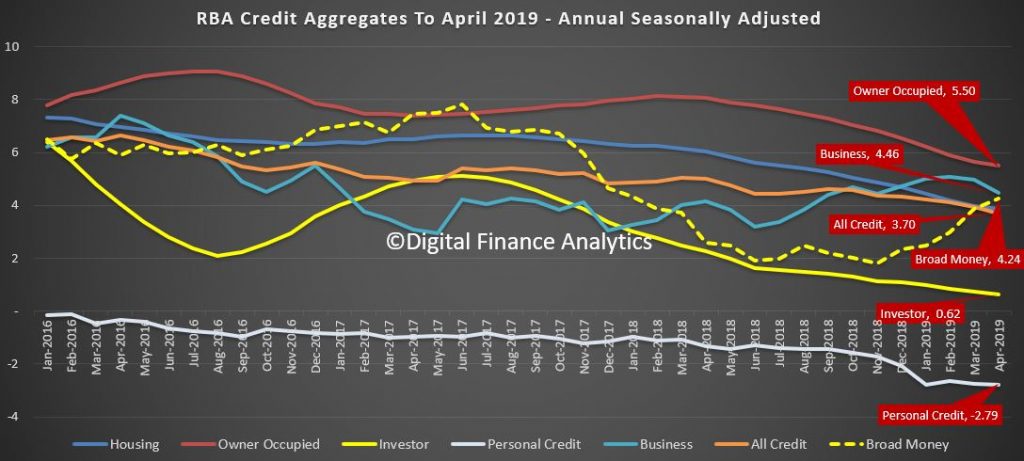

Annual credit growth slowed to 3.7%, the weakest since November

2013 and the trends are clear.

Slowing Housing credit growth is a large element in the

numbers, as we have been tracking. The latest annual figure is just 3.9%, and

this is the lowest ever in the series which started back in the late 1970s.

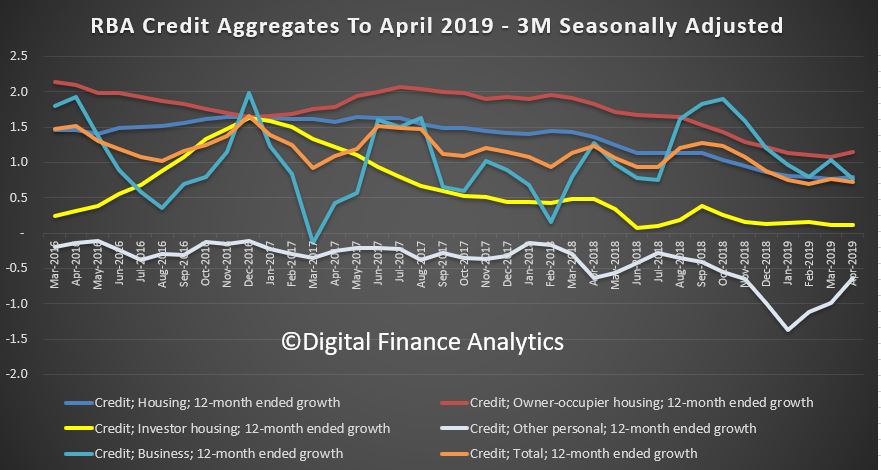

Looking at the three-month series you might argue that the

rate of decline is easing just a little, there is not much here really to get

excited about. Of course, most of the commentators are now looking ahead

following the Coalitions return to power. The RBA I think cut rates on Tuesday,

which is the first cut since August 2016. And of course, APRA is consulting on

a proposal to loosen the interest rate buffer test.

I won’t repeat here the significant downside forces which

will make a rebound in housing lending difficult, other than to say, the

Coalition has promised a home price recovery, so they have to try and engineer

it any cost – even if the debt balloon inflates further.

Investor housing momentum is still very weak, and there is

little to suggest this will change soon – though some might try to sell into

any more optimistic season. So, its down to first time buyers, and those

seeking to trade-up.

Turning to business credit, this grew by 4.5% over the past

year, up from 3.0% for 2017 but is easing back from gains of 6.4% in 2015 and

5.5% in 2016. In fact, this is an

important issue, as business lending and confidence are easing back – not a

good sign.

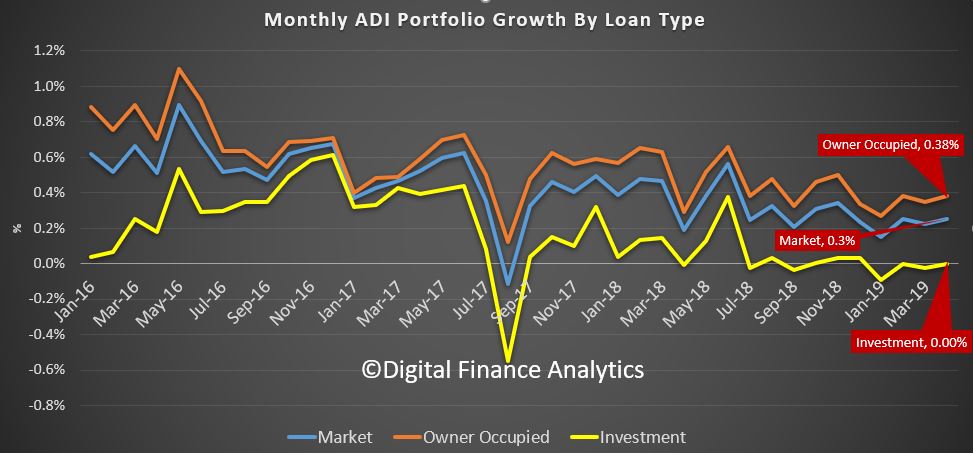

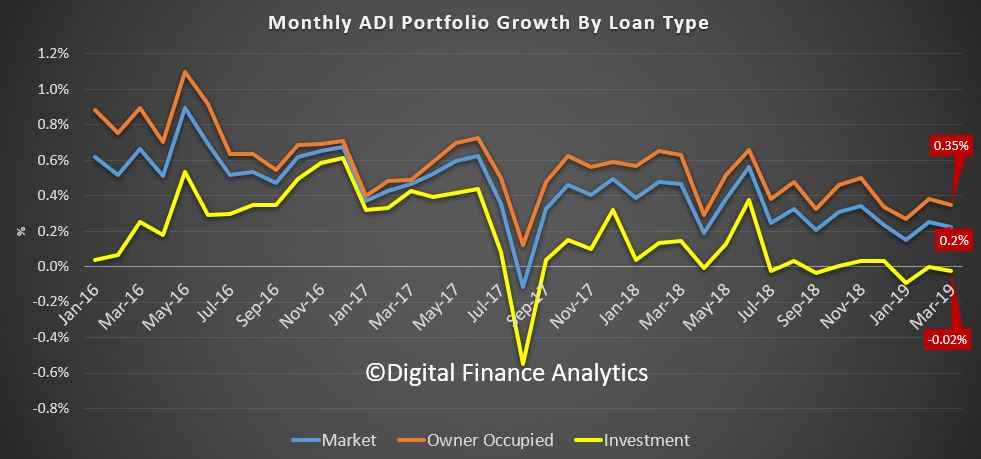

APRA’s data showed that owner occupied lending rose 0.38% in

the month, investor lending was flat, and the market growth was 0.3%.

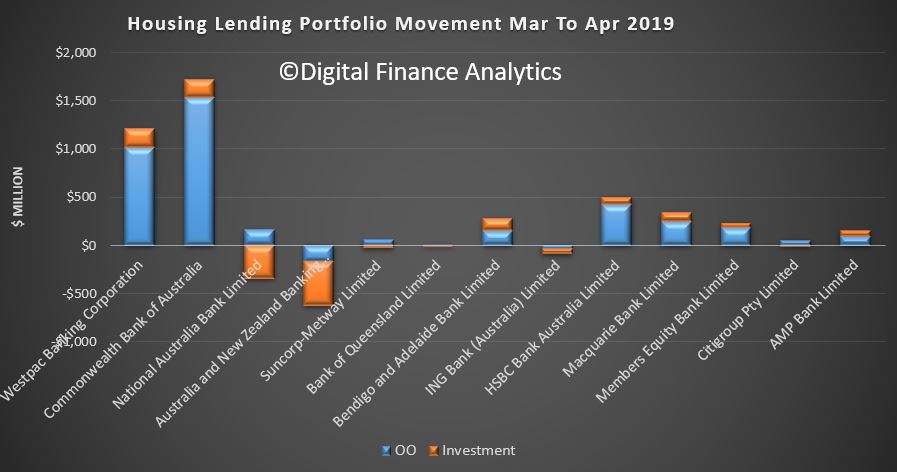

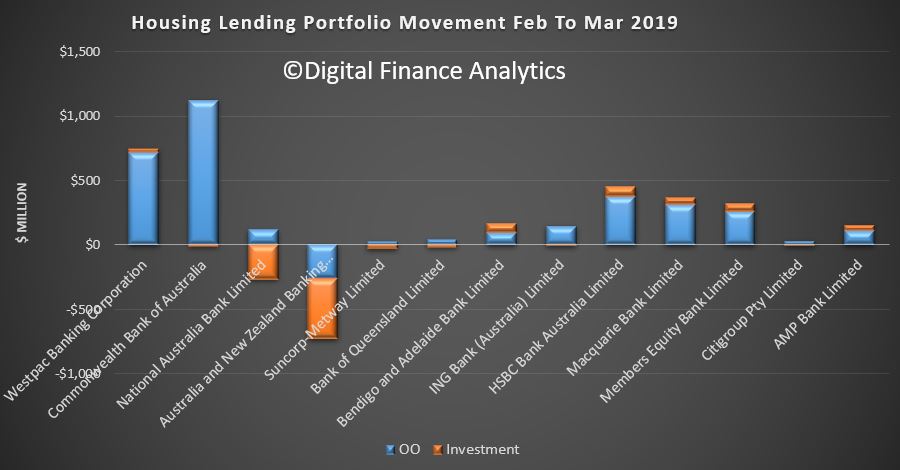

And our analysis of the individual bank data shows that housing market shares did not change that much, although CBA and Westpac were more active in net terms last month, though mainly in owner occupied lending. NAB and ANZ dropped more investor loans.

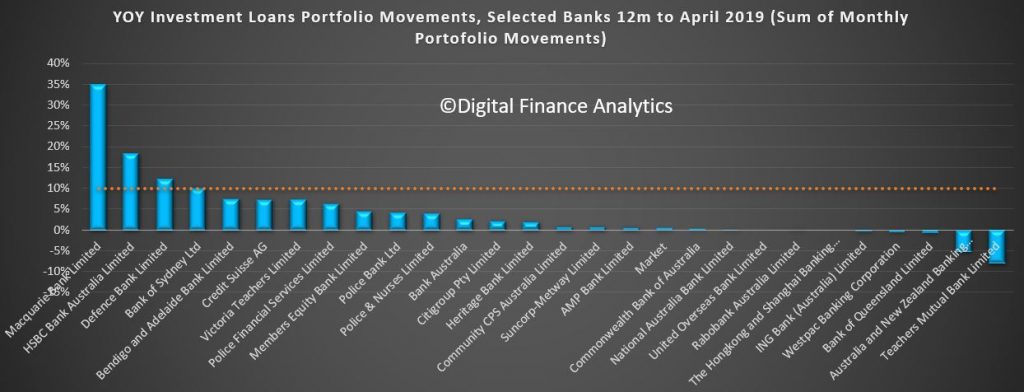

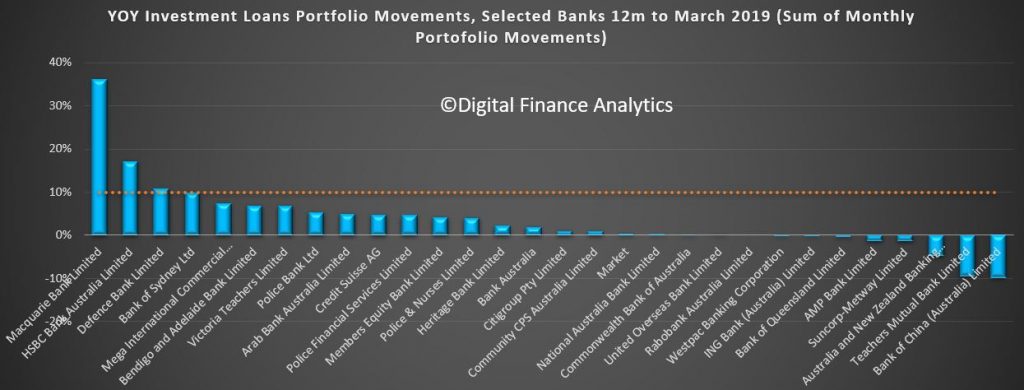

The 12-month portfolio moves for investor loans reveals the majors below the market. Macquarie and HSBC are leading the charge.

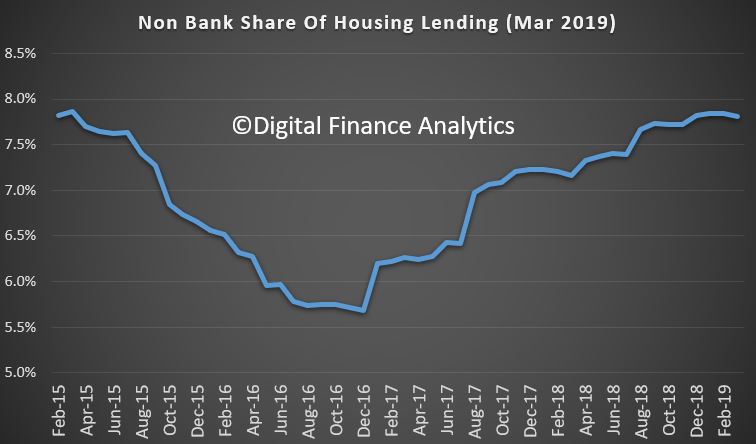

But a comparison of the gap between the Bank lending and RBA data shows the non-banks are still growing their books faster. Overall, they are running at an annualised 7.8%.

And analysis of owner-occupied lending by the non-banks shows it is still at 12.8%, compared with 2.1% for investor loans, but both above system.

So, standing back, the pre-election trends were weakening,

the non-banks were making hay, and investors are still on the sidelines. Now it

will be interesting to see if the so-called sentiment swing, and hype shows up

in the numbers in the next couple of months.

But to state the obvious, a growth rate of 3.9%

for credit for households even now is way stronger than wages growth or

inflation, so the debt burden is building further, and yet the policy settings

are about to be shifted to encourage more of the same. Hardly sensible.

The RBA’s aggregates to April 2019 shows s further slowing, with housing credit over 12 months down to a growth rate of 3.9%.

We will publish more analysis on this later, but no surprise given the unnatural acts now in the pipeline to try and reverse the trend. Plus an analysis of the APRA data, which also looks pretty weak.

The RBA released their minutes today, and things are looking less rosy, even though their rose-tinted glasses.

International Economic Conditions

Members commenced their discussion of the international economy by observing that global growth had

eased in the second half of 2018 and looked to have continued at around this more moderate rate in 2019.

Growth in Australia’s major trading partners was also expected to continue at around this slower

pace over 2019 and 2020. Members also observed that the outlook for China continued to be a significant

uncertainty for the global growth outlook, as were trade tensions, which had escalated again between the

United States and China immediately prior to the meeting. Global financial conditions had become more

accommodative since the turn of the year. Members noted that this could lead to stronger growth than

expected, although there were still risks of events occurring that could lead to both tighter financial

conditions and lower global growth.

March quarter GDP growth had been stronger than expected in the United States and the euro area, but

had been quite weak in a number of trade-intensive economies in east Asia. The latest monthly data had

shown that growth in Chinese industrial production, fixed asset investment and total social financing

had increased, suggesting momentum had picked up in response to targeted policy easing by the Chinese

authorities. Conditions in Chinese property markets had also strengthened. Members noted that economic

sentiment in China had improved since the beginning of the year, partly because small to medium-sized

businesses were obtaining improved access to finance and government infrastructure spending was boosting

demand.

Members noted that the sharp slowing in global trade had been related to slowing growth in China. The

decline in the value of Chinese imports had been broadly based across regions, although the large

decline in the value of trade with the United States suggested that trade diversion as a result of new

tariffs had also been a factor. Growth in China was expected to slow gradually over the forecast period

to the middle of 2021. This was expected to continue to weigh on external demand for trade-intensive

economies in east Asia and the euro area; recent data on export orders in east Asia had been

subdued.

Members discussed various longer-term policy initiatives in China, including policies on investment

abroad and modernisation of China’s manufacturing sector. China’s infrastructure

investment abroad had served to support land and sea trade routes, although there had been some

challenges that Chinese authorities had been addressing. Members also noted the authorities’

efforts to promote innovation, particularly in China’s technology sector, and to upgrade the

Chinese manufacturing sector significantly.

For some economies, the slowing in external demand had been accompanied by lower investment and

investment intentions. In some east Asian economies in particular, including South Korea, the turn in

the cycle in the global electronics industry had dampened exports and investment. Members noted that

firms would also be less likely to commit to long-term investments given the uncertainty around the

evolution of international trade policy.

In many economies, domestically focused sectors, such as services and retail trade, had been more

resilient than externally focused sectors. This was particularly the case in the advanced economies,

where tight labour market conditions had supported growth in spending. Unemployment rates had remained

around multi-decade lows in many advanced economies and wages growth had increased noticeably. In the

United States and Japan, recent wage increases had been larger for low-wage earners than high-wage

earners.

Core inflation had remained subdued in most economies and, following weaker inflation data in the

United States, was below target in the three major advanced economies.

There had been some large movements in commodity prices over recent months. Iron ore prices had

remained high as a result of supply disruptions in Brazil and Australia. Oil prices had also risen,

which had led to higher headline consumer price inflation in most economies and was expected to flow

through to higher prices for Australian liquefied natural gas exports over the following couple of

quarters. As a result, the forecast for Australia’s terms of trade had been revised higher, but

they were still expected to decline over the forecast period to the middle of 2021.

Domestic Economic Conditions

Members commenced their discussion of the domestic economy by noting that growth had been subdued in

the second half of 2018. Indicators of household consumption suggested that growth had remained subdued

in the March quarter. In addition, demand for new dwelling construction was expected to have remained

weak. These factors had been the main drivers of a downward revision to the domestic growth outlook in

the near term. Beyond 2019, these effects were broadly offset by upward revisions to export growth and

some newly announced mining investment projects. Members noted that, overall, the Bank expected

year-ended GDP growth to be 2¾ per cent over 2019 and 2020.

Growth in consumption had been weaker than expected in the second half of 2018 and retail sales data

for the March quarter suggested that this weakness had continued into 2019. Members noted that, as had

been the case for some time, the outlook for growth in consumption was a key uncertainty for the overall

growth outlook. The risks to consumption were tilted to the downside, given the extended period of low

income growth and the adjustment occurring in housing markets. The forecast for an improvement in growth

in consumption depended on an increase in growth in household disposable income over the forecast

period. The forecast increase in household disposable income growth was supported by employment growth,

a pick-up in wages growth and lower growth in tax payments, partly because of the introduction of the

low- and middle-income tax offsets announced in the Australian Government 2019-20 Budget. Members noted

that there was uncertainty about the outlook for fiscal policy and how this might affect the outlook for

growth in household disposable income.

Housing markets had remained weak in the preceding month. The rental vacancy rate in Sydney had

increased to the highest level in around 15 years and housing prices in established markets had

continued to decline. More positively, the pace of price declines had moderated and the modest recovery

in auction clearance rates since the start of the year had been sustained.

Information obtained through the Bank’s liaison program continued to indicate that sales

conditions for off-the-plan apartments and new detached housing had been difficult. The spike in

residential building approvals in February had largely been unwound in March, confirming that underlying

conditions for new dwelling activity remained weak. Data released since the previous meeting had shown

that the pipeline of residential work to be done had decreased in the December quarter, but remained

high. Members noted

that the forecasts for dwelling investment suggested that population growth could exceed growth in the

stock of housing towards the end of the forecast period, and that this possibility had been suggested by

a number of the Bank’s liaison contacts.

Survey measures of business conditions had moved a little higher in March and April and had remained

slightly above average, though well below the high levels that had prevailed throughout most of 2018.

Forward-looking indicators of non-mining business investment had been mixed; non-residential building

approvals had declined, but the pipeline of infrastructure work remained high. Non-mining business

investment was expected to support growth in output over the forecast period.

Mining investment had declined in the December quarter, but was expected to increase over the forecast

period, reflecting investment required to sustain current production levels and an expectation that a

number of new projects would commence towards the end of the forecast period. Recent trade data

suggested resource exports would contribute to output growth in the March quarter, and exports were

expected to contribute to output growth throughout the forecast period. Members noted that the forecast

pick-up in rural exports from 2020 depended on a return to normal weather conditions.

Public demand was expected to continue to support aggregate growth over the forecast period; a

significant share of this expenditure was associated with delivering goods and services to households,

such as the National Disability Insurance Scheme. Members noted that the Victorian Government had

announced measures to contain growth in labour costs in an environment of expected lower stamp duty

revenues.

Growth in employment in the March quarter had been strong, following similar outcomes over much of

2018. Most of the growth in employment since mid 2018 had been in full-time employment. The

unemployment rate had remained around 5 per cent in March. Members observed that conditions in

the labour market had signalled a significantly stronger pace of economic activity since mid 2018

than indicated by the GDP data. Leading indicators of labour demand had eased over recent months and

provided a mixed picture of the near-term outlook. As a result, employment growth was expected to be

similar to the growth rate of the working-age population in the near term. The unemployment rate was

expected to remain around 5 per cent through most of the forecast period, before declining to

around 4¾ per cent in 2021.

Members noted that the forecasts for the labour market suggested that there would be some spare

capacity in the labour market throughout the forecast period, although there was uncertainty about how

quickly the spare capacity would decline and how progress would feed into wage pressures. The central

forecast was for wages growth to pick up gradually. In combination, the forecasts for wages growth and

consumer price inflation implied that real consumer wage growth would be low but positive over the

forecast period.

The inflation data in the March quarter CPI release were noticeably lower than expected. The CPI

increased by 0.1 per cent (seasonally adjusted) in the quarter, while the underlying rate of

inflation was ¼ per cent. In year-ended terms, headline inflation was

1.3 per cent, with the underlying rate at 1½ per cent. The earlier exchange

rate depreciation and the drought-related increase in some food prices had led to relatively strong

retail price inflation in the March quarter. However, these inflationary pressures had been more than

offset by broad-based weakness in other CPI components, which was likely to be more persistent.

Rental inflation had remained low, driven by a marked slowing in rental inflation in Sydney; data on

newly advertised rents suggested that rents had started to pick up in Perth. Developer discounts and

incentives had weighed on the prices of newly built homes, particularly in Melbourne and Brisbane. A

range of government policy decisions had contributed to lower inflation in administered prices in recent

quarters. Market and survey-based measures of inflation expectations had declined in recent months, as

had been the case in other advanced economies.

Members noted that the recent CPI data had led the Bank to reassess the disinflationary effects of the

weak housing market. Combined with the lower GDP growth outlook, this had led to a downward revision to

the inflation outlook, although there was also some uncertainty about the persistence of downward

pressure from utilities and administered price changes and the effect of housing market weakness. The

central forecast scenario was for underlying inflation of around 1¾ per cent over 2019,

2 per cent over 2020 and a little higher after that.

Financial Markets

Members commenced their discussion of financial market developments by noting that global financial

conditions were accommodative and had eased significantly since the start of the year. Market

expectations for the future path of monetary policy in a number of economies had declined earlier in the

year, in line with guidance from major central banks that policy was likely to be more accommodative

than previously expected. The expectation that policy rates would remain little changed for some time

had contributed to very low levels of volatility in most financial markets.

In the United States, with inflation close to but a bit below target and the federal funds rate close

to neutral, the Federal Reserve (Fed) had reiterated that it would take a patient and flexible approach

to its policy decisions. While the Fed’s recent forecast update implied that one more policy rate

increase was likely by the end of 2020, market pricing implied that the Fed was expected to lower its

policy rate around twice over that period. At its April meeting, the European Central Bank had

reiterated that it expected policy rates to remain at current levels at least through to the end of

2019. The Bank of Japan had indicated that its very stimulatory policy settings will remain in place

until at least mid 2020. Market participants expected the next moves in policy rates in Canada, New

Zealand and Australia to be down.

Government bond yields remained at very low levels in the advanced economies, having declined since

late 2018 in line with downward revisions to growth and inflation projections, and the lowering of

policy rate expectations by market participants. In Germany and Japan, long-term bond yields were around

zero, close to the record lows of 2016. Members noted that Australian government bond yields had

declined by more than those in other major markets over the preceding six months, following

weaker-than-expected inflation data and a lower expected path for monetary policy. By contrast, Chinese

government bond yields had increased over the preceding month, as signs emerged that policy stimulus

there was providing support to economic activity.

Members noted that, following the brief inversion of segments of the US yield curve in March, the slope

of the US yield curve had increased a little in April. While market commentators had noted that past

episodes of yield curve inversion had tended to precede recessions, the decline in credit spreads and

rise in equity valuations in 2019 suggested market participants did not perceive this to be a particular

risk.

Members observed that financing conditions for corporations remained favourable. In the advanced

economies, corporate bond yields had declined, partly because of a decline in spreads. In addition,

equity prices had increased substantially since the start of 2019 to be at their highest levels in over

a decade, including in Australia.

In China, growth in total social financing had been steady in recent months and a little higher than in

2018, supported by bank lending and bond issuance. Off-balance sheet financing had continued to decline,

reflecting the authorities’ efforts to discourage riskier forms of financing. Members noted that

the Chinese authorities had introduced additional measures to encourage banks to lend to small private

sector firms, which had previously made use of off-balance sheet financing that was now less readily

available. Members also noted the substantial local government bond issuance to finance infrastructure

projects, which was a key part of the authorities’ stimulus measures.

In foreign exchange markets, volatility had remained low over the preceding month, including in most

emerging markets. Members noted, however, that risks remained pronounced for a small number of economies

with specific vulnerabilities, most notably Turkey and Argentina, where financial conditions had

tightened again.

The Australian dollar had depreciated a little following the weaker-than-expected March quarter CPI

release, but overall had been little changed over recent months and remained around the lower end of its

narrow range of the past few years. Members noted that this reflected the offsetting influences of the

rise in commodity prices and decline in Australian government bond yields relative to those in the major

markets over 2019. The difference between long-term government bond yields in the United States and

Australia had increased to a historically large 75 basis points.

Housing credit growth had slowed over the preceding year, but the monthly pace of growth had stabilised

over recent months. In three-month-ended annualised terms, growth in housing lending was around

4½ per cent for owner-occupiers and ½ per cent for investors. Loan

approvals also appeared to have stabilised in recent months. Members noted that, although lending

practices were tighter than they had been for some time, the decline in housing credit growth over the

preceding year had been driven largely by weaker demand for finance, associated with the decline in

housing prices.

The average interest rate charged on outstanding variable-rate housing loans had remained broadly

steady. While banks had increased their standard variable reference rates since mid 2018, rates on

new loans had remained materially below the average of those on outstanding loans. Members noted that

banks had recently reduced the rates charged on new fixed-rate loans.

Funding costs for the major banks had declined to record lows in preceding months, as the increase in

short-term money market rates in 2018 had been fully unwound and retail deposit rates had continued to

edge lower. Despite the low cost of funding, bank bond issuance in 2019 so far had been a little below

the average of recent years. Issuance of bonds by other corporations and of residential mortgage-backed

securities had been broadly in line with the average of recent years.

The pace of growth in business lending had been maintained in recent months at rates that were above

those of the preceding few years, driven by lending to large businesses. Lending to small businesses had

declined over the preceding year. Interest rates on variable-rate loans to large businesses, which are

linked to bank bill swap rates, had declined in the March quarter. Members observed that the rates

charged on small business loans remained markedly higher than those on large business loans, with the

gap between small and large business loan rates having doubled following the global financial

crisis.

Financial market participants’ expectations of cash rate cuts were brought further forward

following the release of the March quarter CPI. Financial market pricing implied that the cash rate was

expected to be lowered by 25 basis points within the next three months and again by the end of

2019.

Considerations for Monetary Policy

In considering the stance of monetary policy, members observed that growth in Australia’s major

trading partners had slowed, driven by a sharp slowing in global trade associated with slower growth in

China. Members also noted, however, that targeted stimulus measures in China appeared to be having an

effect and global financial conditions remained very accommodative. In a number of advanced economies,

labour markets had continued to tighten and wages growth had increased, but inflationary pressures had

remained subdued.

Domestically, members noted that the sustained low level of interest rates over recent years had been

supporting economic activity and had contributed to a decline in the unemployment rate. However,

household income growth had remained low and the March quarter inflation data indicated that the

inflationary pressures in the Australian economy were lower than previously thought.

After updating the forecasts for the new information, the central forecast scenario remained for

progress to be made on the Bank’s goals of reducing unemployment and returning inflation towards

the midpoint of the target, but at a more gradual pace than previously expected. Under the central

scenario, GDP growth had been revised lower in the near term, but was expected to pick up to be around

2¾ per cent over 2019 and 2020. The unemployment rate was expected to remain around

5 per cent over 2019 and 2020

before declining a little to 4¾ per cent in 2021. This implied that spare capacity would

remain in the economy for some time. Given this, and the subdued inflationary pressures across the

economy, underlying inflation was expected to be 1¾ per cent over 2019,

2 per cent over 2020 and a little higher after that.

Members noted that the central forecast scenario was based on the usual technical assumption that the

cash rate followed the path implied by market pricing, which suggested interest rates were expected to

be lower over the next six months. This implied that, without an easing in monetary policy over the next

six months, growth and inflation outcomes would be expected to be less favourable than the central

scenario.

At the same time, members also recognised that there were risks to the forecasts in both directions.

The risks to the global economy remained tilted to the downside, with uncertainty remaining around the

evolution of international trade policy. Domestically, the outlook for household consumption remained a

key uncertainty, with the risks tilted to the downside given ongoing low income growth and the

adjustment occurring in housing markets. On the upside, it was possible that the combined effects of

continued accommodative financial conditions, the increase in Australia’s terms of trade, a

renewed expansion in the resources sector and the expected lift in household disposable income growth

would result in stronger growth in output than in the central forecast scenario.

Members discussed the outlook for the domestic labour market in some detail. As in the previous

meeting, members discussed the scenario where inflation did not move any higher and unemployment trended

up, recognising that in those circumstances a decrease in the cash rate would likely be appropriate. As

noted at the previous meeting, members recognised that the effect on the economy of lower interest rates

could be expected to be smaller than in the past, given the high level of household debt and the

adjustment that was occurring in housing markets. Nevertheless, a lower level of interest rates could

still be expected to support the economy through a depreciation of the exchange rate and by reducing

required interest payments on borrowing, freeing up cash for other expenditure.

In light of the recent run of inflation data, the Board then discussed the likelihood that the economy

could sustain a stronger labour market with lower rates of unemployment than previously estimated, while

achieving inflation consistent with the target. In this context, members observed that the recent

international experience was that inflation had remained low despite historically low rates of

unemployment. Given the international evidence and the recent Australian inflation data, members agreed

that a further decline in the unemployment rate would be consistent with achieving Australia’s

medium-term inflation target. Given this, members considered the scenario where there was no further

improvement in the labour market in the period ahead, recognising that in those circumstances a decrease

in the cash rate would likely be appropriate.

Taking into account all the available information, including the various uncertainties about the

outlook, members judged that it was appropriate to hold the stance of monetary policy unchanged at this

meeting, noting that holding monetary policy steady had enabled the Bank to be a source of stability and

confidence over recent years. In view of the spare capacity that remained in the economy, however,

members agreed that it was important to continue to pay close attention to developments in the labour

market and set monetary policy to support sustainable growth in the economy and achieve the inflation

target over time.

The Decision

The Board decided to leave the cash rate unchanged at 1.5 per cent.

The RBA released their quarterly Statement On Monetary Policy today. Expect rate cuts, and QE later as the AUD is allowed to slide, as a decade of wrong policy is now coming home to roost. Plus they are tracking the labour market as a key determinate of policy using the wobbly ABS series data, looking past weaker inflation, and hoping for wages growth.

Growth in the Australian economy has slowed and inflation remains low. Subdued growth in household income and the adjustment in the housing market are affecting consumer spending and residential construction. Despite this, the labour market is performing reasonably well, with the unemployment rate steady at around 5 per cent. Underlying inflation has been lower than expected, at 1½ per cent over the year to the March quarter, with pricing pressures subdued across much of the economy.

GDP growth is expected to be around 2¾ per cent over both 2019 and 2020. This is lower than previously forecast, reflecting the revised outlook for household consumption spending and dwelling activity. Stronger growth in exports and, further out, work on new mining investment projects are expected to support growth. Forecasts for inflation have also been revised lower. Trimmed mean inflation is expected to be around 1¾ per cent over 2019 and then increase gradually to 2 per cent in 2020 and a touch above 2 per cent by early

In the near term, CPI inflation is expected to run a little above the rate for trimmed mean inflation, driven by the recent increase in petrol prices.

The Australian dollar is currently around the low end of the narrow range it has been in for some years. Sovereign bond rates in Australia have continued to decline relative to those in the major economies. This has tended to counteract the upward pressure on the exchange rate that would otherwise have come from rising prices for Australia’s key commodity exports.

Conditions in the established housing market remain soft. Housing prices have continued to decline in the largest cities, although the pace of decline has eased a bit recently. Some other indicators, including auction clearance rates, have improved a little since the end of last year, but generally point to continued soft conditions. Prices have also been declining in many other cities and regional areas.

Despite strong employment growth and some recovery in growth of average hourly earnings, growth in household income was very low over Non-labour sources of income have been subdued and are likely to remain so for a while, given the effects of the drought on farm incomes and of soft housing market conditions on the earnings of many other unincorporated businesses. Strong growth in tax payments has also subtracted from disposable income growth over recent years.

Weak growth in household income poses a key risk to the outlook for household consumption, especially in the context of falling housing prices and the need for many households to service high levels of debt. Some recovery in income growth is likely, because employment growth is expected to remain solid, wages are expected to increase and the tax offset for low and middle-income taxpayers is set to come into effect in the second half of this year.

At its recent meeting, the Board focused on the implications of the low inflation outcomes for the economic outlook. It concluded that the ongoing subdued rate of inflation suggests that a lower rate of unemployment is achievable while also having inflation consistent with the target. Given this assessment, the Board will be paying close attention to developments in the labour market at its upcoming meetings.

At its meeting today, the Board decided to leave the cash rate unchanged at 1.50 per cent. They reinforced the labour market as the key to future rate moves, looking past lower inflation. That is a pretty strong signal about what would lead to a cut. They are still reciting stronger growth than many believe is feasible.

Franking, cutting now would be using using up the limited ammo they have, for no good reason. Savers will be relieved!

The outlook for the global economy remains reasonable, although the risks are tilted to

the downside. Growth in international trade has declined and investment intentions have

softened in a number of countries. In China, the authorities have taken steps to support

the economy, while addressing risks in the financial system. In most advanced economies,

inflation remains subdued, unemployment rates are low and wages growth has picked up.

Global financial conditions remain accommodative. Long-term bond yields are low,

consistent with the subdued outlook for inflation, and equity markets have strengthened.

Risk premiums also remain low. In Australia, long-term bond yields are at historically

low levels and short-term bank funding costs have declined further. Some lending rates

have declined recently, although the average mortgage rate paid is unchanged. The

Australian dollar is at the low end of its narrow range of recent times.

The central scenario is for the Australian economy to grow by around 2¾ per cent in 2019

and 2020. This outlook is supported by increased investment in infrastructure and a

pick-up in activity in the resources sector, partly in response to an increase in the

prices of Australia’s exports. The main domestic uncertainty continues to be the outlook

for household consumption, which is being affected by a protracted period of low income

growth and declining housing prices. Some pick-up in growth in household disposable

income is expected and this should support consumption.

The Australian labour market remains strong. There has been a significant increase in

employment, the vacancy rate remains high and there are reports of skills shortages in

some areas. Despite these positive developments, there has been little further progress

in reducing unemployment over the past six months. The unemployment rate has been

broadly steady at around 5 per cent over this time and is expected to remain around this

level over the next year or so, before declining a little to 4¾ per cent in 2021. The

strong employment growth over the past year or so has led to some pick-up in wages

growth, which is a welcome development. Some further lift in wages growth is expected,

although this is likely to be a gradual process.

The adjustment in established housing markets is continuing, after the earlier large

run-up in prices in some cities. Conditions remain soft and rent inflation remains low.

Credit conditions for some borrowers have tightened over the past year or so. At the

same time, the demand for credit by investors in the housing market has slowed

noticeably as the dynamics of the housing market have changed. Growth in credit extended

to owner-occupiers has eased over the past year. Mortgage rates remain low and there is

strong competition for borrowers of high credit quality.

The inflation data for the March quarter were noticeably lower than expected and suggest

subdued inflationary pressures across much of the economy. Over the year, inflation was

1.3 per cent and, in underlying terms, was 1.6 per cent. Lower housing-related costs and

a range of policy decisions affecting administered prices both contributed to this

outcome. Looking forward, inflation is expected to pick up, but to do so only gradually.

The central scenario is for underlying inflation to be 1¾ per cent this year, 2 per cent

in 2020 and a little higher after that. In headline terms, inflation is expected to be

around 2 per cent this year, boosted by the recent increase in petrol prices.

The Board judged that it was appropriate to hold the stance of policy unchanged at this

meeting. In doing so, it recognised that there was still spare capacity in the economy

and that a further improvement in the labour market was likely to be needed for

inflation to be consistent with the target. Given this assessment, the Board will be

paying close attention to developments in the labour market at its upcoming meetings.

The headline news is the overall housing credit is up, to a new record of $1.82 trillion dollars up 0.31% from last month, or 0.31%. Within that owner occupied lending rose 0.32% to $1.22 trillion dollars and investment lending was flat. 32.7% of lending stock is for investment lending purposes, a slight fall from last month, whilst business lending as a proportion of all lending rose from 32.9% from 32.8% to reach $963.7 billion dollars. Personal credit fell 0.27% or $0.4 billion, to $147.1 billion, and continues to fall.

The annualised movements by category shows further weakness, with lending for owner occupied housing now at 5.7%, investment housing lending at 0.7%, giving housing overall growth of just 4% (though still higher than wages growth I would add). Personal credit fell 2.8% over the past year, while business lending rose 4.9% annualised. All these figures are on a seasonally adjusted basis

Turning to the APRA data on the banks, owner occupied lending rose 0.35% in March, while investment lending fell by 0.02%, giving total credit growth of just 0.2%. Over the past year owner occupied loans grew by 4.8% (compared with 5.7% at the aggregate level) and investor loans grew 0.4% (compared with 0.7% at the aggregate level). So the banks loan portfolios are growing more slowly than the market.

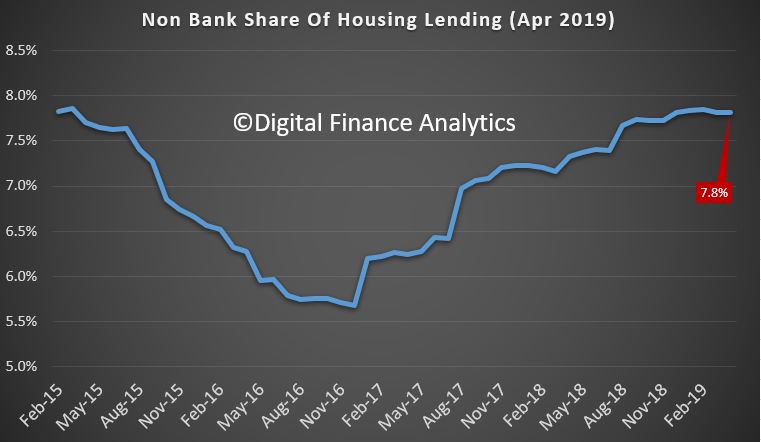

This can be illustrated by comparing the RBA and APRA data (warts and all) to show the non-bank sector is growing faster than the banks. Overall, they have over 7.5% of the market, which is up from the low in December 2016.

In addition, the rate of growth is significantly higher than the banks. Non-bank owner occupied loans are growing at an annual rate of 14%, while investment loans are 2.2%; both significantly higher than the ADI’s. Non-banks have weaker regulation, and more ability to lend. APRA has yet to truly engage with the sector.

Turning back to the individual lenders, the changes in their portfolios over the month show that Westpac and CBA offered the most new owner occupied loans, while ANZ dropped back, on both owner occupied and investment loans, while NAB dropped investment lending. HSBC, Macquarie and Member Equity Bank (ME) lend more than the regionals.

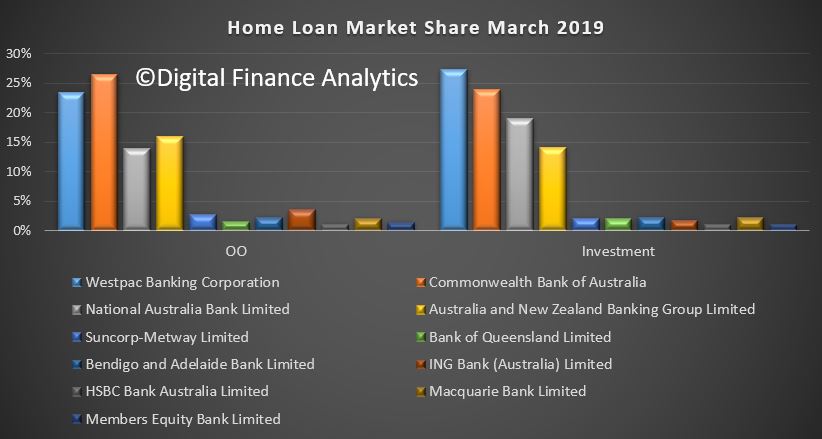

Overall market shares hardly moved, with CBA still the largest owner occupied lending, and Westpac the biggest investor lender.

Investment lending growth over the past 12 months has been anemic, but some lenders such as Macquarie are making hay. Of course the old 10% speed limit from APRA has gone now, but the relative growth highlights the fact that the four majors are well below market growth levels – and ANZ the weakest (which is why they said they wanted to lend more).

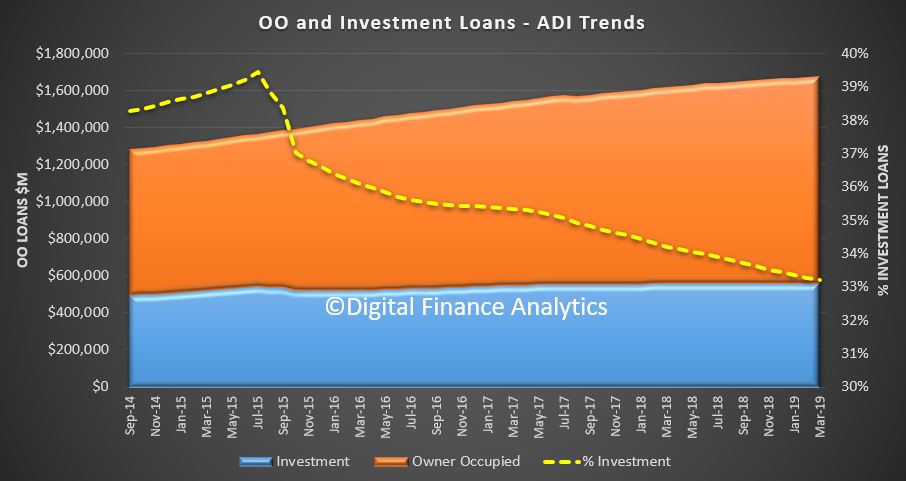

So finally, the total ADI lending book is at $1.68 trillion dollars, with owner occupied loans comprising $1.12 trillion dollars and investment loans $557 billion dollars, and comprising 33.2% of the portfolio – as the ratio continues to fall.

In conclusion, the credit impulse – the rate of change of credit being written is the most significant forward indicator of house price trajectory. The weak state of the market suggests more and significant price falls ahead. Yet despite all this, household debt will continue to rise. There is absolutely no reason to loosen lending requirements, or drop the hurdle rate on these numbers. More households will get into trouble ahead.

The RBA released their minutes today, and they highlight the current tensions between the domestic GDP and labour market data evolve. But more negative news was recited in the minutes, and this suggests rate cuts, not rate rises.

International Economic Conditions

Members commenced their discussion by noting that the slower pace of global economic activity had

continued in recent months. This had been particularly evident in the manufacturing sector. Survey

measures of conditions in the manufacturing sector had declined across a range of economies, although

they had ticked up in China in March. Slower external demand, especially from China, had continued to

weigh on export growth and the manufacturing sectors in the trade-exposed economies of east Asia, Japan

and the euro area. In east Asia, the electronics cycle had turned, which had affected the

region’s exports as well as investment in those economies with sizeable semi-conductor

sectors.

Recent trade talks between the United States and China had taken on a somewhat more positive tone.

However, the United States had also said it would consider imposing restrictions on automotive imports,

which would affect large car exporters, including Germany and Japan.

In the major advanced economies, however, domestic demand conditions had remained positive, supported

by an easing in financial conditions since the beginning of 2019, and were consistent with growth being

around, or even above, potential. Underlying inflation had remained close to target in a number of

advanced economies, but global headline inflation had declined since late 2018 because of the fall in

oil prices.

Growth in consumption in the advanced economies had been supported by ongoing tightness in labour

markets, which had led to an upward trend in wages growth over a number of years. In the United States,

the unemployment rate had remained below levels consistent with full employment and employers had been

finding it increasingly difficult to find suitable labour. Members observed that most sectors of the US

labour market had experienced strong conditions and the pick-up in wages growth had been most pronounced

for lower-income workers.

In Japan, consumption was expected to be supported by a bring-forward of spending ahead of an increase

in the consumption tax in October 2019, as well as ongoing tightness in the labour market. In the euro

area, the unemployment rate had been declining gradually and wage pressures had increased. However,

employment intentions had eased in the euro area and, more sharply, in the United Kingdom in the context

of ongoing uncertainty around Britain’s exit from the European Union.

The outlook for investment across the major advanced economies had been more mixed. In the United

States, investment indicators had eased a little but remained above average, while investment in the

euro area had weakened further. Members noted that political uncertainty in the United Kingdom and the

euro area was weighing on investment in those economies. In Japan, survey measures suggested that

business conditions would remain strong despite a prospective moderation in investment growth.

In China, growth in domestic demand had slowed. At its March meeting, the National People’s

Congress had set a target of 6–6.5 per cent for growth in output in 2019, which was

below the target of around 6.5 per cent in 2018. Members noted signs that stimulus measures

implemented by the authorities over recent months were having an impact: growth in total social

financing had increased a little, after slowing over the preceding year, and growth in infrastructure

investment and retail spending had recovered. Residential construction activity had also increased.

However, some recent indicators of production and investment in the manufacturing sector, which is more

exposed to external demand, had been subdued. Exports from China to the United States had continued to

decline, but China’s imports from the United States had increased a little over the first few

months of 2019, after an earlier sharp decline. Australian coal shipments had continued to be affected

by customs delays at Chinese ports.

Australia’s terms of trade had increased in the December quarter to be around

6 per cent higher over 2018. The terms of trade were expected to have increased further in the

March quarter, although commodity price developments had been mixed since the previous meeting. Bulk

commodity prices had been little changed because falls in coal prices had been largely offset by an

increase in iron ore prices. Oil prices had risen, but were still 20 per cent below their

recent peak in October 2018. Reflecting oil price movements in late 2018, liquefied natural gas (LNG)

prices were expected to have declined over the first quarter of 2019. Other commodity prices had been

little changed over the previous month.

Domestic Economic Conditions

Members commenced their discussion of the domestic economy by observing that growth had slowed markedly

in the second half of 2018 compared with the first half. GDP had increased by 0.2 per cent in

the December quarter and by 2.3 per cent over the year, which was below the forecasts

presented in the February Statement on Monetary Policy. The soft December quarter outcome

partly reflected another weak quarter of consumption growth and a larger-than-expected fall in dwelling

investment. It also reflected some temporary factors, such as the weather-related disruption to resource

exports and the effect of the drought. Public demand and non-mining investment had supported output

growth. Members noted that the income-based measure of GDP growth had been particularly weak over the

preceding year, while the expenditure-based measure had been stronger.

Growth in consumption had clearly slowed in the second half of 2018. The weakness had been concentrated

in discretionary items, especially those that have historically been most correlated with housing prices

and housing turnover, such as motor vehicles and home furnishings. Retail sales data and contacts in the

Bank’s liaison program suggested that growth in housing-related consumption had remained soft in

recent months.

Members noted that growth in household disposable income, which is an important driver of consumption

growth, had been subdued for a number of years. In 2018, labour income growth had been above the very

low rates seen in recent years, supported by a pick-up in growth in average hourly earnings and

continued employment growth, but non-labour income growth had remained weak. Members observed that tax

payments by households had been growing noticeably faster than income growth in recent years, partly

because of efforts to increase tax compliance.

Dwelling investment appeared to have passed its peak, although there continued to be uncertainty about

how quickly dwelling investment might decline over the forecast period. Construction of new dwellings

had contracted in the second half of 2018; the largest falls in the December quarter had been for

apartments in New South Wales and detached housing in Queensland. Slower housing activity had also

weighed on the incomes of some building contractors and property professionals in the December quarter.

There continued to be a large amount of work in the pipeline, which should support a relatively high

level of building activity in the near term. Members noted that there had been a substantial rise in

building approvals for high-density residential projects in February, although this series was volatile

and in trend terms remained well below earlier peaks. Members also noted that population growth was

expected to continue to support demand for housing over the medium term.

Conditions in the established housing market had remained weak in recent months. Housing prices had

continued to fall in Sydney, Melbourne and Perth, and had declined a little in most other capital cities

and regional areas. In March, Sydney prices were 13 per cent below their 2017 peak and

Melbourne prices were 10 per cent below their peak. Although auction clearance rates in Sydney

and Melbourne had increased over the first quarter of 2019, they remained at relatively low levels.

Members noted that in Perth, housing prices had declined over the previous year, while the rental

vacancy rate had declined sharply and there were signs that newly advertised rents were starting to

increase. By contrast, rental vacancies in Sydney had risen, particularly in suburbs where the supply of

new apartments had increased significantly.

Non-mining business investment had grown solidly in the December quarter, with non-residential

construction having made the largest contribution to growth in the quarter, driven partly by strong

growth in private sector infrastructure projects, such as roads and renewable energy. Forward-looking

indicators, such as the substantial amount of work still to be done on private infrastructure projects,

the relatively high level of non-residential building approvals and positive business investment

intentions, pointed to further growth in non-mining business investment. Survey measures of business

conditions had declined in late 2018, but had stabilised at above-average levels.

Mining activity had subtracted from growth in the second half of 2018, mainly reflecting ongoing

declines in mining investment as remaining LNG projects approached completion. Members noted that

investment required to sustain capacity and recently announced expansion projects were expected to

support stronger mining investment over the medium term. Declines in resource exports, partly related to

supply disruptions, had also subtracted from growth in the second half of 2018. Coal exports to China

had declined by 20 per cent, partly as a result of weather-related disruptions. The longer

time taken for imports of coal to clear Chinese customs in recent months was also likely to have played

a role. Liaison contacts had reported that they expected to continue to be able to redirect coal

shipments intended for China to other destinations. Members noted that there had been some disruptions

to iron ore shipments as a result of Tropical Cyclone Veronica, which were likely to have affected iron

ore export volumes in March.

The ongoing effects of the drought had weighed on farm output and income in the December quarter, and

rural exports had declined; farm GDP had fallen by more than 6 per cent over the second half

of 2018. Based on the latest estimates from the Australian Bureau of Agricultural and Resource Economics

and Sciences, farm production was expected to improve gradually in 2019/20

assuming rainfall returned to average levels. This was a more favourable outlook than had been assumed

in the forecasts presented in the February Statement on Monetary Policy. However, members

noted that shortages of water in the Murray-Darling Basin had been severe and that it would take

significant rainfall to increase soil moisture content from current low levels in this region.

Public demand had contributed strongly to GDP growth over 2018, supported by spending on the National

Disability Insurance Scheme and aged care and health services, and investment in infrastructure. Members

noted that, despite this, the overall fiscal impact on the economy had been negative because of slow

growth in some other forms of government expenditure and strong growth in tax revenues.

The labour market had continued to improve in early 2019, despite the slowing in growth recorded in the

national accounts through 2018. Employment had increased a little in February, following strong growth

in January, and the unemployment rate had declined to 4.9 per cent, continuing the run of

months with an unemployment rate at or around 5 per cent. Other measures of spare capacity,

including the underemployment rate and the long-term unemployment rate, had also trended downwards. The

participation rate had been relatively stable at a high level over the preceding year or so.

Employment growth over the previous year had been particularly strong in the health care & social

assistance, professional services and construction industries. Over the same period,

employment-to-population ratios had increased further in New South Wales and Victoria, where

unemployment rates had been around historically low levels. Employment-to-population ratios had declined

a little in other states more recently. Forward-looking indicators of labour demand had been mixed in

recent months. Job advertisements had eased, but job vacancies reported by employers through the ABS

survey had increased further as a share of the labour force in February.

Financial Markets

Members commenced their discussion of financial market developments by noting that global financial

conditions remained accommodative and had eased over the preceding couple of months.

Market expectations for the future path of monetary policy in a number of economies had been lowered

since the beginning of the year. This was consistent with guidance from major central banks that

monetary policy would remain more accommodative than earlier expected, given downward revisions to

growth forecasts and little upside risk to inflation despite increasingly tight labour markets.

At its March meeting, the US Federal Open Market Committee (FOMC) had kept the federal funds rate

unchanged and announced that the decline in the Federal Reserve’s asset holdings would slow from

May and cease after September, which was sooner than had been expected. The FOMC also published the

quarterly update of its members’ projections for where they believed the federal funds rate was

likely to be in coming years. These projections implied that the federal funds rate was likely to remain

unchanged throughout the rest of 2019, followed by one increase (of 25 basis points) in 2020. By

contrast, at the time of the December 2018 meeting, the median FOMC projection had been for two rate

increases in 2019 and one in 2020. Policy expectations implied by financial market pricing had also been

revised down since December. These implied that the next move in the federal funds rate was expected to

be down.

In the euro area and Japan, financial market pricing indicated that policy rates were expected to be

maintained at very low levels for an extended period, in line with recent statements by the respective

central banks. In March, the European Central Bank had announced that it would roll over a long-term

lending program to euro area banks. In Canada, New Zealand and Australia, financial market pricing

implied that declines in policy rates were expected in the coming year or so.

Members noted that 10-year government bond yields had declined noticeably across all major markets over

the preceding month. In some cases, including in Australia, yields had declined to historic lows. These

declines had reflected lower expected paths for monetary policy, lower term premiums and, to varying

extents, lower inflation expectations. In Germany and Japan, long-term bond yields had again turned

negative, approaching the lows that had been reached in 2016. In the United States, long-term rates had

moved below some short-term rates for a brief period, with market commentators noting that past episodes

of yield curve inversion had tended to precede recessions. At the same time, the recent decline in risk

premiums in credit and equity markets suggested financial market participants did not consider a

recession to be likely.

Members observed that financing conditions for corporations had improved. Corporate bond yields had

moved lower, reflecting the decline in government bond yields as well as a decline in spreads following

increases in late 2018. Non-financial firms had increased their bond issuance in 2019, particularly in

the US dollar high-yield sector. By contrast, issuance of leveraged loans had been more subdued, which

partly reflected an easing in investors’ appetites for floating rate securities in response to

the lowering of policy rate expectations. Equity markets in the advanced economies had been little

changed in March, having previously rebounded from their sharp fall in late 2018.

In China, equity markets had risen particularly sharply since the end of 2018, which was likely to have

reflected some easing in US–China trade tensions, as well as the authorities’ stimulus

measures. Growth in total social financing had increased a little in recent months, as the authorities

had taken measures to encourage bond issuance. They had also encouraged banks to provide finance to

smaller private firms. To support this, the authorities had signalled additional targeted monetary

easing for the period ahead. These changes had followed a slowing in the growth of total social

financing over the preceding year or more as the authorities had taken measures to reduce non-bank

lending, which had been an important source of funding for private firms, in order to reduce overall

risks in the financial system.

In other emerging markets, conditions had been relatively stable in 2019, although Argentina and Turkey

had experienced renewed depreciation of their exchange rates in response to continued macro-financial

and political risks in those economies.

Members noted that there had been little change in major economies’ foreign exchange markets

over the preceding month. The Australian dollar had also been little changed, remaining at the lower end

of its range of recent years. The strength in commodity prices and the terms of trade had been

supporting the exchange rate, while the continued decline in Australian government bond yields relative

to those in other major markets had been working in the opposite direction.

Growth in housing lending to owner-occupiers had slowed to 4¾ per cent in

six-month-ended annualised terms, although the monthly growth rate had increased slightly in February.

Growth in housing lending to investors remained at a very low level. Housing loan approvals were

materially below the levels of a year earlier, but had also increased slightly in February, with the

small uptick in approvals broadly based across types of borrowers. Members observed that the slowing in

housing lending over the preceding year had been driven largely by weakness in demand, particularly from

investors. There had also been some tightening in lending practices. Lenders continued to compete for

borrowers of high credit quality by offering lower interest rates on new loans than typically paid on

existing loans.

Members noted that the major banks’ funding costs had declined over the preceding couple of

months. The cost of debt funding had declined as pressures had eased in short-term money markets and

bank bond spreads had narrowed. Deposit rates had also continued to edge downwards.

Funding conditions for Australian businesses more broadly were accommodative. Three-year bond yields

for corporations across all major sectors had declined to record lows, reflecting the decline in both

government bond yields and spreads. Bond issuance by non-financial corporations in the first quarter of

2019 had been in line with that of recent years. Growth in bank lending to businesses had remained

robust, in part reflecting increased lending by the major banks, although other institutions had

accounted for most of the growth. Members observed that the growth in business lending had been entirely

to large businesses. Meanwhile, credit conditions for some small businesses were reported to have

tightened further recently.

Financial market participants’ expectations of a rate cut had been brought forward following

weaker than expected data, most notably the December quarter national accounts. Financial market pricing

implied that the cash rate was expected to be lowered in the second half of 2019 and then again in

2020.

Financial Stability

Members were briefed on the Bank’s regular half-yearly assessment of the financial system.

Overall, members noted that financial stability risks were slightly higher than six months earlier but

were not especially elevated.

Globally, investors were receiving little compensation for taking on risk. Notably, risk-free rates

were very low and the term premium in the United States had briefly turned negative. Furthermore,

corporate bond spreads remained low. These conditions had contributed to the significant increase in

borrowing by businesses since the global financial crisis. However, members noted that debt servicing

costs had not increased to the same extent, given the decline in interest rates over this period. The

high prices of a range of assets in this environment meant that there was heightened risk of an abrupt

repricing in response to news.

Members observed that the profitability of banks globally had generally increased. In part, this

reflected above-trend economic growth in the first half of 2018. However, some European banks remained

fragile, given large stocks of non-performing loans, high cost structures and overcapacity. The large

stock of sovereign debt held by some European banks, along with concerns about sovereign debt

sustainability, raised potential issues about the resilience of some banking systems.

In China, the authorities had taken measures to contain risks in the financial system. As a result, the

pace of growth in debt had slowed to below the pace of growth in the economy. However, given the earlier

rapid growth in debt, China’s ratio of non-financial debt to GDP remained higher than in other

economies with comparable income and even higher than in many high-income economies. Members noted that

the earlier rapid growth in debt had also raised concerns about the lending standards under which those

loans had been made.

In Australia, conditions in the housing market had remained weak. Housing prices had fallen further in

the capital cities and regional areas. Over the preceding six months, the falls had been largest in

Sydney and Melbourne, but prices in these cities had remained more than 40 per cent higher

than in 2012. Falls in housing prices had resulted in some borrowers having negative equity, where the

value of their loans exceeded that of their properties. Nationally, just over 2 per cent of

borrowers, accounting for less than 3 per cent of housing debt, were estimated to have

negative equity. Around 90 per cent of these borrowers were in Queensland, Western Australia

and the Northern Territory. Members observed that negative equity by itself was not a concern for

financial stability. However, if unemployment were to rise and borrowers were not able to continue to

make repayments, then financial institutions would incur increased losses. Members noted that the

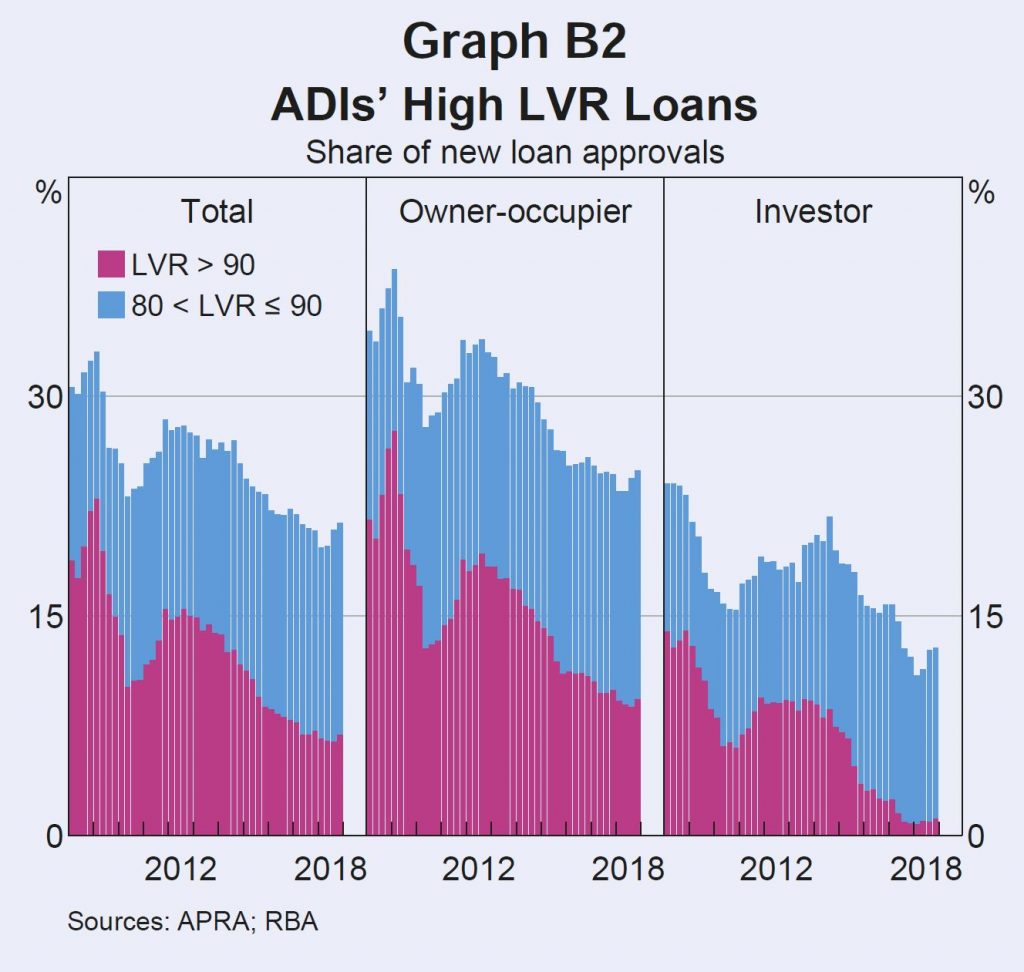

decline in high loan-to-valuation ratio (LVR) lending in recent years was expected to lessen any losses

for lenders. In recent quarters, almost all loans to investors had LVRs less than 90 per cent.

By contrast, a decade earlier only 85 per cent of loans to investors had LVRs less than

90 per cent. The share of owner-occupiers with high LVR loans had also declined.

Members noted that total household payments on housing debt as a share of income had been broadly

stable in recent years. Within the total, however, an increase in scheduled principal repayments had

roughly offset a fall in unscheduled principal repayments. Members noted that households’ excess

payments amounted to about two-and-a-half years’ worth of scheduled repayments on average.

Housing loan interest payments had increased slightly as housing debt had increased.

Banks’ assets had continued to perform well overall. Although banks’ non-performing

housing loans had increased, they remained low at less than 1 per cent of their total housing

lending. Members noted that the increase in housing loan arrears had been driven by loans remaining in

arrears for longer, on average. Banks’ business loans had been performing well, with

non-performing loan rates around their lowest levels in a decade. Banks had continued to accumulate

capital, with the capital ratios of the four major banks all exceeding or close to the

‘unquestionably strong’ benchmarks set out by the Australian Prudential Regulation

Authority (APRA).

The tightening in banks’ housing lending practices over recent years had been accompanied by an

increase in lending by non-banks, although this was still estimated to account for less than

5 per cent of total housing credit. Members noted that, while not subject to prudential

regulation by APRA, non-banks’ housing lending is subject to responsible lending obligations. The

available evidence suggested that the riskiness of non-bank housing lending had not increased.

Members noted that the International Monetary Fund’s Financial Sector Assessment Program report

on the Australian financial system was generally positive about the resilience of domestic financial

institutions and the quality of regulatory and supervisory oversight, but made several high-level

recommendations for improving current arrangements.

Considerations for Monetary Policy

In considering the stance of monetary policy, members observed that growth in the global economy had

slowed over the second half of 2018 and into 2019. Trade tensions and political developments in Europe

remained sources of uncertainty. At the same time, though, global financial conditions had eased in

preceding months and, in China, the authorities had provided targeted stimulus to support domestic

growth. In a number of economies, continued strength in labour market data and moderating GDP growth

were sending different signals about the momentum in economic activity. Members noted that this was also

the case in Australia. While the labour market had continued to improve in early 2019, GDP growth had

slowed over 2018. Continued low growth in household disposable income and the adjustment in housing

markets had weighed on household spending.

Members noted that the sustained low level of interest rates over recent years had been supporting

economic activity and had contributed to progress in reducing the unemployment rate and returning

inflation towards the midpoint of the target, albeit only gradually. The central scenario was for

further gradual progress to be made on both unemployment and inflation. Members observed that a pick-up

in growth in household disposable income was an important element of these forecasts. Given this outlook

for further progress towards the Bank’s goals, members agreed that there was not a strong case

for a near-term adjustment in monetary policy. Members recognised that it was not possible to fine-tune

outcomes and that holding monetary policy steady would enable the Bank to be a source of stability and

confidence.

Members agreed that inflation was likely to remain low for some time. Wages growth had remained low,

there continued to be strong competition in the retail sector and governments had been working to ease

cost of living pressures, including through their influence on administered prices. In these

circumstances, members agreed that the likelihood of a scenario where the cash rate would need to be

increased in the near term was low.

Members also discussed the scenario where inflation did not move any higher and unemployment trended

up, noting that a decrease in the cash rate would likely be appropriate in these circumstances. They

recognised that the effect on the economy of lower interest rates could be expected to be smaller than

in the past, given the high level of household debt and the adjustment that was occurring in housing

markets. Nevertheless, a lower level of interest rates could still be expected to support the economy

through a depreciation of the exchange rate and by reducing required interest payments on borrowing,

freeing up cash for other expenditure.

Taking account of the further progress expected towards the Bank’s goals, members assessed that

it was appropriate to hold the cash rate steady. Looking forward, the Board will continue to monitor

developments, including how the current tensions between the domestic GDP and labour market data evolve,

and set monetary policy to support sustainable growth in the economy and achieve the inflation target

over time.

The Decision

The Board decided to leave the cash rate unchanged at 1.5 per cent.

The RBA released their Financial Stability report today, and even with the rose tinted RBA glasses there are a number of worrying issues touched on. Though none new. But their analysis of negative equity is over optimistic. So we will look at what they say, and highlight some additional considerations.

The RBA said:

Domestic economic conditions remain broadly supportive of financial stability. The unemployment rate has remained around 5 per cent since the previous Review and corporate profit growth has also been strong.

However, GDP growth in Australia also slowed in the second half of 2018. In particular, consumption growth eased and the outlook for consumption is uncertain.

Conditions in the housing market remain weak. Nationally, housing prices are 7 per cent below their late 2017 peak, although they are still almost 30 per cent higher since the start of 2013.

Growth in housing credit was slightly lower over the six months to February than the preceding half year, with investor credit hardly growing at all.

Nationally, falling housing prices have been driven by weaker demand and increased housing supply. The tightening in the supply of housing credit from improved lending standards has played a smaller part. Importantly, these more rigorous lending standards have seen the quality of new loans improve in recent years.

Measures of financial stress among households are generally low and households remain well placed to service their debt given low unemployment, low interest rates and improvements to lending standards. However, there has been an increase in housing loan arrears rates. The increase in arrears has been largest in Western Australia, where the decline in mining related activity has seen housing prices fall for nearly five years and unemployment increase.

They did in “deep dive” on negative equity using their securitised loan data.

Large housing price falls in parts of Australia mean some borrowers are facing negative equity – where the outstanding balance on the loan exceeds the value of the property it is secured against. Negative equity creates vulnerabilities both for borrowers and lenders. A borrower having difficulty making loan repayments who has negative equity cannot fully repay their debt by selling the property. Negative equity also implies that banks are likely to bear losses in the event that a borrower defaults. Evidence from Australia and abroad suggests that borrowers who experience an unexpected fall in income are more likely to default if their loan is in negative equity.

At present, the incidence of negative equity remains low. Given the large increases in housing prices that preceded recent falls and the decline in the share of mortgages issued with high loan to- valuation ratios (LVRs), housing prices would need to fall significantly further for negative equity to become widespread. However, even if this did occur, increased defaults would be unlikely if the unemployment rate remains low, particularly given the improvements in loan serviceability standards over recent years.

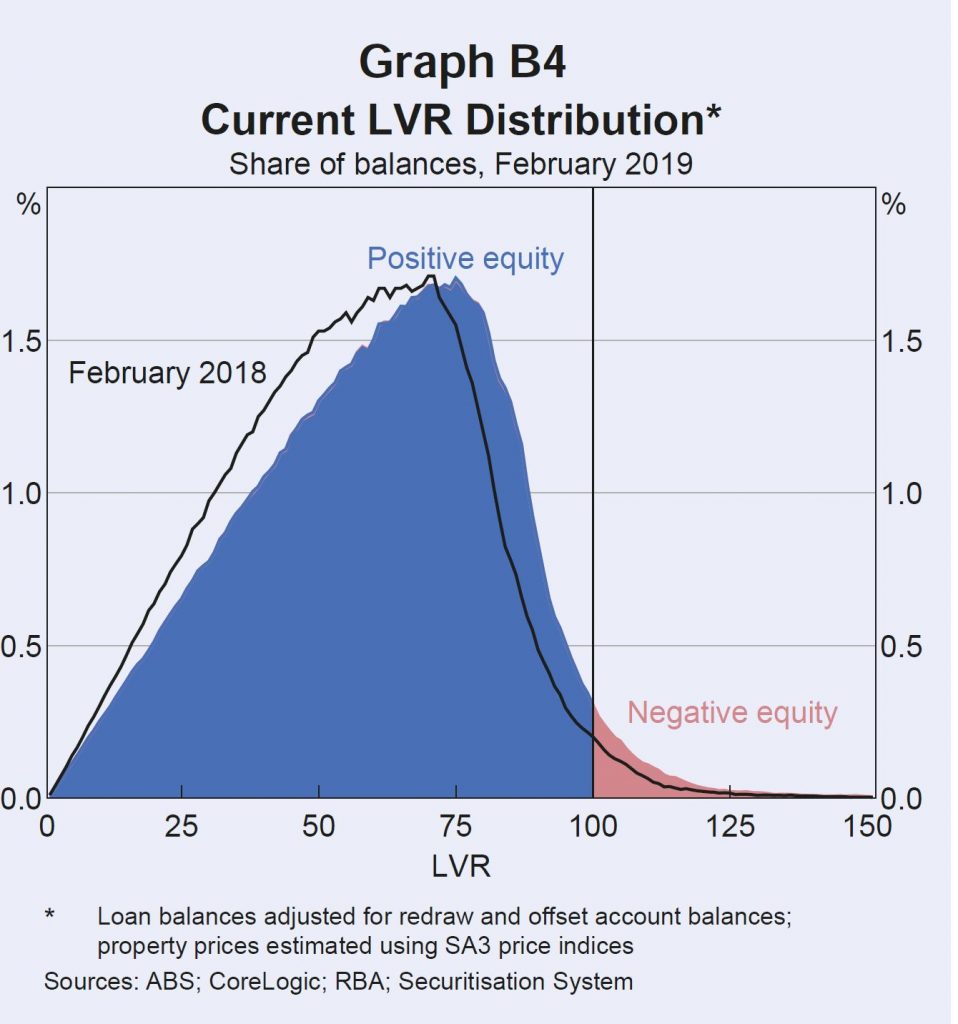

Estimating the share of borrowers with negative equity requires data on current loan balances and property values. The RBA’s Securitisation Dataset contains the most extensive and timely data on loan balances and purchase prices.

The Securitisation Dataset includes about one-quarter of the value of

all residential mortgages, or around 1.7 million mortgages.

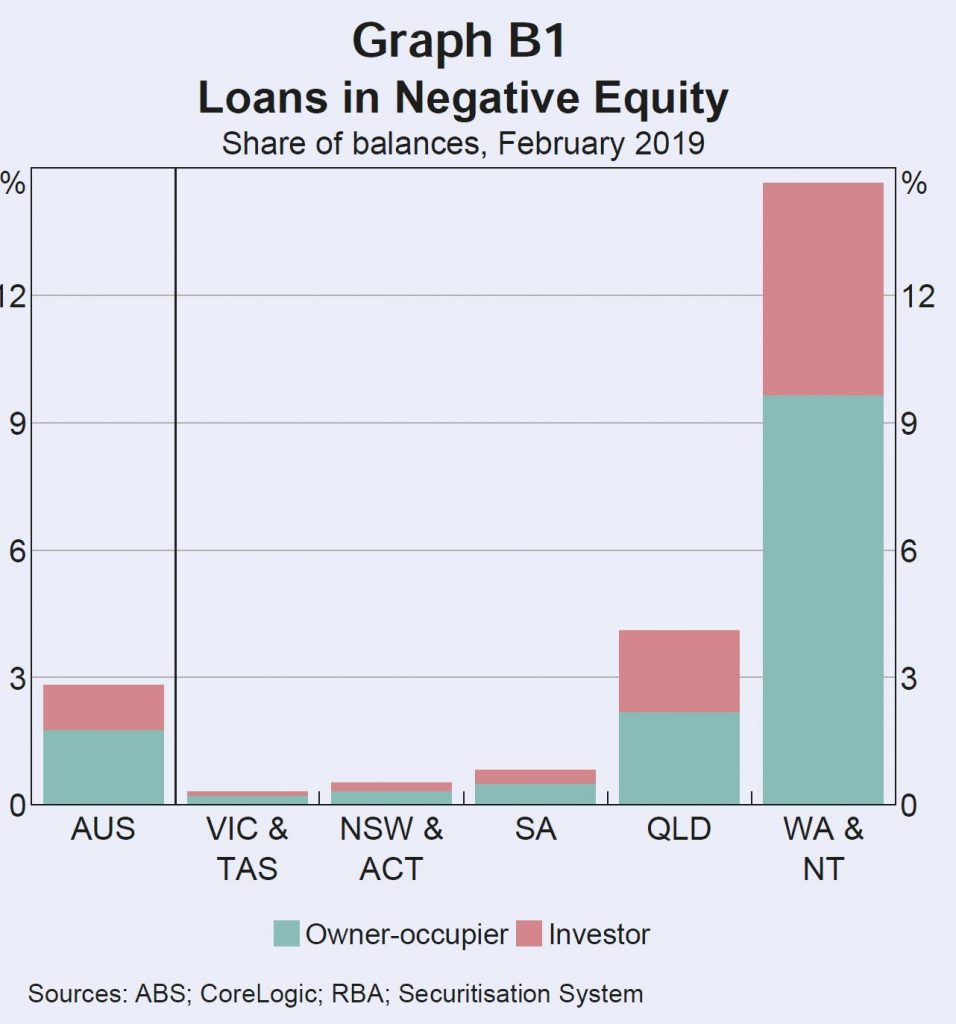

This data can be combined with regional data on housing price movements to estimate the share of loans that are currently in negative equity. This suggests that nationally, around 2¾ per cent of securitised loans by value are in negative equity (just over 2 per cent of borrowers). The highest rates of negative equity are in Western Australia, the Northern Territory and Queensland, where there have been large price falls in areas with high exposure to mining activity. Almost 60 per cent of loans in with negative equity are in Western Australia or the Northern Territory. Rates of negative equity in other states remain very low.

Estimates of negative equity from the Securitisation Dataset may, however, be under or overstated. They could be understated because securitised loans are skewed towards those with lower LVRs at origination. In contrast, the higher prevalence of newer loans in the dataset compared to the broader population of loans, and not being able to take into account capital improvements on values, will work in the other direction. Some private surveys estimate closer to 10 per cent of mortgage holders are in negative equity. However, these surveys are likely to be an overestimate for a number of reasons; for instance, by not accounting for offset account balances.

DFA Says: Of course DFA estimates 10% of households in negative equity, after taking offset balances into account, and also adding in the current forced sale value of the property and transaction costs.

Information from bank liaison and estimates based on 2017 data from the Household Incomes and Labour Dynamics of Australia (HILDA) survey suggest rates of negative equity are broadly in line with those from the Securitisation Dataset.

DFA Says: The HILDA data is at least 2 years old, so before the recent price falls – so this set will understate the current position.

The continuing low rates of negative equity outside the mining exposed regions reflect three main factors: the previous substantial increases in housing prices; the low share of housing loans written at high LVRs; and the fact that many households are ahead on their loans, having accumulated extra principal payments.

Housing prices in some areas of Sydney and Melbourne have fallen by upwards of 20 per cent from their peak in mid to late 2017. But only a small share of owners purchased at peak prices, and many others experienced price rises before property prices began to fall. Properties purchased in Sydney and Melbourne since prices peaked account for around 2 per cent of the national dwelling stock. Looking further back, properties purchased in these two cities since prices were last at current levels still only account for around 4½ per cent of the dwelling stock.