60% of small businesses cease trading within the first three years of operating. While not all close due to business failure, those that do tend to face an awkward insolvency regime that fails to meet their needs in the same way it does Network Ten.

The lack of an adequate insolvency regime for SMEs inhibits innovation and growth within our economy. It adds yet more complexity to the already difficult process of structuring a small business. Further, it inceases the cost of funding. Lenders know that recovering their money can be onerous if not impossible, so they impose higher costs of borrowing.

Australia’s insolvency regime

Australian insolvency law is divided into two streams, each governed by a separate piece of legislation.

The Corporations Act deals with the insolvency of incorporated organisations, and the Bankruptcy Act addresses the insolvency of people and unincorporated bodies (such as sole traders and partnerships).

Both schemes are aimed at providing an equal, fair and orderly process for the resolution of financial affairs. But a large part of the Corporations Act procedure has been developed with the complexity of a large corporation in mind. For example, there are extensive provisions that allow the resolution of disputes between creditors that are only likely to arise in well-resourced commercial entities.

The Bankruptcy Act, by contrast, takes account of the social and community dimensions of personal bankruptcy. This legislation seeks to supervise the activities of the bankrupted person for an extended period of time to encourage their rehabilitation.

SME’s awkwardly straddle the gap between these parallel pieces of legislation. Some SMEs are incorporated, and so fall under the Corporations Act. SMEs that are not incorporated are treated under the Bankruptcy Act as one aspect of the personal bankruptcy of the business owner. But of course, SMEs are neither people nor large corporations.

How insolvency works

Legislation governing corporate insolvency is founded on the assumption that there will be significant assets to be divided among many creditors. Broadly speaking, creditors are ranked and there are sophisticated and detailed provisions for their treatment. If Ten would have proceeded to liquidation, creditors would have been broadly grouped into three tiers and paid amounts well into the tens of millions.

One type of creditor is a “secured creditor”. Banks, for example, will often require that loans for the purchase of business equipment are secured against that equipment. In the event of default, the bank takes ownership of the equipment in place of the debt, if they can’t be paid out.

Unsecured creditors, on the other hand, do not have an “interest” over anything. If a company goes into liquidation, an unsecured creditor will only be paid if there are sufficient funds left after the secured creditors have been paid, and the cost of the process has been covered. There is no guarantee that unsecured creditors will be paid. Most often, they are only paid a portion of what they are owed.

The unique challenges of SME insolvency

When it comes to SMEs, there is little or no value available to lower-ranking, unsecured creditors in an SME insolvency estate. At the same time, higher-ranking, secured creditors tend to have effective methods of enforcing their interest outside the insolvency process. For instance they could individually sue the debtor to recover money owed. As a consequence, creditors are rarely interested in overseeing or pursing an SME insolvency process. This means the system is not often used and creditors with smaller claims go unpaid.

Even if creditors do want to use the insolvency process, it is likely the SME’s assets are insufficient to cover the cost of employing an insolvency practitioner and the required judicial oversight.

This problem is made worse because SMEs often wait too long to file for insolvency, owing to their lack of commercial experience or the social stigma of a failing business. Instead, debts continue to grow well beyond the point of insolvency, and responsibility falls on creditors to deal with the issue.

There are further difficulties depending on whether the SME is incorporated. Incorporated SMEs are frequently financed by a combination of corporate debt, taken on by the SME, and the personal debt of the business owner. This may result in complex and tedious dual insolvency proceedings: one for the bankruptcy of the owner and the other for the business.

Unincorporated SMEs, in turn, suffer from two stumbling blocks. First, the personal bankruptcy scheme has not been created to preserve the SME or encourage its turnaround. Second, personal bankruptcy proceedings require specific evidence that the person has committed an “act of bankruptcy”, such as not complying with the terms of a bankruptcy notice in the previous six months.

This hurdle makes the process far more time-consuming than the corporate scheme. It is also more difficult for creditors to succeed in recovering their investment and, by extension, prevents them from efficiently reallocating it. There is a real danger that this will deter creditors and raise the cost of capital at first instance.

What can we do about it?

The best way to meet the needs of SMEs would be to create a tailored scheme that sits between the corporate and personal regimes, as has been done in Japan and Korea. These regimes focus on speeding up the proceedings, moving the process out of court where possible and reducing the costs involved.

However, as the legislation in these two countries notes, there can be marked differences between small and medium-sized businesses that all fall under the SME banner. Therefore, what is needed is a flexible system made up of a core process, together with a large array of additional tools that may be invoked.

Designing such a scheme remains no easy feat. However, at its core, such a scheme would ideally allow business owners to commence the insolvency process and remain in control throughout. The process would sift through businesses to identify those that remain viable, and produce cost-effective means for their preservation.

Non-viable businesses would be swiftly disposed of, using pre-designed liquidation plans where possible and relying on court processes and professionals only where absolutely necessary. Creditors would therefore receive the highest return possible, and importantly, honest and cooperative business owners would be quickly freed from their failed business and able to return to economic life.

Authors: Kevin B Sobel-Read, Lecturer in Law and Anthropologist, University of Newcastle; Madeleine MacKenzie, Research assistant, Newcastle Law School, University of Newcastle

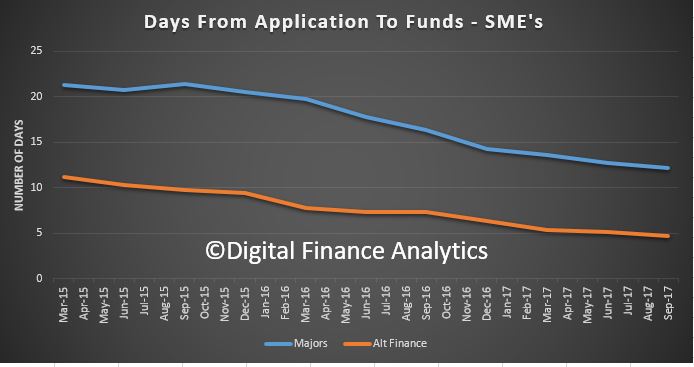

SME’s as they become more digitally aligned, also have a higher expectation of service, with firms saying that 4.8 days would be considered, on average, a reasonable time to time wait, as we discussed in the Disruption Index, a joint DFA and Moula initiative. The next edition will be out soon.

SME’s as they become more digitally aligned, also have a higher expectation of service, with firms saying that 4.8 days would be considered, on average, a reasonable time to time wait, as we discussed in the Disruption Index, a joint DFA and Moula initiative. The next edition will be out soon.