We just got the results of the Reserve Bank New Zealand Stress Tests, and this year the RBNZ undertook both its regular solvency stress test, challenging the resilience of banks’ capital to a severe downturn, and also put the spotlight on banks’ liquidity and funding resilience through a liquidity stress test ahead of next year’s review of the RBNZ’s liquidity policy. The solvency stress test included the five largest banks – ANZ NZ, ASB, BNZ Westpac and Kiwibank – and the liquidity stress test featured those five plus Co-operative Bank, Rabobank NZ, Heartland, SBS and TSB.

Large banks fared worse than the smaller banks. However, banks were able to identify actions that, if effective, would considerably improve the outcome.

Now the banks is at pains to highlight the stress test scenarios are hypothetical and don’t represent its view of the most likely future path for financial stability risks. And the RBNZ doesn’t release individual banks’ stress test results. Unlike the results from the Federal Reserve in the US, where individual banks results are disclosed. In this respect New Zealand is following the opaque strategy APRA also executes, which is a pity. Not least because in New Zealand, Bank Deposit Bail-In is a thing via the Open Banking Resolution, and the RBNZ has warned people to do due diligence on the individual banks – so why don’t they disclose the detail we ask?

Go to the Walk The World Universe at https://walktheworld.com.au/

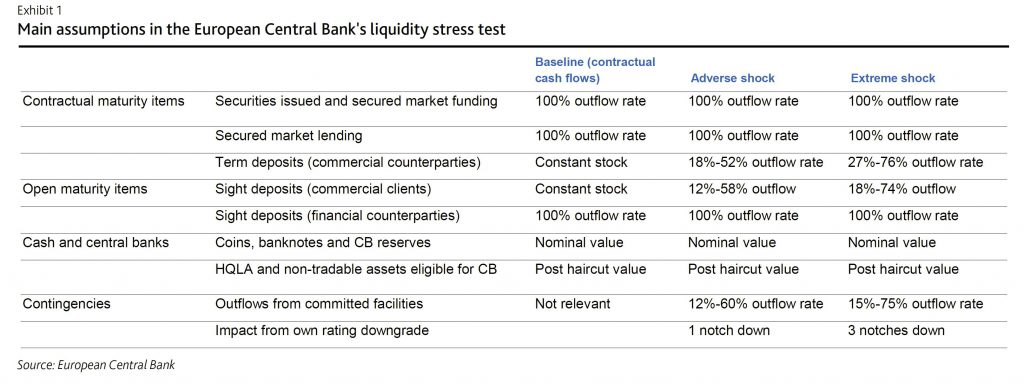

On 7 October, the European Central Bank (ECB) published its liquidity stress test results for 103 euro area banks. ECB’s increased focus on stressed liquidity is credit positive for these banks. As the liquidity coverage ratio (LCR) has a very short 30-day horizon, ECB looking at liquidity stresses lasting six months provides a much more meaningful measure. The test results will be used to strengthen the liquidity risk assessment in the 2019 Supervisory Review and Evaluation Process (SREP), but will not have a direct effect on capital requirements. Via Moody’s.

Overall, the stress test highlights a marked variation in euro area banks’ ability to cope with severe liquidity shocks. It demonstrated that there are pronounced pockets of vulnerability, with 75% of banks being unable to cope with a severe stress that lasted six months. While individual bank results were not released, the ECB stated that large universal banks and G-SIBs were the most exposed.

The ECB focused on idiosyncratic (rather than systemwide) shocks calibrated on the basis of recent liquidity crises. The effect was measured in terms of survival horizons by looking at banks’ cumulative cash flows and available counterbalancing capacity (i.e. the liquidity the banks can generate based on available collateral) in three scenarios. The scenarios include a baseline, in which the bank is no longer able to tap the wholesale funding market; an adverse shock, which adds a limited deposit outflow, limited withdrawals of committed lines, and a one-notch rating downgrade; and an extreme shock scenario, which adds severe deposit run-offs, pronounced withdrawals of committed lines, and a three-notch rating downgrade.

Overall, the banks’ reported median survival period was 176 days, or almost six months, under the adverse shock scenario and 122 days (just over four months) in the extreme shock scenario. Only 25% of the banks have liquidity buffers that would withstand the extreme shock scenario for six months or longer, and the majority (75%) have a survival period that is shorter than six months. Survival periods varied markedly, with differences driven mainly by the banks’ funding mix.

There are significant pockets of vulnerability. Although results for individual banks have not been disclosed, four banks from different jurisdictions and with different business models have a survival period of less than six months even in the baseline scenario, which we consider very weak, and 11 banks have a survival period of less than two months under the extreme shock scenario. Universal banks and global systemically important banks (G-SIBs) are also harder hit by the stress scenarios.

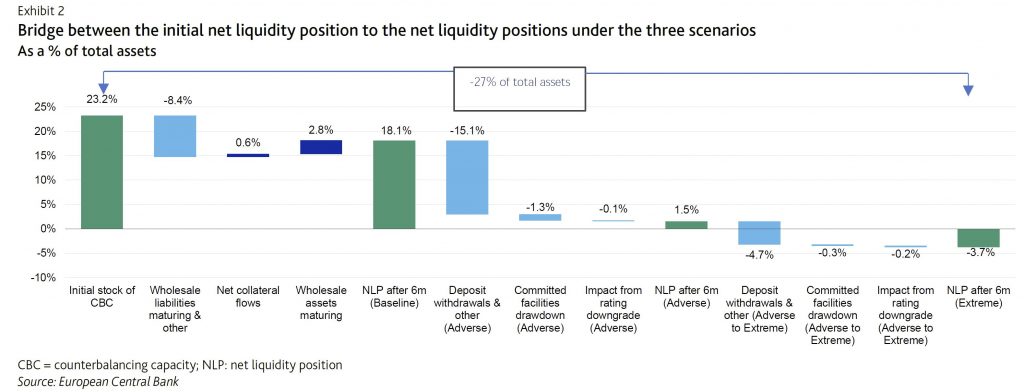

Exhibit 2 shows the (simple average) effect of the three scenarios compared to the initial stock of net liquidity, with overall outflows equivalent to around 27% of total assets under the extreme scenario. The key effect under the baseline scenario is caused by the lack of access to wholesale markets, followed by deposit withdrawals under the adverse and extreme scenarios.

Although any stress test must be based on assumptions and scenarios, we note that past liquidity crises (according to the ECB’s stress test announcement in February 2019) lasted between four and five months on average. However, 43% of the real life stresses lasted longer than six months. With a median survival horizon of a little longer than four months, many banks may have a survival horizon that may prove short, particularly in a bank-specific crisis with more limited opportunities for the central bank to intervene with extraordinary measures. It also points to the need for banks to mobilize additional non-tradable collateral in addition to the readily available liquidity buffers, which is one of the areas where the ECB observed scope for improvement.

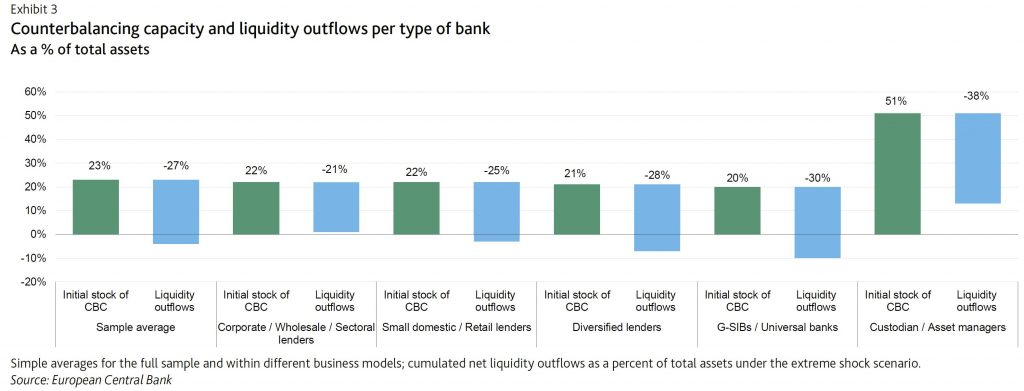

Universal banks and G-SIBs, which are generally more reliant on less stable deposits and wholesale funding, despite having large liquidity buffers, were the hardest hit by the stress scenarios. Their median survival in the adverse shock scenario was 126 days, and 80 days in the extreme shock scenario.

Small domestic and retail lenders, which generally benefit from more stable deposits and lower reliance on wholesale funding, were relatively less affected. Their median survival was more than 180 days under the adverse shock scenario and was 140 days under the extreme shock scenario, indicating that they would maintain positive liquidity for significantly longer than the universal banks and G-SIBs. The results are in line with our assessment where large banks often have weaker funding and liquidity assessments compared to smaller domestic retail banks. Exhibit 3 shows the counterbalancing capacity and the liquidity outflows per type of bank, with G-SIBs/universal banks significantly more negatively affected compared to small domestic/retail lenders.

The stress test also identified vulnerabilities related to cash flows in foreign currencies, where survival periods generally are shorter than those reported at consolidated level. Whereas the median survival period in EUR was 125 days, the median survival periods in USD and GBP were 57 and 53 days, respectively. This suggests that the lessons during the global financial crisis have not been fully learnt. In addition, some banks’ collateral management practices, which are essential in the event of a liquidity crisis, also need improvement.

The ECB also cautioned that banks may underestimate the negative effect that a credit rating downgrade could trigger. Previous liquidity crises have shown that deteriorations can go quickly and fast.

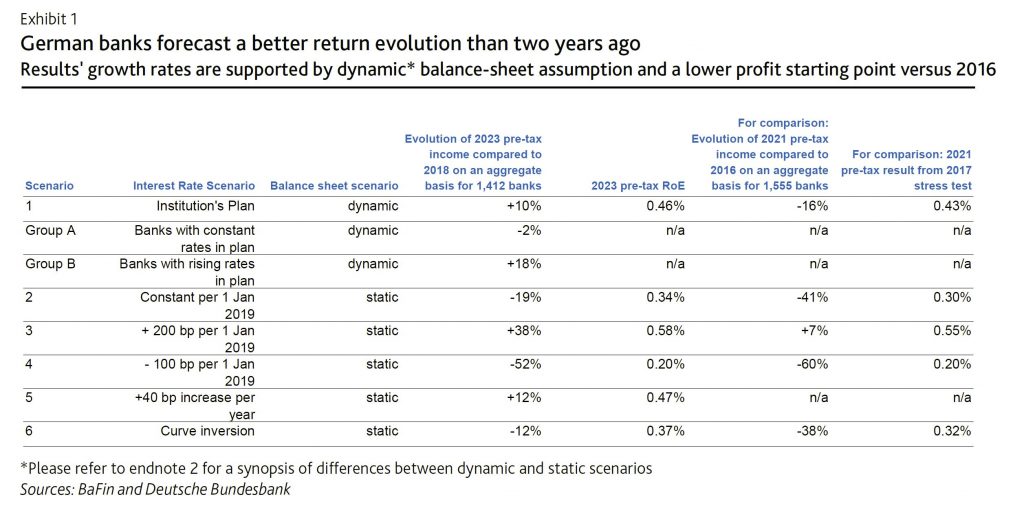

Moody says that on 23 September, German bank regulator Bundesanstalt fuer Finanzdienstleistungsaufsicht (BaFin) and the German central bank, the Deutsche Bundesbank, published the results of their biennial stress test applied to 1,412 small and midsize German banks that fall under BaFin’s direct oversight. The tested banks represent 38% of German banking system assets. The stress test scenario was designed well ahead of the recent decision of the European Central Bank (ECB) to lower the rate on its deposit facility to a negative 0.50%.

Instead, the scenario tests the banks for a severe economic downturn combined with rising interest rates and credit spreads. The capital buffers of the tested German banks remained robust under stress with a Common Equity Tier 1 ratio of 13.0% on average, down 3.5 percentage points from the year-end 2018 starting point of 16.5%. The drawback of this scenario is that it does not address the more plausible future environment of weakening economic growth combined with extended low interest rates.

A return on equity

survey that accompanied the stress test, however, was more revealing. The

survey required the banks to contrast their five-year base-case assumptions for

return on equity evolution (from 2018 to 2023) with five defined interest-rate

scenarios.

The closest interest

rate scenario to current market expectations simulates the present ultra-low

interest rates lasting throughout the five years. In terms of potential to

impair the banks’ profitability, it is also the most severe. Based on the

assumption of a static balance sheet,2 banks would see their profitability

falling by more than 50%. The high probability of this interest rate scenario

unfolding suggests that the banks need to materially increase their focus on

cost management to protect their credit profiles.

Unchanged rate environment is the most severe scenario. The survey results show improved forecasts for base-case profitability at the end of the five-year horizon against the same survey two years ago (2016-21). In part, this reflects moderate progress in trimming high cost bases. The German regulators cautioned, however, that the improvement is substantially driven by the fact that about half of the participating banks (Group B) assumed a rise in interest rates over the five-year horizon from year-end 2018 levels.

They added that even the

flat interest rate assumption employed by the other half (Group A) based on

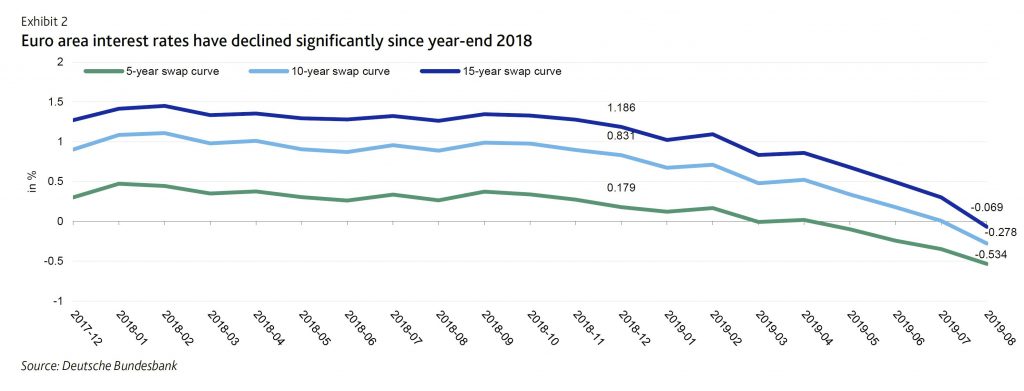

year-end 2018 interest rates has become an optimistic scenario. Exhibit 2 shows

that long-term interest rates have in fact declined by around 100 basis points

since the end of 2018, broadly in line with Scenario 4 (the most severe

scenario), with an even more pronounced decline in longer-term rates.

The banks’ simulated results are better under the assumption of dynamic balance sheets. This is because active management intervention to counteract interest rate-driven income declines remains an important lever to reduce the profitability pressure on German banks. Close to half the bank managers surveyed indicated that under Scenario 4, an interest rate drop of 100 basis points, they would consider applying negative interest rates to the deposits of retail clients. Less than one third excluded this for retail and corporate clients under this scenario.

Managers of banks that participated in this year’s stress test expect a combination of weaker deposit margins and a reduced contribution from maturity transformation business to outweigh moderately improving lending margins. This was the case even in Scenario 1 (based on year-end 2018 institutions’ plans with a dynamic balance sheet). It illustrates that banks with lower dependence on maturity transformation results (i.e. with higher fees and commissions income) and with more flexible funding options are better positioned to defend their profitability during a period of extended low interest rates.

As in prior years, the

stress test exercise excluded the 21 large German banking groups that are under

the direct supervision of the ECB.

We believe that, on

aggregate, these larger banks benefit from their access to more diversified

funding sources.

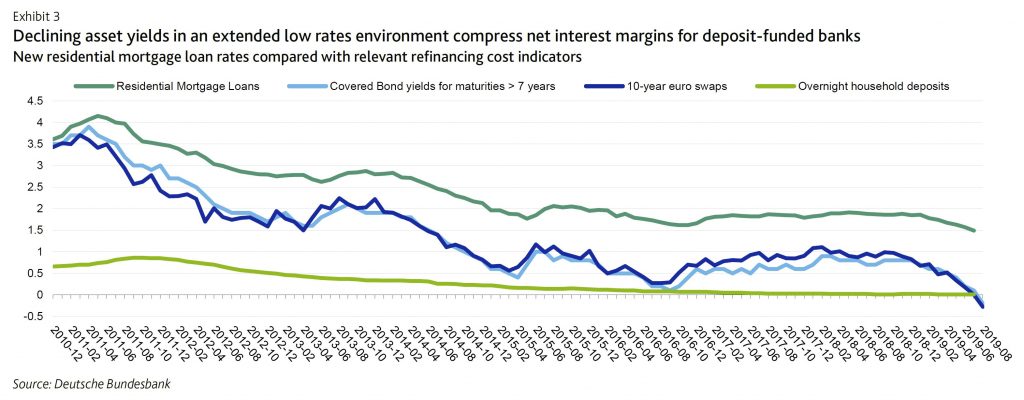

The low interest rate

environment has particularly compressed the net interest margin on newly

originated loans if these new loans have been financed with retail deposits.

This is because banks have so far felt unable to charge for retail deposits and

these deposits have effectively been floored at 0% interest, even as lending

rates have continued to fall.

In contrast, the use of

secured or unsecured market funding sources (where costs have continued to

fall) available to the larger banks, enables them to substantially offset the

decline in interest rates earned on their newly originated loans. This is

illustrated in Exhibit 3 using residential mortgage loans as an example. On the

other hand, despite economies of scale, large banks’ cost efficiency materially

lags the efficiency of smaller German banks – and in turn the efficiency of

small German banks lags international peers.

But, the Reserve Bank of Australia has pointed to Australia’s high debt levels as a factor in its decision making for the cash rate, fearing that it will make the economy more vulnerable to shocks.

Just remember this in the context of APRA reducing the lending standards recently! And in APRA’s Corporate plan Australia’s banking watchdog will stress test the country’s banks every year, instead of the current three-year cycle, ramping up oversight of a sector that has been marred by misconduct.

In the most recent series of stress tests in 2017, all 13 of the country’s largest banks passed the “severe but plausible” scenarios applied by the regulator, despite projected losses of about A$40 billion in home loans alone.

The RBA published its four-year corporate plan on Friday, pointing to the banks’ exposure to housing loans and cyber security in financial institutions as the largest risks to the country’s financial stability.

In Australia, wages growth is low, reflecting spare capacity in the labour market as well as some structural factors.

The

central bank expects the unemployment rate will remain around 5.25 per

cent for a time, before declining to around 5 per cent in 2021, with

wages growth expected to remain stable and then increase modestly from

2020.

Consumer price inflation is forecast to increase to be a

little under 2 per cent over 2020 and a little above 2 per cent over

2021.

The

RBA noted over the next four years, “movements in asset values and

leverage may be more important for economic developments than in the

past given the already high levels of debt on household balance sheets.

“Especially

in the context of weak growth in household income, high debt levels

could complicate future monetary policy decisions by making the economy

less resilient to shocks,” the RBA said.

The central bank noted

policymakers in the US and other countries employing quantitative easing

as a result of intensifying trade and technology disputes.

Globally,

the RBA reported, labour market conditions remain tight in major

advanced economies, although unemployment rates are at multidecade lows.

“Global

interest rates and measures of financial market volatility both remain

low compared with historical experience,” the RBA said in its corporate

plan.

“The future path of global monetary policy and financial

conditions more generally remain subject to substantial uncertainty.

These global factors significantly influence the environment in which

monetary policy in Australia is conducted,” the RBA said.

Last

week, RBA governor Philip Lowe reflected on the RBA’s decision on the

cash rate during an address to Jackson Hole Symposium in Wyoming.

“So

the question the Reserve Bank Board often asks itself in making its

interest rate decision is how our decision can best contribute to the

welfare of the Australian people,” Mr Lowe said.

“Keeping

inflation close to target is part of the answer, but it is not the full

answer. Given the uncertainties we face, it is appropriate that we have a

degree of flexibility, but when we use this flexibility we need to

explain why we are doing so and how our decisions are consistent with

our mandate.”

He said a challenge the central bank is facing is elevated expectations that monetary policy can deliver economic prosperity.

“The

reality is more complicated than this, not least because weak growth in

output and incomes is largely reflecting structural factors,” Mr Lowe

commented.

“Another element of the reality we face is that

monetary policy is just one of the levers that are potentially available

for managing the economy. And, arguably, given the challenges we face

at the moment, it is not the best lever.”

The RBA is due to deliver its cash rate decision tomorrow.

On 21 June, the US Federal Reserve (Fed) published the results of the 2019 Dodd-Frank Act stress test (DFAST) for 18 of the largest US banking groups, all of which exceeded the required minimum capital and leverage ratios under the Fed’s severely adverse stress scenario; via Moodys’.

These results are credit positive for the banks because they show that the firms are able to withstand severe stress while continuing to lend to the economy. In addition, most firms achieved a wider capital buffer above the required minimum than in last year’s test, indicating a higher degree of resilience to stress. The 2019 results support our view of the sector’s good capitalization and benefit banks’ creditors.

The median stressed capital buffer above the required Common Equity Tier 1 (CET1) ratio increased to 5.1% from 3.5% last year, a substantial change. However, the 18 firms participating in 2019 were far fewer than the 35 that participated in 2018, helping lift the results this year. This is because passage of the Economic Growth, Regulatory Relief, and Consumer Protection Act in May 2018 resulted in an extension of the stress test cycle to two years for 17 large and non-complex US bank holding companies, generally those with $100-$250 billion of consolidated assets, which pose less systemic risk.

This is the fifth consecutive year that all tested firms exceeded the Fed test’s minimum CET1 capital requirement. As in prior years, the banks’ Tier 1 leverage and supplementary leverage ratios had the slimmest buffers of 2.8% and 2.4%, respectively, above the required minimums as measured by the aggregate.

Under DFAST, the Fed applies three scenarios – baseline, adverse and severely adverse – which provide a forward-looking assessment of capital sufficiency using standard assumptions across all firms. The Fed uses a standardized set of capital action assumptions, including common dividend payments at the same rate as the previous year and no share repurchases. In this report, we focus on the severely adverse scenario, which is characterized by a severe global recession accompanied by a period of heightened stress in commercial real estate markets and corporate debt markets.

This year’s severely adverse scenario incorporates a more pronounced economic recession and a greater increase in US unemployment than the 2018 scenario. The 2019 test assumes an 8% peak-to-trough decline in US real gross domestic product compared with 7.5% last year and a peak unemployment rate of 10% that, although the same as last year, equates to a greater shock because the starting point is now lower (the rise to peak is now 6.2% compared with 5.9% last year).

The severely adverse scenario also includes some assumptions that are milder than last year: housing prices drop 25% and commercial real estate prices drop 35%, compared with 30% and 40% last year; equity prices drop 50% compared with 65% last year; and the peak investment grade credit spread is 550 basis points (bp), down from 575 bp last year. We consider this exercise a robust health check of these banks’ capital resilience.

Finally, the three-month and 10-year Treasury yields both fall in this year’s severely adverse scenario, resulting in a mild steepening of the yield curve because the 10-year yield falls by less. As a result banks’ net interest income faces greater stress than in last year’s scenario, which assumed unchanged treasury yields and a much steeper yield curve.

The Federal Reserve Board has released the scenarios banks and supervisors will use for the 2019 Comprehensive Capital Analysis and Review (CCAR) and Dodd-Frank Act stress test exercises. The extreme scenario assumes a short sharp fall, in 2020.

Whilst its a theoretical exercise, kudos to the FED for making public the inputs, and of course they will publish results, to an individual firm level later (unlike or opaque APRA tests, where disclosure remains appalling).

Stress tests, by ensuring that banks have adequate capital to absorb

losses, help make sure that they will be able to lend to households and

businesses even in a severe recession. CCAR evaluates the capital

planning processes and capital adequacy of the largest U.S. bank holding

companies, and large U.S. operations of foreign firms, using their

planned capital distributions, such as dividend payments and share

buybacks and issuances. The Dodd-Frank Act stress tests also help ensure

that banks can continue to lend during times of stress, but use

standard capital distribution assumptions for all firms. Both

assessments only apply to domestic bank holding companies and foreign

bank intermediate holding companies with more than $100 billion in total

consolidated assets.

The stress tests run by the firms and the Board apply three

hypothetical scenarios: baseline, adverse, and severely adverse. For the

2019 cycle, the severely adverse scenario features a severe global

recession in which the U.S. unemployment rate rises by more than 6

percentage points to 10 percent. In keeping with the Board’s public

framework for scenario design, a stronger economy with a lower starting

point for the unemployment rate results in a tougher scenario. The

severely adverse scenario also includes elevated stress in corporate

loan and commercial real estate markets.

“The hypothetical scenario features the largest unemployment rate

change to date,” Vice Chairman for Supervision Randal K. Quarles said.

“We are confident this scenario will effectively test the resiliency of

the nation’s largest banks.”

The adverse scenario features a moderate recession in the United

States, as well as weakening economic activity across all countries

included in the scenario.

The adverse and severely adverse scenarios describe hypothetical sets

of events designed to assess the strength of banking organizations and

their resilience. They are not forecasts. The baseline scenario is in

line with average projections from surveys of economic forecasters. It

does not represent the forecast of the Federal Reserve.

Each scenario includes 28 variables–such as gross domestic product,

the unemployment rate, stock market prices, and interest rates–covering

domestic and international economic activity. Along with the variables,

the Board is publishing a narrative description of the scenarios that

also highlights changes from last year.

Firms with large trading operations will be required to factor in a

global market shock component as part of their scenarios. Additionally,

firms with substantial trading or processing operations will be required

to incorporate a counterparty default scenario component.

Banks are required to submit their capital plans and the results of

their own stress tests to the Federal Reserve by April 5, 2019. The

Federal Reserve will announce the results of its supervisory stress

tests by June 30, 2019. The instructions for this year’s CCAR will be

released at a later date.

Also on Tuesday, the Board announced that it will be providing relief

to less-complex firms from stress testing requirements and CCAR by

effectively moving the firms to an extended stress test cycle for this

year. The relief applies to firms generally with total consolidated

assets between $100 billion and $250 billion.

As a result, these less-complex firms will not be subject to a

supervisory stress test during the 2019 cycle and their capital

distributions for this year will be largely based on the results from

the 2018 supervisory stress test. At a later date, the Board will

propose for notice and comment a final capital distribution method for

firms on an extended stress test cycle in future years.

On 9 January, Moody’s says, the Federal Reserve Board (Fed) proposed revisions to company-run stress testing requirements for Fed-regulated US banks to conform with the Economic Growth, Regulatory Relief, and Consumer Protection Act (the EGRRCPA), which became law in May 2018.

Among the revisions, which are similar to those proposed in December 2018 by the Office of the Comptroller of the Currency (OCC) and the Federal Deposit Insurance Corp. (FDIC), is a proposal that would eliminate the requirement for company-run stress tests at most bank subsidiaries with total consolidated assets of less than $250 billion. The proposed changes would be credit negative for affected US banks because they would ease the minimum requirements for stress testing at the subsidiary level.

The proposed revisions would also require company-run stress tests once every other year instead of annually at most banks with more than $250 billion in total assets that are not subsidiaries of systemically important bank holding companies. Additionally, the proposal would eliminate the hypothetical adverse scenario from all company-run stress tests and from the Fed’s own supervisory stress tests, commonly known as the Dodd-Frank Stress Test (DFAST) and the Comprehensive Capital Analysis and Review (CCAR); the baseline and severely adverse scenarios would remain.

The proposed changes aim to implement EGRRCPA. As such, we expect that they will be adopted with minimal revisions. In late December 2018, the FDIC and OCC published similar proposals governing the banks they regulate. The stress testing requirements imposed on US banks over the past decade have helped improve US banks’ risk management practices and have led banks to incorporate risk management considerations more fully into both their strategic planning and daily decision making. Without periodic stress tests, these US banks may have more flexibility to reduce their capital cushions, making them more vulnerable in an economic

downturn.

On 31 October 2018, the Fed announced a similar proposal for the company-run stress tests conducted by bank holding companies as a part of a broader proposal to tailor its enhanced supervisory framework for large bank holding companies. Positively, the Fed’s 31 October 2018 proposal would still subject bank holding companies with total assets of $100-$250 billion to supervisory stress testing at least every two years and would still require them to submit annual capital plans to the Fed, even though the latest proposal would no longer require their bank subsidiaries to conduct their own company-run stress tests. Also, supervisory stress testing for larger holding companies would continue to be conducted annually. Continued supervisory stress testing should limit any potential reduction

in capital cushions at those bank holding companies.

We believe that some midsize banks will continue to use company-run stress testing in some form, but more tailored to their own needs and assumptions. Nevertheless, this may not be the view of all banks, particularly those for which stress testing has not been integrated with risk management. Additionally, smaller banks may have resource constraints.

The reduced frequency of mandated company-run stress testing for bank subsidiaries with assets above $250 billion that are not subsidiaries of systemically important bank holding companies is also credit negative, although not to the same extent as the elimination of the requirement for the midsize banks. The longer time between bank management’s reviews of stress test results introduces a higher probability of changing economic conditions that could leave a firm with an insufficient capital cushion.

The Fed’s proposal also would eliminate the hypothetical adverse scenario from company-run stress tests and the Fed’s supervisory stress tests. The market has focused on the severely adverse scenario, which is harsher than the adverse scenario so this proposed change is unlikely to have significant consequence.

APRA has released some information relating to their 2017 stress tests in their “APRA Insight Issue Three 2018“. We discussed the results in a recent Adams/North video. We were not impressed!

This is what APRA has now released. Compared with the bank by bank data the FED releases, its VERY high level!

Stress testing plays an important role for both banks and APRA in testing financial resilience and assessing prudential risks. This article provides an overview of APRA’s approach to stress testing, with insights into how APRA developed the 2017 Authorised Deposit-taking Institution (ADI) Industry Stress Test. This builds on the recent speech by APRA Chairman Wayne Byres, “Preparing for a rainy day” (July 2018), which outlined the results from the 2017 exercise.

Why stress test

The aim of stress testing is, broadly, to test the resilience of financial institutions to adverse conditions, including severe but plausible scenarios that may threaten their viability. The estimation of the impact of adverse scenarios on an entity’s balance sheet provides insights into possible vulnerabilities and supports an assessment of financial resilience. It can be a key input into capital planning and the setting of targets, and in developing potential actions that could be taken to respond and rebuild resilience if needed.

Stress tests are particularly important for the Australian banking system, given the lack of significant prolonged economic stress since the early 1990s. As a forward-looking analytical tool, stress testing can help to improve understanding of the impact of current and emerging risks if a downturn were to occur. Stress tests provide an indication, however, rather than a definitive answer on the impact of adverse conditions, and the results will always reflect the inherent uncertainty that exists in any scenario.

Scenarios – the starting point

The starting point in developing a stress test is to design the scenarios. This is the foundation of the exercise, and it is important that scenarios are calibrated effectively and are well targeted. For industry stress tests, APRA collaborates with both the Reserve Bank of Australia (RBA) and Reserve Bank of New Zealand (RBNZ) on the design of scenarios and the economic parameters that define them. In 2017, APRA also engaged with the Australian Securities and Investments Commission (ASIC) in the design of the operational risk scenario.

Scenarios should be aligned to the purpose of the exercise. At a high level, these are guided within APRA by several objectives – namely to:

assess system-wide and entity-specific resilience to severe but plausible scenarios;

improve stress testing capabilities across the industry; and

support the identification and assessment of core and emerging risks.

In line with these objectives, APRA developed two scenarios for the 2017 industry stress test. The first was a macroeconomic scenario with a China-led recession in Australia and New Zealand. This was considered the most severe but plausible adverse economic scenario for the banking system at the time.[1] In this scenario, there was assumed to be a fall in Australian GDP of 4 per cent, while house prices declined 35 per cent nationally over three years. The chart below provides an indication of the severity of the scenario: it shows that the assumed peak unemployment rate in the scenario was similar to the 1990s recession in Australia, the United States’ experience in the global financial crisis (GFC), as well as recent overseas regulatory stress tests.

Chart 1: International comparison: Peak unemployment rate

The second scenario involved the same macroeconomic parameters, with an additional operational risk event added. This was designed to test bank resilience beyond traditional economic risks and to consider other vulnerabilities. In this operational risk scenario, APRA asked the participating banks to identify a material operational risk event involving conduct risk and/or mis-selling in the origination of residential mortgages.[2]

The banks chosen for the exercise were selected based primarily on scale, enabling a clear system-wide view to be generated. The 2017 stress test covered 13 of the largest banks with aggregate assets of nearly 90 per cent of the system, as well as the leading lenders mortgage insurers. It included both the major banks and smaller entities that have a significant presence in particular regions or asset classes.

The testing process

The 2017 stress test was run in two phases. In the first phase, banks generated results using their own stress testing methodologies and models.[3] The results of this phase varied by differences in the risk characteristics of each bank, as well as by how they interpreted and modelled the scenarios.

In the second phase, APRA provided more prescription with specified risk estimates for loan portfolios and other assumptions. This enabled greater comparability across the banks and more consistency in the results. The APRA estimates were developed based on the banks’ results from the first phase, APRA’s own internal modelling, historic and peer stress testing benchmarks, internal and external research and expert judgement.

The estimates were also differentiated based on inherent risk characteristics. For example, riskier interest-only loans were assumed to be more likely to default and losses were estimated to be greater for loans with higher Loan to Valuation Ratios (“LVRs”). For the operational risk scenario, APRA defined key elements and estimates to be applied by the banks, based on research of overseas experience as benchmarks for potential impacts.

Interpreting the results

The table below summarises some key results from the macroeconomic scenario. As important as the quantified outcomes are the lessons learned and implications of the exercise. Stress testing should not be an academic exercise, but should be used to inform assessments of resilience, risks and capacity to respond to stress.

In analysing the results, APRA assessed not only the impact on capital, but also the effects on profitability and loan portfolios. The differences between phase 1 (based on bank’s own modelling) and phase 2 (based on APRA risk estimates) can also shed light on bank stress testing modelling capabilities.

Macroeconomic scenario – aggregate results

Phase 1

Phase 2

Peak to trough decline in Common Equity Tier 1 capital

-2.87%

-3.21%

Peak to trough decline in Return on Equity

-9.86%

-12.05%

Peak credit loss rate[4]

0.81%

0.90%

Macroeconomic scenario

Given the design of the scenario, the impact on the participating banks was material. The results show that in this scenario the decline in profitability was severe and occurred quickly. Return on equity (ROE) in aggregate fell materially in the first two years before recovering after year three. The impact on profitability led to a significant fall in capital in both phases, as shown in Chart 3. There was, however, a wide range in results across banks in both phases.[5]

The losses were driven by bad debts in residential mortgage lending, corporate lending and other credit portfolios, as well as lower net interest income and losses on large single counterparties. Across the mortgages portfolios of the banks, aggregate losses were similar in both phases and although the mortgage portfolio contributed the largest aggregate loss, the loss rate was lower than business lending and other consumer lending portfolios.[6] The banks also modelled the impact of the scenario on liquidity and funding positions; most banks were able to maintain their liquidity with a liquidity coverage ratio (LCRs) above 100 per cent (or initiated strategies to restore their LCR within a reasonable timeframe).

Chart 4: Aggregate cumulative credit losses

Operational risk scenario

In the second scenario, the impact of the operational risk event led to a more severe capital outcome, as shown in Chart 5. The operational risk events modelled by the banks in Phase 1 represented a wide range of potential risks, including broker fraud, inappropriate product design and sales practices, inappropriate verification and documentation, overstatement of valuation errors at origination, and serviceability errors. The impact of the operational risk event in Phase 2 based on APRA-defined assumptions was, however, more severe.

Following industry stress test exercises, APRA provides participating entities with formal feedback. In the 2017 stress test, APRA noted the importance of ongoing improvements in modelling capabilities and developing better internal model governance and discussions on results. In practice, a stress event is unlikely to play out exactly as designed and simulated in hypothetical scenarios, reinforcing the need to continue to stress test and enhance stress testing capabilities.

In APRA’s view, the results of the 2017 exercise provide a degree of reassurance: ADIs remained above regulatory minimum levels in what was a very severe stress scenario. In addition, the results were presented before taking into consideration management actions that would likely be taken to rebuild capital and respond to risks in the scenarios.[7] The impact on profitability, loan portfolios and capital would, however, be substantial: this underlines the importance of maintaining strong oversight and prudent risk settings, unquestionably strong capital and ongoing crisis readiness.

Footnotes

The RBA’s Financial Stability Review in October 2016 highlighted the risks posed by high and rising levels of debt in China, at a time of slowing growth and signs of excess capacity.

Overseas experience in the GFC has highlighted that operational risk events can impact the financial system alongside an economic downturn. For example, in the US, there was a significant impact from sub-prime mortgage lending, while in the UK, there was additional stress related to the mis-selling of payment protection insurance.

In order to ensure consistency for the exercise, APRA provided guidance and templates for results.

This represents the credit loss rate in the most severe year of the stress. Aggregate losses over the duration of the stress period were higher.

The range presented in the charts is the interquartile range (middle 50 per cent of entities).

Banks determine credit losses by calculating the likelihood of the loans defaulting (“probability of default”) and then the actual loss on the defaulted loans (“loss given default”) which is then applied to the stressed value of the asset. For mortgages, insurance on higher LVR loans helps to mitigates losses.

These actions include raising equity, loan repricing, cost cutting, tightening lending standards and balance sheet measures. Within this set, the cornerstone action was typically equity raisings, as a relatively quick step. In the operational risk scenario, the participating banks raised around $40bn in equity, almost twice the level as during the GFC. The assumption that banks were last to market challenged thinking around the potential capacity and pricing implications.