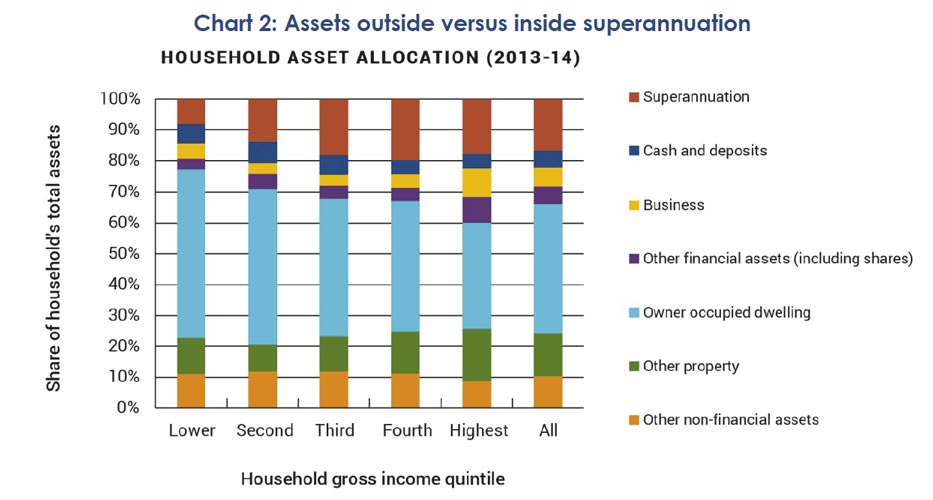

Bear in mind also that superannuation savings is a relatively small proportion of total household assets – property being the largest element (thanks to the massive rise in value), according to the ABS.

The Government agreed to support the development of more efficient retirement income products and to facilitate trustees offering these products to members, in response to the Financial System Inquiry.

These products were labelled by the Murray Inquiry (Financial System Inquiry) as ‘Comprehensive Income Products for Retirement’, or CIPRs; however the Government proposes to use ‘MyRetirement products’ as a more consumer‑friendly and meaningful label.

The MyRetirement framework is intended to increase individuals’ standard of living in retirement, increase the range of retirement income products available, and empower trustees to provide members with an easier transition into retirement. Through this framework, the Government is aiming to increase the efficiency of the superannuation system so it can better achieve the proposed objective of superannuation, which is to provide income in retirement to substitute or supplement the Age Pension.

The Government has released, for public consultation, a discussion paper that explores the key issues in developing the framework for Comprehensive Income Products for Retirement, or MyRetirement products. Views are sought from interested stakeholders, in particular on:

- the structure and minimum requirements of these products;

- the framework for regulating these products; and

- the offering of these products.

The Government is committed to consulting extensively with stakeholders on this framework.

A public consultation process will run from 15 December 2016 to 28 April 2017.

The discussion paper covers a lot of ground, in this complex policy area.

WHAT IS A COMPREHENSIVE INCOME PRODUCT FOR RETIREMENT (CIPR)?

It is envisaged that a CIPR would be a mass-customised, composite retirement income product (for example, combining a pooled product with a product that provides flexibility), which trustees could choose to offer to their members at retirement.

The offering of a CIPR would provide an ‘anchor’ to help guide individuals in their retirement income decision-making. Importantly, an individual would have the freedom to choose whether to take up the CIPR or take their retirement income benefits in another way.

Under the CIPRs framework although different product providers (for example, life insurance companies) could administer the underlying component products, trustees would offer a single income stream to their members.

If a trustee designs a product that: meets the proposed minimum product requirements; is in the best interests of the majority of their members; and offers the product in line with the offering requirements, it is proposed that the trustee will receive a safe harbour. The safe harbour would protect the trustee from a claim on the basis that the CIPR was not in the best interest of an individual member. This is intended to provide legal certainty for trustees in undertaking the CIPR offering.

PROPOSED STRUCTURE AND MINIMUM PRODUCT REQUIREMENTS OF A CIPR

Ensuring all CIPRs meet minimum product requirements is a key way to achieve good outcomes for consumers and to increase comparability between products.

The paper seeks feedback on possible minimum product requirements of this composite product, such as requiring a CIPR to:

- deliver a minimum level of income that would generally exceed an equivalent amount invested 1.in an account-based pension drawn down at minimum rates, with recognition of the benefit of a guaranteed level of income where relevant;

- deliver a stream of broadly constant real income for life, in expectation (in particular, to manage 2.longevity risk); and

- include a component to provide flexibility to access a lump sum (for example, via an 3.account-based pension) and/or leave a bequest.

PROPOSED REGULATION OF CIPRS AND TRUSTEES

The paper also seeks views on how to regulate both trustees and CIPRs, in addition to regulation of the proposed minimum product requirements outlined above.

Trustees could choose to design a single mass-customised CIPR that would be in the best interests of, and offered to, the majority of their members. However, trustees would not be required to design and/or offer a product that is in the best interests of any particular member. In designing the product, trustees would need to consider whether it is in the best interests of members to outsource the administration of underlying component product(s) where the trustee does not have the necessary skill set or scale to administer the underlying component product(s).

As is currently the case, trustees and other product providers such as life insurers could also create new retirement income products that are tailored to particular member segments or individuals, rather than to the majority of the membership. These products could be offered via personal financial advice (including through robo advice) where the adviser is required to consider the individual’s circumstances and needs. Individuals could also purchase these products via direct channels. If these products are certified to meet the proposed minimum product requirements of a CIPR, it may be appropriate to allow a label to be attached indicating that the product ‘meets the minimum product requirements of a CIPR’.

WHAT THE CIPRS FRAMEWORK IS NOT ABOUT

It is important to debunk some myths about the CIPRs framework. The CIPRs framework is not intended to:

- encourage annuities over other products;

- compel retirees to take up a certain retirement income product; or

- replace the need for financial advice.

EXAMPLES

Below are three illustrative examples of possible CIPRs: ‘the cut’, ‘the stack’, and ‘the wrap’.

For ‘The cut’ CIPR, the deferred longevity product component could represent as little as 15 to 20 per cent of an individual’s total superannuation balance and still provide a higher and more stable

income than an account-pension drawn down at minimum rates. The large account-based pension component provides a high degree of ‘flexibility’, thereby efficiently managing the concern about dying early and forfeiting an individual’s superannuation savings.superannuation savings.

‘The stack’ CIPR would provide an individual with the flexibility to access ‘lumpy’ income throughout retirement from an account-based pension component drawn down at minimum rates. Compared to ‘The cut’, a larger proportion of the individual’s total superannuation balance would go towards a longevity product component.

‘The wrap’ CIPR represents a combination of ‘The cut’ and ‘The stack’ CIPRs and in doing so, delivers a balance of their benefits. ‘The wrap’ provides longevity risk management (through the deferred longevity product), higher income than an account-based pension drawn down at minimum rates, and provides a degree of flexibility to access ‘lumpy’ income throughout retirement.

FEES AND CHARGES

Increasing the fees charged on a CIPR, post-commencement

Currently, fees for annuities and defined benefit pensions are essentially ‘locked in’ at the time of purchase due to the guaranteed level of income these products provide. However, for an account-based pension component or a group self-annuitisation component of a CIPR, there is a risk that increases in administration fees would decrease income in retirement. Individuals would not easily be able to change CIPRs in response to an increase in fees.

One option may be to restrict administrative fees from increasing over the life of a CIPR, although there is a risk that if administrative costs increased substantially accumulation members may need to cross-subsidise members in the pension phase.

Another option may be to rely on the income efficiency concept. However, given that administration fees would have a small effect on efficiency as compared with bequests and capital costs, there would need to be a large increase in fees before income efficiency is affected.

An alternative option could be to allow trustees to increase fees so long as there is no differentiation between the fees paid by existing members and new members of the CIPR. This would ensure trustees continue to face competitive fee pressure.

Trustees could lose the right to offer a CIPR to new members if they increased their fees only for existing members.

This paper also seeks alternative ideas on how to protect individuals from significant increases in fees that would erode retirement incomes.

TIMETABLE

In due course, consultation will also be undertaken on exposure draft legislation and regulations to give effect to the CIPRs framework.

It is envisaged that the CIPRs framework would not commence until trustees and other product providers have had sufficient lead-time to develop appropriate products. Given a commencement date for alternative income stream product rules of 1 July 2017, and the Government is currently reviewing the social security means testing of retirement income streams, the CIPRs framework is not expected to commence any earlier than mid-2018.

The Government could, at a later date, and following an appropriate transition period, consider whether certain trustees should be obliged to offer CIPRs to any of their members. Given this, it will be important for the current proposed CIPRs framework to be sufficiently robust to accommodate a potential change in trustee obligations down the track.