This is an edited version of our live discussion about the current state of play of mortgage, rental and financial household stress across Australia, based on our latest surveys and modelling. We had our post code engine online.

Find out more beforehand by watching this show: Many Households Are In Trouble – Mate! https://youtu.be/np4H9RkPqEo

Original live version with chat here: https://youtube.com/live/Qs__lYQMhP4

Go to the Walk The World Universe at https://walktheworld.com.au/

Here we answer viewers specific post code requests, following our recent show discussing Household Mortgage, Rental and Financial stress last week “Many Households Are In Trouble – Mate!” https://youtu.be/np4H9RkPqEo

On Tuesday 13th February in our live show we will discuss this further, so if you have additional requests for post code level analysis, drop them in the chat.

You can get more info about our One to One service here: https://digitalfinanceanalytics.com/blog/dfa-one-to-one/

http://www.martinnorth.com/

Go to the Walk The World Universe at https://walktheworld.com.au/

This is our weekly market update, starting with the US, Europe, Asia and Australia, as well as Oil and Crypto.

The S&P 500 soared to fresh highs on Friday, but fewer stocks have been participating in the rally, stirring worries that recent gains could reverse if the market’s leaders stumble.

We are talking market breadth, or the number of stocks taking part in a broader index’s rise. A high breadth is often viewed as a healthy sign by investors as it shows gains are less dependent on a small cluster of names.

The reverse, a narrowing, on the other hand is a warning. And in fact, the Magnificent Seven have accounted for nearly 60% of the S&P 500’s gain this year, according to Dow Jones Indices.

The problem is the narrow group of stocks powering the market could make it more vulnerable to swift declines if an earnings disappointment or other issue hits its biggest stocks. While most of the megacaps have powered higher this year, shares of Tesla have fallen 22%, the third-worst performer in the S&P 500, demonstrating how quickly the market’s superstars can fall out of favor.

http://www.martinnorth.com/

Go to the Walk The World Universe at https://walktheworld.com.au/

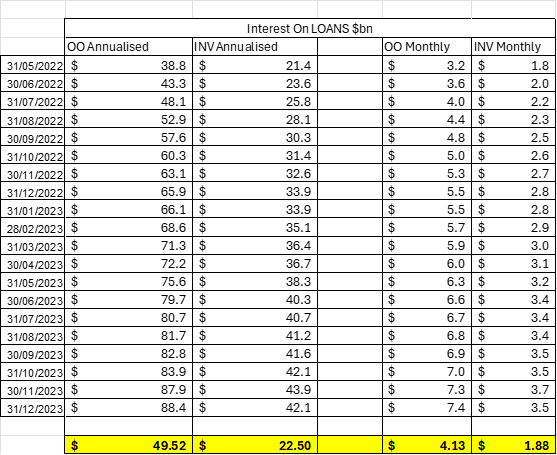

Using data from various sources including the RBA and APRA, we have estimated the gross and net additional payments households are making to financial institutions in Australia, following the RBA cash rate lifts from May 2022 to date.

We have only included owner occupied and investor loans, as these are the main foci of debt, but of course higher rates have also been applied to SME’s, personal loans and credit cards, but these are excluded from this analysis. These findings are indicative only.

Approach

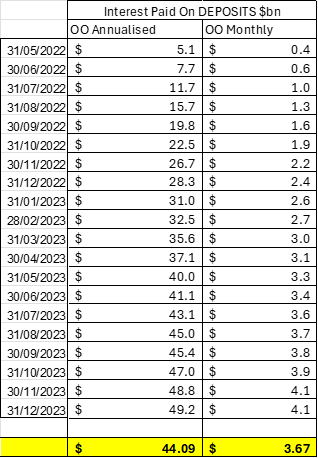

We took the loans outstanding data from the RBA monthly series, for both owner occupied and investor loans from their monthly series. We took the average interest rate charged on these loans again from relevant RBA data sources. We also took the total deposit pools held by the banks, using data from APRA (authorised depository institutions) and the typical interest paid from the RBA rate series.

During the period under review, the net value of loans and deposits grew, so we used the average balance each month. We applied the average interest rate charged to each balance, and compared the outcome in May 2022 to December 2023, the period over which interest rates rose. The different between the May 2022 to December 2023 is the gross increase in payments households were forced to make.

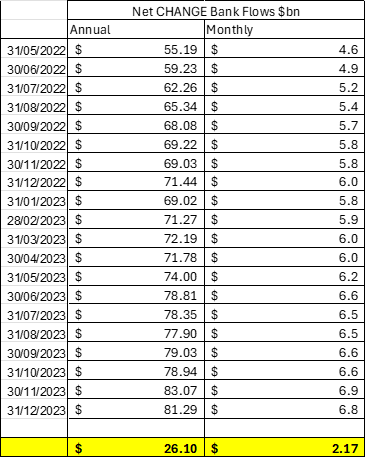

We also provided a net offset calculation because banks in the period also provided higher rates, at least to some extent on deposits, calculated with a similar method. These payments went to different households of course.

Note we have not included any assessment of capital being repaid during this period, as we worked on gross average balances. But this effectively isolates the impact of the higher rates.

Results

On a gross basis, banks received an additional $49.52 billion on an annualised basis between May 2022 and December 2023, on owner occupied loans, and $22.5 billion on investment loans. Together this is worth around $70 billion annualised. This translates to $4.13 billion per month for owner occupied loans and $1.88 billion for investor loans.

Turning to deposits, banks paid out and additional $44.09 billion on an annualised between May 2022 and December 2023, or $3.67 billion per month.

Offsetting the deposit interest paid to the mortgage interest received, Banks received an additional $26.1 billion from households on an annualised basis, or $2.17 billion per month.

We would also make the point that the interest paid by some households are generally returned to asset rich savers, not the same households. So it would be appropriate to cite the gross impact, rather than the net impact if this distinction is made.

This is in addition to returns deposited with the RBA under the Term Funding Facility.

Reserve Bank governor Michele Bullock was back in front of the bright lights, appearing at a House Economics Committee Hearing on Friday.

I have selected the edited highlights in this show, from the 3 hours of questions, and have included some of her statements. While she didn’t add a whole lot more to what she said at Tuesday’s press conference, she emphasised two points that should give pause to those expecting multiple rate cuts this calendar year.

The first was in response to a question on inflation expectations: by the time inflation gets back to the midpoint of the target band of 2 per cent to 3 per cent, as required by the RBA’s new mandate – which occurs some time beyond the middle of 2026 on the RBA’s latest forecasts – inflation will have been outside the target range for four years, which is right on the edge of what the RBA will tolerate.

The second was on productivity.

But she also touched on the risks in the forecasts, the impact of the Bank of Mum and Dad, and other distributional impact questions across households. Frankly, I found this unconvincing. So the think the RBA has much to do to gain a better set of insights into the current state of play!..

Let me know what you think in the comments!

http://www.martinnorth.com/

Go to the Walk The World Universe at https://walktheworld.com.au/

Interesting to see the momentum now turning to discussion of whether the Government intends to tackle negative gearing having U-turned on the tax cuts.

As The Conversation put it, there are two things the prime minister needs to get into his head about tax. One is that saying he won’t make any further changes no longer works. The other is that negative gearing doesn’t do much to get people into homes.

Australia’s Treasury has begun publishing estimates of the cost of the present unfocused system of negative gearing. Its latest, released last week, puts the cost at $2.7 billion per year, to which should probably be added a chunk of the $19 billion per year lost as a result of the capital gains concession.

Albanese is normally cautious. But as he is showing us right now with his rejigged Stage 3 tax cuts, there are times when he is not. If he really wants to throw everything he has got at building more homes, he knows what to do.

http://www.martinnorth.com/

Go to the Walk The World Universe at https://walktheworld.com.au/

Today’s post is brought to you by Ribbon Property Consultants.

We discuss the latest from the RBA, via the new press conference and the Statement On Monetary Policy.

In short, the RBA Governor Michele Bullock says she is yet to be convinced inflation is on a sustainable path back to target and further interest rate rises could not be ruled out as the bank seeks to curb price rises stoking the nation’s cost-of-living crisis.

“Domestically, there are uncertainties regarding the lags in the effect of monetary policy and how firms’ pricing decisions and wages will respond to the slower growth in the economy at a time of excess demand, and while the labour market remains tight,” the board statement said.

This translates into higher rates for longer, which was not what the market wanted to hear!

Do not expect a rate cut soon. Plan accordingly.

http://www.martinnorth.com/

Go to the Walk The World Universe at https://walktheworld.com.au/

Today’s post is brought to you by Ribbon Property Consultants.

Go to the Walk The World Universe at https://walktheworld.com.au/

Find more at https://digitalfinanceanalytics.com/blog/ where you can subscribe to our research alerts

Please consider supporting our work via Patreon: https://www.patreon.com/DigitalFinanceAnalytics

Or make a one-off contribution to help cover our costs via PayPal at: https://www.paypal.me/MartinDFA

We also can receive bitcoins at: 13zBL1oRib9VJu8Uc9zUGNhxKDBBgUpDN1

Please share this post to help to spread the word about the state of things….

Caveat Emptor! Note: this is NOT financial or property advice!!

🚨BEWARE OF SCAMMERS🚨

As there are accounts impersonating Walk The World in the comments on YouTube, note that our comments will have a distinguishable verified symbol. And remember that we will never message you asking you to give us money or talk to us on other platforms such as WhatsApp or Telegram

This is an edited version of a live discussion with Damien Klassen, Head of Investments at Walk The World Funds and Nucleus Wealth. Markets are rising, thanks mainly to AI related stocks, while expectations of rate cuts are being pushed out. More broadly, are returns able to justify current valuations, and which sectors are the most interesting ahead.

Original stream with chat here: https://youtube.com/live/lqYE35qTatw

Go to the Walk The World Universe at https://walktheworld.com.au/

Another week shoots past, so Edwin is back for another property update. The chaos continues with talk of “pre-war”, home price rises, and more Government support for property. What could possibly go wrong?

http://www.martinnorth.com/

Go to the Walk The World Universe at https://walktheworld.com.au/

Today’s post is brought to you by Ribbon Property Consultants.

If you are buying your home in Sydney’s contentious market, you do not need to stand alone. This is the time you need to have Edwin from Ribbon Property Consultants standing along side you.

Buying property, is both challenging and adversarial. The vendor has a professional on their side.

Emotions run high – price discovery and price transparency are hard to find – then there is the wasted time and financial investment you make.

Edwin understands your needs. So why not engage a licensed professional to stand alongside you. With RPC you know you have: experience, knowledge, and master negotiators, looking after your best interest.

Shoot Ribbon an email on info@ribbonproperty.com.au & use promo code: DFA-WTW/MARTIN to receive your 10% DISCOUNT OFFER.