A professional indemnity (PI) specialist has expressed grave concern over new requirements for brokers to confirm that there are no signs of financial abuse when they assist clients in securing a loan; via Australian Broker.

The action has been taken by the banks in response to the Australian

Banking Association’s updated code of practice requiring a higher

standard for dealing with vulnerable customers. However, Darren Loades,

the FBAA’s dedicated PI insurance specialist for Queensland and the

Northern Territory, has questioned the sudden announcement, the lack of

clarity as to what the agreement entails, and the days-long timeframe

before the 1 July implementation.

“Do you think that’s by accident? I sure don’t,” said Loades.

“The main point is that it’s been rushed through, no one has actually

seen the details, and it could have very far-reaching and onerous

implications for brokers. Do not sign anything for the moment.”

Loades highlighted the serious liability concerns of signing an

agreement that could likely take brokers out of their current coverage

and leave them “entirely exposed.”

“Professional indemnity policies only respond to claims made under

common law. Signing one of these declarations could incur contractual

liabilities, over and above the liabilities a broker would owe at common

law,” he explained.

“The standard PI policy out there on the market will not pick up any

liabilities owed under contract. Brokers could potentially be left

exposed and not insured at all.”

Last week, FBAA managing director Peter White expressed concern that

“PI insurance could increase tenfold to cover a declaration like this.”

“To try and ram this through with little notice is not only

ridiculous and ill-conceived, but creates massive risks for brokers with

almost no benefit to borrowers,” he added.

As White expressed last week, Loades finds it suspect that the

agreements the banks are asking brokers to sign have yet to be made

accessible.

He continued, “But knowing the banking industry, the documents are

going to be pretty far-reaching with some nasty little clauses in there

along the lines of, ‘If you drop the ball in this area, you agree to

indemnify the bank against any losses.’ Otherwise, why would they be

going to this trouble?

“This seems to be a push from the banks to transfer their liability onto the broker, which isn’t all that fair or realistic.”

While Loades does acknowledge that brokers are the ones to have

face-to-face interaction with the borrower, he has serious doubts that a

set of written guidelines provided by the bank could translate to

brokers being able to identify signs of abuse in real life stations.

“That’s a whole different ballgame. Brokers aren’t qualified or

licenced to provide advice in this area of financial abuse,” he said.

“What happens if the broker happens to innocently miss a situation

where there is financial abuse? The bank is going to rely on this

document to say, ‘Well, you signed off. You’re the one who is liable.’”

The fall in interest rates and an easing of lending standards will “breathe life” into the property market, but not without consequences, according to Moody’s Analytics, via The Adviser.

Financial intelligence agency Moody’s Analytics has released its Second Quarter 2019 Housing Forecast Report, in which it has noted its outlook for the Australian housing market.

Drawing on CoreLogic’s Hedonic Home Value Index,

the research agency noted the correction in residential property

prices, which it said was “a long time coming” after a “strong run-up”

in values across more densely populated markets, particularly in Sydney

and Melbourne.

However, Moody’s has observed that while

residential home prices have moderated from their peak in September

2017, the decline has not led to a “material” improvement in housing

affordability, with values still 20 per cent higher than during the

pre-boom period in 2013.

Nonetheless, Moody’s has reported that it expects the Reserve Bank of Australia’s (RBA) cut to the official cash rate and proposals

to ease home loan serviceability guidelines from the Australian

Prudential Regulation Authority (APRA) to rekindle demand for credit and

spark activity in the housing market.

“An important driver of the

slowdown in Australia’s housing market has been tighter credit

availability, partly as a consequence of the regulator – the Australian

Prudential Regulation Authority – tightening lending conditions, which

has made it relatively more difficult to purchase a property,

particularly for investors,” Moody’s noted.

“These serviceability requirements were eased in May.

“Expectations

of further lending reductions flowing on from RBA cash rate reductions

will also breathe life into the property market and add weight to our

view that the national housing market will reach a trough in the third

quarter of 2019 and gradually improve thereafter.”

However,

Moody’s warned that a resurgence in the housing market activity could

further expose the economy to risks associated with high levels of

household debt.

“This could see the household leverage-to-GDP

ratio climb, making Australia stand out further amongst its peers,”

Moody’s stated.

“This is an undesirable position to be in,

particularly given the questions around sustainability of the

potentially rising debt load.”

Moreover, recent changes in the

regulatory landscape have been interpreted by some observers as as a

sign that the economy could be at risk of falling into recession amid growing internal and external headwinds.

Treasurer Josh Frydenberg recently acknowledged that “international challenges” could pose a threat to the domestic economy.

Fears

of a looming recession have prompted some observers, including the CEO

of neobank Xinja, Eric Wilson, to encourage borrowers to pocket mortgage rate cuts passed on following the RBA’s decision to lower the cash rate.

Mr

Wilson claimed that resisting the urge to accrue more debt would help

borrowers build a buffer against downside risks in the economy.

The

Australian Bureau of Statistics’ (ABS) Australian National Accounts

data for the quarter ending March 2019, reported GDP growth of 0.4 per

cent, with annual growth slowing to 1.8 per cent – the weakest since

September 2009.

However, Moody’s economist Katrina Ell has said she expects the RBA’s monetary policy agenda to help revive the economy.

“The

combination of increased monetary policy stimulus, expectations of the

housing market reaching a trough in the third quarter of 2019, and

fiscal policy playing a relatively supportive role including via income

tax cuts should boost GDP growth to 2.8 per cent in 2020,” Ms Ell said.

In the Phase 2 document released today, Deposit Insurance, funded by a bank levy is proposed. Unlike the Australian $250k scheme (which is not activated until the Government says so, and is taxpayer funded initially), the NZ scheme is for a lower amount with a protection limit in the range of $30,000 – $50,000. Implementation will probably take at least two years.

One question so far not answered is the interaction with the deposit bail-in. Generally bail-in stops a failing bank from failing, whereas deposit guarantees are activated on failure. So bail-in might stop deposit guarantees even being called on…

Depositor Protection

Why is a range of $30,000 – $50,000 for the proposed depositor protection scheme proposed?

Available data suggests that a protection limit in the range of

$30,000 – $50,000 could fully protect from loss more than 90 percent of

individual bank depositors in New Zealand, while leaving the majority of

banks’ deposit funding exposed to risk. This would strike the right

balance between protecting small depositors from loss and enhancing

public confidence in the banking system on the one hand, while

maintaining private incentives to monitor bank risk taking on the other.

It would also be broadly consistent with international schemes in terms

of the share of deposits and depositors that would be fully protected

(albeit relatively low in terms of the absolute dollar value of

protections).

More work will be required to choose the limit within this range that

is the best for advancing the public policy objectives chosen for the

protection scheme. The consultation seeks feedback on these choices.

The Reserve Bank is proposing high capital requirements for

banks which should reduce the risk of bank failure. Why is depositor

protection required if the risk of bank failure is small?

Even with high capital requirements, banks can still fail for a

variety of reasons. Regulation, supervision, resolution, and deposit

protection all make up a ‘financial safety net’ that supports a stable

and resilient financial system and protects society from the damage

caused by bank failures. The safety net tools interact and overlap,

which can make it seem that not all of the tools are necessary. However,

if the safety net is incomplete, it will be difficult to find effective

solutions for dealing with serious problems in the banking system. This

means that capital tools that help to keep banks safe and sound at the

‘top of the cliff’, must be complemented by robust tools to deal with

banks that may still fall to the bottom.

The OECD and IMF have warned that, without depositor protection, New

Zealand is vulnerable to contagious bank runs. Bank runs can escalate

into banking crises that destroy social and financial capital. For New

Zealand’s safety net to be effective in good times and bad, the tools

within the net must each be strong in its own right, and work well

together.

How will the risks associated with moral hazard be addressed in the proposed depositor protection scheme?

Moral hazard arises when people are protected from the consequences

of their risky behaviour. If deposit protection is introduced,

depositors may take less care when assessing the risks associated with

their banks, and banks may take less care with depositors’ money. Moral

hazard costs are part of the reason why New Zealand has until now chosen

not to have a depositor protection regime.

There is considerable international experience on how to design an

effective deposit protection scheme, within the broader financial safety

net, that mitigates moral hazard. International experience demonstrates

that strong regulatory monitoring of deposit-takers’ corporate

governance and risk management systems goes a long way to addressing the

moral hazard of depositor protection. Maintaining private monitoring

incentives is also important, and can be achieved through carefully

calibrating the protection scheme’s scope of coverage. For example,

setting the protection limit at a level that fully covers most household

and small business depositors, but leaves large institutional

depositors exposed to risk, will support private monitoring incentives.

In conjunction, having effective resolution tools (that make it more

credible investors’ money is at risk should their institution fail) can

sharpen monitoring by institutional investors.

International practice and guidance, as well as the views of experts

and the public, will inform the design of New Zealand’s depositor

protection scheme.

What are the costs of funding the proposed depositor protection scheme and who will bear these costs?

A primary tool of the protection scheme will be insurance. Deposit

insurance transfers the risks and costs of bank failures away from

depositors onto an insurance scheme. This will come with upfront costs

of establishing a deposit insurer, and ongoing operational costs.

Modern deposit insurance schemes are normally funded by levies on

member banks, supported (where necessary) by temporary lending paid for

by taxpayers. If the insurance scheme is accompanied by a depositor

preference, this might also increase banks’ non-deposit funding costs as

risks are transferred from depositors onto institutional investors.

Details of the scheme, including costs, are still to be worked out in

the next phase of the work programme. To the extent that depositor

protection increases banks’ average costs, this might be passed on to

customers through higher mortgage rates or lower deposit rates.

Alternatively, costs might be absorbed by banks’ own margins and

retained earnings. The extent to which costs are shared between banks

and their customers depends on competition and contestability in the

sector.

A fuller cost-benefit analysis will follow as we learn more about the

specific design features of New Zealand’s depositor protection scheme.

When will the depositor protection scheme be introduced?

A work programme running alongside the Reserve Bank Review process

will develop a depositor protection scheme that is best for New Zealand.

The work programme will be guided by a framework setting out some key

design principles for an effective scheme, and will draw (where

relevant) on international standards and best practice. The work

programme will determine the:

mandates and powers

governance and decision making structure

coordination arrangements with other safety net providers

membership and coverage arrangements

funding and pay-out mechanics, and

design features to mitigate moral hazard

that are appropriate for New Zealand’s protection scheme. The Review

Team’s discussions with the global coordinating body for deposit

insurers indicates that the path from policy recommendations to scheme

implementation will probably take at least two years.

On 21 June, the US Federal Reserve (Fed) published the results of the 2019 Dodd-Frank Act stress test (DFAST) for 18 of the largest US banking groups, all of which exceeded the required minimum capital and leverage ratios under the Fed’s severely adverse stress scenario; via Moodys’.

These results are credit positive for the banks because they show that the firms are able to withstand severe stress while continuing to lend to the economy. In addition, most firms achieved a wider capital buffer above the required minimum than in last year’s test, indicating a higher degree of resilience to stress. The 2019 results support our view of the sector’s good capitalization and benefit banks’ creditors.

The median stressed capital buffer above the required Common Equity Tier 1 (CET1) ratio increased to 5.1% from 3.5% last year, a substantial change. However, the 18 firms participating in 2019 were far fewer than the 35 that participated in 2018, helping lift the results this year. This is because passage of the Economic Growth, Regulatory Relief, and Consumer Protection Act in May 2018 resulted in an extension of the stress test cycle to two years for 17 large and non-complex US bank holding companies, generally those with $100-$250 billion of consolidated assets, which pose less systemic risk.

This is the fifth consecutive year that all tested firms exceeded the Fed test’s minimum CET1 capital requirement. As in prior years, the banks’ Tier 1 leverage and supplementary leverage ratios had the slimmest buffers of 2.8% and 2.4%, respectively, above the required minimums as measured by the aggregate.

Under DFAST, the Fed applies three scenarios – baseline, adverse and severely adverse – which provide a forward-looking assessment of capital sufficiency using standard assumptions across all firms. The Fed uses a standardized set of capital action assumptions, including common dividend payments at the same rate as the previous year and no share repurchases. In this report, we focus on the severely adverse scenario, which is characterized by a severe global recession accompanied by a period of heightened stress in commercial real estate markets and corporate debt markets.

This year’s severely adverse scenario incorporates a more pronounced economic recession and a greater increase in US unemployment than the 2018 scenario. The 2019 test assumes an 8% peak-to-trough decline in US real gross domestic product compared with 7.5% last year and a peak unemployment rate of 10% that, although the same as last year, equates to a greater shock because the starting point is now lower (the rise to peak is now 6.2% compared with 5.9% last year).

The severely adverse scenario also includes some assumptions that are milder than last year: housing prices drop 25% and commercial real estate prices drop 35%, compared with 30% and 40% last year; equity prices drop 50% compared with 65% last year; and the peak investment grade credit spread is 550 basis points (bp), down from 575 bp last year. We consider this exercise a robust health check of these banks’ capital resilience.

Finally, the three-month and 10-year Treasury yields both fall in this year’s severely adverse scenario, resulting in a mild steepening of the yield curve because the 10-year yield falls by less. As a result banks’ net interest income faces greater stress than in last year’s scenario, which assumed unchanged treasury yields and a much steeper yield curve.

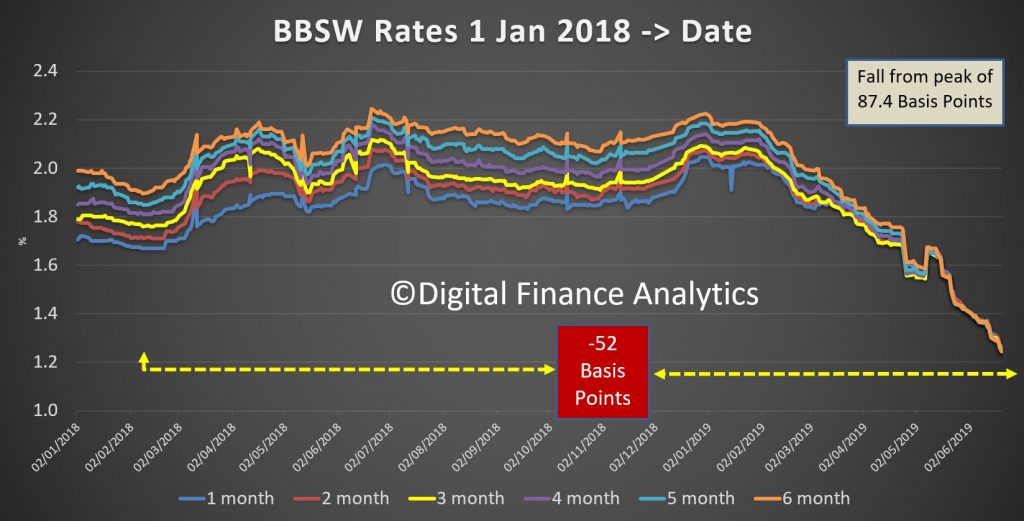

In the June RBA Bulletin, there was an article which describes how the RBA executes its market interventions to effect a cash rate change. It is important to understand these inner workings, despite it appearing complicated on first blush.

And consider this, this tool box is being used by many central banks around the world to direct the financial system.

In summary, the RBA’s operations in domestic markets support the implementation of monetary policy. The most important tool to guide the cash rate to the target set by the Board is the interest rate corridor. To support this, the RBA pursues daily open market operations in order to keep the pool of exchange settlement (ES) balances at the appropriate level for the cash market to function smoothly. The daily market operations are conducted to offset the effects on liquidity of the many transactions between the banking system and the Australian Government. Open market operations are primarily conducted through repos and FX swaps. These provide flexibility for liquidity management and also help to manage risk for the RBA’s balance sheet.

The cash rate is a key determinant of interest rates in domestic financial markets and hence underpins the structure of the interest rates that influence economic activity and financial conditions more generally.

This helps to explain the sharp falls in the BBSW rates, which are now around 87 basis points lower than the recent peak. Such a fall has been engineered.

The cash rate is an effective instrument for implementing monetary policy because it affects the broader interest rate structure in the domestic financial system. The cash rate is an important determinant of short-term money market rates, such as the bank bill swap rate (BBSW), and retail deposit rates (Graph 1). These rates – as well as a number of other factors – then influence the funding costs of financial institutions and the lending rates faced by households and businesses. As a result, the cash rate influences economic activity and inflation, enabling the RBA to achieve its monetary policy objectives. However, while changes in the cash rate are very important, they are not the only determinant of market-based interest rates. Other factors, such as expectations, conditions in financial markets, changes in competition and risks associated with different types of loans are also important.

Graph 1

The Cash Market and the Interest Rate Corridor

The RBA implements monetary policy by setting a target for the cash rate. This is the interest rate at which banks lend to each other on an overnight unsecured basis, using the exchange settlement (ES) balances they hold with the RBA. ES balances are at-call deposits with the RBA that banks use to settle their payment obligations with other banks. Banks are required to have a positive (or zero) ES balance at all times, including at the end of each day. It is difficult for institutions to predict whether they will have adequate funds at the end of any particular day, which generates the need for an interbank overnight cash market. Those banks that need additional ES balances after they have settled all payment obligations of their customers, borrow from banks with surplus ES balances. The interbank cash market is the mechanism through which these balances are redistributed between participants.

The RBA sets the supply of ES balances to ensure that the cash market functions smoothly by

providing an appropriate level of ES balances to facilitate the settlement of interbank

payments. The RBA manages the supply of ES balances available to the financial system through

its open market operations (see below). Excessive ES balances could lead institutions to lend

below the target cash rate, while a shortage might result in the cash rate being bid up above

the target.

The interest rate corridor ensures that banks have no incentive to deviate significantly from

the cash rate target when borrowing or lending in the cash market. Banks can borrow ES balances

overnight on a secured basis from the RBA at a margin set 25 basis points above the cash rate

target. As a result, banks have no need to borrow from other banks at a higher rate. Similarly,

banks receive interest on their surplus ES balances at 25 basis points below the cash rate

target. Therefore, they have no incentive to lend to other banks at a lower rate.

The operation of the interest rate corridor means that there is no need for the RBA to adjust

the supply of ES balances to bring about a change in the cash rate (Graph 2 and Graph 3). For

example, when the RBA lowered the cash rate target by 25 basis points from 1.5 per cent

to 1.25 per cent in early June, the rates associated with the corridor also moved

lower, to be 1.0 per cent on overnight deposits and 1.5 per cent on

overnight loans (down from 1.25 per cent and 1.75 per cent). A bank that

would have previously required a return above 1.25 per cent to lend ES balances in the

cash market is, under the new corridor, willing to lend at a lower return. And so a bank wanting

to borrow cash pays a lower rate than before. Similarly, if the RBA had instead raised

the cash rate by 25 basis points from 1.5 per cent, the corridor would have moved up,

to be 1.5 per cent to 2.0 per cent. A bank that would have previously lent

surplus ES funds to another in the cash market at 1.50 per cent would, under the new

corridor, no longer have an incentive to do so. Indeed, it would require a higher return to lend

ES balances, rather than leaving those funds in its ES account and receiving 1.50 per cent

from the RBA. Hence, a bank wanting to borrow in the cash market would have to pay a higher

interest rate than it did previously.

In other words, interbank transactions automatically occur within the interest rate corridor without the RBA needing to undertake transactions beyond its usual market operations to manage liquidity.

Graph 2

Graph 3

The incentives underlying the corridor guide the cash rate to the target and ordinarily all transactions occur at the rate announced by the RBA. The last time there was a small deviation in the published cash rate (which is a weighted average of all transactions in the cash market) from the target (of 1 basis point for two days) was in January 2010 (Graph 4). The lack of deviation of the cash rate from the target has brought about a self-reinforcing market convention where both borrowers and lenders in the cash market expect to transact at the prevailing target rate. This market convention helps to address the uncertainty that banks would otherwise face about the price at which they can borrow sufficient ES balances to cover their payment obligations each day. In 2018, daily transactions in the overnight interbank market were typically between $3 billion and $6 billion.

Graph 4

As in Australia, many other central banks implement monetary policy with an interest rate corridor to guide the policy rate. The width of the corridor tends to differ, typically from 50 to 200 basis points. The choice of the width of the corridor is seen as a reflection of a trade‐off between interest rate control and the desire to avoid the central bank becoming an intermediary in the money market. All other things being equal, cross-country studies suggest that a narrower corridor is preferred by central banks that have a strong preference for low volatility of short-term interest rates, whereas a wider corridor is usually preferred by central banks that seek to encourage more interbank trading activity.

Over the past 10 years, many central banks (other than the RBA) have significantly expanded

their balance sheets. This has resulted in significantly more liquidity in their respective

systems and so banks typically do not need to borrow funds in the overnight cash market. In

these cases, the policy rate typically converges toward the rate on deposits paid by the central

bank; this is often referred to as a ‘floor system’. Small changes in liquidity in

such a system do not tend to have much effect on the policy rate.

Liquidity Management and Open Market Operations

Transactions between the government (which banks with the RBA) and the commercial banks would, by themselves, change the supply of ES balances on a daily basis. ES balances in accounts of commercial banks increase whenever the government spends out of its accounts at the RBA. Similarly, when the government receives cash into its accounts at the RBA, such as from tax payments or debt issuance, ES balances decline. The RBA monitors and forecasts these changes actively through the day. It offsets (i.e. ‘sterilises’) these changes in ES balances with its daily open market operations so that government receipts and payments do not affect the aggregate level of ES balances. If transactions that affect system liquidity were not offset by the RBA, ES balances would be much more volatile and the payments system would suffer frequent disruptions (Graph 5). Ultimately this is likely to lead to a more volatile cash rate.

Graph 5

The main tools used in open market operations are repurchase (repo) agreements and foreign exchange swaps. Both repos and foreign exchange swaps involve a first and a second leg (Figures 1 and 2):

The first leg of a typical repo in open market operations (which injects ES balances)

involves the RBA providing ES balances to a bank and the bank providing eligible debt

securities as collateral to the RBA. Taking collateral safeguards the RBA against loss in

the case of counterparty default. The second leg, which occurs at an agreed future date,

unwinds the first leg: the bank returns the ES balances and the RBA returns the securities

to the bank.

The first leg of a foreign exchange swap designed to inject ES balances into the system

involves the RBA providing ES balances to a bank and the bank providing collateral in the

form of foreign currency to the RBA (typically US dollars, euros or Japanese yen). The

second leg, at the agreed future date, consists of the bank returning the ES balances and

the RBA returning the foreign exchange.

Figure 1

Figure 2

Repos and swaps provide more flexibility for liquidity management than outright purchases or sales of assets since they involve a second leg (when the transaction unwinds) with a date chosen to support liquidity management on that day. It also allows the RBA to accept a much broader range of collateral, such as unsecured bank paper, than it would be willing to purchase outright. By contrast, buying (and then selling) securities outright requires the RBA to take on the price and liquidity risk associated with owning the assets outright. Conducting open market operations by buying and selling government securities outright, while also ensuring that the RBA’s market operations do not affect liquidity in the bond market, would require more government securities than are available in Australia.

The size of daily open market operations is based on forecasts of daily liquidity flows between

the RBA’s clients (mainly the Australian Government) and the institutions with ES accounts.

In a typical round of market operations, a public announcement is made at 9.20 am that the RBA

is willing to auction ES balances against eligible collateral for a certain number of days

(ranging from two days to several months, with an average term of around 30 days). Institutions

have 15 minutes to submit their bid. The RBA ranks these bids from highest to lowest repo

rate and then allocates ES balances to the highest bidders until the amount the RBA intends to

auction has been dealt. All auction participants are informed electronically about their

allocation. If they have been successful, they will pay the rate at which they bid for the

amount allocated. The aggregate results of the auction, including the amount dealt, the average

repo rate and the lowest repo rate accepted are published.

Market Operations and the RBA Balance Sheet

The transactions entered into as part of open market operations are reflected in changes in the

RBA’s balance sheet. Changes in the size and composition of liabilities (mainly issuance of

banknotes and government deposits) may need to be offset via open market operations to ensure

that the availability of ES balances remains appropriate for the smooth functioning of the cash

market (Graph 6).

Graph 6

Open market operations affect the asset side of the balance sheet (Graph 7). When the RBA purchases securities under repo, it has a legal claim on the security that was transferred as collateral for the duration of the repo. These claims appear as assets on the balance sheet, along with outright holdings of domestic government securities. When the RBA uses foreign exchange swaps to supply Australian dollars into the local market, the foreign currency-denominated investments associated with the swap are also reflected as assets on the balance sheet. The choice between using repo, foreign exchange swaps or outright purchases to adjust the supply of ES balances is determined by market conditions and pricing. When a large amount of ES balances needs to be supplied or drained, such as when a government bond matures, the RBA might choose to do so using a combination of instruments.

Graph 7

The RBA supplies ES balances not only for monetary policy implementation but also to facilitate

the functioning of the payment system. Over recent years, the RBA has been providing more ES

balances to banks to enable the settlement of payments outside normal banking hours, such as

through direct-entry and the New Payments Platform. These ES balances are supplied under ‘open

repos’. An open repo is set up in a similar way to the repo explained in Figure 1, with

the initial leg transferring ES balances to banks in return for eligible debt securities as

collateral. However, the date of the second leg is not specified, so it is open ended. The ES

balances are available (and the claim on securities remain on the RBA’s balance sheet) until

the open repo is closed out. These ES balances provided under open repo are held purely to

facilitate the effective operation of the payments system after hours and cannot be lent

overnight in the cash market. As a result, they have no implications for the implementation of

monetary policy. Currently, these balances are around $27 billion. The remainder of ES

balances that are available for trading in the cash market are referred to as ‘surplus ES

balances’, and are the focus of daily open market operations. Recently, surplus ES

balances have been around $2–3 billion. This amount has increased in recent years as

demand for balances has risen, partly in response to new prudential regulations on liquidity.

The New Zealand Reserve Bank is requesting two reports from ANZ New Zealand to provide assurance it is operating in a prudent manner.

They say, that section 95 of the Reserve Bank of New Zealand Act 1989 gives the Reserve Bank the power to require a bank to provide a report by a Reserve Bank-approved, independent person. These reviews can investigate such issues as risk management, corporate or financial matters, and operational systems.

The first report will cover ANZ New Zealand’s

compliance with the Reserve Bank’s current and historic capital adequacy

requirements.

The second report will assess the

effectiveness of ANZ New Zealand’s Director’s Attestation and Assurance

framework, focussing on internal governance, risk management and internal

controls.

Reserve Bank Governor Adrian Orr said ANZ

remains sound and well capitalised.

“We continue to engage constructively with

ANZ New Zealand’s board, and they remain focussed on these important issues.

These formal reviews will allow us to work with the bank to ensure the public,

and we as regulator, can have continued confidence in the bank and that it is

operating in a prudent manner.”

“Section 95 reports are part of our

supervisory toolkit and provide independent assurance and insight about banks’

systems and practices. We have used them effectively in the past, and we will

continue to do so.”

New housing in Australia must meet minimum energy performance requirements. We wondered how many buildings exceeded the minimum standard. What our analysis found is that four in five new houses are being built to the minimum standard and a negligible proportion to an optimal performance standard. Via The Conversation.

There have been calls

for these minimum standards to be raised. However, many policymakers

and building industry stakeholders believe the market will lift

performance beyond minimum standards and so there is no need to raise

these.

What did the data show?

We wanted to understand

what was happening in the market to see if consumers or regulation were

driving the energy performance of new housing. To do this we explored

the NatHERS data set of building approvals

for new Class 1 housing (detached and row houses) in Australia from May

2016 (when all data sets were integrated by CSIRO and Sustainability

Victoria) to December 2018.

Our analysis focuses

on new housing in Victoria, South Australia, Western Australia,

Tasmania and the ACT, all of which apply the minimum six-star NatHERS

requirement. The other states have local variations to the standard,

while New South Wales uses the BASIX index to determine the

environmental impact of housing.

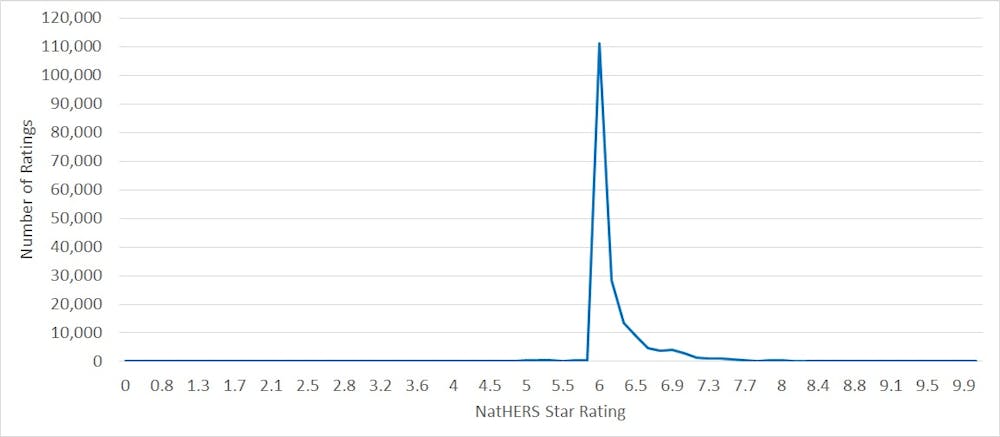

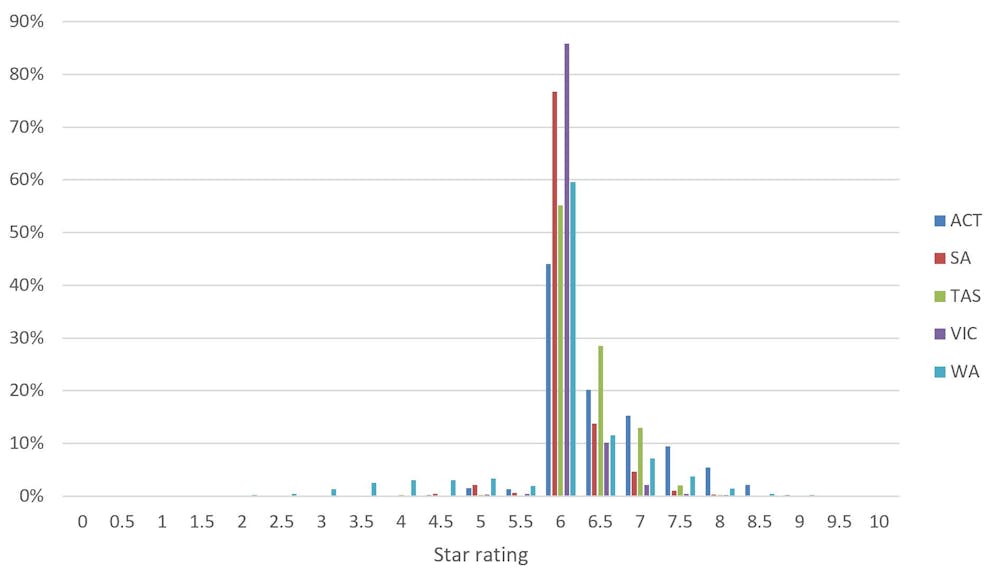

The chart below shows the performance for 187,320 house ratings.

Almost 82% just met the minimum standard (6.0-6.4 star). Another 16%

performed just above the minimum standard (6.5-6.9 star).

Only 1.5% were designed to perform at the economically optimal 7.5

stars and beyond. By this we mean a balance between the extra upfront

building costs and the savings and benefits from lifetime building

performance.

NatHERS star ratings across total data set for new housing approvals, May 2016–December 2018.

Author provided

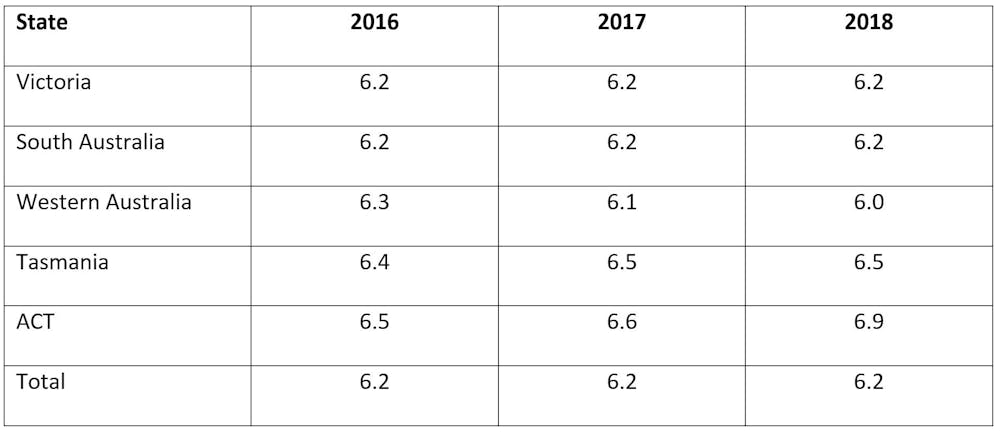

The average rating is 6.2 stars across the states. This has not changed since 2016.

Average NatHERS star rating for each state, 2016-18.

Author provided

The data analysis shows that, while most housing is built to the

minimum standard, the cooler temperate regions (Tasmania, ACT) have more

houses above 7.0 stars compared with the warm temperate states.

NatHERS data spread by state.

Author provided

The ACT increased average performance each year from 6.5 stars in

2016 to 6.9 stars in 2018. This was not seen in any other state or

territory.

The ACT is the only region with mandatory disclosure of the energy rating

on sale or lease of property. The market can thus value the relative

energy efficiency of buildings. Providing this otherwise invisible

information may have empowered consumers to demand slightly better

performance.

We are paying for accepting a lower standard

The evidence suggests consumers are not acting rationally or making

decisions to maximise their financial well-being. Rather, they just

accept the minimum performance the building sector delivers.

The fact that these improvements aren’t being made suggests there are

significant barriers to the market operating efficiently. This is

despite increasing awareness among consumers and in the housing industry

about the rising cost of energy.

Eight years after the introduction of the six-star NatHERS minimum

requirement for new housing in Australia, the results show the market is

delivering four out of five houses that just meet this requirement.

With only 1.5% designed to 7.5 stars or beyond, regulation rather than

the economically optimal energy rating is clearly driving the energy

performance of Australian homes.

Increasing the minimum performance standard is the most effective way to improve the energy outcomes.

The next opportunity for increasing the minimum energy requirement

will be 2022. Australian housing standards were already about 2.0 NatHERS stars behind comparable developed countries in 2008. If mandatory energy ratings aren’t increased, Australia will fall further behind international best practice.

If we continue to create a legacy of homes with relatively poor

energy performance, making the transition to a low-energy and low-carbon

economy is likely to get progressively more challenging and expensive. Recent research has calculated

that a delay in increasing minimum performance requirements from 2019

to 2022 will result in an estimated A$1.1 billion (to 2050) in avoidable

household energy bills. That’s an extra 3 million tonnes of greenhouse

gas emissions.

Our research confirms the policy proposition that minimum house energy regulations based on the Nationwide House Energy Rating Scheme are a powerful instrument for delivering better environmental and energy outcomes. While introducing minimum standards has significantly lifted the bottom end of the market, those standards should be reviewed regularly to ensure optimal economic and environmental outcomes.

Authors: Trivess Moore, Lecturer, RMIT University; Michael Ambrose, Research Team Leader, CSIRO; Stephen Berry, Research fellow, University of South Australia

An executive board member of APRA has told delegates that failing to take action on climate change now will lead to much higher economic costs in the long term, via InvestorDaily.

Executive

board member Geoff Summerhayes spoke to the International Insurance

Society Global Insurance Forum in Singapore and told delegates that

short-term pains were needed for long-term gains.

“The level of

economic structural change needed to prepare for the transition to the

low-carbon economy cannot be undertaken without a cost,” he said.

“But

it’s also true that failing to act carries its own price tag due to

such factors as extreme weather, more frequent droughts and higher sea

levels.”

Mr Summerhayes said that Australia had its share of the

climate change debate, with one side calling for action and the other

viewing climate change action as expensive.

“The

risk is global, yet the costs of action may not fall evenly on a

national basis. And second, the benefits will accrue in the future, but

many of the costs of change must be borne now. For the Australian

community, this remains a highly contentious set of issues,” he said.

Talking

to experts in risk management, Mr Summerhayes called on the insurance

industry to play a leadership role in bringing forward better data for

what the costs of climate action are.

“By developing more

sophisticated tools and models, and especially through enhanced

disclosure of climate-related financial risks, insurers can help

business and community leaders make decisions in the best interests of

both environmental and economic sustainability,” he said.

APRA

raised the issue in 2017 of the financial risks of climate change and

since then has been endorsed by the RBA and ASIC as well.

“When a

central bank, a prudential regulator and a conduct regulator, with

barely a hipster beard or hemp shirt between them, start warning that

climate change is a financial risk, it’s clear that position is now

orthodox economic thinking,” Mr Summerhayes said.

How best to act

remains a challenge, Mr Summerhayes admitted, and people were still

debating who should carry the burden and whether the benefits were worth

the costs.

“Government spending decisions may need to be

reprioritised, and not every member of society will be able to bear

these short-term costs equally comfortably,” he said.

However, what many forgot is that economic change also presents economic opportunities, the board member added.

“Forward-thinking

businesses have for years been seeking to get ahead of the low-carbon

curve by developing new products, expanding into untapped markets or

investing in green finance opportunities,” he said.

Ultimately, it was a fight between short-term impact or long-term damage, Mr Summerhayes said.

“Controlled

but aggressive change with a major short-term impact but lower

long-term economic cost? Or uncontrolled change, limited short-term

impact and much greater long-term economic damage?

“When put like

that, it seems such a straight-forward decision, but in reality,

businesses around the world are struggling to find the appropriate

balance.”

Climate risk was ultimately an environmental and

economic problem, and Mr Summerhayes said framing it as a cost-of-living

problem presented a false dichotomy.

“That approach risks

deceiving investors or consumers into believing there is no economic

downside to acting slowly or not at all. In reality, we pay something

now or we pay a lot more later. Either way, there is a cost,” Mr

Summerhayes said.

Ultimately, better data could help everyone to

better understand the physical risk trade-off and the reality that there

was no avoiding the costs of adjusting to a low-carbon future.

“Taking

strong, effective action now to promote an early, orderly economic

transition is essential to minimising those costs and optimising the

benefits. Those unwilling to buy into the need to do so will find they

pay a far greater price in the long run,” he said.

The final results last week were slightly higher then recently, but on lower volumes. Still looking for real signs of life… is the dead cat bounce dead??

In Canberra 28 auctions were listed, 20 results were confirmed and 14 sold with 3 withdrawn and 9 passed in, giving a Domain result of 61%.

In Brisbane, 62 properties were listed, 40 results were confirmed with 10 sold, 7 withdrawn and 30 passed in, giving a Domain result of 21%.

In Adelaide, 61 were listed, 35 results were confirmed and 23 sold, with 6 withdrawn and 12 passed in, giving a Domain result of 56%.