A two-year probe by Australia’s consumer watchdog has resulted in criminal charges against ANZ, Citigroup and Deutsche Bank, as well as six of their senior executives, over alleged “cartel-like” behaviour.

The case, brought by the Commonwealth Director of Public Prosecutions (CDPP) after an investigation by the Australian Competition and Consumer Commission (ACCC), is the second prosecution of its kind to be brought in Australia since competition laws were tightened almost a decade ago.

The banks and six investment bankers are charged with cartel conduct related to the sale of A$2.5 billion worth of unsold ANZ shares to investors in August 2015. The ACCC alleges that senior executives from the three banks colluded in the way they dealt with these shares.

The exact details of the alleged criminal conduct will only become clear at a Sydney court hearing on July 3, 2018.

What is cartel behaviour?

Cartels are forms of anti-competitive conduct where cartel participants decide to stop competing and start colluding. Australian civil law has banned cartels for decades. But the practice only became a criminal offence in 2010. Only its serious forms are subject to criminal law; civil law still governs the rest.

Cartels can take different forms. In the most common instance, participants collude by setting their prices. Other forms include: output restrictions; dividing markets among cartel participants on mutually agreed terms; and bid-rigging, in which a commercial contract is decided in advance but other operators put in sham bids to give the appearance of competition.

There is one primary reason why businesses or executives would stop competing and start colluding: profit. In short, cartel participants cheat to get more money, creating higher prices and lower output in the process. This disadvantages consumers, the economy and society at large.

But proving criminal collusion in a court is harder than it might seem.

Beyond reasonable doubt

Although we need to wait for the case to unfold to find out more, what we can tell at this stage is that the ACCC and the CDPP perceive the alleged conduct as serious enough for it to constitute a criminal case. Criminal cases are harder to prove than civil cases. Cartel collusion must be proved beyond reasonable doubt, and the evidence has to show that the individuals involved knew (or believed) that they were colluding.

What these charges also show is that the ACCC and the CDPP are prepared to go after the most powerful corporations and their executives for alleged cartel-like conduct. This is an enormously important step for deterrence, because criminal charges are naturally more attention-grabbing than civil lawsuits.

Charging high-ranking bank executives will potentially make the deterrent more effective still, because high-ranking executives set the cultural tone for their organisations.

Research has shown that significant prison time – or the threat of it – for individuals is a more effective deterrent than civil penalties; especially if the penalties are not high enough, as was argued in the recent OECD report on corporate penalties for cartels in Australia. The report showed that the penalties applied in Australia were low in comparison with competition law regimes in the European Union and the United States.

Just the beginning?

This is the second Australian criminal case of cartel conduct – the first involved a Japanese company shipping cars to Australia. We can reasonably expect more of these kinds of charges in the future, given that the laws are only eight years old and investigations of this type typically take years to reach fruition. (The alleged cartel conduct in the latest case took place in August 2015, almost three years ago.)

There are differences in investigation procedures between criminal and civil cases, to ensure that collected pieces of evidence are admissible in a criminal proceeding. It is ultimately the CDPP’s (and not the ACCC’s) decision whether or not to prosecute.

The final step is for criminal proceedings to be prosecuted. The first cartel criminal case, which concerned the shipping industry, can be perceived as successful, with two global shipping companies pleading guilty.

It is still early days for Australia in terms of tracking down and punishing examples of cartel behaviour via criminal prosecutions. But the latest developments suggest that Australia is prepared to follow the example of the world leader in successful cartel-related criminal prosecutions: the United States.

The US criminal regime is one of the oldest in the world, having existed since 1890. The US boom of cartel-related criminal cases began in the late 1990s with the lysine cartel and the vitamin cartel and with the first foreign national being sentenced to imprisonment in July 1999. One of the first criminal cartel investigations inspired the production of the 2009 movie The Informant!.

CBA has announced changes to its volume-based ‘diamond, gold, silver and bronze’ service model for brokers following advice from the Combined Industry Forum and intense questioning at the royal commission.

During the royal commission hearing on 15 March, Daniel Huggins, CBA’s executive general manager home buying, acknowledged that the bank decided to change the volume-based structure after acknowledging that it could create conflicts of interest with diamond brokers being awarded faster turnaround times and better service.

In a note to MPA on Wednesday, Huggins explained that the new two-tiered system is part of the bank’s “ongoing commitment to support and recognise brokers who are consistently delivering good customer outcomes”.

CBA’s previous model had 11 segments with the top being diamond. Those brokers who qualified had to write at least $15m and/or settle at least 75 CBA loans per year and achieve three out of five quality metrics.

Under the new regime, there will only be two categories: essential and elite.

The model moves away from volume-based requirements, as recommended by the Combined Industry Forum. Instead, a broker’s performance will be assessed on five key quality metrics and five complementary metrics. Their performance will be evaluated on a quarterly basis.

This should help even the playing field for regional brokers who generally have smaller average loan sizes and wouldn’t have made the top tier under CBA’s previous structure.

“We are really pleased to announce a simplified tiered service model with a focus on quality that seeks to recognise and reward our accredited brokers who deliver strong customer outcomes,” Huggins said.

CBA and accreditation

CBA also recently announced that instead of de-accrediting brokers who hadn’t written a loan with the major in 12 months, it would just require them to complete an e-learning training module to ensure they are updated on current products and criteria.

The bank said it will no longer require brokers to write a minimum number of loans to retain accreditation.

In the past, brokers who wanted to maintain CBA accreditation had to submit a minimum of four home loan applications and settle at least three every six months, although according to CBA this was not systematically enforced.

The royal commission revealed that in 2017 CBA revoked the accreditation of 710 brokers due to inactivity.

Mortgage Choice, the ASX-listed broking group has responded to media criticism regarding a high-sales culture and poor remuneration structures for franchisees, saying that it is working closely with franchisees to assist them in growing their business.

Mortgage Choice responded to the reports from the Sydney Morning Herald and the ABC’s 7:30 program, suggesting that its franchise system — which was introduced 25 years ago when the group was established by multimillionaire brothers Peter and Rodney Higgins — was in need of update.

“The market has evolved, with other business models being introduced, specifically aggregator models that have higher payouts but don’t offer the same level of support services,” Mortgage Choice said in a statement.

The brokerage acknowledged that the balance between services offered and remuneration “needs adjusting” to encourage franchisees to invest in their businesses. As such, the group has said that it will be undertaking a review of its franchisee remuneration structure, with a view of implementing a “more competitive” model.

Mortgage Choice has been consulting with its franchisees regarding a new remuneration model “to underpin long-term sustainable growth” and attract “new high-quality businesses to the franchise network”.

The company has reportedly been undertaking a “confidential and collaborative process” to update the remuneration model, which has included numerous workshops across Australia with franchisees and reviewing more than 30 different remuneration structures.

Subject to discussions with its franchise network and board approval, the new remuneration model would be introduced by August 2018.

Speaking following the media reports, Mortgage Choice CEO Susan Mitchell said: “We acknowledge that our model is outdated, it needs to be more flexible, it needs to be less volatile in the way it pays our franchisees.”

She continued: “Our business was started as a full service model. All the services that were need to help a broker start their own business, providing brand, marketing, IT, compliance, training and all those sorts of things.

“Over the years, since the introduction of the Mortgage Choice model, there have been other models that have been introduced — aggregator models — that pay out a higher proportion of income but don’t offer the same level of service. So what’s happened is, I believe, our balance between remuneration and provision of service has gotten out of kilter, so we just need to address that balance between remuneration and service provision.”

The new CEO said that one of the most important things she wanted to do as CEO was to “drive a change process”, and her “first priority was to change this model”.

Indeed, the need for updating the commission model has been further emphasised by the findings of the 2018 Momentum Intelligence Broker Group of Choice: Switching Aggregators report.

Based on a survey of mortgage brokers from across Australia, Mortgage Choice was rated the lowest of nine groups, with 90 per cent of Mortgage Choice brokers saying that the number one reason they would leave the group would be because of its commission structure.

However, the group did score highly for it compliance assistance.

Allegations of poor behaviour “strongly refuted”

Addressing some of the allegations in the 7.30 report, the CEO said that the company “strongly refutes allegations in the media that its current model encourages poor behaviour or practices”. It added that the company has in place “robust” compliance processes and credit policy controls, which franchisees must adhere to.

Ms Mitchell said: “Our franchisees are very diligent and want to do the right thing for their customers. We take any allegation of fraudulent behaviour extremely seriously and we have a very thorough and structured compliance regime in place.”

Several commentors on The Adviser website have also voiced their frustration with the misrepresentation, with Renee saying: “I have owned a Mortgage Choice franchise for nearly four years and the model has assisted me in building a successful business that I am very proud of.

“These recent media allegations are not a reflection of my experience with Mortgage Choice or a reflection of how I do business, and it’s disappointing that I am put in a position to have to defend this. Doing the right thing by our customers, and being known for this, is how my business has grown, and this will continue to be our priority.”

Likewise, Mortgage Choice franchise owner Maria Zappia said that while she supports the right to “demand a more consistent payment model”, she absolutely “refute[s] out of hand any suggestions displayed in recent media reports that ‘desperate times have called for desperate measures’ in terms of fraud or any other wrongdoing”.

The commenter said: “I have been with this business 15 years and have worked hard to build a strong vibrant business, as so many of my fellow franchise owners have done. I can assure you we have (and have had for quite some time) one of the most stringent compliance regimes of any aggregator in this country. We are well known among our panel of lenders, including all of the major banks, for the high quality of our loan submissions. Very importantly, we are well known among our many thousands of customers for our incredible levels of customer service.

“The challenges of running a small business in this industry are many, but those of us who choose this path do so with the utmost integrity and always in the best interests of our clients.”

She continued: “At Mortgage Choice, we are in the midst of great change and I’m convinced that our CEO Susan Mitchell, together with the executive team and our board, ha[s] matters well in hand and [is] committed to delivering a remuneration solution that will benefit all franchise owners. Let’s give them every opportunity to finish the job.”

Noting some of the suggestions that brokers have been affected by stress-induced health issues as a result of financial distress from running a franchise, Ms Mitchell said that she did not believe it was a “fair representation” of Mortgage Choice.

The CEO said: “It’s very difficult to run a small business in Australia today, and one of the reasons why you would join a franchise organisation like Mortgage Choice is we help you do that, and you have a higher chance of success by doing that.

“Having said that, as CEO, there have been circumstances where I worked one on one with franchisees on a confidential basis to help them when they had hardship or health issues.

“So, I think the important thing is we want to help franchisees through their issues. They just need to come and talk to use about them, and we’ll proactively work with them for a solution tailored to their needs.”

Ms Mitchell continued: “The wellbeing of our franchisees is our number one concern.

“We provide any business owner experiencing hardship with personalised support, including from our field‐based teams.”

She concluded: “We are well progressed in consulting with franchisees on a new remuneration model that will help them to succeed and invest in growing their businesses.”

Citigroup Global Markets Australia Pty Limited (Citigroup), Deutsche Bank Aktiengesellschaft (Deutsche Bank) and Australia and New Zealand Banking Group Ltd (ANZ) have been charged with criminal cartel offences following an investigation by the ACCC.

Criminal charges have also been laid against several senior executives: John McLean, Itay Tuchman and Stephen Roberts of Citigroup; Michael Ormaechea and Michael Richardson formerly of Deutsche Bank; and Rick Moscati of ANZ.

The charges involve alleged cartel arrangements relating to trading in ANZ shares held by Deutsche Bank and Citigroup. ANZ and each of the individuals are alleged to have been knowingly concerned in some or all of the alleged conduct.

The cartel conduct is alleged to have taken place following an ANZ institutional share placement in August 2015.

“These serious charges are the result of an ACCC investigation that has been running for more than two years,” ACCC Chairman Rod Sims said.

“Charges have now been laid by the Commonwealth Director of Public Prosecutions and the matter will be determined by the Court.”

The matter is listed before the Downing Centre Local Court in Sydney on 3 July 2018.

The Competition and Consumer Act requires any trial of such offences to proceed by way of indictment in the Federal Court of Australia or a State or Territory Supreme Court.

As this is a criminal matter currently before the Court, the ACCC will not be providing further comment at this time.

Background

The ACCC investigates cartel conduct, manages the immunity process and, in respect of civil cartel contraventions, takes proceedings in the Federal Court of Australia.

The Commonwealth Director of Public Prosecutions (CDPP) is responsible for prosecuting criminal cartel offences in accordance with the Prosecution Policy of the Commonwealth. The ACCC refers serious cartel conduct to the CDPP for consideration of prosecution in accordance with the Memorandum of Understanding between the CDPP and the ACCC regarding Serious Cartel Conduct.

According to the SMH, a joint media investigation by Fairfax and ABC’s 7.30 can reveal scores of current and former franchisees have been financially devastated after signing up to the high profile brand.

One of the country’s biggest mortgage brokers, Mortgage Choice, is in damage control as it faces an uprising from its franchisees on the back of a business model that is pushing many into financial ruin, depression and cutting corners on arranging loans.

Confidential documents show as many as 173 franchisees, almost half the franchisees in the system, are considering setting up a fighting fund to take legal action if the company doesn’t make the relationship fairer. Late last year they agreed to commit almost $200,000 to set up the fund if their demands aren’t met.

The investigation can reveal that a harsh business model and remuneration structure is pushing franchisees to cut corners, including churning customers, writing inflated loans to meet aggressive targets and in some cases committing fraud.

Mortgage Choice, which has a loan book worth $54 billion, has been making record profits for its shareholders, which include Commonwealth Bank and the founders, the Higgins brothers, who also sit on the board.

On Monday, shortly after being contacted by the joint investigation, Mortgage Choice issued a statement to the ASX saying it was reviewing its franchisee remuneration structure. It says the purpose of an “updated remuneration model was to increase franchisee remuneration and reduce franchisee income volatility to allow them to grow their businesses and assist more customers with their home loan needs.

Commonwealth Bank of Australia (CBA) has announced it has entered into an agreement with AUSTRAC, the Australian Government’s financial intelligence agency, to resolve the civil proceedings commenced by AUSTRAC in the Federal Court of Australia on 3 August 2017.

The agreement follows Court-ordered mediation between CBA and AUSTRAC and remains subject to Court approval. As part of the agreement:

CBA will pay a civil penalty of $700 million together with AUSTRAC’s legal costs of $2.5 million.

CBA has admitted further contraventions of Australia’s Anti-Money Laundering and Counter-Terrorism(AML/CTF) Act, beyond those already admitted, including contraventions in risk procedures, reporting,monitoring and customer due-diligence.

AUSTRAC’s civil proceedings are otherwise dismissed.

CBA Chief Executive Officer Matt Comyn said: “This agreement, while it still needs to be approved by the Federal Court, brings certainty to one of the most significant issues we have faced.

“While not deliberate, we fully appreciate the seriousness of the mistakes we made. Our agreement today is a clear acknowledgement of our failures and is an important step towards moving the bank forward. On behalf of Commonwealth Bank, I apologise to the community for letting them down.

“Banks have a critical role to play in combating financial crime and protecting the integrity of the financial system. In reaching this position, we have also agreed with AUSTRAC that we will work closely together based on an open and constructive approach.

“We are committed to build on the significant changes made in recent years as part of a comprehensive program to improve operational risk management and compliance at the bank. To date we have spent over $400 million on systems, processes and people relating to AML/CTF compliance and will continue to prioritise investment in this area.

“We have changed senior leadership in the key roles overseeing financial crimes compliance supported by significant resources and clear accountabilities.

“We have started implementing our response to the recommendations provided to us by our prudential regulator, APRA, to ensure our governance, culture and accountability frameworks and practices meet the high standards expected of us.

“I am also very focused on ensuring we have clear lines of accountability across our entire business. This includes an approach to risk management that recognises the importance of non-financial risks, including an escalation framework that ensures key operational and compliance issues such as these are identified, escalated and resolved in a timely manner.

“These changes are part of a large and concerted effort to become a better, stronger bank – one that earns the trust of our customers, staff, regulators and shareholders. Today is another very important step forward, and continuing to make the changes we need in an open, transparent and timely way is my absolute priority as CBA’s new chief executive,” Mr Comyn said.

CBA provided for an estimated penalty of $375 million in the half year ending 31 December 2017 at which time the bank noted the proceedings were complex and ongoing, and the ultimate penalty determined by the Court may be higher or lower than the amount provided for. CBA will recognise a $700 million provision in its financial statements for the full year ending 30 June 2018 which will be announced on 8 August.

Background

The settlement with AUSTRAC includes a Statement of Agreed Facts and Admissions. A copy of the Statement is attached to this announcement and is available on CBA’s website. In summary, as part of the agreement CBA has admitted to:

Late filing of 53,506 Threshold Transaction Reports for cash deposits through Intelligent Deposit Machines (IDMs).

Inadequate adherence to risk assessment requirements for IDMs on 14 occasions.

Transaction monitoring did not operate as intended in respect of a number of accounts between October 2012 and October 2015.

149 Suspicious Matter Reports were filed late or were not filed as required.

Ongoing customer due-diligence requirements were breached in respect of 80 customers.

We appreciate the key role we play in supporting law enforcement to fight financial crime. Our contribution includes:

During the period of the claim, we submitted more than 44,000 Suspicious Matter Reports, including 264 SMRs in relation to the syndicates and individuals referred to in AUSTRAC’s claim.

We submitted more than 19 million reports to AUSTRAC (including SMRs, TTRs and international fund transfer instructions) during the period covered by the AUSTRAC claim up to the end of 2017. We submitted over 4 million of these reports to AUSTRAC in 2017 alone.

We responded to approximately 20,000 law enforcement requests for assistance in 2017.

CBA has made significant progress in strengthening its policies, processes and systems relating to its obligations under the AML/CTF Act through our Program of Action. This is a continuing process of improvement and has already included:

Boosting AML/CTF capability and reporting by hiring additional financial crime operations, compliance and risk professionals with more than 300 professionals dedicated to financial crimes operations, compliance and risk across the group.

Strengthening Know Your Customer processes with the establishment in 2016 of a specialist hub providing consistent and high-quality on-boarding of customers, at a cost of more than $85 million.

Launching an upgraded financial crime technology platform used to monitor accounts and transactions for suspicious activity.

Adding new controls such as using enhanced digital electronic customer verification processes to supplement face-to-face identification to reduce the risk of document fraud.

Introducing an account based daily limit of $10,000 for cash deposits using IDMs, the first Australian bank to do so.

The Commonwealth Director of Public Prosecutions (CDPP) advised ANZ late yesterday it intends to commence proceedings against the bank for being knowingly concerned in alleged cartel conduct by the joint lead managers of ANZ’s underwritten Institutional Equity Placement of approximately 80.8 million shares in August 2015.

The proceedings relate to an arrangement or understanding allegedly made between the joint lead managers in relation to the supply of ANZ shares. ANZ understands the CDPP also intends to bring proceedings against ANZ Group Treasurer Rick Moscati.

ANZ Chief Risk Officer Kevin Corbally said: “We believe ANZ acted in accordance with the law in relation to the placement and on that basis the bank intends to defend both the company and our employee.”

ANZ is also co-operating with an investigation by the Australian Securities and Investments Commission (ASIC) in relation to the placement.

ASIC is investigating whether ANZ’s announcement of 7 August 2015 should have stated the joint lead managers took up approximately 25.5 million shares of the placement. This represented approximately 0.91% of total shares on issue at that time.

ANZ does not intend to provide further comment at this time.

Following an announcement made by ANZ to the ASX this morning regarding anticipated criminal cartel charges, the ACCC confirms that criminal cartel charges are expected to be laid by the Commonwealth Director of Public Prosecutions (CDPP) against ANZ, ANZ Group Treasurer Rick Moscati, two other companies and a number of other individuals. These charges will be laid following an investigation by the ACCC.

“The charges will involve alleged cartel arrangements relating to trading in ANZ shares following an ANZ institutional share placement in August 2015,” ACCC Chairman Rod Sims said.

“It will be alleged that ANZ and the individuals were knowingly concerned in some or all of the conduct.”

The ACCC will not make any further comment until charges are laid.

Background

The ACCC investigates cartel conduct, manages the immunity process and, in respect of civil cartel contraventions, takes proceedings in the Federal Court of Australia.

The CDPP is responsible for prosecuting criminal cartel offences in accordance with the Prosecution Policy of the Commonwealth. The ACCC refers serious cartel conduct to the CDPP for consideration of prosecution in accordance with the Memorandum of Understanding between the CDPP and the ACCC regarding Serious Cartel Conduct.

Further to its earlier statement regarding criminal cartel charges expected to be laid by the Commonwealth Director of Public Prosecutions (CDPP) against ANZ and its Group Treasurer Rick Moscati, the ACCC can confirm that Deutsche Bank AG is one of the two other companies against which charges are expected to be laid, along with a number of individuals.

The expected charges follow an extensive ACCC criminal cartel investigation.

The ACCC will not make any further comment until charges are laid.

Further to its earlier statements regarding criminal cartel charges expected to be laid by the Commonwealth Director of Public Prosecutions (CDPP) against ANZ, its Group Treasurer Rick Moscati, and Deutsche Bank, the ACCC can confirm that Citigroup Global Markets Australia Pty Limited is the other company against which charges are expected to be laid, along with a number of individuals.

The expected charges follow an extensive ACCC criminal cartel investigation.

The ACCC will not make any further comment until charges are laid.

Misconduct exposed by the banking Royal Commission is the tip of the iceberg, with the catastrophic consequences of Australia’s broken financial sector yet to be revealed, according to a Deakin University corporate law expert.

Deakin Law School’s Professor Gill North, who has a background as a chartered accountant and financial analyst, as well as doctorate in law, said the Royal Commission would not fully address the broader impact of financial misconduct.

“Australians are horrified now by what they’re learning from the Royal Commission, but news on the finance sector is set to get much worse, with likely catastrophic consequences,” Professor North said.

“Systemic risks across the financial sector are already much higher than most people realise, and these risks are being exacerbated by the concentration of the sector, lax lending standards, high levels of household debt, and the heavy reliance of the economy on the health of the residential property market.

“As levels of household debt and financial stress rise, disparities between those who have considerable income, savings and wealth buffers and those who don’t will only become starker.

“The true resilience of the financial institutions, their consumers, and the broader economy will be tested and put under extreme pressure at some point – much of Australia is in for a bumpy and uncomfortable ride.”

Professor North is co-director of the analyst firm Digital Finance Analytics and has worked in senior executive positions at multinational corporations and investment banks in major financial centres including London, Tokyo, New York and Sydney.

She said the Royal Commission was shining a light on the most powerful corporations in Australia, but the investigation so far had been predominantly restricted to the most significant examples of non-compliance with the law by the largest financial institutions.

“The dirty linen of these entities and the practices they’ve gotten away with for many years are finally being effectively challenged,” Professor North said.

“The Commission is expected to have a profound and long-lasting impact on the sector, however the many governance and systemic concerns that flow from the identified misconduct are unlikely to be fully examined and addressed.”

Professor North said the Commission’s recommendations could include changes to consumer lending, while opening the door to future litigation.

“Changes to the consumer credit regimes under the National Consumer Protection Act are inevitable, including the way loan brokers can be remunerated and the processes used by lenders to verify information provided by consumers and intermediaries,” she said.

“The Commission has provided additional information and admissions that corporate regulator ASIC could use in actions against lenders, credit assistance providers, financial advisers, and directors.

“But future litigation in this space won’t be limited to regulators – actions by consumers who were issued loans or provided financial advice in breach of the law are likely to accelerate, and become a flood of litigation as the circumstances in Australia deteriorate and household financial stress levels climb to new records.”

When I last addressed this Committee, I outlined some of the many ways APRA is accountable to both the Parliament and the Australian people. These measures are crucial for APRA to maintain the trust of industry and the public as we aim to fulfil our mandate as a prudential regulator, promoting financial safety and thereby protecting the interests of bank depositors, insurance policyholders and superannuation members.

The core of APRA’s mission is safety and soundness. Clearly, some of the revelations emerging from the Royal Commission have been disturbing and go to the heart of whether financial institutions treat their customers fairly. However, while institutions have a great deal of work to do to restore trust, I want to emphasise that Australians can be reassured that the industry is financially sound, and that the financial system is stable. That reflects considerable policy reform and hands-on supervision, over a long period of time, designed to build strength and resilience. We don’t know when the next period of adversity will arrive or what will trigger it, but when it does arrive we need to have done what we could to strengthen the financial system so that it can continue to provide its essential services to the Australian community when they are needed most.

The importance of accountability has been one of our key themes this year, and was front and centre with the release in April of our review of executive remuneration practices in large financial institutions. Incentives and accountability can play an important role in driving positive outcomes such as growth, innovation and productivity, and also in deterring behaviours or decisions that produce poor risk-taking and damaging results. Our review found that while policies and processes existed within institutions to align remuneration with sound risk outcomes, their practical application was often weak. We have indicated that we are minded to strengthen the prudential framework to give better effect to the principles we want to see followed – less rewards based on narrow and mechanical shareholder metrics, and greater exercise of Board discretion to judge senior executive performance more holistically. But we have also urged institutions to push ahead with their own improvements, notwithstanding some investor opposition, in light of the long-term commercial benefits that can flow from better remuneration practices.

A lack of accountability for poor outcomes was a theme that also emerged in the Final Report of the Prudential Inquiry into the Commonwealth Bank of Australia, which was released earlier this month. The Report is clear and comprehensive, and provides a strong message – not just to CBA but to the entire financial services industry – about the importance of cultivating a robust risk culture, especially when it comes to non-financial risks. We are keen that the Report will be seen not just a road map for CBA, but a useful guide for all institutions in relation to strengthening governance, culture and accountability.

Residential mortgage lending is another area where APRA has been lifting industry standards. Although there remains more to do before we are ready to significantly dial back our supervisory intensity, there has been a lift in industry lending practices. As a result, last month we announced we would remove the 10 per cent investor growth benchmark for those lenders who could provide a range of assurances as to the quality of their lending standards and practices now and into the future.

Superannuation is an area where APRA consistently emphasises the need for trustees, regardless of size or ownership structure, to go beyond compliance with minimum regulatory requirements and aim to deliver the best possible outcomes for members. In this vein, we have just released the results of two thematic reviews of superannuation licensees; on board governance and the management of related parties. Both reviews noted improvements in industry practices in recent years, but also found more work was needed to address some longstanding weaknesses, including finding ways to bring fresh ideas, perspectives and skills onto trustee boards. Our post-implementation review of 2013’s Stronger Super reforms, launched last week, should also provide us additional insights on how the prudential framework is performing, and whether any adjustments would help to better achieve our objectives. Many of the findings in the Productivity Commission report into superannuation released this week are consistent with APRA’s approach to supervising RSE licensees. In particular, they align with APRA’s focus on enhancing the delivery of member outcomes through our engagement with trustees with “outlier” underperforming funds and products.

Technology is rapidly changing the way financial institutions operate. In all likelihood, the financial system will look very different in five years’ time relative to the way it looks today. Much of that change will bring benefits to the community, in the form of new competitors, products and ways of access. But it will also bring risks, and the accelerating threat of cyber-attacks to regulated entities has prompted APRA to recently propose its first prudential standard on information security. Industry consultation is ongoing, but we hope to implement the new cross-industry standard from 1 July next year. This is an issue which is only going to grow in importance.

Continuing to look ahead, APRA’s preparations are well advanced for the commencement of the Banking Executive Accountability Regime (BEAR), which will begin in just over a month. The BEAR largely strengthens APRA’s existing powers to identify and address the prudential risks arising from poor governance, weak culture, or ineffective risk management. However, I have made the point previously that while important, the BEAR alone will not remedy perceived weakness in financial sector accountability, and we have encouraged all regulated entities – not just ADIs – to use the new regime as a trigger to genuinely improve systems of governance, responsibility and accountability.

Finally, APRA is continuing to provide relevant information to the Royal Commission to help it in its inquiries. In addition, APRA and the Australian financial system more broadly, will be subject to intensive scrutiny from the International Monetary Fund in the weeks ahead as part of its 2018 Financial Sector Assessment Program (FSAP). The FSAP will examine in quite some detail financial sector vulnerabilities and the quality of regulatory oversight arrangements in Australia. As ever, APRA will fully cooperate with our international reviewers, and look forward to their report card, including any recommendations on how we could perform our role more effectively in the future.

With those opening remarks, we would now be happy to answer the Committee’s questions.

At first blush the news at home and abroad appears to be steering us towards our most risky – scenario 4 outcome, where global financial markets are disrupted and home prices fall by 20-40 percent or more as confidence wains.

Some would call this GFC 2.0. So let’s looks at the evidence.

In Australia, as we predicted, a massive class action lawsuit is being planned on behalf of “Australian bank customers that have entered into mortgage finance agreements with banks since 2012”.

Law firm Chamberlains has been appointed to act in the planned class action lawsuit, which has been instructed by Roger Donald Brown of MortgageDeception.com in the action that aims to represent various Australian bank customers that are “incurring financial losses as a result of entering into mortgage loan contracts with banks since 2012”.

As the AFR put it – Lawyers’ representing up to 300,000 litigants are planning an $80 billion action against mortgage lenders, mortgage brokers and financial regulators in a class action that would dwarf previous actions. Roger Brown, a former Lloyds of London insurance broker, said he already has about 200,000 borrowers ready to join the action and has $75 million backing from UK and European investors. There has been a scam, he said about mortgage lending to Australian property buyers. “But the train has hit the buffers and there needs to be recompense.

As we discussed before, if loans made were “unsuitable” as defined by the credit legislation, there is potential recourse. This could be a significant risk to the major players if it gains momentum. And more will likely join up if home prices fall further and mortgage repayments get more difficult. But we think individuals must take some responsibility too!

Next, we now see a number of the major media outlets starting to blame the Royal Commission for the falls in home prices, tighter lending standards and even damage to the broader economy. Talk about shoot the messenger. The fact is we have had years of poor lending practice, and poor regulation. But the industry and regulators kept stumn preferring to enjoy the fruits of over generous lending. The Royal Commission is doing a great job of exposing what has been going on. In fact, the reaction appears to be that what had been hidden is now in the sunshine, and it is true the sunlight is the best disinfectant. Structural malpractice is being exposed, some of which may be illegal, and some of which certainly falls below community expectations. But let’s be clear, it’s the poor behaviour of the banks and the regulators which have placed us in this difficult position. Hoping bad lending remans hidden is a crazy path to resolution. At least if the issues are in the open they stand a chance of being addressed.

But it is also true that just a lax lending allowed households to get bigger mortgages than they should, and bid home prices higher, to be benefit of the banks, and the GDP out-turn, the reverse is also true. Tighter lending will lead to less credit being available, which in turn will translate to lower home prices, and less book growth for the banks. But do not lay this at the door of the Royal Commission. They are actually doing Australia a great service, in a most professional manner.

But that does not stop the rot. UBS came out today with an update saying that the housing market is slowing, with house prices falling and credit conditions tightening. Given the number of headwinds the market is facing; many investors are now questioning whether the housing correction could become disorderly. We expect credit growth to slow sharply and believe the risk of a Credit Crunch is rising.

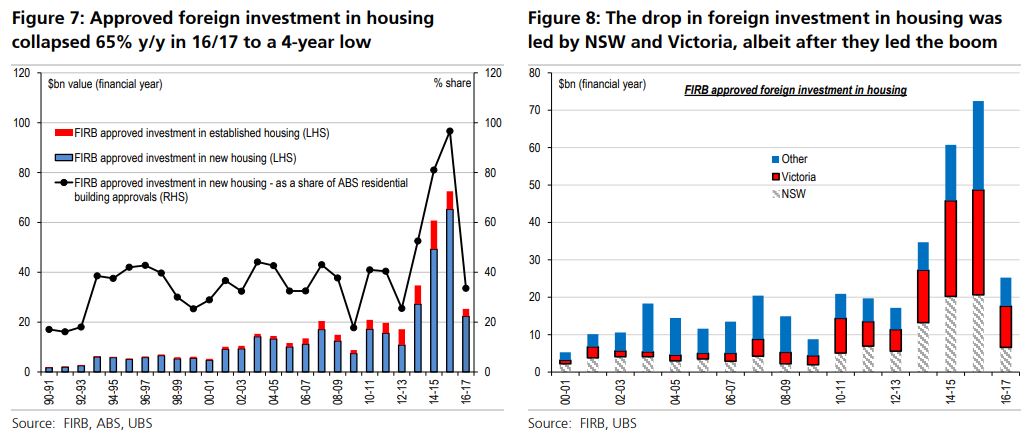

They walk through the main areas, including tighter lending, interest only loans and foreign buyers. Specifically, they highlight that approved foreign investment in housing is down -65%. The Foreign Investment Review Board just released data for 16/17. The value of approvals to buy residential housing collapsed 65% y/y to $25bn in 16/17, the lowest level since 12/13, and mostly reversing the prior ‘super boom’. The fall was across both new (-66% to $22bn) and established housing (-59% to $3bn) – led by total falls in NSW (-66% to $7bn) and Victoria (-61% to $11bn.

They say that the collapse in 16/17 may be overstated because of the introduction of application fees in Dec-15 – meaning the fall in transactions is less pronounced. But, there is still likely to have been a drop in transactions, reflecting more structural factors including – the lift in taxes on foreigners; domestic lenders tightening standards for foreign buyers (effectively no longer lending against foreign sources of income or collateral); as well as tighter capital controls especially from China.

Their base case is for a small fall in prices ahead, and assumes house prices fall by 5%+ over the coming year and that bad and doubtful debts increase only modestly given the current very benign credit environment. but they also talk about a downside scenario which reflects a more disorderly correction in the housing market (ie a Credit Crunch) and could result in approximately 40% reduction in major bank share prices. This is likely due to credit growth falling more substantially, by ~2-3% compound and credit impairment charges rising significantly as the credit cycle turns. This scenario would put pressure on bank NIMs. Litigation risk from class actions for mortgage misselling is also a tail risk. Dividends would need to be cut in this scenario. Given the leverage in the banking system, accurately predicting the extent of a downturn is very difficult, as was seen in 2008.

And the reason they still hold to their milder view is the expectation that the Government will step in to assist, and slow the implementation of recommendations from the Royal Commission. To quote Scott Morrison on 2GB radio on 23d March.

If banks stop lending, then what do people think that is going to mean for people starting businesses or getting loans or getting jobs or all of this. In the budget papers, the Treasury have actually highlighted this as a bit of a risk with the process we are going through. We have got to be very careful. These stories are heartbreaking, I agree, but we have to be also very cautious about, well, how do we respond to that. What is the right reaction to that? Is it to just throw more regulation there which basically constipates the banking and financial industry which means that people can’t start businesses and people can’t get jobs, people can’t get home loans. Or do we want to move to a smarter way of how this is all done and I think in the era of financial technology in particular there are some real opportunities there. We are going to continue to listen and carefully respect the royal commission, not prejudge the findings, but be very careful about any responses that are made because this can determine how strong an economy we live in over the next ten years and whether people get jobs and start businesses.

But in essence, expect some unnatural acts from the Government to try to keep the bubble going a little longer. All bets are off the other side of the election.

And the third risk, and the one which takes us closest to GFC 2.0 is what is happening in Italy. I am not going to go back over the history, but after months of wrangling, Italy’s political crisis has a hit an impasse, with new elections now increasingly likely. The country faces an institutional crisis without precedent in the history of the Italian republic. Its implications extend well beyond Italy, to the European Union as a whole.

Since an election on March 4, there have been endless vain attempts to form a government – with the likely outcome changing every 24 hours. By mid-May, the Five Star Movement (M5S) and the League, both populist parties, had come together to draft a programme for government featuring tax cuts and spending plans. But it sent shivers down the spines of those contemplating Italy’s public debt – running at over 130% of GDP – and threatened the stability of the eurozone.

The appointment of Carlo Cottarelli, a former official from the International Monetary Fund, as prime minister on May 28 was merely a stop-gap measure until fresh elections in the autumn. His government will almost certainly fail to win the necessary vote of confidence required of all incoming governments upon taking office. This means that it will be unable to undertake any legislative initiatives that go beyond day-to-day administration.

ITALY’S president, Sergio Mattarella had originally planned to put a former IMF economist, Carlo Cottarelli, at the head of a government of technocrats, tasked with steering the country back to the polls after the summer. But Mr Mattarella was reportedly considering changing tack after meeting Mr Cottarelli on May 29th amid growing evidence of support in parliament for an earlier vote. Not a single big party has declared its readiness to back Mr Cottarelli’s proposed administration in a necessary vote of confidence.

So the president is expected to decide on May 30th whether to call a snap election as early as July in an effort to resolve a rapidly deepening political and economic crisis that has sent tremors through global financial markets. There was also concern that the populist parties could win a bigger parliamentary majority in the new election, creating a bigger risk for the future of the eurozone.

In a sign of investors’ concern, the yield gap between Italian and German benchmark government bonds soared from 190 basis points on May 28th to more than 300. The governor of the Bank of Italy, Ignazio Visco, warned his compatriots not to “forget that we are only ever a few steps away from the very serious risk of losing the irreplaceable asset of trust.”

The yield on two-year debt has risen from below zero to close to 2% and Italy’s 10-year bond yields, which is a measure of the country’s sovereign borrowing costs, breached 3 per cent on Tuesday, the highest in four years. At the start of the month they were just 1.8 per cent. Italy’s sovereign debt pile of €2.3 trillion is the largest in the eurozone

The Italian stock market was also down 3 per cent on Tuesday, and has lost around 13 per cent of its value this month.

But these movements need to be put in some context. The Italian stock market is still only back to its levels of last July, after experiencing a strong bull run since later 2016.

In 2011 and 2012 Italian bond breached 7 per cent and threatened a fiscal crisis for the government in Rome. Yields are still some distance from those extreme distress levels.

George Soros was quoted in the FT:

The EU is in an existential crisis. Everything that could go wrong has gone wrong,” he said. To escape the crisis, “it needs to reinvent itself.” Mr Soros said tackling the European migration crisis “may be the best place to start,” but stressed the importance of not forcing European countries to accept set quotas of refugees. He said the Dublin regulation — which decides which nation is responsible for processing a refugee’s asylum status, largely based on which country the individual first enters — had put an “unfair burden” on Italy and other Mediterranean countries, “with disastrous political implications.” While austerity policies appeared initially to have been working, said Mr Soros, the “addiction to austerity” had harmed the euro and was now worsening the European crisis. US president Donald Trump’s exit from the nuclear arms deal with Iran and the uncertainty over tariffs that threaten transatlantic trade will harm European economies, particularly Germany’s, he said, while a strong dollar was prompting “flight” from emerging market economies. “We may be heading for another major financial crisis,” he said. Meanwhile, years of austerity policies had led working people to feel “excluded and ignored,” sentiment that had been exploited by populist and nationalistic politicians, said Mr Soros. He called for greater emphasis on grassroots organisations to meaningfully engage with citizens.

To play devil’s advocate, if Italy were to leave the Eurozone, the Lira would drop, hard. Most probably Italy would default on debt, and this would hit the Eurozone banks hard, especially those in German and French banks will be hit hard and they are saddled with about half the outstanding debt. Just like in the GFC a decade back, global counter-party bank risk will rise, and this time sovereign are involved, so it may go higher. The US Dollar will run hot, and there will be a flight to quality, tightening the capital markets, lifting rates and causing global stocks and commodities to crash, possibly a recession will follow.

In Australia, the dollar would slide significantly, fuelling stock market falls and a further drop in home prices, leading to higher levels of default, and recession, despite the Reserve Bank cutting rates and even trying QE.

Now the financial situation in Italy at the moment, a far cry from the height of the eurozone crisis in 2012, when it really did look possible that weaker member states would be imminently forced to default and the single currency would collapse. Then, that situation was finally defused when the head of the European Central Bank, Mario Draghi, announced he would do “whatever it takes” to stop this break up happening, unveiling an emergency programme of backstop bond buying by the central bank. This reassured private investor that they would, at least, get their money back and bond yields in countries like Italy and Spain fell back to earth, ending the risk of a destructive debt spiral.

But the latest deadlock in Rome is nevertheless the biggest crisis in the eurozone since Greece last threatened to leave in 2015. And Italy is a much larger economy than Greece. If the third largest country in the bloc exited the euro, it is doubtful the single currency would survive.

Falling bank shares dragged down Europe’s main share markets. At the close the UK’s FTSE 100 fell almost 1.3%, while Germany’s Dax was down 1.5% and France’s Cac 1.3% lower. “It’s a market that is totally in panic”, said a fund manager at Anthilia Capital Partners, who noted “a total lack of confidence in the outlook for Italian public finances”. And the chief economic adviser at Allianz in the US said: “If the political situation in Italy worsens, the longer-term spill overs would be felt in the US via a stronger dollar and lower European growth.”

So whether you look locally or globally its risk on at the moment, and we are it seems to me teetering on the edge of our Scenario 4. This will not be pretty and it will not be quick. I see that slow moving train wreck still grinding down the tracks, with no way out.