Global litigation firm Quinn Emanuel Urquhart & Sullivan is investigating a class action lawsuit against AMP for shareholder losses following revelations at the royal commission last week.

Giving evidence before the royal commission, AMP head of financial advice Jack Regan admitted his firm lied to ASIC on 20 separate occasions about its practice of providing ‘fees for no service’ to financial advice clients.

Quinn Emanuel has backing from global litigation funding firm Burford Capital for the potential class action.

The class action is open to shareholders who acquired shares between 24 May 2013 and 16 April 2018.

Quinn Emanuel partner Damian Scattini said: “The revelations of AMP’s misconduct are especially upsetting given the people who were hurt – the ordinary Mums and Dads who as shareholders gave AMP one of Australia’s largest shareholder registers, who have now lost their savings due to its dishonesty, and who as customers were charged for services AMP has admitted they never received, all so executives could make hefty bonuses.”

“QE has been investigating AMP’s precipitous share price fall even before the most recent revelations of misconduct, and having Burford, the world’s top litigation finance company, in place as our partner means we’re ready to move quickly on behalf of shareholders,” Mr Scattini said.

Burford managing director Craig Arnott said: “The conduct admitted at the Royal Commission is starkly at odds with AMP’s responsibilities and shareholders’ legitimate expectations, requiring redress so that AMP’s shareholders can recover the value that has been lost.

“Burford is glad to join forces with Quinn’s first-rate team so we can help deliver that result for shareholders, which we hope will be as swift as possible.”

Former prime minister Tony Abbott has strongly condemned the performance of financial sector regulators, suggesting they should be sacked and replaced by “less complacent” people.

With increasing attention on the apparently inadequate performance of the Australian Securities and Investments Commission (ASIC), Abbott raised the question of what the regulators had been doing as the scandals had gone on.

“We all know there are greedy people everywhere, including in the banks,” he told 2GB on Monday. “But banking is probably the most regulated sector of our economy. What were the regulators doing to allow all this to be happening?”

Abbott said his fear was “that at the end of this royal commission we will have yet another level of regulation imposed upon the banks when frankly what should happen is, I suspect, all the existing regulators should be sacked and people who are much more vigilant and much less complacent go in in their place.”

He said the analogy was, “yes, punish the criminals but if the police are turning a blind eye to the criminals, you’ve got to get rid of the police and get decent people in there”.

Meanwhile Malcolm Turnbull, speaking to reporters in Berlin, defended refusing for so long to set up a royal commission, although he said commentators were correct in saying that “politically we would have been better off setting one up earlier”.

Turnbull said that by taking the course it had the government “put consumers first”.

“The reason I didn’t proceed with a royal commission is this – I wanted to make sure that we took the steps to reform immediately and got on with the job.

“My concern was that a royal commission would go on for several years – that’s generally been the experience – and people would then say, ‘Oh you can’t reform, you can’t legislate, you’ve got to wait for the royal commissioner’s report.’

“So if we’d started a royal commission two years ago, maybe it would be finishing now and then we’d be considering the recommendations … With the benefit of hindsight and recognising you can’t live your life backwards, isn’t it better that we’ve got on with all of those reforms?”

Turnbull dismissed Bill Shorten’s call for the government to consider a compensation scheme for victims by saying this matter was already in the commission’s terms of reference.

Among the reforms it has made, the government highlights giving ASIC more power, resources and a new chair.

But Nationals backbencher senator John Williams, who has been at the forefront of calls for tougher action against wrongdoing in the financial sector, told the ABC that ASIC has got to be “quicker, they’ve got to be stronger, they’ve got to be seen as a feared regulator.

“That is not the situation at the moment,” he said.

He had sent a text message to Peter Kell, ASIC deputy chair, a couple of nights ago “and I said, mate, Australia is waiting for you to act”.

Asked how the culture within ASIC could be changed, Williams said, “I suppose you keep asking them questions at Senate estimates, keep the pressure on them, keep the message going on with the management of ASIC regularly.

“As I have said to the new boss [chair James Shipton], you’ve got to act quickly, you’ve got to be severe, you’ve got to be feared. If you’re not a feared regulator, people are going to continue to abuse the system, do the wrong thing without fear of the punishment”.

He welcomed the increased penalties announced by the government last week.

The chair of the Australian Competition and Consumer Commission (ACCC), Rod Sims, while declining to comment on ASIC, said he agreed with Williams “that you really do have to be feared. And frankly I’d like to think the ACCC is.

“I won’t comment on others but you want people to be really watching out – watch out for the ACCC, watch out that you don’t get caught because if they catch us it’s going to be really dire consequences. And I think we’ve got that mentality,” he told the ABC.

Updated at 4:30pm

In an interview on Sky late Monday, Finance Minister Mathias Cormann admitted, “With the benefit of hindsight, we should have gone earlier with this inquiry.” This was in stark contrast with his colleague, Minister for Financial Services, Kelly O’Dwyer, refusing to make the concession when she was repeatedly pressed in an interview on Sunday.

Author: Michelle Grattan, Professorial Fellow, University of Canberra

Given the range of issues already exposed by the Royal Commission into Financial Services Misconduct, including selling loans outside suitable criteria, fees from advice not given and other factors; we need to ask about the impact on the profitability of the banks and so share prices.

And all this is in the context of higher funding costs already hitting.

A number of international investors and hedge funds have placed shorts on the major banks, signalling an expectation of further falls in share price ahead, but the majors have already dropped by around 15% in the past year.

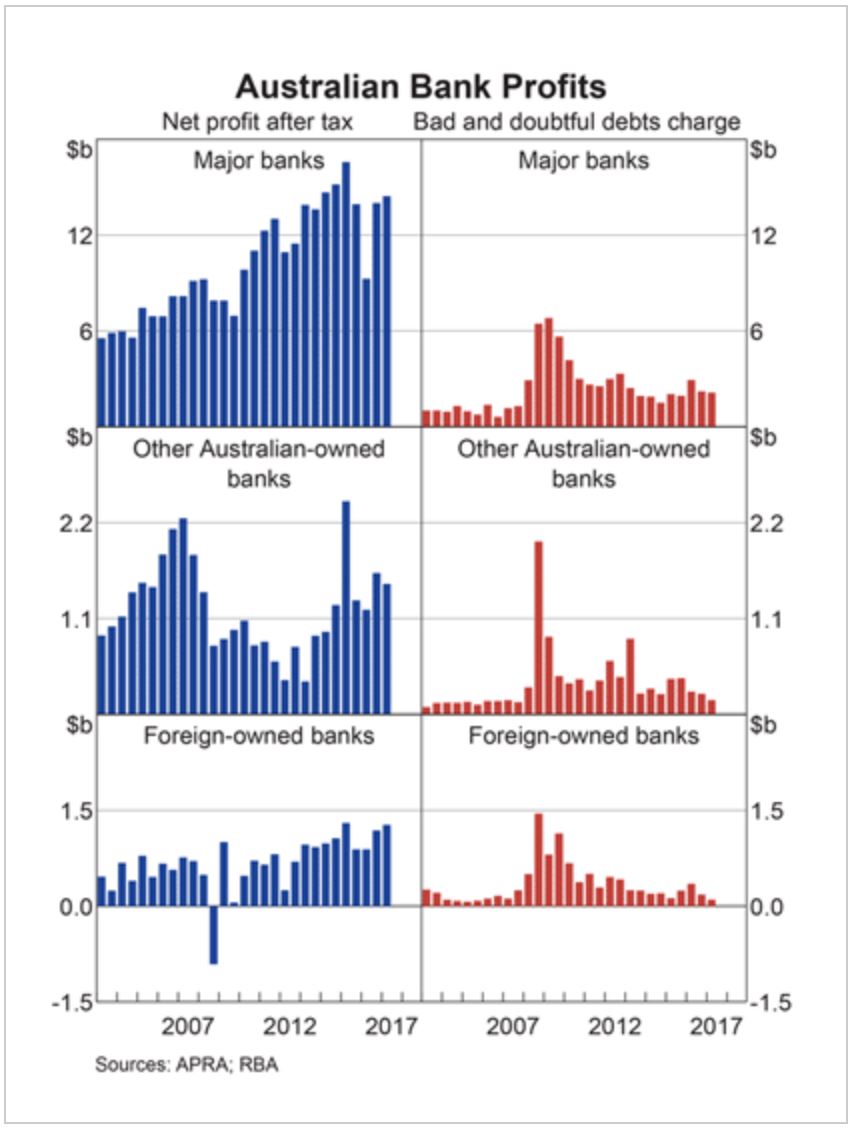

The recent RBA chart pack contained this picture on profitability. Bad and doubtful debts are very low, thanks to low interest rates. But that may change if rates were to rise, and “liar loans” are wide spread. There is no good data on the potential impact so far.

It is important to remember the Productive Commission recently called out that :

A quick survey of the banks from last year show that the return on equity – a measure of absolute profitability – or ROE range from 14.5% for CBA, 10.3% from NAB, 10.9% for ANZ and Westpac was 13.3% while AMP was 11.5%.

Looking overseas, US based Wells Fargo, which happens to be a key Warren Buffett holding, was 11.5% , the Bank of America earned less than 6.8% and Lloyds earns 4%. Barclays was -2.7%. In fact among western markets, only Canadian banks come close to our ROE’s – for example of Bank of Montreal was 11.3% but then they have the same structural issues that we do.

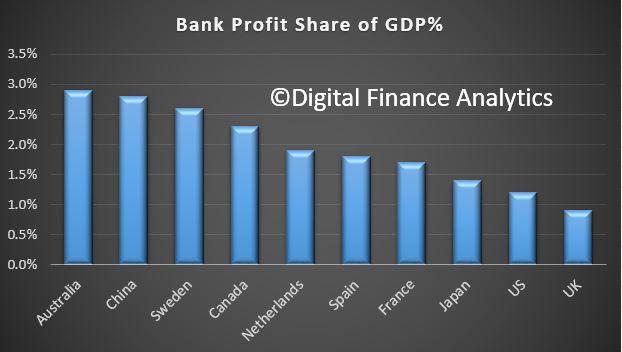

Data from news.com.au from 2016 shows the relative profit to GDP across several countries. Australia Wins.

That means 2.9 per cent of every $100 earned in Australia ends up as bank pre-tax profit, compared to the US and UK at $1.2 and 90 cents per cent respectively.

China is the highest after Australia at $2.80, Sweden $2.60 and Canada $2.30.

The Australia Institute also pointed to public money being used to secure the banking sector.

“Excessive profits provide a drag on the economy and hurt consumers who pay higher margins on bank products. The Reserve Bank found the big four banks enjoy an implicit government subsidy worth up to $4 billion dollars a year,”

The Royal Commission revelations have the potential to impact the market value of the banks as reflected in their share prices, and also raises questions about the financial stability of the entire system in Australia. APRA, in particular and the RBA have been (over?) focussed on financial stability, as the recent Productive Commission draft report highlighted.

Regulators have focused on a quest for financial stability prudential stability since the Global Financial Crisis, promoting the concept of an unquestionably strong financial system.

The institutional responsibility in the financial system for supporting competition is loosely shared across APRA, the RBA, ASIC and the ACCC. In a system where all are somewhat responsible, it is inevitable that (at important times) none are. Someone should.

The Council of Financial Regulators should be more transparent and publish minutes of their deliberations. Under the current regulatory architecture, promoting competition requires a serious rethink about how the RBA, APRA and ASIC consider competition and whether the Australian Competition and Consumer Commission (ACCC) is well-placed to do more than it currently can for competition in the financial system.

Over the next few days we will try to assess the potential impact ahead, from higher loss rates, lower fee income and potential fines and penalties. Then of course, there is the question, will these additional costs be passed on to investors and shareholders, or simply recovered from the current customer based by higher fees.

We expect banks to start making provisions for the revenue hits ahead. ANZ, for example, said their RC legal bill will be around $15 million. CBA made a $200 million expense provision for expected costs relating to currently known regulatory, compliance and remediation program costs, including the Financial Services Royal Commission.

To start the journey lets look at the relative performance of the banks’ share prices over the past year. Westpac share price is 16.8% lower compared with a year ago.

ANZ is down 16% over the same period

CBA has fallen 15.9% in the past 12 months.

and NAB’s share price dropped 14.2% over the same period.

In comparison, the ASX 200 is up 0.25% over the past year.

Among the regional banks, Bendigo Bank has fallen 16.6%

Bank Of Queensland has fallen 11.7% over the past year.

In contrast Suncorp is 0.74% higher

and Macquarie Group was up 19.5%. They of course have more than half their business offshore now.

Next time, we try to size the revenue hits ahead, and think about what that may mean for the banks and their customers.

Mr Turnbull and his senior colleagues have spent the past two years arguing against a royal commission into the financial sector, although some of his backbenchers were campaigning vigorously for a royal commission.

ABC Insiders did a nice montage yesterday showing the evolution of the spin, from initially vehemently resisting a commission.

The PM finally called a royal commission late last year and shocking revelations have emerged as it has been taking evidence.

This was after an appalling interview with Kelly O’Dwyer who has been the Minister for Revenue and Financial Services, since July 2016.

Public hearings into the financial advice sector continued on Friday as BT Financial Advice general manager Michael Wright continued giving evidence.

Counsel assisting Rowena Orr grilled Mr Wright on the remuneration practices of Westpac/BT and whether its planners could be considered professionals when they are incentivised with sales targets.

Mr Wright said that while advisers are not viewed as ‘professionals’ by Australians in the same way that doctors are, the perception is changing for the better.

Furthermore, he said, the ‘balanced scorecard’ for Westpac advisers will be changed to include more non-financial factors.

“We’ll be setting peoples’ remuneration off their qualifications, based off their competency as an adviser, based off the standards that they go through with advisers,” he said.

“We will not set people’s remuneration – fixed or variable – based off how much money they write,” Mr Wright said.

However, Ms Orr pointed out that one-fifth of the ‘balanced scorecard’ for the company’s advisers will include financial measures.

“We debated this long and hard. The reality is we want to have a viable, sustainable, professional business. We’ve not a charity,” he said.

“We considered removing revenue from the scorecard and having 100 per cent non-financials,” Mr Wright said.

From 1 October 2018, Mr Wright said, BT will be ending grandfathered commissions for superannuation and investments – although risk commissions will remain (as per the Life Insurance Framework).

When it comes to the advice business he oversees, Mr Wright said he would be “delighted” if BT moved to a completely fee-for-service model.

However, with his “BT product provider hat on”, he said there is a first-mover disadvantage to being the first institution to end grandfathering completely.

The finance sector unmentionable hits the proverbial fan. Welcome to the Property Imperative Weekly to 21st April 2018.

We start this week’s review of the latest finance and property news with the latest from the Royal Commission into Financial Services Misconduct.

After the shameful disclosures relating to poor lending practices, bad advice, misaligned incentives and poor regulation last time; now they have been looking to the nether regions of financial planning and advice. And guess what, the same behaviours are evident again, in spades. Bearing in mind 48% of the $4.6 billion annual revenue from wealth management goes to the big four banks and AMP, they were forced to admit their mistakes in public. You can watch our separate video on the detailed findings “More Cultural Badness from The Finance Sector”. But here are a few highlights.

AMP apologised unreservedly for the misconduct and failures in regulatory disclosures in the advice business as revealed in the Royal Commission and Chief Executive Officer, Craig Meller will step down from his role with immediate effect.

The Australian Bankers Association admitted that the issues raised have been unacceptable and do not meet the high standards the community rightly expects of banks. And the Treasurer announced significant increases in penalties ASIC can impose. The government will increase penalties under the Corporations Act to: “For individuals: 10 years’ imprisonment; and/or the larger of $945,000 OR three times the benefits; For corporations: the larger of $9.45 million OR three times benefits OR 10% of annual turnover. “The Government will expand the range of contraventions subject to civil penalties, and also increase the maximum civil penalty amounts that can be imposed by courts, to the maximum of: the greater of $1.05 million (for individuals, from $200,000) and $10.5 million (for corporations, from $1 million); or three times the benefit gained or loss avoided; or 10% of the annual turnover (for corporations). “In addition, ASIC will be able to seek additional remedies to strip wrongdoers of profits illegally obtained, or losses avoided from contraventions resulting in civil penalty proceedings.”

These increases are right, as before the financial impact of poor behaviour was very low. However, do not be misled, changing penalties will not address the fundamental cultural, structural and economic issues which have combined to deliver a finance sector which is simply not fit for purpose.

We need to remove incentives from the advice sector (mortgage brokers included). Actually we need unified regulation across credit and wealth sectors (the current two regimes are an accident of history).

We need structural separate and disaggregation of our financial conglomerates. We need a realignment of interests to focus on the customer – which by the way is not at odds with shareholder returns, as customer focus builds franchise value and returns in the long term.

We need cultural reform and new values from our finance sector leaders. And Executive Pay should come under the spot light.

We need a reform of the regulatory structure in Australia, because they are captured at the moment at least by group think, and their interests are aligned too closely to the finance sector. This must include ASIC, APRA, RBA and ACCC. All have bits of the finance puzzle, but no one is seriously accountable.

But there is a more fundamental issue. We have relied on overblown credit, and superannuation sectors, as a proxy for high quality economic growth. This inflated housing and lifted household debt and GDP. We need a fundamental economic reset, because reforming financial services alone won’t solve our underlying issues.

The Government, who resisted the Royal Commission, has now also indicated they are receptive to expanding the scope and term of the inquiry, which in my view should include regulation of the sector, and the macroprudential settings in place. So write to the Commissioner, and your MP advocating a broader scope.

Finally, on this, it is worth noting that former deputy prime minister Barnaby Joyce went with a full-monty confession. “In the past I argued against a Royal Commission into banking. I was wrong. What I have heard … so far is beyond disturbing”, he tweeted. Joyce is now a backbencher, and free with his opinions. It’s another story with current ministers. They continue trying to score political points over Labor, which had been agitating for a royal commission long before it was set up.

My suggestion is this financial sector mess is so significant, that both sides of politics should set aside party differences and focus on the main game. Because what happens next will fundamentally determine the future economic success of the country, no less. If we continue with the current sets of assumptions we will run the country into the ground as the debt burden becomes unbearable, and savings for retirement are devalued and destroyed. It’s that serious.

Turning now to more immediate economic news, the latest lending stats from the ABS underscores that the “Great Credit Binge Is Ending”. You can watch our recent video where we discuss the results in full. To start at the end of the story, we see significant falls across most states in investment lending flows, with the most significant falls in the Sydney market. The share of investment flows continues to drift lower, to around 35%. But that is still substantial investment lending! Finally, the percentage of investment lending of all lending flows is below 20%, and shows a small fall. But we also see a fall in business lending to around 55%, excluding investment property lending.

The ABS also released their March 2018 unemployment statistics. It was not good with the trend unemployment rate increasing slightly to 5.6 per cent though the trend participation rate increased to a record high of 65.7 per cent. WA has the highest rate of unemployment at 6.4% and is still rising, whilst rates in NSW and ACT also rose.

The HIA released their latest Housing Affordability report, claiming that affordability improved in most of Australia’s capital cities during the first three months of 2018 as house price pressures eased. But this is largely spin, as their calculations do not necessarily take account of the now tighter, and becoming even tighter lending standards now in play. And in any case, in most centres, affordability is still well below the long term averages. But of course, they are advocates for the property sector, so there should be no surprise.

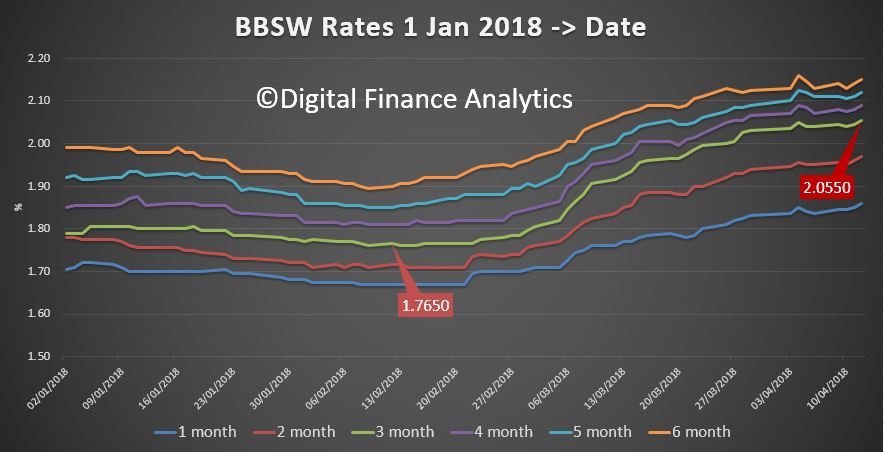

There was important evidence of the rising costs of funds this week as ME Bank says it has lifted its standard variable rate on existing owner-occupier principal and interest mortgages, effective April 2018. ME’s standard variable rate for existing owner-occupier principal-and-interest borrowers with an LVR of 80% or less, will increase by 6 basis points to 5.09% p.a. Variable rates for existing investor principal-and-interest borrowers will increase by 11 basis points, while rates for existing interest-only borrowers will increase by 16 basis points. ME CEO Mr Jamie McPhee said the changes are in response to increasing funding costs and increased compliance costs. More hikes will follow, across the industry together with reductions in rates paid on deposits as the fallout of the Royal Commission and higher international funding costs take their toll.

For example, the 10-year US Bond rate is moving higher again, following some slight fall earlier in April. Have no doubt, funding cost pressure will continue to rise. We discussed the whole question of debt and the potential trigger for a recession in a recent video blog, “Global Debt and the Upcoming Recession”. The outlook looks more and more like our Armageddon scenario, as we discussed in detail in an earlier programme “Four Scenarios (None Good)”. Worse, regulators in the USAand China are both weakening banking regulation, at this time of high risk, high debt.

Oh, and by the way, we think it quite possible the RBA will need to do its own form of quantitative easing down the track, and that they will most likely buy pools of residential mortgages (yes including those with breached lending standards) to assist the banks in their liquidity, to assist home prices to rise, and allowing the debt bomb to tick for longer. Sound of can being kicked firmly down the road! But that would be the time to buy Australian equities, and even property. Maybe we need a scenario 5!

We released the latest Digital Finance Analytics Household Finance Confidence Index for March 2018 shows a further slide in confidence compared with the previous month. The current score is 92.3, down from 94. 6 in February, and it has continued to drop since October 2016. The trend is firmly lower and below the neutral setting. You can watch our separate video on this “Why Household Finance Confidence Fell Again”. But in summary, across the states, confidence is continuing to fall in NSW and VIC, was little changes in SA and QLD, but rose in WA. There were there were falls in all age groups. Turning to the property-based segmentation, owner occupied householders remain the most confident, while property investors continue to become more concerned about the market. Those who are property inactive – renting, or living with parents or friends remain the least confident. Nevertheless, those who are property owners remain more confident relative to property inactive households. Based on the latest results, we see little on the horizon to suggest that household financial confidence will improve. We expect wages growth to remain contained, and home prices to slide, while costs of living pressures continue to grow. There will also be more pressure on mortgage interest rates as funding costs rise, and lower rates on deposits as banks trim these rates to protect their net margins.

Finally, we turn to CoreLogics’s auctions data. They suggest that fewer auctions will take place this week, with a total of 1,592 properties scheduled, compared with last week’s final result of1,915 auctions held. This is also lower than a year ago when 1,751 auctions were held across the capital city markets. Sydney is set to see the most significant drop in activity this week. Victoria’s Reservoir and Surfers Paradise in Queensland both top the busiest suburb list this week, each with 19 properties scheduled to go to auction. Following with 14 scheduled auctions each is Burwood and Point Cook both in Victoria.

Turning to last week’s final results the clearance rate was a 61.7 per cent success rate which was lower than the week prior when 62.8 per cent. Melbourne’s final auction clearance rate fell to 62.4 per cent last week across a slightly higher volume of auctions week-on-week with 873 held, up on the 723 over the week prior when a higher 68.2 per cent cleared. In Sydney, the final clearance rate fell to 61.5 per cent, down on the 62.9 per cent the previous week, with volumes across the city remaining steady over the week with a total of 795 held. Clearance rates improved across all of the remaining auction markets last week, with the exception Tasmania which remained unchanged. Geelong recorded the highest clearance rate of the non-capital city regions, with 77.1 per cent of 54 auctions clearing.

You might want to watch my video on “Auction Results Under The Microscope”, where we discuss how the results are collated and whether we can trust them.

So overall, there is little evidence to suggest the property market is recovering (despite more from the Industry claiming that this was the case, this week). And we have yet to see the impact of tighter lending standards flowing through. Our survey data indicates that more households are finding it tougher to meet the income and expenditure hurdles now, and as a result we expect credit and therefore home prices to continue to fall. And if anything, that fall will likely accelerate, unless we get unusual measures in the budget, which by the way we think are quite likely.

In a statement issued today, Treasurer Scott Morrison said the reform will represent the “most significant increases in maximum civil penalties in twenty years”.

These increases are right, as before the financial impact of poor behaviour was very low However, do not be misled, changing penalties will not address the fundamental cultural, structural and economic issues which have combined to deliver a finance sector which is simply not fit for purpose.

We need a removal of incentives from the advice sector (mortgage brokers included). Actually we need unified regulation across credit and wealth sectors (the current two regimes are an accident of history).

We need structural separate and disaggregation of our financial conglomerates. We need a realignment of interests to focus on the customer – which by the way is not at odds with shareholder returns, as customer focus builds franchise value and returns in the long term.

We need cultural reform and new values from our finance sector leaders. (Executive Pay should come under the spot light).

We need a reform of the regulatory structure in Australia, because they are captured at the moment at least by group think, and their interests are aligned too closely to the finance sector. This must include ASIC, APRA, RBA and ACCC. All have bits of the finance puzzle, but no one is seriously accountable.

But there is a more fundamental issue. We have relied on overblown credit, and superannuation sectors, as a proxy for high quality economic growth. This inflated housing and lifted household debt.

We need a fundamental economic reset, because reforming financial services alone won’t solve our underlying issues.

Here are the changes:

The government will increase penalties under the Corporations Act to:

“For individuals: (i) 10 years’ imprisonment; and/or (ii) the larger of $945,000 OR three times the benefits;

For corporations: (i) the larger of $9.45 million OR (ii) three times benefits OR 10% of annual turnover.

“The Government will expand the range of contraventions subject to civil penalties, and also increase the maximum civil penalty amounts that can be imposed by courts, to the maximum of:

the greater of $1.05 million (for individuals, from $200,000) and $10.5 million (for corporations, from $1 million); or

three times the benefit gained or loss avoided; or

10% of the annual turnover (for corporations).

“In addition, ASIC will be able to seek additional remedies to strip wrongdoers of profits illegally obtained, or losses avoided from contraventions resulting in civil penalty proceedings.”

The ABA says that the past few days of hearings at the Royal Commission have been sobering for the entire industry.

The issues raised have been unacceptable and do not meet the high standards the community rightly expects of banks.

Australia’s banks are committed to tackling misconduct head-on and strongly back the reforms proposed today by the Turnbull Government to penalise bad conduct within the industry.

A stronger range of penalties for misconduct is vital to tackling criminal and unacceptable behaviour by individuals and corporations.

The industry has supported the strengthening of the penalties regime for misconduct since the Federal Government announced its review 18 months ago, as an outcome of the Financial Services Inquiry.

Before today’s announcement, banks had already recognised the need for change and have put in place a rigorous conduct background check for bank employees to stop those with a history of misconduct simply moving from one institution to another.

Many of the issues raised over the last few days are the subject of investigation with changes already underway in the sector to ensure cases such as these cannot reoccur. The industry expects that further changes should and will be made following the final recommendations of the Commission.

AMP says the company apologises unreservedly for the misconduct and failures in regulatory disclosures in the advice business as revealed in the Royal Commission.

The AMP Limited Board today announces the following actions to accelerate the necessary change within the organisation:

The Board and the Chief Executive Officer, Craig Meller, have agreed that he will step down from his role with immediate effect.

Mike Wilkins, a Non-Executive Director on the AMP Limited Board since September 2016 and a former CEO of IAG Limited, has been appointed as acting Chief Executive Officer until the search for the new CEO is completed.

An immediate, comprehensive review of AMP’s regulatory reporting and governance processes will be undertaken. This work will be overseen by a retired judge or equivalent independent expert who will be appointed imminently.

A Board Committee has been established to review the issues related to the advice business raised in the Royal Commission. The Committee is chaired by Mike Wilkins and will act with the assistance of external counsel, King & Wood Mallesons.

The Group General Counsel, Brian Salter, has agreed to take leave while the review is undertaken. David Cullen, AMP General Counsel, Governance has been appointed as acting Group General Counsel.

AMP will be making a submission to the Royal Commission to respond to the issues raised. The submission will, among other matters, address the issue of the independence of the Clayton Utz report.

The Board will withdraw resolution four from its Notice of Meeting to the 2018 Annual General Meeting, which relates to an equity grant for the Chief Executive Officer.

The actions announced today build upon the existing program of work, instigated in 2017. The work underway includes:

Customer remediation, with the program well progressed and 15,712 customers identified and $4.7 million fees refunded to date.

An external review to ensure all fee for no service business practices have ceased. This review is now complete and has confirmed that the practices ceased in November 2016.

An independent investigation into employee conduct. Based on the review’s findings, the Board will determine the employment and remuneration implications for any relevant individuals around the fee for no service matter.

A review and complete overhaul of governance, systems and processes in the advice business.

An enterprise-wide cultural audit conducted by an external consultant.

An enterprise-wide review of risk governance, controls and culture also conducted by an external consultant.

AMP Chairman Catherine Brenner said: “AMP apologises unreservedly for the misconduct and failures in regulatory disclosures in our advice business. The Board is determined that we will meet these challenges head on, accelerating changes in both culture and performance at AMP.

“We have been driving much-needed change and improvement in our advice business, which has undergone significant leadership and governance renewal over the past year but we know we have much more to do to.”

Craig Meller said: “I am honoured to have been the CEO of AMP. I am personally devastated by the issues which have been raised publicly this week, particularly by the impact they have had on our customers, employees, planners and shareholders. This is not the AMP I know and these are not the actions our customers should expect from the company.

“I do not condone them or the misleading statements made to ASIC. However, as they occurred during my tenure as CEO, I believe that stepping down as CEO is an appropriate measure to begin the work that needs to be done to restore public and regulatory trust in AMP.”

Mike Wilkins – biography

Mike Wilkins was appointed to the AMP Limited Board and as a member of its Audit and Risk Committees in September 2016. In May 2017, he became Chairman of the Risk Committee. He was also appointed to the AMP Life Limited and The National Mutual Life Association of Australasia Limited Boards in October 2016.

Mike has more than 30 years’ experience in financial services in Australia and Asia in sectors such as life insurance and investment management. Mike has more than 20 years’ experience as CEO for ASX100 companies. Most recently, he served as Managing Director and CEO of Insurance Australia Group (IAG). He is the former Managing Director and CEO of Promina Group Limited and Tyndall Australia Limited.

Mike is a Fellow of Chartered Accountants Australia and New Zealand and is also a Fellow of the Australian Institute of Company Directors. Mike was made an Officer of the Order of Australia in 2017 for distinguished service to the insurance industry.

If you are a politician, what do you do when your bad judgement – or worse – has been dramatically called out for all to see?

That’s the question which has faced the government as appalling behaviour by the Commonwealth Bank, AMP and Westpac has been revealed this week at the royal commission into misconduct in the banking, superannuation and financial services industry.

Former deputy prime minister Barnaby Joyce went the full-monty confession. “In the past I argued against a Royal Commission into banking. I was wrong. What I have heard … so far is beyond disturbing”, he tweeted.

Joyce is now a backbencher, and free with his opinions. It’s another story with current ministers. They continue trying to score political points over Labor, which had been agitating for a royal commission long before it was set up.

The ministers claim the government laid down terms of reference that took the inquiry beyond what Labor was proposing. But although Labor never released terms of reference, it flagged in April 2016 a broad inquiry into “misconduct in the banking and financial services industry”.

The real difference between the government and the opposition was the emphasis on superannuation. While Labor’s inquiry would have covered it, the government wrote in a specific term of reference, hoping evidence about industry funds might embarrass the unions and therefore the ALP. The commission has yet to reach those funds.

Revenue Minister Kelly O’Dwyer, pressed about her refusal to admit the government had erred in opposing a commission, told the ABC on Thursday, “Initially, the government said that it didn’t feel that there was enough need for a royal commission. And we re-evaluated our position and we introduced one”.

Well, that’s the short version. In fact, the government was forced to drop its resistance when Nationals rebels threatened to revolt. Take a bow, Queensland Nationals backbenchers Barry O’Sullivan, George Christensen and Llew O’Brien. You did everyone a service.

Indeed, the Nationals were on the case of the banks very early. Nationals senator John “Wacka” Williams for years pursued the rorts, through Senate committee investigations.

The government’s resistance to the royal commission was bad enough but remember its earlier record on consumer protections in the financial services area.

When the Coalition came to power it was determined to weaken measures Labor had introduced. Eventually, it was thwarted by the Senate crossbench, with the upper house disallowing its changes.

Just why the government was so keen to shield an industry where wrongdoing had been obvious is not entirely clear. It appears to have been a mix of free market ideology, a let-the-buyer-beware philosophy, and some close ministerial ties with the banking sector.

In light of what is coming out, the government should be ashamed of its past performance.

This week, the commission heard about AMP, which provides a wide range of financial products and advice, charging for services it didn’t deliver, and deliberately misleading the regulator, the Australian Securities and Investments Commission (ASIC), about its behaviour.

It also heard how the Commonwealth Bank’s financial planning business charged customers it knew had died, including in one case for more than a decade. Linda Elkins, from CBA’s wealth management arm Colonial First State, agreed with the proposition put to her that the CBA would “be the gold medallist if ASIC was handing out medals for fee for no service.”

A nurse told of the financial disaster after she and her husband, aspiring to set up a B&B, received advice from a Westpac financial planner, including to sell the family home.

Seasoned journalist Janine Perrett, who now works for Sky, tweeted, “I thought nothing could shock me anymore, but in my forty years as a journo, most of it covering business, I have never seen anything as appalling as what we are witnessing at the banking RC. And I covered the 80’s crooks including Bond and Skase.”

The commission’s interim report is due September 30 and its final report by February 1, not long before the expected time of the election. There is speculation over whether the reporting date will be extended. Bill Shorten says the inquiry should be given longer if needed; Finance Minister Mathias Cormann has indicated the government would do what Commissioner Kenneth Hayne wanted.

Those in the government who think the original timetable should be adequate note that, unlike for example the royal commission into institutional responses to child sexual abuse, this inquiry is not undertaking deep dives into everything, but exposing the general problems.

From the opposition’s point of view, it would be desirable for the inquiry to run on. That would keep the banks a live debate, and leave it for Labor, if elected, to deal with the commission’s outcome. Shorten is already paving the way for a compensation scheme financed by the industry. Given the poisonous unpopularity of the banks, the Coalition could hardly run a scare about what a Shorten government might do.

Ideally, the government needs the issue squared away before the election.

The government insists it has already put in train a good deal to clean up the industry including a one-stop-shop for complaints, higher standards for financial advisers, beefing up ASIC, and a tougher penalty regime.

Morrison on Friday will announce the detail of stronger new penalties for corporate and financial misconduct, including ASIC being able to ban people from the financial services sector.

One argument the government made against a royal commission was that it would just delay action. But of course if it had been held much earlier, by now we might have in place a full suite of reforms.

Most immediately, the shocking stories from the commission are adding to the government’s problems in trying to sell its company tax cuts for big business to key crossbench senators and to the public.

Author: Michelle Grattan, Professorial Fellow, University of Canberra