Another week of hearings of the Financial Services Royal Commission has seen financial services company AMP admitting it mislead the Australian Securities and Investment Commission (ASIC) on 20 occasions. The commission also saw evidence of both AMP and the Commonwealth Bank of Australia paying themselves client money when there was no adviser allocated to provide services, or the client had passed away.

It seems ASIC and the Director of Public Prosecutions will have no lack of evidence to pursue civil penalties and criminal cases. The bigger issue is what charges to go with.

In deciding what to pursue, ASIC and the DPP will need to weigh up the costs, the charges individuals are willing to plead guilty to, and the outcomes that will best serve the public interest.

Convicting individuals clearly “sends a message”, but these employees are easily replaced with others just as willing to commit the offences, unless the organisation’s culture is changed.

Whether or not bankers get jail time will depend on the actual offences charged and a range of sentencing factors. However, the courts are increasingly emphasising the importance of substantial sentences for white collar crime.

Offences with similar maximum penalties in the UK led to a UBS banker who manipulated the London Interbank Offered Rate being sentenced to 14 years jail in 2015. Another joined him in 2016 for two years and nine months and three others were also convicted.

What AMP and CBA did

AMP and CBA have admitted they failed to provide information and report breaches to ASIC as required by the Corporations Act. Misleading Australian government agencies is also a criminal offence under the Act and the Commonwealth Criminal Code.

As well as dealing truthfully with ASIC, all entities licensed to offer financial services must act “efficiently, honestly and fairly” and take reasonable steps to ensure their employees do likewise.

It is not hard to see how taking clients’ money without providing a service is not efficient, honest or fair.

Civil penalties

Civil sanctions could apply to conduct at AMP and CBA which could ultimately involve disqualification for up to 20 years from working as a corporate officer and/or a fine of up to A$200,000.

Officers of a corporation are very senior employees and usually immediately below board level. They have a duty to be careful and diligent and act in the best interests of the company under the Corporations Act. There is a range of lesser charges from general dishonesty to false documentation offences.

Officers of a corporation have duties which require them to be careful and diligent. This is because the officers may have failed to follow up or failed to prevent conduct) after finding out about what was going on.

If ASIC and the DPP can go further and prove that AMP and CBA officers have intentionally caused their company to break the law, it is virtually impossible that conduct could be in the interests of the corporation. AMP and CBA officers may have also breached criminal offences in the Corporations Act if the wrongdoing was reckless or intentionally dishonest.

Criminal charges

Turning to more general offences, here criminal penalties range from 12 months in jail for misleading ASIC, to significant penalties for conspiracy to defraud.

Any bank employee who was involved in the creation of misleading documentation might well be exposed to fraud charges. Under Commonwealth and state law, fraud can involve reckless deception of another (either ASIC or the clients) with an intention to gain a financial advantage for another (AMP or CBA) Those offences have maximum penalties of 10 years jail. There is a range of lesser charges from general dishonesty to false documentation offences.

Those who assisted might well also be liable through accessorial liability.

Prosecutors could also turn to the conspiracy to defraud offence. The Commonwealth version of the offence involves an agreement to dishonestly influence a public official’s decisions. An agreement to provide false documents to ASIC would seem easily to fit this offence. Again, this has a maximum penalty of 10 years.

Similarly, common law conspiracy to defraud charges could be available for dishonestly misleading customers in a way that caused them financial loss. There are no prescribed maximum penalties for this version of the offence.

Multiple offences could mean sentences served concurrently, or partly cumulatively.

Although the wrongdoing may seem clear to the public, it is likely that complex matters of proof will emerge and ASIC will need to make a range of decisions about the best approach to ensuring cultural change occurs. While convictions might be deserved, the public interest is best served by ensuring that prosecutions are part of wider regulatory action leading to better banking practices.

Authors: Dimity Kingsford Smith, Professor and Director, Centre for Law Markets and Regulation, UNSW Law, UNSW; Alex Steel, Professor, UNSW Scientia Education Fellow, UNSW

The Reserve Bank hosted a roundtable discussion on small business finance today, along with the Australian Banking Association and the Council of Small Business Australia. The roundtable was chaired by Philip Lowe, Governor of the Reserve Bank.

Small businesses are very important for the economy. They generate significant employment growth, drive innovation and boost competition in markets. Access to external finance is an important issue for many small businesses, particularly when they are looking to expand.

Our own SME survey highlights the problems SME’s face in getting finance in the face of the banks focus on mortgage lending. The latest edition of our report reveals that more than half of small business owners are not getting the financial assistance they require from lenders in Australia to grow their businesses.

The aim of the roundtable was to provide a forum for the discussion of small business lending in Australia. The participants included entrepreneurs from the Reserve Bank’s Small Business Finance Advisory Panel along with representatives from financial institutions, government and the financial regulators.

The challenges faced by small businesses when borrowing were discussed. The entrepreneurs highlighted a number of issues, including:

access to lending for start-ups

the heavy reliance on secured lending and the role of housing collateral and personal guarantees in lending

the loan application process, including the administrative burden

the ability to compare products across lenders and to switch lenders.

The participants discussed a range of ideas for addressing these challenges. Financial institutions shared their perspectives and discussed some of the steps that are being taken to address concerns of small business. The roundtable heard some suggestions about how to improve the accessibility of information for small businesses about their financing options. The roundtable also heard from the Australian Prudential Regulation Authority regarding the proposed revisions to the bank capital framework that relate to small business lending.

The roundtable discussed some other policy initiatives that are currently underway, including the introduction of comprehensive credit reporting and open banking. Participants agreed that these initiatives could help to improve access to finance, and the Reserve Bank will continue to monitor developments closely.

Background

The Small Business Finance Advisory Panel was established by the Reserve Bank in 1993 and meets annually to discuss issues relating to the provision of finance, as well as the broader economic environment for small businesses. The panel provides valuable information to the Reserve Bank on the financial and economic conditions faced by small businesses in Australia.

The Reserve Bank has previously hosted discussions on small business finance issues, including a Small Business Finance Roundtable in 2012 and a Conference on Small Business Conditions and Finance in 2015.

The Australian Banking Association, along with the Australian Council of Small business, representatives for member Banks and other stakeholders were also in attendance to bring their own perspective on the issues and to answer questions. The event was agreed to and organised at the end of last year.

Australian Banking Association CEO Anna Bligh said that the Roundtable was an important opportunity for Australia’s banks to listen first hand to the needs of small business.

“Small business is the engine room of the Australian economy, accounting for more than 40% of all jobs or around 4.7 million people,” Ms Bligh said.

“This Roundtable was an important step in building the relationship between banks, small businesses and their representatives.

“Banks are working hard to better understand the needs of business, their challenges and how they can work with them to help them achieve their goals,” she said.

Today we take a look at the latest from the Royal Commission into Financial Service Misconduct, which recommenced its hearings yesterday again, with a focus on the Financial Planning Sector.

Financial Advisers provide advice on a range of areas of consumer finance, investing, superannuation, retirement planning, estate planning, risk management, insurance and taxation.

ASIC says between 20 and 40% of the Australian adult population use or have used a Financial Planner. That means that around 2.3 million Australians over 18 received advice. A number of issues have surfaced in recent years, including charging fees for no service, or advice not provided in full, the provision of inappropriate financial advice, as well as improper conduct by financial advisors and the misappropriation of customer’s funds.

There has been massive growth in the number of financial advisers, to more than 25,000 up 41% from 2009. 5,822 Financial Advice licences were issued in Australia to firms able to offer advice. What you may not know is that the top five players in Financial Advice in Australia are the big four banks and AMP, who together have nearly 48% of the $4.6 billion dollars in annual revenue. 30% of advisers work for one of the major banks and 44% work for the top 10 organisations by revenue, so it is very concentrated. Then there is a long tail of smaller organisations with 78% operating a firm with less than 10 advisors. The average advice licence covers 34 individuals operating under it.

There have been a number of significant scandals relating to the provision of financial advice in recent years.

Townsville based Storm Financial encourage investors to borrow against their home to invest in indexed share funds, in a “one size fits all model” of advice. Storm collapsed in 2009 will losses of more than $3 billion dollars. Around 3,000 of its 14,000 clients had suffered significant losses. Many of the investors were retired or about to retire, and with limited assets and income. Some lost their family homes or had to postpone their retirement. The founders were found to have caused or permitted inappropriate advice to be given and had breech their duty of care under the corporations’ act. Specifically, the one size fits all model of advice failed to take into account individual circumstances which led to devastating consequences for the individual investors. They had focused too much on the profitability of the business as opposed to the best interests of individual investors. ASIC worked with a number of major players for customers who had made investments through Storm. CBA undertook to make $136 million dollars in compensation to many CBA customers who borrowed from the bank to invest through Storm and who had suffered financial losses. This is in addition to $132 million CBA paid under the Storm resolution scheme. ASIC looked at settlements distributed by Macquarie Bank to Storm investors leading to a revised agreement where the bank agreed to pay $82.5 million by way of compensation and costs. Bank of Queensland agreed to pay $17 million as compensation for Storm related losses.

The second scandal involved Commonwealth Financial Planning Limited. A whistle-blower revealed allegations of misconduct within CFL to ASIC in 2010. It was suggested that some advisers were encouraging investors to invest in high risk, but profit generating products which were not appropriate. Some were even switching products without the client’s permission. This also included forging client signatures. When the GFC hit in 2008, thousands of CFL clients, many of whom were nearing or in retirement, lost significant amounts as a result of this misconduct. More than $22 million was paid to clients in compensation for receiving inappropriate financial advice from two financial planning advisers. Later it became evident the misconduct was more widespread so CBA implemented a second programme of compensation relating to advice from advisers. Their Open Advice programme had conducted more than 8,600 assessments, of which more than 2,500 required compensations to a total of $37.6 million has been offered.

So turning to the hearings. First up was Peter Kell from ASIC who described the “Fee for no service” problem.

The Future of Financial Advice reforms (FOFA) has tightened the rules, but the fees can be significant. And as we will see, some players simply took the fees to bolster their profits.

Next up was AMP, and we heard over the next day or so of more than 20 occasions when AMP failed in their duty to notify ASIC of a number of potential breaches.

Despite the fact AMP was aware of a range of issues they simply allowed the practices to continue. There was an absence of monitoring activities, what AMP said it was going to do to ASIC, e.g. training for staff in new procedures was different from what they actually did. The issues had been occurring since 2009, and AMP acknowledge that on at least 20 occasions they made false and misleading statements to ASIC about potential breeches.

Worse, the Royal Commission revealed today that AMP’s law firm, Clayton Utz, removed outgoing chief executive Craig Meller’s name from a draft of a critical report about the business.

So once again we see the cultural norms in financial services driving poor behaviour, which may bolster profits but at the expense of their customers, and an apparent willingness to avoid the issues with the regulators. This is shameful, but not surprising.

So we see mismanagement again, and failure of regulation.

We suspect we will see more of the same in the day ahead. Frankly I am not surprised because the cultural norms we see displayed here are precisely the same as were observed in the previous lending related hearings. The quantum of change required within our financial services organisations is profound and I also believe the scope of the Royal Commission should be expanded to include the role and function of our regulators.

Multiple failures are clearly costing households dear. But then the companies seem willing to cop the settlements, and move on, without root cause analysis and fixing the problem. This is not acceptable behaviour in my book and is well below community expectations.

The ABA says today’s release of the final report of independent governance expert, Mr Ian McPhee AO PSM, shows that Australia’s banks have made significant progress on the Better Banking Reform Program, including finalising many of its measures.

The program, which began in April 2016, outlined a range of changes and initiatives to achieve three outcomes – better products, better service and better culture. Banks have been implementing these reforms over the last two years, with Mr McPhee independently monitoring their program as part of the industry’s commitment to accountability and transparency.

A major part of this reform has revolved around changes to the way banks pay their staff, as outlined in the Sedgwick Review completed in 2017. These changes include removing direct sales incentives, abolishing mortgage broker commissions directly linked to loan size and introducing balanced scorecards in each bank. The review set a deadline for these changes to be completed by 2020 however banks are already well underway in implementing these reforms.

Australian Banking Association CEO Anna Bligh thanked Mr McPhee for his expert oversight over the last two years providing independent governance advice and monitoring for the ambitious industry reform program.

“Ian McPhee and Price Waterhouse Coopers have done a rigorous job over the last two years in their independent monitoring of the implementation of the Better Banking Reform Program,” Ms Bligh said.

“The industry has set a cracking pace on some of the toughest reforms in over a decade, as detailed in Mr McPhee’s final report, however there is still further work to be done to bed these down.

“Banks have made a large investment in reform to better meet community expectations, such as changing the way bank staff are paid and improving customer protections under the new Banking Code.

“Banks are on track to meet the 2020 deadline set by the Sedgwick Review to reform the way they pay their staff including abolishing direct sales incentives and scrapping mortgage broker commissions directly linked to loan size.

“While this is the final report by Ian McPhee the industry has taken his advice and will be putting in place further arrangements for public reporting.

“Banks will be making further regular public reports on the success of the program and their ongoing implementation of the Sedgwick recommendations and the new Banking Code,” she said.

Key initiatives already implemented include:

Customer advocates within banks to ensure complaints are resolved quickly and fairly

Improving protections and awareness of processes for whistleblowers, including best practice industry guidelines

Stamping out poor conduct in the industry by ensuring staff with records of poor behaviour do not simply move around the industry.

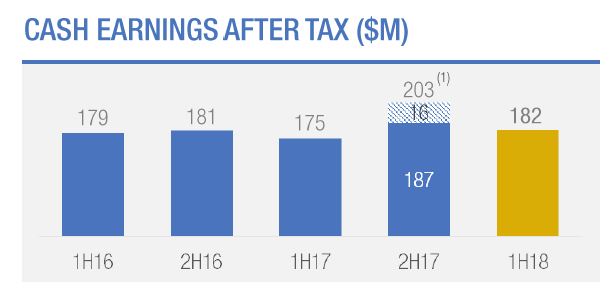

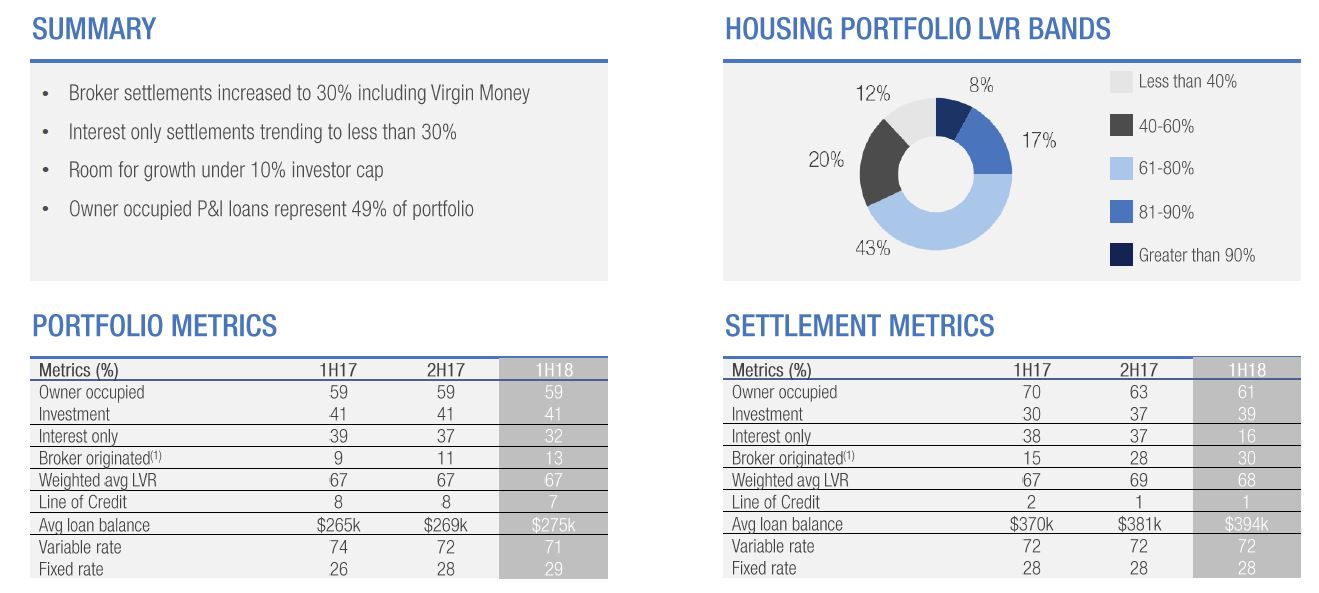

Bank of Queensland (BOQ) has announced cash earnings after tax of $182 million for 1H18, up 4 per cent on 1H17. This is weaker than expected. They continue to bat on a sticky wicket. Being a regional bank is a tough gig! The BOQ Board has maintained a fully franked interim dividend of 38 cents per ordinary share.

Statutory net profit after tax increased by 8 per cent to $174 million.

Net Interest Margin was up 1 basis point on the prior half to 1.97%, helped by loan book growth and deposit repricing, but under pressure thanks to intense new mortgage loan discounting. Growth in overall NIM was lower than expected. Ahead we think the higher BSBW rates will impact NIM adversely alongside discounted attractor rates..

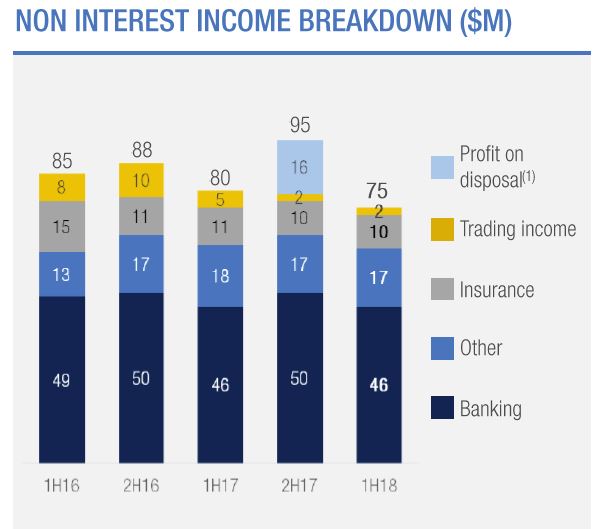

In addition, lower than expected non-interest income hit the result, thanks to an ATM fee impact of $0.6m, banking fees under pressure and a fall in trading income opportunities.

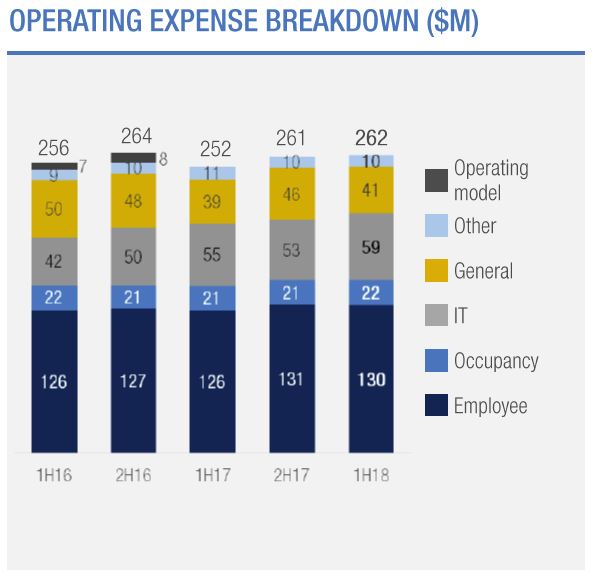

Also higher than expected costs impacted the result. Their Cost to Income ratio was up 20 bps to 47.6%

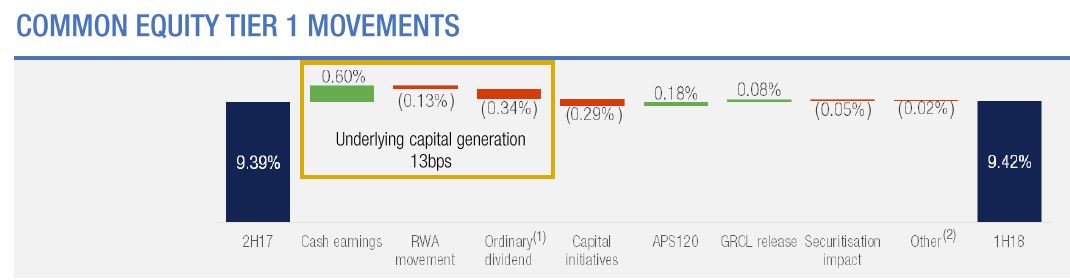

BOQ also today announced the sale of St Andrew’s Insurance to Freedom Insurance Group. More detail on this transaction is provided in a separate announcement. The CET1 uplift was estimated at 20 basis points after completion, with completion expected in second half of the year.

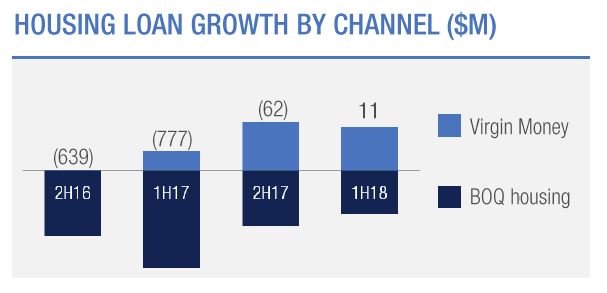

The Banks says there has been a notable improvement in lending growth, continuing the positive business momentum that returned in the previous half. This was supported by the commercial niche segments, as well as home loan growth through the Virgin Money, BOQ Specialist and BOQ Broker channels. Total lending growth of $671 million in 1H18 represents an uplift of more than $800 million compared to the contraction of $157 million in 1H17.

This has been delivered through 3 per cent annualised housing loan growth (+$382 million) at 0.5x system, together with strong commercial loan growth of 6 per cent annualised (+$292 million), which was 1.6x system.

They show that broker settlements increased to 30%, including via Virgin Money, whilst the proportion of investment loans rose to 39%, compared with 30% a year ago. Interest only loans were 16% of flows, compared with 38% a year ago, and represents 32% of their portfolio. The average loan balance has risen to $394k and the weighted average LVR on new loans was 68%.

“We moved to adopt enhanced servicing, validation and responsible lending practices much earlier than many of our peers” the bank said.

“Although this has hampered our growth in prior periods, we think it was the most prudent approach to take for the long term,” he said.

Impaired assets as a percentage of gross loans were down to 39 basis points, while loan impairment expense was just 10 basis points of gross loans during the half.

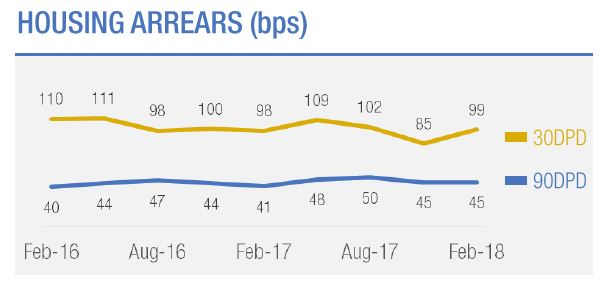

Arrears levels remained benign across all portfolios and there were signs of improvement in the Queensland and Western Australian economies. But they noted an uptick in the most recent quarter in housing …

… and consumer credit.

They also showed potential construction exposure to apartments – at $90m, at 16 developments across 3 states completing 2018 to 2019. They observed this was a well diversified cross-state portfolio. But $53m is in Victoria.

They also have $100m exposure to the mining sector.

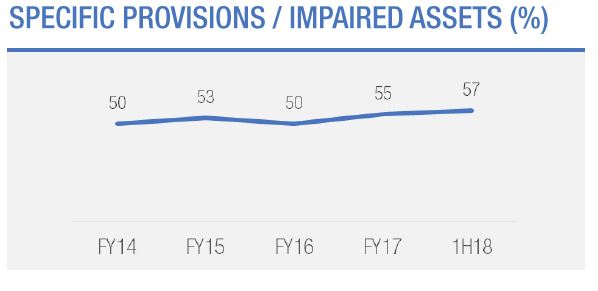

Loan impairment rose, but remained at 10 basis points of GLA. Impaired assets fell a further 10% from 2H17 and new impaired asset volumes also reduced to the lowest level since pre-2012.

Specific provisions were increased to 57%.

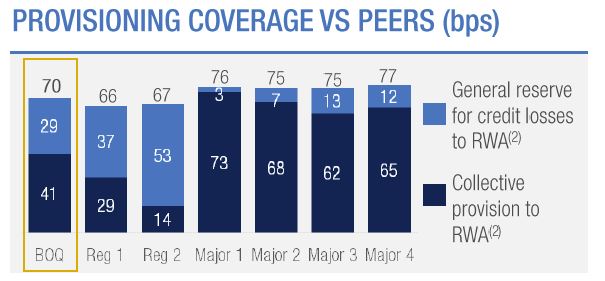

They say total provisions remain strong and provisional coverage compares favorably with peers.

BOQ’s capital position has been maintained. The CET1 ratio was up 3 basis points over the half to 9.42 per cent.

The bank said that the recent Basel and APRA papers suggest BOQ’s current CET1 ratio positions it well for the changes that are coming.

Ahead, they said that the industry was facing a number of headwinds, but BOQ remains well placed.

“The industry faces challenges of low credit growth, low interest rates, regulatory uncertainty, increasing consumer expectations and increased scrutiny of conduct and culture.

“In this environment, our long term strategy remains the right one; we are building out our business bank in higher growth sectors of the economy and opening up new retail channels.

“We also remain focused on our customers, investing in a number of initiatives across the group that will improve our digital offering, bring us closer to our customers and enable us to provide them with a differentiated service offering.

“Our very strong capital position provides us with flexibility to consider options that will deliver the best value to our shareholders,”

The FBAA has called for “perspective” on broker remuneration amid “unprecedented, unnecessary and crazy” opinions by some ill-informed commentators on the industry.

FBAA executive director Peter White has criticised the number of probes by authorities – including the Productivity Commission, ACCC and Royal Commission – as they `”are falling over each other on their quest for profile.” He also said ASIC itself has only recently conducted a comprehensive review

“I have never seen such craziness around our sector, and this is leading to reactionary comments rather than considered approaches,” he said in a statement.

White pointed out the industry has already been undergoing a process of reform directly with regulators for the past few years to achieve better consumer outcomes.

White believes “there really is no problem” – It’s just that “these multiple inquiries and statutory bodies have to justify their existence and fat pay packets by kicking someone, and at the moment it’s finance brokers.”

“Let’s keep in mind that consumers are not complaining; we know they are happy with the current system because they are voting with their feet and overwhelmingly choosing brokers,” White added.

White suggests that brokers avoid reacting to quotes coming from bank bosses because their words can easily be edited and used out of context.

He recognizes that banks have raised some eyebrows, but he also points out that their Royal Commission submissions, except for one bank, show support for the existing system. And that doesn’t surprise him because he believes “it’s better for banks, brokers, and borrowers.”

White hopes to hear less speculative reporting, and more rational and informed discussion moving forward.

Welcome to the Property Imperative Weekly to 14 April 2018. We review the latest property and finance news.

There is a massive amount to cover in this week’s review of property and finance news, so we will dive straight in.

CoreLogic says that final auction results for last week showed that 1,839 residential homes were taken to auction with a 62.8 per cent final auction clearance rate, down from 64.8 per cent over the previous week. Auction volumes rose across Melbourne with 723 auctions held and 68.2 per cent selling. There were a total of 795 Sydney auctions last week, but the higher volumes saw the final clearance rate weaken with 62.9 per cent of auctions successful, down on the 67.9 per cent the week prior. All of the remaining auction markets saw a rise in activity last week; clearance rates however returned varied results week-on-week, with Adelaide Brisbane and Perth showing an improvement across the higher volumes while Canberra and Tasmania both recorded lower clearance rates. Across the non-capital city regions, the highest clearance rate was recorded across the Hunter region, with 72.5 per cent of the 45 auctions successful.

This week, CoreLogic is currently tracking 1,690 capital city auctions and as usual, Melbourne and Sydney are the two busiest capital city auction markets, with 795 and 678 homes scheduled to go to auction. Auction activity is expected to be lower week-on week across each of the smaller auction markets

Two points to make. First is a slowing market, more homes will be sold privately, rather than via auctions, and this is clearly happening now, and second, we discussed in detail the vagaries of the auction clearance reporting in our separate blog, so check that out if you want to understand more about how reliable these figures are.

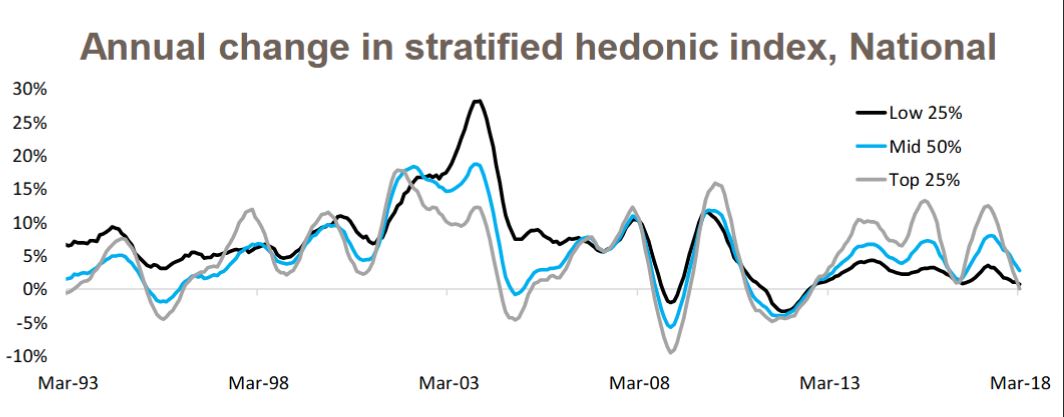

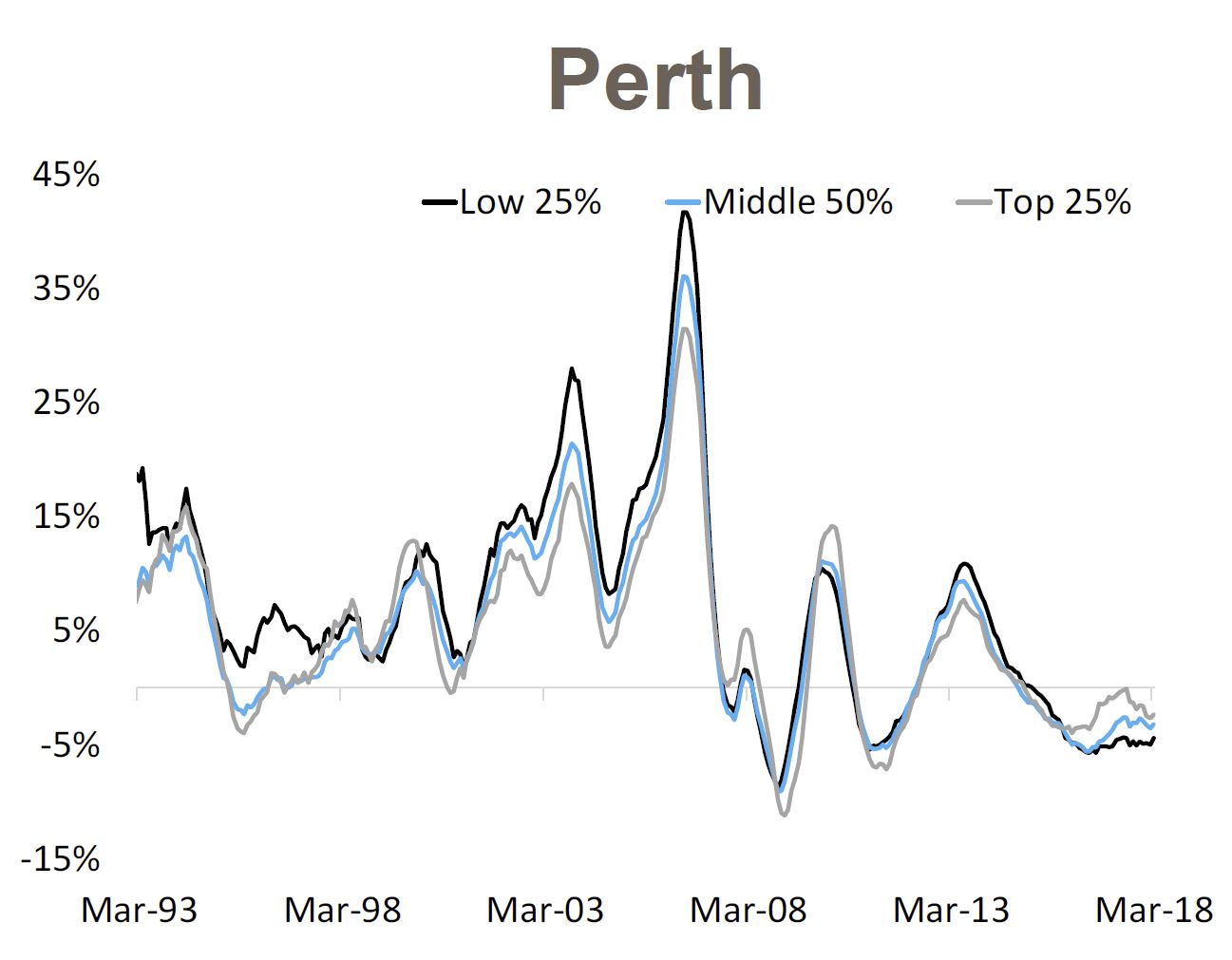

Home prices slipped a little this past week according to the CoreLogic index, but their analysis also confirmed what we are seeing, namely that more expensive properties are falling the most. In fact, values in the most expensive 25% of the property market are falling the fastest, whereas values for the most affordable 25% have actually risen in value.

Their analysis shows that over the March 2018 quarter, national data shows that dwelling values were down by 0.5%, however digging below the surface reveals the modest fall in values was confined to the most expensive quarter of the market. The most affordable properties increased in value by +0.7% compared to a +0.3% increase across the middle market and a -1.1% decline across the most expensive properties.

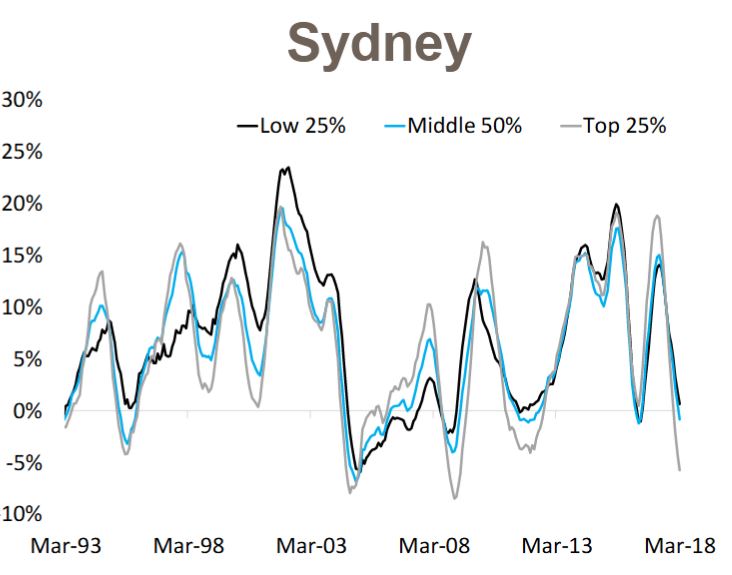

But looking at the details by location, in Sydney, over the past 12 months, the most expensive properties have recorded the largest value falls (-5.7%) followed by the middle market (-0.9%) and the most affordable market managed some moderate growth (+0.6%).

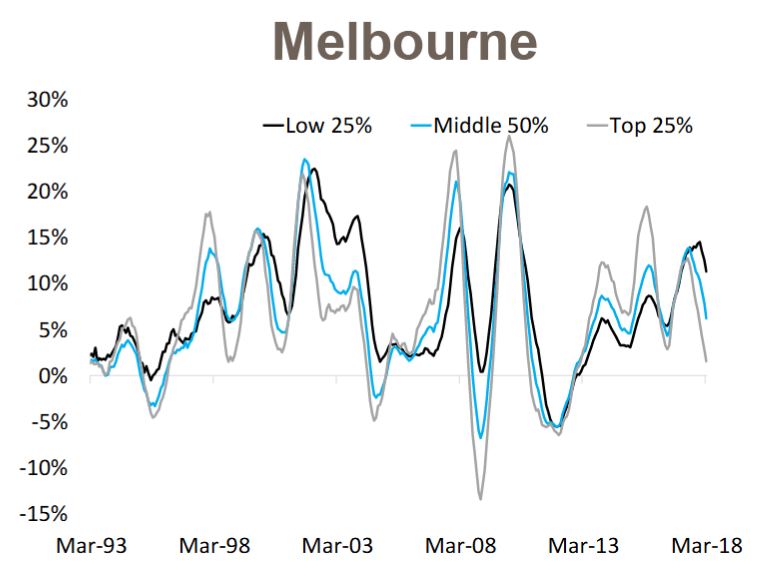

Compare that with Melbourne where values have increased over the past year across each segment of the market, with the most moderate increases recorded across the most expensive segment (+1.6%), then the middle 50% (+6.2%) while the most affordable suburbs have recorded double-digit growth (+11.3%)

Finally, in Perth values have fallen over the past year across each market sector with the largest declines across the most affordable properties (-4.4%) followed by the middle market (-3.2%) with the most expensive properties recording the most moderate value falls (-2.4%).

This shows the importance of granular information, and how misleading overall averages can be.

The RBA has released their Financial Stability Review today. It is worth reading the 70 odd pages as it gives a comprehensive picture of the current state of play, though through the Central Bank’s rose-tinted spectacles! They do talk about the risks of high household debt, and warn of the impact of rising interest rates ahead. They home in on the say $480 billion interest only mortgage loans due for reset over the over the next four years, which is around 30 per cent of outstanding loans. Resets to principal and interest will lift repayments by at least 30%. Some borrowers will be forced to sell.

This scenario mirrors the roll over of adjustable rate home loans in the United States which triggered the 2008 sub-prime mortgage crisis. Perhaps this is our own version! We have previously estimated more than $100 billion in these loans would now fail current tighter underwriting standards.

I published a more comprehensive review of the Financial Stability Review, and you can watch the video on this report. Importantly the RBA suggests that banks broke the rules in their lending on interest only loans before changes were made to regulation in 2014. The RBA says that there is the potential that these will result in banks having to set aside provisions and/or face penalties for past misconduct or perhaps (more notably) being constrained in the operation of parts of their businesses.

We also did a video on the RBA Chart pack which was released recently. Household consumption is still higher than disposable income, and the gap is being filled by the falling savings ratio. So, we are still spending, but raiding our savings to do so. Which of course is not sustainable. Now the other route to fund consumption is debt, so there should be no surprise to see that total household debt rose again (note this is adjusted thanks to changes in the ABS data relating to superannuation, we have previously breached the 200% mark). But on the same chart we see home prices are now falling – already the biggest fall since the GFC in 2007.

We see all the signs of issues ahead, with household debt still rising, household consumption relying on debt and savings, and overall growth still over reliant on the poor old household sector. We need a proper plan B, where investment is channelled into productive growth investments, not just more housing loans. Yet regulators and government appear to rely on this sector to make the numbers work – but it is, in my view, lipstick on a pig!

Another important report came out from The Bank for International Settlements, the “Central Bankers Banker” has just released an interesting, and concerning report with the catchy title of “Financial spillovers, spillbacks, and the scope for international macroprudential policy coordination“. But in its 53 pages of “dry banker speak” there are some important facts which shows just how much of the global financial system is now interconnected. They start by making the point that over the past three decades, and despite a slowdown coinciding with the global financial crisis (GFC) of 2007–09, the degree of international financial integration has increased relentlessly. In fact the rapid pace of financial globalisation over the past decades has also been reflected in an over sixfold increase in the external assets and liabilities of nations as a share of GDP – despite a marked slowdown in the growth of cross-border positions in the immediate aftermath of the GFC. My own take is that we have been sleepwalking into a scenario where large capital flows and international financial players operating cross borders, negating the effectiveness of local macroeconomic measures, to their own ends. This new world is one where large global players end up with more power to influence outcomes than governments. No wonder that they often march in step, in terms of seeking outcomes which benefit the financial system machine. You can watch our separate video discussion on this report. Somewhere along the road, we have lost the plot, but unless radical changes are made, the Genie cannot be put back into the bottle. This should concern us all.

And there was further evidence of the global connections in a piece from From The St. Louis Fed On The Economy Blog which discussed the decoupling of home ownership from home price rises. They say recent evidence indicates that the cost of buying a home has increased relative to renting in several of the world’s largest economies, but the share of people owning homes has decreased. This pattern is occurring even in countries with diverging interest rate policies. And the causes need to be identified. We think the answer is simple: the financialisation of property and the availability of credit at low rates explains the phenomenon.

And finally on the global economy, Vice-President of the Deutsche Bundesbank Prof. Claudia Buch spoke on “Have the main advanced economies become more resilient to real and financial shocks? and makes three telling points. First, favourable economic prospects may lead to an underestimation of risks to financial stability. Second resilience should be assessed against the ability of the financial system to deal with unexpected events. Third there is the risk of a roll back of reforms. The warning is clear, we are not prepared for the unexpected, and as we have been showing, the risks are rising.

Locally more bad bank behaviour surfaced this week. ASIC says it accepted an enforceable undertaking from Commonwealth Financial Planning Limited and BW Financial Advice Limited, both wholly owned subsidiaries of the Commonwealth Bank of Australia (CBA). ASIC found that CFPL and BWFA failed to provide, or failed to locate evidence regarding the provision of, annual reviews to approximately 31,500 ‘Ongoing Service’ customers in the period from July 2007 to June 2015 (for CFPL) and from November 2010 to June 2015 (for BWFA). They will pay a community benefit payment of $3 million in total. Cheap at half the price!

In similar vein, ASIC says it has accepted an enforceable undertaking from Australia and New Zealand Banking Group Limited (ANZ) after an investigation found that ANZ had failed to provide documented annual reviews to more than 10,000 ‘Prime Access’ customers in the period from 2006 to 2013. Again, they will pay a community benefit payment of $3 million in total.

Both these cases were where the banks took fees for services they did not deliver – and this once again highlight the cultural issues within the banks, were profit overrides good customer outcomes. We suspect we will hear more about poor cultural norms this coming week as the Royal Commission hearing recommence with a focus on financial planning and wealth management.

Finally to home lending. The ABS released their February 2018 housing finance data. Where possible we track the trend data series, as it irons out some of the bumps along the way. The bottom line is investor as still active but at a slower rate. Some are suggesting there is evidence of stabilisation, but we do not see that in our surveys. Owner occupied loans, especially refinancing is growing quite fast – as lenders seek out lower risk refinance customers with attractive rates. First time buyers remain active, but comprise a small proportion of new loans as the effect of first owner grants pass, and lending standards tighten. You can watch our video on this.

But the final nail in the coffin was the announcement from Westpac of significantly tighten lending standards, with a forensic focus on household expenditure. They have updated their credit policies so borrower expenses will need to be captured at an “itemised and granular level” across 13 different categories and include expenses that will continue after settlement as well as debts with other institutions. They will also be insisting on documentary proof. Moreover, households will be required to certify their income and expenses is true. This cuts to the heart of the liar loans issue, as laid bare in the Royal Commission. That said, Despite the commission raising questions over whether the use of benchmarks is appropriate when assessing the suitability of a loan for a customer, the Westpac Group changes will still apply either the higher of the customer-declared expenses or the Household Expenditure Measure (HEM) for serviceability purposes. You can watch our separate video on this. Almost certainly other banks will follow and tighten their verification processes. This will put more downward pressure on lending multiples, and will lead to a drop in credit, with a follow on to put downward pressure on home prices.

We discussed this in an article which was published under my by-line in the Australian this week, where we argued that excess credit has caused the home price bubble, and as credit is reversed, home prices will fall.

Our central case is for a fall on average of 15-20% by the end of 2019, assuming no major international incidents. The outlook remains firmly on the downside in our view.

ASIC says it has has accepted an enforceable undertaking (EU) from Commonwealth Financial Planning Limited (CFPL) and BW Financial Advice Limited (BWFA), both wholly owned subsidiaries of the Commonwealth Bank of Australia (CBA).

ASIC found that CFPL and BWFA failed to provide, or failed to locate evidence regarding the provision of, annual reviews to approximately 31,500 ‘Ongoing Service’ customers in the period from July 2007 to June 2015 (for CFPL) and from November 2010 to June 2015 (for BWFA).

The EU requires, among other things:

CFPL and BWFA to pay a community benefit payment of $3 million in total;

CFPL to provide an attestation from senior management setting out the material changes that have been made to CFPL’s compliance systems and processes in response to the misconduct; and

CFPL to provide further attestations from senior management, supported by an expert report, that:

CFPL’s compliance systems and processes are now reasonably adequate to track CFPL’s contractual obligations to its Ongoing Service clients; and

CFPL has taken reasonable steps to identify and remediate its Ongoing Service customers to whom CFPL did not provide annual reviews in the period from July 2015 to January 2018.

As BWFA ceased trading in October 2016, CFPL is the focus of the compliance improvements required under the EU.

ASIC Deputy Chair Peter Kell said, ‘Our report into Fees For No Service in October 2016 identified the major financial institutions’ systemic failures in this area, and called for fair compensation to be paid to customers who did not receive the advice reviews that they were promised and paid for.

‘This enforceable undertaking follows on from the earlier enforceable undertaking accepted by ASIC in relation to ANZ’s fees for no service conduct. These failures show that all too often the financial institutions prioritised revenue and fee generation over the delivery of advice and services paid for by their customers.’

In addition to the EU, CFPL and BWFA have also agreed to compensate approximately 31,500 affected customers in the period from July 2007 to June 2015 (for CFPL) and from November 2010 to June 2015 (for BWFA). The compensation program is nearing completion and as at 28 February 2018, CFPL and BWFA have paid or offered to pay approximately $88 million (plus interest) to these customers (with the total compensation estimated at $88.6 million (plus interest)).

Background

The EU follows an ASIC investigation into CFPL and BWFA in relation to their fees for no service conduct concerning various Ongoing Service packages which were offered to CFPL and BWFA financial planning customers for an annual fee. A key component of those packages from about 2004 (for CFPL) and from 2010 (for BWFA) was the provision of an annual review of the customer’s financial plan.

As a result of the investigation, ASIC was concerned that:

CFPL and BWFA either did not provide, or have not identified evidence regarding the provision of, annual reviews to approximately 31,500 Ongoing Service customers who had paid for those reviews;

CFPL and BWFA did not have adequate systems and processes in place for tracking their Ongoing Service customers and ensuring that annual reviews were provided to them;

senior management were aware from at least mid-2012 that a relatively small number of CFPL Ongoing Service customers who were not assigned to an active adviser may not have received an annual review, and that there was a potential risk of a broader ‘fees for no service’ issue in relation to other Ongoing Service customers, but CFPL did not notify ASIC of the issue until July 2014; and

CFPL and BWFA failed to comply with section 912A(1)(a) of the Corporations Act which provides that a financial services licensee must do all things necessary to ensure that the financial services covered by the licence are provided efficiently, honestly and fairly, and a condition of their respective Australian financial services licence.

Both CFPL and BWFA have acknowledged in the EU that ASIC’s concerns were reasonably held.

The EU has been accepted by ASIC as part of ASIC’s Wealth Management Project to address systemic failures by financial institutions and advisers, over a number of years, to provide ongoing advice services to customers who paid fees to receive those services (commonly referred to by ASIC as Fees for No Service conduct). A report on ASIC’s work in this area was released in October 2016 (Report 499), and updated in May 2017 (17-145MR) and December 2017 (17-438MR).

Westpac has tightened its expense analysis for mortgages. Sound of door firmly shutting after the horse has bolted! I wonder is this might impact the current ASIC case on mortgage underwriting with Westpac? The bank will still apply either the higher of the customer-declared expenses or the Household Expenditure Measure (HEM) for serviceability purposes.

The Westpac Group has updated its credit policies so borrower expenses will need to be captured at an “itemised and granular level” across 13 different categories and include expenses that will continue after settlement as well as debts with other institutions.

The changes, which apply to all loans submitted to any bank within the Westpac Group from Tuesday (17 April), aim to “provide a more accurate view” of borrower expenses so that the bank can “better determine their financial situation and repayment ability”.

The move comes just weeks after the Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry questioned whether credit providers have adequate policies in place to ensure that they comply with “their obligations under the National Credit Act when offering broker-originated home loans to customers, insofar as those policies require them to make reasonable inquiries about the consumer’s requirements and objectives in relation to the credit 25 contract, to make reasonable inquiries about the consumer’s financial situation, and to take reasonable steps to verify the consumer’s financial situation”.

Despite the commission raising questions over whether the use of benchmarks is appropriate when assessing the suitability of a loan for a customer, the Westpac Group changes will still apply either the higher of the customer-declared expenses or the Household Expenditure Measure (HEM) for serviceability purposes.

Expense types

Brokers are being advised that they will no longer be able to bundle living expenses.

Instead, for all loans submitted from Tuesday, 17 April, brokers will need to capture all applicable expenses over 13 categories during the needs assessment conversation.

“Absolute Basic Expenses” will be replaced with seven mandatory expense types. These are:

Clothing and personal care

Groceries

Medical and health

Transport

Insurance

Telephone, internet, pay TV and media streaming subscriptions

Recreation and entertainment

There will also be an additional optional expense type, too. These are:

Owner-occupied property utilities, rates and related costs

Childcare

Education

Investment property utilities, rates and related costs

Other

Notional rent

An additional category of rented property utilities and related costs will be applied if the customer’s post-settlement housing situation is either “rent”, “board” or “living with parents”.

Where an applicant has this type of post-settlement housing situation, if the monthly rental amount is stated to be less than $650 per month, a “notional” rent amount of $650 per month will be applied automatically to each applicant on the loan, regardless of marital status.

For other categories, the Westpac Group has outlined that a broker will still be able to enter $0 for an expense type, but for certain mandatory expenses, when $0 is entered into an expense type, the broker will need to select a reason to explain why the expense does not apply to the applicant.

Evidence

It will also be mandatory for the customer to provide evidence for other financial liabilities, including ongoing rent/board, child support and any secured or unsecured debts held with other financial institutions.

These can include documents such as bank statements, signed and dated rental agreements, letters from property managers, transaction listings, court order or child support agency letters.

For debts with other financial institutions, the documents cannot be more than six weeks apart from allocation date.

This documentation must be included in the loan application submission. Assessors will then verify the documents submitted.

The existing requirements for HELP, HECS and TSL debt will still apply.

Declaration

The customer must also now sign a “financial acknowledgment” as part of the loan offer documents indicating that all details relating to expenses and debts are true.

The bank said: “Westpac is committed to responsible lending and ensuring that we have a clear understanding of our customers’ financial situations.

“We are proud to work closely with our broker partners to continue to meet our responsible lending obligations and do the right thing by our customers. That’s why we are updating the Westpac credit policies to enhance the way we capture living expenses, commitments, and verify documentation.”

It added: “It’s all about looking after the customer by fully capturing their financial commitments to ensure they can adequality manage the mortgage liability they are potentially signing up for.”

How the changes will impact lodgements

ApplyOnline (AOL) and aggregator systems are currently being updated to cater for these changes.

The bank has outlined that any applications submitted before 17 April will be assessed as pipeline deals.

Applications saved or drafted in ApplyOnline before this date (or for applications resubmitted after this date) will need to be updated with the new expense type.

The banking group warned that any changes outside of the acceptable amendments under pipeline will require a reassessment and the previous approval may no longer be valid.

Brokers are being asked to check Westpac Broker Net or speak to their BDM if they have any further questions.

Crackdown on expenses

The move by Westpac marks the first wholesale change made by the major banks to tighten up their expenses collection process following the royal commission.

The commission was damning in its critique of the lenders’ policies when it came to ensuring customers can afford their home loans, with ANZ being called out for their “lack of processes in relation to the verification of a customer’s expenses”, and both Westpac and NAB revealing that there had been instances of their staff accepting falsified documentation for loans.

For example, it was revealed that there had been “at least 55 instances of Westpac staff either falsifying or accepting falsified supporting documentation in connection with home and personal loan applications, [and] a number of instances of Westpac staff receiving payments from referrers for the referral of customers to Westpac for loans”; while some NAB staff members were allegedly “charging NAB customers a fee for personal loans… made as cash payments under the table”.

It is expected that several other banks will follow in the footsteps of Westpac and make similar changes to their expense verification process in the coming weeks.