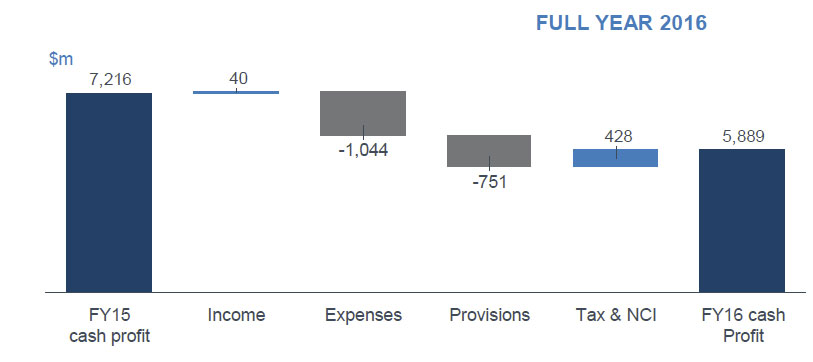

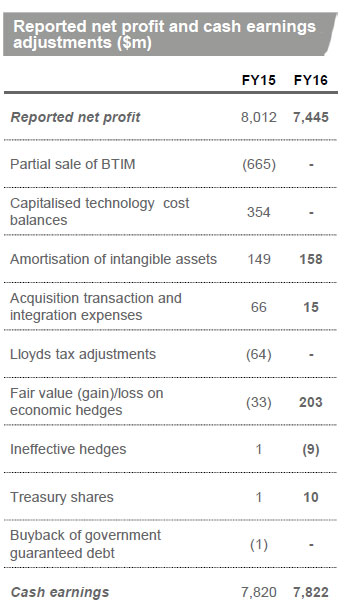

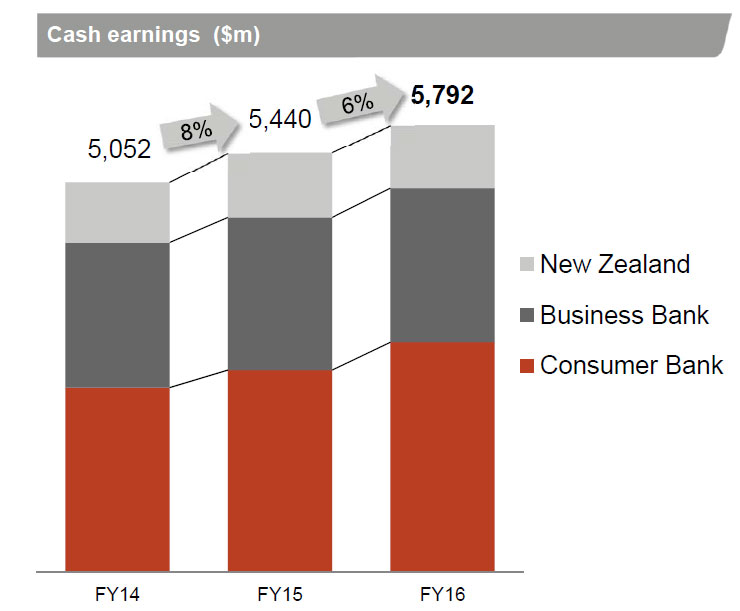

Westpac Group today announced a Full Year 2016 statutory net profit of $7,445 million, down 7% compared to the prior corresponding period. However, cash earnings were $7,822 million, in line with the prior year, and above expectations, thanks mainly to a lower than anticipated impairment charge. The balance sheet remains strong, with NSFR above 100%. The Australian retail banking operations have been the pillar of the business, whilst wealth, institutional and insurance is under pressure. Mortgage lending is the pillar within the pillar!

It is worth saying that cash earnings is not a measure of cash flow or net profit determined on a cash accounting basis, as it includes non-cash items reflected in net profit determined in accordance with Australian Accounting Standards. So the specific adjustments include both cash and non-cash items. Cash earnings is reported net profit adjusted for material items to ensure they appropriately reflect profits available to ordinary shareholders. All adjustments shown are after tax.

Here is a quick summary of the results.

Here is a quick summary of the results.

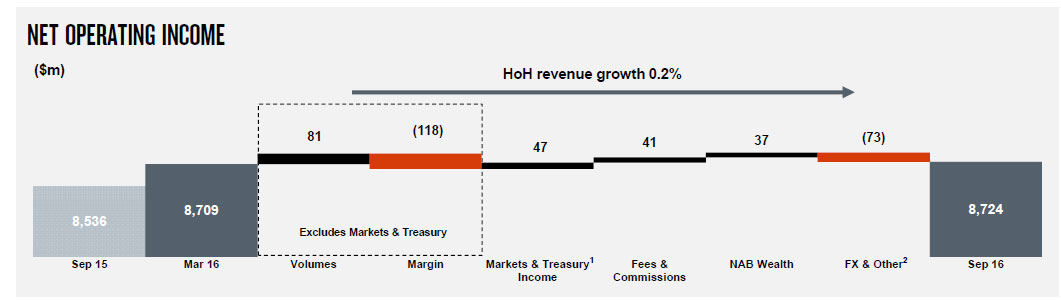

Total revenue was up 3%, with good growth in net interest income to $15,348 million, up 8%. The expense to income ratio at 42%, down 7 basis points.

Total revenue was up 3%, with good growth in net interest income to $15,348 million, up 8%. The expense to income ratio at 42%, down 7 basis points.

Total lending rose 6%, with growth in Australian mortgages of 8% and Australian business lending rising 3%, with a skew to SME lending. New Zealand lending increased 9% in NZ$.

Loan growth was fully funded by customer deposits which increased by $39 billion, or 9%, with the deposit to loan ratio improving 2 percentage points to 70.5%.

Loan growth was fully funded by customer deposits which increased by $39 billion, or 9%, with the deposit to loan ratio improving 2 percentage points to 70.5%.

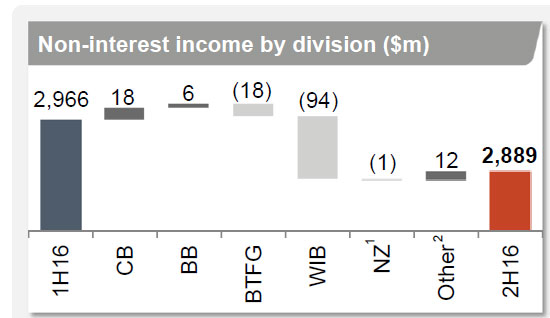

Non-interest income of $5,855 million was down 7%. This reflects a range of infrequent and volatile items including lower revenue from BTIM following the partial sell down in the second half of 2015. Excluding infrequent and volatile items, most of the decline was due to lower markets activity — impacting fees in WIB — and lower cards-related income in the Consumer Bank;

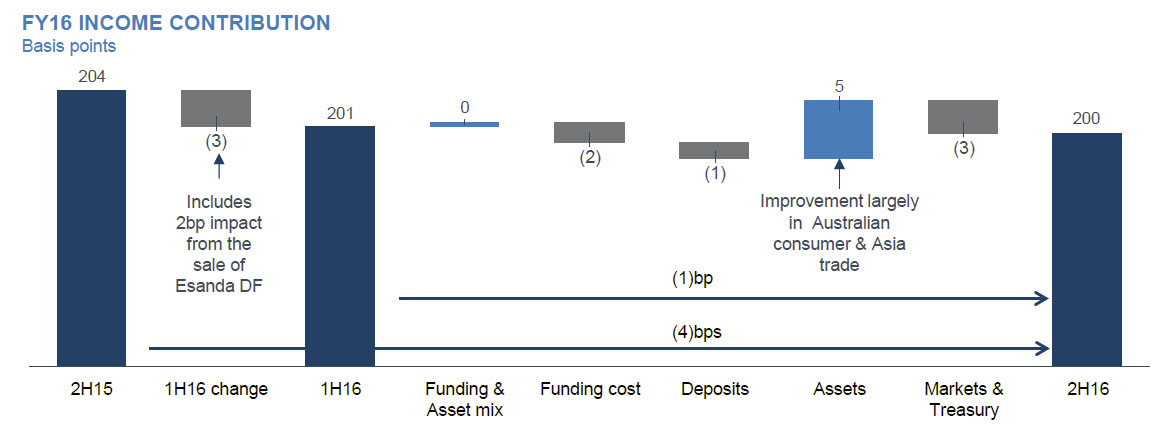

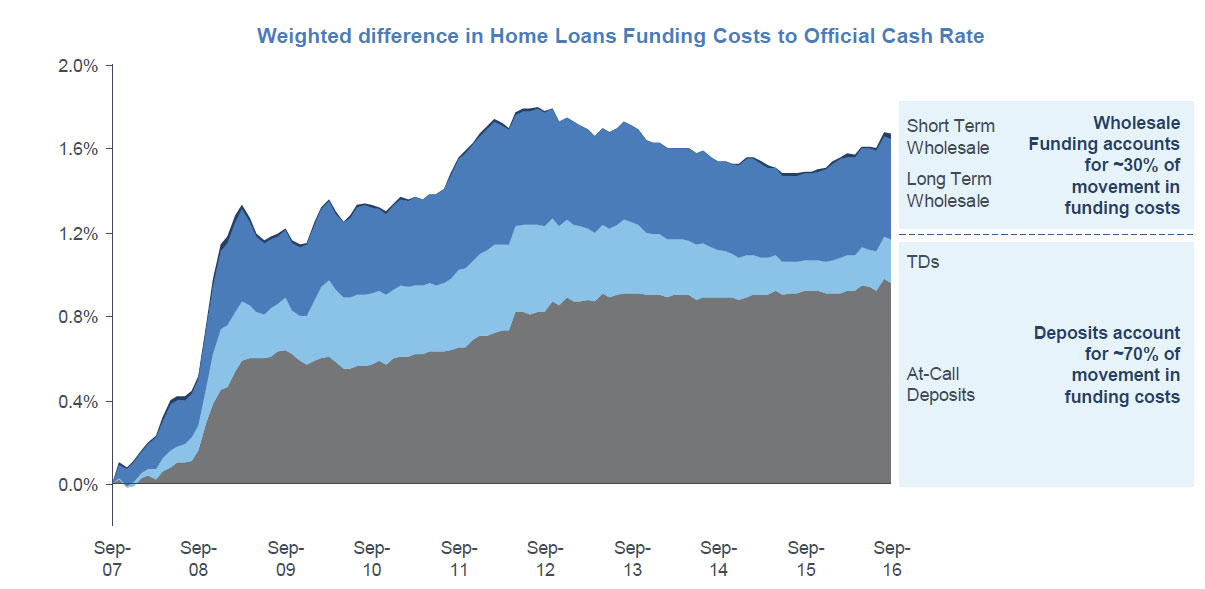

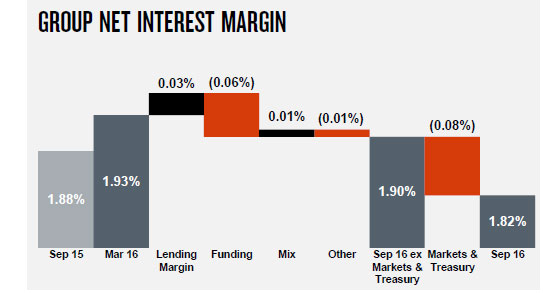

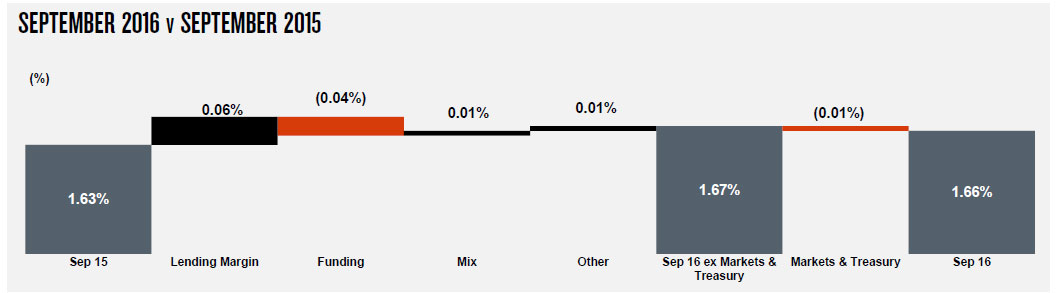

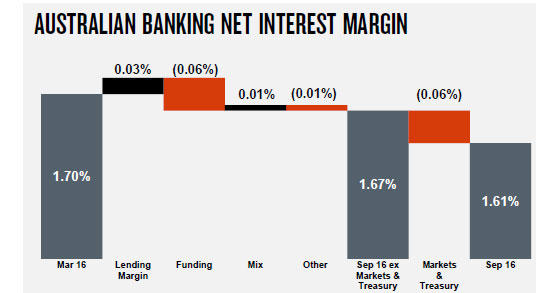

The net interest margin was up 5 basis points to 2.13%. Excluding Treasury and Markets, net interest margin was up 3 basis points. During the second half the 3 basis point fall in the margin reflects the impact of higher funding costs and lower interest rates.

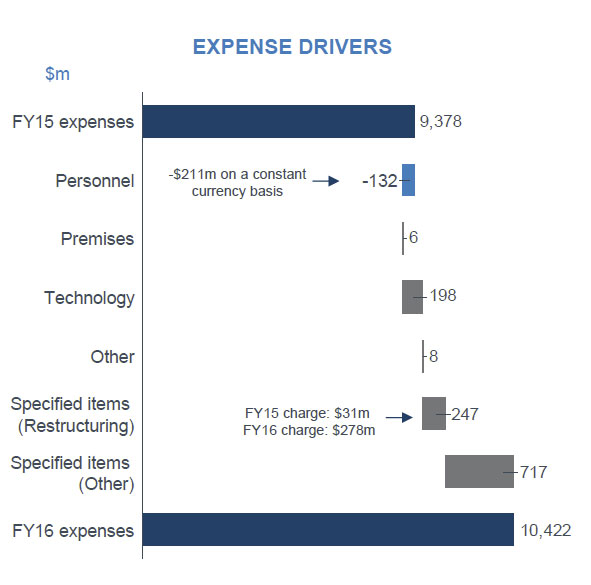

The expense to income ratio was 42%, with expenses up 3% in line with revenue growth. Regulatory and compliance costs added 1% to expense growth for the year.

The expense to income ratio was 42%, with expenses up 3% in line with revenue growth. Regulatory and compliance costs added 1% to expense growth for the year.

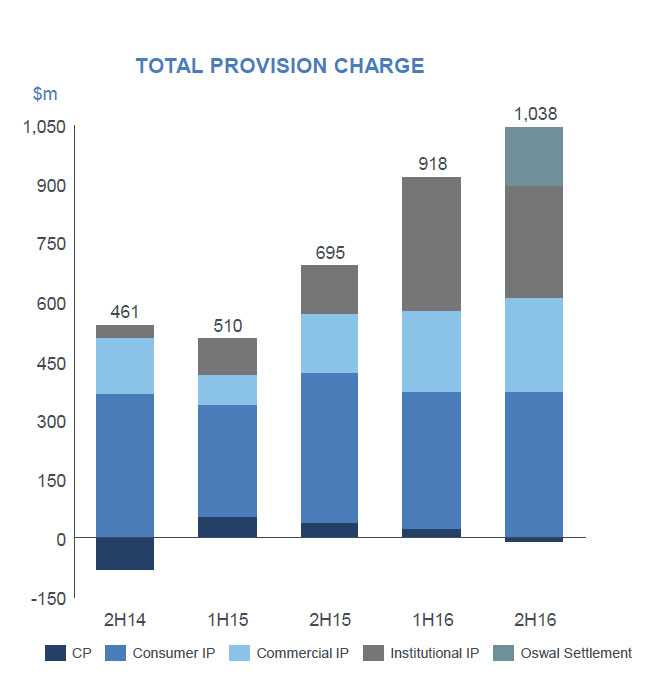

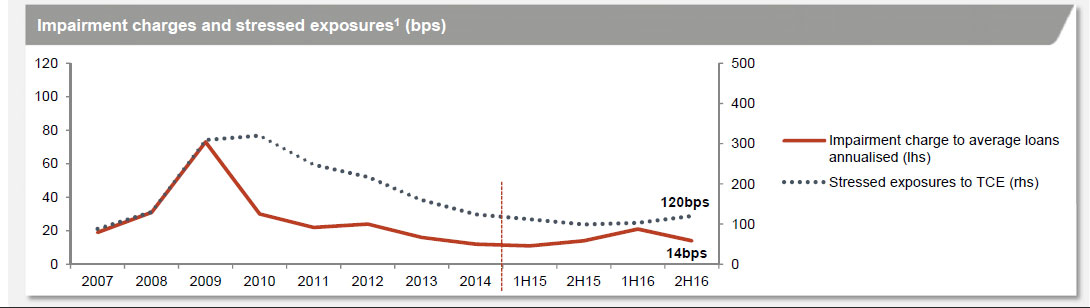

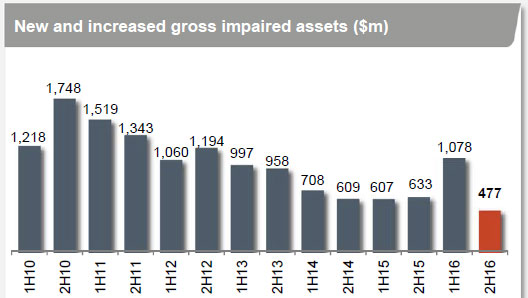

The 49% rise in impairments compared to the prior corresponding period mostly reflects a small number of institutional exposures that were downgraded in the first half 2016.

However, the second half impairment charge of $457 million was 31% lower compared to the first half 2016. We wonder whether the divergence between stressed and impaired loans is sustainable.

However, the second half impairment charge of $457 million was 31% lower compared to the first half 2016. We wonder whether the divergence between stressed and impaired loans is sustainable.

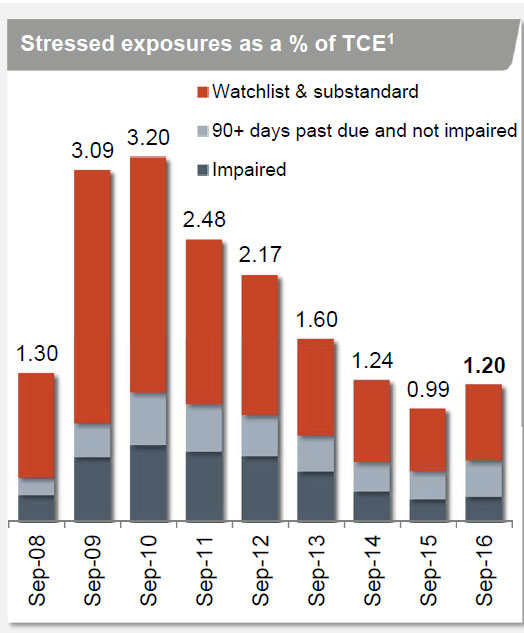

Whilst credit quality remains sound, the level of stressed assets rose modestly over the year by 21 basis points to 1.20% at 30 September 2016. Second Half 2016 saw an increase in stressed exposures, reflecting continuing low prices for NZ dairy products and the ongoing impact of the slowdown in mining investment on some regions.

Whilst credit quality remains sound, the level of stressed assets rose modestly over the year by 21 basis points to 1.20% at 30 September 2016. Second Half 2016 saw an increase in stressed exposures, reflecting continuing low prices for NZ dairy products and the ongoing impact of the slowdown in mining investment on some regions.

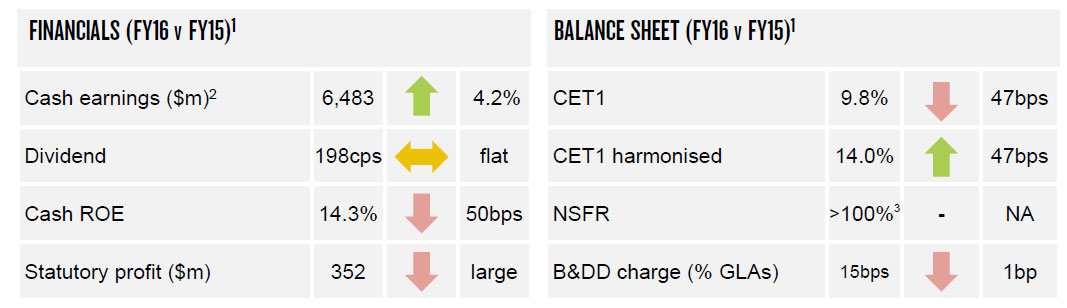

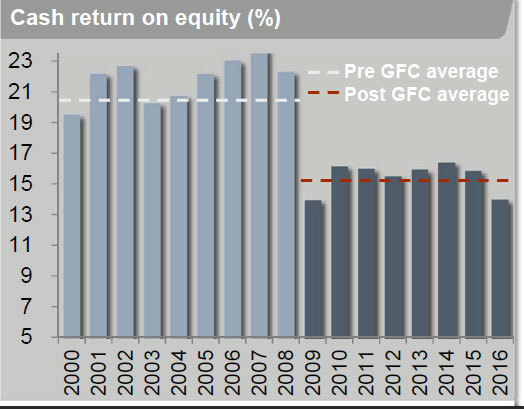

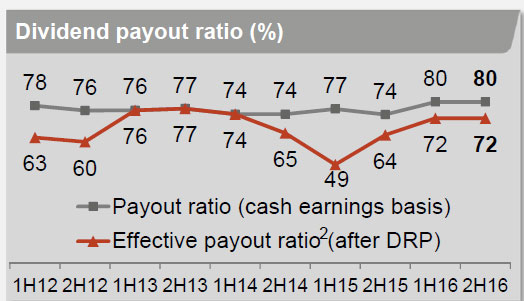

The cash return on equity (ROE) of 14.0%, down 185 basis points whilst the final, fully franked dividend of 94 cents per share (cps), taking total dividends paid for the year to 188 cps, was unchanged.

The cash return on equity (ROE) of 14.0%, down 185 basis points whilst the final, fully franked dividend of 94 cents per share (cps), taking total dividends paid for the year to 188 cps, was unchanged.

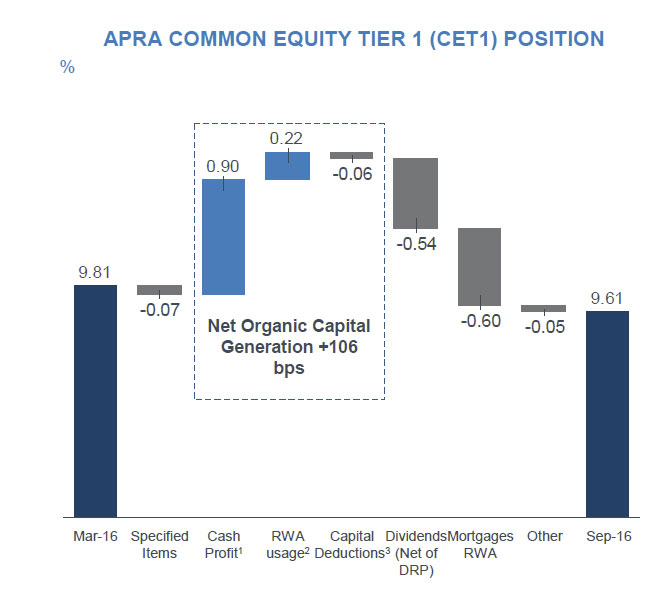

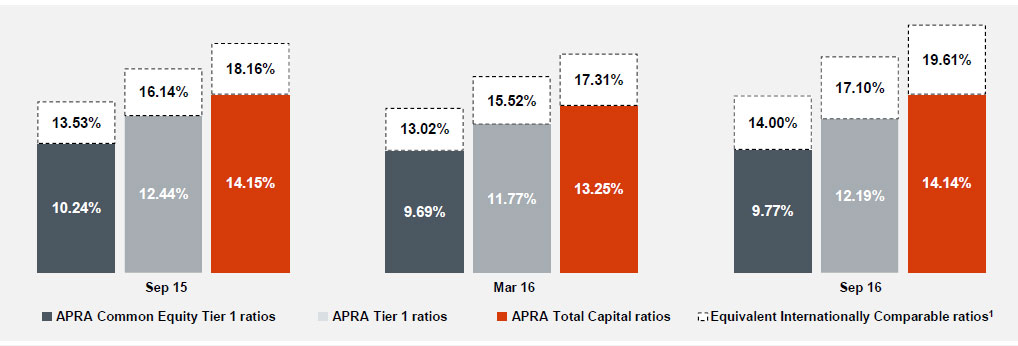

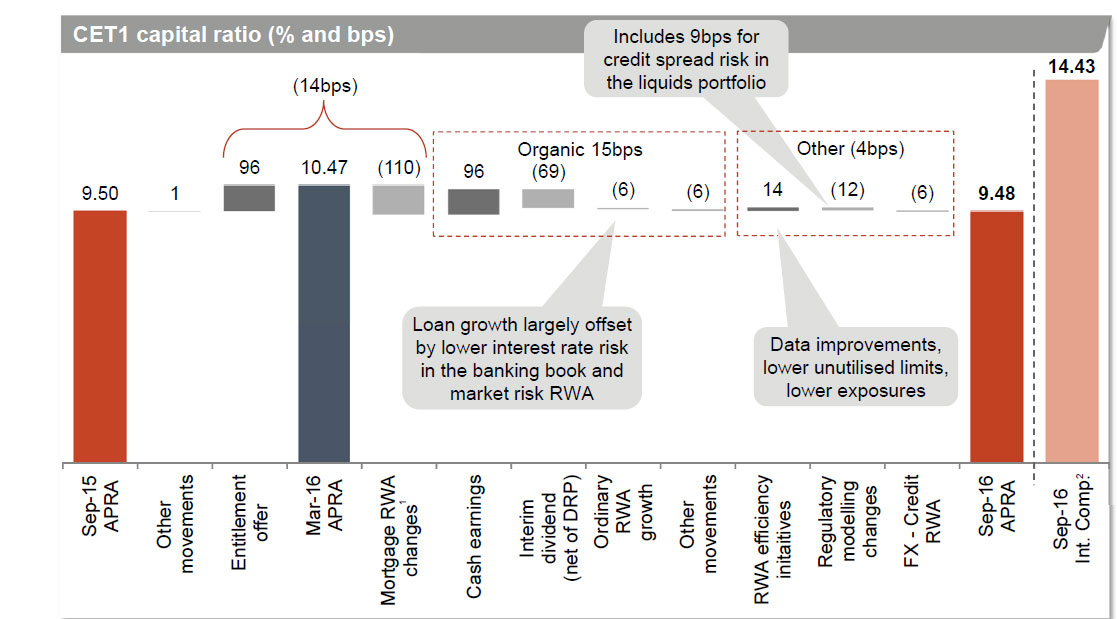

Common equity Tier 1 capital ratio of 9.5%, down 2 basis points, having raised around $3.5 billion in capital through the Entitlement Offer in November 2015.

Common equity Tier 1 capital ratio of 9.5%, down 2 basis points, having raised around $3.5 billion in capital through the Entitlement Offer in November 2015.

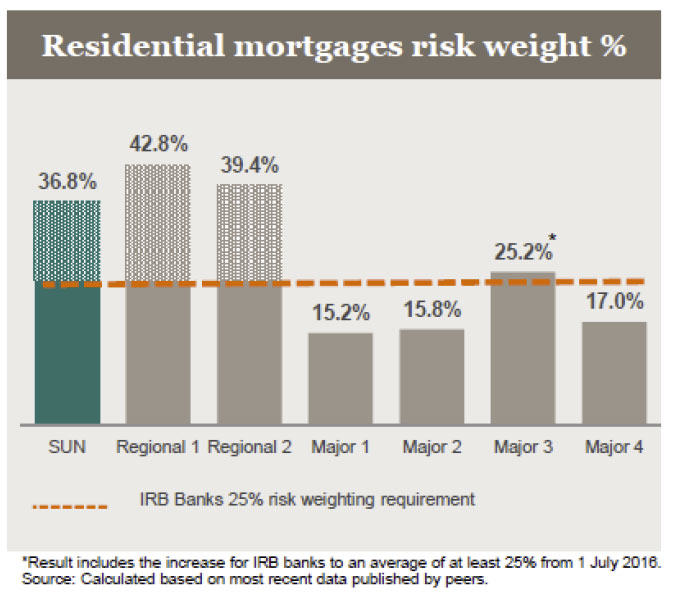

On an internationally comparable basis, Westpac’s CET1 capital ratio was 14.4% Group implemented recent APRA requirements that increased RWA by $43 billion for Australian residential mortgages.

On an internationally comparable basis, Westpac’s CET1 capital ratio was 14.4% Group implemented recent APRA requirements that increased RWA by $43 billion for Australian residential mortgages.

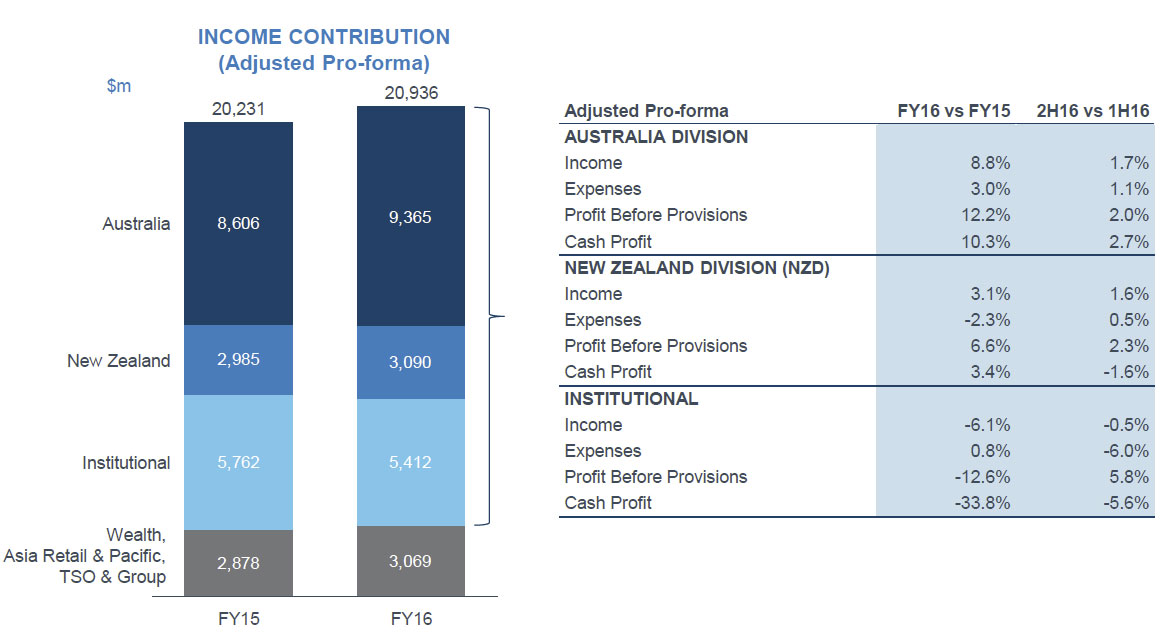

Looking at the performance of the business segments, there was strong growth in the retail franchise, especially in the Australian consumer bank.

However, conditions were tougher in the Wealth and Insurance businesses.

However, conditions were tougher in the Wealth and Insurance businesses.

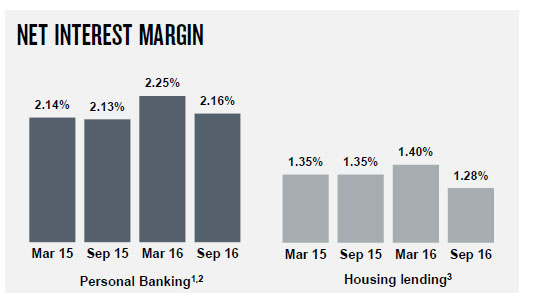

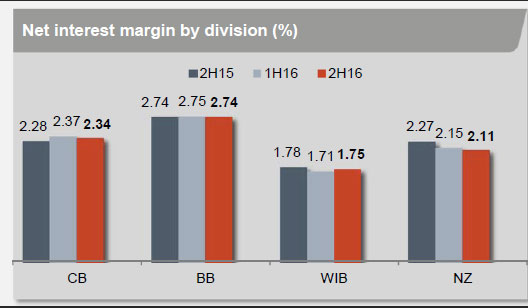

Net interest margin varies by segment.

Net interest margin varies by segment.

Fee income rose in the Australian consumer and business banks.

Fee income rose in the Australian consumer and business banks.

Consumer Bank continued to build the value of the franchise, with record new customer acquisition and 8% loan growth, contributing to a 14% rise in cash earnings. However, growth slowed in the second half, in part reflecting the impact of higher funding costs and increased competition.

Consumer Bank continued to build the value of the franchise, with record new customer acquisition and 8% loan growth, contributing to a 14% rise in cash earnings. However, growth slowed in the second half, in part reflecting the impact of higher funding costs and increased competition.

The business has continued to invest in service initiatives by improving its mobile banking apps and increasing the functionality of its online platforms. Consumer Bank remained disciplined on costs, with its cost to income ratio down 166 basis points to 40.8%.

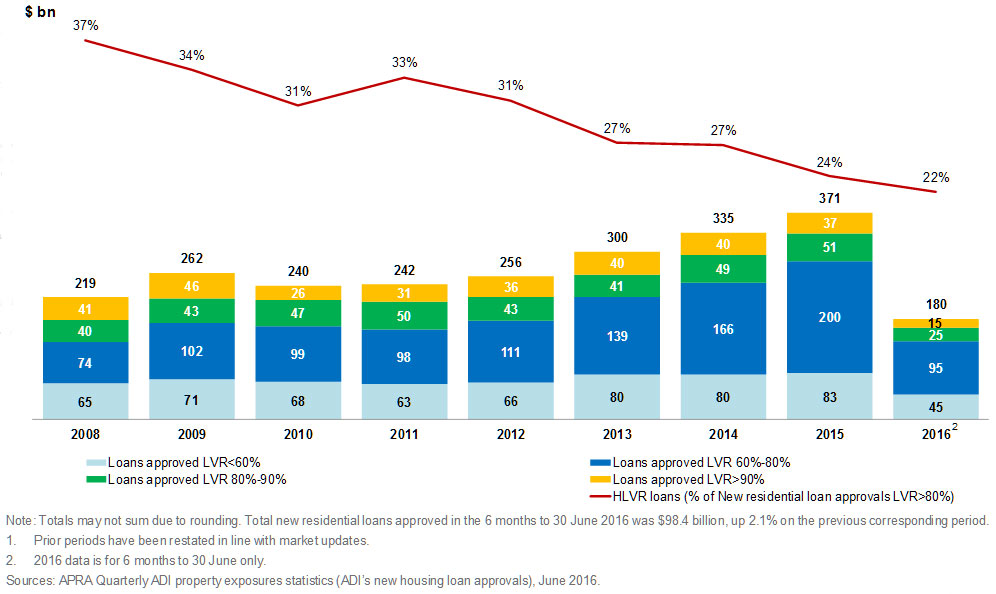

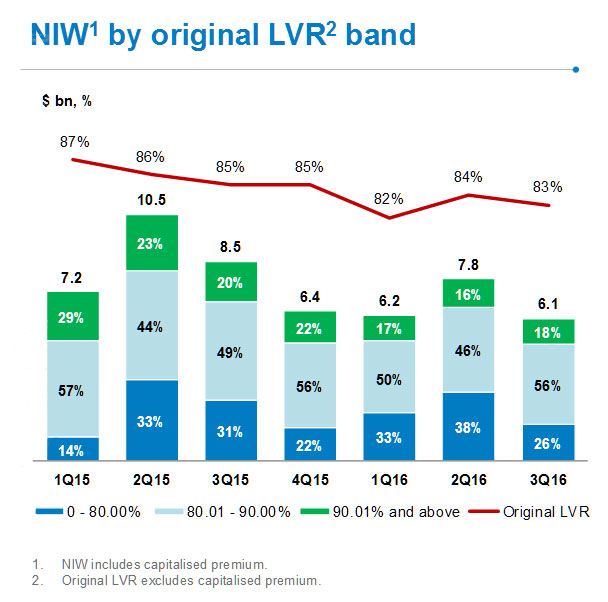

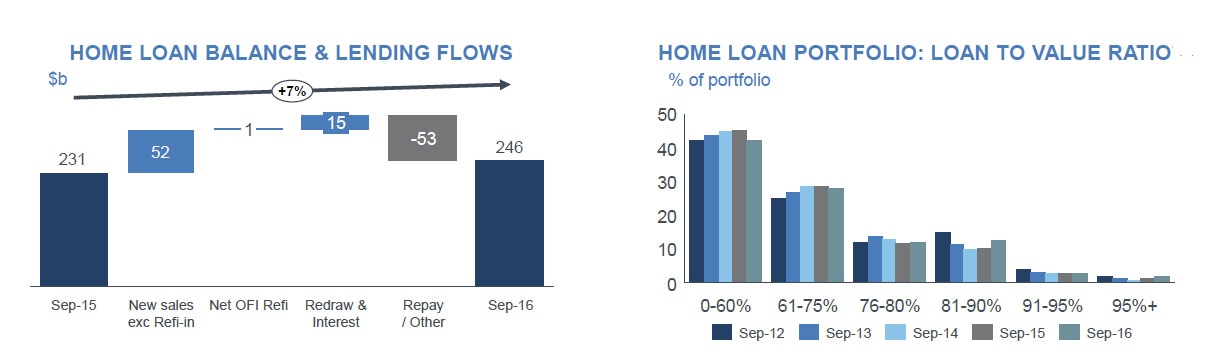

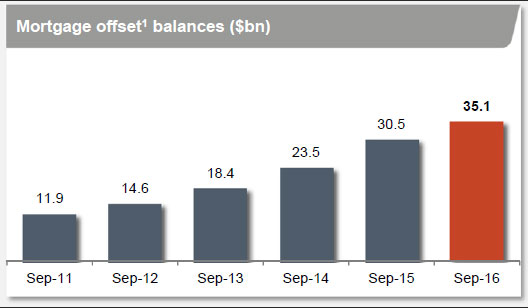

Given the importance of the mortgage book to the bank, we note the book grew from $375.8 bn in Sep 15 to $404.2 bn in Sept 16. They showed that $35.1bn are offset, including current account balances.

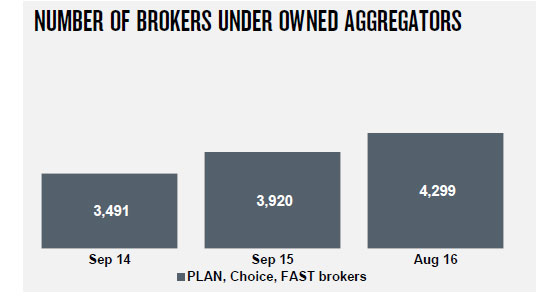

They had a flow of new mortgages of $41.8 in 2H. 39.5% are investment loans, no change on last year, and are growing at 5.9% currently. The share of loans via the broker channel have risen from 41.8% to 44.1% since last year. 83% are variable rate loans.

They had a flow of new mortgages of $41.8 in 2H. 39.5% are investment loans, no change on last year, and are growing at 5.9% currently. The share of loans via the broker channel have risen from 41.8% to 44.1% since last year. 83% are variable rate loans.

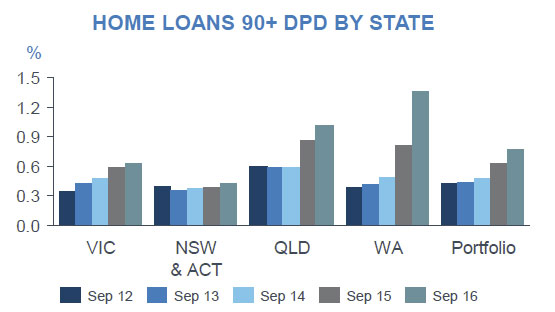

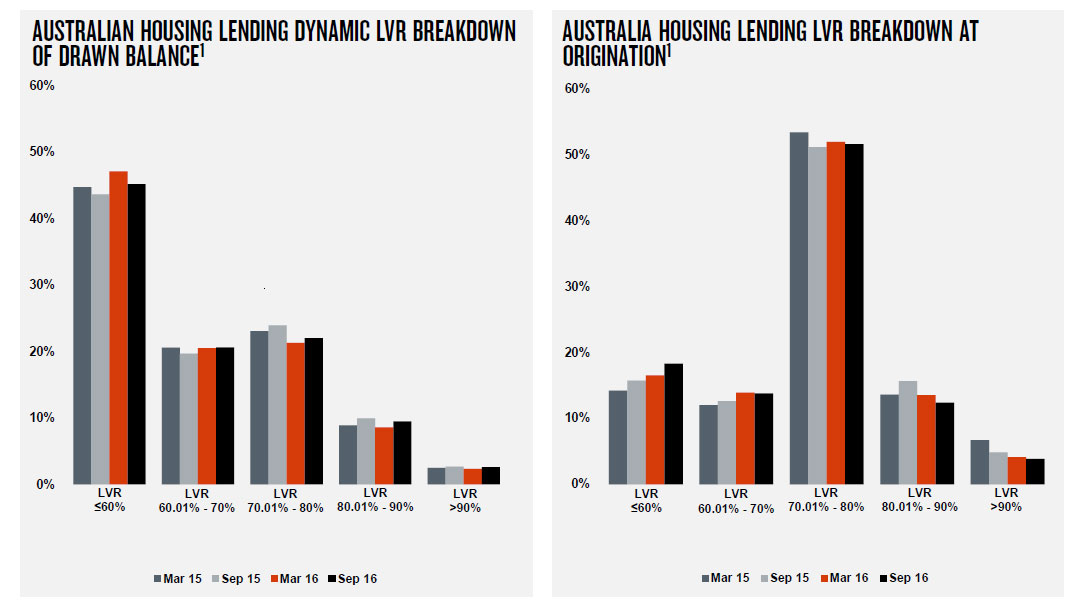

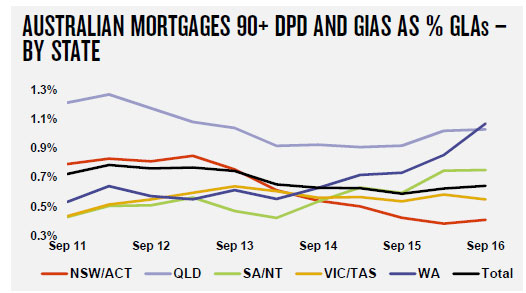

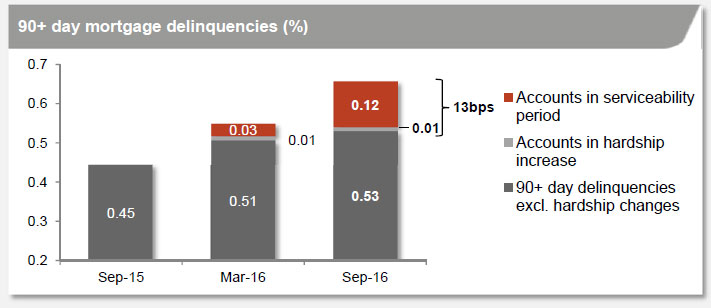

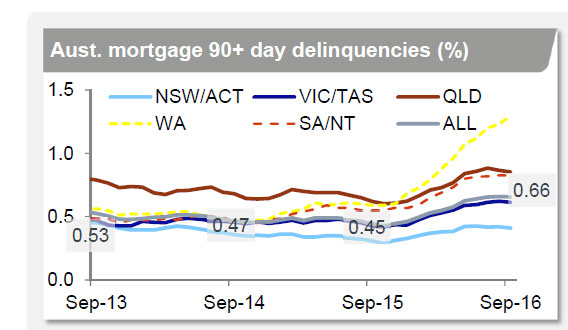

The average LVR of new loans is 70%. 72% of households are ahead with payments. Australian mortgage 90+ day delinquencies have increased 21 basis points compared to 2015, including 13 basis points from changes in how loans to customers that have been granted hardship assistance are reported.

Actual mortgage losses remain at 2 basis points, but delinquency continues to rise in WA.

Actual mortgage losses remain at 2 basis points, but delinquency continues to rise in WA.

There are only 262 houses in possession in a mortgage book which comprises 1.6 million mortgages; with losses in the portfolio equivalent to 0.02%.

There are only 262 houses in possession in a mortgage book which comprises 1.6 million mortgages; with losses in the portfolio equivalent to 0.02%.

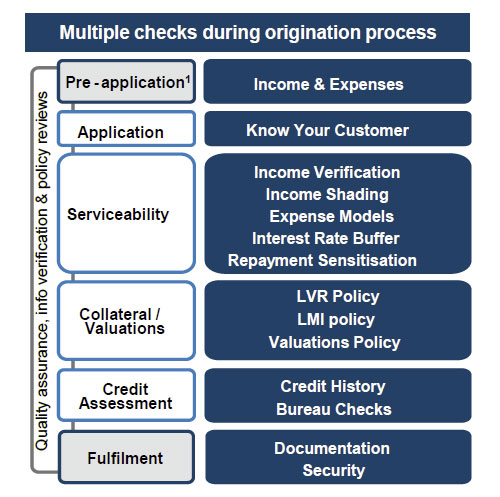

In terms of mortgage underwriting, they have had a minimum assessment (floor) rate 7.25% and buffer rate of at least 2.25% since September 2015. They have tightened policy on assessment of living expenses and income since verification in November 2015 and are discounting of rental income, annuity and pension income increased for certain loans since January 2016.

In addition, non-resident and ex-pat lending has been tightened, from April 2016, non-resident customers no longer qualify for mortgage

loans (limited exceptions) and for Australian and NZ citizens and permanent visa holders using foreign income, tightened verification processes and LVR restricted to 70% maximum.

Different rates for investment property loans and interest only

repayment types progressively introduced from August 2015.

Following guidance from APRA the industry is aligning treatment of hardship in delinquencies. Westpac changed measurement and

delinquency treatment of new hardship accounts in 1H16. No impact on the risk profile of the Group or asset classes. At the same time, hardship policies have tightened. An account in hardship is no longer frozen and

continues to migrate through delinquency buckets until 90+ days. Accounts continue to be reported as delinquent until the customer has maintained repayments for 6 months – called the ‘serviceability period’. The average hardship period granted is 3-4 months, so the hardship + serviceability period = 10 months average.

Business Bank grew core earnings by 5%, with 5% growth in lending, including 8% growth in business lending to small and medium enterprises. This reflects success in strengthening the franchise, including investing in improved digital platforms for both customers and bankers, with LOLA originating $1.4 billion in new lending to date. Revenue was up 5%, while cost growth was contained to 4% despite significant investment in digital applications. Cash earnings growth was lower at 1%, due to higher impairment charges. This largely reflects lower write-backs than previous years, and increased provisions for auto finance and those sectors and regions that are affected by the slowdown in mining investment.

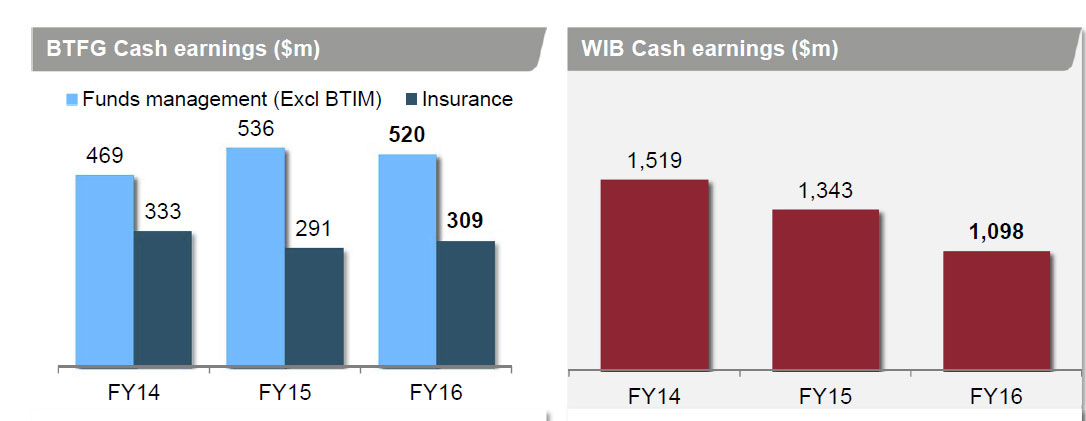

BT Financial Group achieved significant strategic milestones, although cash earnings were 4% lower due to the partial sale of BTIM, lower Ascalon contribution, and higher regulatory costs. Excluding the impact of the partial sale of BTIM in 2015, cash earnings reduced by 2%. BTFG has delivered important new core capabilities through the development of its Panorama platform, as well as significantly expanding its insurance product offering and growing FUM and FUA by 5% and 7% respectively.

Westpac Institutional Bank continues to face both structural and cyclical pressures with cash earnings down 18%. The lower result was driven by a $215 million increase in impairment charges and reduced fee income from subdued lending and markets activity. Markets income was $109 million higher due to the absence of the derivative valuation impact last year. While margins were lower over the year, WIB’s margin stabilised in the second half, expanding by 4 basis points. Despite difficult conditions, WIB was disciplined on balance sheet growth and costs, while continuing to support key customers. WIB’s asset quality remains sound. However, provisions for four large names in First Half 2016 and lower write-backs and recoveries saw an impairment charge of $177 million, compared to an impairment benefit of $38 million in full year 2015.

Westpac New Zealand’s cash earnings decreased 4% to NZ$872 million. Loans grew 9%, however, intense competition for new lending and a shift to lower-spread fixed rate mortgages has compressed margins. Weak financial conditions in the dairy sector drove stressed assets to TCE up 94 basis points to 2.54%. Impairment charges increased $12 million as a result of the increased stress in the dairy portfolio and also from a lower level of write-backs and recoveries compared to the prior corresponding period.