In a candid interview with the Australian Financial Review column, Chanticleer, high-profile business guru and founder of financial firm Yellow Brick Road Mark Bouris has reportedly said he will fire himself this financial year if his company could not to make a profit.

He admitted his reputation was at stake if he could not build YBR into one of Australia’s largest independent financial firms, the AFR said.

However, a company spokesperson told Australian Broker that this comment was intended as a direct reflection of Bouris’ commitment to do everything he could to deliver.

“He hasn’t made a commitment to resign; he has indicated his commitment to work as hard as he possibly can to deliver to outcomes the market expects,” they said.

These statements come at a tumultuous time for YBR after the firm failed to bring in a profit for FY16.

In an interview with Chanticleer, owner of accounting firm Kelly+Partners, Brett Kelly, criticised YBR’s wealth management strategy, saying it will never work.

However, in a response to this article, Bouris told Australian Broker that this was an over-simplification and that YBR was not reliant on home loans as a single entry point.

“The person talking here has never once sat down with me to talk about our wealth management strategy,” Bouris said. “He miscast the strategy and doesn’t understand Australian consumers and their preferences when it comes to financial advice. Nor does he understand our value proposition.

“In reality, Yellow Brick Road is made up of representatives across the nation – several hundred of which are financial planners. Business is driven both through people seeking a mortgage and the ensuing opportunity to discuss holistic financial goals, and conversely through a customer requiring financial advice or a specific wealth management product. This multi-faceted approach allows the business to ensure relevance to a wide demographic of people at different stages of their financial journey.”

The company also responded to Kelly’s comments to Chanticleer that Australians with money for wealth management do not go to mortgage brokers.

“It may be true that traditional mortgage broking models don’t lend themselves easily to wealth management integration,” a spokesperson told Australian Broker. “This is not the case for us. Yellow Brick Road was set up from the get-go as an integrated total wealth business where mortgages are part of a broader financial services offering.”

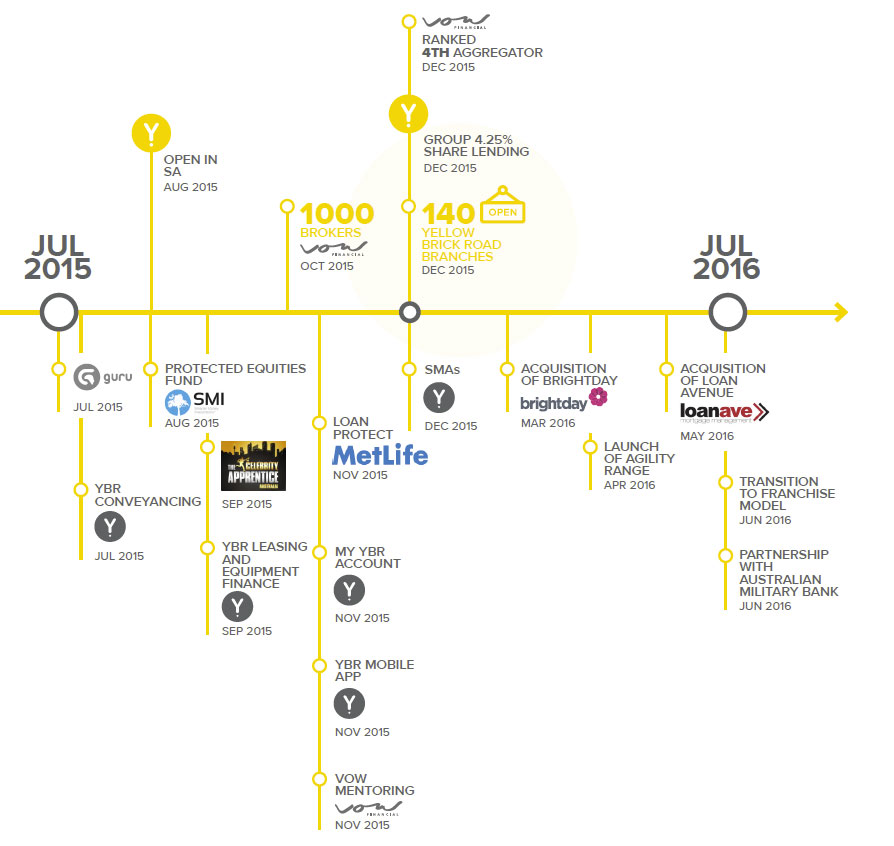

The company’s corporate strategy was changed in an investor update released last week with new goals for 2017 and 2020. This included an improved focus on wealth management, increased levels of accountability and greater branch commerciality through a franchise model.

Currently with a $38b loan book, YBR hopes to increase this to $100 billion by 2020. The firm’s distribution network presently consists of 300 branches and 1,000 broker groups.

In 2017, the company hopes to drive out its wealth model by doubling the number of branches with specialist wealth advisors. Bouris also hopes to dramatically increase lending conversion by recruiting experienced brokers with business acumen.

“Our loan book is at $38b. For context, that’s a $43b asset on our balance sheet and a 28% increase on the prior comparable period,” a spokesperson said. “We currently write more than 4% of all home loans in Australia and our market share continues to improve year on year.”