Challenger Limited (Challenger) is an investment management firm managing $60.0 billion in assets. It is focused on providing customers with financial security for retirement. Challenger operates two core investment businesses, a fiduciary Funds Management division and an APRA-regulated Life division. Challenger Life Company Limited (Challenger Life) is Australia’s largest provider of annuities.

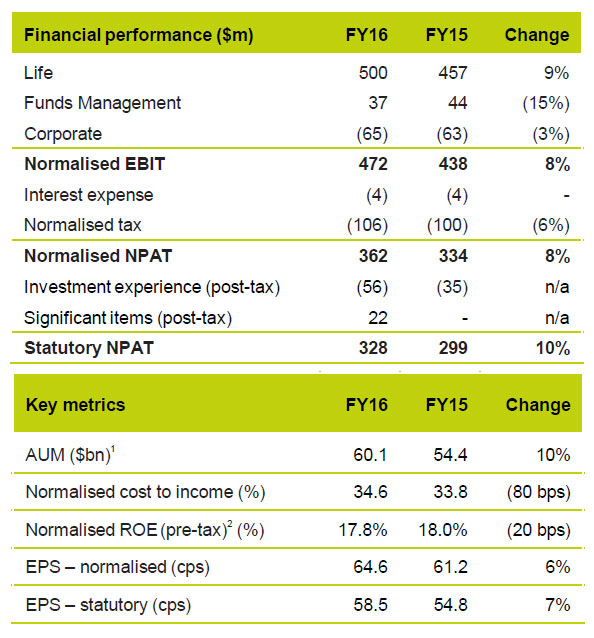

Normalised profit after tax (NPAT) rose 8% to $362 million while statutory net profit after tax was up 10% to $328 million.

The Group reported record annuity sales, up 22% on the previous year, boosted by superannuation industry moves to include Challenger annuities on investment and administration platforms. Sales accelerated in the second half with annuity sales up 45% on the prior corresponding period (pcp).

The Group reported record annuity sales, up 22% on the previous year, boosted by superannuation industry moves to include Challenger annuities on investment and administration platforms. Sales accelerated in the second half with annuity sales up 45% on the prior corresponding period (pcp).

Normalised earnings per share were up 6% to 64.6 cents per share (cps) with earnings from higher normalised NPAT partially offset by a higher share count.

Normalised return on equity (ROE) was 17.8% pre-tax, down slightly due to the impact of Brexit and market disruption affecting Fidante Partners Europe earnings.

Challenger’s sustained growth allowed the Board to declare a final dividend of 16.5 cents per share, contributing to a full year record dividend of 32.5 cents, up 8%. Dividends have doubled over the past five years.

Chief Executive Officer Brian Benari said: “We have leveraged our leadership position in a growing retirement incomes market to deliver record annuity sales and record normalised profit. We’ve rewarded our shareholders with record dividends.

“Challenger is generating superior shareholder returns through a highly efficient, profitable and sustainable model. In our Life business we have been able to maintain consistent margins for the past four years which means the growth opportunities we are capturing feed directly through to our earnings and higher shareholder dividends.

“A key feature of these results has been sales achieved through our expanded distribution capability. Building scale via platforms is an important part of Challenger’s strategy with both retail and industry fund partners.

“Over the past year Challenger has launched a number of distribution partnerships to make Challenger annuities more readily available to financial advisers and super fund members. These are already bearing fruit. Sales momentum is building through our Colonial First State (CFS) partnership with sales volume through CFS doubling in the first year that our annuities have been on their platform. Notably this includes an increased proportion of lifetime annuity sales. In 2H16, 40% of sales from platforms were lifetime annuities.

“We are launching five new annuity partnerships in 1H17 including teaming up with Suncorp to white-label Challenger term and lifetime annuities.

“The bottom line is that more retirees are buying Challenger annuities because they better understand retirement risk and seek guidance from advisers who rate us highly and can access our products much more easily from a growing range of platforms.

“Our Funds Management business is achieving double digit organic growth in FUM, benefiting from strong underlying flows of $2.4 billion in FY16. In Europe our boutique growth plan remains on track, however our listed fund capital raising business has been affected by uncertainty in the run up to Brexit. This has reduced Funds Management earnings.”

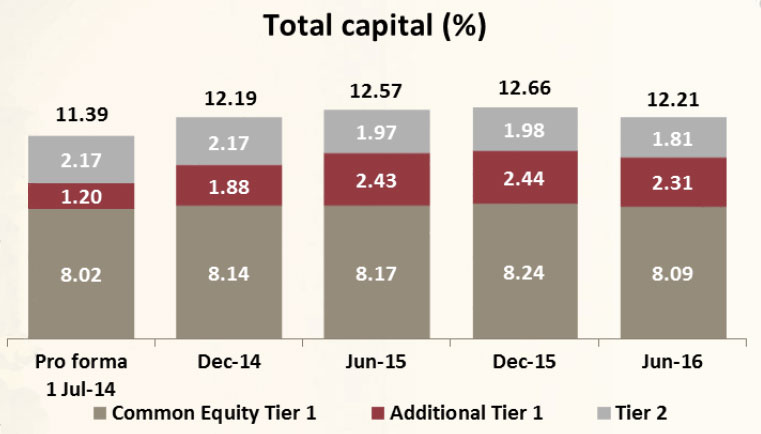

As at 30 June 2016, Challenger Life held substantially more capital than required by the Australian Prudential Regulatory Authority (APRA) capital standards comprising $1.1 billion of excess regulatory capital and group cash. Challenger Life’s prescribed capital amount ratio of 1.57 times is at the top end of its target range.

Looking at the segmental contributions:

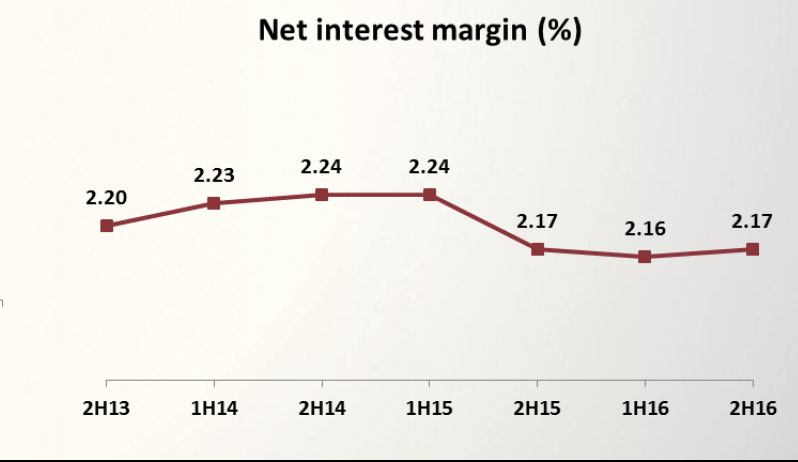

1. Challenger Life had average assets under management (AUM) over the year of $13.2 billion, up 8%. Margins continued to be stable at 4.5% which meant AUM growth in the Life business fed directly through to higher cash operating earnings (COE) of $592 million, up 9%. Life’s COE margin has consistently been in the range of 4.4% to 4.5% since 1H13.

1. Challenger Life had average assets under management (AUM) over the year of $13.2 billion, up 8%. Margins continued to be stable at 4.5% which meant AUM growth in the Life business fed directly through to higher cash operating earnings (COE) of $592 million, up 9%. Life’s COE margin has consistently been in the range of 4.4% to 4.5% since 1H13.

Annuity sales were supported by new distribution initiatives through investment and administration platforms. This contributed not only to volume but also to longer tenor of annuities. An increasing proportion of lifetime sales and longer tenor term annuity sales resulted in new business tenor for FY16 extending to 6.5 years and, for 2H16, 7.2 years.

Total annuity sales were up 22% to $3.4 billion. They comprised term sales of $2.8 billion, up 22%, with sales increasing in all quarters relative to the pcp, and lifetime sales of $0.6 billion, up 21%. Lifetime sales accounted for 21% of 2H16 annuity sales, up from 14% in 1H16.

FY16 total Life net book growth was 11.1%. Challenger’s annuity book grew by 8.5% and a Guaranteed Index Return mandate contributed a further 2.6% growth.

Sales of the CarePlus aged care product, which was launched in August 2015, accounted for $60 million, with $32 million of that being in Q416. CarePlus will be available on the CFS FirstChoice platform by September 2016.

2. Funds Management. Despite challenging markets, average funds under management (FUM) rose to $55.1 billion, up 11% once allowing for the derecognition of $5.4 billion of institutional client FUM from Kapstream Capital following our sale of that business in July 2015. The Funds Management business continued to generate strong organic net flows, amounting to $2.4 billion. This comprised $1.3 billion from pre-existing Fidante Partners boutiques, $1.0 billion from Fidante Partners Europe and $0.1 billion from Challenger Investment Partners.

Funds Management has a broad base of boutique fund managers and has a strong track record of growth. FUM has more than doubled from $24 billion five years ago at an annual growth rate of 19%, twice system growth during that period. Despite volatile markets, the business has achieved 11 consecutive quarters of positive organic flows.

In FY16 Challenger Investment Partners expanded its offshore client base, including $0.4 billion in new property and fixed income mandates from offshore investors which contributed to a 14% increase in third party FUM.

However, Funds Management earnings before interest and tax (EBIT) was down 15% to $37 million due to a loss in the Fidante Partners Europe business that was previously flagged to the market. This was impacted by capital markets uncertainty which stalled UK capital raising activity, including in the closed-end alternative investment trust segment in which the business specialises. This market is expected to normalise as uncertainty subsides. Excluding Fidante Partners Europe, Funds Management EBIT was up 7%.

3. Distribution, Marketing and Research. Challenger continues to entrench its leadership in the retirement income market through new distribution partnerships, leveraging the strength of the Challenger brand and investing in product and service capabilities.

Five new partnerships with superannuation funds and investment and administrative platforms have launched or are expected to launch in 1H17. From July 2016, Challenger annuities have been available to financial advisers through Clearview Wealth Solutions, which utilises a CFS private label platform.

In August 2016, Challenger formed a strategic relationship with Suncorp. From December, Suncorp’s financial advisers are scheduled to sell a Suncorp-branded annuity, backed by Challenger, through its national branch network.

In the industry fund sector, a previously announced strategic partnership with Link Group, which services 10 million fund members, has led to Challenger annuities being made available to members of Local Government Super and legalsuper from Q117 while caresuper is to launch Challenger annuities in Q217. These three funds combined have more than 400,000 members.

We strengthened our position as a retirement income leader through our life expectancy brand campaign, launched in 2H16, which addresses customer concerns of outliving their savings. In May 2016 Hall & Partners research found that 52% of 55 to 64 year olds would now ask their financial planner about buying annuities.

A key competitive advantage for Challenger is its distribution capability which rates highly with financial advisers. Challenger was ranked first of 20 fund managers, including the leading wealth brands, for overall adviser satisfaction in the 2016 Wealth Insights Fund Manager Service Level Report. This comprised number one ratings for five key categories, including: our business development team, for the fifth straight year; technical services and contact centre teams; and, image and reputation.