Westpac has released their 3Q19 disclosures. Mortgage delinquencies were higher which mirrors other recent bank sector results.

They reported an increase in impaired assets over the quarter, up $0.1 bn to $1.9 bn. Stressed assets to total committed exposures rose 10 basis points to 1.20%, of which 1 basis point was from impairments, 3 basis points from watch-lists etc (mainly in the retail, manufacturing and property segments), and 6 basis points related to 90+ day past due (mainly mortgages).

Total provision balances were up 1.8%.

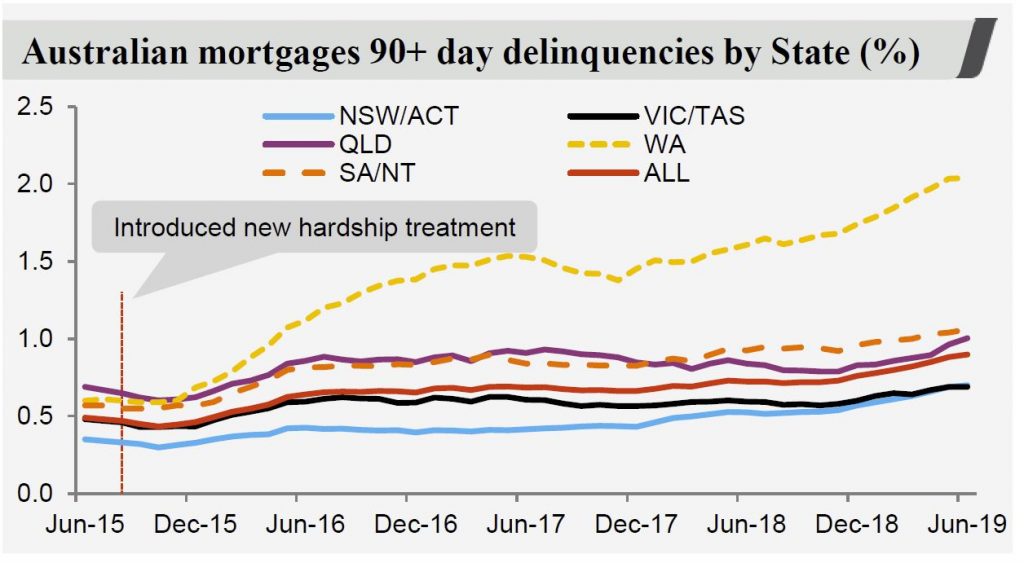

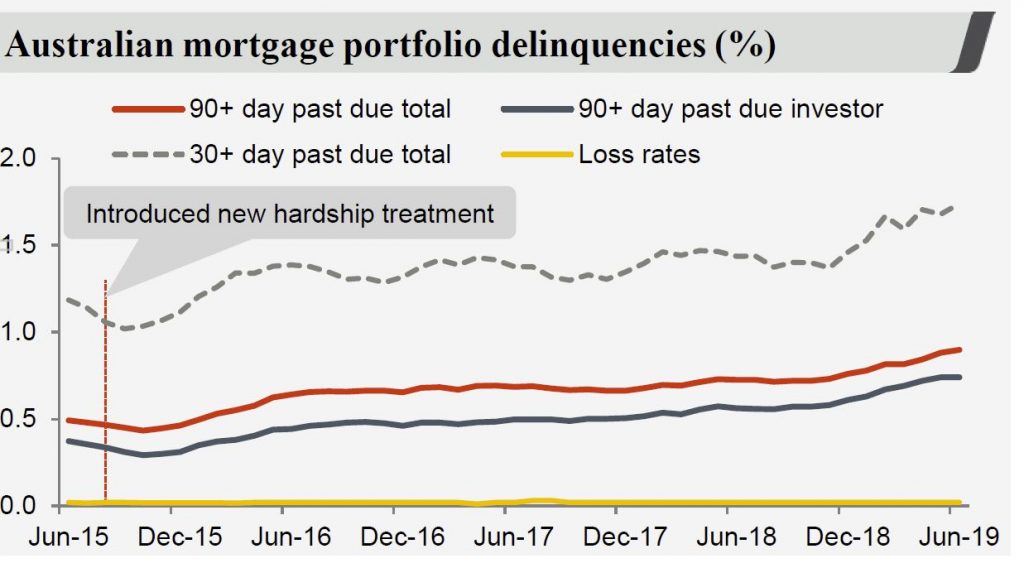

Australian mortgage 90+ delinquencies were up 8 basis points to 0.9%, with properties in possession rising by 68 to 550 in the quarter, mainly from WA and QLD.

They said that the higher stress in the portfolio combined with softness in the property market has contributed to an increase in time to sell a property. In addition, a greater proportion of P&I loans in the portfolio are lifting delinquencies, and NSW delinquencies rose to 71 basis points, though below the portfolio average.

RAMS loans continue to have a higher rate of delinquency.

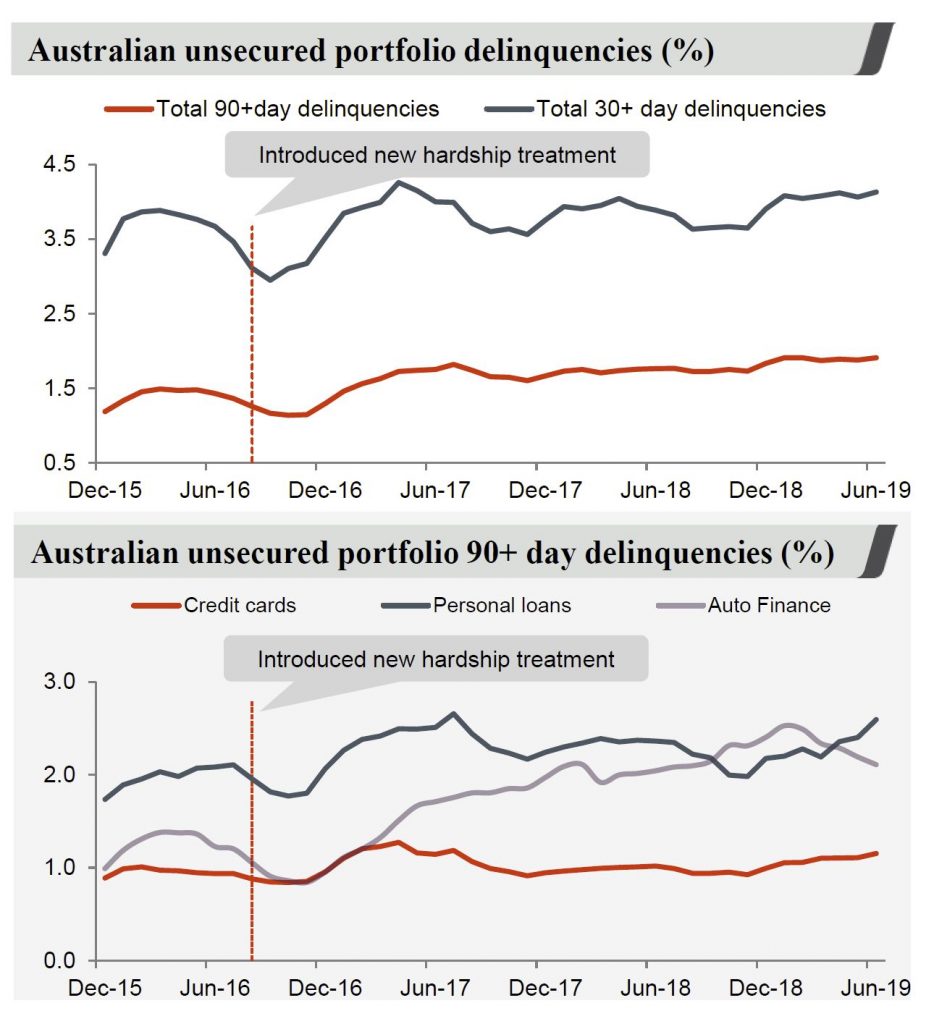

In addition consumer unsecured delinquencies rose 4 basis points, though auto finance was lower thanks to increased collection activities, to 1.91%

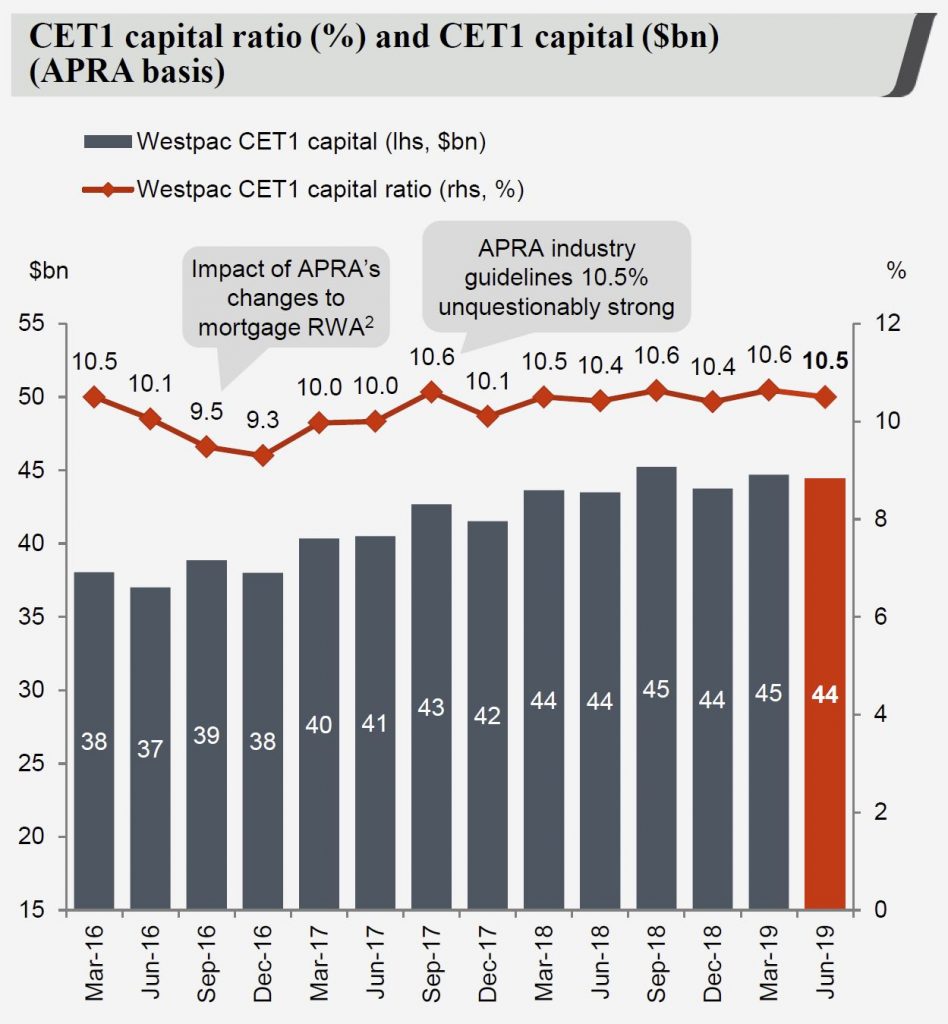

The CET1 ratio dropped to 10.5%, partly thanks to the 2019 dividend payment. The “internationally comparable” CET1 ratio was 15.9% as at June 2019.

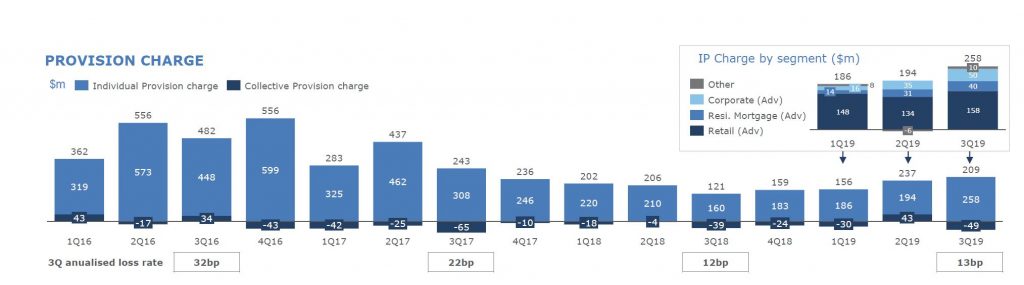

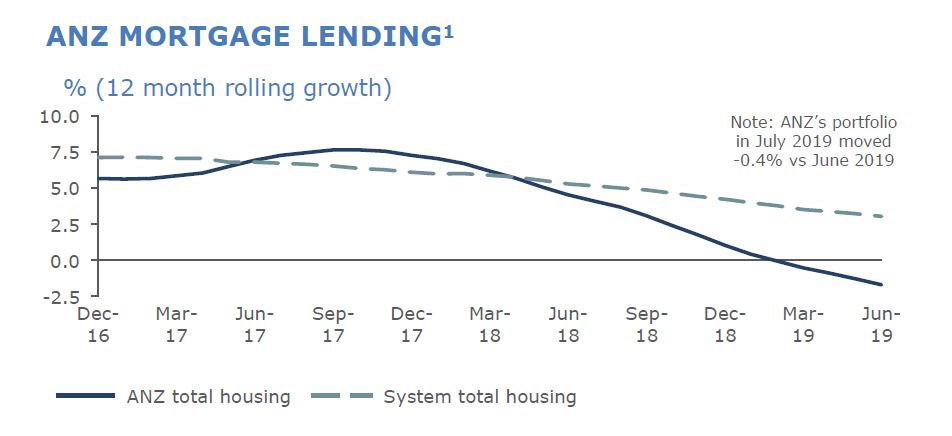

ANZ today provided an update on credit quality, capital and Australian housing mortgage flows as part of the scheduled release of its Pillar 3 disclosure statement for quarter ending 30 June 2019 and associated chart pack. Given the strategy was to shed a portfolio of businesses and focus on the Australian retail market, we need to give attention to their shrinking mortgage book and rising delinquencies.

Total provision charge of $209m for the June quarter remained broadly flat compared with the 1H19 quarterly average, while the individual provision increased $68m to $258m. Total loss rate was 13bp (consistent with the 1H19 loss rate of 13bp).

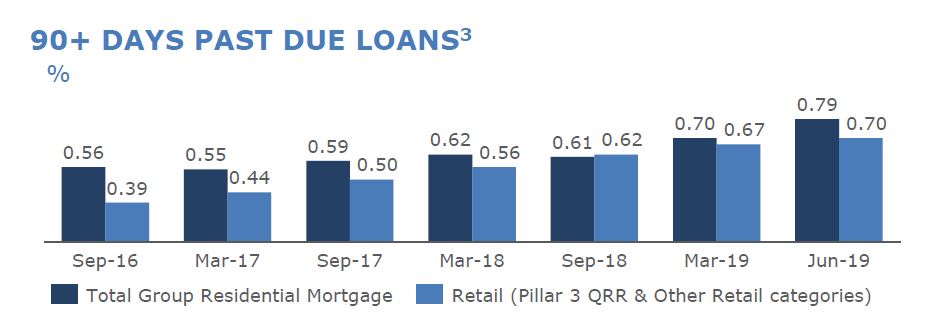

90+ Days Past Due Loans rose in the quarter.

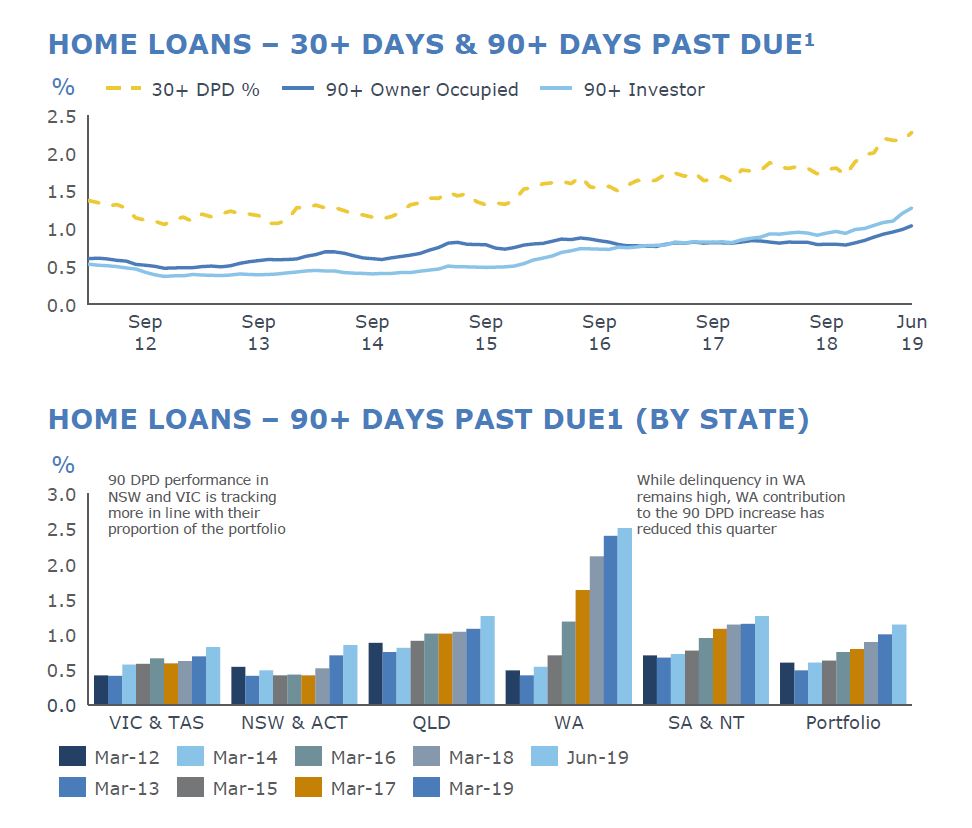

Mortgage delinquency rose in 3Q19, with 90 day increasing 14bp to 114bp. On a geographic basis, ~9bp of the movement came from NSW and VIC in aggregate. On a product basis, ~1/3 of the movement came from Interest Only home loan conversion to Principal & Interest.

WA still leads the way, but delinquencies are also rising in other states. FY17 & FY18 vintages continue to perform better than FY15 & FY16 (when of course lending standards were at their most loose, plus as we know from our mortgage stress work, it can take 2-3 years for households in financial stress to go delinquent). ANZ’s performance is likely to be biased higher given its shrinking mortgage portfolio, as we discuss below.

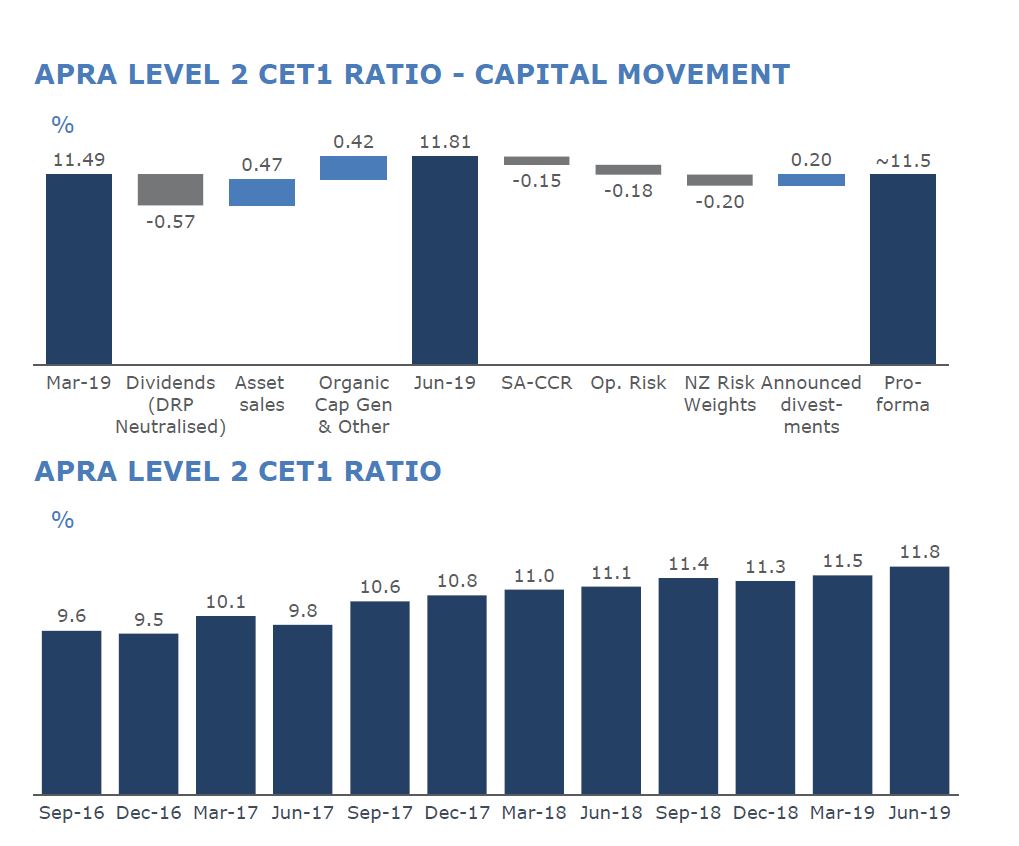

Group Common Equity Tier 1 ratio (APRA Level 2) was 11.8% at the end of June 2019, a ~30bp increase for the June quarter. On a pro-forma basis, inclusive of announced divestments and the recently announced capital changes, ANZ’s Level 2 CET1 ratio is 11.5%.

As indicated at ANZ’s first half result presentation, expectation was for home loan volumes in Australia to decline during the June quarter, with Owner Occupied down 0.2% and Investor down 1.8% (June 2019 compared with March 2019).

They say that home loan applications improved in July 2019 with actions taken in recent months to clarify credit policy and reduce approval turnaround times having a positive impact.

NAB’s update today reported an unaudited statutory net profit of $1.70 billion in the third quarter 2019, and unaudited cash earnings of $1.65 billion. This is a 1% rise in cash earnings compared with 3Q18.

They said that revenue was up 1%, thanks to a rise in SME lending and slightly higher group margins. Net interests margins increased mainly due to lower short-term wholesale funding costs. Expenses were flat, with efficiencies offsetting high compliance and risk costs.

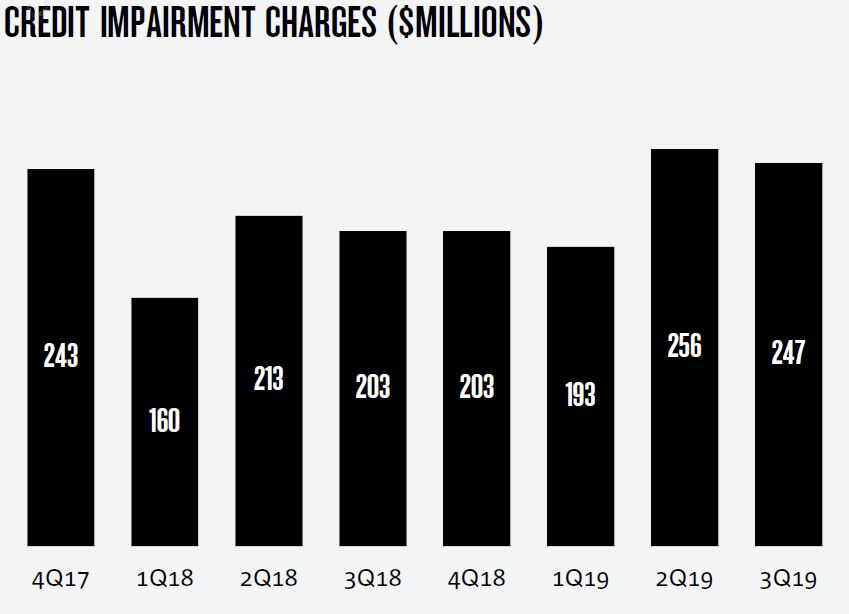

They reported that credit impairment charges increased 10% to $247 million compared to 1H19 quarterly average. The ratio of collective provisions to credit risk weighted assets increased 2 basis points to 96 basis points from March to June.

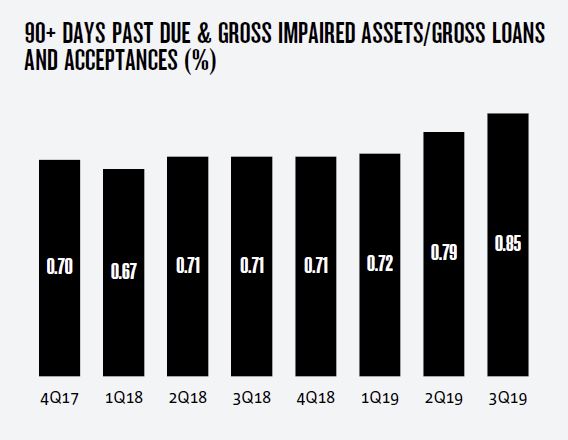

The ratio of 90+ days past due and gross impaired assets to gross loans and acceptances increased from 0.79% to 0.85%, largely due to rising Australian mortgage delinquencies.

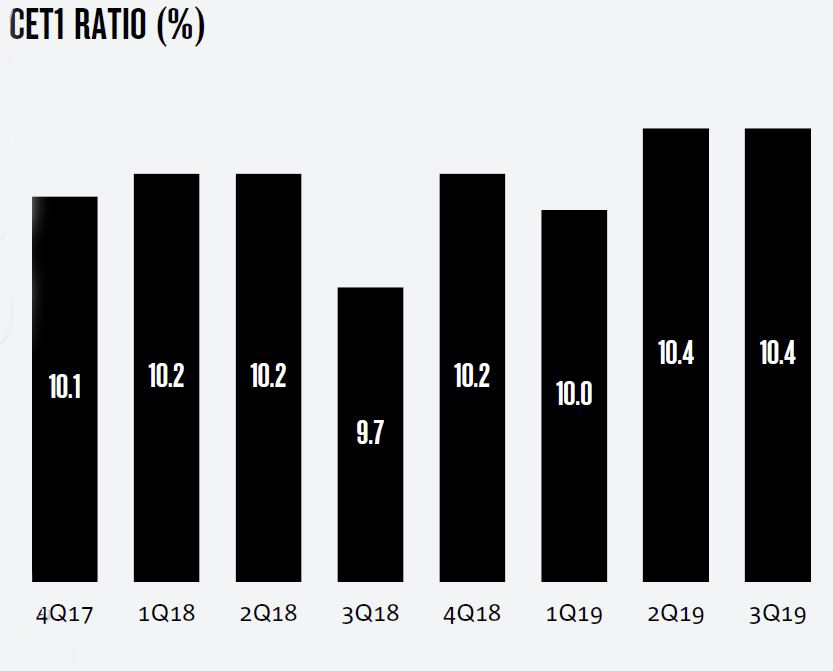

CET1 remains at 10.4%, the APRA leverage ratio is 5.4%, the liquidity ratio (LCR) quarterly average was 128% and the net stable funding ratio (NSFR) was 113%.

Bendigo and Adelaide Bank, Australia’s fifth-largest retail bank, today announced results for the year ending 30 June 2019.

Statutory net profit: $376.8 million, down 13.3 percent, as a result of remediation and redundancy costs and unrealised losses relating to Homesafe due to the decline in property valuations in Melbourne and Sydney

Cash earnings after tax: $415.7 million, down 6.6 percent, primarily attributable to remediation and redundancy costs

Underlying earnings: $435.7 million, down 2.5 percent, excluding remediation and redundancy costs

Net interest margin: 2.36 percent, steady year-on-year, increasing 2 basis points (bps) in second half, compared to the first half

Total income: $1.6 billion, steady

Bad and doubtful debts: $50.3 million, down 28.8 percent

CET 1: 8.92 percent, up 30 bps

Cash earnings per share: 85 cents per share (cps), down 8 percent

Total fully franked dividends: 70.0 cps, steady

Total lending: $62.1 billion, up 1.1 percent, with residential lending above-system, at 3.5 percent

Total deposits: $64.0 billion, up 1.5 percent, with retail deposits up 3.3 percent

“Earnings for the year were impacted by remediation and redundancy

costs. Despite this, we delivered total income of $1.6 billion, in line

with the prior year, in an environment of low growth, political

uncertainty, subdued consumer confidence and increasing competition.

“Net interest margin was steady year-on-year, and, half-on-half,

increased by 2 basis points, reflecting the active management of margin

and volume for both lending and deposits.

Key metrics

Total lending grew by 1.1 percent to $62.1 billion, with noticeably

stronger growth of 3.6 percent in the second half – well above system

growth of 2.6 percent. In the second half, residential lending was up

4.3 percent and agribusiness showed growth influenced by seasonality up

12.8 percent, both well above system; whilst small and medium-sized

business lending grew 9.5 percent.

Bad and doubtful debts being down 28.8 percent to $50.3 million.

During the year, the Bank divested Bendigo Financial Planning which

serves to further simplify and de-risk the business and deliver cost

savings.

The Board declared a final dividend of 35 cents2 per

share, taking the fully franked full year dividend to 70 cents per

share, continuing our history of rewarding shareholders with a high

yield and long-term returns.

During the year, the Bank launched Australia’s first and largest

next-gen digital bank, Up, which has exceeded initial customer growth

expectations. We also became the first lender globally to offer a

digital home loan application and assessment process under its own

brand, Bendigo Express, using Tic:Toc’s instant home loan technology.

Remediation

Total costs for remediation for the year were $16.7 million. These were all self-reported to the regulator and relate to:

Insufficient documentation to demonstrate that services had been

provided to Bendigo Financial Planning customers in accordance with

their service contracts. This business was subsequently sold.

Products not operating in accordance with their terms and conditions.

Operating expenses were $954.5 million, up 5.9 percent on prior year.

This included $16.7 million remediation costs; and $11.9 million

redundancy costs.

Excluding remediation and redundancy costs, adjusted cost to income

ratio was 57.4 percent, up from 55.4 percent in prior year, attributable

to staff costs, including the additional Elders agri-finance managers;

insurance premiums; and IT investment.

In the first half of 2019 AMP posted a $2.3 billion shareholder loss due to a non-cash impairment to write down goodwill in Australian wealth management and legacy issues. Via InvestorDaily.

The wealth giant has announced a

$650 million fully underwritten capital raising which will enable it to

set out on its new three-year transformational business plan.

The

shareholder loss is a far cry from last year when the group posted a

shareholder profit of $115 million but the wealth giant was still able

to announce an underlying profit of the half year of $309 million.

However

this profit was also a decline in the first half of 2018 where the

underlying profit was $495 despite royal commission and client

remediation costs and was short of initial forecasts of a $390 million

underlying profit.

The

capital raising, together with the sale of AMP Life to Resolution Life

for $3.0 billion, will form the financial backing for the ambitious

program announced by chief executive Francesco De Ferrari.

“The

strategy we’re launching today repositions AMP for the future, there’s a

strong need for what we offer across all of our spectrum. And we have

the business model to capitalise on the significant industry disruption

that’s occurring,” he said.

The strategy includes plans to

reinvent its wealth management business to “help clients realise their

ambitions” and will shift focus to direct-to-client channels and digital

solutions.

The strategy will also integrate AMP Bank solutions

with wealth management, grow AMP capital through differentiated

capabilities and transform AMP culture to be client-led with effective

management of financial and non-financial risk.

It is estimated

that this program will cost between $1.0 billion and $1.3 billion said

Mr De Ferrari with an element of that to be delivered by cost savings.

“To

deliver the strategy, we are investing between one at $1.3 billion

during the next three years, and of this investment, approximately a

third will be spent on growth…a third of this to take cost out of our

business. We’re going to spend the last third of this investment toward

de-risking the business and addressing legacy issues,” he said.

According

to AMP’s release $350 million to $450 million will be spent on growth,

the same amount realising cost improvement, including a delivery of $300

million in cost savings by 2022 and a $350 million to $450

million investment in tackling legacy issues.

Mr De Ferrari said

it was important that the balance sheet remains unquestionably strong

and the capital raising would allow AMP to implement its strategy and

continue growth.

“The capital raising and the AMP Life sale will

provide the funds to implement immediately our new transformational

strategy, which creates a simpler, higher growth and higher return AMP

that’s focused on clients and ensures that our balance sheet will be

unquestionably strong,” he said.

AMP also confirmed it was on

track to complete its remediation program during 2021 with an initial

estimate of $778 million including both aligned and salaried advisers.

The

amount provisioned as part of total estimate has increased by $16

million to $672 million reflection lost earnings and program costs with

$60 million spent to date.

AMP’s chief financial officer

designate John Patrick Moorhead has confirmed he is leaving the role

with James Georgeson, current deputy CFO being appointed to the role of

acting CFO and will commence handover with retiring CFO Gordon Lefevre.

Mr

De Ferrari also saw his remuneration adjusted to $2.45 million to

reflect the share price of the group preceding his start date and the

face value of his buyout incentive has decreased to $7 million from $10

million.

The board has also replace the recovery incentive with the new award to have a face value of $4.4 million, down from $6 million.

CBA reported an 8.1% drop in profit over fiscal year 2019 in its full year results released this morning.

Commonwealth Bank’s (CBA) FY19 net profit was $8.6bn as compared to $9.4bn the year preceding. NIM looks under pressure ahead (thanks to lower cash rates) and non-performing loans are on the rise. The mortgage business may offer some support ahead.

CEO Matt Comyn partially attributed the “subdued” result to higher

remediation costs totalling $2.2bn in FY19, up $1bn from the year

before.

He said, “While this year’s headline results were impacted by

customer remediation costs, revenue forgone for the benefit of customers

and elevated risk and compliance expenses, our core business continued

to perform well – underpinned by growth in home lending, business

lending and deposits.”

“Our home lending balances are up 4%, which is above the system. Our

business lending is also up 4% and we’ve continued to see strong

transaction deposit growth of 9% for the year.”

Owner-occupied loans made up 71% of new lending in FY19.

Comyn also provided an update on the implementation of the recommendations from the royal commission.

“We’ve already completed six of the recommendations and we’re going

to make sure we complete at least another eight before the end of the

calendar year, taking the total to 14 of the 23 that we can implement by

ourselves,” he said.

“Specifically in the result, we call out $275m of revenue that’s been

forgone by deliberate choices that we’ve made to make sure we’re

delivering better outcomes for our customers.”

The bank also gave an update on the suspended demerger of its wealth management and mortgage broking businesses, communicating it intends to cease providing licensee services through Financial Wisdom by June 2020 at which point it will proceed with an assisted closure.

When first announced, the demerged business – CFS Group – was to include CBA’s Colonial First State, Colonial First State Global Asset Management (CFSGAM), Count Financial, Financial Wisdom and Aussie Home Loans businesses.

In the subsequent months, CFSGAM and Count Financial have both been

sold or are currently in the process of being sold separately.

In today’s release, CBA reiterated that it’s “committed to the orderly exit of its remaining wealth management and mortgage broking businesses,” comprising Colonial First State, Aussie Home Loans and CBA’s 16% stake in Mortgage Choice. From Australian Broker.

The Australian Information Commissioner (Commissioner) has accepted an Enforceable Undertaking (EU) offered by Commonwealth Bank of Australia (CBA).

The EU underpins

execution of further enhancements to the management and retention of

customer personal information within CBA and certain of its

subsidiaries.

The EU follows CBA’s ongoing work to address two incidents; one

relating to the disposal of magnetic data tapes containing historical

customer statements; and the other relating to internal user access to

certain systems and applications containing customer personal

information. CBA reported both incidents to the Office of the Australian

Information Commissioner (OAIC) in 2016 and 2018 respectively and has

since been working to address these incidents.

As previously announced, CBA has found no evidence to date, as a

result of these incidents, that our customers’ personal information was

compromised, or that there have been any instances of unauthorised

access by CBA employees or third parties.

CBA’s commitments in the EU announced today include reviewing and implementing further enhancements to:

internal privacy policies, procedures and record retention standards;

internal user access controls on systems and applications that hold personal information; and

the privacy risk management and monitoring processes that apply to service providers to CBA and certain subsidiaries.

The EU provides CBA with 90 days to develop and submit to the OAIC a

work plan, and timetable of work that CBA will complete to meet its

obligations under the EU.

Commonwealth Bank Group Chief Risk Officer, Nigel Williams, said: “We

have offered this EU as a demonstration of our continued commitment to

appropriately managing the privacy of customer personal information, and

addressing any concerns identified by the Commissioner.

“We continue to take action to address issues, earn trust and be a

better bank for our customers. This includes proactively engaging with

our regulators to ensure we continue to build better systems, processes

and controls to manage the personal information of our customers.”

Suncorp today announced that CEO and Managing Director Michael Cameron will be leaving the company after almost four years in the role and seven years as a Board member.

Mr Cameron has led a significant digital transformation of Suncorp,

an enterprise wide focus on the customer and navigated the business

through a period of unprecedented regulatory change.

Chairman Christine McLoughlin said that while Mr Cameron had made a

considerable contribution, now was the right time for change. This will

provide the opportunity for the Company to enhance its performance in a

highly competitive and challenging external environment as Suncorp seeks

to strengthen its core businesses by focusing on its customers,

products and brands.

“On behalf of the Board I would like to thank Michael for his

leadership in accelerating our digital capability and in driving a

customer-first culture,” she said.

To ensure a smooth transition, Mr Cameron will remain employed in an

advisory capacity until 9 August 2019 following the release of Suncorp’s

full year results.

Mr Cameron said it had been a great privilege to lead Suncorp and he was proud of what had been achieved.

“Suncorp now has the digital foundations in place to enable it to be

nimble and to seize opportunities. I believe the business has great

potential and will continue to enjoy success,” Mr Cameron said.

In the interim, the Board has appointed Group CFO Steve Johnston as Acting CEO.

Ms McLoughlin said Mr Johnston is an extremely experienced executive

and has a deep understanding of Suncorp’s core insurance and banking

businesses. He is best placed to lead Suncorp and build on the Group’s

multi-channel capability.

“Steve is highly regarded by his peers and has successfully served in

various leadership roles in his 13 years at Suncorp. He has played an

integral role in the transformation of Suncorp,” Ms McLoughlin said.

Mr Johnston said he was honoured to take on the role of Acting CEO and lead this highly respected business.

“I recognise the importance of this role, especially during this

challenging time for the financial services industry. I am truly

passionate about what we do and confident in our future,” he said.

The Board has a robust approach to internal succession planning and

Ms McLoughlin confirmed it is in a strong position to supplement this

with a search to identify external domestic and international candidates

who will also be considered in the selection process. The Board hopes

to be in a position to announce the new CEO in the latter part of the

year.

Jeremy Robson will step into the Acting Group CFO role while the

Board completes the succession process. Mr Robson has been with the

Group for six years, most recently as Deputy CFO.

While the external operating environment remains challenging, Suncorp

confirms its FY19 cash earnings are in line with market expectations.

As noted at the interim result the external operating environment

including natural hazards above allowance, investment market performance

and unforeseen regulatory costs will impact the Group’s FY19 reported

result and outlook.

Suncorp will deliver its full year 2019 result on 7 August 2019.

Brisbane group Blue Sky Alternative Investments has gone into receivership following the breach of its $47.7 million loan facility from US-based Oaktree Capital Partners., via InvestorDaily.

The fund is now considering its options including a wind-down and a return of capital to shareholders.

“This

appointment is necessary if Blue Sky is to maintain its investment

teams, key clients and stabilise the operations and capital structure of

the business,” Blue Sky told its shareholders.

The

company added its administration follows “a period of significant

instability and uncertainty for all stakeholders, including further

commentary regarding possible class actions, turnover of senior

corporate executives and departure of certain partners. There is

considerable work to be undertaken in the immediate future.”

Blue

Sky had $2.8 billion in fee earning assets under management as of 31

March, down from its half year result of $3 billion as reported at the

end of December.

Blue Sky has now paused

trading, but closed on Friday with its shares at 18 cents. They had once

reached $14.99 in November 2017.

The company reported a $25.7 million loss for the half year, which it attributed to its business restructuring costs.

Mark

Korda and Jarod Villani of advisory and investment firm KordaMentha

have been appointed as receivers and managers, while Bradley Hellen and

Nigel Markley of Pilot Managers will be acting as voluntary

administrators.

KordaMentha partner Mark Korda said the appointment would not affect the day-to-day operating activities of the asset manager.

“Our

objective during the first phase of the receivership is to stabilise

the business as a strategic assessment is undertaken,” Mr Korda said.

“Existing

management and key contacts for relevant stakeholders, employees and

unitholders will continue to be in place as normal.

“It

will allow greater flexibility for the restructure of Blue Sky and seek

to ensure the future of the business as an alternative asset investment

management platform.”

Oaktree had given the Brisbane-based asset manager the loan facility in September last year.

The

US investment group’s managing director Byron Beath resigned as a

director on the Blue Sky board as the loan breach was announced to the

market

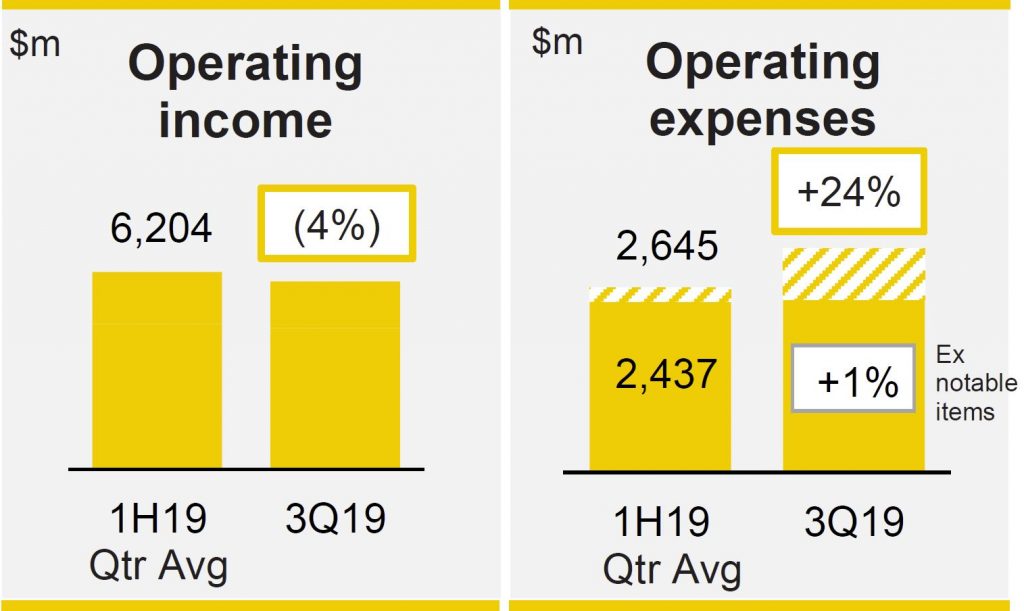

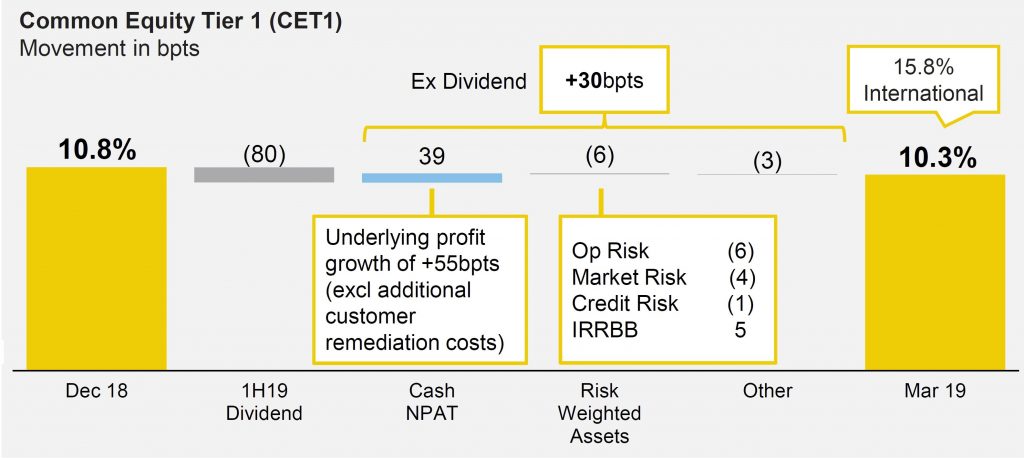

CBA released their quarter update to 31 March 2019. Its an unaudited summary. Its weak, and confirms the trends we saw elsewhere. Customer remediation is costing them dear. CBA shares dropped.

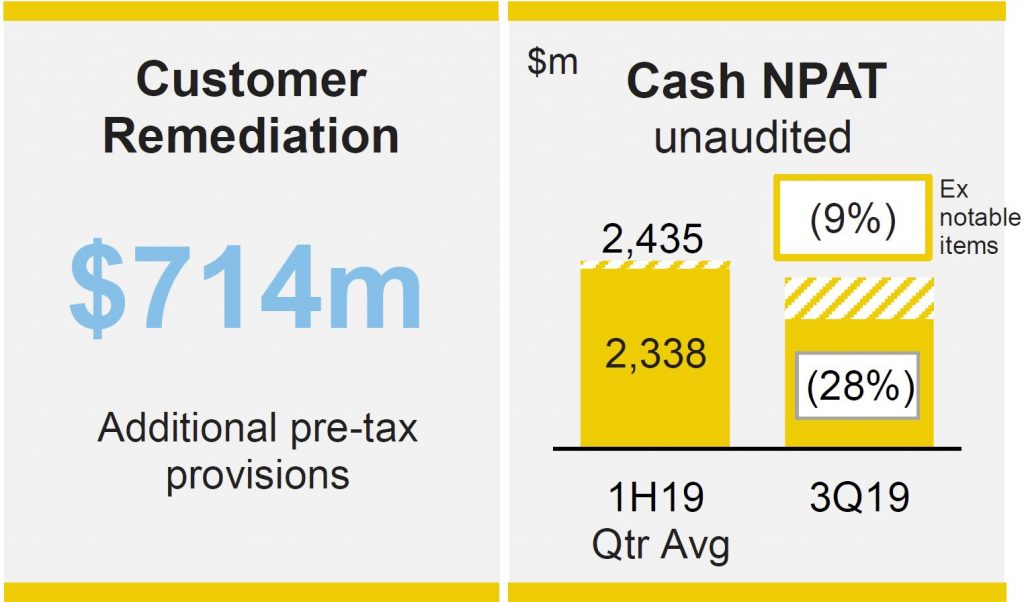

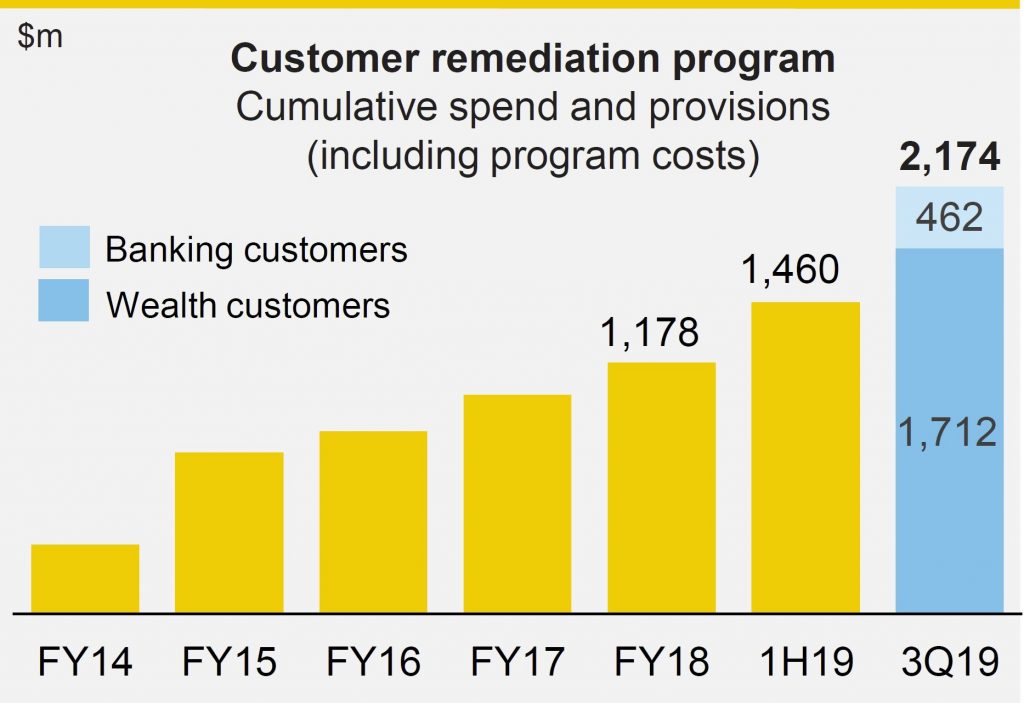

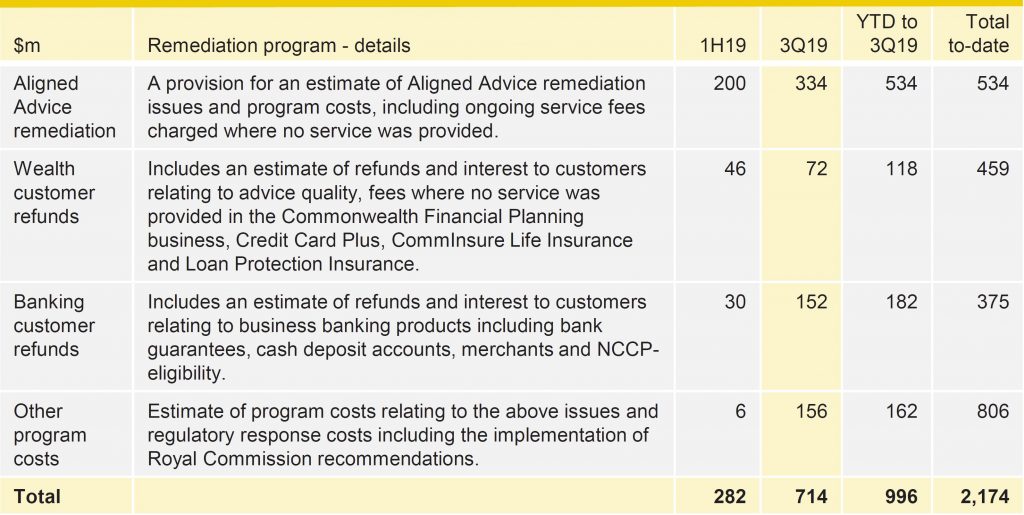

They announced an unaudited statutory net profit of $1.75 billion and a cash net profit of $1.70 billion. Headline profit was impacted by $714 million in pre-tax additional customer remediation which translates to $500 million post-tax.

Customer remediation on a cumulative basis now stands at $2.17 billion, an astonishing amount.

They provided a breakout. Fee for no service and costs of the remediation programmes were the largest items. $374m is included for customer refunds – including $123 million of interest and assumes a refund rate of 24% excluding interest of the ongoing service fee costs from FY09-FY18.

Operating income was 4% lower, thanks to a range of factors, including seasonal factors, “temporary headwinds” including unfavorable derivative valuation adjustments and weather events), and re-based fee income.

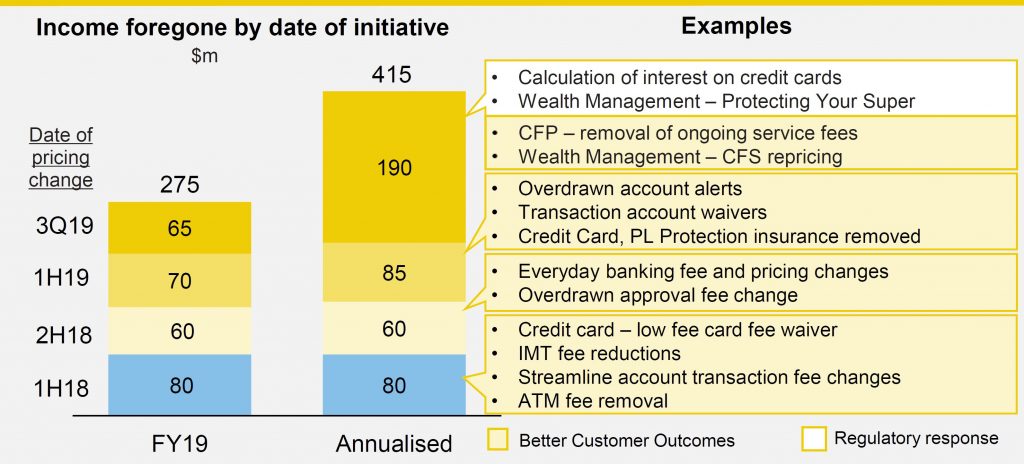

Net interest income was down 3% (due to fewer days in the quarter). The Group’s net interest margin fell “slightly”. Non-interest income was 10% lower, thanks to some “Better Customer Outcomes” initiatives. Income foregone is $415 million, of which $275 million will be recognised in 2019.

Operating expenses rose 1% excluding notable items, of 24% including the additional customer remediation.

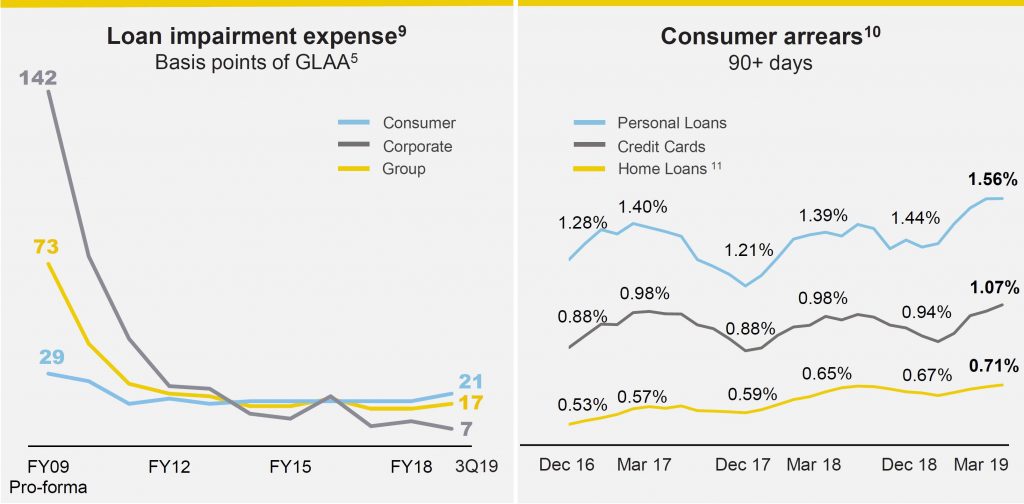

Loan impairment expenses was $314 million in the quarter or 17 basis points of Gross Loans And Acceptances, compared with 15 basis points in 1H19. This includes higher levels of consumer arrears and corporate impaired assets.

Consumer arrears are conveniently attributed to “seasonal factors”, as well as a rising trend, thanks to subdued levels of income growth and cost of living challenges, most evident in the outer metro areas of Perth, Melbourne and Sydney.

Accounts in negative equity are more than 3% of total accounts, based on 31 March 2019 (so higher now). Around three quarters of the negative equity relates to WA and QLD.

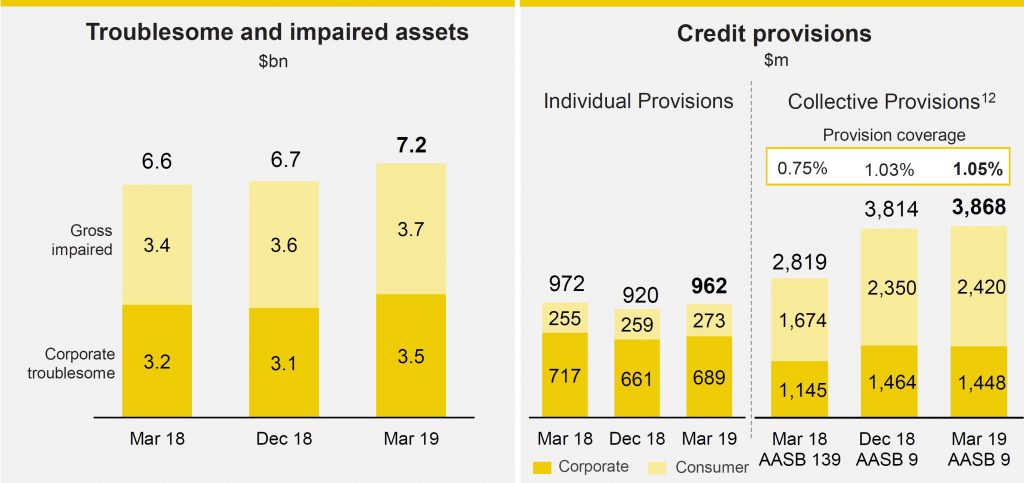

Troublesome and impaired assets rose to $7.2 billion. There are emerging signs of weakness in discretionary retail and drought-affected farmers and communities, including some named corporates, and home loan customers experiencing hardship.

Total provisions were increased by $96 million to around $4.8 billion dollar, and collective provisions were also lifted.

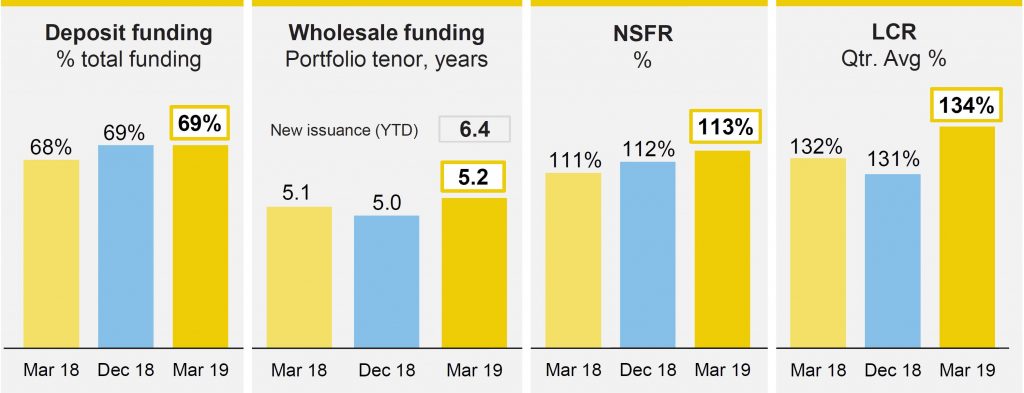

The banks ratios were pretty strong.

But the CET1 ratio fell from 10.8% to 10.3%., after the impact of dividend payments.

We expect to see more pressure on the sector ahead.