Westpac has released their 2018 full year results. They had already signalled customer remediation costs, and its impact on profitability, but their net interest margin was significantly lower in the second half, and 90+ mortgage delinquency continued to rise in Australia. Total provisions were lower. Capital ratio though are in good shape. The proportion of IO loans is falling, and they expect more home price easing.

CEO Harzter said ““We expect house prices to cool further, and investor demand to remain weak. On the other hand, demand from first home buyers is holding up. These dynamics are likely to lead to housing credit growth easing to 4% next year, with total credit growth of 3.5%. With around 70% of Australian customers ahead on their repayments and delinquencies low, credit risks in the housing market currently remain low”.

However, their disclosed stress tests suggest in a severe downturn cumulative total losses could be $3.9bn over three years.

Cash earnings were $8,065 million, little changed on last year. Cash earnings per share, 236.2 cents, down 1% and the cash return on equity (ROE) was 13.0%, at the lower end of the range Westpac is seeking to achieve. The final, fully franked dividend was unchanged, of 94 cents per share (cps), so the full year, fully franked dividend of 188 cps. Statutory net profit was $8,095 million, up 1%.

The cash earnings included $163 million in remediation charges, and a fall of $240 million in non-interest income, a a reduction in impairment charges.

There was a fall of $263 million in the second half in net interest income. and a 10% reduction in earnings, with remediation costs of $430 million.

Income was down 3% over the half, thanks to margin decline and customer remediation.

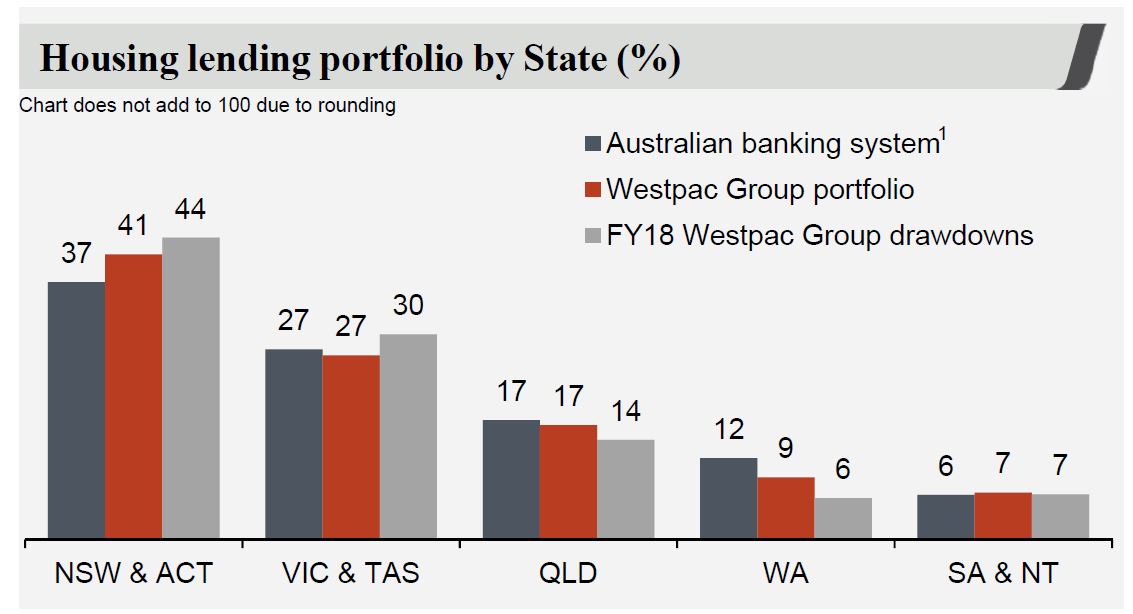

They highlight that Australian mortgage growth is moderating and interest only loans are down $53 billion since March 2017.

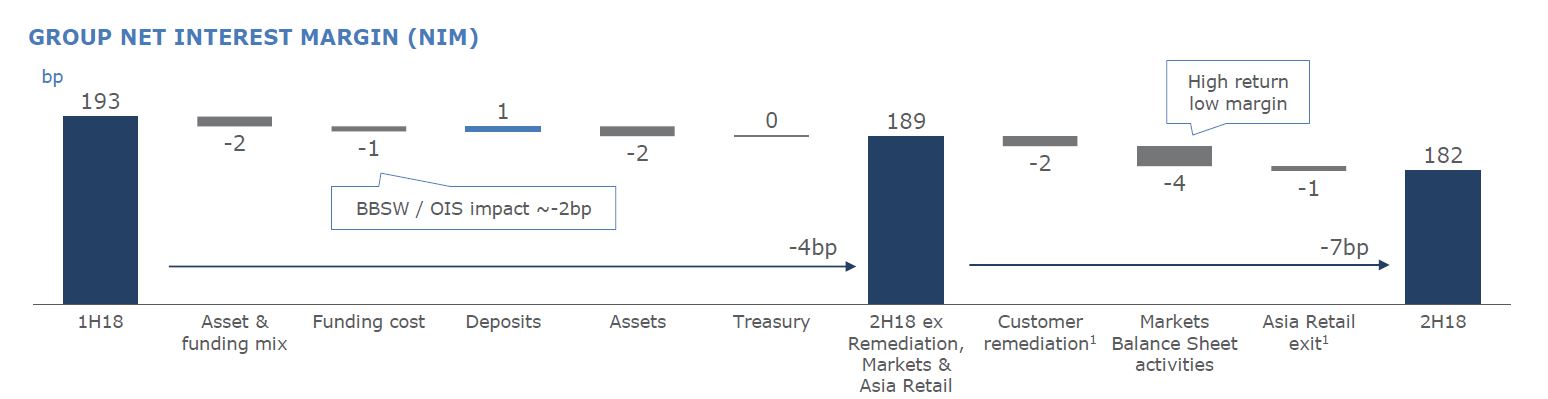

Margins in the second half were down from 2.05 to 1.95, or 10 basis points in the main banks, and from 0.12 to 0.10 in the Treasury and Markets. 5 basis points related to wholesale funding, and 4 basis points loans, offset by 1 basis point from deposits.

Non interest income fell and included provisions for customer refunds of $156 million and lower trading income, which was down 18% in the second half.

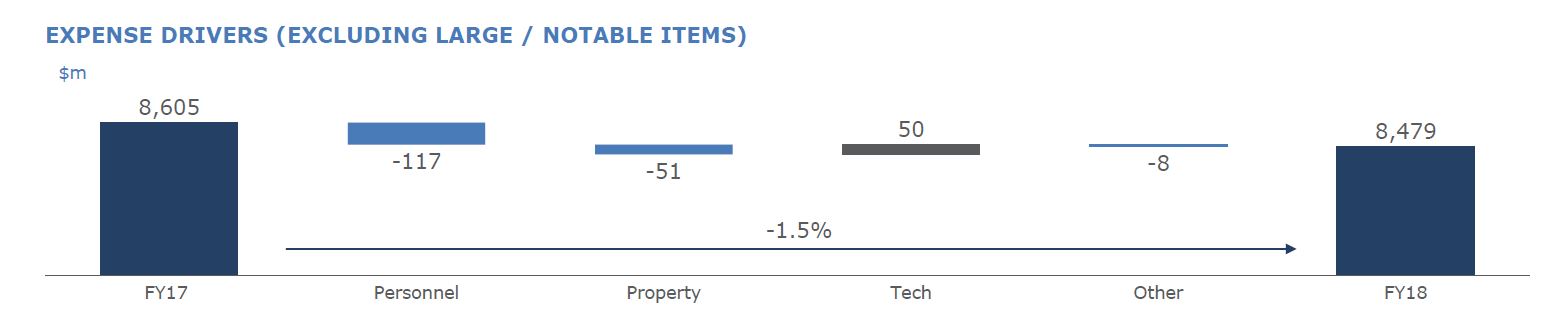

Expenses were higher thanks to regulation and compliance, remediation and platform investments.

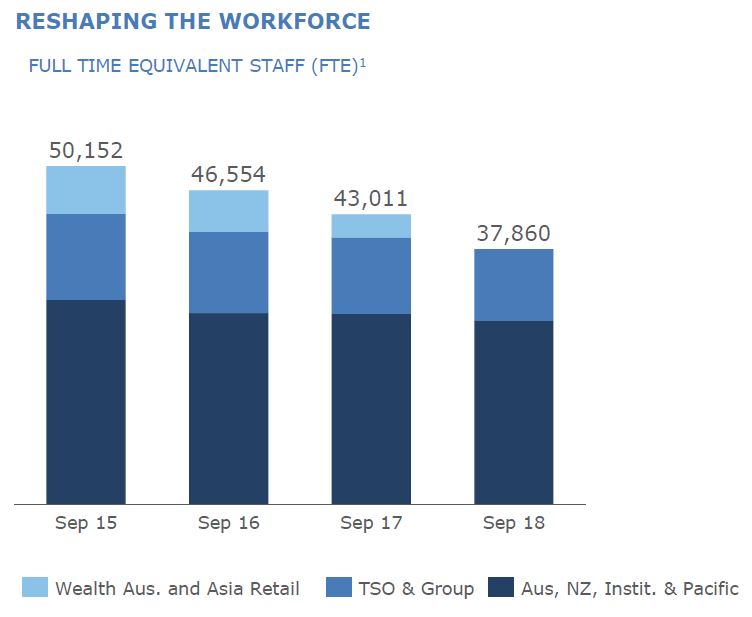

FTE were down by around 700 from the first half.

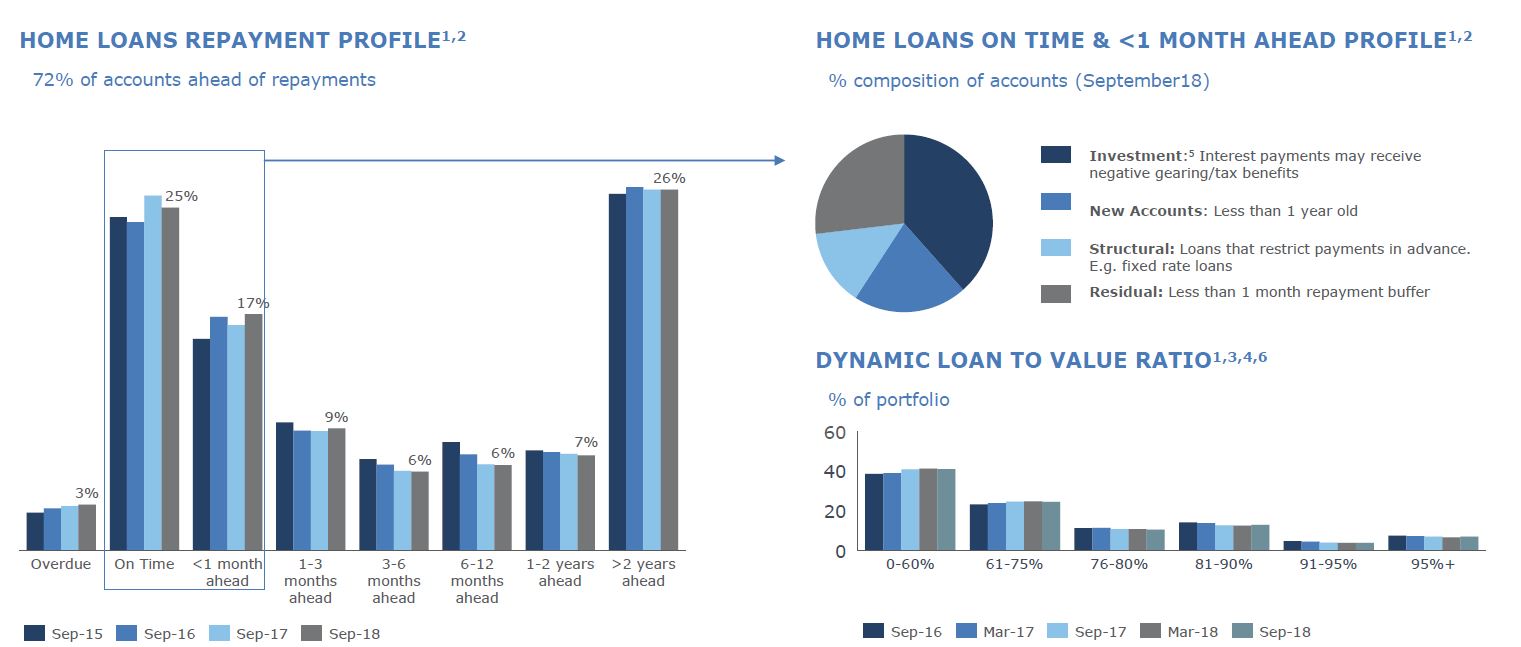

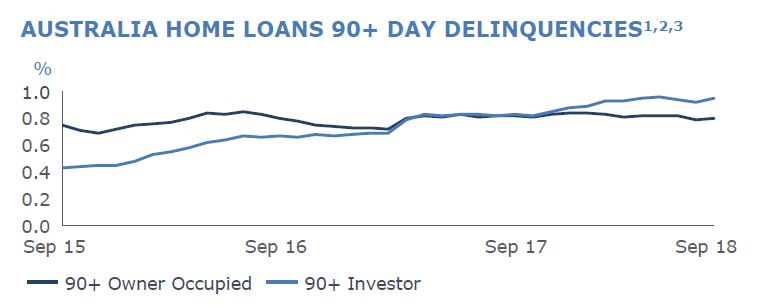

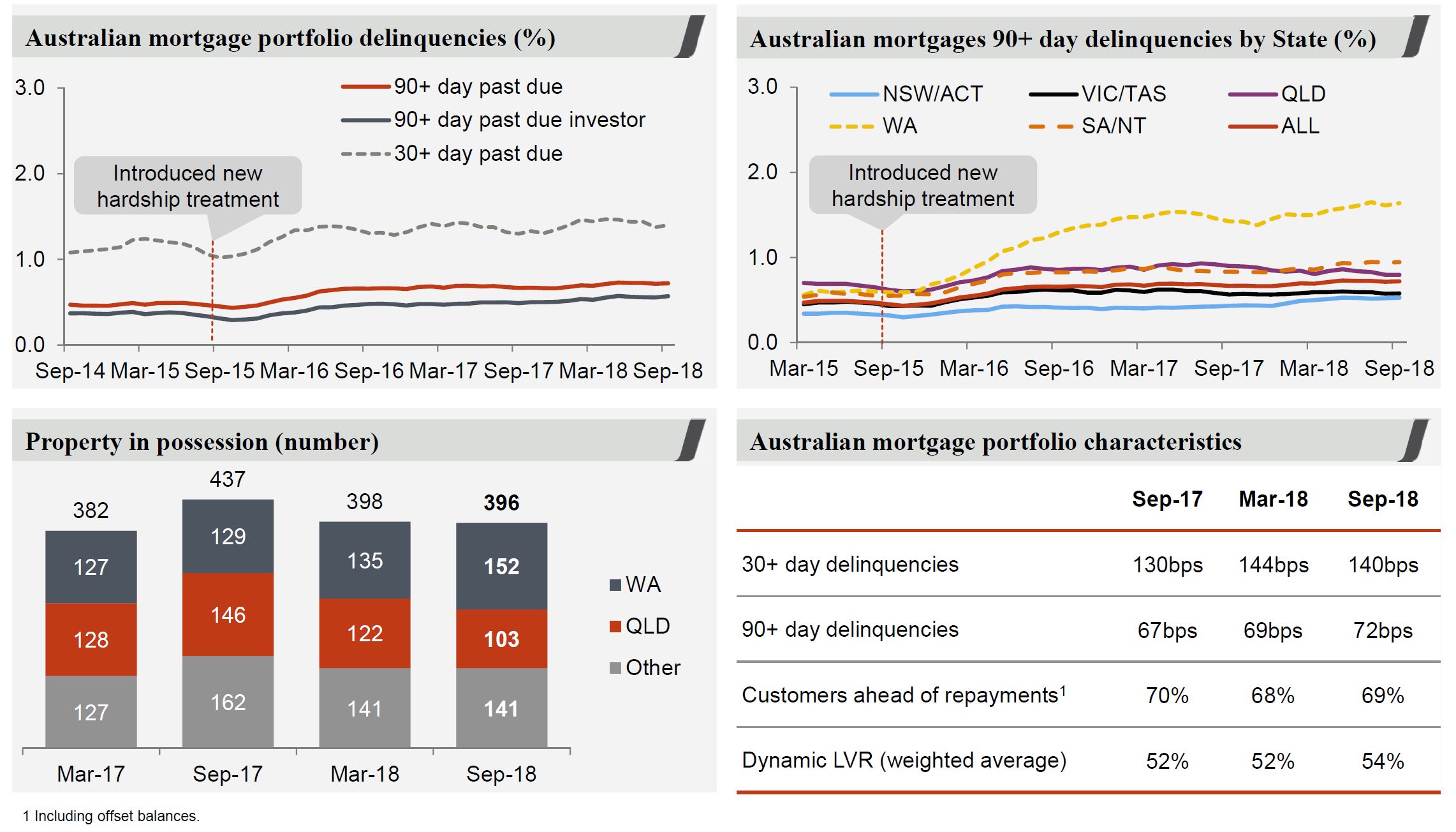

Stressed assets as proportion of total committed exposure (TCE) was lower, despite a rise in 90 days+ past due. Australian 90 day + mortgage delinquencies rose from 69 to 72 basis points in the second half.

Westpac is writing more mortgage loans from NSW and VIC, relative to system and 51.6% of new flows came from propitiatory channels. 8.2% of new loans were from first time buyers. Borrowers applying for a mortgage must be able to service the higher of either: 7.25% minimum assessment rate; or product rate plus 2.25% buffer. Actual mortgage losses are 2 basis points.

The schedule of IO loan expiry reaches out over the next 10 years!

The Australian mortgage book shows a rise in delinquencies, a small fall in those paying ahead, and a rise in dynamic LVR (in response to falling prices). Dynamic LVR is the loan-to-value ratio taking into account the current loan balance, estimated changes in security value, offset account balances and other loan adjustments. WA and SA/NT are most exposed.

Westpac reported their mortgage stress tests which assumes a severe

recession in which significant reductions in consumer spending and business investment lead to six consecutive quarters of negative GDP growth. This results in a material increase in unemployment and nationwide falls in property and other asset prices. They say that estimated Australian housing portfolio losses under these stressed conditions are manageable and within the Group’s risk appetite and capital base.

Cumulative total losses of $3.9bn over three years for the uninsured portfolio (1H18: $3.5bn).

Cumulative claims on LMI, both WLMI and external insurers, of $911m over the three years (1H18: $911m).

Peak loss rate in year 2 has increased to 52bps (1H18: 48bps) due to recent

declines in house prices which leads to a higher dynamic LVR starting point for the portfolio. In addition, the unemployment rate for September of 5.0%

creates a bigger peak to trough change compared to 1H18.

WLMI separately conducts stress testing to test the sufficiency of its capital

position to cover mortgage claims arising from a stressed mortgage

environment.

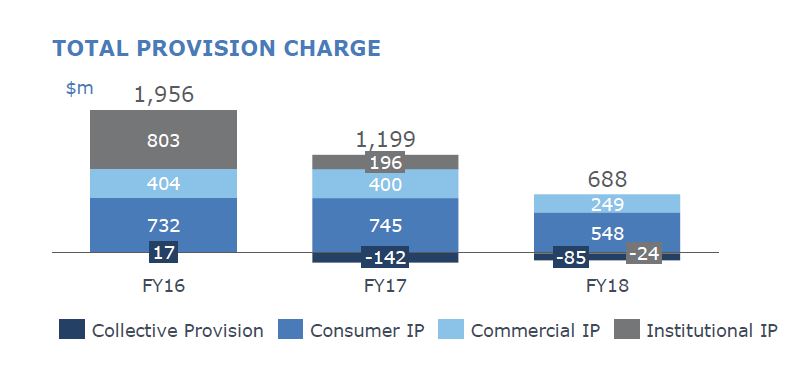

Total impairments were down to $3,053 million (44% of impaired assets).

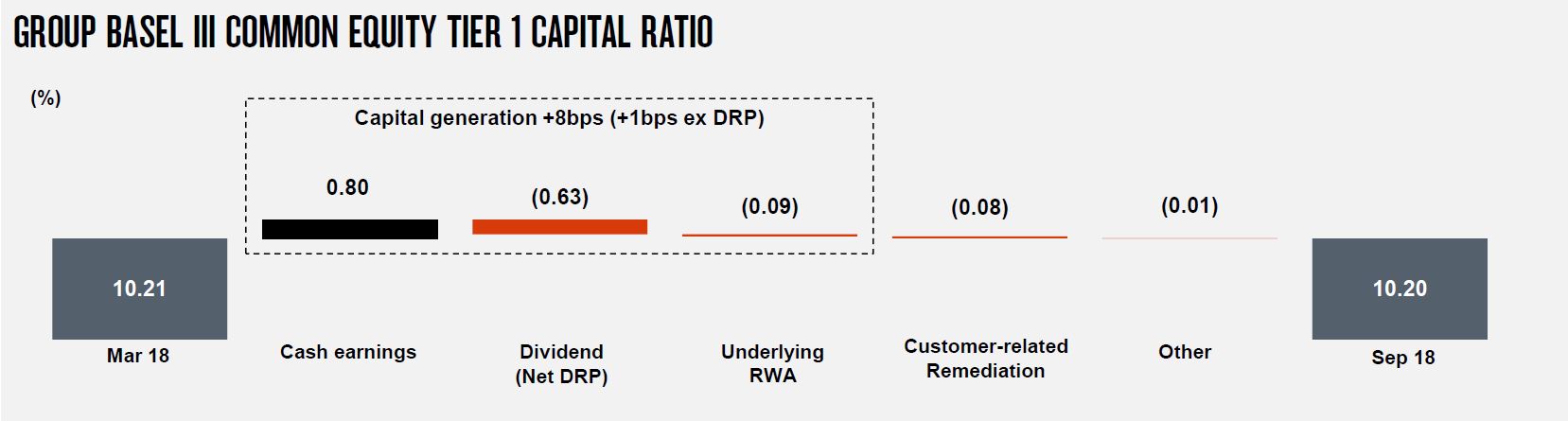

The CET1 ratio was 10.63%, up 13 basis points from March 2018.

Macquarie Group released their 1H19 results today, and continues its strong run, benefiting from its international business portfolio. International income accounted for 67 per cent of the Group’s total income. The Capital Markets business performed strongly.

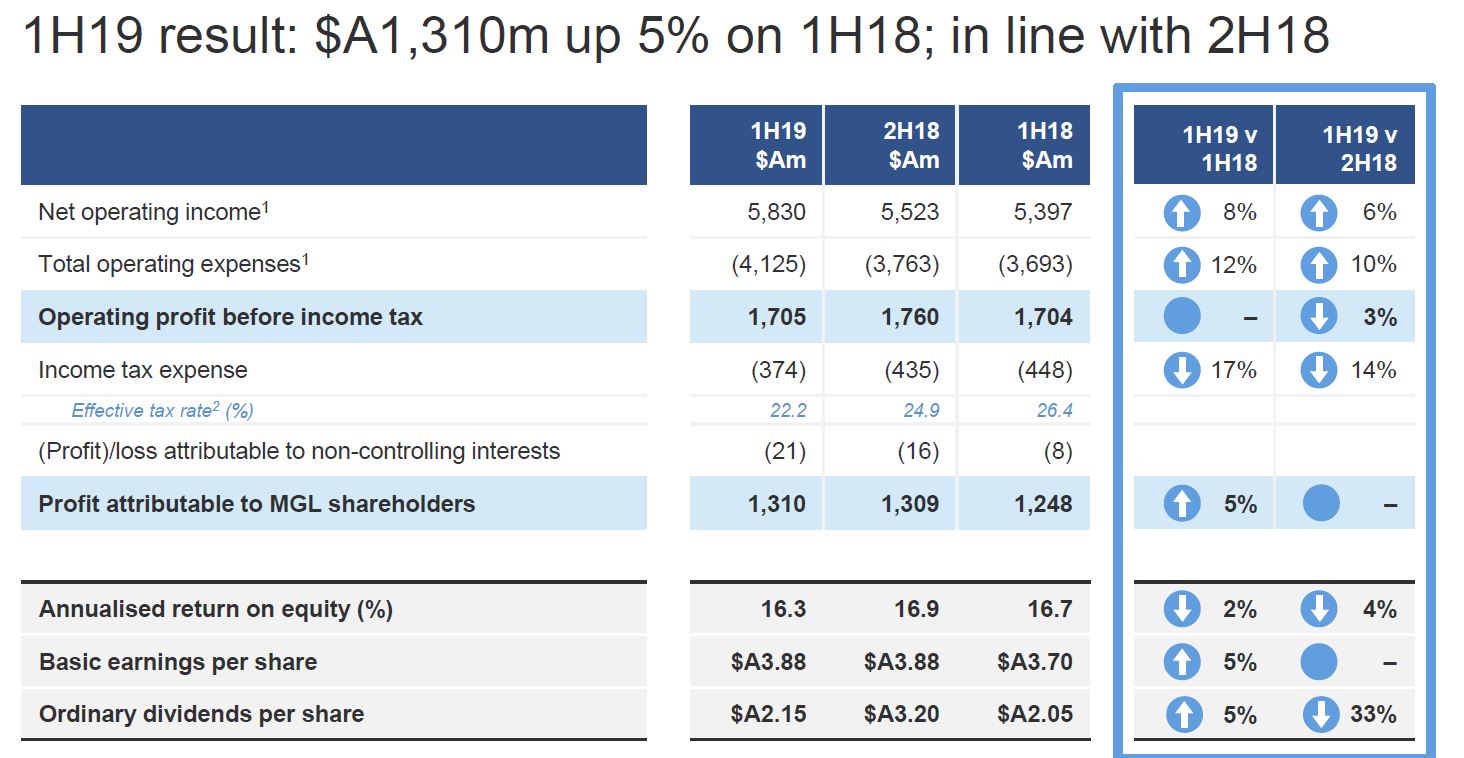

They announced a net profit after tax attributable to ordinary shareholders of $A1,310 million for the half-year ended 30 September 2018 (1H19), up five per cent on the half-year ended 30 September 2017 (1H18) and in line with the half-year ended 31 March 2018 (2H18).

Macquarie’s annuity-style businesses (Macquarie Asset Management (MAM), Corporate and Asset Finance (CAF) and Banking and Financial Services (BFS)), which represented approximately 60 per cent of the Group’s 1H19 performance, generated a combined net profit contribution of $A1,495 million, down 29 per cent on 1H18 and up 10 per cent on 2H18.

Macquarie’s capital markets facing businesses (Commodities and Global Markets (CGM) and Macquarie Capital) delivered a combined net profit contribution of $A1,106 million, up 95 per cent on 1H18 and up six per cent on 2H18.

Net operating income of $A5,830 million in 1H19 was up eight per cent on 1H18 and up six per cent on 2H18, while operating expenses of $A4,125 million were up 12 per cent on 1H18 and up 10 per cent on 2H18.

Macquarie’s assets under management (AUM) at 30 September 2018 were $A551.0 billion, up 11 per cent from $A496.7 billion at 31 March 2018, primarily due to investments made by Macquarie Infrastructure and Real Assets (MIRA) managed funds, foreign exchange impacts, positive market movements and contributions from businesses acquired during the period, namely GLL Real Estate Partners and ValueInvest Asset Management S.A.

Macquarie also announced today a 1H19 interim ordinary dividend of $A2.15 per share (45 per cent franked), up five per cent on the 1H18 interim ordinary dividend of $A2.05 per share (45 per cent franked) and down 33 per cent on the 2H18 final ordinary dividend of $A3.20 per share (45 per cent franked). This represents a payout ratio of 56 per cent. The record date for the final ordinary dividend is 13 November 2018 and the payment date is 18 December 2018.

Half-year result overview Net operating income of $A5,830 million for 1H19 was up eight per cent on 1H18, while total operating expenses of $A4,125 million were up 12 per cent on 1H18.

Key drivers of the change from 1H18 were:

An 18 per cent increase in combined net interest and trading income to $A2,229 million, up from $A1,892 million in 1H18. The movement was mainly due to increased contribution across the commodities platform and growth in deposit and Australian loan portfolios in BFS. This was partially offset by reduced income from early repayments, realisations and the reduction in the size of the CAF Principal Finance portfolio.

A four per cent increase in fee and commission income to $A2,661 million, up from $A2,568 million in 1H18, due to: an increase in brokerage commission in Futures and Cash equity markets from increased market turnover and client activity in Asia; an increase in CGM equity capital markets fee income in the Asia-Pacific; higher fee income from mergers and acquisitions, debt capital markets and equity capital markets in Macquarie Capital; and a $A141 million increase in income offset in operating expenses following the adoption of AASB 15 Revenue from Contracts with Customers on 1 April 2018. This was partially offset by lower performance fees compared to a strong prior corresponding period in MAM.

A two per cent decrease in net operating lease income to $A461 million, down from $A469 million in 1H18, due to a reduction in underlying Aviation income partially offset by improved income from the Energy and Technology portfolios and favourable foreign exchange movements in CAF.

Share of net profits of associates and joint ventures of $A7 million in 1H19 decreased from $A103 million in 1H18, primarily due to losses from associates and joint ventures reflecting expenditure on green energy and other projects in the development phase in Macquarie Capital partially offset by an increase in share of net profits from the sale and revaluation of a number of underlying assets within equity accounted investments in MAM.

Other operating income and charges of $A472 million in 1H19, up 29 per cent from $A365 million in 1H18. The primary drivers were lower credit and other impairment charges compared to 1H18 which recognised impairments relating to legacy assets in Corporate and underperforming financing facilities in CGM; higher investment income primarily due to gains generated across unlisted investments in the green energy and technology sectors in Macquarie Capital; and an increase in other income predominantly relating to asset sales in CAF. This was partially offset by the non-recurrence of gains on reclassification on certain investments in MAM and a UK toll road investment by CAF as well as expenditure in green energy projects in the development phase in Macquarie Capital.

Total operating expenses of $A4,125 million in 1H19 increased 12 per cent from $A3,693 million in 1H18, mainly due to higher average headcount across the Group; unfavourable foreign currency movements, higher project activity in BFS; increased investment in technology platforms in CGM; a $A141 million increase in fee expenses offset in fee and commission income following the adoption of AASB 15 on 1 April 2018; and increased business activity in the majority of operating groups.

Staff numbers were 14,869 at 30 September 2018, up from 14,469 at 31 March 2018.

The income tax expense for 1H19 was $A374 million, a 17 per cent decrease from $A448 million in 1H18. The decrease was mainly due to a reduction in US tax rates and the geographic composition and nature of earnings. The effective tax rate for 1H19 was 22.2%, down from 26.4% in the prior corresponding period and 24.9% in the prior period.

Operating group performance

Macquarie Asset Management delivered a net profit contribution of $A762 million for 1H19, down 36 per cent from $A1,189 million in 1H18. Performance fee income of $A282 million was down from a strong prior corresponding period of $A537 million which included performance fees from MEIF3, Atlas Arteria – ALX (formerly Macquarie Atlas Roads) and other managed funds, Australian managed accounts and co-investors. Base fees of $A884 million were up 11 per cent from $A795 million in 1H18, benefiting from: investments made by MIRA-managed funds; increases in AUM primarily driven by foreign exchange impacts and positive market movements; and contributions from businesses acquired during the period (GLL Real Estate Partners and ValueInvest Asset Management S.A.). This was partially offset by asset realisations by MIRA-managed funds. Investment-related income was lower than the prior corresponding period which included gains on reclassification of certain investments.

Corporate and Asset Finance delivered a net profit contribution of $A437 million for 1H19, down 29 per cent from $A619 million in 1H18. The decrease was mainly driven by reduced income from early repayments, realisations and investment-related income and lower portfolio volumes in Principal Finance. The Asset Finance contribution was broadly in line with 1H18 driven by improved income from the Energy and Technology portfolios offset by lower underlying net operating lease income in Aviation. The remaining portfolios continued to perform well. CAF’s asset and loan portfolios of $A33.7 billion decreased two per cent from 31 March 2018.

Banking and Financial Services delivered a net profit contribution of $A296 million for 1H19, up three per cent from $A286 million in 1H18. The improved result reflects increased income from growth in deposits, the Australian loan portfolio and funds on platform partly offset by the entire period effect of the Australian Government Major Bank Levy relative to the prior corresponding period and increased costs associated with investment in technology projects and headcount in key areas to support business growth. 1H19 also includes expenses associated with bringing together the private bank and private wealth businesses. Total BFS deposits5 of $A49.4 billion increased eight per cent on 31 March 2018 and funds on platform6 of $A88.1 billion increased seven per cent on 31 March 2018. The Australian mortgage portfolio of $A36.1 billion increased 10 per cent on 31 March 2018, representing approximately two per cent of the Australian mortgage market.

Commodities and Global Markets delivered a net profit contribution of $A700 million for 1H19, up 85 per cent from $A378 million in 1H18. The result primarily reflects an increased contribution across the commodities platform driven by: client activity; improved trading opportunities; increased fee and commission income in Asia driven by increased market turnover and client activity; and an increased contribution from equity capital markets fee income in Asia-Pacific. This was partially offset by: reduced opportunities and challenging markets impacting equity trading activities; increased operating expenses reflecting increased client activity; the impact of acquisitions completed in the prior year; and an increase in technology investment.

Macquarie Capital delivered a net profit contribution of $A406 million for 1H19, up 114 per cent from $A190 million in 1H18. The result reflects: higher investment income; higher fee income from both debt and equity capital markets; and higher mergers and acquisitions fee income. During 1H19, Macquarie advised on 228 transactions valued at $A267 billion7 including as joint financial adviser to the Sydney Transport Partners consortium on its acquisition of a 51 per cent interest in WestConnex from the NSW Government for $A9.3 billion; and joint lead manager, bookrunner and underwriter to Transurban Group on its $A4.2 billion entitlement offer, the largest M&A fund raising by an ASX-listed company in the last decade8. During 1H19, Macquarie Capital completed a number of balance sheet transactions including the acquisition and development of a 235MW onshore wind farm (under construction) in central Sweden and raised €270 million of related construction financing. In addition, Macquarie Capital successfully exited its investment in TriTech Software Systems and subsequently acted as financial adviser on its merger with Superion and Aptean and joint bookrunner on the $US1.0 billion related financing.

Total customer deposits9 increased nine per cent to $A52.3 billion at 30 September 2018 from $A48.1 billion at 31 March 2018. During 1H19, $A5.9 billion of new term funding10 was raised covering a range of tenors, currencies and product types.

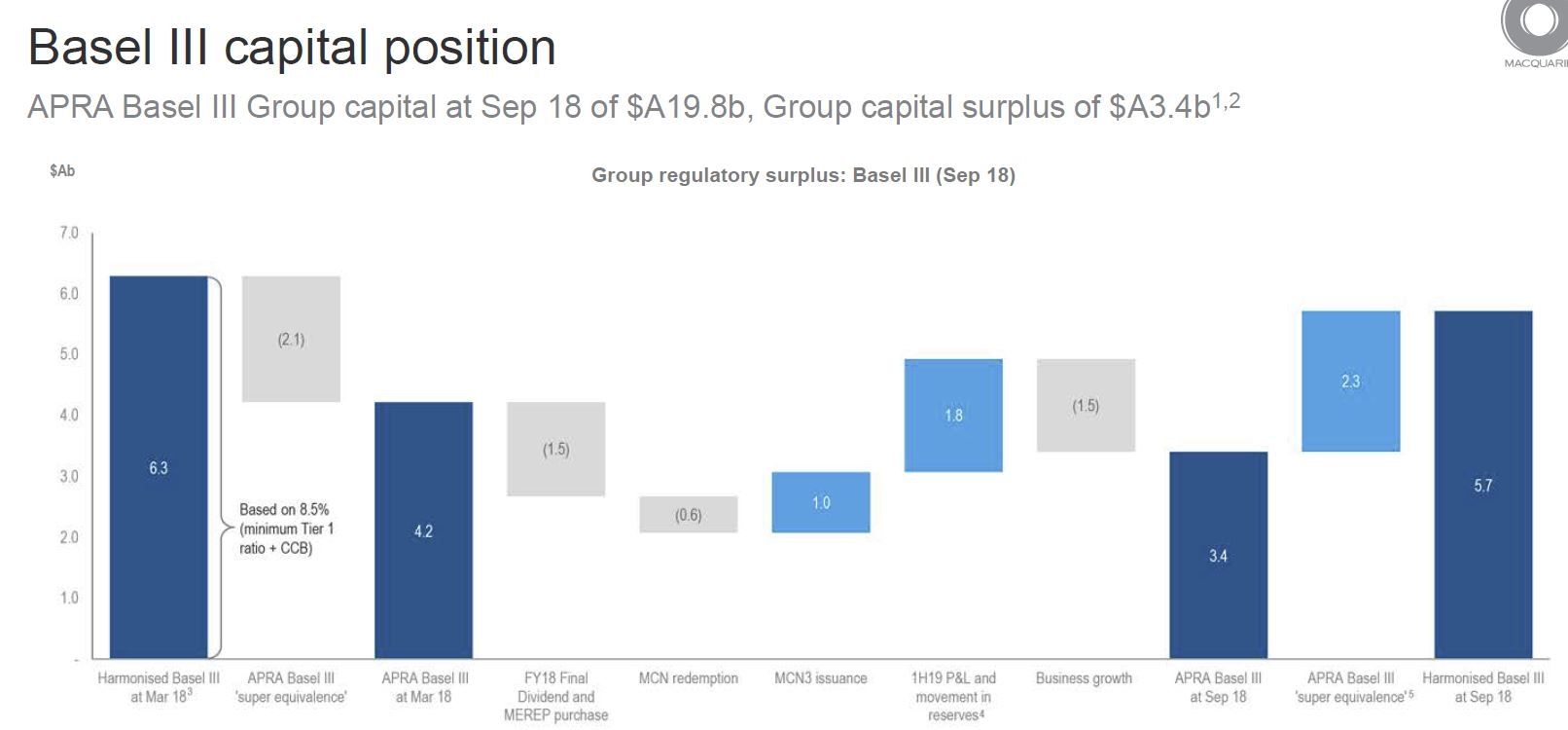

Capital management Macquarie’s financial position comfortably exceeds APRA’s Basel III regulatory requirements, with a Group capital surplus of $A3.4 billion at 30 September 2018. This surplus was down from $A4.2 billion at 31 March 2018, following payment of the FY18 final dividend and FY18 Macquarie Group Employee Retained Equity Plan buying requirement, together with strong business growth of $A1.5 billion, partially offset by 1H19 profit and movement in reserves. The Bank Group APRA Basel III Common Equity Tier 1 capital ratio was 10.4 per cent (Harmonised: 13.0 per cent) at 30 September 2018, down from 11.0 per cent (Harmonised: 13.5 per cent) at 31 March 2018. The Bank Group’s APRA leverage ratio was 5.6 per cent (Harmonised: 6.4 per cent), LCR was 159 per cent and NSFR was 110 per cent at 30 September 2018. No discount will apply for the 1H19 Dividend Reinvestment Plan (DRP) and the shares are to be acquired on-market11.

Regulatory update APRA is yet to release final standards for Australian banks to ensure that their capital levels can be considered ‘unquestionably strong’.

Based on existing guidance, Macquarie’s surplus capital position remains sufficient to accommodate likely additional requirements. In August 2018, APRA released a discussion paper setting out potential options to improve the transparency, international comparability and flexibility of the capital framework. The proposals are not intended to change the amount of capital that ADIs are required to hold13. In addition, APRA released a discussion paper on their implementation of a minimum requirement for the leverage ratio of four per cent from July 201914. MBL’s leverage ratio is 5.6 per cent as at September 2018.

Share buyback Given significant business growth in 1H19, Macquarie did not purchase any shares under the share buyback program announced at the 1H18 result announcement. There is currently no prospect of buying any shares under the share buyback program and so the program has ended.

While the impact of future market conditions makes forecasting difficult, the Group currently expects the FY19 result to be up approximately 10 per cent on FY18.

National Australia Bank (NAB) released their full year 2018 results today. They may have saved the day by reducing their markets business, and provisions are low (too low?), but the business does appear to be under pressure. Net interest margin in down, despite reducing returns to depositors, and funding pressure remains, to say nothing of the “unknown unknowns” from the Royal Commission.

That said, initial reactions from analysts seem positive (no surprises) and the market went higher.

Cash earnings were $5,702m down 14% on FY17. They included restructuring costs of $530m and customer related remediation of $261m, leading to a cash earnings figure before these of $6,493m down 2.2% on FY17.

The earnings per share was 202.4 cps, down 16%, and the Cash ROE was down 230 basis points to 11.7%.

Statutory profit was $5,554m, up 5%, and the CET1 ratio was 10.2% up 14 basis points.

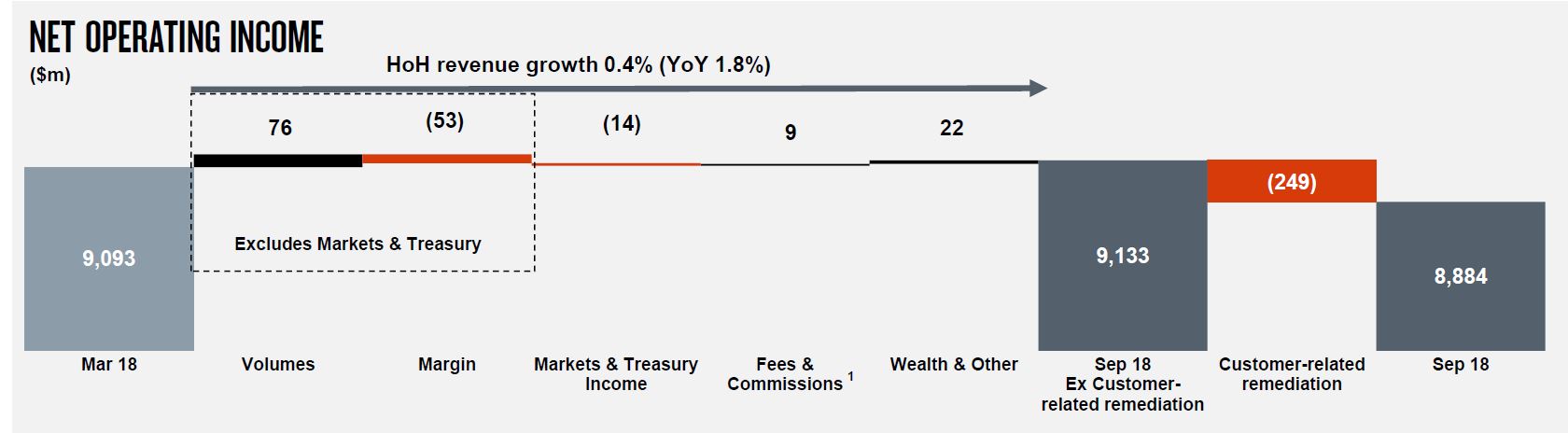

The net operating income rose by 0.4% in the second half of 2018, from $8,884m to $9,093m after allowing fro the customer remediation costs. Volume was up (excluding markets) but margin was down.

The net interest margin fell 4 basis points from 1.88% in 2017 to 1.84% in 2018. This included 2 basis point falls in lending margin, and liquidity/funding plus 2 basis points from markets, offset by clawing back margin from depositors of 2 basis points.

Group Markets and Treasury Income declined.

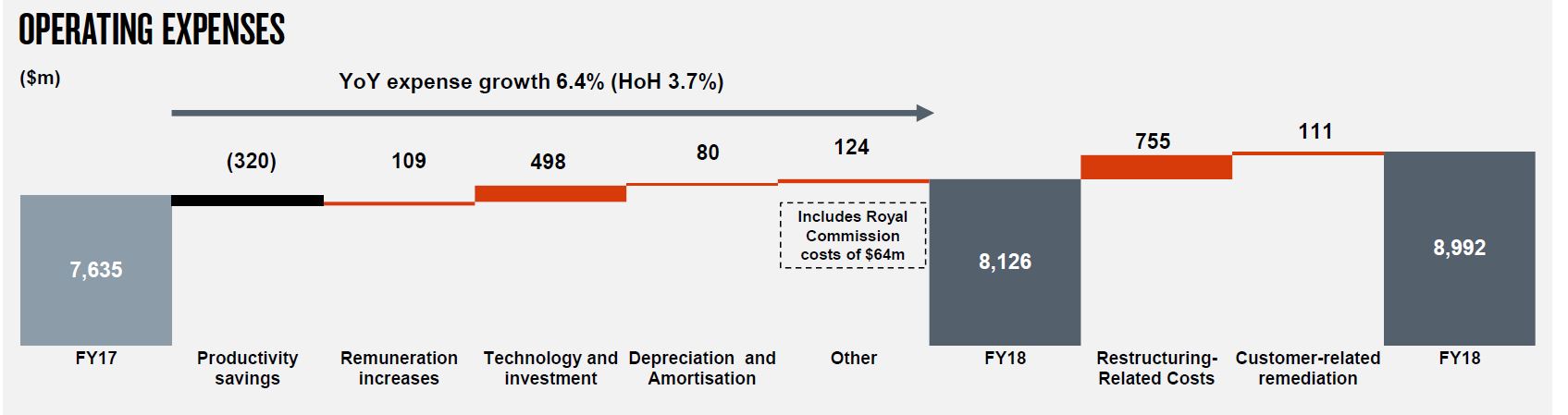

There was a significant rise in operating expenses from $7,635m last year t0 $8,992m in 2018, which were helped by $320m productive savings, but hit by technology investments of $498m and restructuring costs of $755m plus costs relating to customer remediation and Royal Commission. 70 Retail outlets were closed.

Total customer remediation costs were $360m split between revenue ($249m) and expenses ($111m). These included refunds and compensation in NAB’s Wealth business, including adviser service fees, plan service fees, the Wealth advice review and other Wealth related issues; Costs for implementing remediation processes and other charges associated with regulatory compliance investigations.

Of the ~6,000 FTE cut targetted by 2020, 1,897 were made, and of the ~2,000 upskilling, 195 were added. Total FTE in the group was 33,283 compared with 33,422 in 2017.

Looking at the home lending business in Australia, housing revenue has fallen, though with a small rise in interest only loan interest income.

Loan balances grew a little from $295.1 billion in 2017 to $303.1 billion in 2018, and grew at around system to give a 15.4% market share. The net interest margin has fallen from 1.38% in 2017 to 1.22% in 2018.

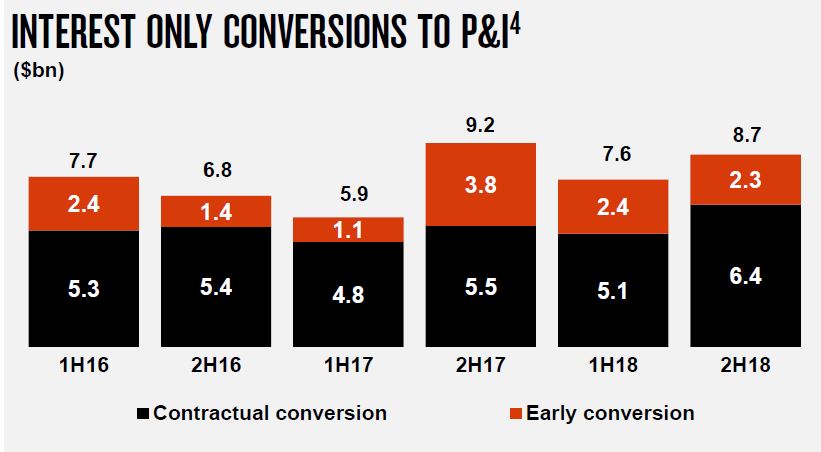

Interest only conversions to P&I loans are running at ~$8 billion per half, with more driven by contractual conversions.

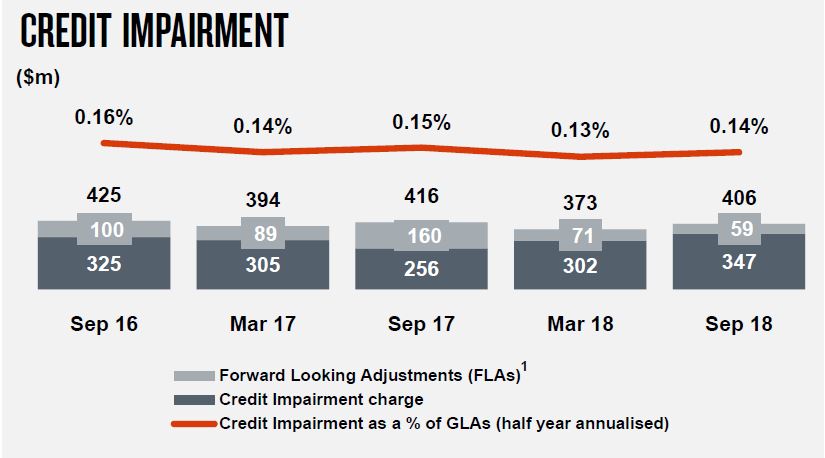

Credit impairments rose to $403 million, or 0.14% of GLA.

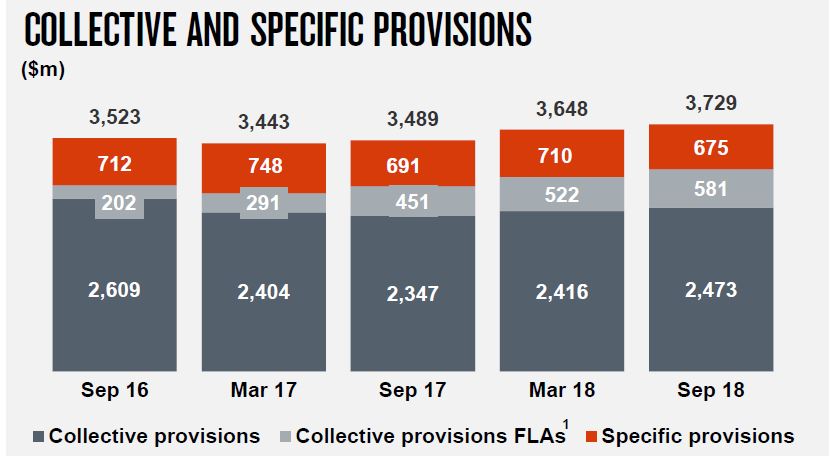

The specific provisions were $3,729m, higher than a year ago.

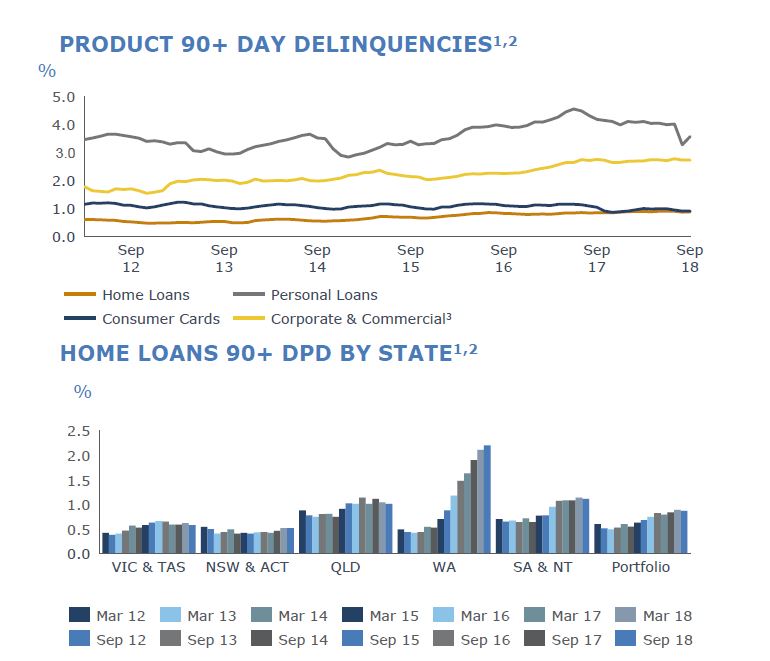

Looking at the Australian Housing Lending, we see a rising default trend, with WA leading the way.

They increased their collective provisions from $270m in 2017 to $515m in 2018, which is 0.17% of GLA.

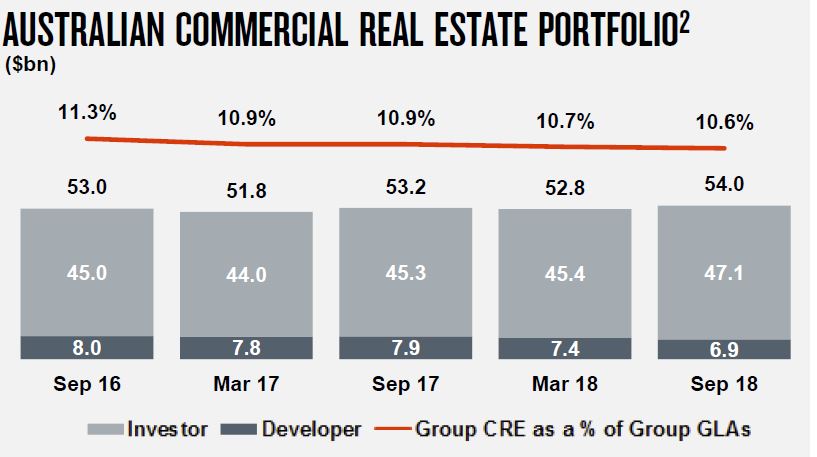

NAB has $54bn Australian Commercial Real Estate drawn balance, of which 13% is Developer. They have imposed tighter lending restrictions (introduced cap on foreign buyer pre-sales, reduced maximum loan to cost ratio by ~10% and increased minimum pre-sales requirement).

They say exposure under construction limits are down 20% since

September 2016, Greater Brisbane and Greater Perth limits

down >50%1, >90% of limits amortise within 2 years and that higher risk inner city postcodes account for ~18% of total residential developer exposure.

The CET1 ratio fell to 10.20% in Sept 2018. They say they are on track to achieve 10.5% CET1 ratio benchmark “in an orderly manner by 1 January 2020”.

However, the total APRA capital ratio has fallen.

The LCR is reported at 129%

The Net Stable Funding Ratio was 113%

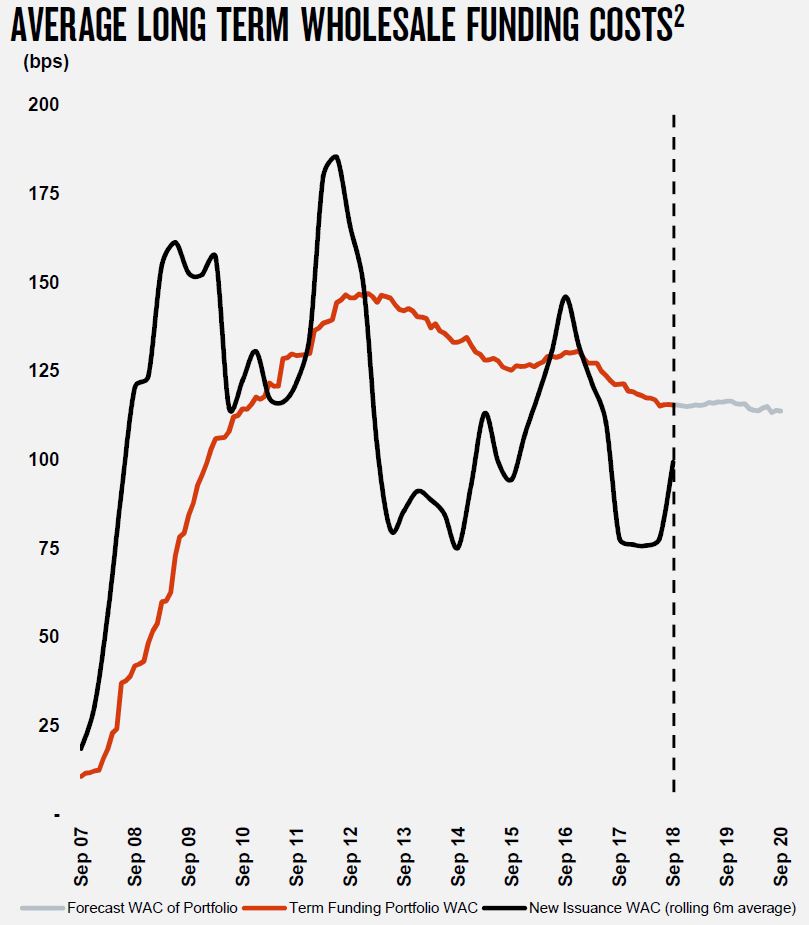

The costs of new long funding are rising, although the portfolio costs overall are not. But the benefits of cheaper funding is passing, so putting more pressure on margins ahead.

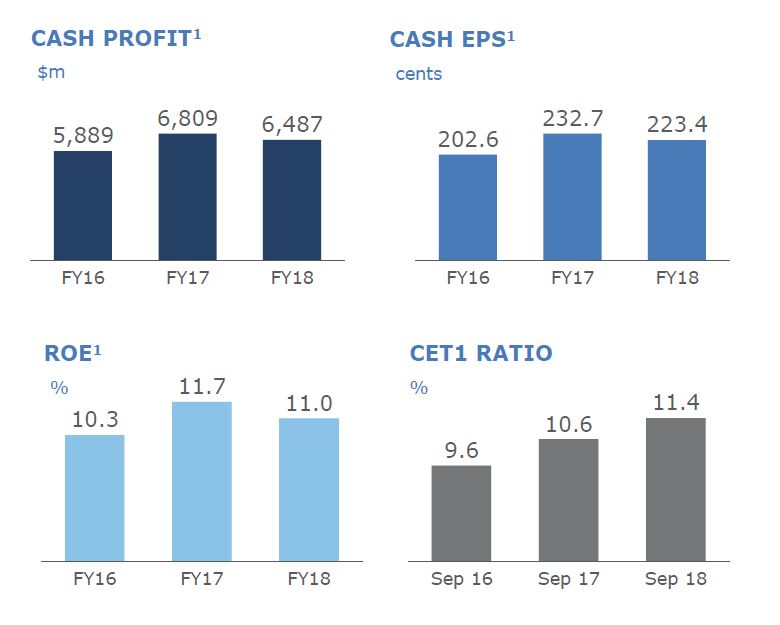

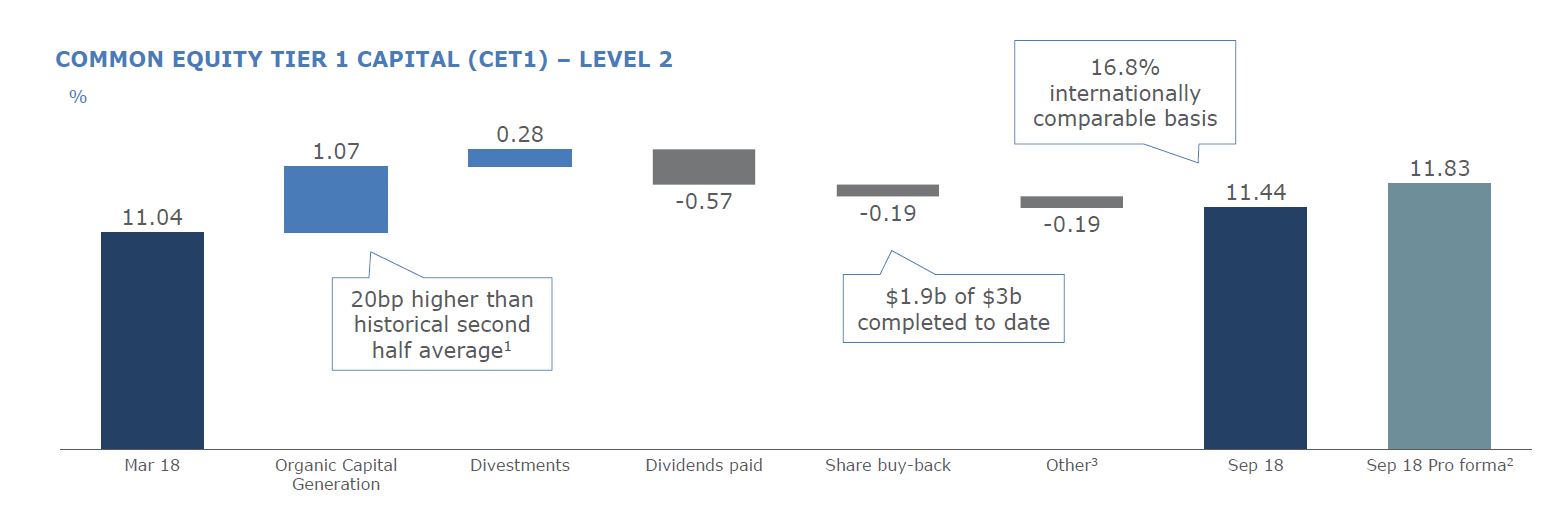

ANZ today announced a Statutory Profit after tax for the Full Year ended 30 September 2018 of $6.40 billion, flat on the comparable period and a Cash Profit on a continuing basis of $6.49 billion, down 5%. Their approach to simplify the business and reduce costs have bolstered their capital position, but also left them potentially more exposed to a mortgage and construction sector downturn.

ANZ’s Common Equity Tier 1 Capital Ratio was 11.4% up 87 basis points (bps). Return on Equity decreased 67 bps to 11.0% with Cash Earnings per Share down 4% to 223.4 cents (continuing). The Final Dividend is 80 cents per share, fully franked, bringing the Full Year Dividend to 160 cents.

They called out the headwinds facing Retail banking thanks to housing growth slowing, and borrowing capacity reduced. They said they had sacrificed sort-term revenue growth and high margins in Australia, particularly in the investor and interest-only segments. New Zealand performed well. The risk adjusted performance for Australia FELL in the second half, as the impact of the tighter mortgage sector hit home.

Net Interest Margin was significantly lower, thanks to the change in business mix, funding and customer remediation charges.

The results were supported by the $3 billion share buy-back and the neutralisation of the full year dividend reinvestment plan. They reduced variable remuneration paid to staff this year across the bank by $124 million and are undertaking the urgent work required to fix the failures that have been highlighted by the Royal Commission.

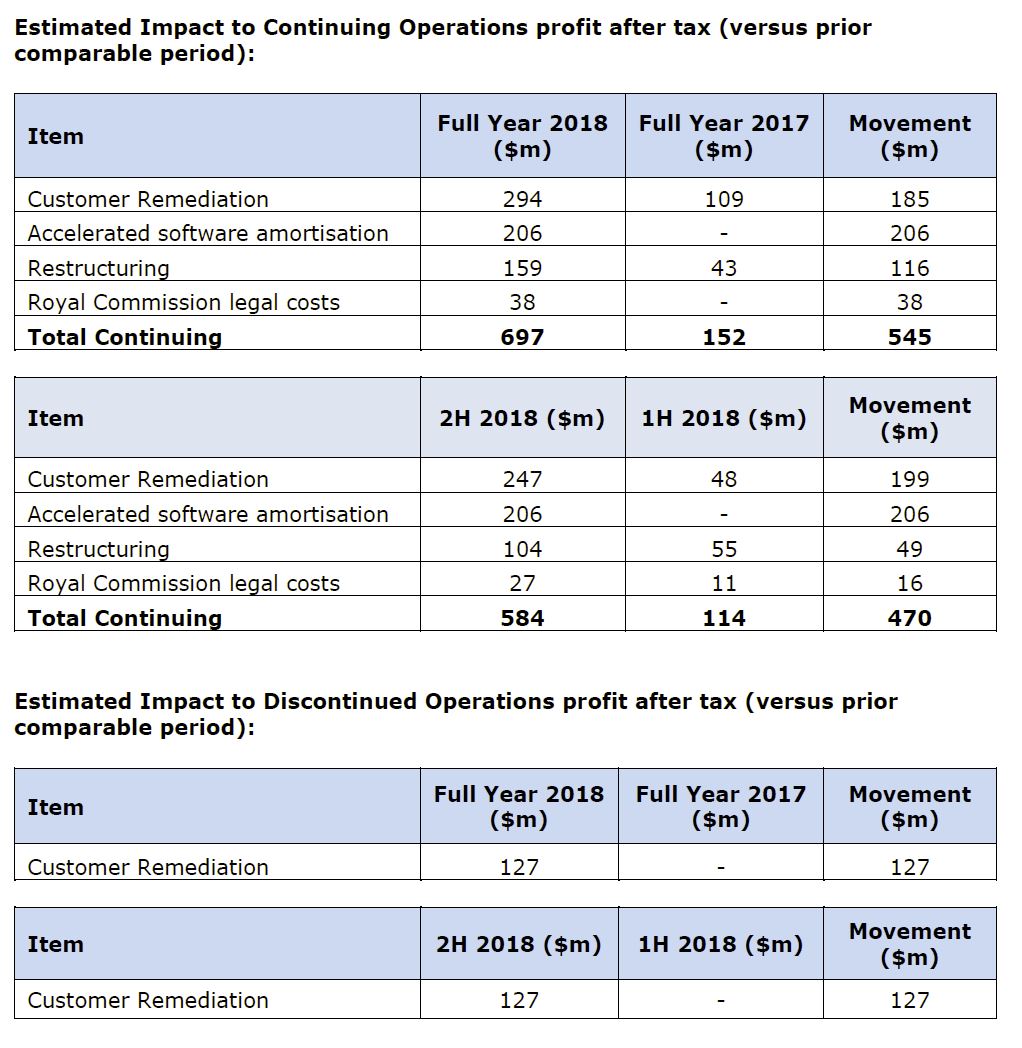

ANZ announced earlier this month charges of $377 million after tax have been recognised in 2H18 for refunds to customers and related remediation costs. ANZ also recorded accelerated amortisation expense of $206 million in 2H18, predominantly relating to its International business. A restructuring charge of $104 million, largely relating to the previously announced move of the Australia and Technology Divisions to agile ways of working, was also recorded in 2H18.

Staff numbers have fallen significantly from 50,152 in 2015 to 37,860 in 2018.

As a result, costs were lower, despite significant technology investments.

The total provision charge for the year was $688 million down 43%.

Looking at the Australian Home Lending portfolio, they say 72% of households are ahead on repayments. They hold more loans above 95% than 90% in their portfolio.

Australian Home Loan 90+ Delinquencies were higher, especially investor loans, rising from 0.84% in September 2017 to 0.86% in September 2018.

WA continues to show more 90+ delinquency, and WA is 13% of funds under management, but 33% of 90+ and over half of portfolio losses. This shows the long slow drag on performance from a slowing economy.

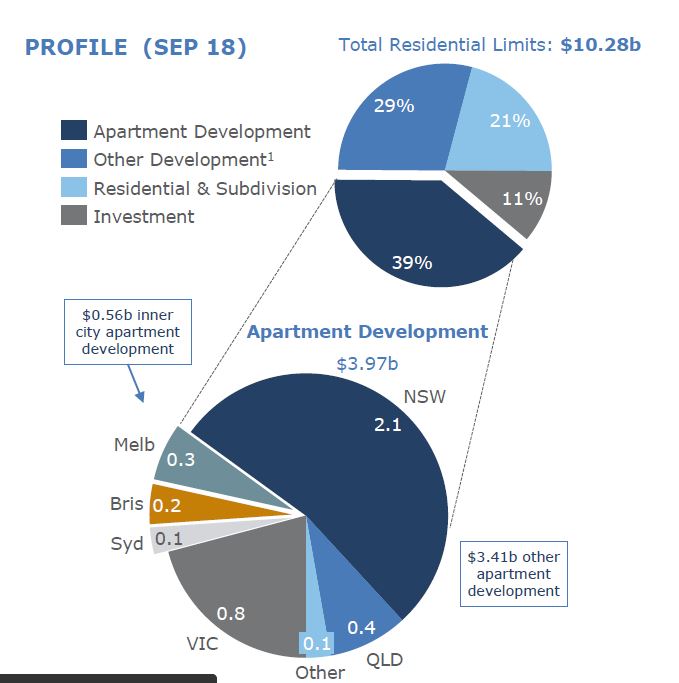

They also increased their exposure to commercial property, with apartment development limits up 17% to ~$4 billion, which accounts for ~39% of total residential limits. Inner City apartment limits totalled $0.56 billion and was 14% of the total apartment development limit in FY18, down from 20% in the prior year. This was thanks to developments in Sydney and Melbourne being repaid. They have highest exposure in NSW.

The Group Loss rate reduced to 12 bps with the second half loss rate 9 bps. New Impaired assets declined just over $1.1 billion or 34% with Gross Impaired Assets down 16%. The significant decline in the Group loss rate reflects portfolio credit quality improvement driven by strategic changes to the composition of the asset book, such as the sale of retail and commercial in Asia, together with tighter lending standards and a relatively benign credit environment.

The APRA CET1 capital ratio at 30 September 2018 was 11.4% (16.8% on an Internationally Comparable basis). This places ANZ well above the APRA prescribed ‘unquestionably strong’ threshold, comfortably ahead of the 2020 deadline.

Completed assets sales during the year increased the CET1 position by ~84bps. They commenced an on market share buyback in January 2018 and was increased to $3 billion in June 2018. As at 30 September $1.9bn of this had been completed, representing ~2% of ANZ shares outstanding. They expect the remaining ~$1.1bn to be completed during 1H19.

The Group’s funding and liquidity position remained strong with the Liquidity Coverage Ratio at 138% and Net Stable Funding Ratio at 115%. Other asset sales already announced will provide further flexibility.

AMP Limited has announced the successful completion of its portfolio review including an agreement to divest its Australian and New Zealand wealth protection and mature businesses (AMP Life) and reinsure New Zealand retail wealth protection for total proceeds of A$3.45 billion.

The stock dropped (in a down day) to a new low.

AMP will exit its Australian and New Zealand wealth protection and mature businesses via a sale to Resolution Life1 for total cash and non-cash consideration of A$3.3 billion; transaction expected to complete in 2H 2019; subject to regulatory approvals.

Binding agreement with Swiss Re2 to reinsure New Zealand retail wealth protection, releasing additional capital of up to A$150 million to AMP prior to completion of sale; subject to regulatory approvals.

Intention to seek divestment of New Zealand wealth management and advice businesses via initial public offering (IPO) in 2019 subject to market conditions and regulatory approvals, unlocking further value.

Significant capital release will strengthen AMP’s balance sheet and provide strategic flexibility; all options for use of proceeds to be evaluated and update to be provided following transaction completion.

Wealth protection and mature – Resolution Life transaction summary

Under the terms of today’s agreement, AMP will sell its Australian and New Zealand wealth protection and mature businesses (AMP Life) to Resolution Life for a total consideration of A$3.3 billion, which comprises:

A$1.9 billion in cash.

A$300 million in AT1 preference shares in AMP Life (issued on transaction completion).

A$1.1 billion in non-cash consideration:

o Economic interest in future earnings from the mature business, equivalent to A$600 million; expected to provide steady ongoing earnings to AMP of approximately A$50 million after tax per annum, assuming an annual run-off at 5 per cent.

o A$515 million interest in Resolution Life, focused on the acquisition and management of in-force life insurance books globally.

AMP expects to monetise all non-cash consideration over time.

Together with the New Zealand reinsurance agreement, the total value equates to approximately 0.82x pro forma embedded value of the sold businesses at 30 June 2018, excluding franking credits.

Resolution Life assumes risk and profits of the wealth protection and mature businesses from 1 July 20183, subject to Australian wealth protection risk-sharing arrangements.

A new relationship Agreement has been established with Resolution Life and AMP Capital will continue to manage wealth protection and mature assets under management. AMP Capital will also join Resolution Life’s global panel of preferred asset managers.

The transaction is subject to regulatory approvals and other conditions precedent and is expected to complete in 2H 2019.

Partnering to ensure smooth transition for customers

Resolution Life is an international insurance and reinsurance group whose management has a 15-year track record in providing quality service to in-force insurance customers.

The transaction has been designed to ensure all existing terms and conditions will be retained. The teams supporting existing AMP customers will largely transfer on completion to maintain continuity of service.

AMP and Resolution Life will work closely together to ensure a smooth transition for customers.

New Zealand wealth protection reinsurance

AMP has entered into a binding reinsurance agreement with Swiss Re for the New Zealand retail wealth protection portfolio which is expected to release up to A$150 million of capital to AMP, subject to regulatory approval. The agreement is expected to be effective from 31 December 2018, and will cover approximately 65 per cent of the New Zealand retail wealth protection portfolio for new claims incurred from that date.

The reinsurance agreement is expected to reduce New Zealand profit margins by A$20 million on a full-year basis. The reinsurance outcomes are factored into the Resolution Life transaction.

New Zealand wealth management and advice businesses

AMP is today also announcing its intention to seek divestment of its New Zealand wealth management and advice businesses via an IPO in 2019. The decision to proceed with an IPO and its timing remain subject to market conditions and regulatory approvals.

These businesses have FY18 pro forma operating earnings of approximately A$40 million on a standalone basis. The IPO would release capital to AMP and create a standalone New Zealand wealth management and advice business.4

Portfolio review outcomes will release capital, simplify portfolio and create strategic flexibility

The completion of the portfolio review will strengthen AMP’s balance sheet and provide strategic flexibility. All options for use of proceeds will be considered including growth investments and/or capital management activity.

The exit from Australian and New Zealand wealth protection and mature will also significantly simplify AMP and its earnings profile, enabling it to focus on its higher growth businesses of Australian wealth management, AMP Capital and AMP Bank.

The simplification and separation costs related to the Resolution Life sale transaction are expected to be in the order of A$320 million post-tax.

Additional capital from the transaction with Resolution Life will facilitate a reduction in AMP’s corporate debt of up to A$800 million.

The financial impacts of the transaction on AMP post-separation are outlined in the investor presentation.

AMP will exclude the 2H 18 earnings from the discontinued businesses in determining the FY 18 dividend. AMP continues to target a total FY 18 dividend payout within, but towards the lower end of its dividend guidance range of between 70 – 90 per cent of underlying profit.

Further guidance on use of proceeds will be provided following the completion of the transaction in 2H 2019.

More putting the trash out, before the results season.

NAB announced today additional costs of $314 million after tax in connection with its customer remediation programme. This will reduce 2H18 cash earnings by an estimated $261 million and earnings from discontinued operations by an estimated $53 million.

These matters include:

refunds and compensation to customers impacted by the issues in NAB’s Wealth business, including advisor service fees, plan service fees, the Wealth advice review and other Wealth related issues

costs for implementing remediation processes

other costs associated with regulatory compliance matters

Of the cash earnings impact, approximately 69% of these costs will impact revenue, with the balance reported in expenses.

As outlined in the third quarter trading update, these additional costs will be excluded from the FY18 expense growth guidance of 5-8%. Costs associated with responding to the Royal Commission are not included in these additional charges.

NAB says it remains well positioned to meet APRA’s ‘unquestionably strong’ benchmark in an orderly manner by January 2020.

But they also said that these customer remediation programs are expected to continue into FY19, with potential for further costs, which remain uncertain at this point in time.

Further detail will be provided when NAB releases its 2018 Full Year results on 1 November 2018.

Welcome to the Property Imperative weekly to 13th October 2018, our digest of the latest finance and property news with a distinctively Australian flavour.

This week saw major ructions on the financial markets, which may be just a short-term issue, or a signal of more disruption ahead. And locally, the latest data reveals a slowing of lending to first time buyers and owner occupied borrowers, suggesting more home price weakness ahead. So let’s get stuck in.

Watch the video, listen to the podcast, or read the transcript.

And by the way you value the content we produce please do consider joining our Patreon programme, where you can support our ability to continue to make great content.

Let’s look at property first.

The IMF’s latest Global Financial Stability Report (FSR) says Australia is one of a number of advanced economies where rising home prices are a risk. “household leverage stands out as a key area of concern, with the ratio of household debt to GDP on an upward trajectory in a number of countries, especially those that have experienced increases in house prices (notably, Australia, Canada, and the Nordic countries). Housing market valuations are relatively high in several advanced economies. Valuations based on the price-to-income and price-to-rent ratios, as well as mortgage costs, have been on the upswing over the past six years across major advanced economies, with valuations relatively high in Australia, Canada, and the Nordic countries.

And they also warn that the effect of monetary policy tightening (lifting interest rates to more normal levels) – could reveal financial vulnerabilities. Indeed, it’s worth looking at expected central bank policy rates globally. Bloomberg has mapped the relative likelihood of increases and decreases across a number of major economies, and most advanced economies are on their way up. Worth thinking about when we look at the long term home prices trends across the globe. Guess where Australia sits? High debt, in a rising interest rate environment is not a good look, so expect more stress in the system.

Yet the latest RBA Financial Stability review, out last Friday seems, well, in a different world. They go out of their way to downplay the risks in the system, and claim that households are doing just fine, based on analysis driven by the rather old HILDA data – again.

But back in the real world, Corelogic’s auction results for last week returned an aggregated clearance rate of 49.5% an improvement on the week prior at 45.8 per cent of homes sold, which was the lowest weighted average result since 42 per cent in June 2012. There was a significantly higher volume of auctions with 1,817 held, rising from the 895 over the week prior.

Melbourne’s final clearance rate fell last week, to 51.8 per cent the lowest seen since 50.6 per cent in December 2012. There were 904 homes taken to auction across the city. Compared to one year ago, the Melbourne auction market was performing very differently, with both volumes and clearance rates significantly higher over the same week (1,119 auctions, 70.3 per cent).

Sydney’s final auction clearance rate increased last week, with 46.1 per cent of the 611 auctions held clearing, up from the 43.8 per cent the week prior when a similar volume of auctions was held. One year ago, Sydney’s clearance rate was 61.3 per cent across 818 auctions.

Across the smaller auction markets, Canberra returned the strongest final clearance rate of 64.6 per cent last week, followed by Adelaide where 62.3 per cent of homes sold, while only 11.1 per cent of Perth homes sold last week.

Looking at the non-capital city regions, the Geelong region was the most successful in terms of clearance rates with 48.5 per cent of the 41 auctions recording a successful result.

This week, CoreLogic is tracking 1,725 auctions across the combined capital cities, which is slightly lower than last week. Compared to one year ago, volumes are down over 30 per cent (2,525).

They also highlighted the growing settlement risk relating to off the plan high-rise sales. Prospective buyers may sign a contract to purchase from the plan, but when the unit is ready – perhaps a year or two later, a bank mortgage valuation may not cover the purchase price. Meaning the buyer may be unable to complete the transaction. CoreLogic says that in Sydney, 30% of off-the-plan unit valuations were lower than the contract price at the time of settlement in September, double the percentage from a year ago. In Melbourne, 28% of off-the-plan unit settlements received a valuation lower than the contract price. In Brisbane, where unit values remain 10.5% below their 2008 peak, the proportion was substantially higher, at 48%. And they also argue that loss making resales are rising, especially in the unit sector, although it does vary by location.

The latest housing finance figures from the ABS showed that lending flows for owner occupied buyers appear to be following the lead from the investment sector. Both were down. This is consistent with our household surveys. Looking at the original first time buyer data, the number of new loans fell from 9,614 in July to 9,534 in August, a fall by 80, or 0.8%. As a proportion of all loans written in the month, the share by first time buyers fell from 18% to 17.8%.

Looking at the trend lending flows, the only segment of the market which was higher was a small rise in refinanced owner occupied loans. These existing loans accounted for 20.5% of all loans written, up from 20.3%, and we see a rising trend since June 2017, from a low of 17.9%. Total lending was $6.3 billion dollars, up $31 million from last month. Investment loan flows fell 1.2% from last month accounting for $10 billion, down 120 million. Owner occupied loans fell 0.6% in trend terms, down $81 million to $14.5 billion. 41% of loans, excluding refinanced loans were for investment purposes, the lowest for year, from a high of 53% in January 2015.

On these trends, remembering that credit growth begats home price growth, the reverse is also true. Prices will fall further, the question remains how fast and how far? We will be revising our scenarios shortly.

The latest weekly indices from CoreLogic shows price falls in Sydney, down 0.16%, Melbourne down 0.18%, Brisbane down 0.08%, Adelaide down 0.09% and Perth down 0.38% giving a 5 cities average of down 0.18%.

Morgan Stanley revised their house prices forecasts, down. They say “We struggle to see improvement in any of our components over the next year. We now see a 10-15 per cent peak to trough decline in real house prices (from 5-10 per cent), which would mark the largest decline since the early 1980s. With households 2x more leveraged to housing than back then, the impact on housing equity would be larger again. This downgrade largely reflects the downturn’s extended length, as we expect the relatively orderly declines to date will continue. However, an acceleration of declines is in our bear case, and we will continue to monitor stress points, including arrears trends. Strong employment growth and temporary migration has helped contain reported vacancy rates thus far, but we see a sustained overbuild into 2019 weighing on rentals”.

NABs latest quarterly property survey index fell sharply in Q3, to the lowest level in 7 years, Sentiment was dragged lower by big falls in NSW and VIC. NAB’s view is the orderly correction in house prices will continue over the next 18-24 months with Sydney falling around 10% peak to trough and Melbourne 8%. This reflects a bigger fall than previously expected but would still leave house prices well up on 2012 levels. Their central scenario does not include a credit crunch event leading to disorderly falls in house prices. They also say the boom in Australian real estate sales to foreign investors has run its course, with NAB’s latest survey results continuing to highlight a decline in foreign buying activity resulting from policy changes in China on foreign investment outflows and tighter restrictions on foreign property buyers in Australia. In Q3, there were fewer foreign buyers in the market for Australian property, with their market share falling to a 7-year low of 8.1% in new housing markets and a survey low 4.1% in established housing markets.

Expect the calls for an increase in migration, and a freeing of lending standards to reach fever pitch – both of which MUST be ignored. We have to get back to more realistic home price ratios, despite the pain. So it was interesting to note that the NSW State Government this week, suggested that migration needed to slow, to provide breathing space, and for infrastructure to catch up. Better late than never. Remember the 2016 Census revealed that Australia’s population increased by 1.9 million people (+8.8%) in the five years to 2016, driven by a 1.3 million increase in people born overseas (i.e. new migrants)!

We published our latest household survey data this week. Mortgage stress rose again, to cross the one million households for the first time ever. We discussed the results in full in our post “Mortgage Stress Breaks One Million Households” The latest RBA data on household debt to income to June reached a new high of 190.5. This high debt level helps to explain the fact that mortgage stress continues to rise. Across Australia, more than 1,003,000 households are estimated to be now in mortgage stress (last month 996,000). This equates to 30.6% of owner occupied borrowing households. In addition, more than 22,000 of these are in severe stress. We estimate that more than 61,000 households risk 30-day default in the next 12 months. We continue to see the impact of flat wages growth, rising living costs and higher real mortgage rates. Bank losses are likely to rise a little ahead.

Moodys released a report suggesting that Mortgage delinquencies and defaults are more likely to occur in outer suburbs of Australian cities than inner-city areas, because of the lower average incomes and weaker credit characteristics in these suburbs. “Delinquency rates are highest in outer suburban areas. On average across Australian cities, mortgage delinquency rates are lowest in areas within five kilometers of central business districts and highest in areas 30-40 kilometers from CBDs. In the residential mortgage-backed securities they rate, delinquency rates are in many cases higher in deals with relatively large exposures to mortgages in outer areas.

We agree there are higher loan to value and debt to income ratios in the outer areas, but the overall debt commitments are higher closer in and so we suspect that many more affluent households are going to get caught, because of multiple mortgages, including investment mortgages and their more affluent lifestyles. My thesis is the banks have been lending loosely to these perceived lower risk high income households, but it ain’t necessarily so…

We also published our Household Financial Confidence index. The latest read, to end September shows a further fall, and continues the trend which started to bite in 2017. The current score is 88.4, just a bit above the all-time low point of 87.69 which was back in 2015. Last month – August – it stood at 89.5. You can watch our video “Household Financial Confidence Drifts Lower Again” where we discuss the results. We expect to see the index continuing to track lower ahead, because the elements which drive the outcomes are unlikely to change. Home prices will continue to move lower, the stock markets are off their highs, wages are hardly growing and costs of living are rising. Household financial confidence is set to remain in the doldrums.

Finally, we also published our survey results in terms of forward intentions. So what is in store for the next few months? Well, in short it’s more of the same, only more so, with more households reporting difficulties in obtaining finance, fewer expecting to transact in the next year and to see home prices rise. You can watch our video “Decoding Property Buying Intentions” where we analyse the results. The single most startling observation is the fall in the number of property investors, including those who hold portfolios of investment properties intending to transact. 20% of portfolio investors are expecting to transact, and the bulk of these intend to sell a property, compared with a year ago when 50% said they would transact, and most were looking to add to their portfolios. Most solo property investors are now on the side lines, with around 10% expecting to transact, and most of these on the sell side. Demand for investment property will continue to fall, as rental yields and capital appreciation fall.

So to the markets.

Locally, the ASX 100 ended the week well down, although there was small rise on Friday, after the heavier falls earlier in the week. We ended at 4,849, up 0.20%. The local volatility index remains elevated, ending at 20.4 on Friday, though that 6.5% lower than the previous day. Expect more ahead.

The ASX Financials index however did less well, and ended at 5,744, up just 0.03% and below the June lows. The banking sector is under pressure, for example Macquarie ended at 115.5, up 0.03% on the day, but well down from its 125 range. And AMP continues to languish at 3.05. We heard from some of the major bank CEO’s this week, with Westpac and ANZ apologising for the issues revealed in the Royal Commission, but I also note that CBA has so far only addressed one of the many issues which APRA agreed with them in terms of behavioural remediation. The banks have a long way to go to regain trust, and we expect more weakness ahead. And the latest estimates are that the sector will be up for something like $2.4 billion dollars in remediation costs and other charges. And guess who will end up paying for their bad behaviour?

The Aussie ended the week at 71.10, having reached the 70.5 range in the week. This has more to do with the US dollar movements than changes in sentiment here.

There are debates about what caused the significant falls, after all the FED rate lift strategy, and the trade wars have been around for some time. But my guess is the market has finally understood the era of low-cost or no-cost money is over. Thus expect more volatility ahead. The US fear index fell back on Friday, down 13.8% to 21.31, but is still elevated.

In fact, Wall Street indexes rose on Friday after a week of significant losses as investors returned to technology and other growth sectors, but gains were hampered by ongoing worries about U.S.-China trade tensions and rising interest rates.

Energy and financial stocks continued to fall and bank stocks kicked off the third-quarter financial reporting season with a whimper, while investors fled insurance stocks after Hurricane Michael slammed into Florida.

The technology sector was the biggest gainer of the S&P’s 11 major industry indexes, with a 1.5 percent advance, but it was still on track for its biggest weekly drop since March. The Dow Jones ended up 1.15% to 25,340, but is well off its recent highs. The NASDAQ was up more, 2.29% to 7,497, as buyers came back into the sector. The S&P 500 ended up 1.37% to 2,765.

All three indexes were on track for their biggest weekly declines since late March.

The S&P Financial index was down 0.42% to 465.07, on mixed trading results which came out on Friday. The S&P 500 banks subsector slid 1.6 percent. The biggest drag on the subsector was JPMorgan Chase & Co which reversed early gains to trade down 2 percent despite its quarterly profit beating expectations. PNC Financial led the percentage losers among bank stocks, with a 6.5 percent drop after the regional bank reported disappointing quarterly loan growth and said it expected only a small improvement in lending this quarter. The only gainers among banks were Citigroup, which rose 0.6 percent, and Wells Fargo which eked out a 0.64 percent gain after upbeat results.

The bank results launch a quarterly reporting season that will give the clearest picture yet of the impact on profits from President Donald Trump’s trade war with China.

The short term 3-Month Treasury remained flat at 2.27 at the end of the week, while the 10-Year bond rose a little to 3.165, up 1.09%. The Treasury yield is now at a 7-year high. The suspicion is that perhaps rates have turned and will go higher still, as a longer term view shows. It is also interesting to compare the US 3-Month Bill Rate minus the same rates in Germany and the UK. Short term rates in the US are higher, in fact reaching the highest positive difference since September 1984. This highlights the different path now being taken by the US, but the fall-out will be global.

Gold, which had moved higher among the market ructions, slide a little, and was down 0.52% on Friday to end at 1,221. Bitcoin finished at 6,316 up 0.57%, and continues in its marrow range for now. And Oil which had fallen earlier in the week moved up 0.72% to 71.48.

Finally, it’s worth noting that the Reserve Bank Of New Zealand is now publishing a bank specific set of scorecards to help consumers weigh up the risks bank to bank. This is essential, given the now explicit Deposit Bail-In which exists there. We discussed this most recently in our Post “The Never Ending “Bail-In” Scandal, and in the Video that Economist John Adams and I released yesterday. In fact, the bank specific data which is available in Australia is derisible compared with the NZ stats, but I came across this slide from LF Economics which highlights how the ratio of Bank Loans To Bank Deposits compares across a number of Banks, including the big four. It’s fair to assume the higher the ratio, the greater the potential risk. Westpac, CBA, NAB and ANZ are all in the top half. I believe we need more specific disclosure from the sector, and I suggest that APRA continues to provide only a partial view of the banking system here. The fact is, Bail-In, or no, we need much more transparency. It would help to negate the spin presented in the RBA’s Financial Stability Review, which in my view is not effective. Oh, and look out for our joint video on Gold, coming up in the next few days, it will surprise you!

Finally, a reminder that on Tuesday 16th October at 20:00 Sydney we are running our next live stream Q&A event. The reminder is up on YouTube, and you can send me questions before hand, or join in the live chat. So mark your dairies.

ANZ has warned today that their Full Year Cash Profit will be impacted by additional charges for customer compensation, accelerated amortisation of software and other notable items.

Charges of $374 million have be recognised in 2H18 for refunds to customers and related remediation costs. These relate to issues that have been identified from reviews to date. These reviews remain ongoing.

Approximately 57% relates to customer refunds impacting revenue, with the balance relating to remediation costs recorded as n expense. The total remediation charge is split approximately 66%/35% between Continuing and Discontinued operations.

Key items of customer remediation include:

Compensating customers for issues arising from product review in the Australian division.

Compensation for customers receiving inappropriate advice or for services not provided within ANZ’s former aligned dealers group. (These were sold to IOOF on 1 October 2018).

ANZ has accelerated the amortisation of certain software assets, predominantly relating to its International business. This follows a recent review of the International business along with a number of divestments announced or completed this year. Accelerated amoritisation expenses of $206 million will be recorded in 2H18.

Along with announced divestments and the matters above, they also declared:

Restructuring charge of $104 million in 2H18, largely relating to the previously announced move of the Australian and Technology Divisions to agile ways of working.

External legal costs associated with responding to the Royal Commission which will total $55 million (pre-tax) for FY18.

The impact of these additional charges on ANZ’s Common Equity Tier 1 capital position compared to 1H18 is expected to be less that 10 basis points.

ANZ’s FY18 Results Announcement will be released on 31 October 2018.

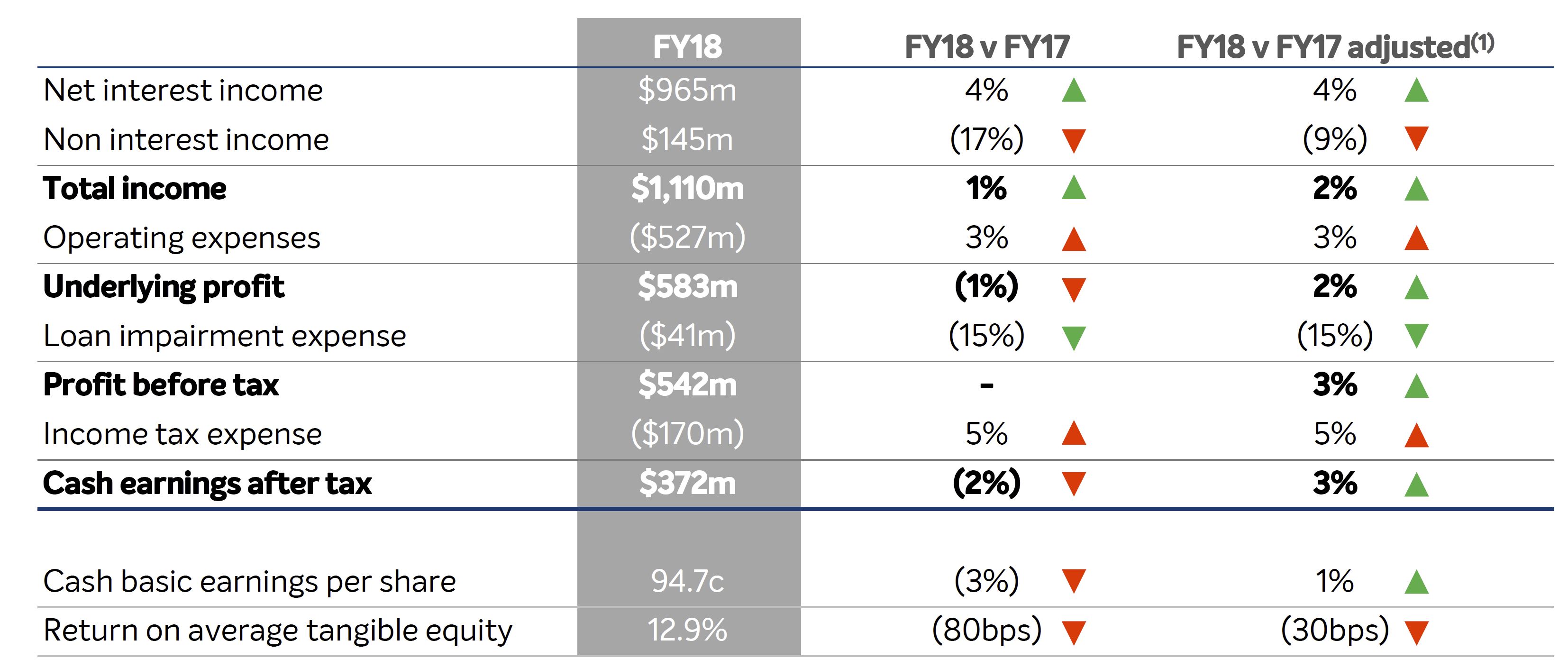

The Bank of Queensland have announced FY18 cash earnings after tax of $372 million, down two per cent on FY17. Statutory net profit after tax of $336 million, was down 5%.

Being a regional is a tough gig, and they continue to drive significant digital transformation, but despite some accounting wizardry, the cracks are showing in our view. The tighter home lending sector, and reduce fee income both hit home. As a result capital is weaker than expected.

Statutory net profit after tax decreased 5 per cent to $336 million. The BOQ Board has maintained a fully franked final dividend of 38 cents per ordinary share. Basic earnings per share was down 3% to 94.7 cents. Their return on average ordinary equity down 50 bps to 9.9%

2H18 cash earning was $190 million and bad loan expenses were lower, down 15% to $41 million or 9 bps of gross loans.

Net interest margin ended the year at 1.98% a little higher, but reflected hedging cost headwind mitigated by improvements driven through funding mix and asset pricing, front book vs back book repricing and >2bps benefit from extension in weighted average life of housing loans, reflecting portfolio trends.

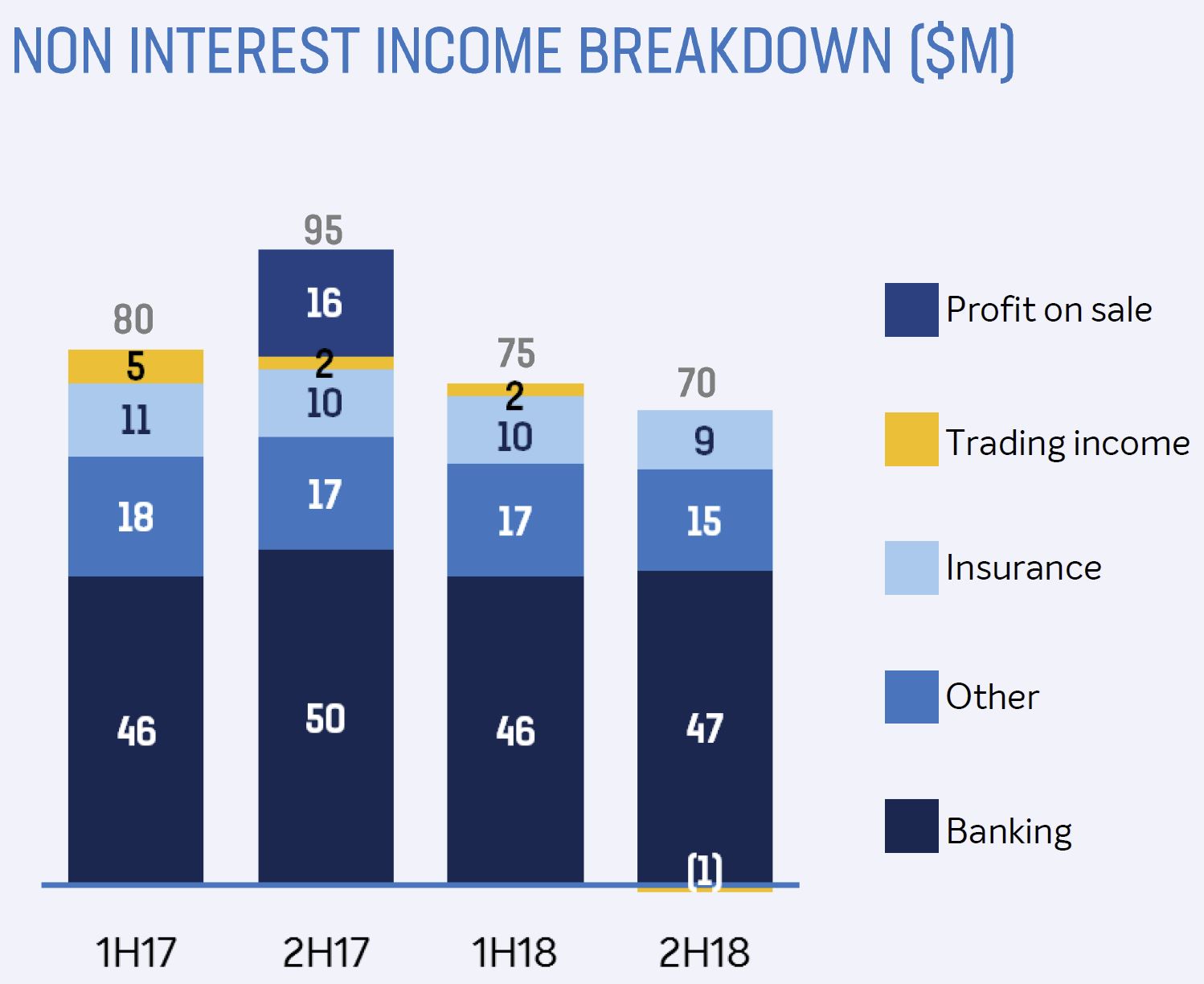

Non interest income fell thanks to ongoing pressure on banking fees, insurance income continuing to trend lower, and limited opportunities for trading income generation.

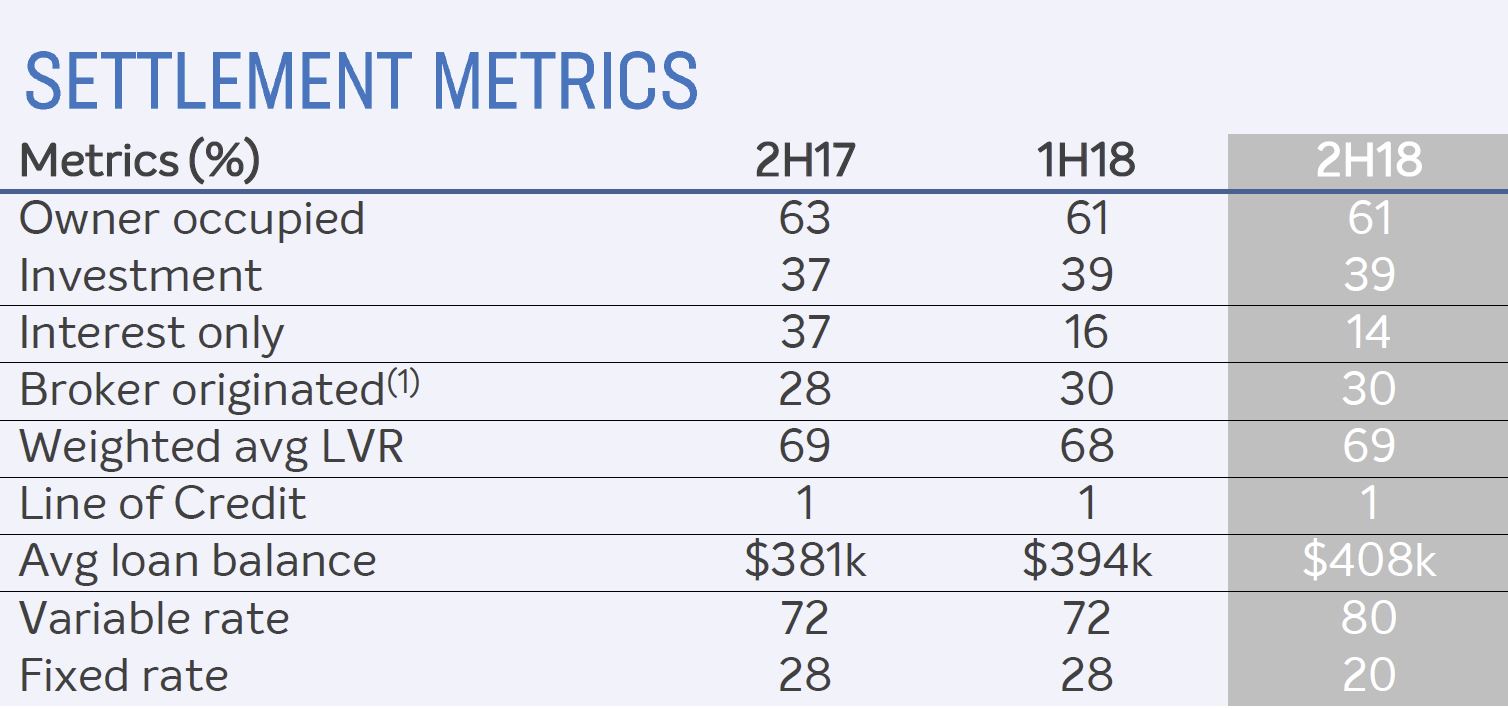

Within their housing portfolio, broker settlements were at 30%. Interest only settlements reduced significantly and owner occupied P&I loans represent 50% of portfolio.

Interest only loans are now 14% of new settlements, down from 37% in 2017. The average loan balance is growing (despite the tighter lending conditions across the industry). They hold 16% above an LVR of 81-90% and 8% greater than 90%.

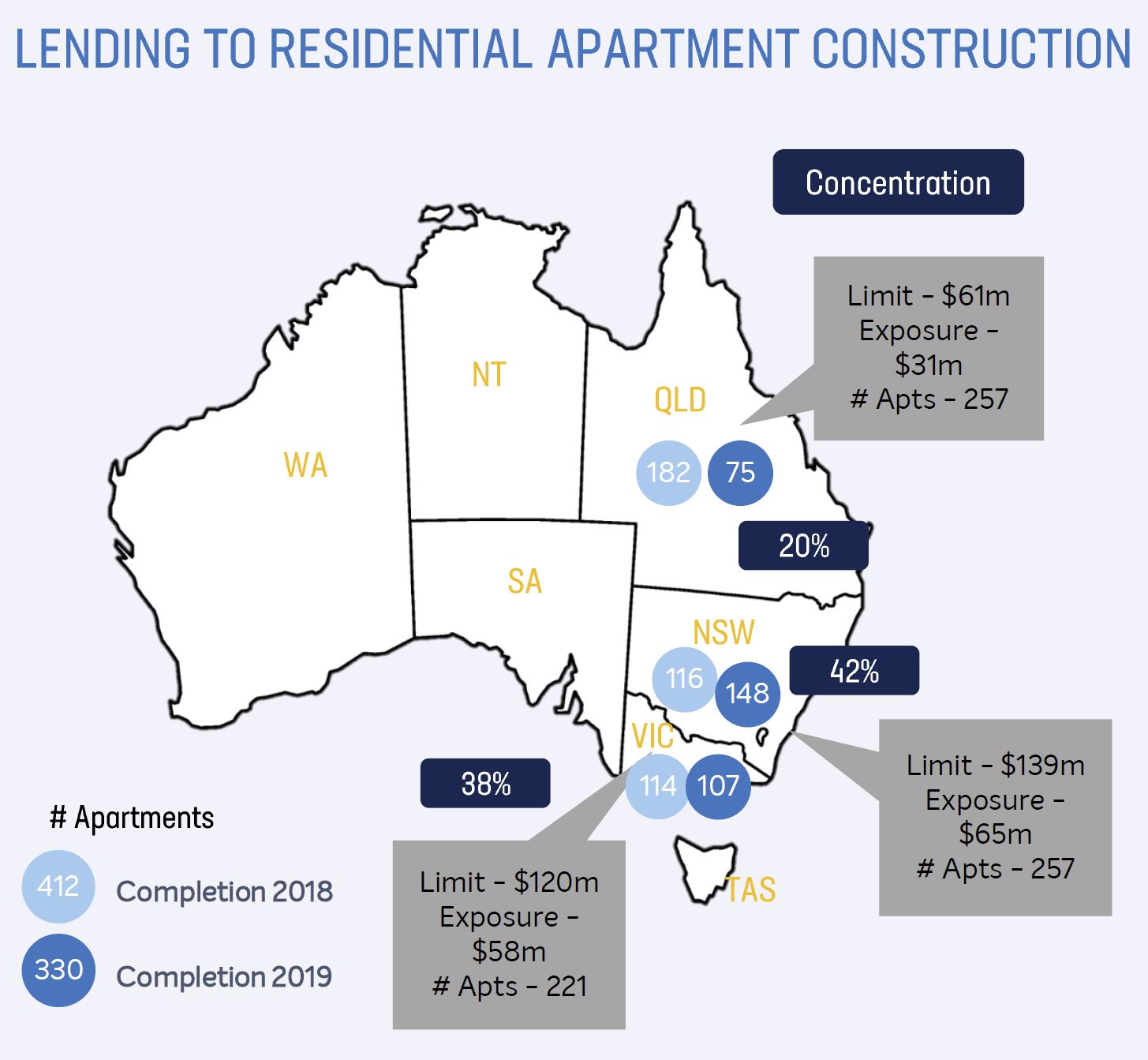

They have $154m current exposure to residential construction, representing 14 developments across 3 states, completing 2018 through 2019. They say it is well diversified intra-state within NSW and VIC.

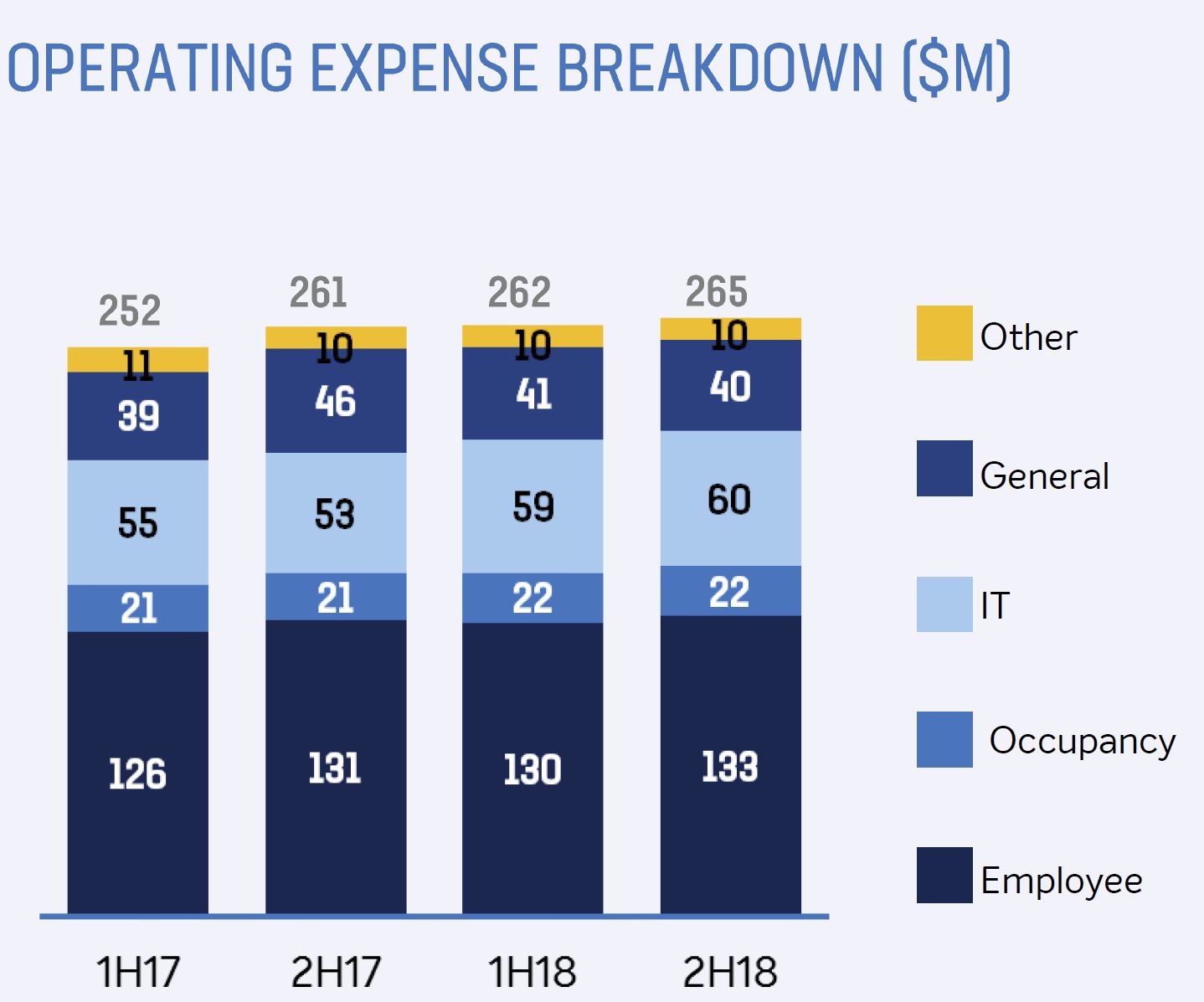

Overall expenses grew at 3% and cost to income ratio was up 90 bps to 47.5%, despite core operating expense growing at 1%. They increased the amortization of ongoing IT investment and increased capital investment flagged for FY19.

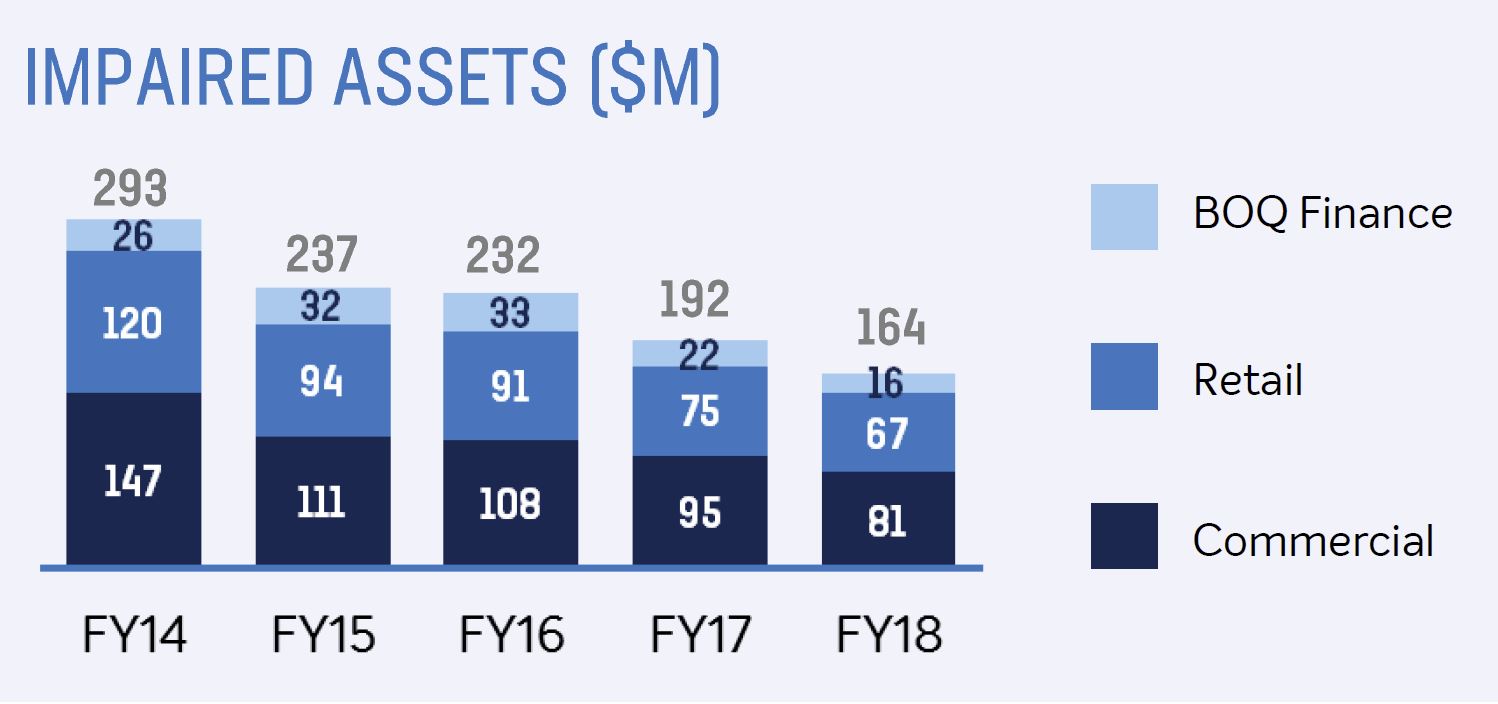

Impaired assets for the year stood at $164 million, down from $192 million in FY17.

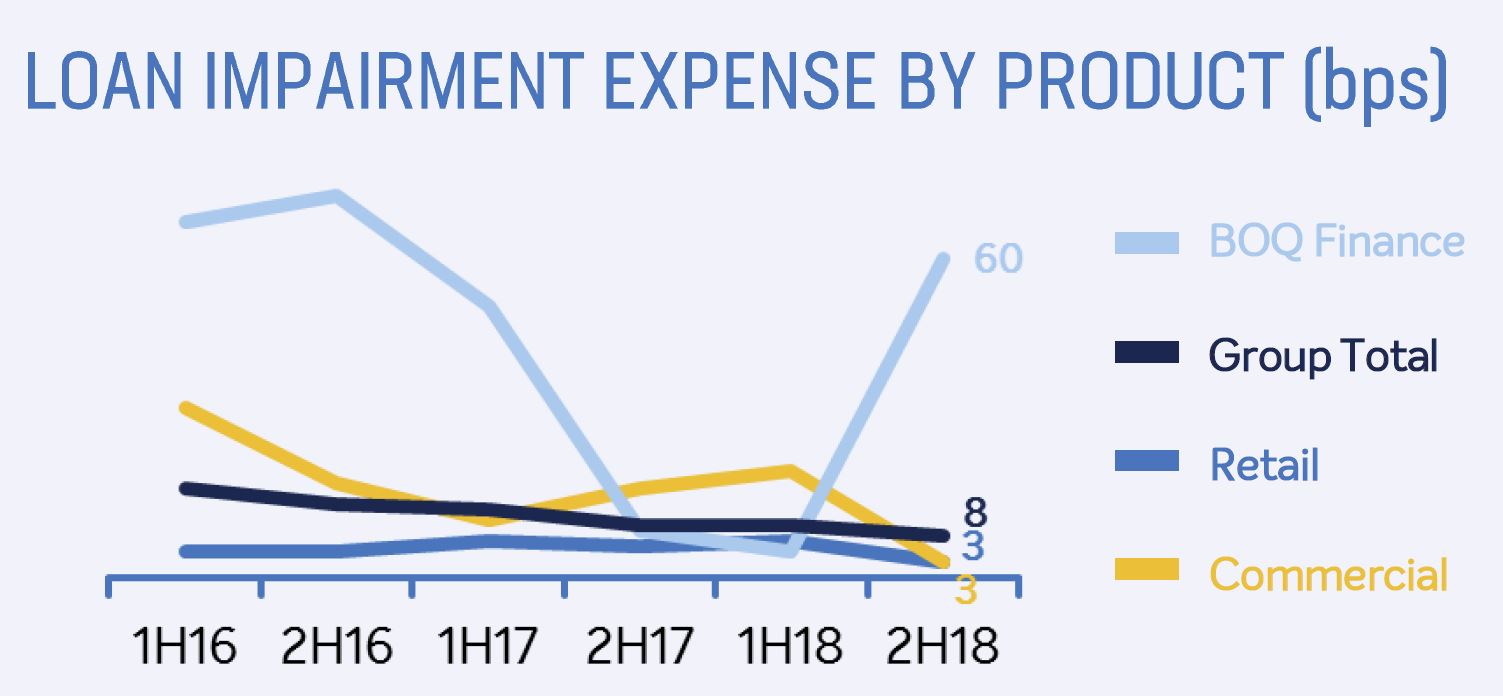

Loan impairments for BOQ Finance rose to 60 basis points in 2H18.

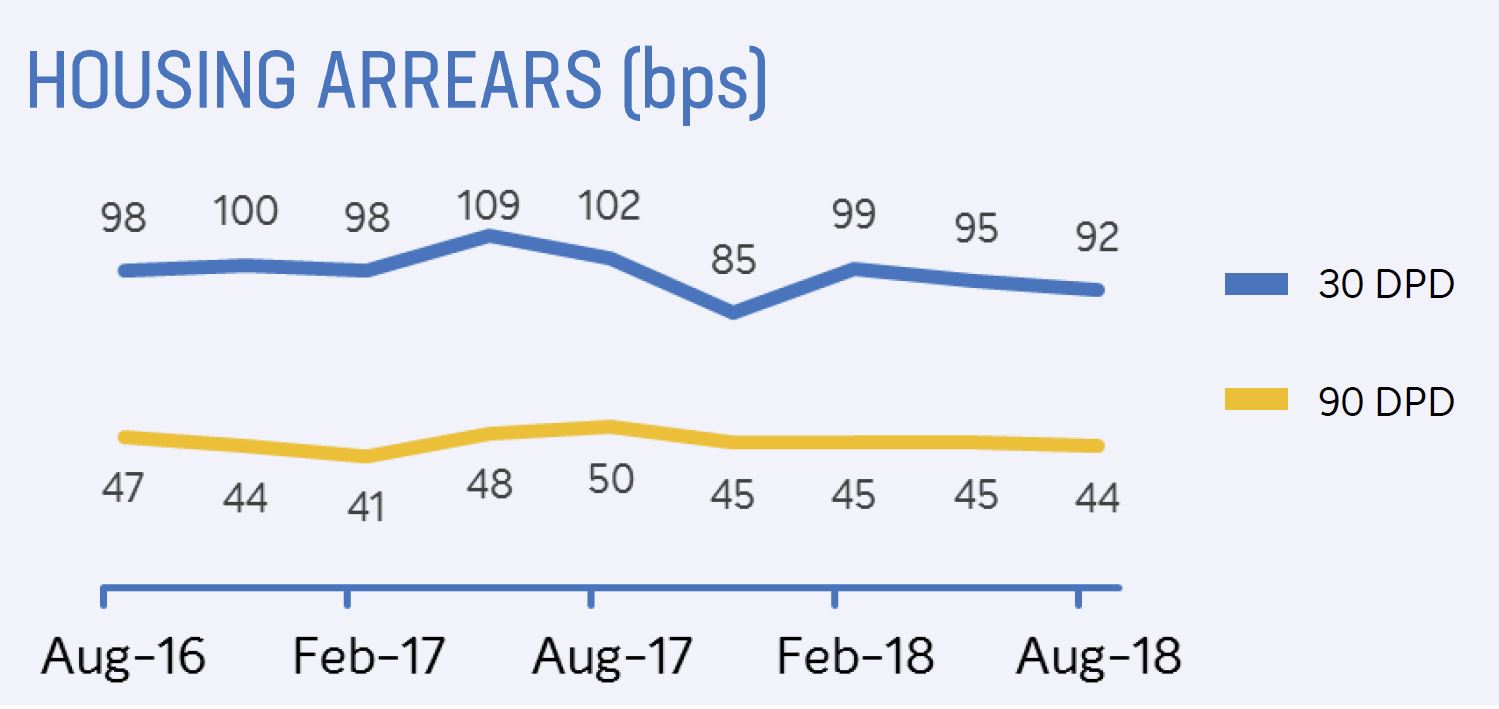

Housing loan arrears are relatively stable.

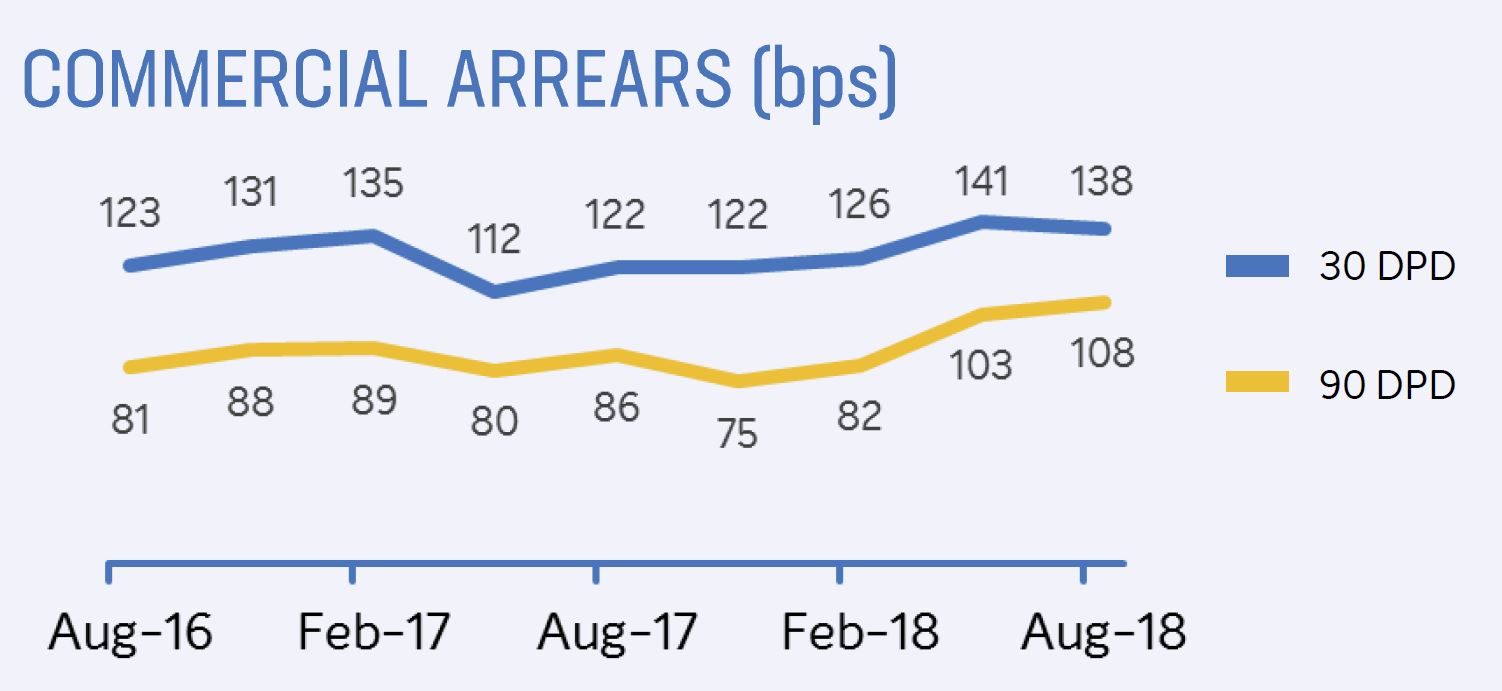

Commercial arrears past 90 day have risen.

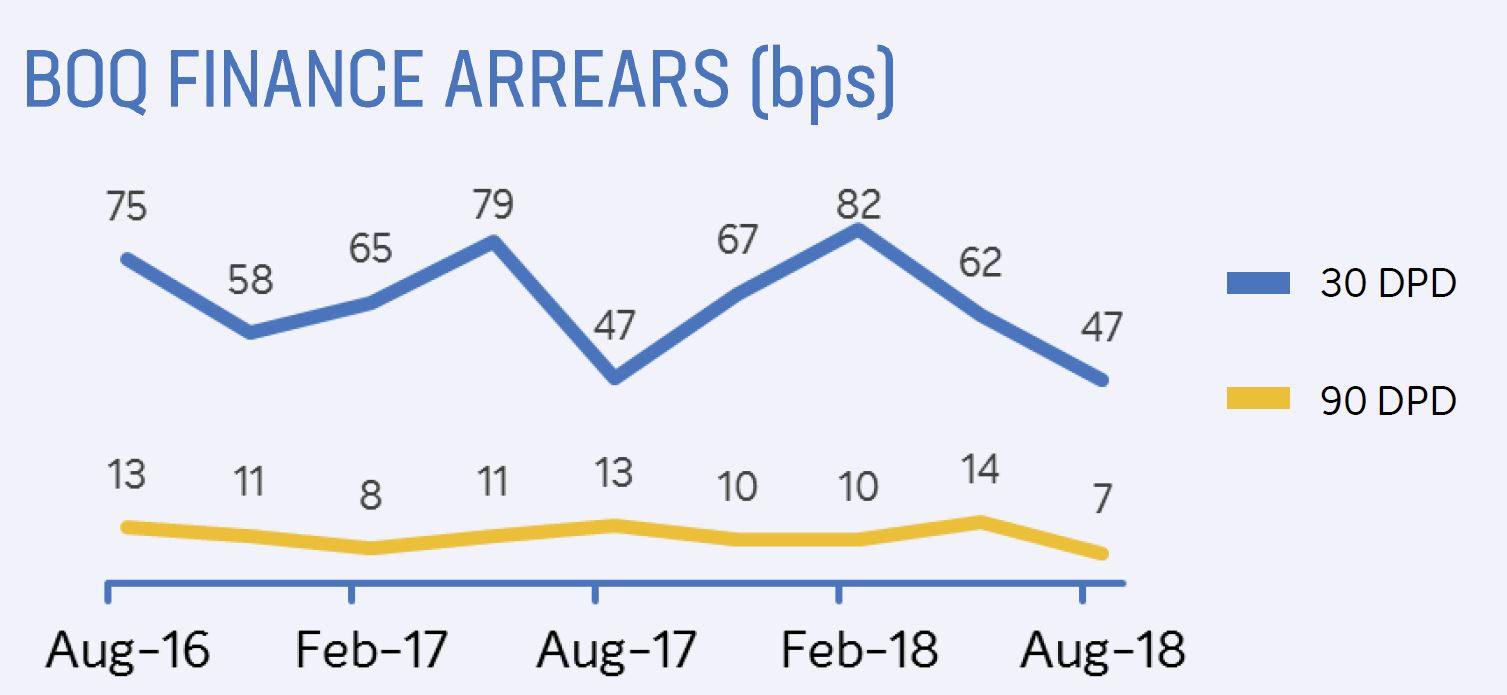

BOQ finance arrears appear more volatile.

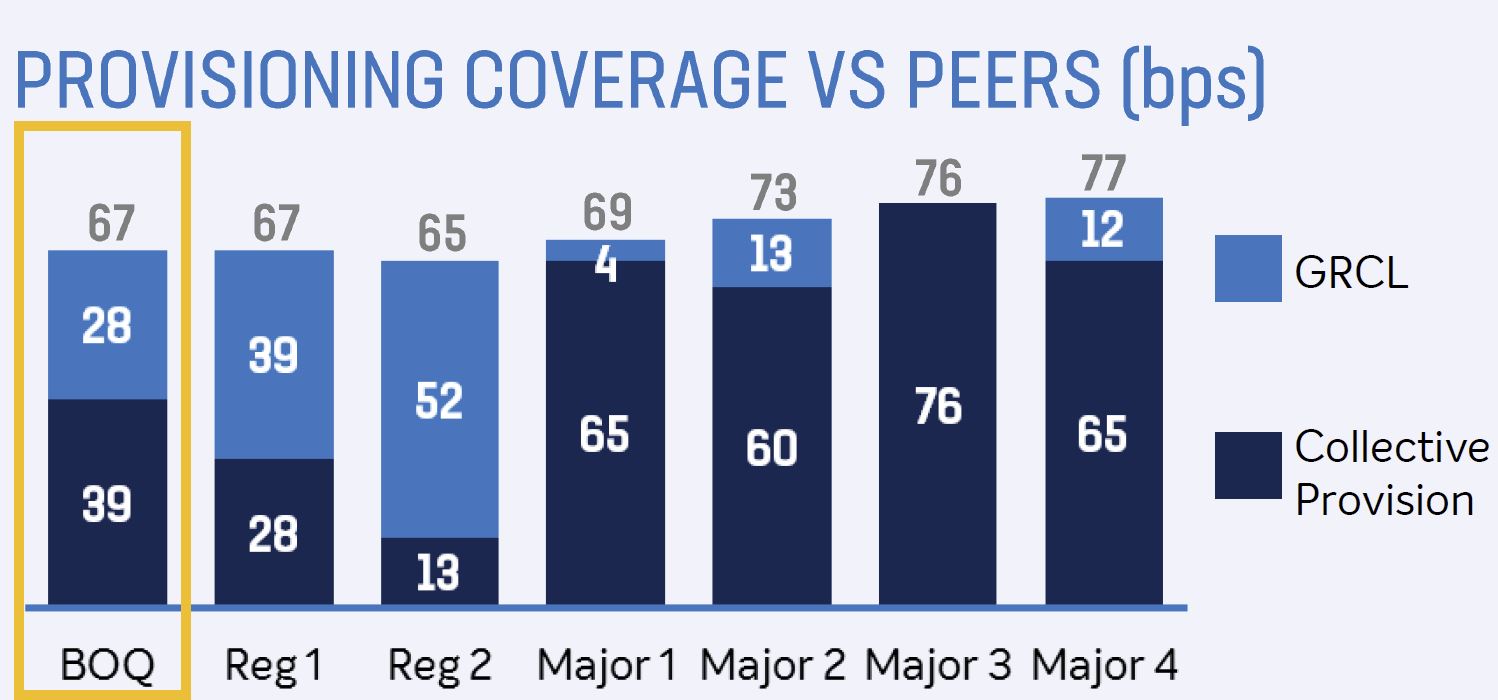

BOQ provisions are at the lower end of the spectrum compared with major players, but similar to other regionals.

They had a deposit growth rate of 4% and 65% of loans are covered by deposits.

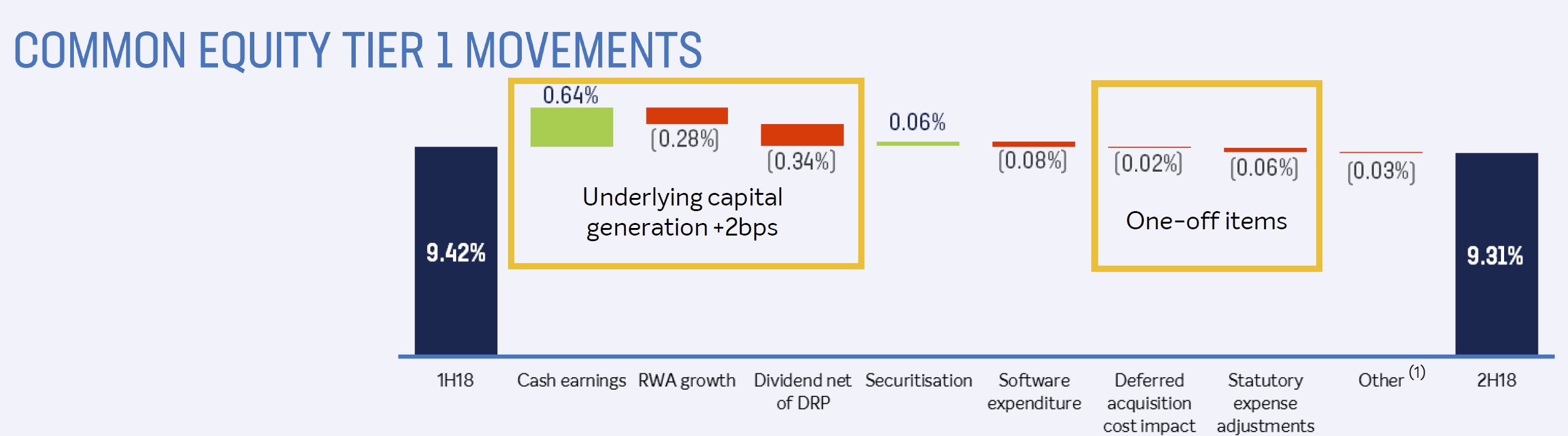

The CET1 ratio at 9.31% is lower than some analysts were expecting.

The underlying capital generation of +2bps, with an impact from one-off items of (8bps) and increased investment spend reduced CET1 by 8bps. We think the banks capital management flexibility is reduced, especially as it flagged it will use 7bps of excess capital over FY19/FY20 to accelerate digital investment.

Finally, its worth noting that there was no update on the progress of the St Andrews disposal, which remains ‘subject to regulatory approval’.

Westpac Banking Corporation has today announced that it’s Cash earnings in Full Year 2018 will be reduced by an estimated $235 million following continued work on addressing customer issues and from provisions related to recent litigation.

The key elements include:

Increased provisions for customer refunds associated with certain advice fees charged by the Group’s salaried financial planners due to more detailed analysis going back to 2008. These include where advice services were not provided, as well as where we have not been able to sufficiently verify that advice services were provided;

Increased provisions for refunds to customers who may have received inadequate financial advice from Westpac planners;

Additional provisions to resolve legacy issues as part of the Group’s detailed product reviews;

Provisions for costs of implementing the three remediation processes above; and

Estimated provisions for recent litigation, including costs and penalties associated with the already disclosed responsible lending and BBSW cases.

Details of the provisions/costs are still being finalised and the Group expects to provide more information when it releases its Full Year 2018 Results template, later in October 2018. As a guide, approximately two thirds of the impact is expected to be recorded as negative revenue while the remainder will be recorded in costs. Costs associated with responding to the Royal Commission are not included in these amounts

The program of reviews will continue into Full Year 2019. This includes continuing to investigate and consider potential further costs associated with advice fees charged by our aligned planners.

Westpac is scheduled to report its Full Year 2018 results on 5 November 2018.

Notwithstanding these new provisions, Westpac remains well placed to meet APRA’s unquestionably strong capital benchmark.

Westpac first commenced its “get it right put it right” initiative in early 2017 to address legacy issues in some products and practices.

Westpac Chief Executive Officer, Brian Hartzer said “It is disappointing some of our past practices have not lived up to appropriate standards. We are committed to fixing any issue identified, as well as ensuring that any customer affected has not been disadvantaged.”

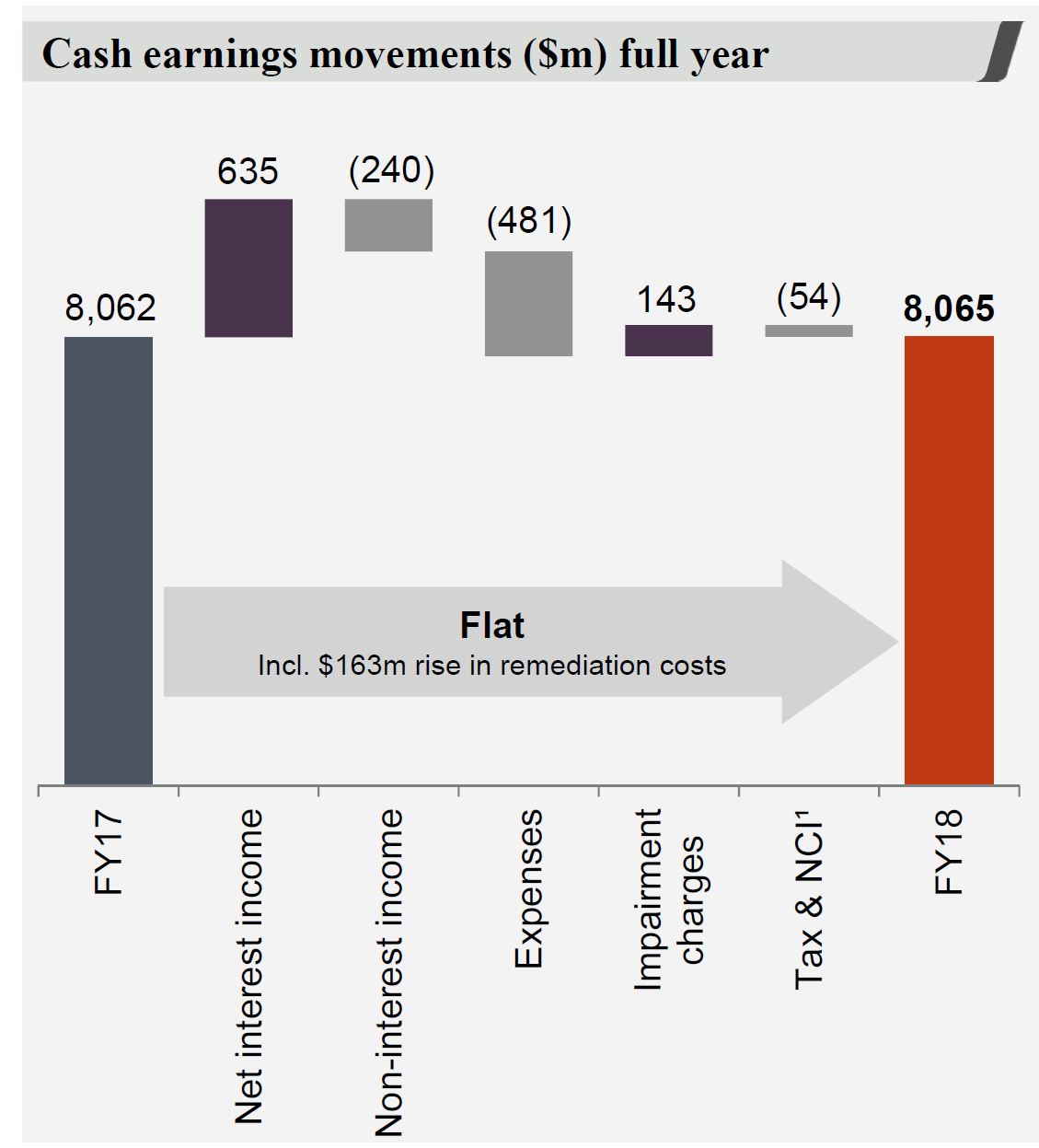

Cash earnings were $8,065 million, little changed on last year. Cash earnings per share, 236.2 cents, down 1% and the cash return on equity (ROE) was 13.0%, at the lower end of the range Westpac is seeking to achieve. The final, fully franked dividend was unchanged, of 94 cents per share (cps), so the full year, fully franked dividend of 188 cps. Statutory net profit was $8,095 million, up 1%.

Cash earnings were $8,065 million, little changed on last year. Cash earnings per share, 236.2 cents, down 1% and the cash return on equity (ROE) was 13.0%, at the lower end of the range Westpac is seeking to achieve. The final, fully franked dividend was unchanged, of 94 cents per share (cps), so the full year, fully franked dividend of 188 cps. Statutory net profit was $8,095 million, up 1%. The cash earnings included $163 million in remediation charges, and a fall of $240 million in non-interest income, a a reduction in impairment charges.

The cash earnings included $163 million in remediation charges, and a fall of $240 million in non-interest income, a a reduction in impairment charges. There was a fall of $263 million in the second half in net interest income. and a 10% reduction in earnings, with remediation costs of $430 million.

There was a fall of $263 million in the second half in net interest income. and a 10% reduction in earnings, with remediation costs of $430 million. Income was down 3% over the half, thanks to margin decline and customer remediation.

Income was down 3% over the half, thanks to margin decline and customer remediation.

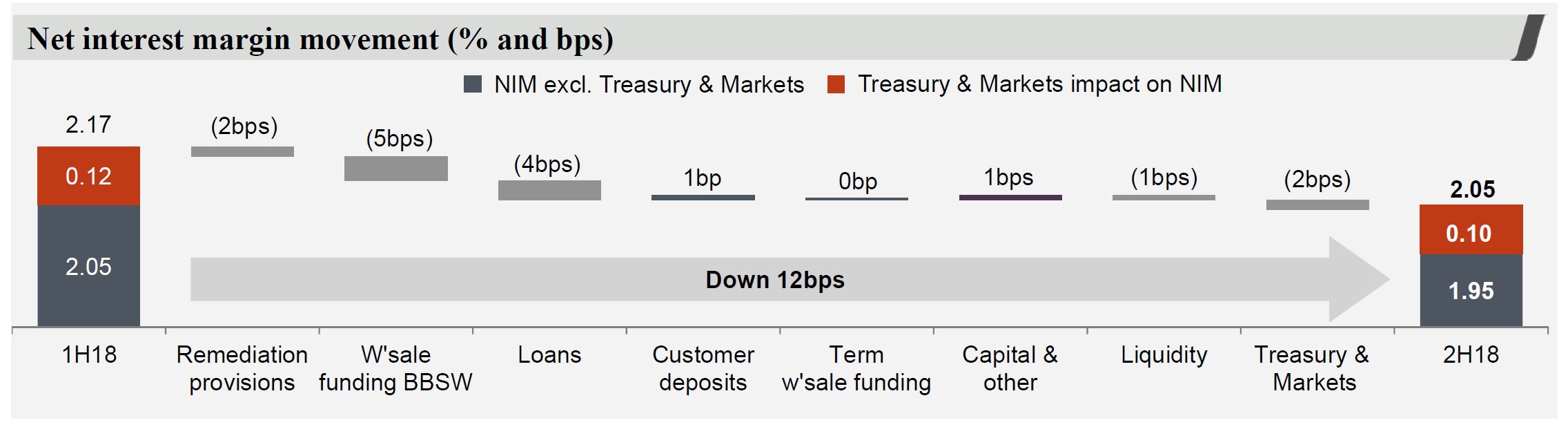

Margins in the second half were down from 2.05 to 1.95, or 10 basis points in the main banks, and from 0.12 to 0.10 in the Treasury and Markets. 5 basis points related to wholesale funding, and 4 basis points loans, offset by 1 basis point from deposits.

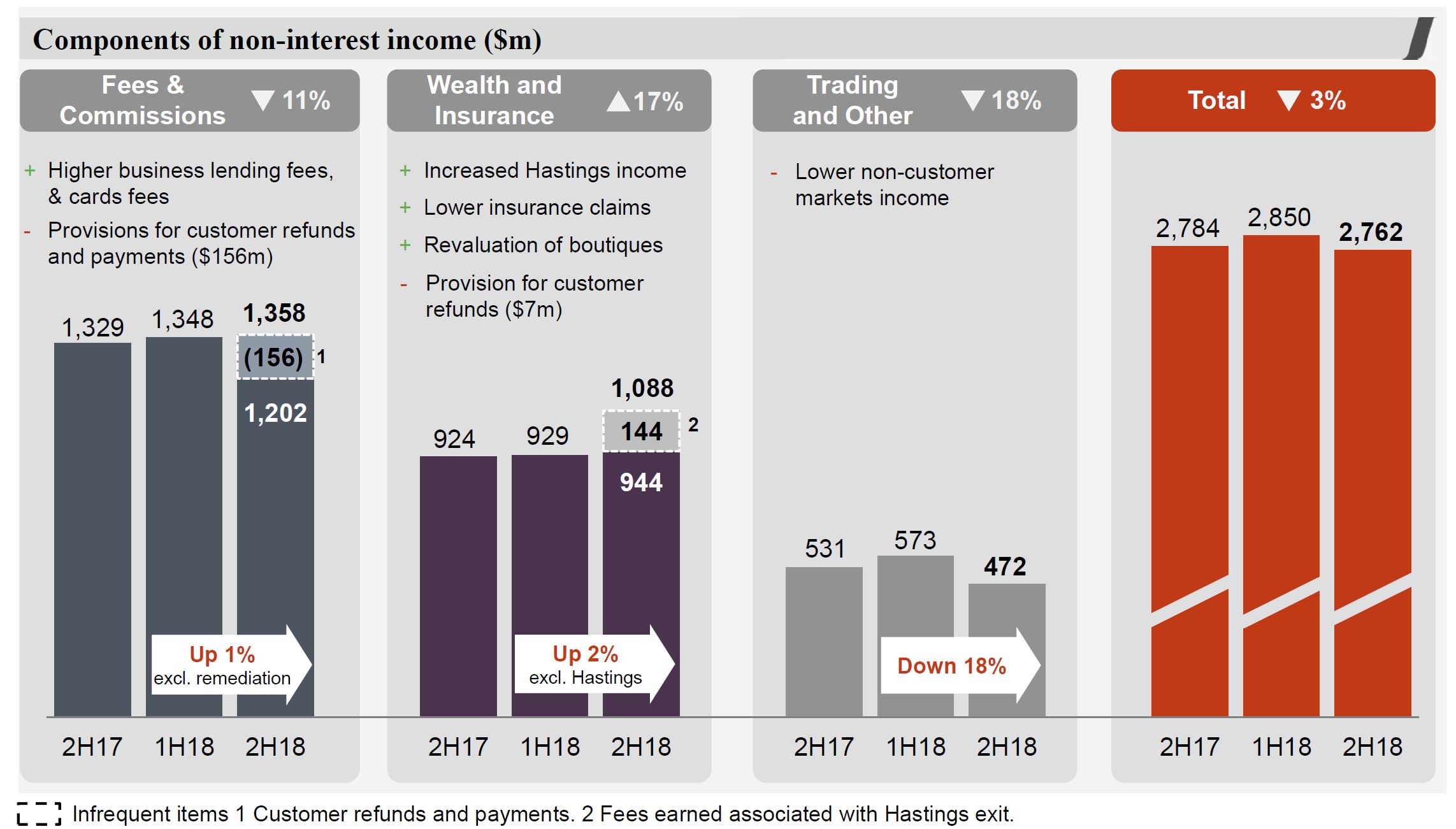

Margins in the second half were down from 2.05 to 1.95, or 10 basis points in the main banks, and from 0.12 to 0.10 in the Treasury and Markets. 5 basis points related to wholesale funding, and 4 basis points loans, offset by 1 basis point from deposits. Non interest income fell and included provisions for customer refunds of $156 million and lower trading income, which was down 18% in the second half.

Non interest income fell and included provisions for customer refunds of $156 million and lower trading income, which was down 18% in the second half. Expenses were higher thanks to regulation and compliance, remediation and platform investments.

Expenses were higher thanks to regulation and compliance, remediation and platform investments. FTE were down by around 700 from the first half.

FTE were down by around 700 from the first half. Stressed assets as proportion of total committed exposure (TCE) was lower, despite a rise in 90 days+ past due. Australian 90 day + mortgage delinquencies rose from 69 to 72 basis points in the second half.

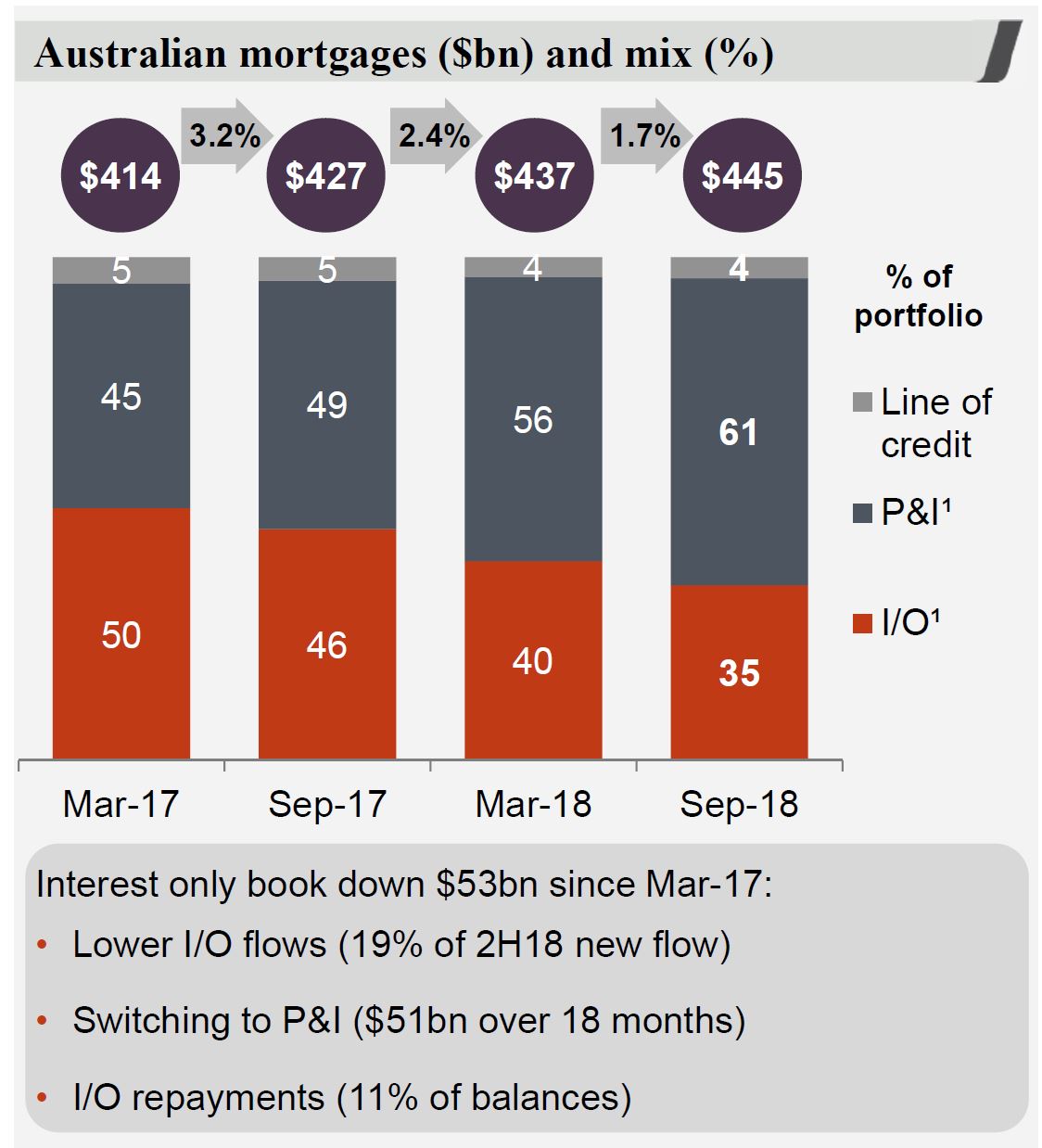

Stressed assets as proportion of total committed exposure (TCE) was lower, despite a rise in 90 days+ past due. Australian 90 day + mortgage delinquencies rose from 69 to 72 basis points in the second half. Westpac is writing more mortgage loans from NSW and VIC, relative to system and 51.6% of new flows came from propitiatory channels. 8.2% of new loans were from first time buyers. Borrowers applying for a mortgage must be able to service the higher of either: 7.25% minimum assessment rate; or product rate plus 2.25% buffer. Actual mortgage losses are 2 basis points.

Westpac is writing more mortgage loans from NSW and VIC, relative to system and 51.6% of new flows came from propitiatory channels. 8.2% of new loans were from first time buyers. Borrowers applying for a mortgage must be able to service the higher of either: 7.25% minimum assessment rate; or product rate plus 2.25% buffer. Actual mortgage losses are 2 basis points.

The schedule of IO loan expiry reaches out over the next 10 years!

The schedule of IO loan expiry reaches out over the next 10 years! The Australian mortgage book shows a rise in delinquencies, a small fall in those paying ahead, and a rise in dynamic LVR (in response to falling prices). Dynamic LVR is the loan-to-value ratio taking into account the current loan balance, estimated changes in security value, offset account balances and other loan adjustments. WA and SA/NT are most exposed.

The Australian mortgage book shows a rise in delinquencies, a small fall in those paying ahead, and a rise in dynamic LVR (in response to falling prices). Dynamic LVR is the loan-to-value ratio taking into account the current loan balance, estimated changes in security value, offset account balances and other loan adjustments. WA and SA/NT are most exposed. Westpac reported their mortgage stress tests which assumes a severe

Westpac reported their mortgage stress tests which assumes a severe The CET1 ratio was 10.63%, up 13 basis points from March 2018.

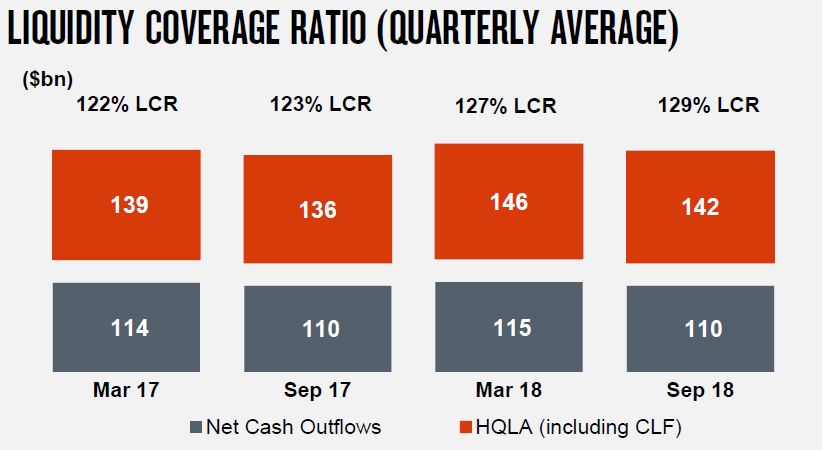

The CET1 ratio was 10.63%, up 13 basis points from March 2018. LCR and NSFR both improved.

LCR and NSFR both improved.