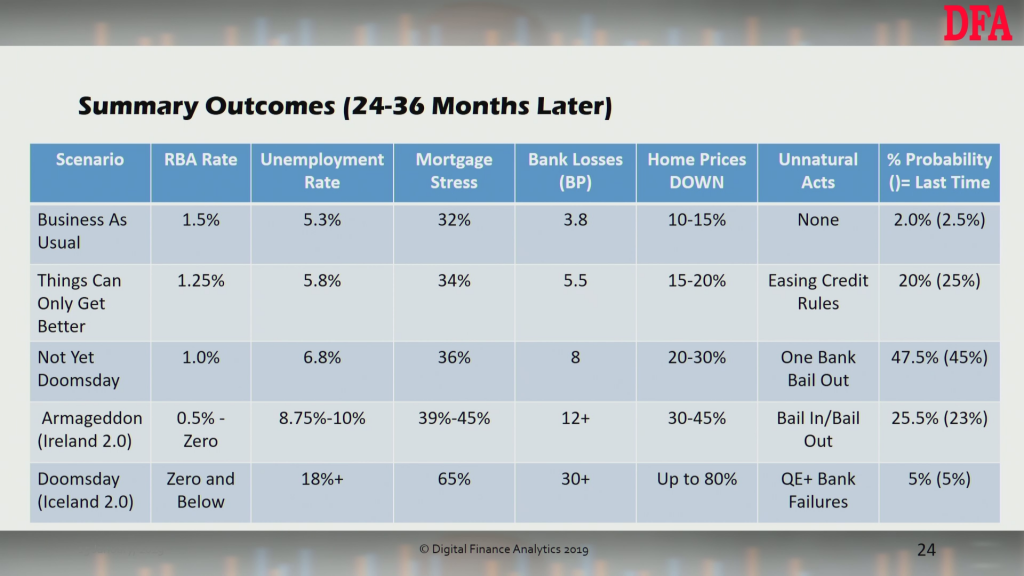

We have updated our scenarios to take account of potential RBA rate cuts later in the year, revised mortgage stress and household confidence data and other factors. We also updated our probability allocation. Here is a summary.

Our central scenario is one of home price fall, peak to trough, of up to 30%. A deeper fall, in the event of international financial stability is also possible. We do not think the RBA has any hope of lifting rates from current emergency levels, having dropped them too low previously.

We discussed these updates during yesterdays live stream Q&A event. Here is a high quality edited version.

You can also watch the recorded “live” version, including the chat replay here:

Another blowout in bank funding costs is adding to the pressure for an RBA rate cut, according to a leading forecaster, via InvestorDaily.

AMP Capital chief economist Shane Oliver is confident that the

Reserve Bank will be forced to cut the cash rate by 50 basis points to 1

per cent this year.

He explained that Australian economic data has been soft in recent

weeks with weak housing credit, sharp falls in home prices in December,

another plunge in residential building approvals pointing to falling

dwelling investment, continuing weakness in car sales, a loss of

momentum in job ads and vacancies and falls in business conditions for

December.

“Retail sales growth was good in November but is likely to slow as home prices continue to fall,” Mr Oliver said.

“Income tax cuts will help support consumer spending, but won’t be

enough so we remain of the view that the RBA will cut the cash rate to 1

per cent this year.”

Meanwhile, another spike in funding costs has seen a number of

lenders hike their mortgage rates in the first few weeks of 2019.

Bank of Queensland lifted rates by 18 basis points, while home loan

providers Virgin Money and HomesStart Finance have also announced

interest rate rises.

“The gap between the 3-month bank bill rate and the expected RBA cash

rate has blown out again to around 0.57 per cent compared to a norm of

around 0.23 per cent,” Mr Oliver said.

“As a result, some banks have started raising their variable mortgage

rates again. This is bad news for households seeing falling house

prices. The best way to offset this is for the RBA to cut the cash rate

as it drives around 65 per cent of bank funding.”

Digital Finance Analytics principal Martin North believes even small

rate rises could see more households pushed into mortgage stress and

increase the risk of default among those already under pressure to meet

their monthly repayments.

“The other point is that it will actually tip more borrowers into

severe stress, that’s when you’ve got a serious monthly deficit. That’s

the leading indicator for default 18 months down the track,” he said.

The second wave of out-of-cycle mortgage rate hikes has continued, with another lender announcing increases of up to 20 basis points, via The Adviser.

NAB-owned

lender UBank has announced that it has increased interest rates on its

fixed rate investor home loan products by 20 basis points, effective for

new loans issued as of 14 January.

The lender’s investor mortgage rate increases are as follows:

A rise of 20bps on its 1-year UHomeLoan fixed rate with interest-only terms, from 3.99 per cent to 4.19 per cent

A rise of 20bps on its 3-year UHomeLoan fixed rate with interest-only terms, from 3.99 per cent to 4.19 per cent

A rise of 20bps on its 5-year UHomeLoan fixed rate with interest-only terms, from 4.49 per cent to 4.69 per cent

UBank is the latest lender to increase its home loan rates, after the Bank of Queensland (BOQ) and Virgin Money announced rate increase of up to 18bps and 20bps, respectively.

Both BOQ and Virgin Money attributed their decisions to lift home loan rates to the sustained rise in wholesale funding costs.

Speaking

to The Adviser’s sister publication, Mortgage Business, principal of

Digital Finance Analytics (DFA) Martin North said that he expects mortgage stress to continue mounting in the short to medium term, particularly off the back of out-of-cycle interest rate hikes.

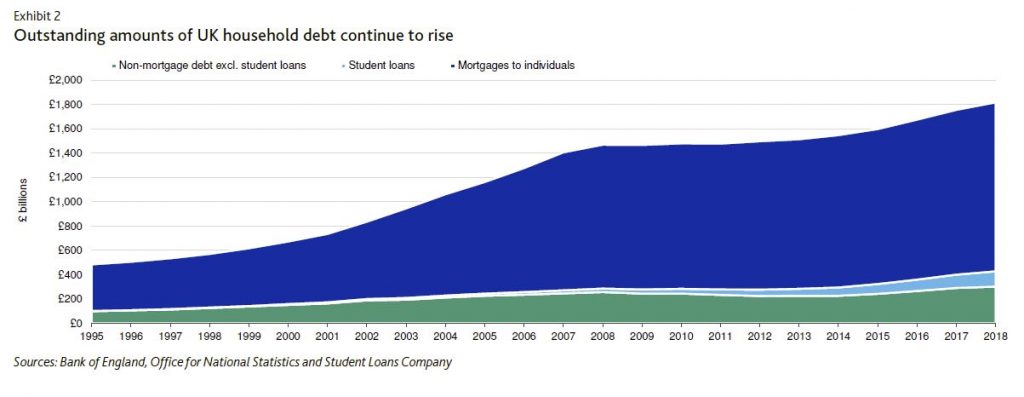

According to Moody’s, on 7 January, UK trade unions published their annual report, which warned about a credit crisis as UK average non-mortgage household debt jumped above £15,000, almost 50% higher than before the 2008 financial crisis. The increase in household debt leaves borrowers vulnerable to sudden economic stress, such as that which might crystallise in a no-deal Brexit scenario. An incremental increase in unemployment would have negative consequences for highly leveraged consumers. Higher joblessness, reduced real wages and, to a lesser extent, lower refinancing availability would increase delinquencies and defaults in consumer loan pools backing residential mortgage-backed securities (RMBS) and asset-backed securities (ABS).

Additionally, softening house prices can exacerbate the negative effect of rising defaults on RMBS. In case of a severe economic stress, the macroeconomic outlook for the UK would weaken, leading to a decline in house prices nationwide, which would have a mixed effect regionally across the UK. We expect more negative consequence in regions with higher unemployment and in industries that are more materially affected by such a stress scenario. However, we expect that any deceleration in house prices will be less severe than during the 2008-09 financial crisis given less inflationary stresses within the market. The performance of buy-to-let (BTL) and nonconforming transactions would weaken, especially for some recently originated collateral pools that have assets with relatively weaker underwriting standards. The performance of credit card ABS collateral would also deteriorate, especially for those pools with more exposure to highly leveraged obligors.

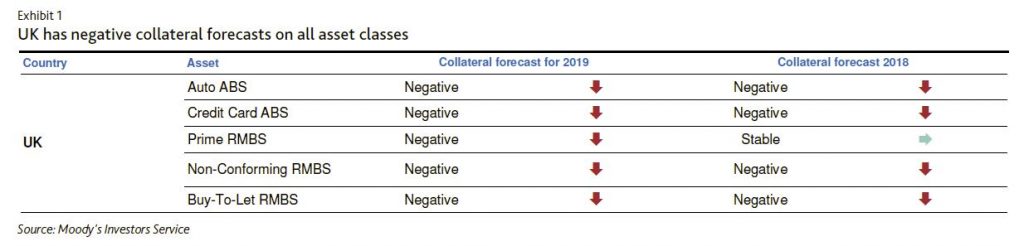

We have negative collateral forecasts for all UK consumer sectors

Our forecasts are negative for all UK consumer sector collateral. Our collateral performance forecasts over the next 12-18 months address the direction of expected losses for the market in general, not specific collateral pools among the deals we rate.

In normal circumstances, the absolute level of household debt is not necessarily as important as affordability measures such as the ratio of payment or loan to disposable income. Given the low interest rate environment, affordability is still relatively high for UK borrowers. However, sudden economic stress that leads to negative real wage growth and increasing unemployment has the potential to change matters.

The average household debt figure in the trade union’s analysis is based on data from Bank of England, Office for National Statistics and the Student Loans Company. It excludes mortgages but includes everything else (i.e., credit cards, personal loans, payday loans and student loans), which deviates from the Bank of England’s definition of non-mortgage household debt.

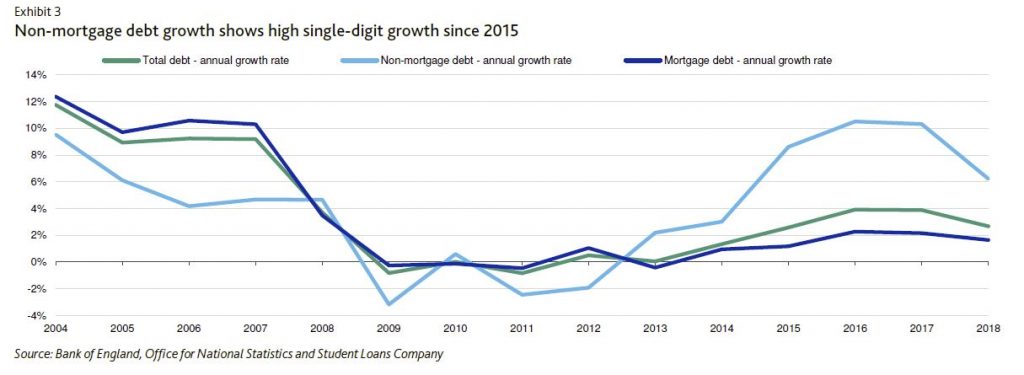

The rapid growth of non-mortgage (mainly unsecured) debt has contributed to household debt since 2013 after years of constrained credit in the aftermath of the 2008 financial crisis. The growth patterns of mortgage and non-mortgage debt have switched gears compared with pre-crisis patterns: non-mortgage debt (e.g., credit cards and consumer loans) have had a high single-digit growth rate since 2015, with slightly slowing growth in 2018 to a level of 6%, whereas pre-crisis, mortgage debt had these high growth rates. The 2018 data shows that UK households had average non-mortgage debt of approximately £10,000, even excluding student loans, and this is in line with levels reported in 2008.

On 9 January, Moody’s says, the Federal Reserve Board (Fed) proposed revisions to company-run stress testing requirements for Fed-regulated US banks to conform with the Economic Growth, Regulatory Relief, and Consumer Protection Act (the EGRRCPA), which became law in May 2018.

Among the revisions, which are similar to those proposed in December 2018 by the Office of the Comptroller of the Currency (OCC) and the Federal Deposit Insurance Corp. (FDIC), is a proposal that would eliminate the requirement for company-run stress tests at most bank subsidiaries with total consolidated assets of less than $250 billion. The proposed changes would be credit negative for affected US banks because they would ease the minimum requirements for stress testing at the subsidiary level.

The proposed revisions would also require company-run stress tests once every other year instead of annually at most banks with more than $250 billion in total assets that are not subsidiaries of systemically important bank holding companies. Additionally, the proposal would eliminate the hypothetical adverse scenario from all company-run stress tests and from the Fed’s own supervisory stress tests, commonly known as the Dodd-Frank Stress Test (DFAST) and the Comprehensive Capital Analysis and Review (CCAR); the baseline and severely adverse scenarios would remain.

The proposed changes aim to implement EGRRCPA. As such, we expect that they will be adopted with minimal revisions. In late December 2018, the FDIC and OCC published similar proposals governing the banks they regulate. The stress testing requirements imposed on US banks over the past decade have helped improve US banks’ risk management practices and have led banks to incorporate risk management considerations more fully into both their strategic planning and daily decision making. Without periodic stress tests, these US banks may have more flexibility to reduce their capital cushions, making them more vulnerable in an economic

downturn.

On 31 October 2018, the Fed announced a similar proposal for the company-run stress tests conducted by bank holding companies as a part of a broader proposal to tailor its enhanced supervisory framework for large bank holding companies. Positively, the Fed’s 31 October 2018 proposal would still subject bank holding companies with total assets of $100-$250 billion to supervisory stress testing at least every two years and would still require them to submit annual capital plans to the Fed, even though the latest proposal would no longer require their bank subsidiaries to conduct their own company-run stress tests. Also, supervisory stress testing for larger holding companies would continue to be conducted annually. Continued supervisory stress testing should limit any potential reduction

in capital cushions at those bank holding companies.

We believe that some midsize banks will continue to use company-run stress testing in some form, but more tailored to their own needs and assumptions. Nevertheless, this may not be the view of all banks, particularly those for which stress testing has not been integrated with risk management. Additionally, smaller banks may have resource constraints.

The reduced frequency of mandated company-run stress testing for bank subsidiaries with assets above $250 billion that are not subsidiaries of systemically important bank holding companies is also credit negative, although not to the same extent as the elimination of the requirement for the midsize banks. The longer time between bank management’s reviews of stress test results introduces a higher probability of changing economic conditions that could leave a firm with an insufficient capital cushion.

The Fed’s proposal also would eliminate the hypothetical adverse scenario from company-run stress tests and the Fed’s supervisory stress tests. The market has focused on the severely adverse scenario, which is harsher than the adverse scenario so this proposed change is unlikely to have significant consequence.

An alternative to the big banks already exists and it isn’t in neobanks according to the chief executive of a mutual bank, via InvestorDaily.

Heritage Bank chief executive Peter Lock said that neobanks did not offer anything new to the banking system.

“Forget the hype about neobanks. There’s nothing that digital banks

and neobanks offer that customer-owned institutions such as Heritage

Bank don’t already offer to people frustrated by the listed banks,” he

said.

Mr Lock said that mutuals were tried and tested institutions who had

market-leading technology and weren’t owned by investors looking to turn

a profit.

“Unlike many neobanks, mutuals aren’t owned by big investors looking

to make a profit. If you’re turning to them to escape the

profit-maximisation excesses of the big banks, then you should think

again.

Mr Lock said that mutuals offered a different mindset to listed banks as they did not have profit maximisation incentives.

“Regardless of their rhetoric, the listed banks face an inherent

conflict between the interests of their customers and the interests of

their shareholders. At the end of the day, the listed model exists to

serve their shareholders above all else, not customers,” he said.

However, APRA’s general manager of licensing Melisande Waterford

defended new entrants to the market during a panel last year where she

said neobanks offered something new.

“Neobanks have a completely different mindset and a different approach to providing a service,” she said.

This mindset has proven to be popular with consumers as well according to recent data from Nielsen.

Nielsen’s latest data found a five-percentage point increase over

twelve months of Australians looking to switch to a digital bank.

Not only are Australian’s looking to switch to digital banks but 75

per cent of digital bank customers would recommend their bank to others,

compared to just 45 per cent of the big four.

GlobalData’s head of banking content for Asia-Pacific Andrew Haslip

said that conditions in Australia were ripe for neobanks given the lack

of trust in the industry.

“‘The clutch of neobanks waiting in the wings in Australia will have

no better time to launch recruitment drives, while a range of

robo-advisors, none of which have yet broken out into the mainstream,

will have the best conditions yet to draw in new money,” he said.

Recently neobanks like Volt and Xinja have been granted restricted

ADI licenses, making them one step away from a full banking licence.

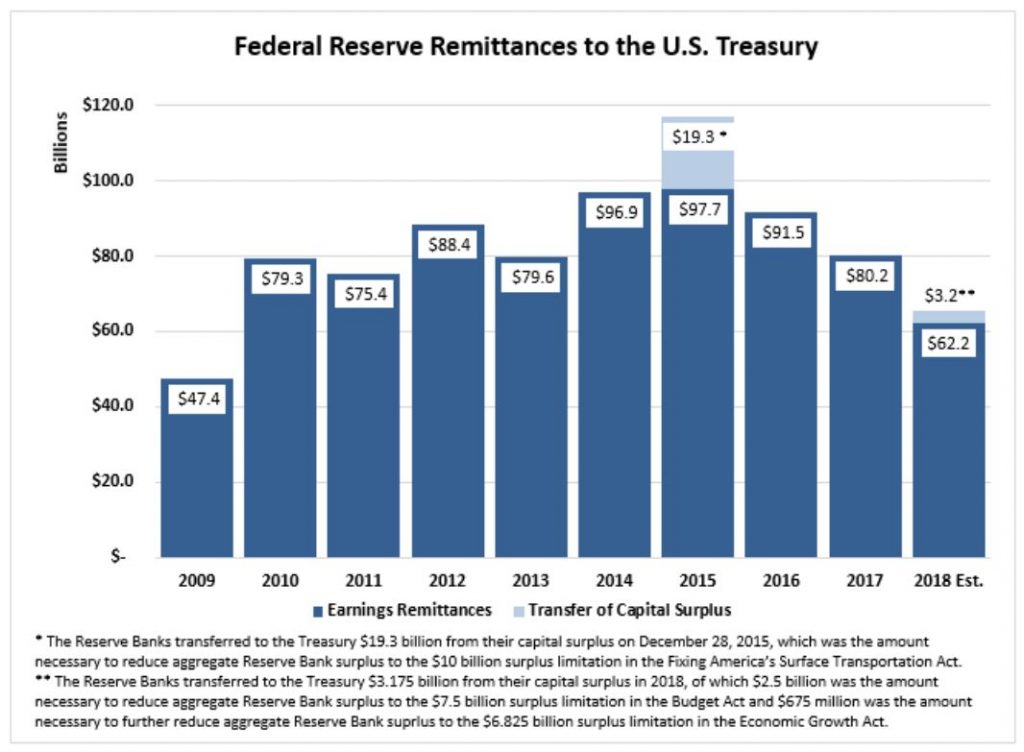

The Federal Reserve Board announced preliminary results indicating that the Reserve Banks provided for payments of approximately $65.4 billion of their estimated 2018 net income to the U.S. Treasury. The payments include two lump-sum payments totaling approximately $3.2 billion, necessary to reduce aggregate Reserve Bank capital surplus to $6.825 billion as required by the Bipartisan Budget Act of 2018 (Budget Act) and the Economic Growth, Regulatory Relief, and Consumer Protection Act (Economic Growth Act). The 2018 audited Reserve Bank financial statements are expected to be published in March and may include adjustments to these preliminary unaudited results.

The Federal Reserve Banks’ 2018 estimated net income of $63.1 billion

represents a decrease of $17.6 billion from 2017, primarily

attributable to an increase of $12.6 billion in interest expense

associated with reserve balances held by depository institutions. Net

income for 2018 was derived primarily from $112.3 billion in interest

income on securities acquired through open market operations–U.S.

Treasury securities, federal agency and government-sponsored enterprise

(GSE) mortgage-backed securities, and GSE debt securities. The Federal

Reserve Banks had interest expense of $38.5 billion primarily associated

with reserve balances held by depository institutions, and incurred

interest expense of $4.6 billion on securities sold under agreement to

repurchase.

Operating expenses of the Reserve Banks, net of amounts reimbursed by

the U.S. Treasury and other entities for services the Reserve Banks

provided as fiscal agents, totaled $4.3 billion in 2018.

In addition, the Reserve Banks were assessed $849 million for the

costs related to producing, issuing, and retiring currency, $838 million

for Board expenditures, and $337 million to fund the operations of the

Consumer Financial Protection Bureau. Additional earnings were derived

from income from services of $444 million. Statutory dividends totaled

$1 billion in 2018.

Another lender has repriced their back book, citing higher funding costs. “We have absorbed higher funding costs for the last twelve months in order to delay the impact for our home loan customers. Unfortunately, funding costs remain high and are likely to remain elevated into the foreseeable future.” It’s connected with the Bank of Queensland, who already lifted, of course.

As a result, Virgin Money has announced changes to its variable rates for all existing principal and interest (P&I) and interest only (IO) home loans, increasing rates by 20 basis points (bps).

However, the majority of standard variable rates for new home loan applications will remain unchanged, with only a few set to increase.

They also announced small reductions of between 5bps and 10bps for some new fixed rates products with an LVR below 90%.

So once again loyalty is NOT being rewarded.

The interest rate changes are effective Friday, 11 January 2019.