According to Moody’s, on 11 January, the Canadian government published a consultation paper on its previously announced open banking initiative to foster competition within its banking industry. The initiative will provide policy recommendations on how best to allow retail bank customers to share their financial transaction data with fintechs and other financial services providers such as small and mid-sized banks to facilitate application development so that retail clients can compare financial products and change bank accounts more easily.

The government initiative is credit negative for the largest Canadian banks’ retail operations because it has the potential to incrementally weaken the industry’s favorable industry structure of a few concentrated players, and therefore the banks’ retail franchise strength and associated high profitability.

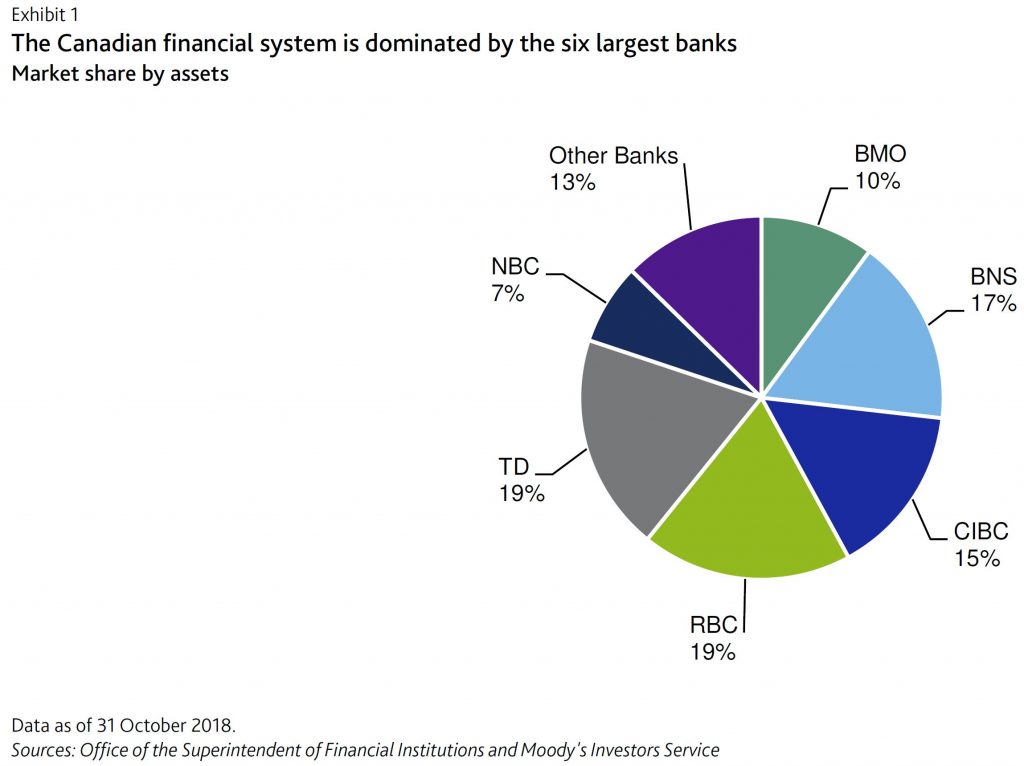

The largest Canadian banks are Bank of Montreal (BMO, Bank of Nova Scotia (BNS), Canadian Imperial Bank of Commerce (CIBC), Royal Bank of Canada (RBC), The Toronto-Dominion Bank (TD) and National Bank of Canada (NBC). As of 31 October 2018, these six banks held 87% of Canada’s banking assets.

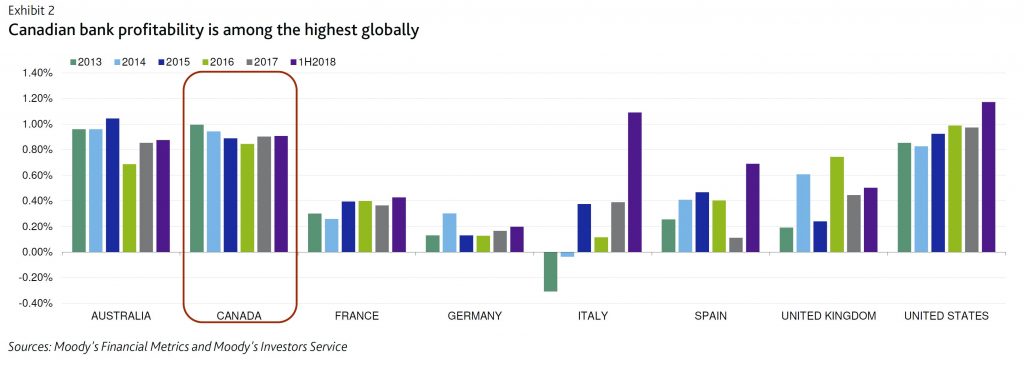

Canada’s banking system is highly concentrated and more profitable for the largest incumbents than in other banking jurisdictions.

Moody’s says “we believe the six largest banks have sufficient financial resources and fintech expertise to adapt to innovation in consumer banking. Nonetheless, technological disruption is likely to erode the incumbents’ profitability in certain retail lending products, such as credit cards, and/or payments over the long term as smaller, more agile banks achieve competitive advantages”.

In an article, released by the US FED via the first issue of Consumer & Community Context, they explore the impact that rising student loan debt levels may have on home ownership rates among young adults in the US. They suggest that higher debt overall helps to explain lower home ownership.

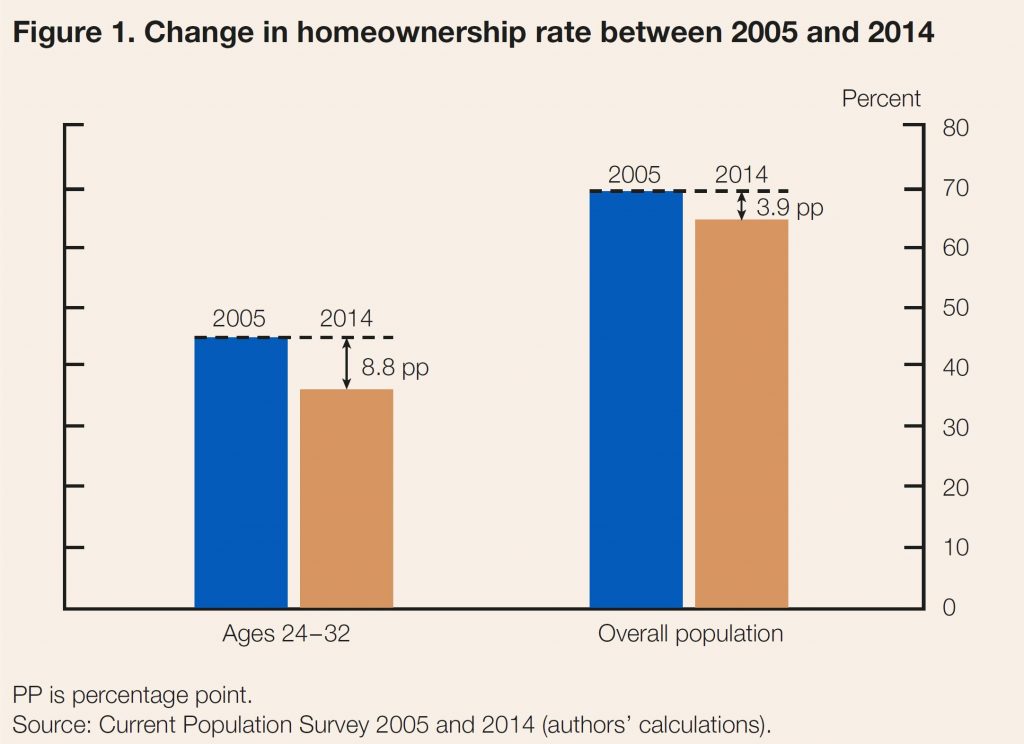

The home ownership rate in the United States fell approximately 4 percentage points in the wake of the financial crisis, from a peak of 69 percent in 2005 to 65 percent in 2014. The decline in home ownership was even more pronounced among young adults. Whereas 45 percent of household heads ages 24 to 32 in 2005 owned their own home, just 36 percent did in 2014—a marked 9 percentage point drop

While many factors have influenced the downward slide in the rate of home ownership, some believe that the historic levels of student loan debt have been particular impediments. Indeed, outstanding student loan balances have more than doubled in real terms (to about $1.5 trillion) in the last decade, with average real student loan debt per capita for individuals ages 24 to 32 rising from about $5,000 in 2005 to $10,000 in 2014.3 In surveys, young adults commonly report that their student loan debts are preventing them from buying a home.

They estimate that roughly 20 percent of the decline in home ownership among young adults can be attributed to their increased student loan debts since 2005. Our estimates suggest that increases in student loan debt are an important factor in explaining their lowered home ownership rates, but not the central cause of the decline.

Estimating the Effect of Student Loan Debt on Home ownership

The relationship between student loan debt and home ownership is complex. On the one hand, student loan payments may reduce an individual’s ability to save for a down payment or qualify for a mortgage. On the other hand, investments in higher education also, on average, result in higher earnings and lower rates of unemployment. As a result, it is not immediately clear whether, on balance, the impact of student loan debt on home ownership would be positive or negative.

Since we are interested in isolating the negative effect of increased student loan burdens on home ownership from the potential positive effect of additional education, our analysis aims to estimate the effect of debt on home ownership holding all other factors constant. In other words, if we were to compare two individuals who are otherwise identical in all aspects but the amount of accumulated student loan debt, how would we expect their home ownership outcomes to differ?

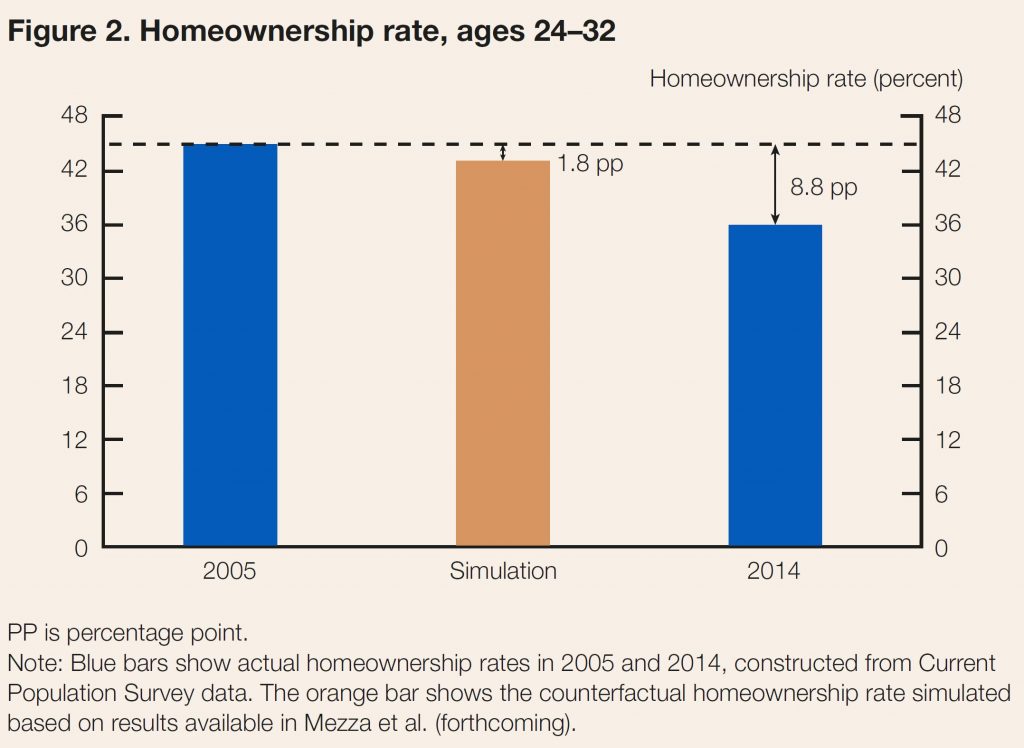

To estimate the effect of the increased student loan debt on home ownership, we tracked student loan and mortgage borrowing for individuals who were between 24 and 32 years old in 2005. Using these data, we constructed a model to estimate the impact of increased student loan borrowing on the likelihood of students becoming homeowners during this period of their lives. We found that a $1,000 increase in student loan debt (accumulated during the prime college-going years and measured in 2014 dollars) causes a 1 to 2 percentage point drop in the home ownership rate for student loan borrowers during their late 20s and early 30s. Our estimates suggest that student loan debt can be a meaningful barrier preventing young adults from owning a home. Next, we apply these estimates to another interesting question: How much of the 9 percentage point drop in the home ownership rate of 24 to 32 year olds between 2005 and 2014 can be attributed to rising student loan debt?

The Rise in Student Loan Debt and Decline in Home ownership since 2005 Answering this question requires two steps. First, we calculate an expected probability of home ownership in 2005 for each individual in our sample using the estimated model from our previous research. Second, we produce a simulated scenario for the probability of home ownership by increasing each individual’s debt to match the student loan debt distribution of this age group in 2014. The difference between the probabilities calculated in these two steps determines the effect of the increased debt on the home ownership rate of the young, holding demographic, educational, and economic characteristics fixed.

This exercise captures two key dimensions of the shifts in the distribution of student loan debt between 2005 and 2014, in addition to the overall increase in the average amounts borrowed. First, the fraction of young individuals who have borrowed to fund post secondary education with debt has increased by roughly 10 percentage points over this period, from 30 to 40 percent. Second, the amounts borrowed at the upper end of the distribution increased more rapidly than in the middle.

According to our calculations, the increase in student loan debt between 2005 and 2014 reduced the home ownership rate among young adults by 2 percentage points. The home ownership rate for this group fell 9 percentage points over this period (figure 2), implying that a little over 20 percent of the overall decline in home ownership among the young can be attributed to the rise in student loan debt. This represents over 400,000 young individuals who would have owned a home in 2014 had it not been for the rise in debt.

An important caveat to keep in mind when interpreting our estimates is the difference in mortgage market conditions before and after the financial crisis. The model used to develop these estimates was built using data for student loan borrowers who were between 24 and 32 years old in 2005, so a large fraction had made their home-buying decisions before 2008, when credit was relatively easier to obtain. Following the crisis, loan underwriting may have become more sensitive to student loan debt, increasing its importance in explaining declining home ownership rates.

Student Loan Debt May Have Even Broader Implications for Consumers

There are multiple channels by which student loans can affect the ability of consumers to buy homes. One we would like to highlight here is the effect of student loan debt on credit scores. In our forthcoming paper, we show that higher student loan debt early in life leads to a lower credit score later in life, all else equal. We also find that, all else equal, increased student loan debt causes borrowers to be more likely to default on their student loan debt, which has a major adverse effect on their credit scores, thereby impacting their ability to qualify for a mortgage.

This finding has implications well beyond home ownership, as credit scores impact consumers’ access to and cost of nearly all kinds of credit, including auto loans and credit cards. While investing in post secondary education continues to yield, on average, positive and substantial returns, burdensome student loan debt levels may be lessening these benefits. As policymakers evaluate ways to aid student borrowers, they may wish to consider policies that reduce the cost of tuition, such as greater state government investment in public institutions, and ease the burden of student loan payments, such as more expansive use of income-driven repayment.

IT Wire reports that New Zealand cryptocurrency exchange Cryptopia has suffered a breach and its operations have been locked down, with police saying that they are not yet in a position to indicate the quantum of the theft.

The company said in a notice on its site

that there had been “significant losses” but went no further, only

saying that “once identified, the exchange was put into maintenance

while we assessed damages”.

Cryptopia was set up in July 2014 and is based in Christchurch. It

has two directors, Adam Clark and Robert Dawson, according to Blockonomi, a site that covers cryptocurrencies, fintech and the blockchain economy.

The police statement said they were trying to establish what happened and how the site had been breached.

“A priority for police is to identify and, if possible, recover missing

funds for Cryptopia customers; however there are likely to be many

challenges to achieving this,” the statement said.

The website Crypto News cited

a tweet from the chief executive of Binance, another cryptocurrency

exchange, as saying some of the funds stolen from Cryptopia had been

frozen.

These funds had been moved to Binance by the individuals who carried out the hack.

The police statement said: “While police are unable to go into

details about specific steps being taken at this stage, we can say that

our focus includes commencing both a forensic digital investigation of

the company, and a physical scene examination at the building.

“We are dealing with a complex situation and we are unable to put a timeframe on how long the investigation may take.

“We are also aware of speculation in the online community about what

might have occurred. It is too early for us to draw any conclusions and

Police will keep an open mind on all possibilities while we gather the

information we need.”

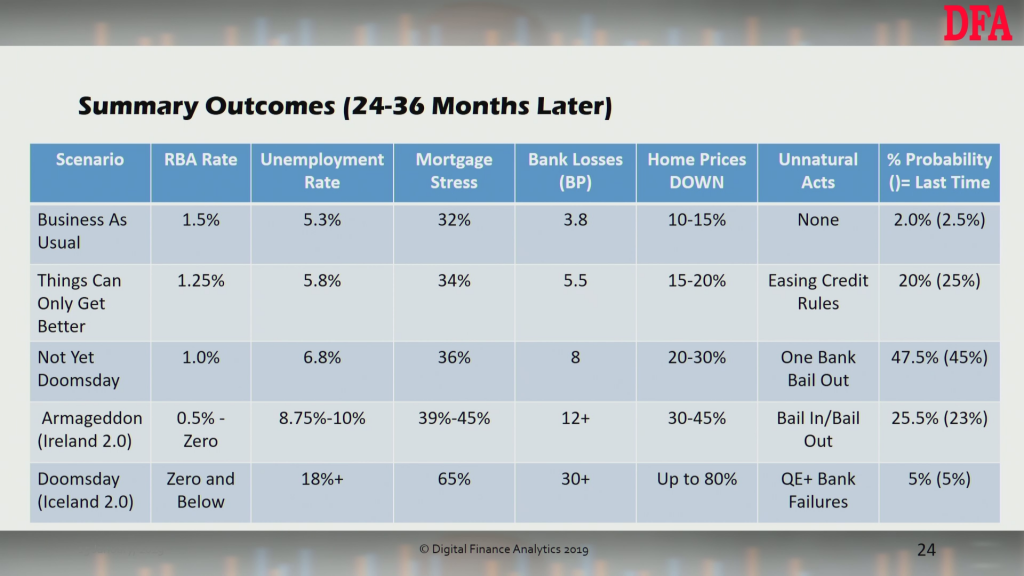

We have updated our scenarios to take account of potential RBA rate cuts later in the year, revised mortgage stress and household confidence data and other factors. We also updated our probability allocation. Here is a summary.

Our central scenario is one of home price fall, peak to trough, of up to 30%. A deeper fall, in the event of international financial stability is also possible. We do not think the RBA has any hope of lifting rates from current emergency levels, having dropped them too low previously.

We discussed these updates during yesterdays live stream Q&A event. Here is a high quality edited version.

You can also watch the recorded “live” version, including the chat replay here:

Another blowout in bank funding costs is adding to the pressure for an RBA rate cut, according to a leading forecaster, via InvestorDaily.

AMP Capital chief economist Shane Oliver is confident that the

Reserve Bank will be forced to cut the cash rate by 50 basis points to 1

per cent this year.

He explained that Australian economic data has been soft in recent

weeks with weak housing credit, sharp falls in home prices in December,

another plunge in residential building approvals pointing to falling

dwelling investment, continuing weakness in car sales, a loss of

momentum in job ads and vacancies and falls in business conditions for

December.

“Retail sales growth was good in November but is likely to slow as home prices continue to fall,” Mr Oliver said.

“Income tax cuts will help support consumer spending, but won’t be

enough so we remain of the view that the RBA will cut the cash rate to 1

per cent this year.”

Meanwhile, another spike in funding costs has seen a number of

lenders hike their mortgage rates in the first few weeks of 2019.

Bank of Queensland lifted rates by 18 basis points, while home loan

providers Virgin Money and HomesStart Finance have also announced

interest rate rises.

“The gap between the 3-month bank bill rate and the expected RBA cash

rate has blown out again to around 0.57 per cent compared to a norm of

around 0.23 per cent,” Mr Oliver said.

“As a result, some banks have started raising their variable mortgage

rates again. This is bad news for households seeing falling house

prices. The best way to offset this is for the RBA to cut the cash rate

as it drives around 65 per cent of bank funding.”

Digital Finance Analytics principal Martin North believes even small

rate rises could see more households pushed into mortgage stress and

increase the risk of default among those already under pressure to meet

their monthly repayments.

“The other point is that it will actually tip more borrowers into

severe stress, that’s when you’ve got a serious monthly deficit. That’s

the leading indicator for default 18 months down the track,” he said.

The second wave of out-of-cycle mortgage rate hikes has continued, with another lender announcing increases of up to 20 basis points, via The Adviser.

NAB-owned

lender UBank has announced that it has increased interest rates on its

fixed rate investor home loan products by 20 basis points, effective for

new loans issued as of 14 January.

The lender’s investor mortgage rate increases are as follows:

A rise of 20bps on its 1-year UHomeLoan fixed rate with interest-only terms, from 3.99 per cent to 4.19 per cent

A rise of 20bps on its 3-year UHomeLoan fixed rate with interest-only terms, from 3.99 per cent to 4.19 per cent

A rise of 20bps on its 5-year UHomeLoan fixed rate with interest-only terms, from 4.49 per cent to 4.69 per cent

UBank is the latest lender to increase its home loan rates, after the Bank of Queensland (BOQ) and Virgin Money announced rate increase of up to 18bps and 20bps, respectively.

Both BOQ and Virgin Money attributed their decisions to lift home loan rates to the sustained rise in wholesale funding costs.

Speaking

to The Adviser’s sister publication, Mortgage Business, principal of

Digital Finance Analytics (DFA) Martin North said that he expects mortgage stress to continue mounting in the short to medium term, particularly off the back of out-of-cycle interest rate hikes.

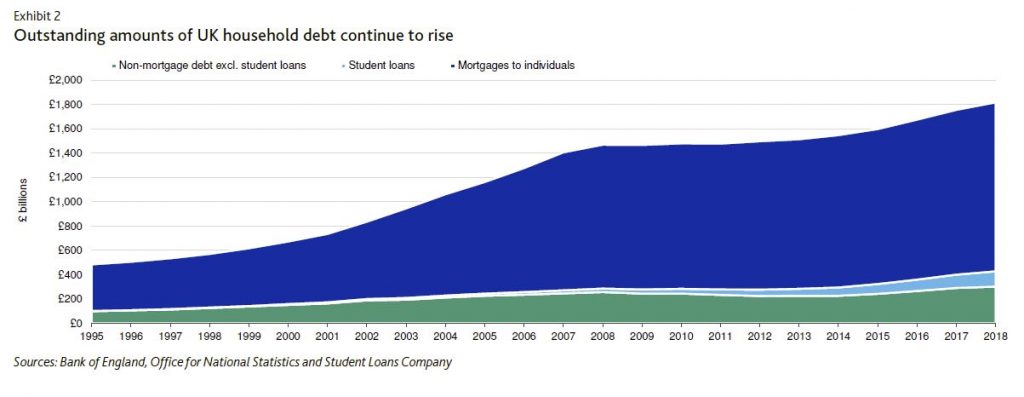

According to Moody’s, on 7 January, UK trade unions published their annual report, which warned about a credit crisis as UK average non-mortgage household debt jumped above £15,000, almost 50% higher than before the 2008 financial crisis. The increase in household debt leaves borrowers vulnerable to sudden economic stress, such as that which might crystallise in a no-deal Brexit scenario. An incremental increase in unemployment would have negative consequences for highly leveraged consumers. Higher joblessness, reduced real wages and, to a lesser extent, lower refinancing availability would increase delinquencies and defaults in consumer loan pools backing residential mortgage-backed securities (RMBS) and asset-backed securities (ABS).

Additionally, softening house prices can exacerbate the negative effect of rising defaults on RMBS. In case of a severe economic stress, the macroeconomic outlook for the UK would weaken, leading to a decline in house prices nationwide, which would have a mixed effect regionally across the UK. We expect more negative consequence in regions with higher unemployment and in industries that are more materially affected by such a stress scenario. However, we expect that any deceleration in house prices will be less severe than during the 2008-09 financial crisis given less inflationary stresses within the market. The performance of buy-to-let (BTL) and nonconforming transactions would weaken, especially for some recently originated collateral pools that have assets with relatively weaker underwriting standards. The performance of credit card ABS collateral would also deteriorate, especially for those pools with more exposure to highly leveraged obligors.

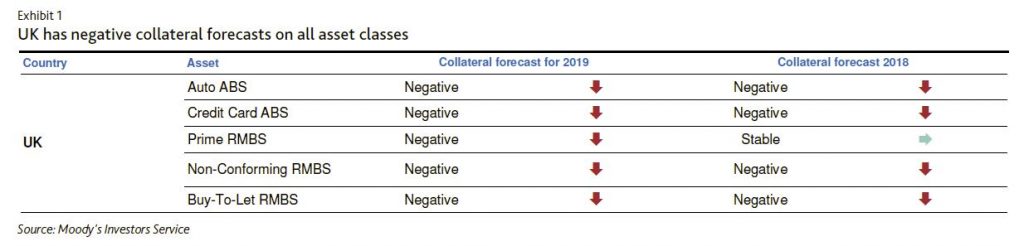

We have negative collateral forecasts for all UK consumer sectors

Our forecasts are negative for all UK consumer sector collateral. Our collateral performance forecasts over the next 12-18 months address the direction of expected losses for the market in general, not specific collateral pools among the deals we rate.

In normal circumstances, the absolute level of household debt is not necessarily as important as affordability measures such as the ratio of payment or loan to disposable income. Given the low interest rate environment, affordability is still relatively high for UK borrowers. However, sudden economic stress that leads to negative real wage growth and increasing unemployment has the potential to change matters.

The average household debt figure in the trade union’s analysis is based on data from Bank of England, Office for National Statistics and the Student Loans Company. It excludes mortgages but includes everything else (i.e., credit cards, personal loans, payday loans and student loans), which deviates from the Bank of England’s definition of non-mortgage household debt.

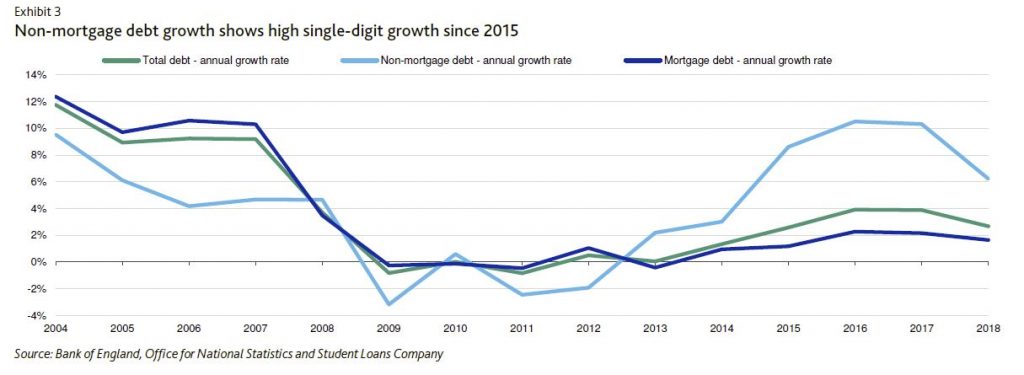

The rapid growth of non-mortgage (mainly unsecured) debt has contributed to household debt since 2013 after years of constrained credit in the aftermath of the 2008 financial crisis. The growth patterns of mortgage and non-mortgage debt have switched gears compared with pre-crisis patterns: non-mortgage debt (e.g., credit cards and consumer loans) have had a high single-digit growth rate since 2015, with slightly slowing growth in 2018 to a level of 6%, whereas pre-crisis, mortgage debt had these high growth rates. The 2018 data shows that UK households had average non-mortgage debt of approximately £10,000, even excluding student loans, and this is in line with levels reported in 2008.

On 9 January, Moody’s says, the Federal Reserve Board (Fed) proposed revisions to company-run stress testing requirements for Fed-regulated US banks to conform with the Economic Growth, Regulatory Relief, and Consumer Protection Act (the EGRRCPA), which became law in May 2018.

Among the revisions, which are similar to those proposed in December 2018 by the Office of the Comptroller of the Currency (OCC) and the Federal Deposit Insurance Corp. (FDIC), is a proposal that would eliminate the requirement for company-run stress tests at most bank subsidiaries with total consolidated assets of less than $250 billion. The proposed changes would be credit negative for affected US banks because they would ease the minimum requirements for stress testing at the subsidiary level.

The proposed revisions would also require company-run stress tests once every other year instead of annually at most banks with more than $250 billion in total assets that are not subsidiaries of systemically important bank holding companies. Additionally, the proposal would eliminate the hypothetical adverse scenario from all company-run stress tests and from the Fed’s own supervisory stress tests, commonly known as the Dodd-Frank Stress Test (DFAST) and the Comprehensive Capital Analysis and Review (CCAR); the baseline and severely adverse scenarios would remain.

The proposed changes aim to implement EGRRCPA. As such, we expect that they will be adopted with minimal revisions. In late December 2018, the FDIC and OCC published similar proposals governing the banks they regulate. The stress testing requirements imposed on US banks over the past decade have helped improve US banks’ risk management practices and have led banks to incorporate risk management considerations more fully into both their strategic planning and daily decision making. Without periodic stress tests, these US banks may have more flexibility to reduce their capital cushions, making them more vulnerable in an economic

downturn.

On 31 October 2018, the Fed announced a similar proposal for the company-run stress tests conducted by bank holding companies as a part of a broader proposal to tailor its enhanced supervisory framework for large bank holding companies. Positively, the Fed’s 31 October 2018 proposal would still subject bank holding companies with total assets of $100-$250 billion to supervisory stress testing at least every two years and would still require them to submit annual capital plans to the Fed, even though the latest proposal would no longer require their bank subsidiaries to conduct their own company-run stress tests. Also, supervisory stress testing for larger holding companies would continue to be conducted annually. Continued supervisory stress testing should limit any potential reduction

in capital cushions at those bank holding companies.

We believe that some midsize banks will continue to use company-run stress testing in some form, but more tailored to their own needs and assumptions. Nevertheless, this may not be the view of all banks, particularly those for which stress testing has not been integrated with risk management. Additionally, smaller banks may have resource constraints.

The reduced frequency of mandated company-run stress testing for bank subsidiaries with assets above $250 billion that are not subsidiaries of systemically important bank holding companies is also credit negative, although not to the same extent as the elimination of the requirement for the midsize banks. The longer time between bank management’s reviews of stress test results introduces a higher probability of changing economic conditions that could leave a firm with an insufficient capital cushion.

The Fed’s proposal also would eliminate the hypothetical adverse scenario from company-run stress tests and the Fed’s supervisory stress tests. The market has focused on the severely adverse scenario, which is harsher than the adverse scenario so this proposed change is unlikely to have significant consequence.

An alternative to the big banks already exists and it isn’t in neobanks according to the chief executive of a mutual bank, via InvestorDaily.

Heritage Bank chief executive Peter Lock said that neobanks did not offer anything new to the banking system.

“Forget the hype about neobanks. There’s nothing that digital banks

and neobanks offer that customer-owned institutions such as Heritage

Bank don’t already offer to people frustrated by the listed banks,” he

said.

Mr Lock said that mutuals were tried and tested institutions who had

market-leading technology and weren’t owned by investors looking to turn

a profit.

“Unlike many neobanks, mutuals aren’t owned by big investors looking

to make a profit. If you’re turning to them to escape the

profit-maximisation excesses of the big banks, then you should think

again.

Mr Lock said that mutuals offered a different mindset to listed banks as they did not have profit maximisation incentives.

“Regardless of their rhetoric, the listed banks face an inherent

conflict between the interests of their customers and the interests of

their shareholders. At the end of the day, the listed model exists to

serve their shareholders above all else, not customers,” he said.

However, APRA’s general manager of licensing Melisande Waterford

defended new entrants to the market during a panel last year where she

said neobanks offered something new.

“Neobanks have a completely different mindset and a different approach to providing a service,” she said.

This mindset has proven to be popular with consumers as well according to recent data from Nielsen.

Nielsen’s latest data found a five-percentage point increase over

twelve months of Australians looking to switch to a digital bank.

Not only are Australian’s looking to switch to digital banks but 75

per cent of digital bank customers would recommend their bank to others,

compared to just 45 per cent of the big four.

GlobalData’s head of banking content for Asia-Pacific Andrew Haslip

said that conditions in Australia were ripe for neobanks given the lack

of trust in the industry.

“‘The clutch of neobanks waiting in the wings in Australia will have

no better time to launch recruitment drives, while a range of

robo-advisors, none of which have yet broken out into the mainstream,

will have the best conditions yet to draw in new money,” he said.

Recently neobanks like Volt and Xinja have been granted restricted

ADI licenses, making them one step away from a full banking licence.