Bank of Queensland has announced it will be increasing interest rates across its variable home loans and Lines of Credit for owner occupiers and investors.

We expect other banks to follow, as they are all sitting on the same funding cost volcano.

BOQ said that the variable home loan rate for owner occupiers (principal and interest repayments) will increase by 0.09 per cent, per annum; variable home loan rate for owner occupiers (interest only repayments) will increase by 0.15 per cent, per annum; variable home loan rate for investors (principal and interest and interest only repayments) will increase by 0.15 per cent, per annum; and Owner occupier and investor Lines of Credit will increase by 0.10 per cent, per annum.

Anthony Rose, Acting Group Executive, Retail Banking said today’s announcement is largely due to the increased cost of funding.

“Funding costs have significantly risen since February this year and have primarily been driven by an increase in 30 and 90 day BBSW rates, along with elevated competition for term deposits.

“While the bank has absorbed these costs for some time, the changes announced today will help to offset the ongoing impact of the increased funding costs.

“These decisions are always difficult and BOQ balances the needs of our borrowers and depositors when making changes,” Mr Rose said.

The interest rate changes are effective Monday, 2 July 2018.

The appointment of Mr Lowe as Chair of the CGFS is for a term of three years, starting immediately. He succeeds William C Dudley, CGFS Chair since January 2012. Mr Dudley retired from his position as President and Chief Executive Officer of the Federal Reserve Bank of New York on 17 June 2018. The GEM Governors expressed their gratitude to Mr Dudley for his leadership during his time as Chair and wish Mr Lowe every success in his new role.

Mr Lowe has been Governor of the RBA since September 2016. He joined the Bank in 1980, and previously held the positions of Deputy Governor, Assistant Governor (Economic) and Assistant Governor (Financial System). Mr Lowe is a member of the Financial Stability Board. He also spent two years at the Bank for International Settlements working on financial stability issues.

The CGFS is a central bank forum for the monitoring and analysis of broad financial system issues. It supports central banks in the fulfilment of their responsibilities for monetary and financial stability by contributing appropriate policy recommendations.

The Banker’s Bank, in their annual report confirmed that there is evidence that some banks are massaging their quarter end results to fit within certain capital ratios using Repurchase Agreements (REPO’s). So Central banks’ own financial operations with bank counterparties are making a mockery of any macroprudential regulation attempts by central banks … plain alarming!

Several years ago we showed how the Fed’s then-new Reverse Repo operation had quickly transformed into nothing more than a quarter-end “window dressing” operation for major banks, seeking to make their balance sheets appear healthier and more stable for regulatory purposes.

And this is a snapshot of what the reverse-repo usage looked like back in late 2014:

Today, in its latest Annual Economic Report, some 4 years after our original allegations, the Bank for International Settlements has confirmed that banks may indeed be “disguising” their borrowings “in a way similar to that used by Lehman Brothers” as debt ratios fall within limits imposed by regulators just four times a year, thank to the use of repo arrangements.

For those unfamiliar, the BIS explains that window-dressing refers to the practice of adjusting balance sheets around regular reporting dates, such as year- or quarter-ends and notes that “window-dressing can reflect attempts to optimise a firm’s profit and loss for taxation purposes.”

For banks, however, it may also reflect responses to regulatory requirements, especially if combined with end-period reporting. One example is the Basel III leverage ratio. This ratio is reported based on quarter-end figures in some jurisdictions, but is calculated based on daily averages during the quarter in others. The former case can provide strong incentives to compress exposures around regulatory reporting dates – particularly at year-ends, when incentives are reinforced by other factors (eg taxation).”

But why repo? Because, as a form of collateralised borrowing, repos allow banks to obtain short-term funding against some of their assets – a balance sheet-expanding operation. The cash received can then be onlent via reverse repos, and the corresponding collateral may be used for further borrowing. At quarter-ends, banks can reverse the increase in their balance sheet by closing part of their reverse repo contracts and using the cash thus obtained to repay repos. This compression raises their reported leverage ratio, massaging their assets lower, and boosting leverage ratios, allowing banks to report them as being in line with regulatory requirements.

So what did the BIS finally find? Here is the condemning punchline which was obvious to most back in 2014:

“The data indicate that window-dressing in repo markets is material”

The report continues:

Data from U.S. money market mutual funds point to pronounced cyclical patterns in banks’ U.S. dollar repo borrowing, especially for jurisdictions with leverage ratio reporting based on quarter-end figures (Graph III.A, left-hand panel). Since early 2015, with the beginning of Basel III leverage ratio disclosure, the amplitude of swings in euro area banks’ repo volumes has been rising – with total contractions by major banks up from about $35 billion to more than $145 billion at year-ends. Banks’ temporary withdrawal from repo markets is also apparent from MMMFs’ increased quarter-end presence in the Federal Reserve’s reverse repo (RRP) operations, which allows them to place excess cash (right-hand panel, black line).

This is problematic because this central-bank endorsed mechanism “reduces the prudential usefulness of the leverage ratio, which may end up being met only four times a year.” Furthermore, the BIS alleged that in addition to its negative effects on financial stability, the use of repos to game the requirement hinders access to the market for those who need it at quarter end and obstructs monetary policy implementation.

This is hardly a new development, and as we explained in 2014, one particular bank was notorious for its use of similar sleight of hand: as Bloomberg writes, the use of repo borrowings is similar to a “Lehman-style trick” in which the doomed bank used repos to disguise its borrowings “before it imploded in 2008 in the biggest-ever U.S. bankruptcy.”

The collapse prompted regulators to close an accounting loophole the firm had wriggled through to mask its debts and to introduce a leverage ratio globally.

How ironic, then, that it is central banks’ own financial operations with bank counterparties, that make a mockery of any macroprudential regulation attempts by central banks, and effectively exacerbate the problems in the financial system by implicitly allowing banks to continue masking the true extent of their debt.

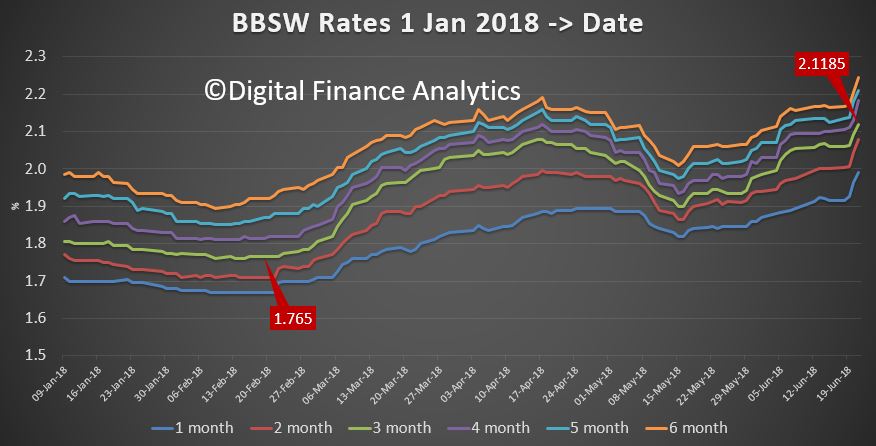

The benchmark BBSW rate has moved higher again, with the 3 month series now at a high of 2.1185; up ~36 basis points from February.

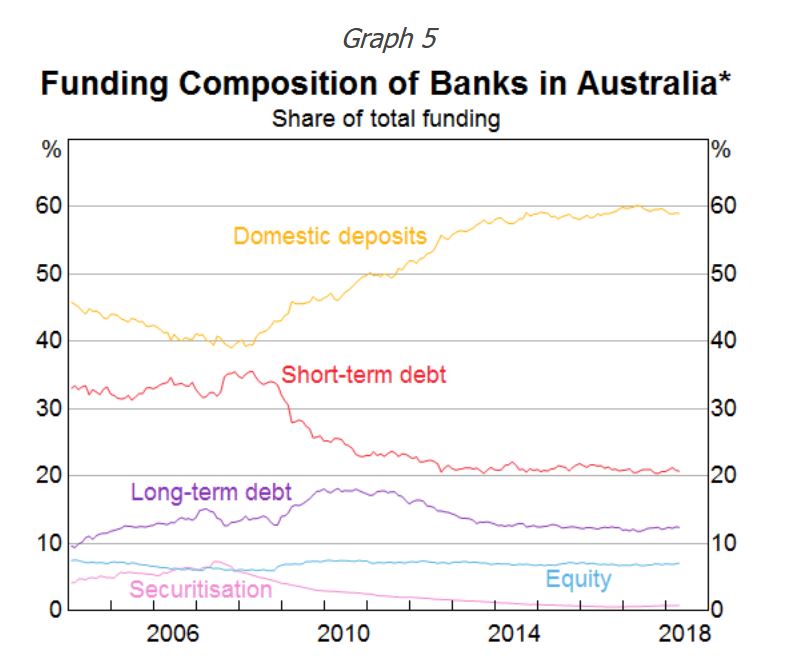

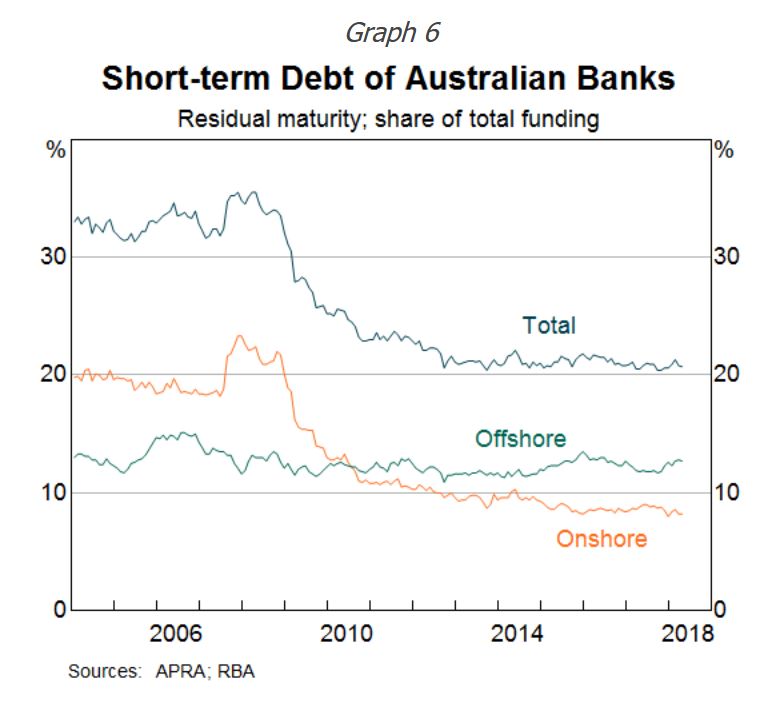

We know that around 20% of bank funding is from short term sources, according to the RBA.

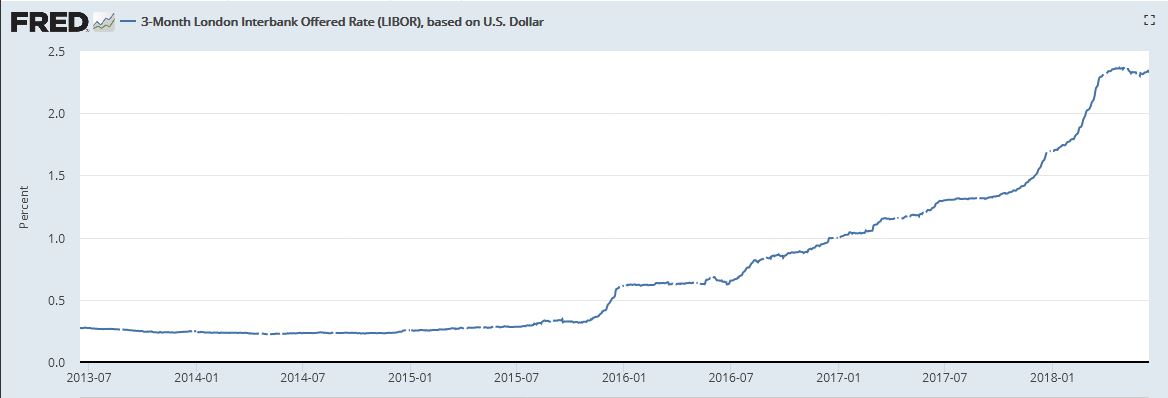

Of that, more is sourced offshore than onshore. Both overseas rates – as typified by the US LIBOR …

… and the local BBSW rates as we looked at before, suggest a hike in mortgage rates is coming. In fact more smaller lenders quietly lifted their rates last week, following Suncorp, ME Bank and others.

IMB Bank said from 22 June, its standard variable interest rate will increase by 0.08 per cent for new and existing home loan customers and Auswide has also lifted with increases of five basis points (0.05%) for owner occupied home loans and thirteen basis points (0.13%) for investment home loans and residential lines of credit, effective 27th June.

Unless the majors follow suite, expect their profits to drop, and returns of bank deposit to fall further.

As banks continue to tighten their home lending policies in response to regulatory pressure and the negative press surrounding the royal commission, Australia’s top brokers are finding it increasingly difficult to help their clients; via The Adviser.

ANZ has become the latest lender to tweak its credit policy for home loan borrowers. Late on Friday, the major bank notified aggregators that it has made changes to minimum living expense values.

It is now common for lenders to ask for 29 fields of expenses when assessing a mortgage application. Some banks that previously required no bank statements from applicants are now asking for up to six months’ worth of transaction account information to verify living expenses.

In many instances where banks find that an applicant’s living expenses for a certain item are higher than declared, brokers must go back over their client’s records to explain “one-off” expenses to the lender, such as a renovation cost or an overseas holiday. This process is creating significant delays in the settlement process.

Some of the industry’s most successful brokers have told The Adviser that the environment has become extremely tough, but most believe the credit squeeze will be short-lived.

“As a broker running a business that settles over $200 million a year, we don’t normally get declined by lenders,” one award-winning broker told The Adviser. “But I’m getting declined now.”

Refinancing has become particularly difficult in the current climate, with many borrowers failing to switch to a different lender and a better rate.

Last week, The Adviser ran an editorial that highlighted how Australia, like the UK, is beginning to see a number of “mortgage prisoners” shackled to home loans as a result of tighter credit policies and increased regulation.

One broker told The Adviser that he has started repricing loans for clients through their existing bank when they are unable to refinance.

“I’m doing a lot of that. I go back to the lender and negotiate a better rate. There is nothing in it for me in terms of remuneration, but the customer is getting a better deal,” the broker said

Research from consumer education website, CreditSmart, has found that many of us hold misconceptions about what goes into our credit report, and what credit providers look for when checking a credit report.

The CreditSmart website is owned by the Australian Retail Credit Association (ARCA), which is the peak body for organisations involved in the disclosure, exchange and application of credit reporting data in Australia. ARCA’s members are the most significant credit providers including the four major banks, credit reporting bodies (CRBs), specialist consumer finance companies, and marketplace lenders. A list of companies that support the CreditSmart education campaign is listed below.

They say that almost nine in ten Australians (88%) understand that banks and lenders check their credit report when they apply for a loan or credit.

Mike Laing, CEO and Chairman of ARCA, which founded CreditSmart, said that, unfortunately, too many people in Australia misunderstand their credit report and the information it contains.

“Accessing credit is part of everyday life and yet alarmingly, most consumers are unaware of the information included in their credit report. Your credit report will influence whether your application for credit or a loan is approved as your credit report forms part of a credit provider’s assessment of your application for credit or a loan,” said Mr Laing.

The research, undertaken by YouGov Galaxy, was done ahead of the upcoming changes to the credit reporting system. Known as comprehensive credit reporting (CCR), from July 2018, the four major banks will be required to share 50% of customers’ data with lenders, to ensure a complete picture.

What does my credit report include?

A huge 63% of Aussies believe how much money they make is included in their credit report. Further, 40% think the balance on their savings account is also on their credit report.

“Your income and bank balance isn’t included in your credit report. When you apply for credit or a loan, the lender will ask you about your income, expenses and your financial assets, as all of this is taken into consideration, but it will not come from your credit report.

“You could have a lot of savings in the bank, but a bad credit report because you were careless about paying your financial accounts on time”, said Mr Laing.

Separately, more than half of Australians believe that gender and marital status are included in their credit report, and one-third think that their place of birth and car insurance claims are also shown. All of these are incorrect.

A further 63% of consumers thought their credit report already shows whether or not they make their monthly credit card and loan payments on time. This is a change that is only starting to happen now as part of CCR.

According to CreditSmart, a credit report is made up of:

Identifying information (e.g. name, address, date of birth, employment and driver’s licence number)

Information about the credit accounts you have and, for credit cards, personal loans, mortgages or car loans, your repayment history on these accounts over the last two years

Credit applications over the last five years

Default information (if any) over the last five years (payments at least 60 days overdue)

Personal insolvency information and serious credit infringements (if any) for up to seven years

Who can access my credit report?

While most of us know that a bank or lender will look at our credit report when we apply for a loan, many are unaware that our credit report can be checked when we apply to open a new gas or electricity account (46%) or contract a mobile phone (46%).

“Most credit providers, which can include gas, electricity and phone providers, will carry out a credit check to find out how you’ve handled your debts in the past – something to keep in mind,” said Mr Laing.

Your credit report can’t be accessed when you apply for a job or take out or make a claim on insurance, which is not well known by Australians.

According to CreditSmart, your credit report will likely be requested from a credit reporting body by a credit provider when you:

Apply for a loan from a bank (or any other finance provider)

Apply for a store card (e.g. when you buy a TV on interest free finance)

Rent items like a TV, fridge or computer, but not home rental

Apply for a car loan

Buy a mobile phone on a post-paid mobile plan

Sign up for a phone, gas or electricity account

Checking your credit report frequently

Mr Laing stresses the importance of checking your credit report annually.

“A popular misconception is that checking your credit report can negatively impact your credit score, but that is not true. As a security measure your credit report will show who has looked at your credit report, including you, but this is done to protect your privacy and is not shown to a credit provider when you apply for a loan.

“Every consumer should check their credit report annually. Monitoring your credit health regularly – like your physical health – lets you confirm you’re managing your credit well and are able to access credit when you need to,” concluded Mr Laing.

For more information on how to get your free credit reports, and to understand what is on them or fix any errors, consumers should go to http://www.creditsmart.org.au website, set up by credit experts to provide clear information on the credit reporting system to assist consumers to optimise their credit health.

Companies that support the CreditSmart education campaign include:

ANZ

Bankwest

Bendigo and Adelaide Bank/ Delphi Bank

BOQ

Citi

Commonwealth Bank

Compuscan

Credit Savvy

Credit Simple

CUA

Customs Bank

Experian

Firefighters Mutual

Bank/Teachers Mutual Bank

Genworth

GetCreditScore

Good Shepherd Microfinance

HSBC

Keypoint Law

Macquarie

ME Bank

MoneyMe

MoneyPlace

NAB

Now Finance

Pepper Money

Police Bank

QBE

SocietyOne

Suncorp

Toyota Finance/Hino Financial Services/Lexus Financial Services/Power Torque Financial Services

Unibank

Westpac/ Bank of Melbourne/ BankSA/ StGeorge/ RAMS

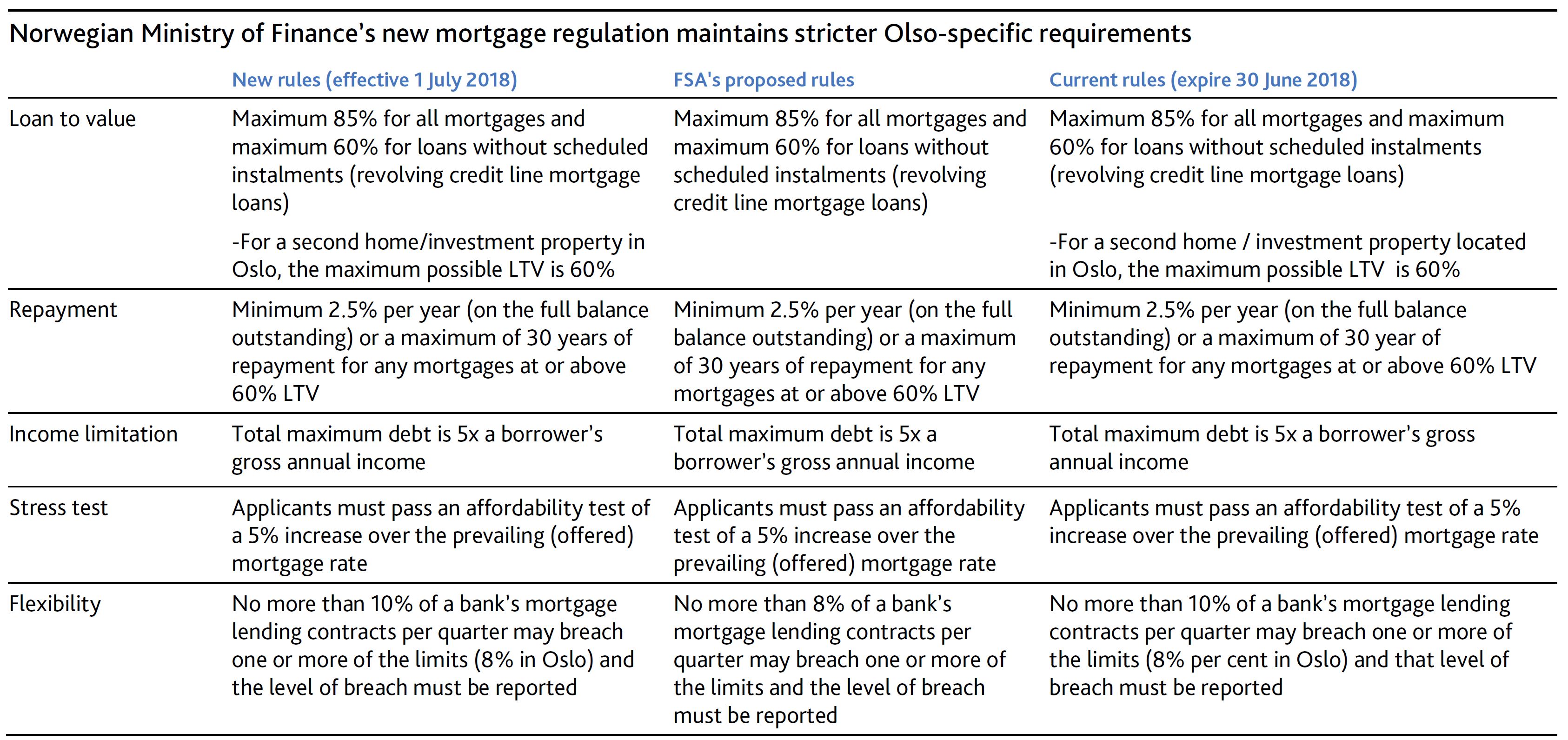

Household debt in Australia is around 190%, which is high by any standard, but Norway wins the award for the most indebted households at 224% and this is a structural risk for Norway’s Banks. So its interesting to compare the measures taken there with Australian regulation, which appears to be several years behind the pace….

Last Tuesday, the Norwegian Ministry of Finance extended until 31 December 2019 its strict regulations on mortgage underwriting standards, introduced in January 2017 and scheduled to expire on 30 June 2018. In addition, the ministry decided to maintain the stricter Oslo-specific measures regarding loan-to-value (LTV) ratios on secondary homes of 60%, rejecting the Norwegian Financial Services Authority’s (FSA) March 2018 proposal to remove the Oslo-specific measures.

Extending these measures past their scheduled expiration will dampen house price inflation and contain borrower leverage, a structural risk for Norway’s banks, both credit positive says Moody’s.

The proposal maintains the maximum LTV for home equity credit lines at 60%, the 85% LTV cap on mortgages, and the limit on borrowers’ aggregate debt at 5x gross annual income. It caps the portion of mortgages that do not comply with the national applicable LTV ratio limit at 10%. However, the ministry decided against the FSA’s suggestion of eliminating the existing LTV limit of 60% for secondary homes located in Oslo as well as applying nationwide the Oslo-specific cap on the portion of mortgages non-compliant with the LTV ratio of 8% (see exhibit). By maintaining the 8% cap on the portion of non-compliant mortgages only in Oslo and not extending it nationwide, the ministry has reduced the possibility that exceptions to the LTV rule for national lending would become concentrated in Oslo, a credit positive for cover pools that have concentrations in Oslo loans.

Norwegian banks are retail focused, with mortgages accounting for almost 50% of their total lending. The extension of the regulation until December 2019 is a step toward improving mortgage underwriting standards by containing borrower leverage. Household debt reached a record 224% of disposable income in December 2017, far above that of other Nordic countries, and we expect it to remain close to those levels over the next 12-18 months. Substantial household debt remains a structural risk for Norway’s banks. However, a preliminary analysis by Norway’s central bank has shown that the introduction of a maximum debt-to-income ratio requirement in 2017 has resulted in lower debt growth, particularly in municipalities with a high share of highly leveraged homebuyers.

The ministry’s extension of the regulation will also support the quality of mortgage loans in the cover pools of Norwegian covered bonds by suppressing LTV ratios and reducing the risk of cover pool losses as a result of borrower defaults and falling house prices. Requirements on loan amortization also support reduction of LTV ratios in more seasoned loans, although many cover pools continue to have material levels of interest-only loans and flexi loans that have delayed amortisation provisions.

Maintaining Oslo-specific measures in combination with our expectation of interest rate hikes will limit retail credit growth in the Oslo metropolitan area, particularly as it relates to investment properties and highly leveraged individuals. We expect DNB Bank ASA, which has the largest share of Oslo’s retail market, to be most affected by the extension.

During 2018, house prices have grown 4.5% after falling 4.2% in 2017 from a peak in March 2017. However, the extension of stricter underwriting measures along with our expectation of higher interest rates after seven years of cuts and the completed construction of a large number of new dwellings by this fall will likely restrain house price inflation over the next 12-18 months.

Cyber risk has emerged as a significant threat to the financial system according to the IMFBlog. An IMF staff modeling exercise estimates that average annual losses to financial institutions from cyber-attacks could reach a few hundred billion dollars a year, eroding bank profits and potentially threatening financial stability.

Recent cases show that the threat is real. Successful attacks have already resulted in data breaches in which thieves gained access to confidential information, and fraud, such as the theft of $500 million from the Coincheck cryptocurrency exchange. And there is the threat that a targeted institution could be left unable to operate.

Not surprisingly, surveys consistently show that risk managers and other executives at financial institutions worry most about cyber-attacks, as in the graphic below.

Financial sector’s vulnerability

The financial sector is particularly vulnerable to cyber-attacks. These institutions are attractive targets because of their crucial role in intermediating funds. A successful cyber-attack on one institution could spread rapidly through the highly interconnected financial system. Many institutions still use older systems that might not be resilient to cyber-attacks. And a successful cyber-attack can have direct material consequences through financial losses as well as indirect costs such as diminished reputation.

Recent high-profile cases have increasingly put cyber risk on the agenda of the official sector—including international organizations. However, quantitative analysis of cyber risk is still at an early stage, especially due to the lack of data on the cost of cyber-attacks, and difficulties in modeling cyber risk.

Cyber risk has emerged as a significant threat to the financial system.

A recent IMF study provides a framework for thinking about potential losses due to cyber-attacks with a focus on the financial sector.

Estimating potential losses

The modeling framework uses techniques from actuarial science and operational risk measurement to estimate aggregate losses from cyber-attacks. This requires an assessment of the frequency of cyber-attacks on financial institutions and an idea of the distribution of losses from such events. Numerical simulations can then be used to estimate the distribution of aggregate cyber-attack losses.

We illustrate our framework using a data set covering recent losses due to cyber-attacks in 50 countries. This provides an example of how potential losses for financial institutions could be estimated. The exercise is difficult and is made even more challenging by major data gaps on cyber risk. Moreover, thankfully, there has yet been no successful, large-scale cyber-attack on the financial system.

Our results should thus be considered as illustrative. Taken at face value, they suggest that average annual potential losses from cyber-attacks may be large, close to 9 percent of banks’ net income globally, or around $100 billion. In a severe scenario—in which the frequency of cyber-attacks would be twice as high as in the past with greater contagion— losses could be 2½–3½ times as high as this, or $270 billion to $350 billion.

The framework could be used to examine extreme risk scenarios involving massive attacks. The distribution of the data we have collected suggests that in such scenarios, representing the worst 5 percent of cases, average potential losses could reach as high as half of banks’ net income, putting the financial sector at risk.

Such estimated losses are several orders of magnitude greater than the present size of the cyber insurance market. Despite recent growth, the insurance market for cyber risk remains small with around $3 billion in premiums globally in 2017. Most financial institutions do not even carry cyber insurance. Coverage is limited, and insurers face challenges in evaluating risk because of uncertainty about cyber exposures, lack of data, and possible contagion effects.

The way forward

There is much scope to improve risk assessments. Government collection of more granular, consistent, and complete data on the frequency and impact of cyber-attacks would help assess risk for the financial sector.

Requirements to report breaches—such as considered under the EU’s General Data Protection Regulation—should improve knowledge of cyber-attacks. Scenario analysis could be used to develop a comprehensive assessment of how cyber-attacks could spread and design adequate responses by private institutions and governments.

Further work is needed also to understand how to strengthen the resilience of financial institutions and infrastructures, both to reduce the odds of a successful cyber-attack but also to facilitate smooth and rapid recovery. There is also a need to build capacity in the official sector in many parts of the world to monitor and regulate such risks.

In sum, strengthening the regulatory and supervisory frameworks for cyber risk is needed, and efforts should focus on effective supervisory practices, realistic vulnerability and recovery testing, and contingency planning. The IMF is providing technical assistance to help member countries improve their regulatory and supervisory frameworks.

ASIC chairman James Shipton is asking the government for additional funds to embed his staff within the major banks, but he is wary of the risk of ‘regulatory capture’; via InvestorDaily.

At a public hearing of the House of Representative Economics Committee on Friday, Liberal MP Trevor Evans asked ASIC chairman James Shipton about an ASIC proposal to ‘embed’ its agents within financial institutions.

Under the proposal, ASIC staff would monitor the culture and compliance of the major banks from within rather than at legalistic “arm’s length” – a proposal Mr Evans endorsed.

“It’s a style of collaboration which would be less legalistic, quicker and much more efficient in the use of regulator resources instead of arm’s-length legal tussles,” Mr Evans said.

“It would hopefully, with the cooperation of a lot of businesses, tease out the noncompliance that sits there in a non-deliberate, minor, systemic sort of way,” he said.

In response, Mr Shipton acknowledged ASIC has approached Treasury about the matter, saying there is a “productive conversation” underway.

The ASIC chairman said that by embedding his staff in the major banks, the regulator’s supervisory teams would become “more knowledgeable and understanding of particular institutions” and have a more “real-time” assessment of emerging risks – both financial and non-financial.

“We will be better able to be honest and speak back the same language the financial institution uses so as to get effective change,” Mr Shipton said.

However, the ‘embedding’ idea does not come without its risks, he said – primarily among them the notion of ‘regulatory capture’, whereby ASIC staff could become complicit in the poor cultural or compliance practices of an institution.

“We have been very mindful of the experiences of overseas supervisors in this regard,” Mr Shipton said.

“There are a number of lessons to be learned and to be aware of such as the risk of regulatory capture, which I am very mindful of,” he said.

The Liberal MP questioned whether ASIC required extra funding to carry out an ‘embedded’ function.

“This could be core regulatory business and I think that ASIC already does have all the powers and authorities to enter into agreements and MOUs with businesses,” Mr Evans said.

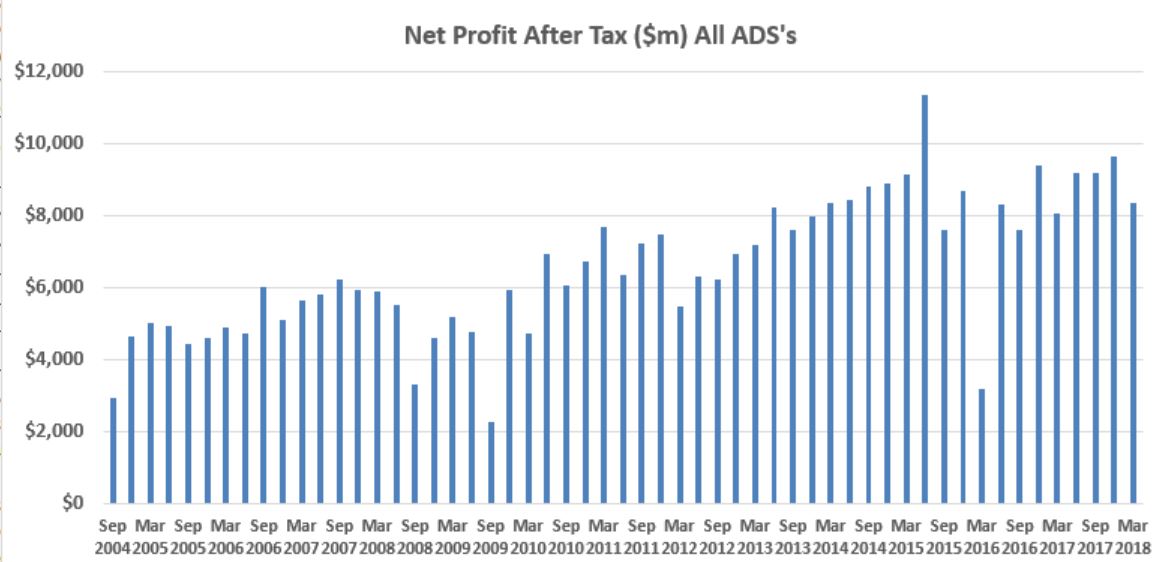

In summary the total profits were up 9.1% compared with a year ago, total assets grew 3% over the same period, the capital base grew 5.8%, the capital adequacy rose 0.4 percentage points and the liquidity coverage ratio rose 8.3 percentage points.

So superficially, all the ratios suggest a tightly run ship. But it is worth looking in more detail at these statistics, because as we will see below the waterline, things look less pristine.

First, there were 148 Authorised Depository Institutions (ADI’s) a.k.a banks at the end of March.

Endeavour Mutual Bank Ltd changed its name from Select Encompass Credit Union Ltd, with effect from 9 February 2018.

Gateway Bank Ltd changed its name from Gateway Credit Union Ltd, with effect from 1 March 2018.

My Credit Union Limited had its authority to carry on banking business in Australia revoked, with effect from 1 March 2018.

So the net number rose by 1 from December 2017.

In terms of overall performance, APRA says that the net profit after tax for all ADIs was $36.4 billion for the year ending 31 March 2018. This is an increase of $3.0 billion or 9.1 per cent on the year ending 31 March 2017.

This was because of a nice hike in mortgage margins, in reaction to the regulator’s intervention in the investor mortgage sector, and a significant drop in overall provisions. But top line revenue growth slowed and margins have started to tighten. As a result, profits were lower this quarter compared with the prior three quarters.

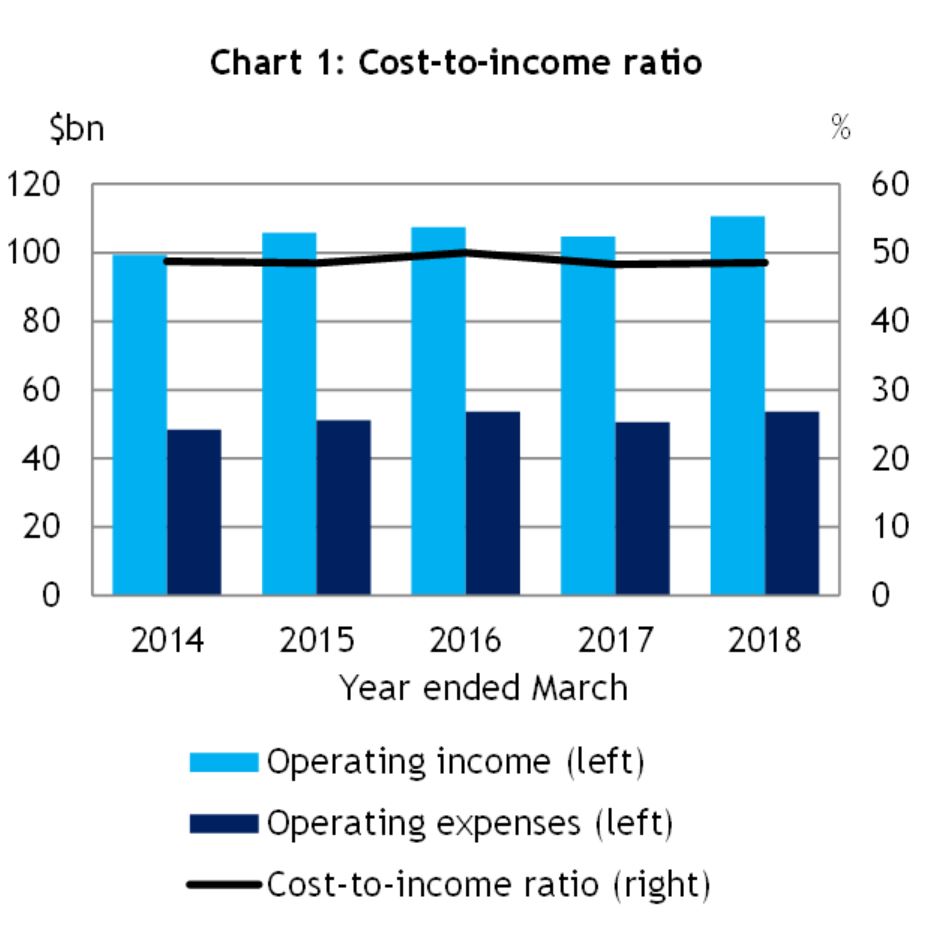

The cost-to-income ratio for all ADIs was 48.5 per cent for the year ending 31 March 2018, compared to 48.2 per cent for the year ending 31 March 2017. In other words, the costs of the business grew faster than income.

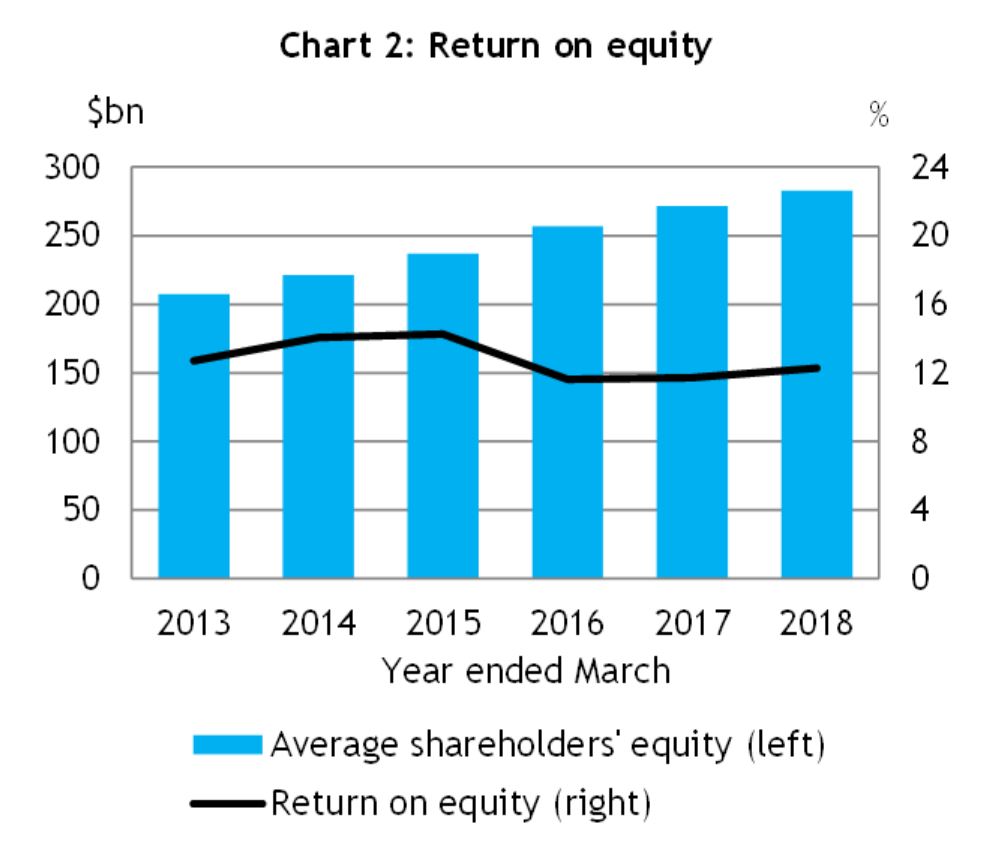

The return on equity for all ADIs increased to 12.3 per cent for the year ending 31 March 2018, compared to 11.7 per cent for the year ending 31 March 2017. We suspect this increase will not be repeated in the coming year.

That said an ROE of 12.3 per cent would still put the banking sector near the top of both Australian companies and global banks, reflecting a lack of true competition and some poor practices as laid bare by the Royal Commission. The quest for profit growth from some players has proved to be at the cost of customers. If banks do become more customer focussed, it is possible ROE’s will fall, and one-off penalties and fees (for example CBA, ANZ) will also hit returns.

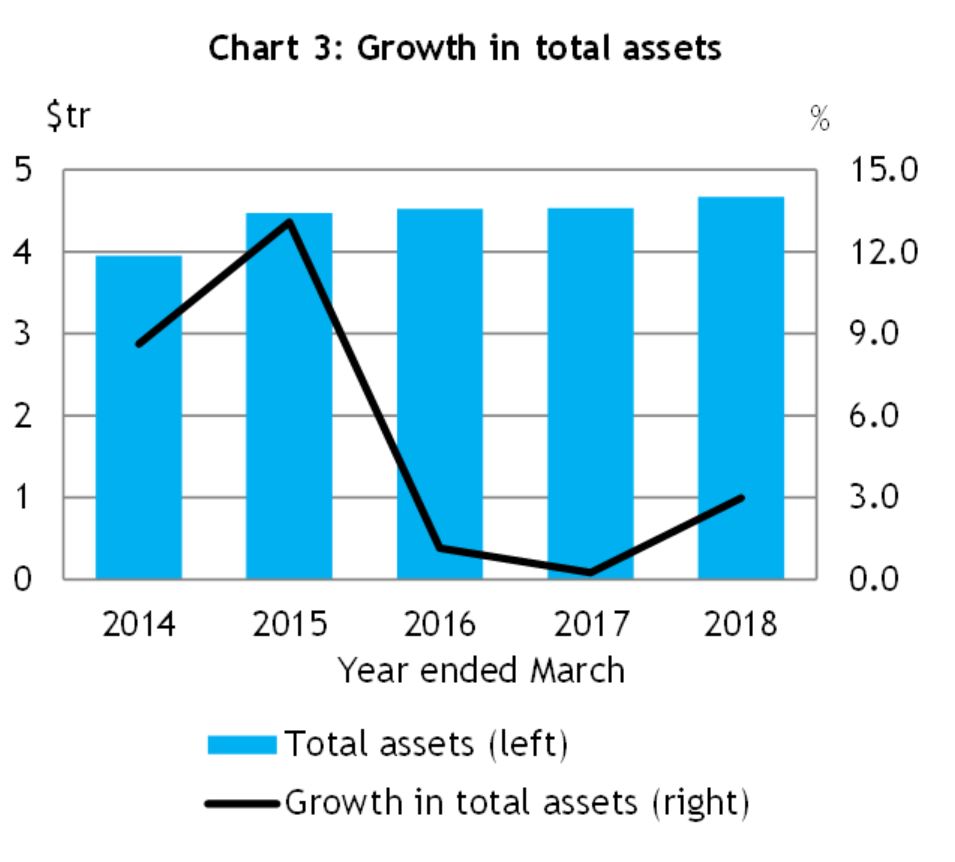

The total assets for all ADIs was $4.67 trillion at 31 March 2018. This is an increase of $135.9 billion (3.0 per cent) on 31 March 2017 and was largely driven by mortgages which grew strongly over the period.

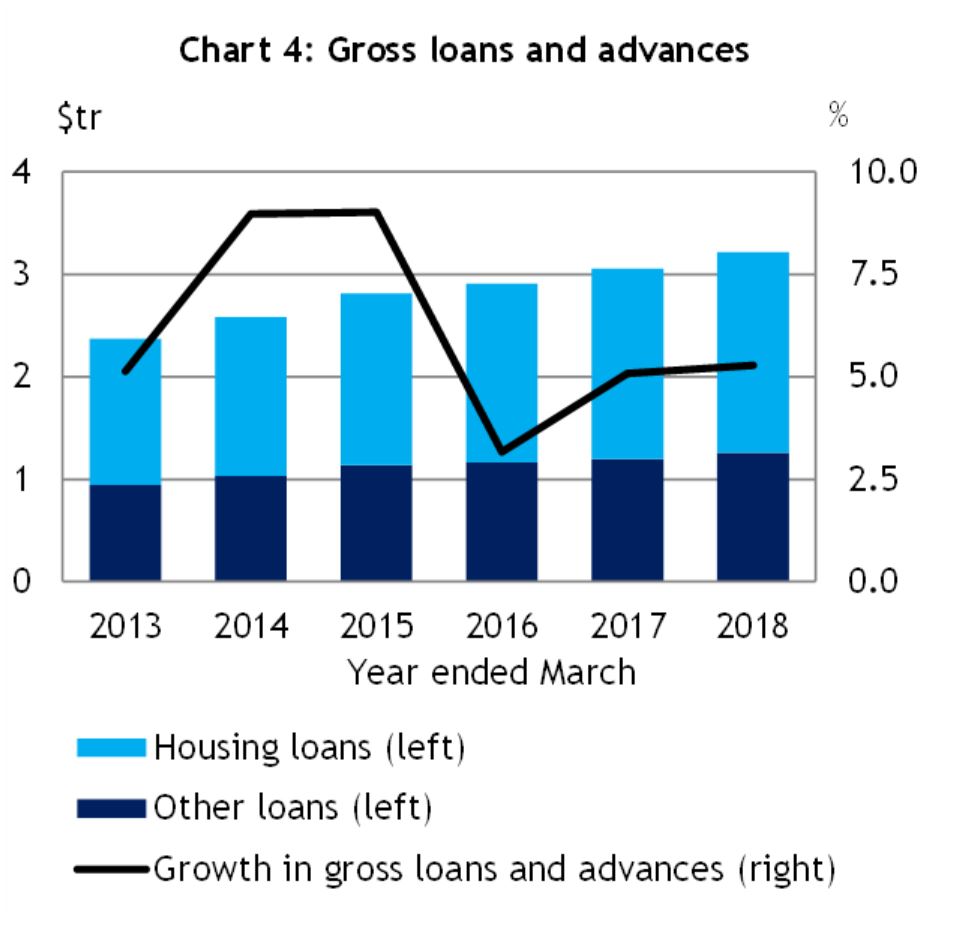

The total gross loans and advances for all ADIs was $3.22 trillion as at 31 March 2018. This is an increase of $161.4 billion (5.3 per cent) on 31 March 2017.

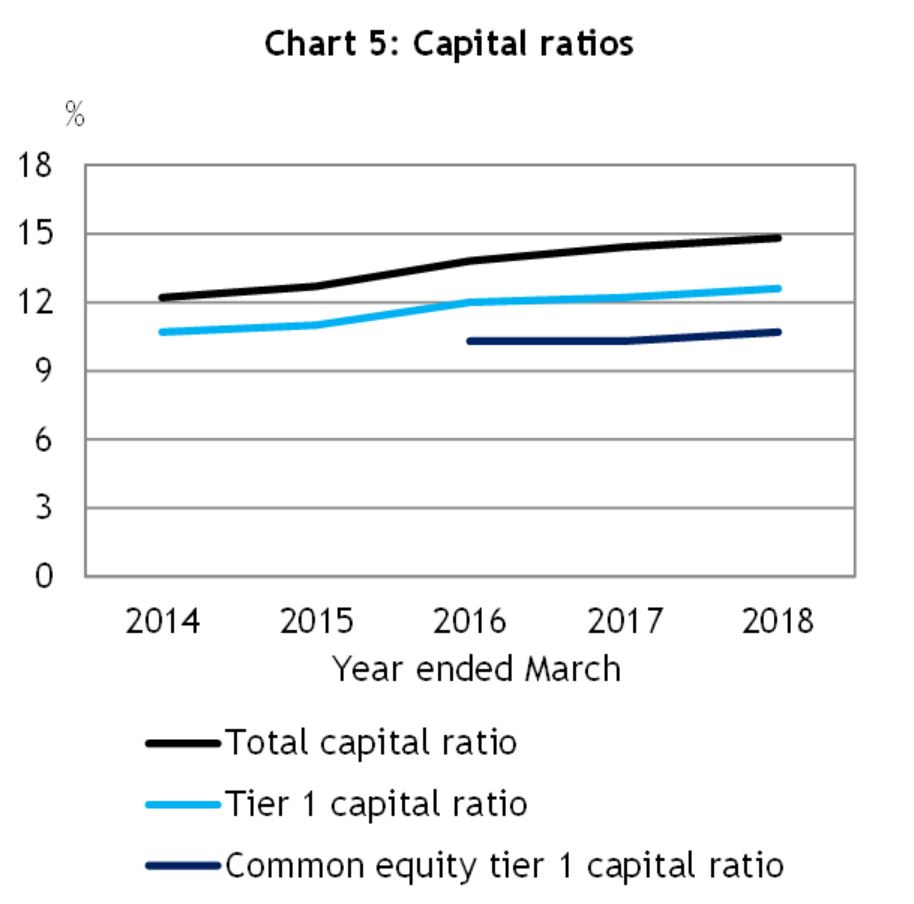

The total capital ratio for all ADIs was 14.8 per cent at 31 March 2018 , an increase from 14.4 per cent on 31 March 2017. This is a reflection of higher APRA targets. The common equity tier 1 ratio for all ADIs was 10.7 per cent at 31 March 2018, an increase from 10.3 per cent on 31 March 2017.

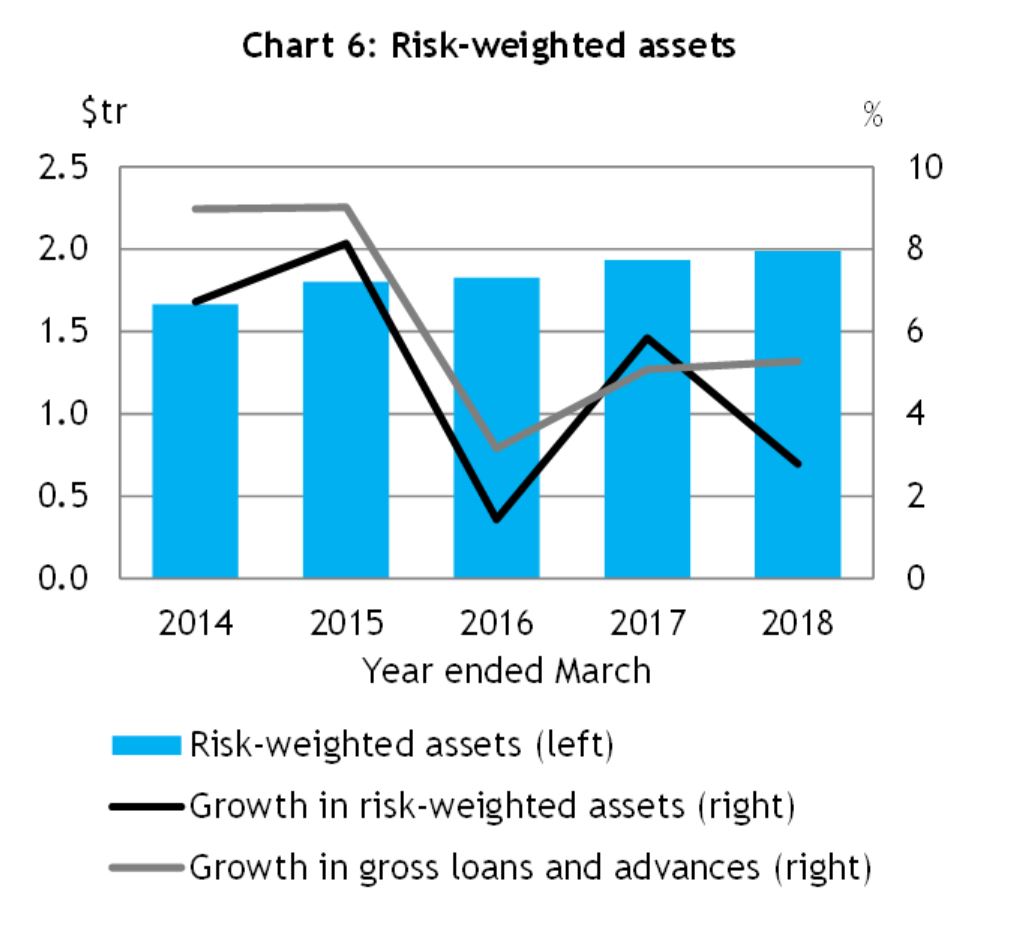

The risk-weighted assets (RWA) for all ADIs was $1.99 trillion at 31 March 2018, an increase of $53.9 billion (2.8 per cent) on 31 March 2017.

So if you compare the $3.22 trillion assets with the $1.99 trillion weighted assets for capital purposes, you can see the impact of lower risk weights for some asset types.

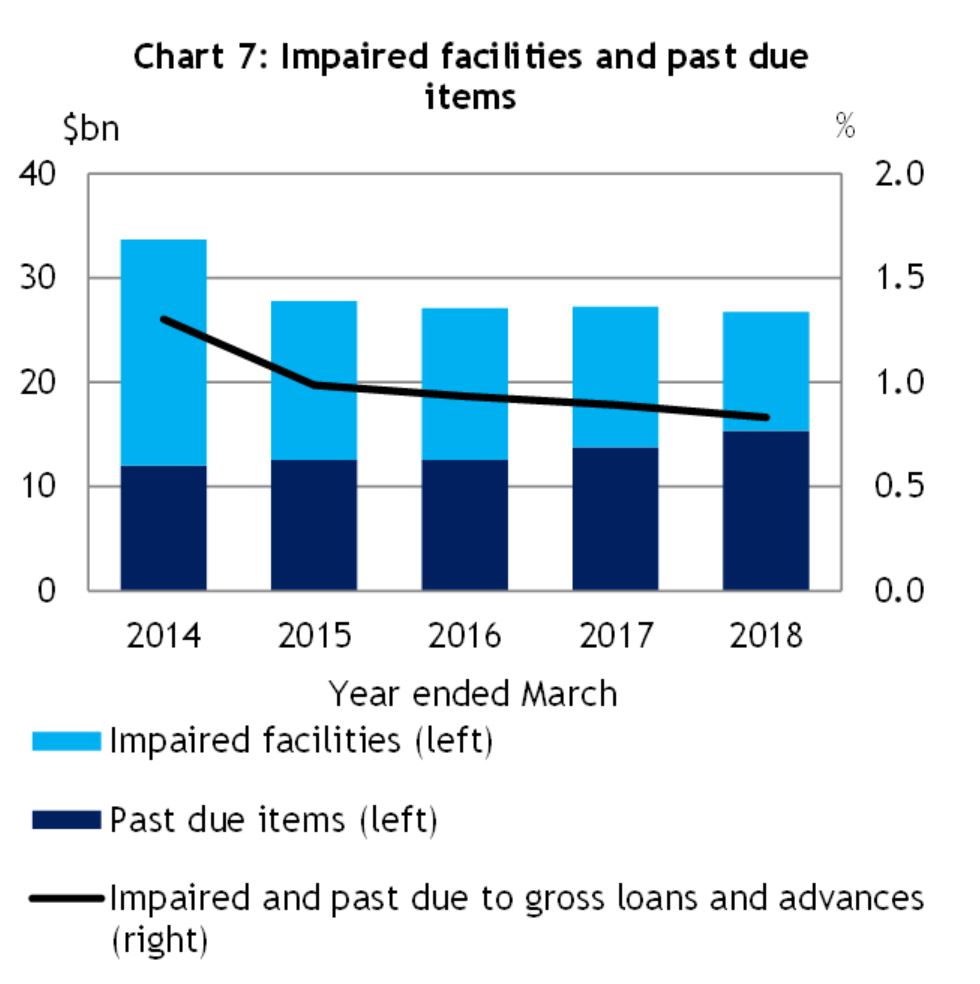

Looking at impairments for all ADIs we see that impaired facilities were $11.4 billion as at 31 March 2018. This is a decrease of $2.1 billion (15.7 per cent) on 31 March 2017.

Past due items were $15.4 billion as at 31 March 2018. This is an increase of $1.6 billion (11.5 per cent) on 31 March 2017. Rising 90 day delinquencies for mortgage loans was the main reason for the uplift, despite commercial loans performing a little better. Expect more delinquencies ahead, as indicated by our mortgage stress analysis. See our post “Mortgage Stress On the Rise”

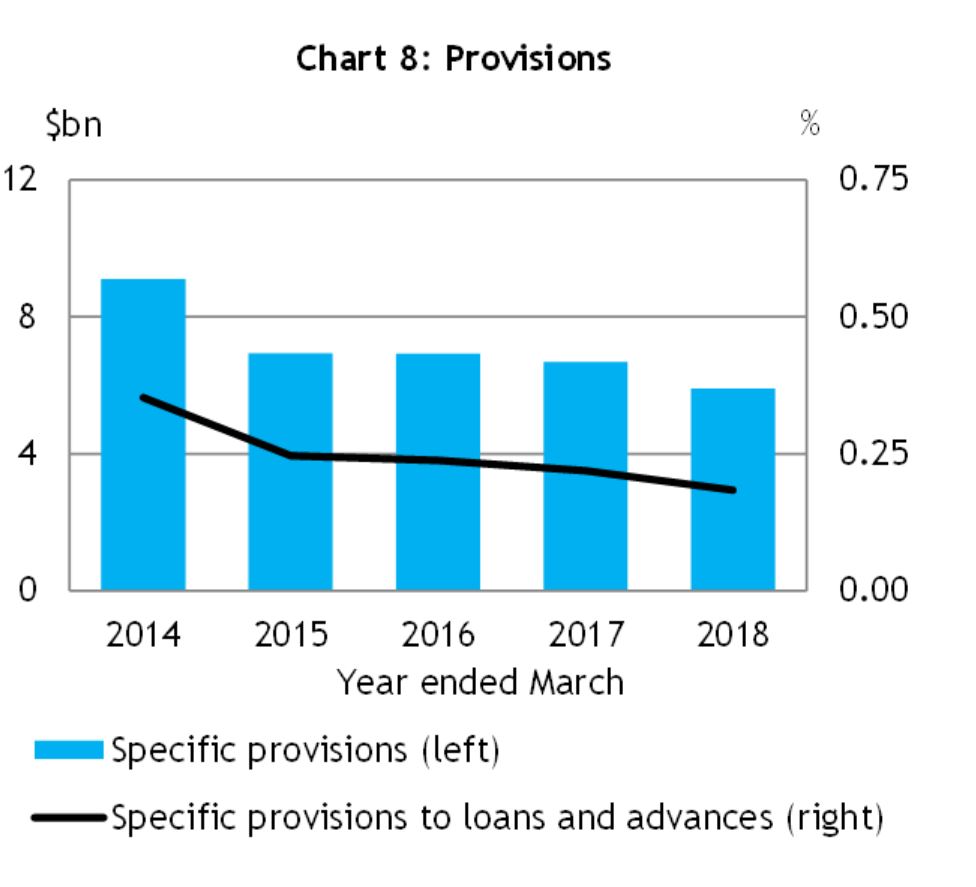

That said, impaired facilities and past due items as a proportion of gross loans and advances was 0.83 per cent at 31 March 2018, a decrease from 0.89 per cent at 31 March 2017 and specific provisions were $5.9 billion at 31 March 2018. This is a decrease of $0.8 billion (11.7 per cent) on 31 March 2017. In addition, specific provisions as a proportion of gross loans and advances was 0.18 per cent at 31 March 2018, a decrease from 0.22 per cent at 31 March 2017.

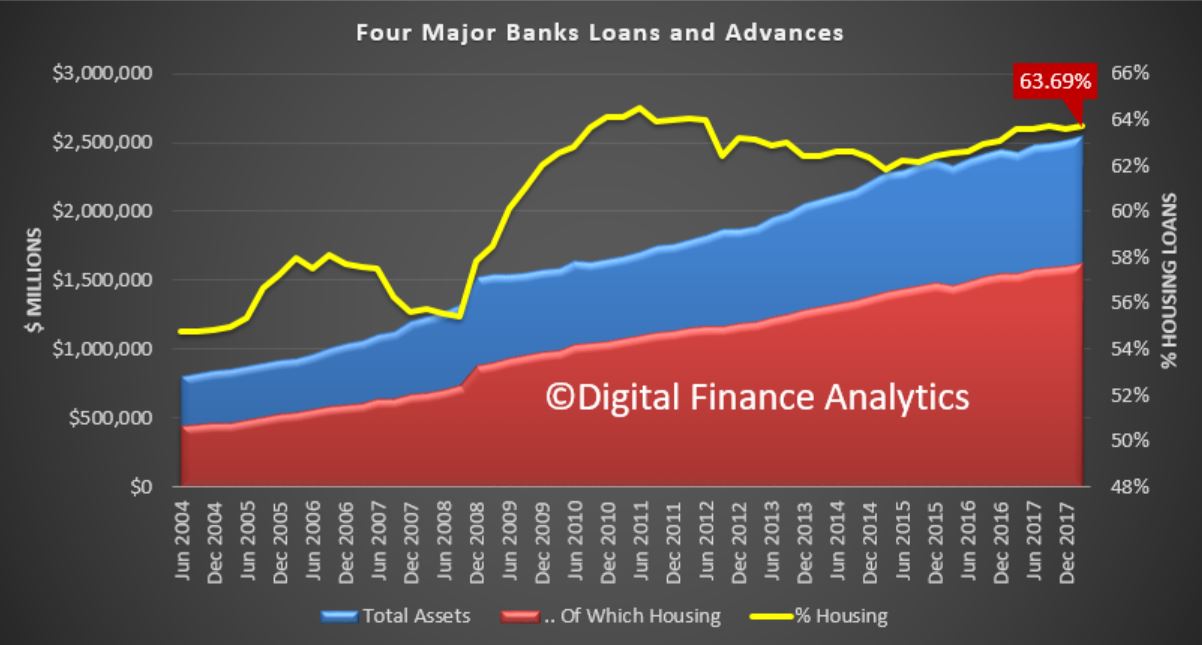

But there were two really important observations in the data, when we look at just the big four. The first is that total loans and advances by the four majors reached $2.55 trillion dollars, a record, and 63.69% of all loans were for housing lending. Not since 2012 has this been such a high proportion, its previous peak was 64.48% in the Jun 2011 quarter. The proportion of investor loans fell slightly, thanks to the recent tightening, but owner occupied lending by the big four remained strong. Think about it, nearly 64% of all loans are property related, so consider what a significant fall in prices would mean for them.

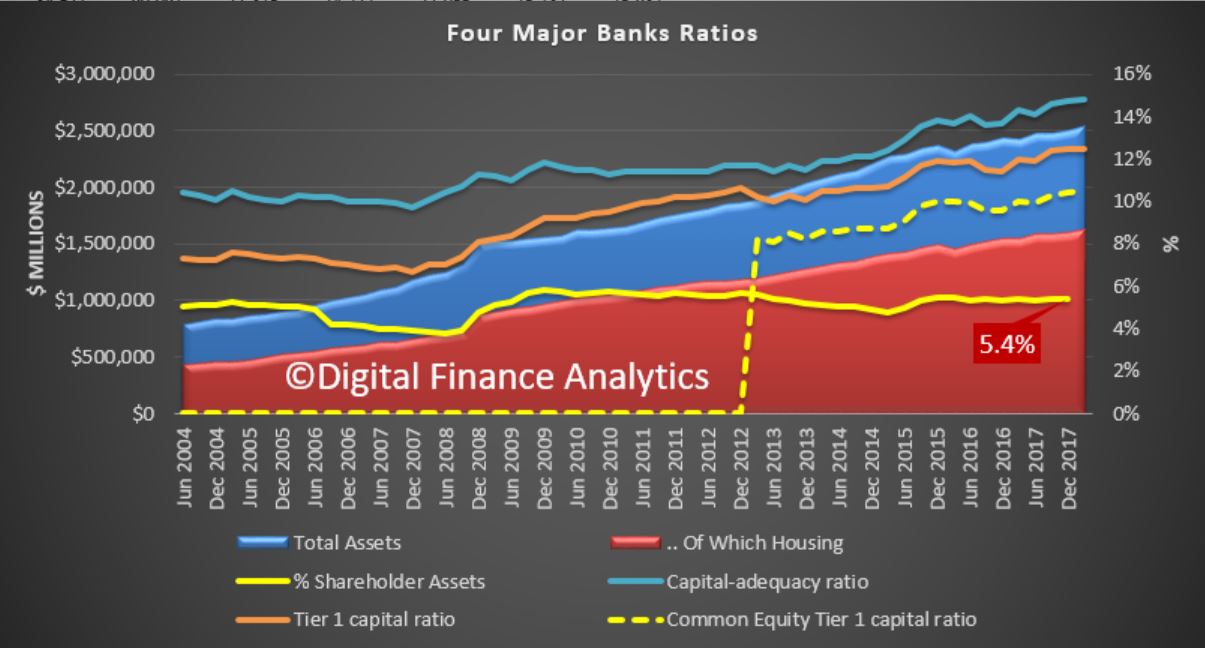

The second observation relates to the critical banking ratios. We all know that APRA has been pushing the capital rations and the newer CET1 (from January 2013) higher, and these are all rising, with the CET1 sitting, on an APRA basis at 10.5%, the highest its been.

However, if you look at the ratio of shareholder capital, it is sitting at a miserly 5.4% of all loans. In other words for every $100 invested in the loans made by an investor, they only have $5.40 at risk. This is, in extremis, the heart of the banking business, and this explains why shareholder returns are so high from the banking sector. These are highly leveraged businesses and if their risk and loan underwriting standards are not correctly calibrated it can go wrong very quickly. By the way the smaller banks and mutual have much lower leverage ratios, so they are simply less risky.

Banking is a risk business, but we see here laid bare, who is really taking the risks while the shareholders are doing very nicely thank-you!

This should come as no surprise, given the rise in the BBSW, as we discussed yesterday.

This should come as no surprise, given the rise in the BBSW, as we discussed yesterday. We expect other banks to follow, as they are all sitting on the same funding cost volcano.

We expect other banks to follow, as they are all sitting on the same funding cost volcano.