Despite the property bulls (who seem to be a bit quiet just now) there are a series of logical reasons why prices will indeed fall from current levels.

First net migration into Australia will stop period. We have been seeing around 300,000 each year, which was one factor supporting demand in some areas.

Second, new property transactions will stall. No one will want to attend an open house, yet alone an auction in the current conditions. Sales transactions have risen more recently, but that just got turned off. How soon will it be before we see zero auctions reported on a Saturday?

Third, property investors, will continue to flee – they already saw rental returns dropping, now no capital growth. Demand from new investors was weak, it will die. They may have to subsidise renters who cannot pay rent due to job loss or income decline.

Fourth, existing mortgage holders will face cash flow issues as income stalls. We already have more than 1 million households in cash flow stress, another 200,000 or so are set to join them, in short order. Around one quarter of households have less than one months free cash available if incomes stall.

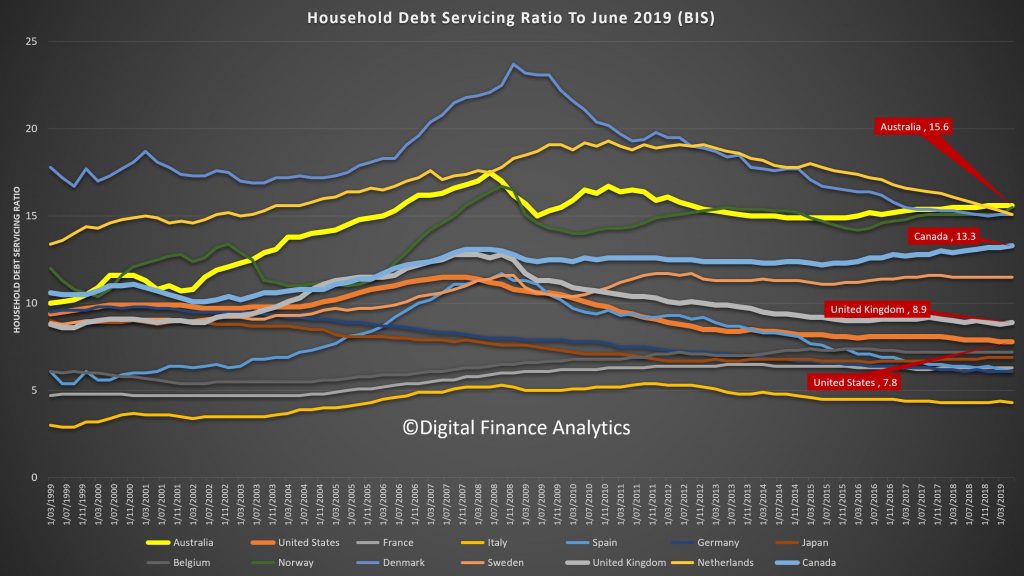

Fifth, banks will (are) cut back on mortgage lending. With margins already low, experience from Europe suggests it is unprofitable to lend. They will also lift risk underwriting standards. Meaning people if they want to borrow will get a lower available loan. Loan books will likely contain more defaults and higher risks – meaning more capital. Some may choose to shrink their balance sheets as liquidity stalls. Recently first time buyers were getting $420,000 mortgages no problems, with income ratios of 6, 7, 8 times or more. Debt servicing ratios are still high – and servicing is now an issue.

Income multiples often assumes double incomes. If one income stopped that would be a big problem.

Sixth, forced sales will eventually occur though nor immediately. I expect banks to support households in financial stress by loan and interest payment postponements, for a time. But eventually forced sales, at lower than current market values will follow. In addition, given the death rates among older people, more supply could well come on stream as estates are liquidated.

Seventh, States will take a hit from falling stamp duty as transactions slow. They will not be able to reverse this.

Eighth, Government will try various stimulation moves to try to prop up the market – but persuading people to buy now will be like selling seawater on the beach. They may well provide cash support direct to households for mortgage and rent payments – they probably should.

Ninth – the property wealth effect, which was a mirage, is dead. Finally. Until the next bubble starts, which it will, unless policy changes. I will have more to say about that ahead.

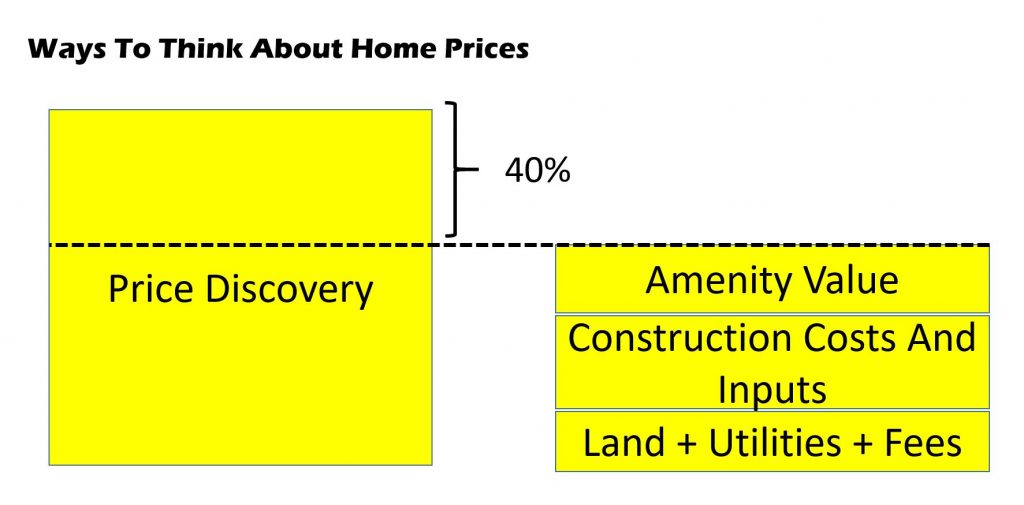

Finally, its worth thinking about this. On average, prices are 40% over their fundamental value. So they have a long way to fall.

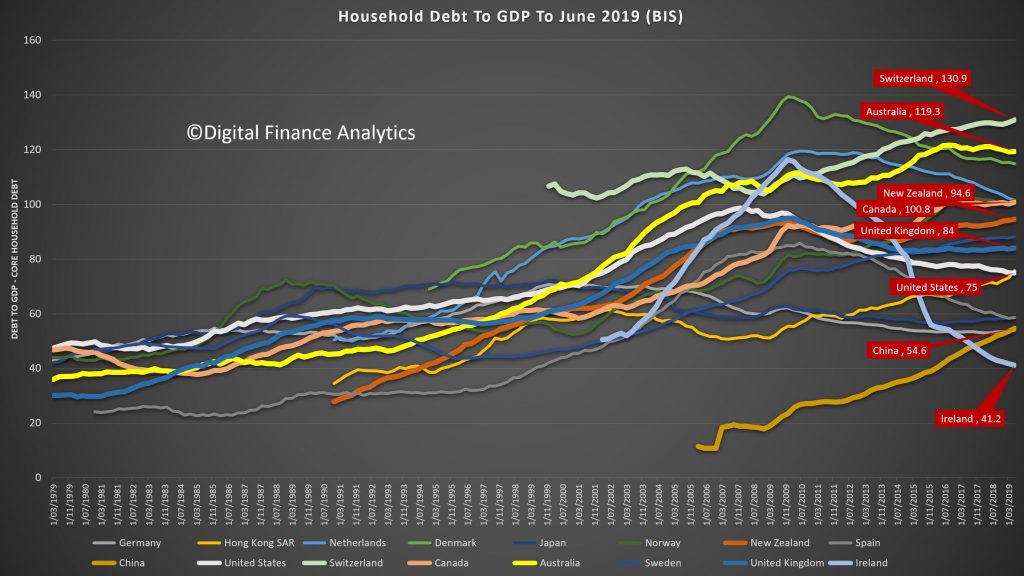

And debt to GDP ratios are, and will go further off the charts.

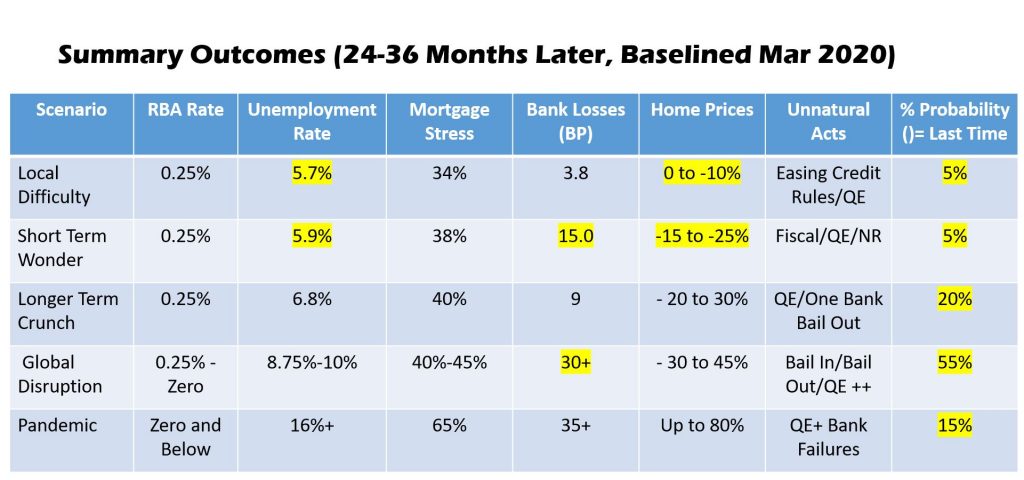

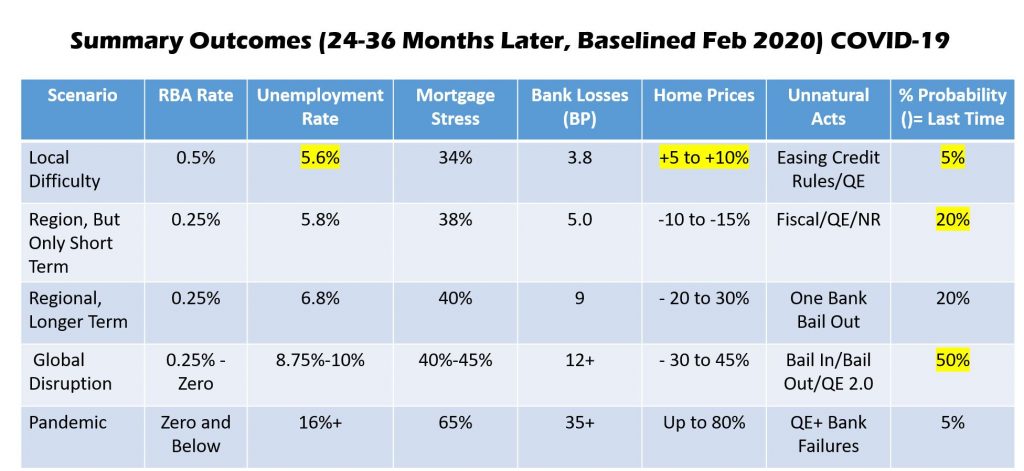

We have updated our scenarios, driven from our core market models.

The drivers are rising unemployment, and business failure thanks to the impact of the virus. We discussed these scenarios in our live stream event last night. This is the full version with live chat. The show starts formally at 32 minutes.

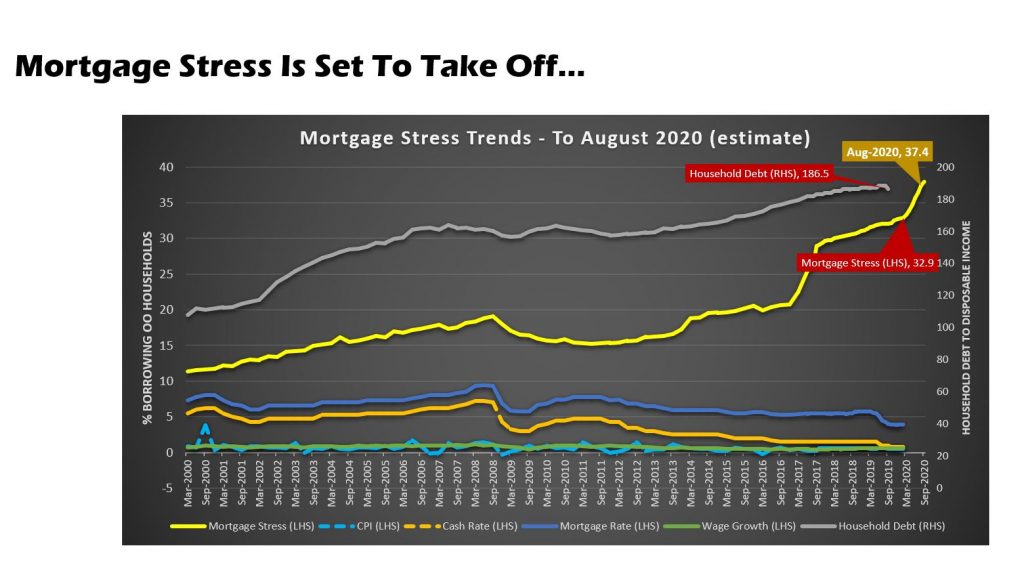

We estimate that mortgage stress is set to rise significantly in the months ahead as household cash-flows are interrupted.

Alternatively we have also released a shorter edited version, without chat here:

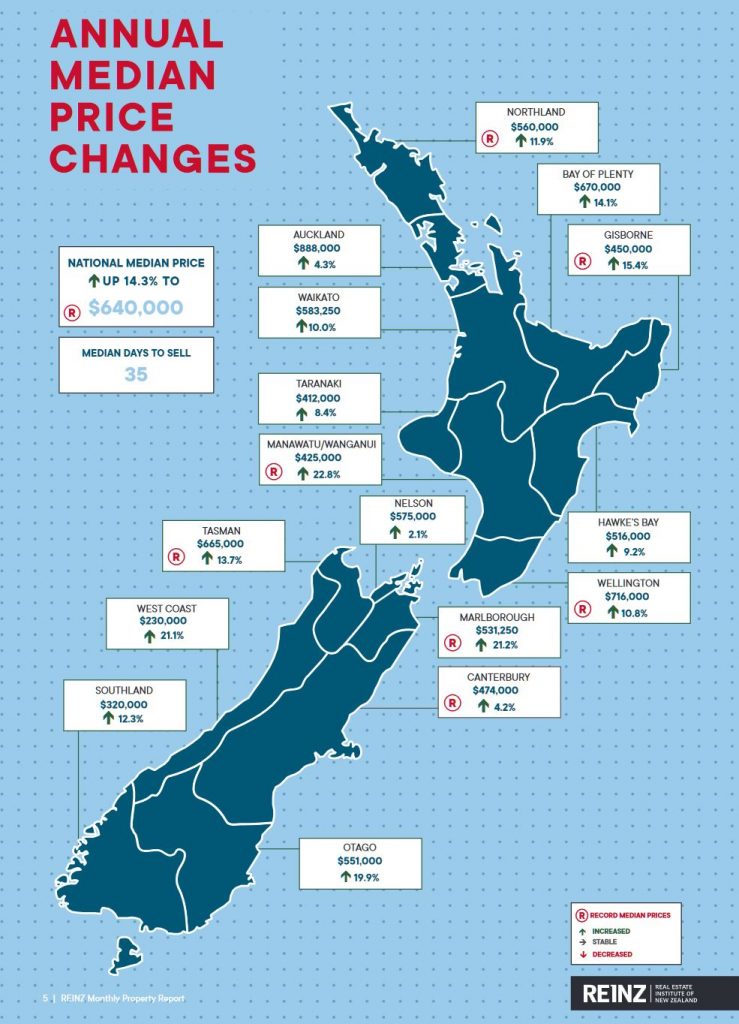

Median house prices across New Zealand increased by 14.3% in February to a new record median price of $640,000, up from $560,000 in February 2019. This was the largest percentage increase in 53 months according to the latest data from the Real Estate Institute of New Zealand (REINZ).

The number of properties sold in February across New Zealand increased by 9.2% from the same time last year (from 6,132 to 6,694) making it the highest number of properties sold in the month of February in 4 years.

For New Zealand excluding Auckland, the

number of properties sold decreased by a marginal -0.3% when compared to the

same time last year (from 4,742 to 4,726) – 16 fewer properties.

In Auckland, the number of properties sold in February increased by 41.6% year-on-year (from 1,390 to 1,968) – the highest number of residential properties sold in the month of February in 5 years.

The REINZ House Price Index for New

Zealand, which measures the changing value of property in the market, increased

8.7% year-on-year to 3,013 – a new record high.

The HPI for New Zealand excluding Auckland

increased 10.2% from February 2019 to 2,995 another new record high.

The Auckland HPI increased by 6.9%

year-on-year to 3,035 – the highest annual percentage increase in 35 months and

the first time the Auckland region crossed the 3,000 mark.

In February the median number of days to sell a property nationally decreased by 12 days from 47 to 35 when compared to February 2019 – the lowest days to sell for the month of February in 13 years.

The total number of properties available for sale nationally decreased by -22.3% in February to 20,875 down from 26,850 in February 2019 – a decrease of 5,975 properties compared to 12 months ago and the lowest level of inventory for the month of February ever. However, this was an uplift on January’s figure of 19,488.

The latest edition of our weekly finance and property news

digest with a distinctively Australian flavour.

Contents:

00:20 Introduction

00:54 US Markets

02:10 Federal Reserve Actions

03:40 Federal Reserve Tools

06:00 Negative Rates

09:00 China

09:40 Japan

10:40 UK

11:20 Global Debt crisis

14:05 Australian Section

14:10 RBA Cuts

15:00 Retail Sales

15:50 Economic Outlook – U shaped

17:00 Markets

18:00 Bank Profitability

19:45 Property Markets

Transcript (by popular demand).

Hello again, its Martin North from Digital Finance Analytics, welcome to our

latest post covering finance and property news with a distinctively Australian

flavour. In the review of this week’s news, we look at the market gyrations,

central bank responses and the limitations of monetary policy. As normal we

start with the global scene, but if you want to jump direct to the Australian

section, the time is shown below. And a

quick reminder, due to YouTube’s restrictions, I will only discuss the current

medical situation obliquely, to avoid demonetisation using the term “Panic Not

101”.

In the

US, Stocks closed in the red on Friday, but well-off lows thanks to some

late-day buying in what was another hectic final hour of trading. At the close

in NYSE, the Dow Jones Industrial Average lost 0.98% to 25,866, while the S&P 500 index

lost 1.71% to 2,971, and the NASDAQ Composite index fell 1.87% to 8,575. But then Stocks moved back

close to their lows of the day in late trading with investors likely nervous

about staying long into a weekend that will be packed with medical related

headlines. Losses in the Oil & Gas, Basic Materials and Financials sectors

led shares lower.

Volume on

U.S. exchanges was 14.2 billion shares, compared to the 10.54 billion average

for the full session over the last 20 trading days.

Data

showing a robust pace of hiring in February largely went ignored, given that

the data captured little of the impact from the “Panic Not 101”. A sharp

downturn in later economic and corporate earnings data would likely strike a

further blow to U.S. markets, analysts said.

The U.S.

Federal Reserve has begun quarantining physical dollars that it repatriates

from Asia before recirculating them in the U.S. financial system as a

precautionary measure against spreading the virus. Regional Fed banks that help

manage the money supply will set aside shipments of dollars from Asia for seven

to 10 days before processing and redistributing them to financial institutions.

The policy, first reported by Reuters, was implemented on Feb. 21. Is this another covert front in the war on

cash? On average, the Fed distributes $34 billion in paper notes every year,

according to the San Francisco Fed.

A bill

signed by President Donald Trump on Friday will provide US$8.3 billion to

bolster the country’s capacity to test for “Panic Not 101” . Trump signed the

legislation at the end of a week in which the virus began to disrupt daily life

for many Americans. As stocks plunge and U.S. companies grapple with the

economic fallout, his administration is also weighing tax relief for the

cruise, travel and airline industries.

The S&P 500 posted its 10th decline in 12 sessions as crippled

supply chains prompted a sharp cut to global economic growth forecasts for

2020. Since its record closing high on Feb. 19, the benchmark index has lost

more than 12%, wiping out $3.43 trillion from its market capitalization.

Even so,

for the week the S&P 500, along with the Dow Jones Industrial Average and the Nasdaq, posted a modest

gain as stocks on Friday pared losses late in the session. Comments from

Federal Reserve officials about the possibility of using other tools in addition

to interest rate cuts to blunt the economic impact of the “Panic Not 101”

helped stocks ease declines. The S&P 500 gained 0.6%, the Dow added 1.8%

and the Nasdaq rose 0.1%. But we still in correction territory, and the markets

have no means of assessing the emerging global uncertainties.

The

central bank has begun to grapple with what measures it would use if the

outbreak of the illness worsens in the United States and causes a severe economic

downturn.

Federal Reserve regional bank president Eric Rosengren, participated in the Shadow

Open Market Committee economics conference in New York.

“We

should allow the central bank to purchase a broader range of securities or

assets,” Rosengren said in prepared remark, noting it would require a

change to the Fed’s mandate as set by Congress.

The Fed of

course slashed its key overnight lending rate by half a percentage point on

Tuesday to a target range of between 1.00% and 1.25% in an emergency move to

mitigate the effects of the escalating global “Panic Not 101” outbreak on the

U.S. economy. Investors are predicting further U.S. rate cuts in the near

future.

Rosengren

said such an approach would be necessary because if the Fed was forced to slash

rates to effectively zero, the circumstances could have changed, which would

limit the effectiveness of purchasing only Treasury and mortgage-backed

securities, as the central bank did in the 2007-2009 recession. Those

large-scale asset purchases or quantitative easing (QE), aim to stimulating the

economy.

What

changed is the drop in the 10-year U.S. Treasury yield. It fell to a record low

of 0.66% earlier on Friday, on pace for its largest daily fall since October

2011 during the depths of the euro zone sovereign debt crisis, amid concerns

the Panic Not 101 outbreak could cause a global recession. It ended at 0.773

down a massive 16.4%. The 3-month rate dropped even more, down 18.16% to 0.51 –

so the yield curve is not inverted, for now.

“There

would be little room for the Federal Reserve to lower rates through large

purchases of long-term Treasury securities – like it did to make conditions

more accommodative in and after the Great Recession – if a recession occurred

in this rate environment,” Rosengren said.

If the

Fed did change its policy, it should be accompanied by agreement from the U.S.

Treasury to indemnify the central bank against losses, Rosengren added. He did

not specify what types of other securities or assets the Fed would buy.

Rosengren

also said he remained skeptical about introducing negative interest rates to

the United States. Other central banks including in Europe in Japan, have

pushed rates below zero. “In my view, negative interest rates poorly

position an economy to recover from a downturn,” Rosengren said.

In perfect timing the IMF just released a paper “How

Can Interest Rates Be Negative?” in which they discuss the negative interest

rate experiment. Note this chilling comment in their penultimate paragraph “But

the concern remains about the limits to negative interest rate policies so long

as cash exists as an alternative”. So,

here clearly is the link between the ban of cash, and monetary policy – no

conspiracy theory, – plain fact.

The

European Central Bank introduced negative interest rates in 2014 and the Bank

of Japan followed in 2016. The German 10-year was up 1.92% to minus 0.7144. It is

within striking distance of its record low set last September near minus 74 bp. Now of course in Japan, the

Central Bank there has been buying up a range of securities, including stocks,

bonds, and frankly anything with value, as they take the rate negative. Two-year notes in Japan currently yield minus -0.28%.

If

longer-dated U.S. Treasury yields hover near zero, some see a risk that a new

wave of buying could turn shorter-dated ones negative, even without the Fed

adopting a negative policy. So monetary policy madness prevails.

The CBOE

Volatility Index, which measures the implied volatility of S&P 500

options, was up 5.86% to 41.94 a new 5-year high. This underscores the

uncertainty in the markets.

Gold Futures for April delivery was up 0.38% to $1,674.35, so traders are

placing their faith in the yellow metal, Gold jumped almost 7% on the week, its

biggest weekly gain in 11 years. but elsewhere in commodities trading WTI crude

oil fell 9.35% to hit $41.61 a barrel, after OPEC and Russia failed to come up with

a deal expected to cut 1.5 million barrels per day off global supply

The US Dollar Index Futures was down 0.75% at 96.060 while the EUR/USD was

up 0.40% to 1.1284.

Bitcoin was up 0.55% to 9,140, as more investors seek out places to store

cash.

Investors lowered bearish bets on the Chinese yuan as a U.S.

rate cut gave Chinese bonds a yield advantage. Aided by a weakening dollar,

short positions on the Chinese yuan stood at their lowest since early January

2019. The yuan immediately jumped after the rate cut to its highest level since

Jan. 23 and erased all losses it had clocked since the Lunar New Year holiday.

It stood at 6.9373 at the close. The Shanghai index stood at 3,034.51, stronger

than recently.

Weakness in consumption in Japan to start the year lends credence to ideas that the world’s third-largest economy is contracting for the second consecutive quarter.Household spending fell 3.9% year-over-year, nearly matching economists’ projections, after a 4.8% decline in December. It is the fourth straight decline. Durable goods have been especially hard hit, led by a 10.7% decline in January auto sales after an 11.1% decline in December. Some daily data suggest that after the school closures were announced in late February, there may have been some a surge in necessity purchases. Labor cash earnings rose 1.5% year-over-year after a 0.2% fall in December. Yet, details may not be as favorable as the optics. Base pay did accelerate, but the real action came from the 10.2% jump in bonuses. Lastly, the January leading economic indicator fell from 91.0 to 90.3, its lowest level since 2009. The Japanese market dropped to a six-month low, with 97% of shares on the Tokyo exchange’s main board in the red.

In London, Europe’s financial capital, the Canary Wharf district was

unusually quiet. S&P Global’s large office stood empty after the company

sent its 1,200 staff home, while HSBC asked around 100 people to work from home

after a worker tested positive for the illness. The Footsie dropped a

further 3.62% on Friday to 6,462, while the financials index fell 3.84% to

699.80 and the pound US Dollar rose 0.74% to 1.3049.

As I see things, the global uncertainty will hit hard and debt will be the

centre of the storm. According to the Institute of International Finance, a

trade group, the ratio of global debt to gross domestic product hit an all-time

high of over 322 per cent in the third quarter of 2019, with total debt

reaching close to US$253 trillion. Much of the debt build-up since the global

financial crisis of 2007-08 has been in the non-bank corporate sector where the

current disruption to supply chains and reduced global growth imply lower

earnings and greater difficulty in servicing debt. In effect, the Panic Not 101

raises the extraordinary prospect of a credit crunch in a world of ultra-low

and negative interest rates.

As the OECD puts it “In a downturn, some of the disproportionately large

recent issuance of BBB bonds — the lowest investment grade category — could end

up being downgraded. That would lead to big increases in borrowing costs

because many investors are constrained by regulation or self-imposed

restrictions from investing in non-investment grade bonds. The deterioration in

bond quality is particularly striking in the $1.3tn global market for leveraged

loans, which are loans arranged by syndicates of banks to companies that are

heavily indebted or have weak credit ratings. Such loans are called leveraged

because the ratio of the borrower’s debt to assets or earnings is well above

industry norms. New issuance in this sector hit a record $788bn in 2017, higher

than the peak of $762bn before the crisis. The US accounted for $564bn of that

total. Much of this debt has financed mergers and acquisitions and stock

buybacks. Executives have a powerful incentive to engage in buybacks despite

very full valuations in the equity market because they boost earnings per share

by shrinking the company’s equity capital and thus inflate performance related

pay. Yet this financial engineering is a recipe for systematically weakening

corporate balance sheets. Exactly. And

more central bank liquidity actually will not help, indeed it expands debt even

more. Perhaps we are approaching that

Minsky moment. We will see.

So to the local market.

Of course, the RBA cut the cash rate this past week, in response to recent

events putting the cash rate at a record-low 50 bp. Because the Fed cut more,

in fact the Ozzie Doller is looking a little stronger, having dropped to record

recent lows. It ended at 66.50, up 0.56%. That is a problem, in that the RBA

needs to dollar to go lower, to help protect the local economy, and this may in

fact signal they should have cut harder. But then again, with only 0.25% in the

locker before practically speaking hitting zero bounds (because of the RBA’s

rate corridor) they are caught now. We

are now expecting a further “emergency” cut, and even QE in short order, to try

to support the economy.

And if you want to understand why that support is needed, you should watch my recent show “The State of the Economy in ~ 10 Slides” There we discuss Australia’s retail sales which unexpectedly fell in January by 0.3% after the 0.7% decline at the end of last year. It is the first back-to-back decline in retail sales since July-August 2017. Weak wages, the peak of the wildfires, and high household debt levels are the likely culprits.

The Australian reported that Australia faces an “unprecedented” fall in

international visitor arrivals from key countries as the Panic Not 101 outbreak

feeds a record number of holiday cancellations and a 36 per cent fall in

bookings since December. Tourism

Australia data revealed a wipe-out in international airline bookings from key

tourism markets, including China, Britain, Canada, the US, India, Japan and

Singapore. The travel ban on China, Australia’s biggest tourism market with

about 1.4 million international visitors each year, has triggered a paralysis

in bookings and a flood of forward cancellations from Chinese tourists.

Belatedly they are trying an advertising blitz in Europe and the USA, but too

little too late.

S&P cut their growth forecast for Asia pacific to 4%, assuming what they

call a U-shaped recovery, and they said that Australia is quite vulnerable, with

growth in 2020 expected to touch 1.2%, well below trend. “Australia’s

most-disrupted sectors employ a large share of workers which will weaken both

the labor market and consumer confidence,” S&P said. Services account for

almost 80% of employment with accommodation and catering, sensitive to tourism

and discretionary consumer spending, alone making up over 7%. We expect the

Reserve Bank of Australia to cut rates once more to 0.25%. Of course no-one can tell for how long the

disruption will run. Our modelling suggests the Australian economy is on the

verge of a six-month shut down. There won’t be much internal movement. The

borders will remain closed, at first by us and then by everyone else as they recover,

but we get sicker. The private sector will hunker down. And the public sector

will enter a valiant struggle with the threat.

The ASX 100 dropped 2.8% to 5157.90, while the ASX financials dropped 4.8% to 5,397.60. Bank stock prices were hit hard this week. ANZ was down 4.73% to 22.14, as it announced further job cuts. CBA slipped 3.67% to 73.93, NAB dropped 5.22% to 22.075 and Westpac was down 4.04% to 21.35, and confirmed that John McFarland will take the Chair at the bank from 1st April. Regionals were crunched, with Bank of Queensland down 4.02% to 6.93, Suncorp down just 2.18% to 11.20 and Bendigo Bank down 8.15% to 7.78. Bendigo did a capital raising, recently and remains under pressure. Elsewhere AFG, the aggregator slid 7.08% to 2.23 and Macquarie fell 4.07% to 131.93.

Lower rates of course crush margins, and most lenders passed on the full 25

basis point cut to mortgage borrowers. They are busily trimming deposit rates further

– savers once again a silent victim in all this. The RBA is of course are assuming

that the banks can lend more as rates fall (to drive more consumption) but

consumers and businesses are not confident at the moment, and household debt is

very high. In addition, many deposit returns are already so close to zero that

they cannot recover another 25 basis points. So net, net rate cuts are eating

into bank profits, dividends will be lower, and risks of default are rising

among consumers and businesses as the economy supply side shocks kick in. We

think there are limited tools to support the market from here, and in fact, QE

will not do much, when it comes. Welcome to a Japanisation of the economy.

Fitch reported little change in mortgage arrears in the last quarter of

2019, Australia’s 30+ days mortgage arrears were down 1bp to 1.06% in 4Q19 from

the previous quarter, and 1bp higher from the year earlier; 30+ days arrears

have now been below 1.2% for the past two and a half years. They make the point

that the bushfires occurred in remote or regional areas with low population

levels, while the mortgage portfolios typically securing RMBS notes are

concentrated in densely populated areas that were not directly affected by the

bushfires. The Panic Not 101 outbreak could indirectly affect arrears

performance due to lower incomes stemming from a fall in tourist numbers

following the implementation of travel restrictions.

Last Saturday we saw significant auction results, with 2,933 listed and 1,592

cleared according to Corelogic, giving a 77.1% weighted average clearance.

Sydney was at 81% and Melbourne at 77%.

A year ago there were 2,301 listed and 50.4% cleared.

Their home price index was up again, with weekly rises of 0.4% in Sydney,

0.3% in Melbourne and 0.12% in Adelaide. Perth managed a 0.08% rise and

Brisbane just 0.06%. As a result, there are average quarterly rises of 4.55% in

Sydney and 3.82% in Melbourne. From peak

though Perth is down 21.0% and Sydney is still also in negative territory

(before any inflation adjustments are applied). And again, these are averages,

prices on the ground vary considerably, with many areas still lower than a year

back. Rises are weighted towards more expensive property, which had dropped the

most earlier.

Corelogic also said that Darwin home prices have fallen for 68 months and is

32.7% below its May 2014 peak. In inflation-adjusted terms, Darwin’s dwelling

values have declined by around 36% from peak. Perth is the other housing market

that is yet to stage any meaningful recovery, even though it rebounded

marginally over the past quarter. Its dwelling values are still 21.0% below

their June 2014, or around 27.0% lower in real terms.

They also reported in their quarterly rental report that annual rental

growth nationally (1.3%) remains below inflation (1.8%), with national capital

city rental growth (0.8%) even weaker. Sydney’s rental growth (0.5% QoQ; -0.6%

YoY) remains especially weak, which pulled down rents nationally. While there

are some variations across locations and between houses and units, property

investors are in for a torrid time. Recent price growth in both Sydney and

Melbourne against soft/negative rental growth has driven gross rental yields

into the gutter, with both Sydney and Melbourne house yields well below 3% –

near the lowest level on record. Net returns are even worse.

And SQM research released its Stock on Market report for February, which

revealed that property listings rose by 0.2% over the month but were still down

13.8% year-on-year. But listings in Sydney and Melbourne bounced, jumping by

9.9% and 10.0% respectively in February.

We think home prices will react to the recent uncertainty, and rising

supply. It is just a timing issue.

The S&P/ASX 200 VIX, which measures

the implied volatility of S&P/ASX 200 options, was up 20.47% to 26.687 a

new 3-years high. Risk is on. The Euro

Aussie Dollar was at 1.6973, the Aussie Gold cross was down 0.41% to 2,519.20

and the Aussie Bitcoin cross was down 0.26% to 13,812.9

So, in summary, the uncertainty in the outlook is looking decidedly dark.

There are few places to hide, and the question now is how soon will property

prices slide back – we are expecting some fiscal stimulus and it will be

interesting to see if it is directed at the property sector – is should not be,

as there are more immediate needs among small businesses, but then again the

Government does appear to love property. We will see.

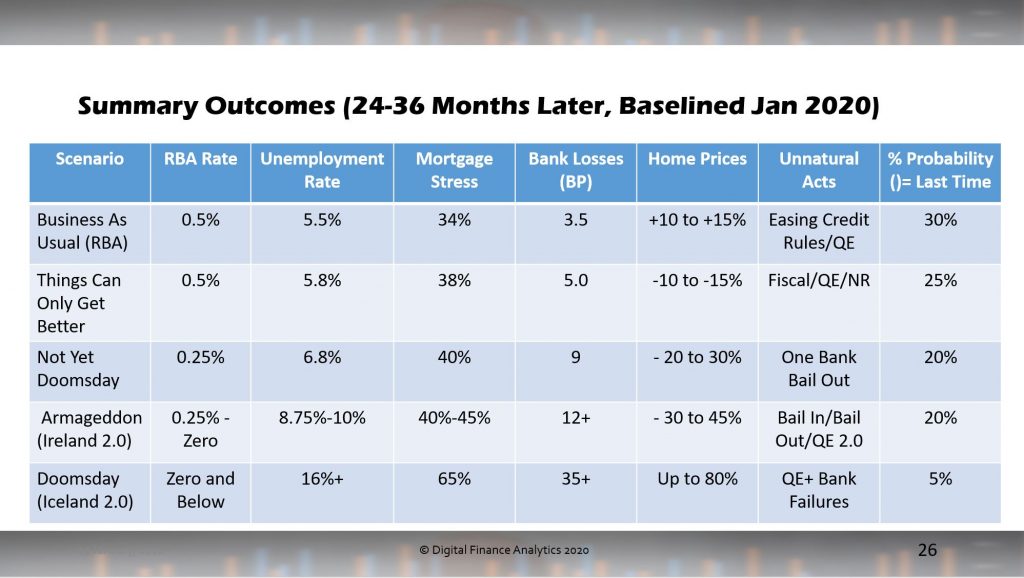

Last week we ran our latest live event, and discussed a range of potential scenarios relating to the virus. If the virus is localised and of short duration, there was still a path to higher prices, but as its severity and reach grows, prices would turn negative. This is a simple (actually complex) set of relationships between economics, human behavior and property.

Here is a summary of the various scenarios from our modelling. We weighted the greatest probability at 30-45% fall in the months ahead, assuming global disruption, financials market falls and reinfection. All of which is coming true.

Begs the question, how soon will prices turn south unequivocally?

Despite the recent influx of positive reporting on the trajectory of the housing market, there remains “a fundamental, structural problem” with the price of property in Australia, according to financial analyst Martin North. Via Australian Broker.

While the rising home values evidenced

from mid-2019 have been largely celebrated as an overtly positive trend,

North has his doubts.

“It’s not sensible to hope and assume

prices will continue to go ever higher. House prices are very high

relative to income. Actually, very high relative to any other measure

you can name, like GDP,” he said.

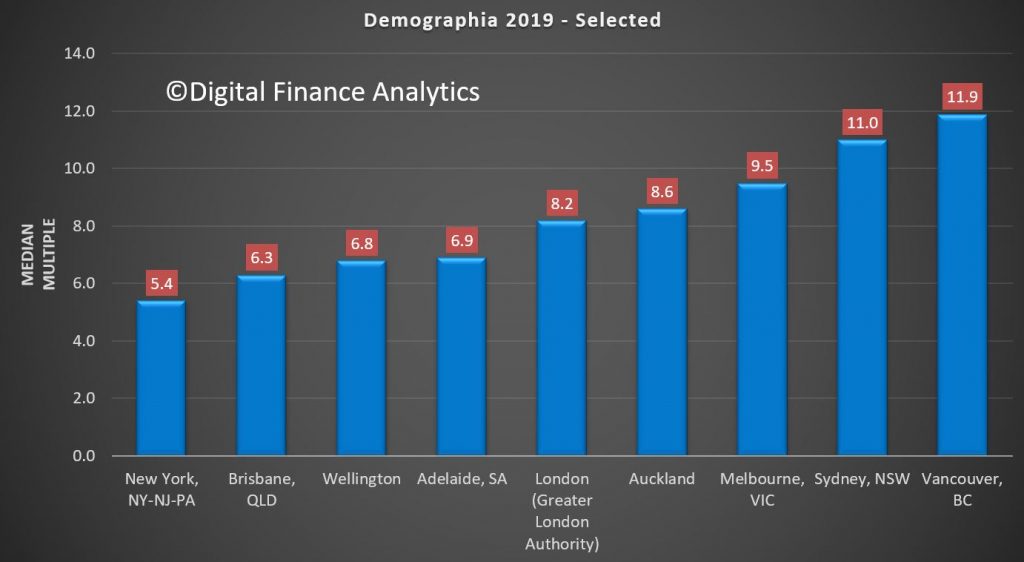

A recently-released Demographia survey

showed Australia has some of the most unaffordable property in the

world. While Hong King and Vancouver claimed the top two spots on the

list, Sydney and Melbourne came right after.

“Further, we’ve got too much debt in our

system, which is supported by debt that’s difficult to repay, even at

low interest rates,” said North.

“There is definitely a cap, in my view, on how much home price growth we should expect and will see.”

The affordability concerns which have

dominated Australia for years were again thrown into sharp relief by

recent figures around hopeful market entrants.

“The latest data shows the first home

buyer average loan is now $408,000 across Australia – the highest it’s

ever been,” said North.

“That’s massive for a first-time buyer

trying to get into the market. Think about the income multiples that

figure represents; that’s maybe eight, nine, 10 times what many people

make.

“It’s an unsustainable position to be in.

We can’t allow home prices to continue to run away. It will create a

bigger problem for us later.”

It’s important to focus on the hard data amidst the sea of vested parties doubling down on their own rhetoric, North said.

“The banks want property prices to go

higher because if they go lower, they have much more risk in their

system and on their books than they want to admit,” he explained.

“The Reserve Bank and Treasury both want

prices to rise to create the wealth effect. If people feel more wealthy,

which they generally do as prices rise, they go and spend more. Trying

to bring prices higher is really the only lever they’ve got.”

However, according to North, it’s “failed

policy” to bank the future of the economy on “ever-inflated house

prices” with nothing else to support it.

“I come back to the fundamental reality of the ratio between debt and income, the ratio between debt and GDP,” he said.

“We’re in an unsustainable position. We’re

betting the farm on the property sector and, in my view, it’s going to

fall over at some point; it’s just a question of how soon.”

Here is the edited version of our live stream event for January. In the show we update our property and finance scenarios, and answer a range of questions from viewers. We ran out of time, so I plan to make a future show covering those I missed. Here are our current scenarios:

The original live recording, with the embedded live chat is also available. You will need to watch on YouTube to follow the interactions:

Our next live show will be at 20:00 Tuesday 18th February.