Great cities and neighbourhoods always have a particular kind of urban intensity – what we might call the “character”, “buzz” or “atmosphere” that emerges over time. While unique in many ways, great cities also have certain things in common. One way to understand these properties is to think about a city’s “urban DMA” – its density, mix and access.

We’re still in the early days of understanding how cities work. But we do know that creative, healthy, low-carbon and productive cities all depend on intensive synergies of density, mix and access.

When we talk about “urban DMA”, we’re talking about the density of a city’s buildings, the way people and activities are mixed together, and the access, or transport networks that we use to navigate through them.

Like biological DNA, urban DMA doesn’t determine outcomes, but establishes what is possible. A low density, largely mono-functional cul-de-sac (such as a shopping mall or a gated enclave) is an anti-urban form. Minimum levels of concentration, co-functioning and connectivity are necessary for any kind of urban life.

The concept of urban DMA can be traced to the work of the late Jane Jacobs, whose book “The Death and Life of Great American Cities” was written in the mid-20th century, when many great cities were being surrendered to cars and poor urban design.

Jacobs wrote of the need for “concentration”, “mixed primary uses”, “old buildings” and “short blocks”. We recognise this as urban DMA – “concentration” is density; “mixed use” and “old buildings” are the conditions for a formal, functional and social mix; and “short blocks” means “walkability” at a neighbourhood scale.

Jacobs’ key contribution was to focus on the city as a set of interconnections and synergies rather than things in themselves – a focus on the city as an assemblage, rather than a set of parts. While the language has evolved, our understanding of these vital synergies needs to be taken much further.

Access

Access is about how we get around in the city. How do we make connections between where we are and where we want or need to be? What are the access routes – are they organised in closed or open networks? How fast are they at different scales and for different modes of transport? How far can we get with a given time frame and with what mix of walking, cycling, car, bus, tram or train?

At a neighbourhood scale access is primarily about “walkability”; at larger scales we depend on a mix of cars, cycling and public transport. But access means nothing if there is nowhere to go – the synergy with density and mix is everything.

Kim Dovey, Author provided

Mix

Mix is about the differences and juxtapositions between activities, attractions and people. It’s not about diversity as spectacle, but a means of enabling encounters and flows between different categories of people, buildings and functions. Mix is about the alliances and synergies between home, work and play; between production, exchange and consumption.

Like density, mix can be uncomfortable; it means proximity to different kinds of people and practices. It means a layering of old and new buildings, of large and small buildings, and of large and small organisations.

Mix is not an unmitigated benefit. Urban planning was largely invented to stop mixing – to prevent living with noise, smells and activities we don’t like. It means keeping where we live away from where we work and shop.

But that separation ceases to be helpful when the result is people living in suburbs with no shops, or working in suburbs with no transport. Great cities will have many different kinds of mix – a “mix of mixes” – each geared in turn to density and access.

There are dangers in an excess of some kinds of density, like the overcrowding of populations and the loss of light and air that comes with excessive building. There are many different kinds of densities – of residents, jobs, buildings, houses and street life. They interconnect, and they all matter.

The big question about density is: how much activity, how many people and how many buildings can be concentrated into one urban area? How close can we live to where we work or need to be? How many urban amenities, places and jobs can we walk or commute to?

Density is not one thing but many and it is the mix that matters.Elek Pafka, Author provided

Urbanity

What is at stake here is the future of this great cauldron of productivity and creativity we call urban life. The 19th century British economist Alfred Marshall famously suggested that there was “something in the air” of a city that made it more economically productive – a phrase that is suggestive of an “atmosphere” and a “buzz” of urban intensity.

Much more than a simple clustering of people and buildings, urbanity is a concentration of intensive encounters and interconnections. And its benefits are much more than economic – they’re social, environmental and aesthetic.

If we want to build great cities, we shouldn’t develop formulae or copies of “best practice” from other cities. We should turn to our existing cities and ask three simple questions:

How dense can we get yet remain liveable?

How mixed can we get while remaining safe and civil? And,

How easily can we get around in a healthy and sustainable way?

Urban planning enables and constrains these dimensions of urban life. And unlike human DNA, urban DMA can be redesigned. If we want a healthy, creative, productive and low-carbon city – if we want “the buzz” – we need to reshape the urban DMA.

Authors: Kim Dove, Professor of Architecture and Urban Design, University of Melbourne; Elek Pafk, Lecturer in Urban Planning and Urban Design, University of Melbourne

The Commonwealth Bank has long been active in the space of financial literacy – that is, educating young people about the importance of managing money effectively.

Just recently it announced an overhaul to its “Start Smart” financial literacy programs, which aim to teach children about money.

The catch phrase seems progressive but is loaded with assumptions about women, men, their relationships, and their financial choices. This downplays the economic and social reasons why women’s financial opportunities and experiences tend to differ from men’s.

Pay gap in the workplace

It’s a bold ambition when you consider the broader context. According to the Workplace Gender Equality Agency, the highest gender pay gap actually occurs in the financial and insurance services industry, where senior management positions continue to be male dominated and the difference between women’s and men’s earnings is 30.2%.

Further, when comparing Indigenous females to non-Indigenous male workers with median incomes, the reported superannuation gap is 39%.

Such programs, like the one Commonwealth Bank is offering, are based on the assumption that a combination of guest speakers visiting schools and downloadable resources hold the key to improving financial literacy teaching and learning.

Why are banks getting involved?

The federal government has invested millions of dollars and entrusted the Australian Securities and Investments Commission (ASIC) to lead initiatives intended to help children understand finance.

We also have consecutive National Financial Literacy Strategies led by ASIC, that are intended to drive improvements in the way financial literacy is taught and learned in schools.

Consumer and financial literacy has an elevated status across the Australian curriculum, signalling opportunities for interdisciplinary approaches, particularly in mathematics and economics and business.

Financial literacy projects are big business for consultancies. And for banks, manoeuvring under the guises of corporate social responsibility serves to position brands favourably.

The ANZ bank, for example, conducts its Survey of Adult Financial Literacy every three years. This is considered the leading measure of adult financial literacy in Australia.

These strategies are important to them since their houses are not in order. The recent parliamentary inquiry confirmed that the big four banks are troubled by bad behaviour and more effective regulation is needed.

How do children learn about money management?

Children tend to learn about money within their homes in different ways – and those teaching around this area need to be sensitively attuned to this learning.

Children become socialised and oriented to consumer, economic and financial issues through a series of conversations, observations, and experiences – consciously and unconsciously.

Even primary-aged students make surprising, insightful comments that show mature understandings about earning, spending, saving, and sharing money. This is particularly true in disadvantaged communities.

How is financial literacy taught?

Research into financial literacy education in schools – how it is taught and learned – is an emerging field, typically characterised by program trials and evaluations.

Program evaluations tell short term success stories – the rubber really hits the road when students need to apply their learning in the real world down the track.

In 2012, the OECD and Programme for International Student Assessment (PISA) included a Financial Literacy Assessment for 15-year-old students. Australia ranked fifth out of the 18 participating countries and economies.

The findings showed that students in city schools achieved higher scores than students in provincial and remote schools; and non-Indigenous students significantly outperformed their Indigenous counterparts.

Teaching kids about managing money is most effective when classroom tasks are tailored to meet students’ family backgrounds and interests, and occurs at the point of need.

Students enjoy financial problem solving and decision-making experiences that captivate their imagination, challenge them to think, and prepare them for the real world.

Devising financial literacy lessons that create connections between students’ financial literacy learning at home and at school is hard to do without really knowing the local context and students.

Because Australian classrooms are diverse, this stuff rarely comes together “off the shelf”.

Not reaching the most vulnerable communities

The uncomfortable truth is that workshops by so-called finance literacy experts and downloadable teaching and learning resources may not reach and resonate with Australia’s most vulnerable communities.

Planning for financial literacy learning requires an understanding of the school community, interdisciplinary navigation of the Australian Curriculum, and skilful inquiry approaches.

This is what teachers are trained to do, although they need and crave quality professional learning to hone their craft.

When it comes to meeting students’ academic, social and emotional needs on any issue, let’s invest in schools and trust teachers to do what they’re qualified to do.

Authors: Carly Sawatzki, Lecturer, Monash University; Levon Ellen Blue, Research fellow, Griffith University

Although the majority of Australians consider themselves financially responsible when paying bills and sticking to a budget, a quarter of the population (26%) are splashing their cash on things they know they will struggle to repay says Veda.

Millennials are leading the pack, with 36% of people aged under 30 admitting to overspending according to new research from Veda, Australia and New Zealand’s provider of consumer and commercial data and insights and a wholly-owned subsidiary of Equifax.

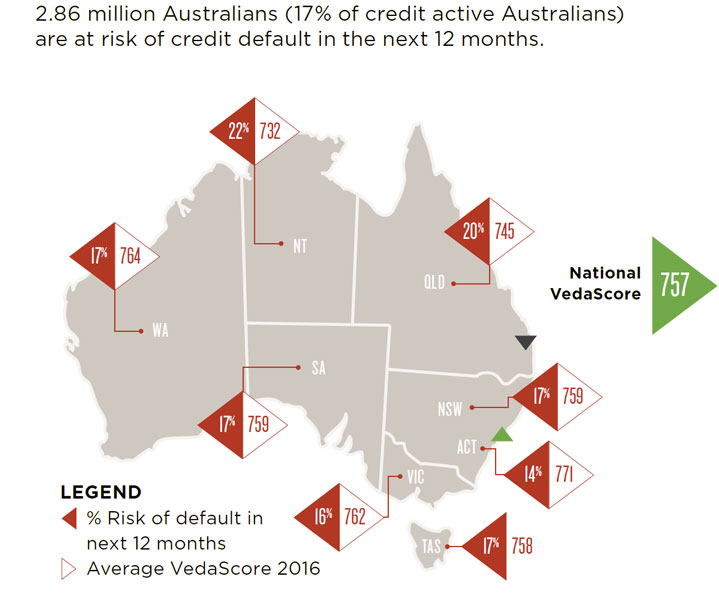

The Veda Australian Credit Scorecard offers market-leading insights into credit habits and VedaScores. It combines an analysis of more than two million VedaScores with consumer research of 1,000 Australians. A VedaScore provides a snapshot of an individual’s creditworthiness, which is useful to know when applying for credit.

Queensland is the state with the highest default risk of 20 per cent, whilst the Australian Capital Territory scored lowest.

Izzy Silva, Veda’s General Manager, Consumer, said the tendency of younger people to overspend was reflected in their credit scores, revealed in the fourth annual Veda Australian Credit Scorecard.

“Millennials (Gen Y) top the table for the generation at highest risk of default within the next 12 months, with 23% of this group considered at risk, compared to 17% of the total population,” Mr Silva said.

In 2016, Millennials also have the lowest average VedaScore (712) and are the only generational group to have an average score lower than the 2016 national average (757).

The good news is Veda’s data shows that the average VedaScore of 757 for Australians in 2016 is considered a very good score.

“It is clear that Australians are more aware of how their credit score can get them a better deal, with an increase in people accessing their credit score to 23%, compared to only 11% in 2015. However, Australians say they want to ‘live in the now’ and tend to splash the cash without worrying about the future – 32% of consumers admitted to this behaviour (up from 24% last year),” Mr Silva added.

Generally speaking, women are more financially conscious than men with the average VedaScore for women sitting at 768, compared to the average VedaScore for men of 749. This financial conscientiousness is illustrated by the statistic that only 13% of women are likely to overspend because they think they deserve it, compared to 23% of men.

“By maintaining a high VedaScore, consumers demonstrate to lenders that they are in control of their credit and spending habits, which in turn makes them a lower credit risk and more attractive to lenders, thus helping them secure better financial opportunities,” Mr Silva said.

Australian Credit Attitudes

Social researcher Mark McCrindle said that gender and age were just two of a number of factors that influenced an individual’s financial personality.

“Through the research conducted by Veda, we have seen a segmentation of people’s attitudes towards credit and there are four individual archetypes we have identified. These are: Money Masters, Slapdash Strivers, Secure Savers and Financial Fumblers.

“Each of the archetypes is shaped by influences including age, income, gender, and work status. There are distinct attitudes and behaviours exhibited by each archetype group,” Mr McCrindle added.

Money Master – Generally classified as wise and knowledgeable when it comes to managing their own credit, with friends and family members often coming to them for advice in regard to their financial goals. Money Masters tend to be predominantly male, work full-time and have a healthy expendable income which they can invest into financial securities.

Slapdash Striver – Often people who take financial risks without completely understanding the consequences. They also consider themselves financially ambitious and have the potential to reach their financial goals with further knowledge of the credit landscape. Slapdash Strivers tend to work full-time and achieve a higher income than the majority of Australians, with an even split between males and females.

Secure Saver – People who are living comfortably within their financial environment and would prefer not to spend money with credit on unnecessary items as they are well informed about money management. They typically have a strict budget and plan ahead for future uncertainty. People who are classified as Secure Savers tend to be female and from the Baby Boomer generation who either work part-time, or are retired.

Financial Fumbler – Often people who live payday to payday and can get overwhelmed when setting financial goals. They are unaware of the benefits of credit and don’t have the appropriate knowledge to invest their money in the right places. With better planning and knowledge, they can get back on track and head towards a positive future. People who are classified as Financial Fumblers tend to be on the lower end of the income spectrum, such as students and/or under 35 (Millennials or Gen Y).

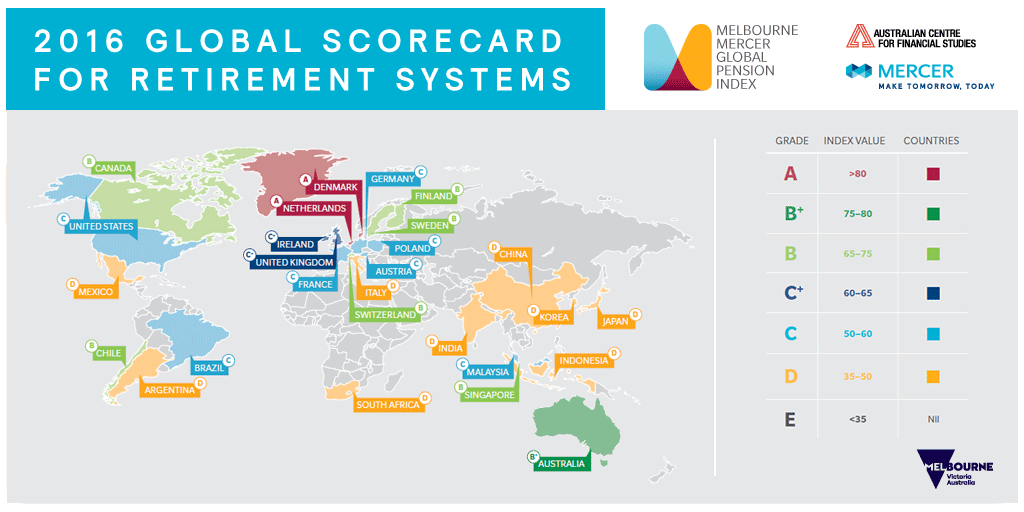

Despite retaining its third-place ranking behind Denmark and Netherlands in the 2016 Melbourne Mercer Global Pension Index (MMGPI), Australia has sustained a slight drop in the rating of its pension system for the second consecutive year.

Whilst not alarming, narrowly missing out on the Index’s A-grade ranking by receiving a score between 75 and 80 for a sixth consecutive year indicates that despite being superior in many ways, further reform is required to ensure that Australia’s retirement system is considered world class, as is the case for Denmark’s and Netherlands’, which both retained their A-grade rankings.

Measures that were suggested to improve Australia’s system include:

Introducing a requirement for an income stream to comprise part of the retirement benefit;pension age relative to ongoing increases in life expectancy;

Increasing the preservation age;

Continuing to increase labour participation rate at older ages.

Australia’s overall Index Value saw a decline from last year’s 79.6 to this year’s 77.9. Author of the report and Senior Partner at Mercer, Dr. David Knox, attributed this to a “reduction in the net replacement rate”, caused by the federal government’s decision last year to defer the increase of the Superannuation Guarantee from its current 9.5 per cent to the proposed 12.

Despite its deferral affecting this year’s Australian adequacy rating, former Commonwealth Bank CEO and most recent Chairman of the Financial System Inquiry (FSI) Dr. David Murray AO insisted in his interview with Franklin Templeton Managing Director Ms. Maria Wilton, that an increased superannuation guarantee was necessary for a sufficient adequacy, given the tightening of the taxation arrangements around superannuation by the Federal Government.

“The nominal contribution rate [of the current superannuation guarantee] is 9.5 per cent. In effect, this is closer to 8 on an after-tax basis, and in adequacy terms” he believed this was insufficient. “You would have to get at least 11 after tax… on a pre-tax basis, allowing for the contributions tax, that’s around 14-15%”, Dr. Murray explained.

More alarmingly perhaps, Dr. Knox hinted at the fact that Australia’s score could undergo a further decline in future years, due to the Index not yet having taken into consideration the tougher 2017 Age Pension assets test, which will see a reduction in pension payments.

“At the moment, there is no allowance for the new assets test that comes on January 1 next year. I’m expecting our net replacement rate… to fall again”, Dr. Knox stated.

Despite these issues, Dr. Knox confirmed that the positives associated with the Australian pension system far outweighed the negatives, noting that a significant factor in Asian countries such as India, Singapore and Korea being the biggest improvers in the 2016 index ratings, was these countries considering the Australian system an archetypal source of recommendations.

These sentiments were endorsed by Dr. Murray, who deduced that “in a low growth world, with unfunded systems from much of the developed world” a country taking Australia’s third rank was “more likely to come from Asia” than anywhere else.

This year, 27 countries were included in the MMGPI, all of which obtained an index value based on more than 40 indicators, each belonging to one of three sub-indices; adequacy, sustainability and integrity. Covering almost 60% of the global population, one of its primary aims is to highlight the shortcomings in each country’s retirement income system, and suggest possible areas of reform.

THE VERY SIGNIFICANT IMPACT OF AGEING POPULATIONS ON GLOBAL PENSIONS

As well as dealing with annual rankings, this year’s edition of the MMGPI closely inspected the impact of an ageing global population, and how well equipped each country in the Index is to deal with this issue.

It was found that each country has experienced improvements, albeit to varying extents, in life expectancy over the last four decades. As outlined by Dr. Knox, when these projected increases in life expectancies are combined with recent marked decreases in fertility rates, the result is that “many countries are facing a significant [old] age dependency ratio over the next 25 years”.

“[In] 1980, we had almost 6 workers per older person, a couple of years ago, we had 4.7 and by 2040, we will have 2.3”.

It was found that of the countries in the Index, the one best placed to tackle this issue of an ageing population was Indonesia, due to the combined effects of its relatively low projected old age dependency ratio in 2040, and its preferable scoring on a range of mitigating factors, which it was explained by Dr. Knox, were very likely to offset the inevitability of having more aged.

These mitigating factors include:

Labour force participation rate for 55-64

Labour force participation rate for 65+

Amount of increase in the labour force participation rate for 55-64

Projected increase in the retirement period over the following 2 decades;

Pension fund assets as a % of GDP.

Professor Rodney Maddock, Interim Executive Director of the Australian Centre for Financial Studies, who hosted the Index’s official launch, echoed Dr. Knox’s thoughts, noting that an adjustment to both the retirement and pension eligibility age was necessary to ensure the continuing sustainability of Australia’s superannuation system: “Australians are living longer, living larger portions of their life in retirement and spending more in retirement, so we need to be well-placed to ensure fulfilling, adequately-funded retirements.”

From a more global perspective, perhaps in a much more dire state, is a nation such as Japan, which according to Dr. Knox, will have “one retiree for every 1.44 people of working age by 2040”, demonstrating the “alarming” projected old age dependency ratios in some nations.

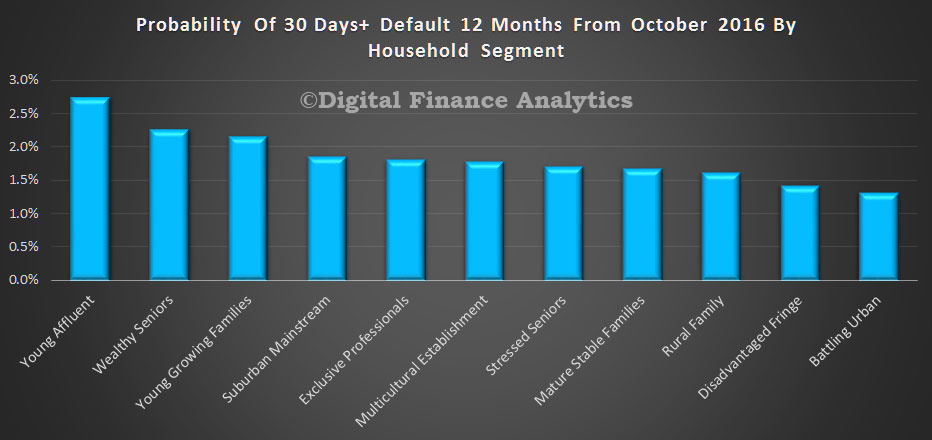

IF YOU’RE already starting to feel the mortgage pinch, this is bad news. New economic modelling shows mortgage defaults are set to rise over the next 12-18 months, and those who will be most affected will surprise you.

The research conducted by Digital Finance Analytics, based on its extensive household surveys, shows those falling behind in their mortgage repayments will continue to increase thanks to low wage growth and employment changes. This is despite record low interest rates.

“Incomes are just not growing and that is creating considerable difficulties for many households,” Principal of Digital Finance Analytics, Martin North told news.com.au.

“What I’m predicting is that incomes are going to remain static for the next 12-18 months … That means that households are in this difficult situation were they can just about afford their mortgages, but things like the general cost of living, which is going up faster than incomes, is going to create considerable pressure on many households.”

Western Australia and Queensland mining areas will bear the brunt, with New South Wales, Victoria and ACT being the best placed.

WHO IS MOST AT RISK?

First home buyers will unsurprisingly be in the firing line, as they are entering the housing market now when prices are so inflated and going in with the assumption that their income will grow.

However, interestingly, those hit the hardest will be affluent young buyers and wealthy seniors. Disadvantaged households on the edge of cities, and battling urban households are at lower risks of default.

“People with large mortgages, so young affluent buyers who bought in Bondi, for example, are finding it much more difficult to keep that property out of default because their income is not growing. Even in the more affluent areas in the states where there is a greater economic momentum, you still have the hot spots of difficulty,” Mr North told news.com.au.

“Interestingly, it is not necessarily the more stressed households — the ones you would expect out on the fringe. And the reason for that is those households never got the pay rises and they never got the big mortgages because they couldn’t afford to.”

Wealthy seniors who own property will also face more mortgage stress due to a combination of stagnating income and lower returns from deposits and the sharemarket.

Mr North said he is concerned this could spell disaster for the economy.

“The reason is we have never had household debt as high as it is. This is new territory,” he told news.com.au.

“We’ve got this very high level of debt and we’ve got very flat incomes so it could work out in a rather bad way.”

He said retail spending and financial stability are going to take a hit as Australians will not have the discretionary income to spend and the performance of our major banks is heavily reliant on mortgages.

French economist Thomas Piketty, currently in Australia, is known for his focus in on the inequality of wealth. His book on the topic has sold two and a half million copies worldwide, which is quite amazing for a book full of economic statistics and graphs.

Piketty concludes, optimistically, by saying that we don’t have to accept the inevitability of wealth inequality. If there were the political will we could, as a society, reduce inequality. This includes his argument for an inheritance tax.

Piketty spends less time explaining why excessive wealth inequality matters. This requires more attention because we cannot presume that there is sufficiently widespread public knowledge about the importance of the issue.

Some people evidently think wealth inequality is a good thing, because they believe it creates stronger economic incentives. It is that sort of reasoning that leads them to favour the Turnbull government’s proposed cuts to company tax rates, even though it would create yet more economic inequalities.

Meanwhile the International Monetary Fund has published research showing that more equality is also conducive to superior macroeconomic performance. Coming from such a usually conservative source, that should shake the belief that inequality is good for the economy.

There is also lots of other social science research showing the social problems that result from widening inequality. This includes the important research work reported by Wilkinson and Pickett in their book The Spirit Level, which explains “why more equal societies almost always do better”. It shows that more equal societies are generally happier and have a lower incidence of social problems, such as physical and mental illness, obesity, crime and violence and low levels of educational attainment. Other studies show that more equality is conducive to more sustainable and peaceful social arrangements.

More equal societies have healthier democracies too, as US economist Joseph Stiglitz has argued, because there is less tendency for wealthy elites to corrupt political institutions.

Why Australia should care

These concerns are currently of great significance for Australia. And we now have the data necessary to understand the dimensions of the challenge.

A new Australian report on wealth inequality by the Evatt Foundation, drawing on the best data available, shows Australia is not the egalitarian nation that many people think it is. Rather, in terms of wealth inequalities, we’re mid-ranking on the international league table. And we’re becoming more unequal.

Currently, the wealthiest 10% of Australian households have approximately half of the total private wealth in the country. The top 1% of households alone have 15% of the total wealth.

At the other end of the spectrum, 40% of households have effectively no wealth. Most of them have modest current incomes, whether from wages or welfare, and they spend it all (and sometimes more, going into debt). Nothing is accumulated over time. Struggling to pay for housing is a big factor keeping them out of the wealth accumulation process enjoyed by those who have more substantial wealth.

Two wealth gaps are widening. One is between the top 10% of Australian households and the next 40% of “middle Australia”. The other is between those two groups and the bottom 40% who are effectively “out of the loop,” as far as sharing in economic prosperity.

These are the hallmarks of an unequal society, not an egalitarian society, as my colleague Chris Sheil and I have argued previously.

I’ve also put the case for inheritance taxation as one of the policy measures that could be considered if we’re serious about reining in inequalities. Piketty’s presence here in Australia makes it timely to reconsider these issues and kickstart some policy action.

Slowing down the intergenerational transmission of inequality would be a good start to reversing the growing inequalities with which Piketty and the new Evatt Foundation report are concerned. That means having an inheritance tax.

Most other developed countries have taxes on inherited wealth. Australia used to have inheritance taxation too, until Queensland Premier Joh Bjelke-Petersen initiated the collapse of those arrangements in the late 1970s.

The case for an inheritance tax is well established. The last major review of the Australian tax system, chaired by former Treasury head Ken Henry, supported it in principle.

The exact form of the tax needs careful consideration. Should it be on the estate itself, or on the windfall incomes that it provides for the participants? What minimum wealth threshold should be set? And, above that threshold, what rate or rates of taxation should apply? Other countries vary in their treatment of these issues, so it is important that we develop a system that is appropriate for local circumstances.

Of course, any such tax would be opposed by the wealthy elite. You wouldn’t expect otherwise. But if the tax threshold were set at, say A$2 million, only a tiny proportion of households would be affected. And the rest of us would benefit directly from the extra revenues, which might then be used to pay for universal free tertiary education, for example, or a major increase in public housing.

We would also benefit indirectly from living in a more cohesive society with less of those problems that the social science researchers have shown to be correlated with extreme inequalities.

Author: Frank Stilwell, Emeritus Professor, Department of Political Economy, University of Sydney

People from cultural backgrounds where getting financial assistance from families is the norm are less likely to default on their mortgages, new research shows. This includes those from South East Asian countries.

We also found in societies where the culture is to save more and for people to control their desires and instincts, the default on mortgages is lower. The findings are true both in relatively stable economic periods (2010-2013) and during a period of financial crisis (2008-2009).

In analysing the factors behind mortgage delinquencies, we used data on default rates from 42 developed and developing countries. These countries represent about 90% of the world’s gross national income and the world’s outstanding balance of housing mortgages in 2013. The rate of people who defaulted on their mortgage varied from 0.05% in Hong Kong to 17.05% in Greece.

Australia has a low default rate on mortgage, thanks to a strong level of national income, stable growth of the property market and a low unemployment rate. But it ranks high in all cultural dimensions that potentially lead to high default rate, this is accentuated during times of widespread economic hardship. So policymakers should be mindful of unfavourable economic conditions that may trigger default on mortgages.

There are a number of explanations for our findings. Individuals who have a tendency to enhance or protect their self esteem, by taking credit for success and denying responsibility for failure, may overestimate their abilities make enough money to meet their long term financial obligations. They also have relatively weaker self-monitoring skills and may not budget well.

Also, in societies where people are expected to be independent and only take care of their own interests, the rate of default on mortgage is higher. A lack of access to support from extended families and groups may make it difficult to pay back their mortgages during the period of financial hardship.

We found that borrowers in countries exhibiting higher degrees of pragmatism (e.g. having a long-term view to life) are less likely to default on their mortgages. People in these countries have a higher tendency to save. These people are also probably less likely to undertake risky mortgages and therefore default less on their mortgages.

In societies with a strong emphasis on enjoying life there was a higher rate of defaults. These people are more likely to follow their impulses and desires and so might not allocate their financial resources efficiently. They may spend more money than they can afford on leisure activities and have less savings to service their mortgages.

Not surprisingly we found countries with higher levels of household disposable income, lower unemployment rates and higher growth in house prices, would have lower default rates on mortgage. However, national debt rules, regulations and chronic and prolonged illness, aren’t significantly associated with defaults on mortgages in our sample countries.

Housing mortgages account for about 75% and 50% of total consumer lending in the developed and developing economies, respectively. Our findings are of particular importance for multinational financial institutions because they hold mortgage loans as a large portion of their assets and therefore higher default rates may significantly lower their market values.

Our results show that lenders should take into account the cultural backgrounds of borrowers when determining how likely it is that they will default. This is in addition to common economic factors, such as income, unemployment, and house prices, socio-demographic factors like divorce and race and health characteristics of borrowers.

For example, multinational financial institutions could promote their mortgage products more in societies where people receive support from their relatives or members of groups. They could also focus on countries where people have a higher propensity to save for the future and are less interested in leisure activities. This could save these institutions a lot in terms of risk, but would also be much better for their customers.

Authors: Reza Tajaddini, Lecturer in Finance, Swinburne University of Technology; Hassan F. Gholipour, Lecturer in Economics, Swinburne University of Technology

Australia’s immigration system is at risk of losing public confidence, undermining its long running success. The government needs to make policy changes to put migrant workers and employers back on equal footing.

The successful “Brexit” campaign to leave the European Union illustrates the consequences of failing to properly manage public perception of immigration. Changes to the United Kingdom’s immigration policy were producing economic benefits and helping to plug gaps in the UK labour market. However, opponents successfully blamed the EU’s free movement of labour for increased immigration and various social and economic problems.

Australia’s situation is different, but there is weak regulation of the employers who hire migrant workers, especially temporary visa holders who are often susceptible to being mistreated. This is serving to marginalise migrants in the labour market and broader society.

Large intakes of economic immigrants have not led to major political upheaval in Australia. Aside from occasional spikes in support for Pauline Hanson’s One Nation, anti-immigration parties have failed to establish ongoing influence. Labor and the Coalition have supported expansive economic immigration policies for much of the post-war era.

The impact of economic immigration on Australia’s population, economy, and labour market is virtually unmatched. Since 1945, immigrants and their immediate descendants have accounted for over half of the nation’s population growth.

More than one in four workers in Australia were born in another country. The foreign-born population as a share of total population is higher in Australia than in any other OECD country, except for Luxembourg and Switzerland.

Australia’s immigration policies have changed significantly in recent years. They have shifted increasingly towards temporary immigration, focused on skilled, working holiday and international student visas.

While this marks a departure from Australia’s legacy of encouraging immigrants to settle on a permanent basis, benefits of these changes are evident.

However reforms are needed to maintain public support for sustained immigration intakes. Most importantly, widespread underpayment and mistreatment of working holidaymakers and international students in the workplace must be addressed urgently.

Recent media reports, government inquiries and academic studies show that mistreatment of temporary migrant workers is not limited to 7-Eleven. Policy changes particularly through strong enforcement of regulations are needed to restore level playing fields for business and the workforce.

Some visa arrangements can cause temporary migrant workers to become dependent on their employers. For example, international students are required to work no more than 40 hours per fortnight.

A small transgression exposes international students to potential visa cancellation and removal. Their resident rights, enrolment in education, and employment are then dependent on employers not sharing any breaches of their visa conditions with the Department of Immigration and Border Protection. Unless these and other arrangements the create dependence on employers are fixed, temporary migrants will remain fearful of seeking redress.

Weak enforcement of employment laws fails to deter unscrupulous employers from underpaying and mistreating temporary migrants and puts honest employers at a competitive disadvantage.

The Fair Work Ombudsman has only 250 inspectors for 2.1 million workplaces and 11.6 million workers. It needs more resources to ensure that our employment laws are enforced in industries with large numbers of temporary migrant workers such as food services, hospitality, retail, and horticulture.

Allocation of temporary skilled 457 visas must reflect genuine skills shortages rather than recruitment problemssome employers experience, which are often the result of the low wages and poor conditions they offer to prospective employees.

Economic immigration in Australia has been managed remarkably successfully. But for the good of the country we must address current challenges that have the potential to undermine public confidence in existing immigration policies.

Authors: Chris F. Wright, Postdoctoral Research Fellow, University of Sydney; Stephen Clibbor, Associate Lecturer, The University of Sydney Business School, University of Sydney

This is an edited extract of a new report published by the Lowy Institute for International Policy.

I think the better question to ask is why the hell anyone in Gen Y would want to buy a house right now?

As a member of Gen Y living in the nation’s most expensive city it’s a question I’ve asked myself many times and, aside from two very fleeting periods in late-2008 and around 2012, it’s been hard to find a good reason to buy.

So if your baby boomer parents are hassling you about rushing into the market to avoid being locked out forever, here are a few responses you can shoot back while you sit down, eat your smashed avo, sip your latte and relax.

1. Australian real estate has never been more expensive

A recent study by global investment bank UBS, using a method developed by a branch of the US Federal Reserve, showed Australian house prices were about 7 per cent above previous peaks in 2003, 2007 and 2010.

What goes up tends to go down, and after each of those peaks house prices tended to stagnate or fall slightly.

And while global real estate markets have been going crazy on low interest rates, Australia has been more insane than just about anywhere else, perhaps excluding Canada, New Zealand and Hong Kong.

Don’t smirk too much if you live outside the Harbour City though, with Melbourne equal fourth and the other three capitals with populations over a million rated “severely unaffordable” for the twelth year in a row, plus plenty of regional areas in that category.

To back up those private sector measures, this is the ABS chart of capital city home prices since 2003. How many other things can you think of that have almost doubled in price over the past 13 years? Certainly not most people’s pay packets.

2. We do not have a property shortage and are heading for a glut

But prices have jumped because we have a terrible housing shortage, I hear the property spruikers respond.

Even in those locations where we might have had a shortage it will soon be replaced by a glut.

According to analysts at Citi, Brisbane is already in a unit glut, Melbourne is on the way and some areas of Sydney are too.

Citi is not alone, with analysts at UBS, Westpac, Morgan Stanley, BIS Shrapnel, Deloitte-Access Economics and even the Reserve Bank, amongst others, warning of an apartment glut.

So why buy now when you can get more choice and cheaper prices later?

3. We are in one of the world’s biggest property bubbles

See above.

Seriously, prices are at record highs in Australia’s two biggest cities, and many other areas, in absolute terms, relative to incomes, relative to rents, relative to just about any other measure you care to name.

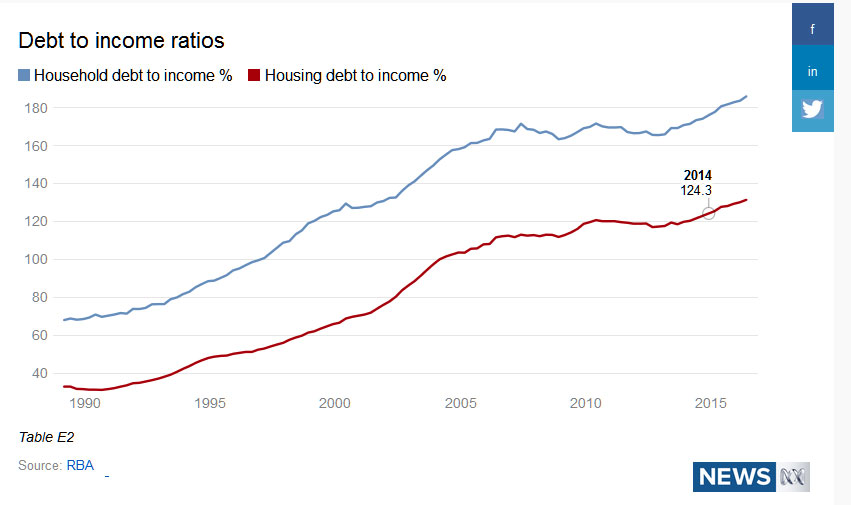

At the same time, household debt, and especially housing debt, is at a record high.

It doesn’t take a genius to figure out why Australian home prices are so high.

The deregulation of the banking system and lower interest rates allowed people to borrow more money, which meant they could keep bidding up the price of homes.

Why is that a bubble?

Basically because you can’t just keep increasing your borrowing faster than your income is growing indefinitely — eventually, even with low interest rates, you simply won’t be able to keep up with the repayments. Ask Greece how this works.

Australia is especially vulnerable since a lot of the money we have borrowed for housing comes from overseas (we’re talking hundreds of billions of dollars here) and if they suddenly stop lending us any more … again, ask Greece.

But you don’t need to take my word for it, ask the OECD, the IMF and the central bank for central bankers, the BIS.

4. Inflation is not going to help you pay off your massive debt

Remember how I said earlier that low interest rates have helped people borrow more money?

Basically, rates are low because inflation is low. Inflation is low because wage growth is slow. Slow wage growth means that the size of your repayments don’t shrink much relative to your pay packet over the decades it takes to pay off a home loan.

This is in contrast to most of the baby boomers. Yes they had to put up with peak mortgage interest rates of 17 per cent for a while, but inflation was also much higher which meant the real size of their debt and repayments fell over the life of the loan.

(Not to mention that the initial size of their loans was generally much lower relative to their incomes than it is now).

5. Interest rates are more likely to rise than fall

There’s more bad news. If inflation does pick up over the medium and longer term, then an inflation-targeting Reserve Bank will have to lift interest rates in response.

While you can get a sub-4 per cent interest rate on many home loans now, more typical interest rates would be around 6.3 per cent, which is the average discount variable rate over the past 12 years.

Most home loans now are for 25 to 30 years, so there’s a fair bet you’ll see rates rise at least a couple of percentage points.

If you believe that we are in an overvalued housing market, then a key danger you should think about is negative equity.

This is where you owe more to the bank on you home loan than your house or flat is worth.

Provided you can afford the loan it doesn’t have to be a disaster, as you can often ride out a fall in prices by not selling and wait for an eventual recovery.

But it could be a long wait and, in the meantime, you are effectively locked into your home and mortgage because if you sold you couldn’t pay back the bank and you’d be bankrupt.

This has other effects on your life.

For example, if you buy a home with your partner and then have relationship problems it becomes very hard to split up when you can’t sell your property. Think about it, who stays there? Does that person pay rent? You have to stay in touch to manage the property even if you now hate each other. Not good.

7. Rents are relatively cheap … and falling

If you don’t own a home, and don’t live with your folks, you’re probably renting.

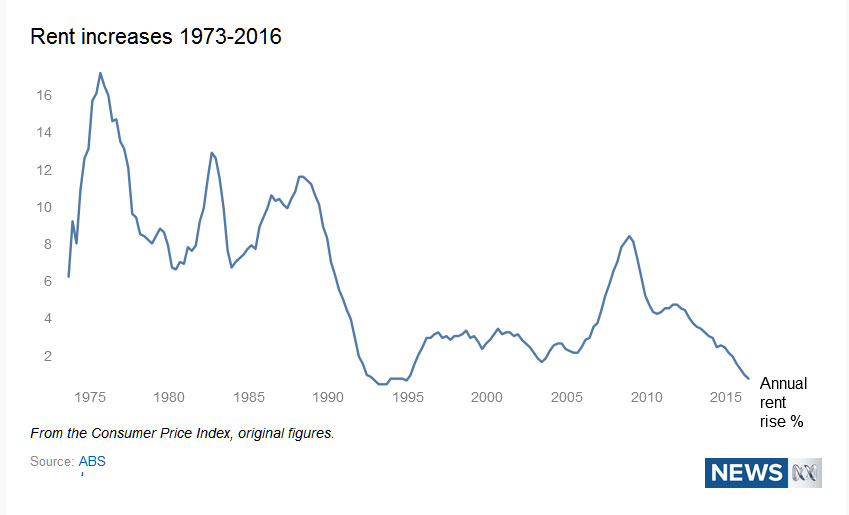

Rent increases also haven’t been as low as they are now since the aftermath of the early-1990s recession.

Not only does this mean that you’re unlikely to be slugged by huge rent increases over the next few years while you save up some money to capitalise on a potential house price crash, it also is a sign such a crash may be coming.

You see, low rental growth is a sign of the property glut we talked about earlier.

Even though purchase prices are being bid up by investors, when they go to rent out these places they struggle to find people to fill them, so they discount their rents.

Landlords with existing tenants become reluctant to raise rents because they can find somewhere cheaper to go.

Even though the negative gearing tax break offsets some of these losses for landlords, if there’s no capital gain then they’re still losing dosh, and eventually they’ll sell.

8. Lifestyle

This is where it gets personal. What do you value in life? And I’m not just talking about smashed avo and lattes.

Where do you want to live? If it’s somewhere you can easily afford to rent but can’t afford to buy, then maybe renting for a bit longer while you save is a smart option.

Do you want to keep travelling? Have kids? Change jobs or career down the track?

Remember, a mortgage is often for 25-30 years and selling a home is potentially a lot more complicated and expensive than exiting a lease.

It’s something best done when you have a pretty good idea about where you want to live and prefer stability over flexibility.

Oh, and don’t forget about the negative equity trap that can lock you into keeping a home you don’t want anymore.

There’s plenty of people in Perth, Darwin, and regional Queensland and Western Australia that are learning all about this the hard way.

Financial stress is now a fact of life for more than one in four Australian workers who say they have low confidence in their financial position and find it difficult to make ends meet.

New research, undertaken by AMP for its 2016 Financial Wellness report, revealed Australians’ confidence in their finances continued to decrease in the past two years from 54 per cent of people confident in 2014 compared to 48 per cent in 2016. Lower confidence is despite an increase in disposable cash held by Australians, rising 6.3 per cent over the past two years.

Vicki Doyle, Director Corporate Superannuation, AMP commented on the impact of financial stress on individuals in the workplace and business productivity.

“Financial stress is a common occurrence in the Australian workforce, with more than 2.8 million employees, representing one in four workers, under financial stress in 2016.

“People who experience financial stress are more likely to be unable to work due to stressrelated sickness, which can affect their health and morale in addition to lowering workplace productivity – at an estimated cost of $47 billion in lost annual revenue for employers.

“It’s important we find ways to address levels of financial stress in the workplace. We know the real difference financial goals can make in preventing and overcoming financial stress. Australians who have clearly defined goals are much more likely to be financially secure,” she said.

Impact on productivity

The research shows financially stressed employees lose on average 6.9 hours of productive work per week and, on average, are absent 1.3 hours per week due to stress-related sickness.

Financial stress is highest among workers in accommodation and food services, with 35 per cent of people financially stressed. Employees are also at high risk of financial stress in healthcare and social assistance (32%), and administrative services (31%).

“In addition to the personal impact of financial stress, we’re also seeing a significant impact on business owners and operators through lost productivity and employee absenteeism, which is particularly high in the hospitality and healthcare industries,” Ms Doyle said.

Importance of goal setting

While the majority of people, at around 80 per cent of the workforce, already have financial goals in-mind, only 18 per cent of these people have a defined plan to achieve their goals.

“Employers can help their employees to bring clarity and shape to their financial goals by supporting financial wellness in the workplace. If employees have well-defined goals and a plan to achieve them, they are less likely to experience financial stress, helping them to be more productive,” Ms Doyle said.

Additional findings

Australians say common triggers for their financial stress are bad debt (50% of stressed workers), the need to save for retirement (35%) and providing for their family (34%). Missing bills and making mortgage repayments also contribute to higher levels of financial stress for 32 and 22 per cent of stressed employees, respectively.

Brisbane is the most financially stressed city, with 30 per cent of workers in this region experiencing financial stress. This is followed by Adelaide (25%), Perth (23%), Sydney (20%) and Melbourne (19%). Darwin and Hobart are the least financially stressed at 18 and 16 per cent, respectively.

Financial stress is highest in the accommodation and food services industry, with 35 per cent of employees stressed. This is followed by healthcare and social services (32%) and administration and support services (31%). Twenty-six per cent of employees in retail jobs say they are financially stressed.

The number of employees experiencing financial stress in the mining industry has significantly increased over the past two years, almost tripling from 9 per cent in 2014 to 26 per cent in 2016.

Females are more likely to experience financial stress with 30 per cent stating this is the case, compared to 19 per cent of males.

Single-parent families are at higher risk of experiencing financial stress (36%) compared to dual-parent households (21%).

Casual workers are more than twice as likely to experience financial stress compared to full-time or part time workers. Fifty-four per cent of casual workers are financially stressed compared to 22 and 27 per cent of full time and part time workers, respectively.

Low income is strongly correlated with financial stress with 34 per cent of people earning less than $50,000 p.a. under stress. However, the incidence of financial stress for highincome earners, earning $150,000 and above, is increasing with 16 per cent stating they are under financial stress compared with only 8 per cent in 2014.

Retirement is a trigger of financial stress, especially among employees aged 50 years and above. Concerns about retirement is the main cause of financial stress for one in five financially-stressed employees aged 50-59 and almost a third of employees aged 60 or above.

Queensland is the state with the highest default risk of 20 per cent, whilst the Australian Capital Territory scored lowest.

Queensland is the state with the highest default risk of 20 per cent, whilst the Australian Capital Territory scored lowest.