Wayne Byres, APRA Chairman spoke at the Financial Stability Institute (FSI) Executives’ Meeting of East Asia-Pacific Central Banks (EMEAP) – Basel Committee on Banking Supervision (BCBS) High Level Meeting, Sydney in Sydney.

He gave APRA a good wrap for is progress on the Basel based supervisory framework. His comments on their mortgage sector interventions were, well, interesting (I would say, too little too late!).

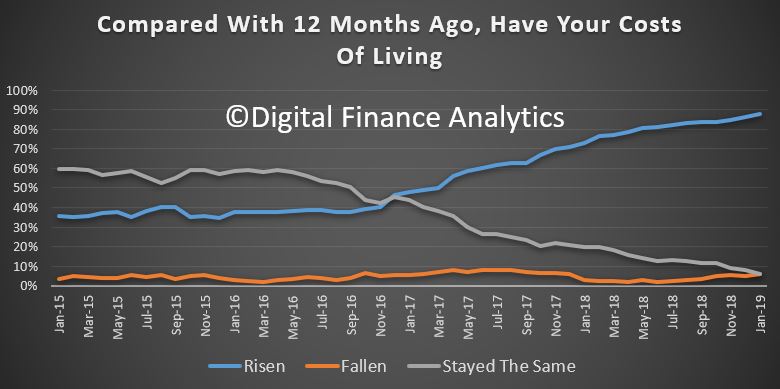

In 2014, we initiated a quite intensive supervisory effort to lift and reinforce lending standards. Our concern was that due to strong competitive pressures, policies were not suitably calibrated to the Australian environment at the time – one of high and rising house prices, high household debt, subdued household income growth and historically low interest rates. We issued additional supervisory guidance, and allocated significant resources to ensure lending policies were suitably aligned with it. Unfortunately, this provided evidence that strong incentives to grow profit and market share often saw lenders weaken and/or override policies in order to generate sales. Moreover, the dangers did not seem to be strongly called out by compliance and audit functions.

To me, the perspective he paints is still far too narrow in terms of really tacking financial stability, Basel is but one element, not the universe!

Here is his introduction…

Translating prudential policy into prudent practice

I’ve been asked to speak this morning about the challenge of translating prudential policy into prudent practice. From a global perspective, that’s an important issue to focus on because policy reform will mean little if it does not translate into improved practices and behaviours.

Translating global reform proposals to improved banking practice is a four-step process:

- global reforms have to be agreed as international standards;

- agreed international standards then need to be translated into domestic regulation;

- bank policies, systems and frameworks then have to be modified to comply with new regulations; and

- actual banking behaviours and practices need to adjust to a new set of constraints on the way business is done.

The first of these steps is pretty much complete. A decade on from the financial crisis, the marathon international policy-making efforts to restore and protect the resilience of the global banking system have, by and large, reached the finish line. Greatly strengthened risk-based capital requirements, a supplementary leverage ratio, with additional buffers for systemically important banks, liquidity and funding requirements in the form of the Liquidity Coverage Ratio (LCR) and the Net Stable Funding Ratio (NSFR), tighter large exposure limits and new margining requirements for OTC derivatives, and an enhanced disclosure regime provide a comprehensive package of prudential policy reforms. The Basel Committee has worked long and hard, and should be commended for the final product.

The Basel Committee’s output – besides lots of paper! – are agreements on the design and calibration of minimum standards. Those agreements are critical to global financial stability. Unfortunately, they are not worth the paper they are written on if they are not translated into domestic regulation by member jurisdictions – the second step in the process I referred to earlier. To repeat the frequent exhortations of the G20 leaders, to achieve the desired objective of a resilient global financial system the reforms need to be implemented in a “full, timely and consistent manner”.

A quick look at the Basel Committee’s latest implementation monitoring report shows something of a mixed scorecard. While the core Basel III risk-based capital requirements and the LCR are largely in force around the world, there has been less progress in some other areas: many requirements are subject to lengthy transitional periods, implementation of the NSFR has been disappointingly slow in a number of jurisdictions, and margining and disclosure requirements can be described as a little patchy.

In short, not all commitments to act have been met by action. That is disappointing. While some delays and trade-offs are valid, on occasion it appears to reflect a regulatory version of the “first mover disadvantage” that supervisors often criticise the industry for – jurisdictions not wanting to do the right thing and move promptly because of a concern that other jurisdictions may not follow suit. This reveals a disappointing penchant to put the interests of banks and their shareholders above that of their depositors and the broader community – something that prudential supervisors must constantly guard against.

For our part, we’ve made good progress on the financial reform agenda in Australia. While the banking sector here escaped the worst of the crisis a decade ago, that didn’t mean APRA was complacent about the importance of building resilience. The core capital, liquidity and funding reforms of Basel III are all in place, with a conservative overlay in many areas. Moreover, we have done this without the extensive transitional periods that have been necessary in other parts of the world. I acknowledge, though, that we don’t have a perfect record and still have a few gaps to close, such as the enhanced Pillar III disclosure requirements. We are committed to addressing these as soon as we can.