He suggests a turning point has been reached. It is now easier than it has been to conceive of a world in which banknotes are used for relatively few payments; that cash becomes a niche payment instrument.

This morning I would like to speak about the shift towards electronic payments; or as the title of my remarks says, the journey towards a near cashless payments system. For some decades, people have been speculating that we might one day go cashless – that we would no longer be using banknotes for regular payments and that almost all payments would be electronic. So far, this speculation has been exactly that – speculation. But it looks like a turning point has been reached. It is now easier than it has been to conceive of a world in which banknotes are used for relatively few payments; that cash becomes a niche payment instrument.

Given this, I would like to structure my remarks around three broad points.

The first is that the shift to electronic payments is occurring quite quickly and it is likely to continue. This shift is a positive development that should promote our collective welfare.

The second is that if we are to realise the benefits of moving to a near cashless payments system, the electronic system needs to offer the functionality, safety and reliability that people require. People need to have confidence that the electronic payment system will be operating when they want to make their payments and that it will deliver the payment services that they need.

The third point is that as we undertake this journey towards a near cashless payment system, there will be a greater focus on the cost of electronic payments. If almost all payments are electronic, then the cost of making these payments matters more than it used to. The electronic system needs to be as efficient as it can be and to be characterised by strong competition. In my view, there is further work to be done here.

1. The Shift to Electronic Payments

The Reserve Bank conducts regular surveys of how Australians make their payments. The next survey will be undertaken in 2019. Until then, perhaps the best illustration of the declining use of cash for transactions is the sharp decline in the number and value of cash withdrawals through ATMs (Graph 1). Around the turn of decade, Australians went to an ATM, on average, around 40 times per year. Today, we go to an ATM around 25 times a year and the downward trend is likely to continue.

Graph 1

At the same time as the use of cash for payments has been declining, the number of electronic transactions has been growing strongly (Graph 2). Today, Australians make, on average, nearly 500 electronic payments a year, up from around 100 per year around the turn of the century.

Graph 2

New payment technologies are being developed that will further encourage this shift to electronic payments. Perhaps the most significant of these is the New Payments Platform, which has made it possible for people to make real-time person-to-person payments without using banknotes. A range of payment apps are also under development that would have the same effect. So the direction of change is clear.

There also continues to be a decline in the use of cheques (Graph 3).[1] In the mid 1990s, Australians, on average, made around 45 cheque payments per year. Today, we make around three per person. Given this trend is likely to continue, it will be appropriate at some point to wind up the cheque system, given the high fixed costs involved in operating the system. We have not reached that point yet, but it may not be too far away. Before we do, it is important that alternative payment methods are available. Progress has been made on this front, but more is required.

Graph 3

It is worth pointing out that despite the decline in cash use, the value of banknotes on issue, relative to the size of the economy, is close to the highest it has been in fifty years. For every Australian there are currently around thirty $50 and fourteen $100 banknotes on issue (Graph 4).

Graph 4

So there is an apparent paradox between the declining use of cash and the rising value of banknotes on issue. The main explanation is that some people, including non-residents, choose to hold a share of their wealth in Australian banknotes. The opportunity cost of doing this is less than it used to be because of the low level of interest rates.

While it is difficult to predict the future, I expect that banknotes will remain part of our payments system for some time to come.

In some situations, paying with banknotes is quicker and more convenient than paying electronically, although this advantage is less than it once was. Some people also simply prefer paying in cash – our 2016 survey indicated that around 14 per cent of Australians had a preference for using cash as a budgeting tool.

Banknotes also allow payments to be made anonymously in a way that is not possible in systems that leave an electronic fingerprint. This privacy aspect is valued by some people. In some circumstances this desire for privacy is entirely legitimate, but in others it has more to do with tax evasion and illegal activities.

Perhaps a more important source of ongoing demand is the fact that using cash does not require the internet to be up, electricity to be working and the banks’ systems to be operational. Banknotes are therefore an important emergency or back-up payment instrument. They are particularly useful in the event of natural disasters or failure of the electronic system. Perhaps one day the various systems will be so reliable that a backup will not be needed, but that day still seems some way off.

Overall, the shift to electronic payments that is occurring makes a lot of sense – it is similar to other aspects of our lives where things that used to be physical have been supplemented with, or replaced by, technology. This shift is likely to promote our collective welfare. I say that even though the Reserve Bank is the producer of banknotes and earns significant income, or as it’s known, seigniorage, for the taxpayer from their use. The greater use of electronic payments can bring efficiency benefits, with lower costs and more functionality and choice for users. One example of this is the reduced tender time involved in card transactions due to contactless technology. There are also non-trivial production and distribution costs involved in the cash system. Some of these are fixed costs, so the average cost of cash transactions is likely to rise as the volume of cash transactions falls. Looking ahead, there is also more limited scope for fundamental innovation in the cash system compared with the scope for dynamic innovation in electronic payments. So this journey is in our national interest.

2. Functionality, Safety and Reliability

I would now like to discuss three interrelated factors that will influence how quickly we undertake that journey. These are: the functionality offered by the electronic system; the safety of that system, and the reliability of that system. The other factor that is also relevant is cost, and I will touch on this a little later.

Functionality

The rapid adoption of contactless payments in Australia shows that Australians change how they pay quite quickly when new functionality is offered. Contactless card payments were slow to take off but once critical mass was established, they grew very quickly. In our 2013 consumer payment study they accounted for around over 20 per cent of point of sale card payments; three years later they accounted for over 60 per cent. So the functionality of the electronic payments system is key.

The development of the electronic payment system took a major step forward earlier this year with the launch of the New Payments Platform (NPP). This system allows people to make payments 24 hours a day, 7 days a week, using just a simple identifier such as a mobile phone number or an email address. It also allows a lot of information to accompany the payment. I expect that over time this extra functionality will further reduce the use of cash in the economy and also improve the efficiency of the electronic system.

The number of transactions through the NPP is steadily increasing (Graph 5). After a relatively low-key start, there are now around 400,000 NPP transactions per day. Over 2 million PayIDs have also been registered, and we expect further growth as the banks continue to roll out services to their customers.

Graph 5

The concept behind the NPP is that so-called ‘overlay’ services are developed, and that these overlay services offer new functionality that utilise the real time capability of the NPP. The first overlay service provides for a basic account-to-account payment. Among the subsequently planned overlay services are ones that will allow someone to send a request to pay, perhaps to a friend for their share of a meal out. Another overlay service would allow a link to a document to be sent with a payment; this could be a payslip or a detailed record of the transaction.

It was originally anticipated that these two overlay services would be up and running not long after the NPP launch. Unfortunately, this timeline has slipped. A number of the major banks have also been slower than was originally expected to roll out NPP functionality to their entire customer bases. This is in contrast to the capability offered by smaller financial institutions, which from Day 1 were able to provide their customers with NPP services. Given the slow pace of roll-out by the banks, and the prospect of delays for additional overlay services, I recently wrote to the major banks on behalf of the Payments System Board seeking updated timelines and a commitment that these timelines will be satisfied. It is important that these commitments are met.

It is worth observing that in other countries where banks have been slow to develop payment applications that meet the needs of the public, other possibilities emerge. China is perhaps the best example of this, with the emergence of QR-code-based payments. I expect that the NPP infrastructure will be the backbone of our electronic payments system for many years to come. But for this to be the case, the system will need to provide the functionality that people require, and it will need to do this on a timely basis.

There are a range of fintech firms that are excited by the capabilities offered by the NPP and the potential for it to be used for innovative payment solutions. In October, the RBA issued a consultation paper seeking views on the functionality and access arrangements for the NPP. In particular we are interested in views on whether the various ways of accessing the NPP, and their various technical and eligibility requirements, are adequate for different business models.

A topic that I get asked about from time to time is whether the functionality of the electronic system would be enhanced by the RBA issuing an electronic version of the Australian dollar, an eAUD. I spoke about this issue at this conference last year, concluding that we did not see a public policy case for moving in this direction at the time. In particular, it is not clear that RBA-issued electronic banknotes would provide something that account-to-account transfers through the banking system do not, particularly with the emergence of the NPP. Another important consideration was the implications for financial stability. A year on, our views have not changed.

Security

A second important influence on the rate at which we shift to a more electronic payments system is the public’s confidence in the security of the system.

Given this, a recent focus of the Payments System Board has been the high and increasing level of fraud in card-not-present transactions (Graph 6). Card-not-present fraud rose by 15 per cent in 2017 and now represents 87 per cent of total scheme card fraud losses.[2] In contrast, the industry has had successes in addressing card-present fraud, with the introduction of chip technology and the switch to PINs. Despite this, growth in e-commerce activity has provided new opportunities for would-be fraudsters.

Graph 6

The Payments System Board identified the rise in card-not-present fraud as a priority for the industry. In August this year, the Board was pleased to welcome AusPayNet’s publication of a draft industry framework to mitigate card-not-present fraud, and supports continued collaboration on this issue.

A separate but not unrelated priority for the industry is to progress work on digital identity. This is another area where barriers to effective coordination can arise. I am pleased that AusPayNet is undertaking work here, under the auspices of the Australian Payments Council. Digital identity is likely to become increasingly important as more and more activity takes place online. The RBA is highly supportive of industry collaboration on this issue and views it as important that substantive progress is made.

More broadly, individuals, businesses, governments and financial institutions all need to be aware of cyber risks. In the RBA’s most recent Financial Stability Review we noted the increasing sophistication of cyber attacks and that regulatory authorities have increased their focus on cyber issues.

Reliability

A third factor is the confidence that people have that they will be able to use the electronic system when they need to make their payments. As I noted earlier, people will still want to hold and use banknotes if they can’t be sure that the electronic system will be available when they need it. In our consumer payments survey in 2016, we asked people about why they held cash in places outside of their wallet. The most common response, from nearly half of respondents, was that it was for emergency transaction needs.

Over recent times, there have been a number of serious operational incidents that have interrupted the payments system. On some occasions these have been caused by problems with the telecommunications companies and at other times by problems at the banks. An operational incident at the RBA in August as a result of problems with a routine fire test also saw a number of RBA core systems unavailable for some hours, including the Fast Settlement Service supporting the NPP.

We all need to do better here. As we rely less on cash, outages affecting retail transactions can have a significant impact on businesses and individuals. So continued effort needs to be made by all participants in the payments system to reduce operational problems. If this does not happen, then it is possible that the Payments System Board could consider setting some standards.

3. Increased focus on Cost and Competition

My third broad point is about the cost of electronic payments and the importance of competition.

As we move to a predominantly electronic world, there will be more focus on the cost of operating the electronic payments systems and how those costs are allocated between those making and receiving payments.

Looking forward, I expect that over time the cost of electronic payments will decline further, due to both advances in technology and economies of scale. Even so, there are significant costs to operate the electronic systems, including costs for front- and back-end systems to maintain accounts, and to deliver functionality and convenience to users, as well as costs in preventing fraud and ensuring resilience. How these costs are managed and who pays for them will have a significant bearing on the efficiency of the overall system.

In terms of card payments, merchants in Australia currently pay less than merchants in many other countries. The comparison with the United States is particularly stark (Graph 7). For credit cards, Australian merchants, on average, pay 0.8 per cent of the transaction value for Mastercard/Visa transactions. In the United States the figure is much higher at around 2.2 per cent. There are also differences in the cost of debit cards and American Express cards between the two countries.

Graph 7

The main reason for the lower merchant costs in Australia is our lower interchange fees. These fees were reduced in Australia as a result of regulation by the Reserve Bank commencing in 2003. The RBA’s reforms reduced average interchange fees in the Mastercard and Visa systems by around 45 basis points. This has been reflected in merchant service fees; indeed, these merchant fees have fallen by somewhat more than the cuts to interchange, likely reflecting an increased focus on card acceptance costs by merchants (Graph 8). In addition, as a result of competitive pressure, including from the removal of no-surcharge rules, fees on American Express and Diners Club have also fallen over time.

Graph 8

Notwithstanding the reduction in interchange fees, these fees still represent, on average, around 60 per cent of the total merchant service fee on credit cards. So they remain an important part of the total cost to merchants. Conversely, these fees mean that the cardholder’s bank gets paid each time the card is used. This has meant that the cost to consumers of using these cards is often low; in some cases, cardholders are actually subsidised to use their card, through reward points and/or interest-free credit. The subsidy is provided by the cardholder’s bank, but ultimately paid for by the merchant.

The close link between interchange and merchant costs means that there continues to be significant focus on interchange and its implications for the distribution of costs between merchants and consumers. For example, there have been recent recommendations from the Black Economy Taskforce and the Productivity Commission for the Reserve Bank to consider regulatory action to lower, or even ban, interchange fees. The Payments System Board will again examine the arguments for lower interchange fees when it next conducts a formal review of the card payments system.

On the competition front, one area that merits close attention is the market for acquiring services. This has come into sharper focus as a result of concerns about the costs to merchants in the debit card system, where most cards allow for transactions to be processed by either of the two networks enabled on the card. The longstanding view of the Payments System Board has been that merchants should at least have the choice of sending the debit payment through the lower cost system, whether that be eftpos or the international scheme.

For merchants to be able to do this though, acquirers need to offer terminals and technical systems enabled to allow least-cost routing. Some acquirers have already completed the necessary work and are attracting new merchants. Others, including the major banks, made commitments earlier in the year regarding the timetable for this work to be completed. Partly on the basis of those commitments, the Payments System Board made a decision not to regulate. Since then, I regret to say there has been slippage by some, who have cited technical problems. It is important that the banks get back on track here. A failure to deliver on commitments or to provide the payment services that the community needs will inevitably lead to calls for further regulation.

4. Looking ahead

Looking beyond interchange and acquiring competition, new technologies open up the prospect of new payment options developing. Recently, there has been much discussion on the role that so-called ‘Big Tech’ firms might eventually play.

These firms have potential advantages over existing providers of payments services. In some cases, their technology and systems are more flexible, they have a greater ability to use and process information, they have well established networks which they can leverage and they are often better at interacting with their users and customers. Given this, one scenario is that these firms become significant players in the payments industry. They might be able to do this through developing new payment applications that provide a commercial return, not through charging for payment services, but by commercialising the value of the information that they obtain as a by-product of offering these services. If this scenario were to play out, it could significantly change the payments landscape, providing both merchants and consumers new payment options at low monetary cost. At the same time though it would raise a number of important issues related to data privacy, ownership and security.

The probability of Big Tech firms entering the payments arena is higher if merchants and consumers feel that the existing payment systems do not offer them the services they need and/or the prices that are being charged are too high. As I noted earlier, where banks have been slow to respond, other payment applications have emerged.

This scenario highlights a broader point. The way that people are charged for payments is complex and is changing: among other things, it is influenced by interchange fees, how the value of information is commercialised, and commercial pressures on banks. It is difficult to predict how things will ultimately play out, but these are issues the Payments System Board continues to keep a close eye on.

5. Summing Up

To conclude, I expect the shift to electronic payments will continue. The issues of functionality, security and reliability, and cost are central to the development of the system. The Payments System Board will be keeping a close eye on these issues.

While I have talked about a near cashless payments system, I want to emphasise that we don’t yet envisage a world without banknotes. The RBA is committed to providing cash consistent with demand by users and to support its distribution. Our development of the Next Generation Banknote series is a clear commitment to ensuring that cash continues to have public confidence and to meet the needs of the community.

The launch of the NPP this year was a big step forward for the industry and a credit to all of the staff at participating organisations who worked hard over the life of the project to bring it to fruition. As I mentioned, there are some key things that need to be done for the full benefits of the NPP to be available to end-users, but I am optimistic that these can be achieved and this new infrastructure can provide great functionality for Australia.

She updated their views on responsible lending, and their new approach to getting better data on the sector. They also to publish a consultation paper on RG 209 revisions and enhancements.

Responsible lending

The National Consumer Credit Protection Act includes an array of obligations designed to protect consumers. Chief among them are the responsible lending provisions – a set of obligations that require lenders and mortgage brokers to do three things before offering a loan to a consumer:

One – the lender or broker must make reasonable inquiries into the requirements, objectives and financial situation of the consumer.

Two – they then need to verify the financial situation of the consumer.

Three – the lender or broker must then make an assessment or preliminary assessment (respectively) of whether the proposed loan is unsuitable for the consumer.

Lenders also have an obligation not to enter into an unsuitable loan contract with the consumer.

The responsible lending provisions are not designed to protect those who invest in residential mortgage-backed securities or other consumer debt securities. However, by protecting consumers in the manner I’ve just described, the provisions necessarily afford investors some secondary protection.

This also means that a failure by a bank that either issues, or sells loans to issuers of, residential mortgage-backed securities to lend responsibly harms both borrowers and investors. As ASIC goes about its responsible lending work, we are cognisant of this fact.

That said, as we all appreciate, compliance with the responsible lending provisions by securitisers alone does not automatically mean a AAA grade rating for a tranche of securities. The provisions set the minimum standard.

ASIC expects and encourages lenders to think about how they can ensure loans provided to consumers are not only ‘not unsuitable’ in accordance with the language of the National Credit Act, but also ‘suitable’ – properly designed and priced to meet the needs of the consumer.

Responsible lending should not be a static, mechanical process devoid of common sense, nor a checkbox exercise. It should be a dynamic, evolving process that looks to continually improve credit quality through the adoption of new practices and new technology, underpinned by basic common sense.

Investors in residential mortgage-backed securities should be looking to those lenders that make this commitment to ongoing improvement.

I should also say something about low-doc loans at this point. As you’ll be aware, many mortgage pools will include some portion of low-doc loans. The definition of a low-doc loan can vary. Nevertheless, it must be said that the idea of a loan provided to a consumer after taking less than reasonable steps to verify the consumer’s financial situation (by obtaining and reviewing reliable documentation) is fundamentallyincompatible with responsible lending.

Investors should be wary of the additional credit and regulatory risks that low-doc loans involve.

There is also a move away from what’s termed ‘low-doc loans’ to the more popular ‘non-confirming loans’. It is fair that all consumers capable of repaying a loan have the opportunity to apply for one, even where the consumer’s circumstances are unusual. But insofar as the phrase ‘non-conforming loans’ could be used as a euphemism for a low-doc or risky consumer loan, our warning remains: lenders and investors face not only higher credit risks, but also the risk of a regulatory response in these situations.

As we begin to see some examples of mortgage stress, particularly as interest rates rise, it becomes more important for investors to be discerning about the securities they invest in. Investors must consider how the mortgage lender goes about lending responsibly.

ASIC’s recent responsible lending initiatives

ASIC’s recent responsible lending initiatives have been informed by three priorities:

Promote responsible lending and appropriate responses to financial difficult

Address the mis-selling of products and promote good consumer outcomes, and

Respond to innovation in financial services and consumer credit and facilitate appropriate reform.

Let me update you on some our initiatives now.

Loan application fraud

ASIC has focused on loan application fraud for some time.

The falsification of loan documents by brokers and lender employees can undermine the integrity of the responsible lending provisions and lead to consumer harm where borrowers obtain loans they can’t afford. It can also harm investors if the loan is securitised.

Insufficient controls to address the risk of loan application fraud and incentive structures that reward poor behaviour jeopardise trust and confidence in the financial sector.

We recognise that lenders have a significant interest (both financial and regulatory) in detecting and responding to loan fraud and ensuring consumers can repay the loans offered to them.

In many cases where we are alerted to alleged loan fraud involving brokers or lender employees, the matters have been brought to our attention by industry, or an industry association, which has already suspended or terminated the individual’s employment, accreditation or aggregator agreement.

We have taken a strategic approach, including civil penalty proceedings against ANZ (Esanda) for breaches of the responsible lending provisions, as they relied on information in falsified payslips submitted by brokers where it had reason to doubt the reliability of that information.

In its judgment, the Court made clear that where unlicensed brokers submit loan applications in reliance on the ‘point of sale’ exemption in regulation 23 of the National Credit Consumer Protection Regulations, lenders have a greater obligation to exercise care. This was the basis for the higher penalties imposed on ANZ relating to the loans submitted by one of the brokers under the point of sale exemption.

In line with our strategic approach, we are undertaking an industry review to better understand the type and level of fraud faced by industry, and how industry goes about preventing, detecting and responding to it.

We are collecting information on industry controls and processes, with a view to promoting best practice. This will help us to improve public confidence in controls for preventing, detecting and responding to loan fraud.

We have met with all of the review participants and have commenced a data collection phase involving selected lenders and aggregators. We expect to release a report next year.

Motor vehicle finance

We are undertaking a review of the car finance industry’s compliance with regulatory obligations relating to responsible lending, collections and hardship.

Our recent work in the car finance industry has identified poor practices such as:

lenders offering loans to consumers that they cannot afford

lenders failing to make reasonable inquiries into, and to verify information about, the consumer’s financial situation, and

consumers being denied important protections under the National Credit Act because of car dealers misrepresenting the loan as a business loan.

We are collecting information from several car financiers to:

understand current trends and practices in the car finance industry

assess the adequacy of their responsible lending, hardship and debt collection processes, and

identify areas of concern or risks that might affect consumers.

We plan to use the findings from the review to drive improved standards of conduct and compliance with regulatory obligations across the industry, including financiers who regularly issue consumer debt securities.

We expect all participants will improve their practices and develop remediation programmes to respond to past instances of poor conduct.

Where we identify concerns, we will be commencing investigations with a view to enforcement action. We have already seen BMW Finance pay $77 million in Australia’s largest consumer credit remediation program. Other financiers engaging in similar conduct can expect a strong response.

We recently issued pilot surveys to participants to obtain feedback on the availability of the data required for the review, with the aim of understanding the systems and methods of data collection and storage. We will use the information provided to further refine our future data requests.

Recurrent data requests

We have also commenced a pilot to obtain home loan data on a recurrent basis.

We will review the results of the pilot in 2019 to assess how to roll out recurrent data requests more broadly.

We will be able to use this data in a number of ways, including to identify potential trends and issues that can help us prioritise regulatory actions and provide feedback to industry. We also envisage releasing the aggregated data to inform consumers and investors more broadly.

We acknowledge that recurrent data collection will have a cost impact on industry, which is why conducting the pilot is so important. We are working with industry and other parts of the government to do this in the most efficient way possible.

By obtaining recurrent granular data, our vision is to reduce the need for ad-hoc and bespoke data collection exercises. This may reduce some costs for the industry in the long run.

Review of Regulatory Guide 209

We are planning to consult on our responsible lending guidance in Regulatory Guide 209 (RG 209).

ASIC first published RG 209 in February 2010 to provide guidance on the processes that we expect licensees to have in place to ensure that consumers are not provided with unsuitable loans.

The Regulatory Guide was last updated in November 2014 following the Cash Store decision.

We believe it’s timely to review the guide, so we can ensure our guidance remains current, addresses emerging issues, and provides a clear indication of what our expectations are.

Since the last revision, there have been a range of developments, including:

thematic ASIC reviews, including ASIC Report 445 and Report 493, which looked at interest-only lending and the conduct of lenders and brokers respectively

law reform in relation to credit cards, with the potential for small amount credit contract and consumer lease reforms

judicial commentary and enforcement outcomes, such as in the Channic, Esanda and Thorn matters, and

commentary from the Royal Commission.

We are still at a reasonably early stage in scoping the kinds of changes or additions that we think would be useful to update.

We intend to engage quite actively about the range of issues that should be addressed, and the approach that we propose to take.

We hope to publish a consultation paper on RG 209 later this year or early next year and will give stakeholders such as the Australian Securitisation Forum the opportunity to make submissions.

Product intervention powers

Treasury recently released draft legislation to introduce design and distribution obligations for persons providing financial services, and a product intervention power for ASIC.

The design and distribution obligations will apply to issuers or distributors of financial products. It is not proposed that these obligations will apply to credit licensees.

However, to complement these obligations, the Government is also introducing a product intervention power for ASIC. This power would enable us to make orders for up to 18 months prohibiting specified conduct in relation to a product, or even ban a product, where we identify a risk of significant consumer detriment. This power is proposed to apply to both financial and credit products.

Under the proposed legislation, this power will only apply prospectively; that is, it will not apply to products that have already been provided. We will need to consult the affected parties prior to making an order.

While the current proposed changes are welcome, we have submitted to the Government that we think the design and distribution obligations should be expanded to cover products regulated by the National Credit Act.

Responsible lending surveillance

Very briefly, I also want to mention a targeted surveillance activity we undertook last year. We reviewed the credit assessment processes of several lenders to assess their compliance with the responsible lending provisions. The participating entities included some issuers of residential mortgage-backed securities.

Following our work, we have seen the participating credit providers improve their processes for the collection and verification of information about the consumers’ financial situation. Industry can expect these kinds of surveillance activities to continue, and regulatory action to follow where breaches of the responsible lending provisions are identified.

Regulatory environment and the future

This is a unique and turbulent time for the financial services industry.

Royal Commission

Three of the rounds of hearings of the Royal Commission have touched on credit matters. Many of the issues raised were already under consideration by ASIC and our work on some of these matters is continuing.

The Royal Commission has produced an interim report that covers the first four rounds of public hearings, including the first round on consumer credit. We have made submissions to the Royal Commission on the content of the interim report.

We look forward to continuing to assist the Government in improving the regulatory framework for financial services in Australia.

ASIC’s enforcement initiatives

ASIC has received additional funding from Government to assist ASIC to accelerate its enforcement in financial services and credit.

Industry should recognise that ASIC will have even greater capacity to pursue breaches of the law we administer and we have very clearly heard the message that the community expects us to utilise court processes as much as possible.

Implementing new supervisory approaches

A key part of our work over the next year will be implementing new supervisory approaches. This work follows additional funding which was recently announced by Government to progress our strategic priorities.

One of our key new initiatives is a Corporate Governance Taskforce, which will undertake targeted reviews of corporate governance practices in large listed entities. This will allow us to shine a light on ‘good’ and ‘poor’ practices observed across these entities. Poor corporate governance practices have led to significant investor and consumer losses as well as a loss of confidence in our markets.

We are also implementing a new and more intensive supervisory approach by regularly placing ASIC staff onsite in major financial institutions to closely monitor their governance and compliance with laws – we call this new programme of work close and continuous monitoring.

These new approaches will help us realise our vision for a fair, strong and efficient financial system for all Australians.

Other initiatives of interest to ASF members

Before I go, there are just a couple of other areas of ASIC work that I want to highlight to you.

Benchmarks Reforms : In July ASIC established a comprehensive regulatory regime for financial benchmarks. This followed on from the work of industry and ASX in May when the new methodology for BBSW came into effect. But it is important for Australian market participants to engage with the changes to LIBOR which will occur at end of 2021. It is critical for all market participants to plan for a post LIBOR world.

Wholesale Market Conduct: We are examining aspects of conduct in the FX Market. We recently reported on High Frequency Trading in the AUD/USD cross rate (Report 597) and we found high frequency trading was 25% of the total, down from a high of 32% in early 2013. We are also examining the practice ‘last look’ and plan to publish our observations and findings in due course.

After plans were originally announced in September, online Australian retail group Kogan.com has launched its home loan offering today (28 November), via Australian Broker.

The website sells everything from technology and homewares to holidays and insurance, and will now begin offering Kogan Money Home Loans.

The products are for a range of borrowers, including first home buyers, refinancers and investors.

Rates for owner-occupiers start from 3.69% per annum, comparison rate 3.70% p.a. or 3.83% p.a. with 100% offset. Investor rates start from 3.89% p.a., comparison rate 3.90% p.a. or 4.03% p.a. with 100% offset.

Kogan lists other benefits as fixed and variable home loans with the option of 100% offset accounts, as well as catering for specialist loans for self-employed, debt consolidation and those with credit issues.

The retailer said it provides a loan calculator to help borrowers get a quicker understanding of how much they can borrow, as well as lending specialists who will call borrowers back “within a few business hours”.

The home loans are funded by Adelaide Bank and Pepper Group.

The Essential Home Loans range, funded by Adelaide Bank, boasts free online redraw, no monthly or ongoing fees on the home loan and $10 per month for the 100% offset account, unlimited extra repayments (up to $20,000 p.a on fixed), interest only options available, and weekly, fortnightly, or monthly repayments (for P&I loans).

The Options Home Loans range funded by Pepper helps those that have unique circumstances, such as having a non-standard income, having suffered previous financial setbacks or are self-employed.

David Shafer, executive director of Kogan.com, said, “Kogan.com delivers products and services that Australians need at some of the most affordable prices in the market, and we’re proud to extend our offerings to the financial services Australians use every day through the launch of Kogan Money Home Loans.

“Digital efficiency continues to be a key driver of our ability to achieve price leadership, and we’ve taken this approach with our Kogan Money Home Loans offering.

“Knowing where to start when getting a home loan can be difficult, especially in a crowded market. Kogan Money Home Loans is making this process easier and more efficient for the many Australians looking to secure a home loan either when purchasing a property or as part of a refinance.

“A large part of Kogan Money Home Loans’ mission is to provide solutions to help people lower the cost of owning homes and investment properties and to achieve property ownership.”

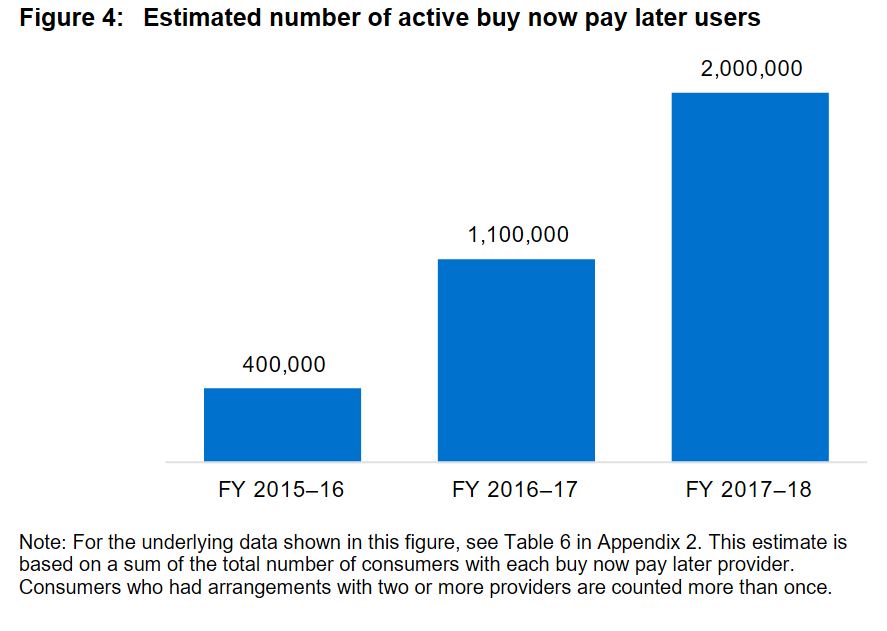

ASIC has released its first review of the rapidly growing buy now pay later industry. The review of this diverse and evolving market has found that buy now pay later arrangements are influencing the spending habits of consumers, especially younger consumers. One in six users had either become overdrawn, delayed bill payments or borrowed additional money because of a buy now pay later arrangement.

They estimate 2 million active buyers use these services.

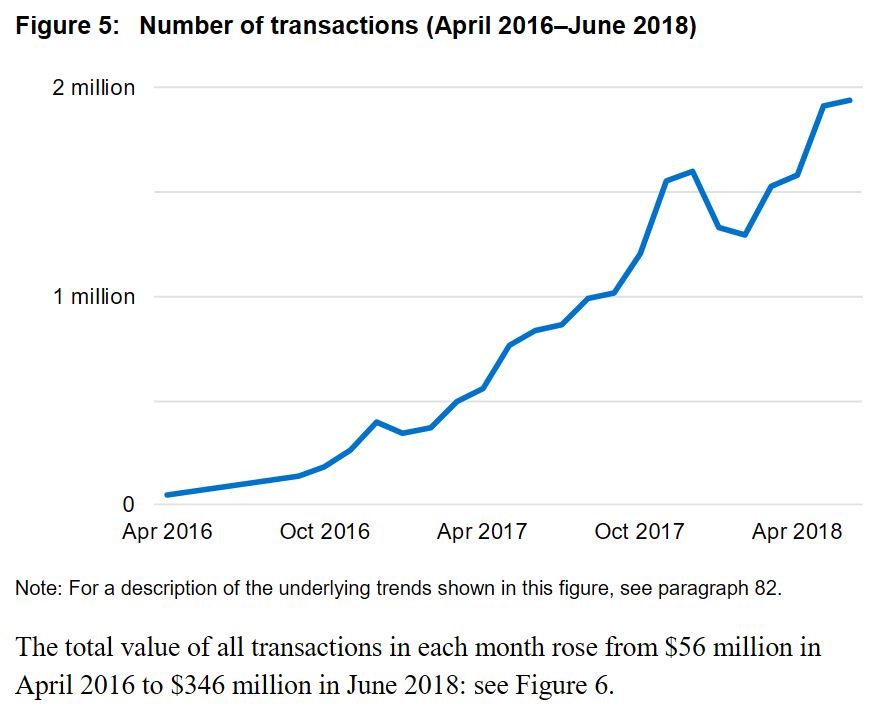

… and transactions are increasing.

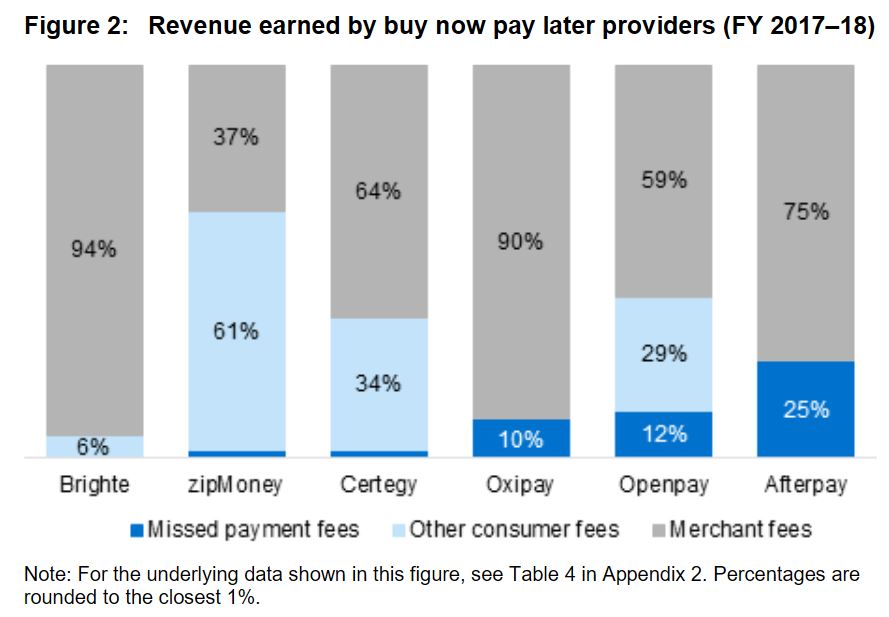

They show that much of the revenue generated comes from merchant fees, but also includes some missed payment and other consumer fees.

A buy now pay later arrangement allows consumers to purchase and obtain goods and services immediately but pay for that purchase over time. While some buy now pay later providers offer fixed term contracts up to 56 days for amounts up to $2,000, other providers offer a line of credit for amounts up to $30,000.

ASIC found that the number of consumers who have used buy now pay later has increased five-fold from 400,000 to 2 million over the financial years 2015-2016 to 2017-2018. The number of transactions has increased from about 50,000 during the month of April 2016 to 1.9 million in June 2018. At 30 June 2018, there was $903m in outstanding buy now pay later balances.

ASIC Commissioner Danielle Press said ‘Although our review found many consumers enjoy using buy now pay later arrangements and plan to continue using them, there are some potential risks for consumers in using these products.

‘The typical buy now pay later consumer is young with 60% of buy now pay later users aged between 18 to 34 years old. We found that buy now pay later arrangements can cause some consumers to become financially overcommitted and liable to paying late fees.’

One in six users had either become overdrawn, delayed bill payments or borrowed additional money because of a buy now pay later arrangement. Most consumers believe that these arrangements allow them to buy more expensive items than they would otherwise and spend more than they normally would. Providers also use behavioural techniques which can influence consumers to make a purchase without careful consideration of the costs.

‘The exponential growth in this industry, along with the risks we have identified, means this will remain an area of ongoing focus for ASIC. One area we will be targeting is where consumers are paying more than they need to for using a buy now pay later arrangement’, said Ms Press.

Given the potential risks to consumers, ASIC supports extending the proposed product intervention powers to all credit facilities regulated under the ASIC Act. Product intervention powers will provide ASIC with a flexible tool kit to address emerging products and services such as buy now pay later arrangements. This will ensure ASIC can take appropriate action where significant consumer detriment is identified.

Background

Buy now pay later arrangements allow consumers to defer payment for purchases from participating merchants and obtain the goods and services immediately.

Under the arrangement, consumers are generally not charged interest. However, some arrangements have an establishment fee and account-keeping fees. Consumers may also be charged a fee if they miss a payment.

Buy now pay later arrangements are available from a range of merchants. For example, these arrangements could be used to finance high-value purchases such as solar power products, health services, travel, and electronics. Buy now pay later arrangements are also available for everyday purchases from retailers such as Big W, Target, Harris Scarfe and Kmart.

These arrangements are not regulated under the National Credit Act and as a result providers are not required to be licensed or to comply with the responsible lending laws that prohibit a lender from providing credit that would be ‘unsuitable’ for the consumer. However, these arrangements are considered ‘credit facilities’ under the ASIC Act meaning that ASIC can take action where a buy now pay later provider engages in conduct that is misleading or unconscionable.

ASIC’s review

ASIC undertook a proactive review of these arrangements to develop a broad understanding of this growing industry and to identify potential risks for consumers. The review examined six providers, four of which are part of larger ASX-listed companies. The buy now pay later arrangements we reviewed were: Afterpay, zipPay, Certegy Ezi-Pay, Oxipay, BrightePay and Openpay.

To better understand how this industry is working in practice, we considered qualitative and quantitative data from July 2016 to June 2018. We also relied on independent consumer research which involved a survey of 600 randomly selected consumers who had recently used a buy now pay later arrangement.

ASIC also tested each of the providers performance in areas such as transparency, dispute resolution and hardship. As a result, all of the providers have made improvements that will benefit consumers. For example, all of the providers are now members of the new Australian Financial Complaints Authority, and all of the providers are reviewing their standard form contracts for potentially unfair contract terms.

ASIC will continue to collect data to monitor the adequacy of consumer protections in this sector and review changes made by buy now pay later providers.

ASIC’s MoneySmart website explains how buy now pay later services work and how consumers can avoid getting into financial trouble when using them.

The Reserve Bank New Zealand says that risks to New Zealand’s financial system have eased over the past six months, but vulnerabilities persist. In particular, households remain exposed to financial shocks due to their large mortgage debt burden.

But they are easing the loan to value restrictions from January 2019.

Up to 20 percent (increased from 15 percent) of new mortgage loans to owner occupiers can have deposits of less than 20 percent.

Up to 5 percent of new mortgage loans to property investors can have deposits of less than 30 percent (lowered from 35 percent).

They say that both mortgage credit growth and house price inflation have eased to more sustainable rates, reducing the riskiness of banks’ new housing lending. In response, we are easing our loan-to-value ratio (LVR) restrictions on banks’ new mortgage loans. If banks’ lending standards are maintained we expect to further ease LVR restrictions over the next few years.

Debt levels also remain high in the agriculture sector, particularly for dairy farms, implying ongoing financial vulnerability. Balance sheets need to be further strengthened. In the medium-term, an industry response to a variety of climate change-related challenges appears likely, requiring investment.

While domestic risks have eased, global financial vulnerability has risen. Significant build-ups in debt and asset prices, and ongoing geopolitical tensions, overhang financial markets. This vulnerability is highlighted by the current elevated price volatility in equity and debt markets. New Zealand’s exposure to these global risks has reduced somewhat, as New Zealand banks have become less reliant on short-term, and foreign, funding.

The domestic banking system remains sound at present. We are using this period of relative calm to reassess whether the banking system has sufficient capital to weather future extreme shocks. Our preliminary view is that higher capital requirements are necessary, so that the banking system can be sufficiently resilient whilst remaining efficient. We will release a final consultation paper on bank capital requirements in December.

The banking system remains profitable, reflecting banks’ low operating costs and strong asset performance. While positive overall, banks’ low costs have been partly achieved through underinvestment in core IT infrastructure and risk management systems in New Zealand. This was highlighted in our review of bank’s conduct and culture with the Financial Markets Authority. We will be jointly reviewing banks’ responses to our review in March 2019, and following up as required.

CBL Insurance Ltd was placed into full liquidation by the High Court on 12 November. Aside from CBL, the insurance sector as a whole is meeting its minimum capital requirements. However, capital strength has declined and a number of insurers are operating with small buffers. The insurance industry must ensure it has sufficient capital to maintain solvency in all business conditions. Our ongoing review of conduct and culture in the insurance sector with the Financial Markets Authority will illuminate the industry’s risk management capability. The review will be released in January 2019.

The NAB chairman has suggested that it is time for the traditional capitalist model to be flipped on its head; via Investor Daily.

Dr Ken Henry, chairperson at National Australia Bank, suggested during round seven of the royal commission that maybe it was time for the banks to rethink its capitalist model.

“The capitalist model is that businesses have no responsibility other than to maximise profits for shareholders. A lot of people over the past 12 months have said that’s all that you should hold boards accountable for.”

Dr Henry said that some people would argue customers were part of pleasing shareholders as treating customers well was important to the long-term interests of shareholders.

“But that approach sees customers as instruments in an instrumental fashion, that the customers are seen as the means by which shareholder profits are secured, rather than the customer being the focus,” he said.

Dr Henry said a debate was now being had over what businesses should be accountable for and the possibility of an alternative solution.

“Within NAB we have thought very deeply about whether we should see our customers in purely instrumental terms, as a means to the end rather than the end to itself.”

Dr Henry noted that views within the bank differ, but added that NAB had realigned its incentives to focus on its customers.

“For what it’s worth, NAB’s view clearly today is that incentives should be aligned with customer experience, customer outcomes to be clear,” he said.

However, as Dr Henry demonstrated on the stand, this has not always been the case for NAB, as counsel-assisting Rowena Orr showed that APRA held the view that NAB’s remuneration was not appropriate.

“APRAs view was that NAB’s remuneration arrangements weren’t operating as they should to support the prudent management of risk at NAB?” said Ms Orr

“That was their view, yes,” said Dr Henry.

As Ms Orr pointed out, APRA’s review of NAB claimed that the bank had a heavy emphasis on profitability measures in individual performance assessments and unlike its peers had no risk-adjusted measures of profitability.

“Well, it was no surprise. Concerning. Absolutely concerning, but not a surprise,” said Dr Henry.

Evidence of the remuneration model was presented by Ms Orr when she questioned Dr Henry why NAB in 2016 gave its executives their full short-term variable remuneration.

Ms Orr pointed out that in 2016, NAB’s bonus pool was set at 100 per cent and that CEO Andrew Thorburn did not even mention the matters when stating the decision.

“So, he (Mr Thorburn) didn’t mention any of those matters, adviser service fees, plan service fees, the bank bills swap rate, the foreign exchange breaches,” said Ms Orr.

Dr Henry said that there was enough information about the issues to have impacted the decision, but it did not concern him that it wasn’t raised.

“You said earlier Dr Henry, that you weren’t sure what the board could have done differently or when it could have. I want to suggest to you squarely that this was a point at which the board could have conducted itself differently. It could have sent a strong message by reducing the pool in response to these very significant compliance issues,” Ms Orr said.

“Of course, we could have, and we decided not to. For very good reasons and I’m still happy with those reasons,” said Dr Henry

The Australian Prudential Regulation Authority (APRA) has released its response to submissions on the introduction of a leverage ratio requirement for authorised deposit-taking institutions (ADIs).

APRA also announced that it is proposing to align the implementation of a range of revisions to the capital framework for ADIs, including the proposed leverage ratio, with the timeline set out in the Basel III framework.

The leverage ratio, which measures the proportion of an ADI’s assets that is funded through equity (capital) rather than debt, is designed to supplement risk-based capital requirements by providing stakeholders with an alternative perspective on ADIs’ capital strength.

APRA released proposals in February 2018 to incorporate a minimum leverage ratio within the ADI prudential framework. Most submissions broadly supported the introduction of a minimum leverage ratio, but raised concerns about the calibration of the minimum requirement and calculation methodology. In response, APRA has proposed to:

set the minimum requirement for ADIs using the internal ratings-based approach (IRB ADIs) to determining capital adequacy at 3.5 per cent, rather than 4 per cent;

keep the leverage ratio for ADIs that use the standardised approach to determine capital adequacy (standardised ADIs) at 3 per cent;

allow standardised ADIs to use Australian accounting standards, rather than the more complex Basel III methodology, to calculate certain parts of the ratio; and

require IRB ADIs to largely follow the Basel III methodology to calculate their leverage ratios.

ADIs’ leverage ratio requirements are outlined in the draft amended Prudential Standard APS 110 Capital Adequacy; APRA is also introducing a new reporting standard, ARS 110.1 Leverage Ratio. APRA is seeking industry feedback on the draft standards and invites interested parties to provide submissions by 22 February 2019.

Small ADIs that qualify for the simplified prudential framework – which is intended to introduce more proportionate and tailored prudential requirements for smaller and less complex ADIs – will be exempt from the leverage ratio requirements, but will still be required to report to APRA under ARS 110.1. Although still consulting on its final design, APRA is considering an eligibility threshold for the simplified framework of $15 billion in total assets, which will be complemented by other qualitative measures.

APRA is now proposing that revisions to the capital framework, initially outlined in February 2018, will come into effect from 1 January 2022, the internationally agreed implementation date set by the Basel Committee on Banking Supervision. APRA had originally proposed an implementation date of 1 January 2021, but is proposing to revise this based on industry concerns about the business impact of moving ahead of international competitors.

In less than six weeks, ten years on from the financial crisis, one of the largest ever reforms to the structure of the UK banking industry comes into force. While most will notice little difference on day one, ring-fencing

the largest UK banks has involved significant changes behind the scenes.

The Bank of England says this reform will make the provision of core banking services more resilient, and protect taxpayers from further bail outs. These are real benefits but are conditional on the ring-fence being maintained over time, meaning this will be a continuous process for both the PRA and the banks.

Financial crises generate significant and persistent costs. The Bank of England has estimated that the costs of crises amount to 75% of GDP on average. The previous crisis resulted in the Government providing £65 billion of capital to RBS and Lloyds to prevent them failing and disrupting the provision of vital banking services to their customers. Since then, a comprehensive regulatory reform package was developed – which in large part has now been implemented – to reduce the likelihood that such a crisis could happen again.

A decade on from the financial crisis, one of the largest ever reforms to the structure of the UK banking industry is coming into force. By 1 January 2019, the largest UK banking groups must have implemented the ‘ring-fencing’ – or separation – of their UK retail business from their international and investment banking operations. This means that the core banking services on which retail and small business customers depend should not be threatened should things go wrong in wholesale financial markets or the global economy.

Banks have now largely completed the ring-fencing of their retail operations, and have done so with little disruption to their customers and counterparties. The PRA’s supervisory focus will turn to ensuring the ring-fences that have been established are effective in practice, and remain so. Ring-fencing both broadens the range of regulatory requirements, and increases the intensity of supervision, for the groups in scope. As such, ring-fencing will remain a focus for the PRA – as well as for the banks themselves – in the coming years.

All large UK banking groups – defined as those with ‘core’ retail deposits greater than £25 billion – are required to implement ring-fencing by 2019. Currently, seven banking groups cross this threshold. Between them, these groups have around £5 trillion of assets, both in the UK and overseas.

The ring-fencing regime is designed to be consistent with the other parts of the post-crisis regulatory framework. The most systemically-important ring-fenced banks will be held to higher capital requirements. The Systemic Risk Buffer will be applied to ring-fenced banks to ensure they are adequately capitalised and resilient to shocks. We expect ring-fenced banks to have, on average, around 1.5 percentage points more high-quality ‘Tier 1’ capital than non-systematically important banks. And a ring-fenced bank will not be able to be capitalised by debt raised externally by its group, which would give rise to so-called ‘double leverage’.

Overall, the Bank estimates that ring-fenced banks’ total loss absorbency will be, on average, around 27% of their risk-weighted assets, higher than the 17% recommended by the ICB. Ring-fencing also helps improve the resolvability of the big UK banking groups. The resolution strategy for groups including ring-fenced banks will typically involve a bail-in at the level of the holding company. Bail-in would recapitalise the relevant entity by passing losses up to the holding company to be borne by shareholders and debt-holders. This should stabilise the group. Structural separation then provides authorities with additional options as part of any subsequent restructuring.

Ring-fencing, together with other elements of the post-crisis regulatory landscape, means that the key providers of important retail banking services are less likely to fail following a shock to the economy or the financial system. But if banks do get into trouble, there will be greater certainty that important banking services will continue to be provided without disrupting customers and without the need for Government bail-outs. This is the key difference ring-fencing delivers should we experience a repeat of the financial crisis.

To comply with the legislation, each banking group has had to restructure to ensure that their new ring-fenced banks can meet prudential requirements on a standalone basis, have their own governance arrangements and have viable business models.

In some cases, a banking group’s ring-fenced bank has been established as a brand new legal entity. Setting up a bank from scratch is a considerable undertaking, even more so for a bank which will have millions of customers from day one. In fact, last year the PRA authorised the three largest new banks ever established in the UK. And by the end of this year, we will have assessed and approved more than 50 applications for senior management positions within these groups, and considered the suitability of their proposed prudential sub-groups, containing hundreds of entities between them. Ring-fencing also resulted in the Bank helping ring-fenced banks undertake around 20 on-boarding operations to payment systems settling across the books of the Bank, and admitting six banks to the Sterling Monetary Framework.

A fintech start-up is celebrating a $25million raise as it continues on its pathway to becoming Australia’s “most innovative home loan provider”; via AustralianBroker.

Athena Home Loans, which is still in its pilot phase, has closed its most recent Series B raise led by Square Peg Capital.

Industry super fund Hostplus and venture firm AirTree also joined the round, taking the group’s total capital raised to date to $45m.

The Series B raise comes six months after the company announced a Series A fund raise led by Macquarie Bank and Square Peg Capital and three months after announcing a strategic partnership with Resimac Group.

Powered by Australia’s first cloud native digital mortgage platform, Athena aims to bypass the banks to connect borrowers to superfund backed loans.

The company was founded by two ex-bankers, Nathan Walsh and Michael Starkey, who said they wanted the journey to home ownership to be faster, cheaper and stress free.

Square Peg Capital invested in Athena in Series A and has further solidified its support of the home loan provider by leading the Series B round.

Venture capitalist and co-founder of Square Peg, Paul Bassat, who also sits on the Athena Board, said investing further into Athena proves the potential they see in the business.

He said, “Having worked with Nathan, Michael and the team over the last year I have enormous admiration for the speed at which they have navigated complex financial systems to develop a robust and customer-centric mortgage service.

“Athena is solving a really important problem for home buyers and is certainly one of the most exciting Fintech companies in Australia.

“We are thrilled to back the team again and look forward to supporting them on this extraordinary journey.”

Industry superannuation fund Hostplus has more than 1.1 million members and $37billion in funds under management.

Hostplus has spearheaded investment in the local start-up ecosystem, with more than $1billion of its fully diversified portfolio committed to Australian venture capital managers.

Hostplus chief investment officer, Sam Sicilia, said that “Athena is a great example of disruptive innovation delivering big savings for home loan borrowers”.

Athena COO Michael Starkey said, “We are delighted to have Hostplus and AirTree joining Athena as investors. Athena’s journey has benefited hugely from the insights and support from some of Australia’s smartest investors. It’s clear the timing has never been better to offer a fairer home loan.”

Athena CEO Nathan Walsh said, “During our pilot, we are already seeing the power of the Athena proposition to save money and change lives.

“A single mum who will be able to pay off her home loan 19 months earlier and save $130,000 over the life of the loan.

“A family with three young kids who will save $40,000 on their home loan can now take the family on the first holiday in years. It’s powerful stuff.”

Commenting on the company’s upcoming launch in Q1 2019, Nathan said, “Our key priorities with the investment will be to continue to innovate our platform, invest in talent and scale the business.