The ABS Residential Price Series also includes transaction data across the country, separated between houses, and other (described as attached). In some cases units may fall into the house bucket, according to the ABS supporting information, due to weaknesses in the data.

We are able to look at the transaction trends, across each state, and they show that to December 2017, the latest date of publication, the volume of settlements overall are significantly lower.

Here is the all Australia plot. The blue area shows the count of houses, the yellow area the volume of transfers for other than houses. We also plot the annualised growth rates. It shows apartment transfers are down more than 7%, and houses down 6.5% to December 2017.

Looking at the individual markets, Sydney both house and unit transfers are more than 8% down to December 2017.

Across the rest of NSW, house transfers are down 3.8% and unit transfers are down 5.8%.

Turning to Melbourne, still seen by many as the “leading market”, houses are down 7.8% and units and apartments, down 10.4% to December 2017.

Across the rest of the state, units were down 8.4% and houses down 7.1%.

So up to Brisbane, where both house and unit transfers have fallen by more than 7% to December 2017.

We can also see falls across the rest of the state, again looking at houses and unit transfers, both of which fell by more than 7%.

Next we go to South Australia. Here in this smaller, yet slightly more buoyant market units were up in Adelaide by 1.2%, whilst house transfers were down 2.8%.

Across the rest of SA, unit transfers were up 5.1% while houses were down 3.8%.

Then across to WA. Here of course property has been under pressure for some time, following a peak in 2009-10 and 2013. In Perth, unit transfers were down 1% and houses up 1.6%.

Across the rest of WA both unit and houses grew by 3.6% and 2.5% respectively.

In Tasmania, another “growth” state, transfers in Hobart were down 3.7% for units, and 7.7% for houses to December 2017

Beyond Hobart, across the rest of the state, house transfers were down 5.1% and units were down 6.9%.

In Darwin, unit transfers rose by 2%, while houses fell 4.7% to December 2017.

Across the rest of NT, unit transfers fell 6.8% and houses rose 2%

Finally, in Canberra, houses fell a significant 7.2% to December 2017, and units a massive 16.5%.

Standing back we see that units in particular have lost momentum, thanks to the lack of momentum in the investment sector, in particular. But more importantly, this data was set before the more recent lending tightening has hit, so expect to see more falls in transaction volumes ahead.

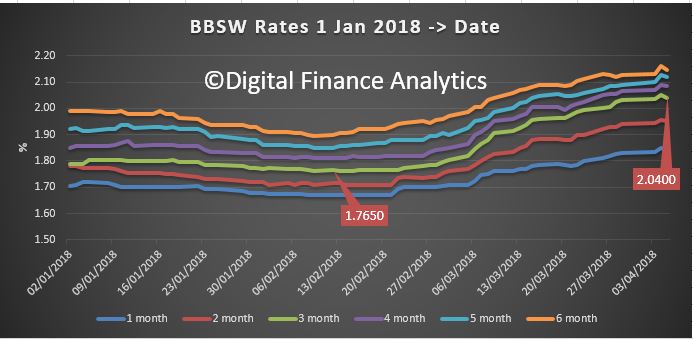

The latest BBSW data shows the trajectory in recent weeks. This will add more pressure to bank funding costs.

The question to consider is whether these moves are reflective of changes in global rates – LIBOR for example is higher (see below) – or whether this reflects the perceived risks in the local bank market in the light of the first rounds from the Royal Commission, which has generally underscored potential risks in their lending books. Or both.

The international rates are probably more the cause of the move of 25 basis points or more, which is significant because it suggests more upward pressure ahead, irrespective of what the RBA may choose to do.

We think mortgage rates will likely (and quietly) go higher in the months ahead.

Loan Market Chairman Sam White says he’s not surprised that fee-for-service is now being supported as a legitimate way of paying brokers in the future, especially when one looks at who is backing this model.

“The biggest winners of a fee-for-service would be the major lenders who would effectively have a reduction in competition and a massive savings to their distribution costs. If I was running a major bank I’d be asking for the same things,” he said.

During a speech last week, Westpac’s CEO Brian Hartzer said the option of customers paying brokers directly could be considered as a way of making commissions more transparent and helping customers make more informed choices. Although, he did add that “the consequences of such a change for all stakeholders would need to be considered carefully”.

White says he understands the logical appeal of fee-for-service from a regulator’s or a consumer’s perspective, but the consequences of adopting that model could result in reduced competition and a much smaller broking market.

“I don’t think it would spell the end of the broker industry, but I think it would pose significant challenges for how the industry operates today and how we work through those. A lot of work would be needed to work that out,” White says.

ASIC wrote in its submission to the royal commission that flat fee remuneration arrangements exist in the Netherlands and that structure has not undermined the existence of the broking sector.

Lack of hard data and evidence

Smartline wrote in its submission to the royal commission that the commission has not received any direct evidence that upfront and trail lead to poor consumer outcomes besides a self-interested and confidential letter from CBA CEO Ian Narev to Stephen Sedgwick for the Retail Banking Remuneration Review. That letter was cited by CBA executives during their royal commission hearings.

Smartline and Loan Market’s White both pointed to ASIC’s review of mortgage broker remuneration from last year as a better data-driven indicator of the broking market and what issues need to be addressed. ASIC concluded that while certain aspects of remuneration needed to be altered, upfront and trail did not lead to poor outcomes overall.

Smartline published the upfront commission rates and loan volumes of its top 20 lenders in 2015, 2016 and 2017 showing that there is no correlation in the level of commission paid by the lender and the volume of loans directed by brokers to that lender.

White also pointed out that one can just look at the data in the banks’ own loan books.

“By their own admission, their books are ‘healthy’ and mortgage brokers represent over half of those customers. There is a disconnect between the service currently being provided by brokers and the call to move to a fee-for-service,” he said.

Welcome to the Property Imperative Weekly to 07 April 2018.

Watch the video, or read the transcript.

In this week’s digest of finance and property news, we start with Paul Keating’s (he of the recession we had to have fame), comment that the housing boom is really over at the recent AFR conference.

He said that the banks were facing tighter controls as a result of the Basel rules on capital adequacy, while financial regulators had had a “gutful” of them. This was likely to lead to changes that would restrict the banks’ ability to lend. He cited APRA’s recent interventions in interest only loans as one example, as they restrict their growth. Keating also said the royal commission into misconduct in the banking and financial services sector would also “make life harder” for the banks and pointed out that banks did not really want to lend to business these days and would “rather just do housing loans”. Finally, he spoke of the “misincentives” within the big banks to grow their business by writing new mortgages, including having a high proportion of interest-only lending.

Anna Bligh speaking at the AFR event, marked last Tuesday her first year as CEO of the Australian Banking Association (ABA) – but said she feels “like 500 years” have already passed. Commenting on the Royal Commission she warned that credit could become tighter ahead. The was she said an opportunity for a major reset, not only in how we do banking but how we think about it, its place in our lives, its role in our economy and, most of all, it’s trustworthiness”.

At the same conference, Rod Simms the Chair of the ACCC speech “Synchronised swimming versus competition in banking” He discussed the results of their recent investigation into mortgage pricing, and also discussed the broader issues of competition versus financial stability in banking. He warned that the industry should be aware of, and respond to, the fact that the drive for consumers to get a better deal out of banking is shared by many beyond the ACCC. Every household in Australia is watching. You can watch our video blog on this for more details.

He specifically called out a lack of vigorous mortgage price competition between the five big Banks, hence “synchronised swimming”. Indeed, he says discounting is not synonymous with vigorous price competition. They saw evidence of communications “referring to the need to avoid disrupting mutually beneficial pricing outcomes”.

He also said residential mortgages and personal banking more generally make one of the strongest cases for data portability and data access by customers to overcome the inertia of changing lenders.

Finally, on competition. he says if we continue to insulate our major banks from the consequences of their poor decisions, we risk stifling the cultural change many say is needed within our major banks to put the needs of their customers first. Vigorous competition is a powerful mechanism for driving improved efficiency, and also for driving improved price and service offerings to customers. It can in fact lead to better stability outcomes.

This puts the ACCC at odds with APRA who recent again stated their preference for financial stability over competition – yet in fact these two elements are not necessarily polar opposites!

Then there was the report from the good people at UBS has published further analysis of the mortgage market, arguing that the Royal Commission outcomes are likely to drive a further material tightening in mortgage underwriting. As a result, they think households “borrowing power” could drop by ~35%, mainly thanks to changes to analysis of expenses, as the HEM benchmark, so much critised in the Inquiry, is revised. Their starting point assumes a family of four has living expenses equal to the HEM ‘Basic’ benchmark of $32,400 p.a. (ie less than the Old Age Pension). This is broadly consistent with the Major banks’ lending practices through 2017. As a result, the borrowing limits provided by the banks’ home loan calculators fell by ~35% (Loan-to-Income ratio fell from ~5-6x to ~3-4x). This leads to a reduction in housing credit and a further potential fall in home prices.

Our latest mortgage stress data, which was picked by Channel Nine and 2GB, thanks to Ross Greenwood, Across Australia, more than 956,000 households are estimated to be now in mortgage stress (last month 924,500). This equates to 30.0% of households. In addition, more than 21,000 of these are in severe stress, no change from last month. We estimate that more than 55,000 households risk 30-day default in the next 12 months. We expect bank portfolio losses to be around 2.8 basis points, though with losses in WA are higher at 4.9 basis points. Flat wages growth, rising living costs and higher real mortgage rates are all adding to the burden. This is not sustainable and we are expecting lending growth to continue to moderate in the months ahead as underwriting standards are tightened and home prices fall further”. The latest household debt to income ratio is now at a record 188.6. You can watch our separate video blog on this important topic.

ABS data this week showed The number of dwellings approved in Australia fell for the fifth straight month in February 2018 in trend terms with a 0.1 per cent decline. Approvals for private sector houses have remained stable at around 10,000 for a number of months. But unit approvals have fallen for five months. Overall, building activity continues to slow from its record high in 2016. And the sizeable fall in the number of apartments and high density dwellings being approved comes at a time when a near record volume are currently under construction. If you assume 18-24 months between approval and completion, then we still have 150,000 or more units, mainly in the eastern urban centres to come on stream. More downward pressure on home prices. This helps to explain the rise in 100% loans on offer via some developers plus additional incentives to try to shift already built, or under construction property.

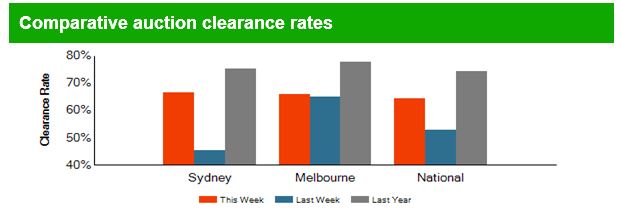

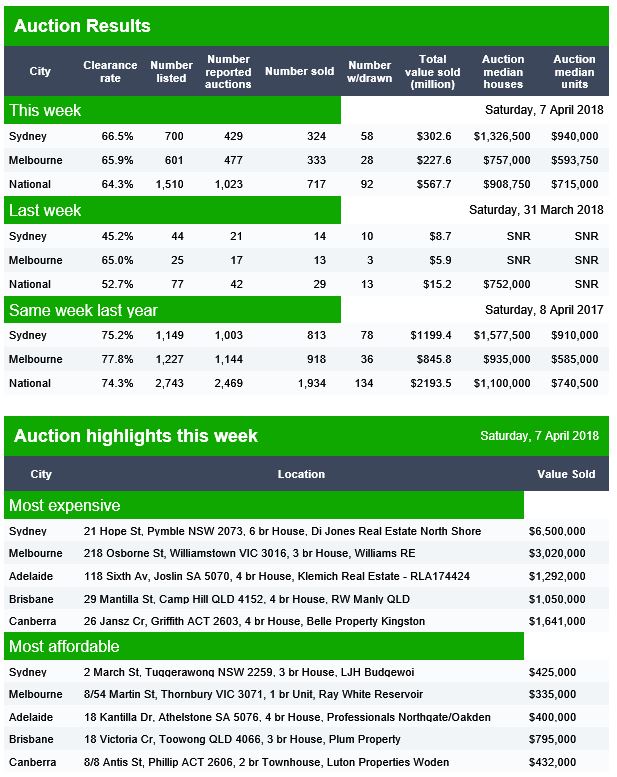

CoreLogic reported last week’s Easter period slowdown saw 670 homes taken to auction across the combined capital cities, down significantly on the week prior when a record number of auctions were held (3,990). The lower volumes last week returned a higher final clearance rate, with 64.8 per cent of homes selling, increasing on the 62.7 per cent the previous week. Both clearance rate and auctions volumes fell across Melbourne last week, with only 152 held and 65.5 per cent clearing, down on the week prior when 2,071 auctions were held across the city returning a slightly higher 65.8 per cent success rate.

Sydney had the highest volume of auctions of all the capital city auction markets last week, with 394 held and a clearance rate of 67.9 per cent, increasing on the previous week’s 61.1 per cent across a higher 1,383 auctions.

Across the smaller capital cities, clearance rates improved week-on-week in Canberra, Perth and Tasmania; however, volumes were significantly lower across each market last week compared to the week prior.

Across the non-capital city auction markets, the Geelong region recorded the strongest clearance rate last week with 100 per cent of the 20 auction results reporting as successful.

The number of homes scheduled to go to auction this week will increase across the combined capital cities with 1,679 currently being tracked by CoreLogic, up from last week when only 670 auctions were held over the Easter period slowdown.

Melbourne is expected to see the most significant increase in volumes this, with 669 properties scheduled for auction, up from 152 auctions held last week. In Sydney, 725 homes are set to go to auction this week, increasing on the 394 held last week.

Outside of Sydney and Melbourne, each of the remaining capital cities will see a higher number of auctions this week compared to last week.

Overall auction activity is set to be lower than one year ago, when 3,517 were held over what was the pre-Easter week last year.

Finally, with local news all looking quite negative, let’s look across to the USA as the most powerful banker in the world, JPMorgan Chase CEO Jamie Dimon, just released his annual letter to shareholders. Given his bank’s massive size (it earned $24.4 billion on $103.6 billion in revenue last year) and reach (it’s a giant in consumer/commercial banking, investment banking and wealth management), Dimon has his figure on the financial pulse.

He says that’s while the US economy seems healthy today and he’s bullish for the “next year or so” he admits that the US is facing some serious economic headwinds.

For one, he’s concerned the unwinding of quantitative easing (QE) could have unintended consequences. Remember- QE is just a fancy name for the trillions of dollars that the Federal Reserve conjured out of thin air.

He said – Since QE has never been done on this scale and we don’t completely know the myriad effects it has had on asset prices, confidence, capital expenditures and other factors, we cannot possibly know all of the effects of its reversal.

We have to deal with the possibility that at one point, the Federal Reserve and other central banks may have to take more drastic action than they currently anticipate – reacting to the markets, not guiding the markets.

And of course the DOW finished the week on a down trend, down 2.34%, and wiping out all the value gained this year, and volatility is way up. Here is a plot of the DOW.

This extreme volatility does suggest the bull market is nearing its end… if it hasn’t ended already. Dimon seems pretty sure we’re in for more volatility and higher interest rates. One scenario that would require higher rates from the Fed is higher inflation:

If growth in America is accelerating, which it seems to be, and any remaining slack in the labor markets is disappearing – and wages start going up, as do commodity prices – then it is not an unreasonable possibility that inflation could go higher than people might expect.

As a result, the Federal Reserve will also need to raise rates faster and higher than people might expect. In this case, markets will get more volatile as all asset prices adjust to a new and maybe not-so-positive environment.

Now– here’s the important part. For the past ten years, the largest buyer of US government debt was the Federal Reserve. But now that QE has ended, the US government just lost its biggest lender.

Dimon thinks other major buyers, including foreign central banks, the Chinese, etc. could also reduce their purchases of US government debt. That, coupled with the US government’s ongoing trade deficits (which will be funded by issuing debt), could also lead to higher rates…

So we could be going into a situation where the Fed will have to raise rates faster and/ or sell more securities, which certainly could lead to more uncertainty and market volatility. Whether this would lead to a recession or not, we don’t know.

We’ll leave you with one final point from Jamie Dimon. He acknowledges markets have a mind of their own, regardless of what the fundamentals say. And he sees a real risk “that volatile and declining markets can lead to a market panic.”

Financial markets have a life of their own and are sometimes barely connected to the real economy (most people don’t pay much attention to the financial markets nor do the markets affect them very much). Volatile markets and/or declining markets generally have been a reaction to the economic environment. Most of the major downturns in the market since the Great Depression reflect negative future expectations due to a potential or real recession. In almost all of these cases, stock markets fell, credit losses increased and credit spreads rose, among other disruptions. The biggest negative effect of volatile markets is that it can create market panic, which could start to slow the growth of the real economy. Because the experience of 2009 is so recent, there is always a chance that people may overreact.

Dimon cautioned investors that interest rates could rise much sooner than they expect. If inflation suddenly comes roaring back. Indeed, it’s entirely possible the 10-year could break above 4% in the near future as inflation returns to 2% and the Fed shrinks its balance sheet.

Dimon also cast a wary eye toward exchange-traded funds, which have seen their popularity multiply since the financial crisis. There are now many ETF products that are considerably more liquid than their underlying assets. In fact far more money than before (about $9 trillion of assets, which represents about 30% of total mutual fund long-term assets) is managed passively in index funds or ETFs (both of which are very easy to get out of). Some of these funds provide far more liquidity to the customer than the underlying assets in the fund, and it is reasonable to worry about what would happen if these funds went into large liquidation.

And Finally America’s net debt currently stands at 77% of GDP (this is already historically high but not unprecedented). The chart below also shows the Congressional Budget Office’s estimate of the total U.S. debt to GDP, assuming a 2% real GDP growth rate. Hopefully, with the right policies they can grow faster than 2%. But more debt does seem on the cards.

And to add to that perspective, we spoke about the recent Brookings report which highlighted the rise in non conforming housing debt in the USA. debt as lending standards are once again being loosened, and risks to mortgage services are rising.

The authors quote former Ginnie Mae president Ted Tozer concerning the stress between Ginnie Mae and their nonbank counterparties.

… Today almost two thirds of Ginnie Mae guaranteed securities are issued by independent mortgage banks. And independent mortgage bankers are using some of the most sophisticated financial engineering that this industry has ever seen. We are also seeing greater dependence on credit lines, securitization involving multiple players, and more frequent trading of servicing rights and all of these things have created a new and challenging environment for Ginnie Mae. . . . In other words, the risk is a lot higher and business models of our issuers are a lot more complex. Add in sharply higher annual volumes, and these risks are amplified many times over. . . . Also, we have depended on sheer luck. Luck that the economy does not fall into recession and increase mortgage delinquencies. Luck that our independent mortgage bankers remain able to access their lines of credit. And luck that nothing critical falls through the cracks…

They say that goldfish have the shortest memory in the Animal Kingdom… something like 3-seconds. But not even a decade after these loans nearly brought down the entire global economy, SUBPRIME IS BACK. In fact it’s one of the fastest growing investments among banks in the United States. Over the last twelve months the subprime volume among US banks doubled, and it’s already on pace to double again this year.

Several major banks have answered a call to clarify where broker allegiances lie, telling the royal commission that brokers act on behalf of customers and are not agents of the banks.

Responding to the Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry’s closing statements, Westpac and Commonwealth Bank of Australia (CBA) have both revealed that they believe brokers act for consumers, rather than the lenders.

In the closing statements, Commissioner Hayne said it would also be of assistance if parties involved in the hearings could seek to answer the question of who a broker acts for.

“It’s a deceptively simple set of questions to ask: who does a mortgage broker act for? You can put it in three ways, I think, and the issue has at least three elements to it. Who does the broker act for? That might be seen as an inquiry about fact or fact and law. Two, who does the customer think the broker is acting for? And third, who does the lender think the broker is acting for? And do you give separate answers at separate steps along the way? If you do, what are the markers that tell you, “I’ve gone from a step where this set of answers is appropriate into the next stage where that set of answers is appropriate”.

“So who does a broker act for, who does the customer think the broker acts for, who does the lender think the broker acts for, are there varying or varied answers at various steps? If there are, what are they?”

In response, Westpac said it was its position that “the broker acts for the customer”.

“Brokers are instructed by and act on behalf of the customers,” the response reads.

“Westpac has direct contractual arrangements with aggregators. Those agreements make it clear that there is no relationship of agency between Westpac and those aggregators.

“Westpac accredits brokers, but the aggregators that Westpac has a contractual relationship with are responsible for managing broker conduct and requirements.”

However, the big four bank said it was “unlikely that customers would think that the broker acts for the lender, rather than for the customer or for themselves as an intermediary or arranger”.

It continued: “The broker’s independence from the lender is one of the things that customers value about brokers (for example, because they offer access to products from multiple lenders).

“To the extent that there is any customer confusion in this regard, such confusion is unlikely to disadvantage any customer. That is because the customer is likely to consider a broker’s recommendation more carefully if they thought that the broker was acting on the lender’s behalf”.

CBA does not consider brokers its agents

Likewise, CBA highlighted that “customers believe that brokers are their agents” and that “customers assess satisfaction with their brokers as if they are their agents”.

It added that “broker firm marketing materials also position brokers as customers’ agents”, highlighting statements from both the MFAA and AFG websites to confirm its position.

Doubling down on its stance, CBA said the evidence put forward to the commission during the hearings “does not establish that CBA regarded an accredited broker as acting as its agent”.

CBA outlined that its agreements describe head groups (i.e. aggregators) as its agents, and then, only in relation to the completion and collection of: customer identification, tax file number disclosure, privacy protection of information forms, and any bank account opening application.

The bank stated: “[A]ccredited mortgage brokers do not act as the agent of CBA. They are authorised by CBA to submit application forms to CBA on behalf of customers who choose to apply for a CBA product.

“When the broker submits the loan application to the lender which the customer has chosen, the broker is acting as the agent of the customer, not as an agent of the lender.”

The bank therefore outlines that its remuneration arrangements with brokers and head groups do not breach its statutory obligations.

“The obligation imposed upon CBA… is an obligation to have adequate arrangements in place to ensure clients are not disadvantaged by any conflict of interest that may arise wholly or partly in relation to credit activities engaged in by CBA or its representatives.

“As brokers are not agents of CBA with respect to the relevant conflict, they are not representatives of CBA, as defined in s 5 of the NCCP Act. Consequently, the obligations under s 47(1)(b) do not apply to broker’s activities, as there is no relevant conflict that arises in relation to credit activities engaged in by CBA or its representatives; only in respect of separate and distinct credit activities engaged in by brokers.”

Question “not capable of a simple answer”

NAB, however, was more guarded in its repsonse.

The major bank said: “This is both a legal and a factual question, which – as posed at the current level of generality – is not capable of a simple answer.

“The answer to this question will depend, in any given case, on matters which are not the subject of evidence presently before the Commission including, amongst other things:

(a) the terms of the relevant contract between the broker and the lender, the broker and the customer, the customer and the lender, the aggregator and the broker, and the aggregator and the lender;

(b) the content of extra-contractual communications between those parties; and

(c) the state of mind of the particular customer and the lender.”

ASIC says it has accepted an enforceable undertaking (EU) from Australia and New Zealand Banking Group Limited (ANZ) after an investigation found that ANZ had failed to provide documented annual reviews to more than 10,000 ‘Prime Access’ customers in the period from 2006 to 2013.

The EU requires ANZ, among other things, to:

pay a community benefit payment totalling $3 million

provide an audited attestation from ANZ senior management to provide ‘reasonable assurance’ that the bank has, since 2014, provided documented annual reviews to customers who were entitled to such reviews, and

provide further audited attestations from ANZ senior management as to the improvements that the bank has made to its compliance systems and processes, and that the design and implementation of those systems and processes will seek to ensure documented annual reviews are provided in accordance with the ANZ Prime Access package.

ASIC Deputy Chair Peter Kell said, ‘Our report into Fees For No Service in October 2016 identified the major financial institutions’ systemic failures in this area, which required affected customers to be fairly compensated and to be provided with the services that they have paid for.

‘ASIC considered it critically important that improved systems and procedures be put in place to ensure this breach of trust could not re-occur. This enforceable undertaking with ANZ will deliver on that commitment,’ he said.

In addition to the EU, ANZ has also agreed to compensate its Prime Access customers who, in the period from 2006 to 2013, did not receive the documented annual reviews that they were entitled to. The compensation program is nearing completion and as at 28 February 2018, ANZ has paid $46.81 million (including earnings) in compensation to these customers (with the total compensation estimated at $46.85 million).

Background

The EU follows an ASIC investigation into ANZ in relation to ANZ’s fees for no service conduct concerning the Prime Access service package which was offered to ANZ’s financial planning customers for an annual fee from 2003. A key component of the package was the provision of a documented annual review of the customer’s financial plan.

As a result of the investigation, ASIC was concerned that:

ANZ had failed to provide documented annual reviews to more than 10,000 Prime Access’ customers who had paid for those reviews

ANZ did not have adequate systems and processes in place to ensure that the ‘Prime Access Service, including the provision of documented annual reviews, was provided to Prime Access customers

from as early as 2008, ANZ Financial Planning was aware of a number of confirmed instances in which documented annual reviews had not been provided to Prime Access customers, and that there was a risk of a broader issue in relation to further Prime Access customers not being provided with documented annual reviews, but the conduct continued until 2013, and ANZ did not breach report the conduct to ASIC until August 2013, and

ANZ failed to comply with section 912A(1)(a) of the Corporations Act which provides that a financial services licensee must do all things necessary to ensure that the financial services covered by the licence are provided efficiently, honestly and fairly and a condition of its Australian Financial Services Licence.

ANZ acknowledged in the EU that ASIC’s concerns were reasonably held.

In ASIC’s post-draft submission to the Productivity Commission’s Inquiry into competition in the Australian financial system, the corporate regulator said it “support[ed] the Productivity Commission’s recognition of the importance of ASIC having a broad, proactive competition mandate”.

“An explicit and broad competition mandate for ASIC would ensure we have a clear basis to consider and promote competition in the financial system,” ASIC’s submission report said.

ASIC also acknowledged previous instances of “uncertainty” regarding “if and how ASIC could consider competition factors”, but pushed back against the idea of actually regulating competition.

“Having a broad competition mandate – to ensure we can appropriately incorporate competition considerations into our existing role as a market conduct regulator – would not make ASIC a competition regulator,” the submission report said.

“We would not have a role in enforcing competition laws – for example, regulating corporate transactions from a competition perspective or monopolies, bringing abuse of market power cases, or regulating pricing and access regimes.”

The regulator added that it supported the co-operation of different regulators in tackling competition issues and the value of learning from each other.

However, ASIC pointed out that each regulator had its own specified area of expertise and “therefore best placed to assess how competition should be weighed and balanced within its area”.

“While we appreciate the Productivity Commission’s concern to ensure that all regulators give appropriate consideration to the competition impacts of their decisions, we are not sure that the role of the competition champion, as envisioned in the draft report, is necessarily the best option to achieve that goal,” the submission report said.

Furthermore, ASIC highlighted the “significant role” of the Australian Competition and Consumer Commission as a regulator of competition “for the entire economy”, as well as its role as a “competition advocate”.

“We acknowledge and support the ACCC’s establishment of its Financial Services Unit, and the role it plays in the financial sector,” the submission report said.

“ASIC maintains a strong working relationship with the ACCC, and welcomes the ACCC’s views and input, including in our work to encourage positive consumer outcomes through effective competition.”

Anna Bligh marked on Tuesday her first year as CEO of the Australian Banking Association (ABA) – but said she feels “like 500 years” have already passed.

In a speech at the AFR Banking and Wealth Summit held yesterday (4 April), the chief executive said the last year has seen the country’s banks confronted with a new tax, and more scrutiny and intervention on top of the 50-odd inquiries and reviews they have faced since the global financial crisis.

Now with the royal commission underway, “without doubt, we have seen some compelling evidence of failures”. But she said some of these issues have already been addressed and remediated by the banks.

The banks face a challenge: they need to lend prudentially and responsibly, be careful and diligent when assessing a customer’s suitability for credit, while also not holding back credit unreasonably or making the process unduly onerous, she said.

The temptation is strong for governments to add complexity and weight to the assessment process to guard against failure, she added.

“At worst, this temptation can tighten access to credit and make it more expensive – this would be a poor outcome for the overwhelming number of customers for whom buying a house is their best financial decision.”

She warned that tightening access to credit could push vulnerable customers out of the regulated banking world and into the far riskier sector of pay day lenders.

“We will all look on with interest as the royal commission does its work and reaches its conclusions. As we do, we should hope that the more measured and sober environment of the judicial setting will produce a more reasoned and balanced outcome for customers and for the system than the overheated corridors of our current federal parliament.”

Transformations are often painful as the old gives way to the new, according to Bligh. But people need to see them as an opportunity.

“An opportunity for a major reset, not only in how we do banking but how we think about it, its place in our lives, its role in our economy and, most of all, its trustworthiness,” Bligh said. “I look forward to the next twelve months with enthusiasm.”