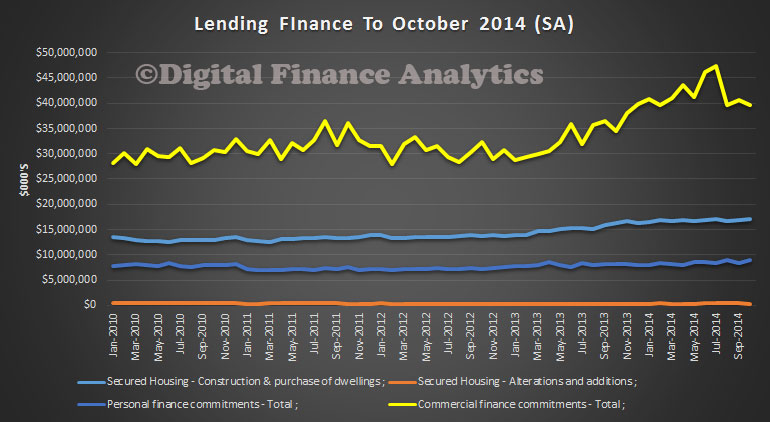

The ABS released their finance data to October 2014. The total value of owner occupied housing commitments excluding alterations and additions rose 0.2% in trend terms, and the seasonally adjusted series rose 1.0%.

The trend series for the value of total personal finance commitments rose 0.7%. Fixed lending commitments rose 1.1% and revolving credit commitments rose 0.1%. The seasonally adjusted series for the value of total personal finance commitments rose 6.5%. Revolving credit commitments rose 11.2% and fixed lending commitments rose 3.0%.

The trend series for the value of total commercial finance commitments fell 2.6%. Revolving credit commitments fell 7.9% and fixed lending commitments fell 0.6%. The seasonally adjusted series for the value of total commercial finance commitments fell 2.2%. Revolving credit commitments fell 11.5%, while fixed lending commitments rose 0.9%.

The trend series for the value of total lease finance commitments rose 0.8% in October 2014 and the seasonally adjusted series fell 4.7%, following a fall of 0.9% in September 2014.

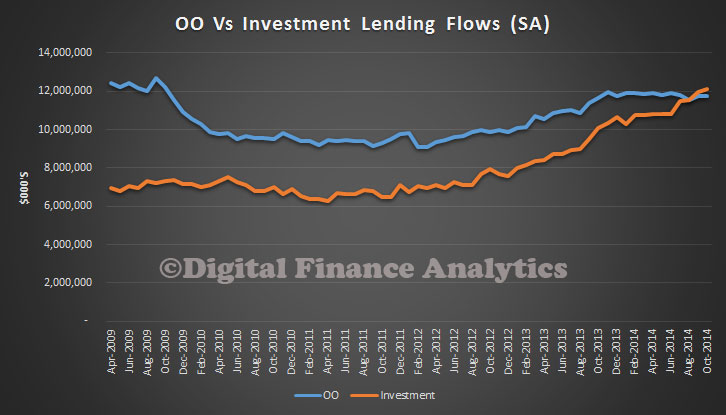

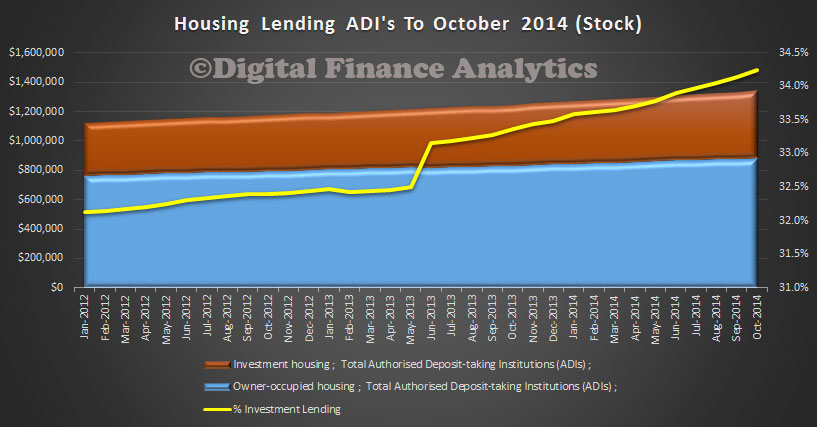

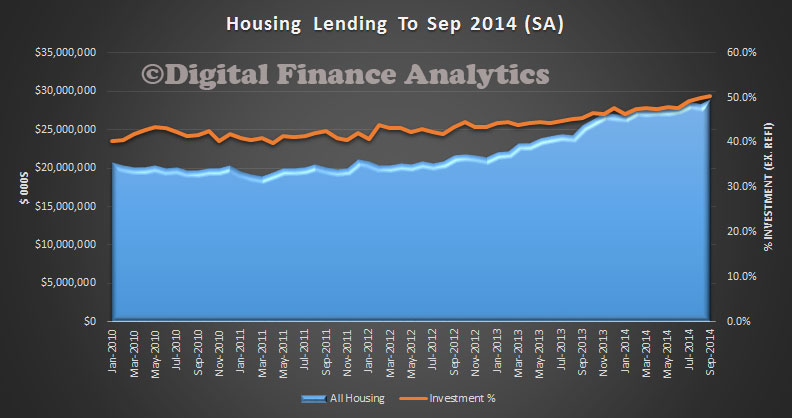

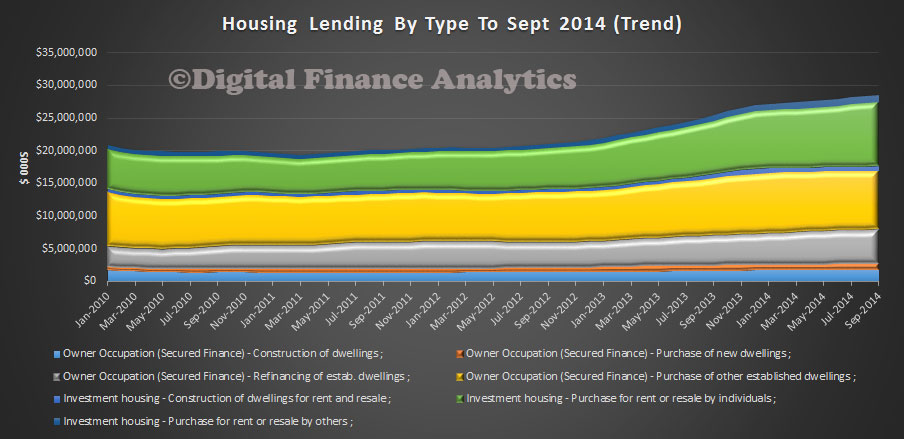

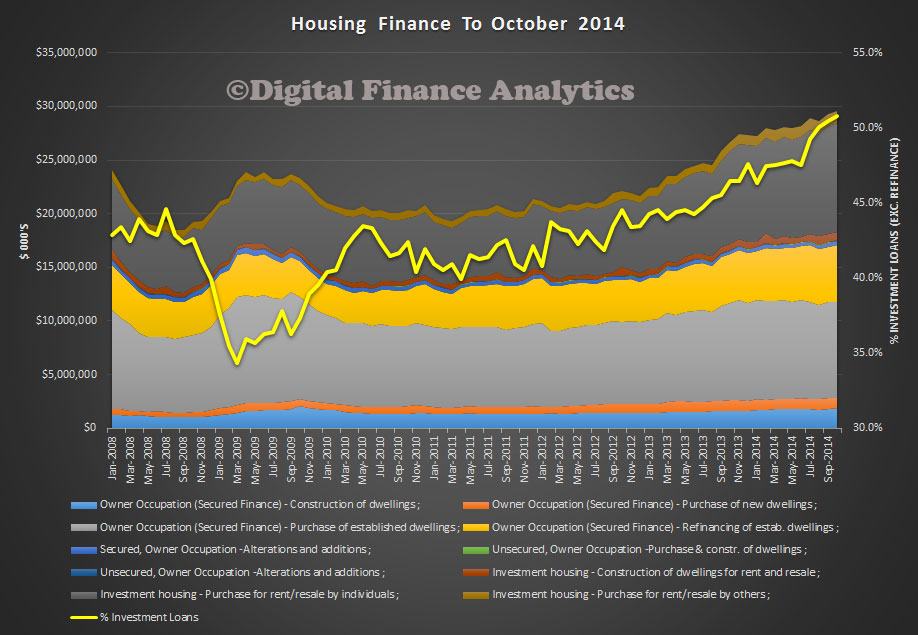

The housing lending data shows another record was achieved last month with 50.8% of mortgages for investment purposes. Another record.

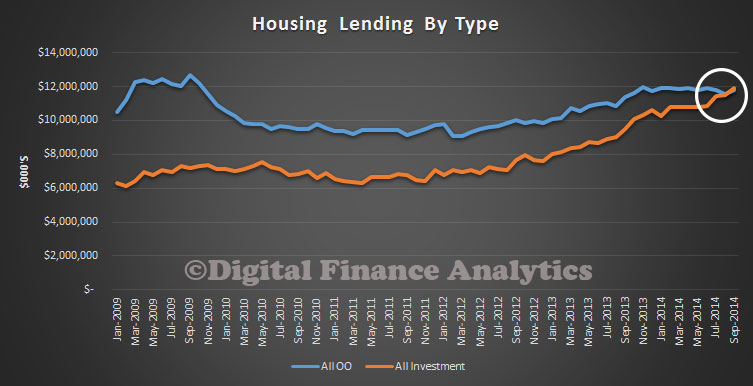

This is starkly show by plotting the flows of owner occupied versus investment loans over the past few years.

This is starkly show by plotting the flows of owner occupied versus investment loans over the past few years.