APRA’s report released today highlights the gaps which still exist across our financial firms, following the CBA analysis. Worryingly, despite firms’ boards and management teams being aware of the risk and accountability deficits which exist, some are not addressing them appropriately. Indeed, in some organsiations, there is still limited visibility of potential non-financial risks.

The Final Report of the Prudential Inquiry into the CBA found that continued financial success dulled the institution’s senses to signals that might have otherwise alerted the Board and senior executives to a deterioration in the bank’s risk profile. This was particularly evident in relation to the management of non-financial risks.

The Prudential Inquiry also found a number of prominent cultural themes; there was a widespread sense of complacency, a reactive stance in dealing with risks, insularity and not learning from experiences and mistakes, and an overly collegial and collaborative working environment that lessened constructive criticism, timely decision-making and a focus on outcomes.

The Final Report listed 35 recommendations focussing on five key levers of change:

more rigorous board and executive committee governance of non-financial risks;

exacting accountability standards reinforced by remuneration practices;

a substantial upgrading of the authority and capability of the operational risk management and compliance functions;

injection of the “should we” question in relation to all dealings with and decisions on customers; and

cultural change that moves the dial from reactive and complacent to empowered, challenging and striving for best practice in risk identification and remediation.

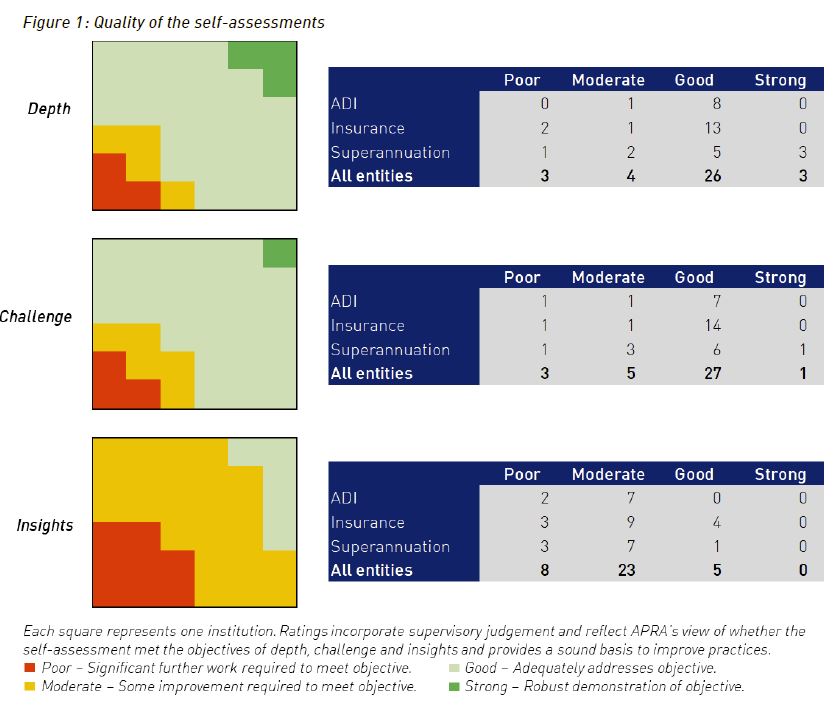

In releasing the Final Report, APRA noted that all regulated financial institutions would benefit from conducting a self-assessment to gauge whether similar issues might exist in their institutions. APRA subsequently wrote to the chairs of 36 institutions requesting a board endorsed written self-assessment of the effectiveness of their own governance, accountability and culture practices. APRA received all of these assessments by mid-December 2018.

APRA’s request for institutions to conduct the self-assessments was intentionally not prescriptive. Boards were asked to determine an approach to the assessment which would provide them with a comprehensive understanding of the effectiveness of governance, accountability and culture, and enable them to form a view as to the extent the ‘tone from the top’ is permeating through and across the institution. As a result, the structure, methodology and format each institution took to completing the self-assessment was considered an important indicator of how seriously boards approached the task.

APRA set three principles that it expected the self-assessments to reflect:

Depth – to enable the board to gain assurance that appropriate governance, accountability and culture are embedded in practices and behaviours, and enforced within the various levels and across the group-wide operations;

Challenge – either independent or self-challenge, to provide the board with fresh perspectives on the strength of governance, accountability and culture (e.g. the assessment should not only reflect the view of the risk function); and

Insights – to inform the board of areas requiring attention and improvement, and how better practice can be achieved.

Emerging themes

While the self-assessments exhibited considerable variation in the number and severity of findings, four themes emerged across all industries:

non-financial risk management requires improvement. This was evidenced through a range of issues identified by institutions, including resource gaps (particularly in the compliance function), blurred roles and responsibilities for risk, and insufficient monitoring and oversight. Institutions acknowledged that historical underinvestment in risk management systems and tools has also contributed to ineffective controls and processes.

accountabilities are not always clear, cascaded, and effectively enforced. Institutions noted that, while senior executive accountabilities are fairly well defined within frameworks, there is less clarity or common understanding of responsibilities at lower levels, and points of handover where risks, controls and processes cut across divisions. This is further undermined by weaknesses in remuneration frameworks and inconsistent application of consequence management.

acknowledged weaknesses are well known and some have been long-standing. The majority of self-assessment findings were reported to be already known to boards and senior leadership. Nevertheless, some issues have been allowed to persist over time, with competing priorities, resource and funding constraints typically cited as the basis for acceptance of slower progress. It was observed that these issues are often only prioritised when there is regulatory scrutiny or after adverse events.

risk culture is not well understood, and therefore may not be reinforcing the desired behaviours. Institutions are putting considerable effort into assessing risk culture, but many continue to face difficulties in measuring, analysing, and understanding culture (and sub-cultures across the institution). It is therefore unclear if these institutions can accurately determine whether their culture is effectively reinforcing desired behaviours (or identify how it would need to be changed to do so).

While the self-assessments contained some in-depth self-reflection and

acknowledgement by institutions of issues within their organisations,

the assessments relating to the effectiveness of boards and senior

leadership were notably less critical. Many self-assessments noted that

the institution is generally well governed, with a respected and

suitably challenging board, strong executive leadership teams and a good

tone from the top, although at the same time acknowledging weaknesses

spanning most or all chapters of the Final Report. This raises the

question of whether boards and senior management have a potential blind

spot when it comes to assessing their own effectiveness.

A new report has found that APRA has “downplayed” and “dismissed” competition risks associated with its regulatory reforms, according to a new report, via InvestorDaily.

A new report commissioned by the Customer Owned Banking Association (COBA) and compiled by Pegasus Economics – titled Reconciling Prudential Regulation with Competition – has found that changes to the regulatory capital framework have undermined competition in the mortgage market.

According

to the report, the Australian Prudential Regulation Authority (APRA)

did not give enough credence to competition risks when applying the

internal ratings basis (IRB) method for calculating risk weights

provided for under Basel II – a banking regulations framework designed

to promote financial stability.

The report found that under Basel

II, credit and operating risk weights determined under the standard

method were “much higher” than those under the IRB method used by the

major banks.

Research from the Reserve Bank of Australia was

cited, in which the central bank found that at the end of June 2015, the

average risk weight of residential mortgage exposures using the IRB

method was 17 per cent, compared to 40 per cent using the standardised

approach used by smaller lenders.

The

report noted that as a result of the disparity, higher costs were

incurred by lenders using the standard method, which influenced the

pricing of lending products and, in turn, reduced competitiveness with

major banks.

According to the report, due to the imbalance, the

major banks have enjoyed a funding cost advantage in excess of $1,000

annually on a residential mortgage of $400,000.

“APRA downplayed

as well as dismissed competition concerns during its implementation of

Basel II and did not follow due process by completing the required

competition assessment checklist in the Regulation Impact Statement it

prepared for Basel II,” the report noted.

“The actions of APRA, in turn, implies the competition-fragility view of banking is endemic to the organisation.

“The

outcomes arising from the interaction of the global financial crisis

(GFC), coupled with the implementation of Basel II, vindicates the

criticisms of Basel II from a competition perspective.”

The report

went on to state: “Through its implementation of Basel II, APRA put

smaller ADIs at a major competitive disadvantage and undermined

competitive neutrality.

“The available evidence suggests the

interaction of the GFC combined with the implementation of Basel II

provided a major fillip to the major banks to the detriment of other

ADIs.”

In addition, the report found that APRA’s decision to

increase the average risk weight for IRB banks from an average of 16 per

cent to a minimum of 25 per cent has prompted some lenders to engage in

“cream skimming” by targeting home loans with the lowest risk profile,

which focused competitive pressures on “high-demand” borrowers.

“Cream

skimming has adverse consequences as it skews the level of risk in

house lending away from the major banks and towards other ADIs who have

to deal with an adversely selected and far riskier group of home loan

applicants,” the report noted.

With APRA set to release a draft

revised capital framework, the COBA-commissioned report called for

policy measures that would ensure regulation does not continue to

“stifle” competition in the banking sector.

The recommendations include:

Addressing

the lack of coordination between prudential regulation and competition

policy and overcoming the “competition-fragility view” of banking, which

the report stated would ensure that competition considerations are

given due deliberation in prudential regulatory policy decisions through

a statutory secondary competition objective for APRA.

Compelling

IRB banks to hold more capital, which the report stated would reduce

the fragility of the banking system and ensure benefits achieved from

injecting greater competition into the banking system can be realised.

Increasing

granularity for risk weights for banks using the standardised approach,

which would “improve competition in home lending”.

Reflecting

on the findings of the report, COBA CEO Michael Lawrence said it’s

“timely” given the “acute need for a competitive and efficient home

lending market”.

“Following the financial services royal

commission, there’s a renewed focus on how regulators and government can

improve competition in banking and ensure major banks are accountable

without reducing financial stability,” Mr Lawrence said.

He

added: “The rules on risk weights mean there is too large a gap between

the amount of capital that smaller banks must hold compared to the major

banks.

“The report says APRA should be looking to close the gap

in risk weights and it should ensure that it does so in a way that

prevents the major banks cream-skimming the lowest-risk home loans.”

Mr

Lawrence recently welcomed the passage of the Treasury Laws Amendment

(Mutual Entities) Bill 2019 through both houses of Parliament.

The

bill includes a new definition for a mutual entity as a company where

each member has no more than one vote, changes to demutualisation rules

to ensure that it is only triggered by an intended demutualisation, not

by other acts such as capital raising, and the creation of a

mutual-specific instrument that can be used to raise capital.

COBA

has also published a ‘Comptetition Agenda’ahead of the federal

election, designed to promote pro-competitive reform in the banking

sector.

A

review of APRA’s 2013 superannuation prudential framework has found it

met its original objectives but must keep evolving to ensure members’

interests are protected.

APRA commenced a post-implementation

review of the framework introduced as part of 2013’s Stronger Super

reforms in May last year, to assess how it had performed in the five

years since it was introduced. Until the package of 13 prudential

standards, supporting guidance and reporting standards came into force,

registrable superannuation entity (RSE) licensees were not subject to

legally binding prudential standards in the same way as other

APRA-regulated entities.

The review found the prudential framework

had materially lifted industry practices in key areas as governance,

risk management and outsourcing. But it also highlighted the need for

APRA to continue strengthening prudential requirements in several areas,

including board appointment processes, management of conflicts of

interest and life insurance in superannuation.

APRA’s review

stated that appropriately managing conflicts of duty and interest is

critical to ensuring that RSE licensees comply with their overarching

obligation to act in the best interests of members.

“However, the Royal Commission noted a number of

areas where RSE licensees appeared not to have managed their conflicts

of interest appropriately, particularly with respect to related party

arrangements,” the regulator said.

While APRA’s review found that

the key procedural requirements of its conflcits management framework

(SPS 521) have “generally been met at an industry-wide level”, the

regulator said it is not clear that the importance of effectively

managing all potential conflicts of interest through a members’ best

interests’ lens is embedded within the culture of all RSE licensees.

APRA’s

proposed enhancements to mitigate conflicts of interest in

superannuation include requiring RSE licensees to explicitly assess the

impact of conflicts of interest on member outcomes and introducing a

two-stage process for the consideration of conflicts of interest.

“First establish interests held, then establish whether those interests give rise to a conflict,” the regulator said.

APRA’s

thematic review noted that policies underlying the conflicts management

framework were in some instances too narrowly focused on conflicts

arising in relation to responsible persons and did not cover conflicts

arising for the RSE licensee as a whole.

“This narrow approach

undertaken by some RSE licensees tended to be characterised by a lack of

consideration of how these conflicts might be perceived by external

stakeholders,” the regulator said.

“The thematic review also

noted that, in many cases, the conflict identification process relied

solely on self-identification by directors or responsible persons, with

no independent review undertaken. It also found a lack of consistency

across the industry in the identification and management of conflicts

when dealing with intra-group services and product providers and other

related parties. These inconsistencies arose, in part, due to

inadequacies in the conflicts management framework for these types of

RSE licensees.”

APRA Deputy Chair Helen Rowell said it was

important that the prudential framework continued to evolve as the

industry developed and regulatory priorities changed.

“The

Stronger Super reforms deliberately focused on ensuring superannuation

trustees that often manage billions of dollars on behalf of members had

the necessary frameworks in place to effectively administer the

fundamentals of operating their business,” Mrs Rowell said.

“As

the industry has matured and lifted its practices, we have shifted our

emphasis to ensuring trustees are focused on enhancing member outcomes,

especially with last December’s package of reforms.

“We are

already taking steps to strengthen the prudential framework in many of

the areas highlighted by the review, and we will look to make further

changes to incorporate its findings as we progress our superannuation

policy priorities. This will include consideration of measures to

address relevant recommendations in the financial services Royal

Commission report and the report on the Productivity Commission’s

superannuation review.”

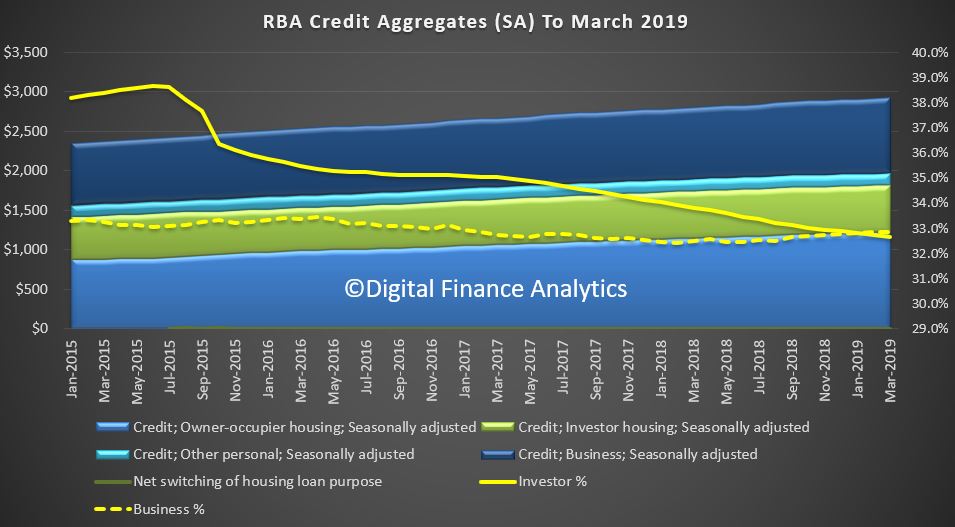

The headline news is the overall housing credit is up, to a new record of $1.82 trillion dollars up 0.31% from last month, or 0.31%. Within that owner occupied lending rose 0.32% to $1.22 trillion dollars and investment lending was flat. 32.7% of lending stock is for investment lending purposes, a slight fall from last month, whilst business lending as a proportion of all lending rose from 32.9% from 32.8% to reach $963.7 billion dollars. Personal credit fell 0.27% or $0.4 billion, to $147.1 billion, and continues to fall.

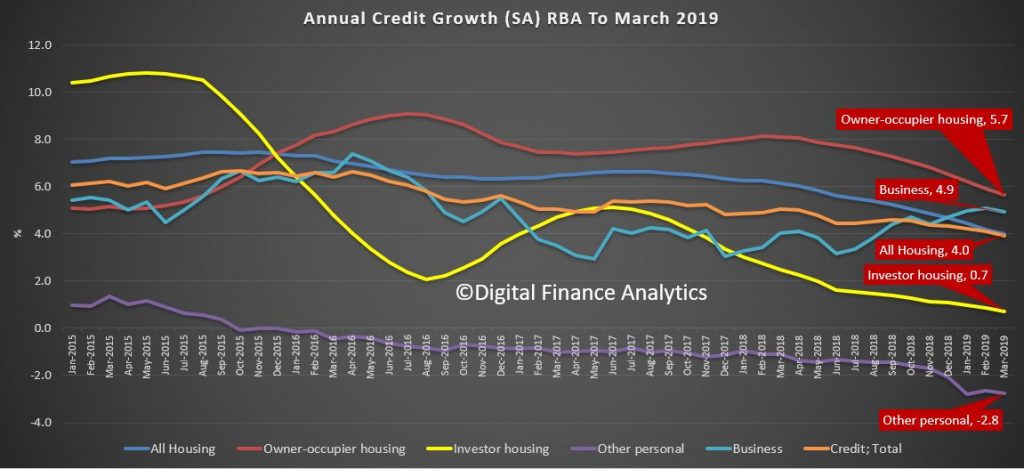

The annualised movements by category shows further weakness, with lending for owner occupied housing now at 5.7%, investment housing lending at 0.7%, giving housing overall growth of just 4% (though still higher than wages growth I would add). Personal credit fell 2.8% over the past year, while business lending rose 4.9% annualised. All these figures are on a seasonally adjusted basis

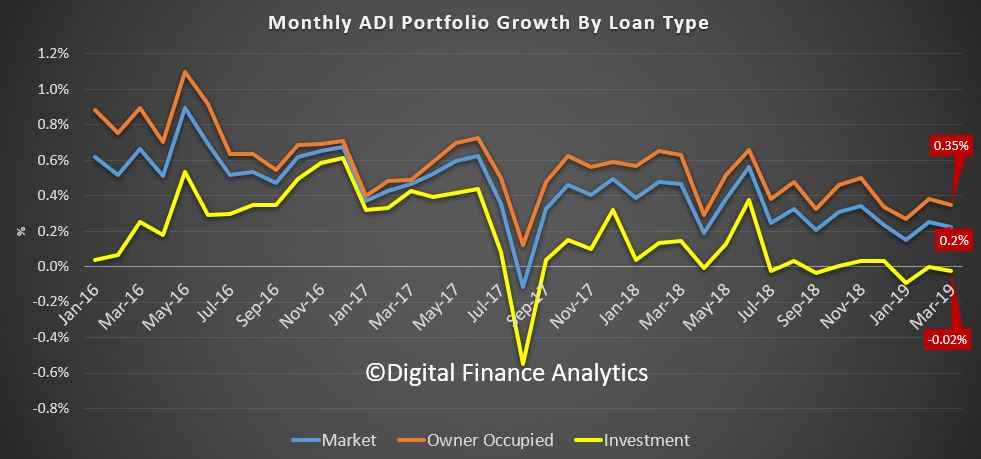

Turning to the APRA data on the banks, owner occupied lending rose 0.35% in March, while investment lending fell by 0.02%, giving total credit growth of just 0.2%. Over the past year owner occupied loans grew by 4.8% (compared with 5.7% at the aggregate level) and investor loans grew 0.4% (compared with 0.7% at the aggregate level). So the banks loan portfolios are growing more slowly than the market.

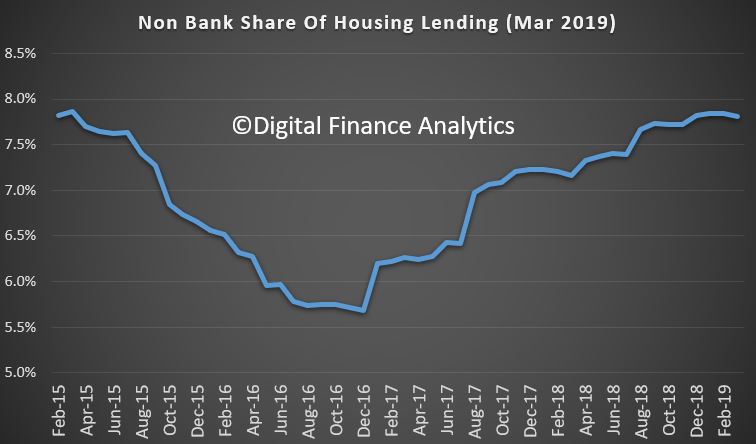

This can be illustrated by comparing the RBA and APRA data (warts and all) to show the non-bank sector is growing faster than the banks. Overall, they have over 7.5% of the market, which is up from the low in December 2016.

In addition, the rate of growth is significantly higher than the banks. Non-bank owner occupied loans are growing at an annual rate of 14%, while investment loans are 2.2%; both significantly higher than the ADI’s. Non-banks have weaker regulation, and more ability to lend. APRA has yet to truly engage with the sector.

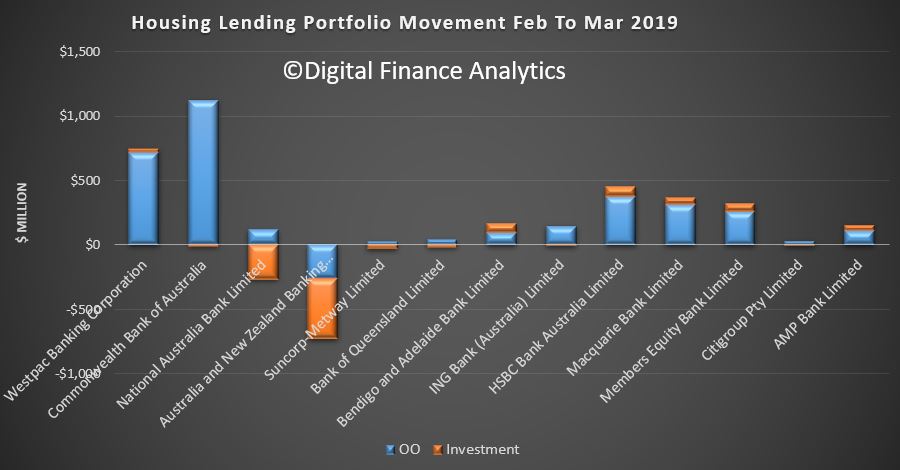

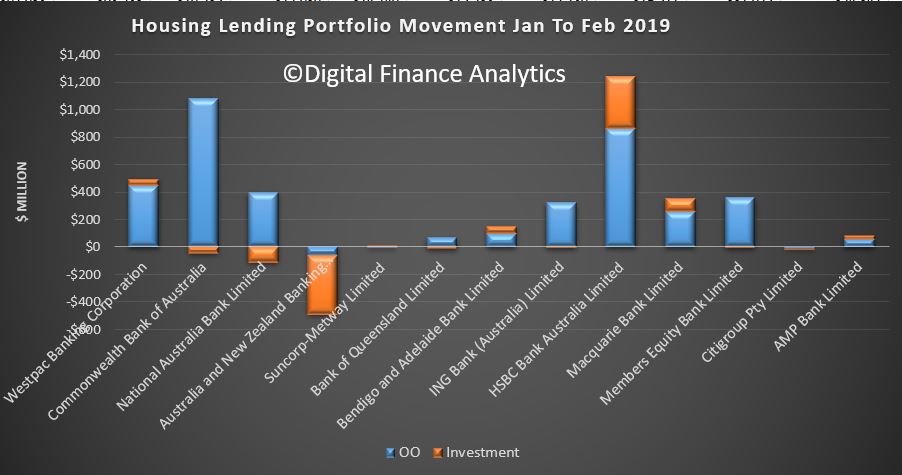

Turning back to the individual lenders, the changes in their portfolios over the month show that Westpac and CBA offered the most new owner occupied loans, while ANZ dropped back, on both owner occupied and investment loans, while NAB dropped investment lending. HSBC, Macquarie and Member Equity Bank (ME) lend more than the regionals.

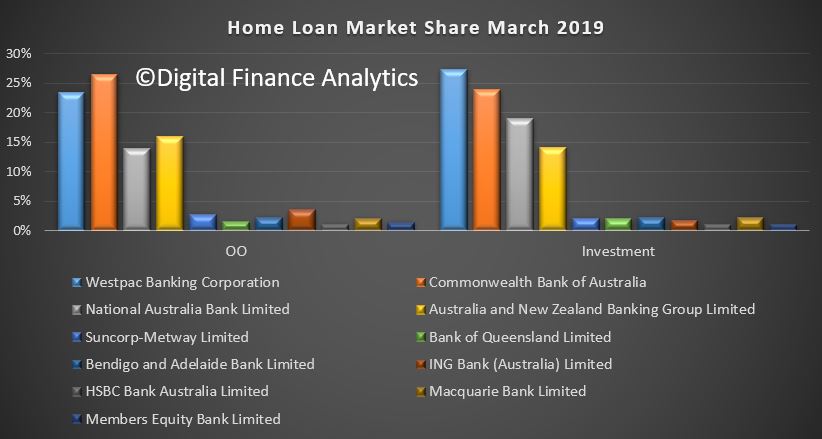

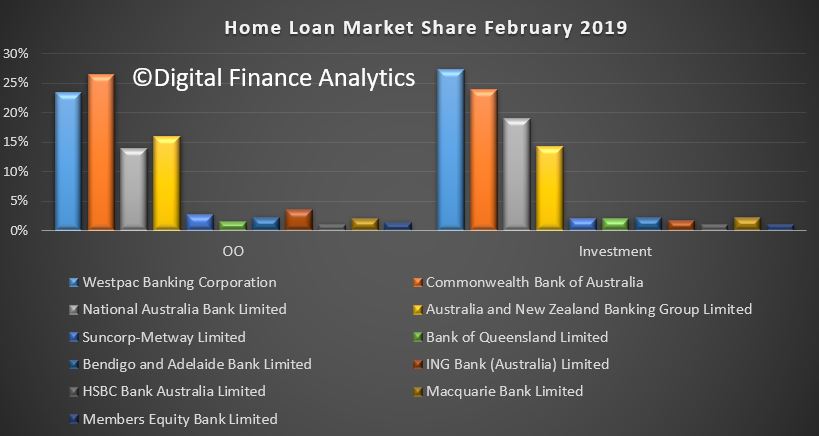

Overall market shares hardly moved, with CBA still the largest owner occupied lending, and Westpac the biggest investor lender.

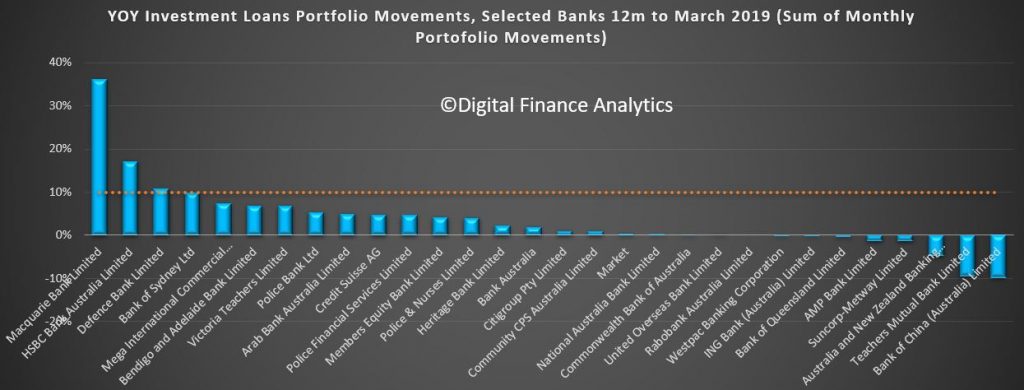

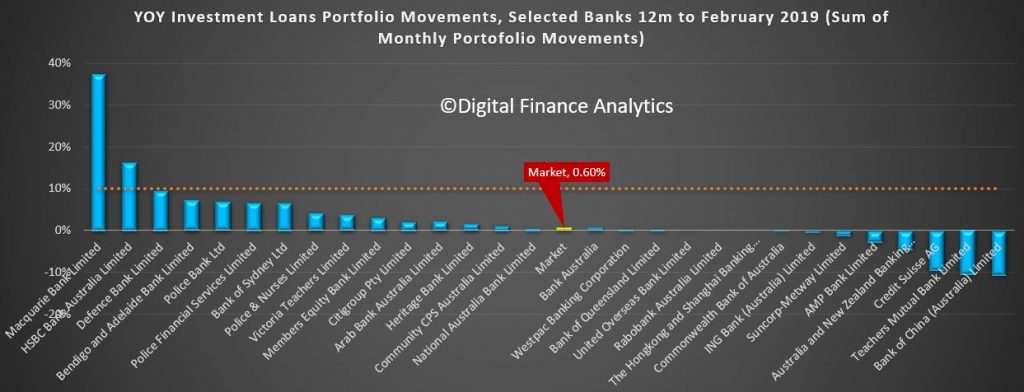

Investment lending growth over the past 12 months has been anemic, but some lenders such as Macquarie are making hay. Of course the old 10% speed limit from APRA has gone now, but the relative growth highlights the fact that the four majors are well below market growth levels – and ANZ the weakest (which is why they said they wanted to lend more).

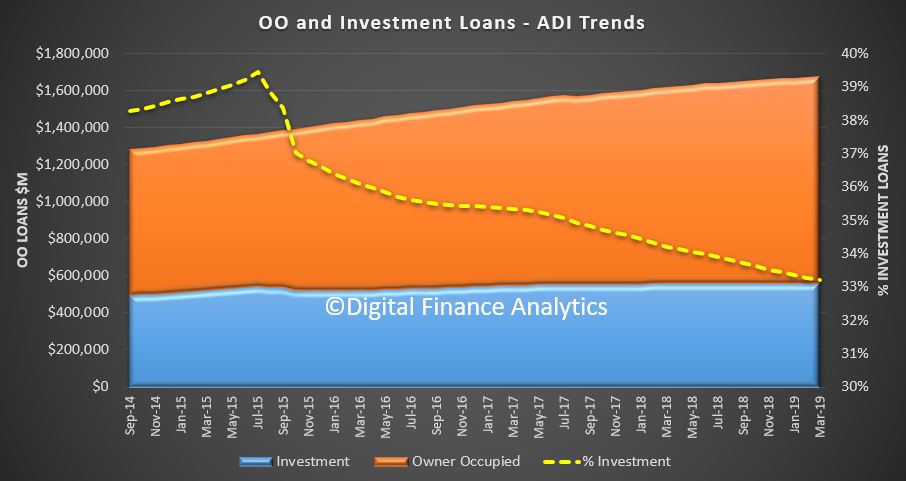

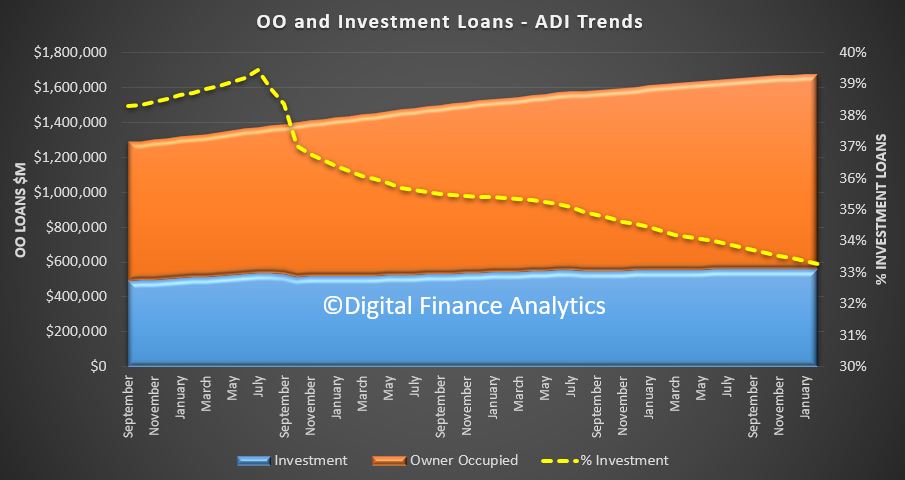

So finally, the total ADI lending book is at $1.68 trillion dollars, with owner occupied loans comprising $1.12 trillion dollars and investment loans $557 billion dollars, and comprising 33.2% of the portfolio – as the ratio continues to fall.

In conclusion, the credit impulse – the rate of change of credit being written is the most significant forward indicator of house price trajectory. The weak state of the market suggests more and significant price falls ahead. Yet despite all this, household debt will continue to rise. There is absolutely no reason to loosen lending requirements, or drop the hurdle rate on these numbers. More households will get into trouble ahead.

The Australian Prudential Regulation Authority (APRA) has released details on the future role and use of enforcement activities in achieving its prudential objectives.

Guiding principals include “risk-based”, “forward-looking”, “outcomes-based” and deterrence impact. Of course the question is, will it really make any difference? Here is the release.

APRA’s new Enforcement Approach, published today, sets out how APRA will approach the use of its enforcement powers to prevent and address serious prudential risks, and to hold entities and individuals to account.

The new Enforcement Approach is founded on the results of its Enforcement Review, which has also been published today. The Review, conducted by APRA Deputy Chair John Lonsdale, made seven recommendations designed to help APRA better leverage its enforcement powers to achieve sound prudential outcomes.

The APRA Members formally commissioned the Enforcement Review last November in response to a range of developments, including the creation of the Banking Executive Accountability Regime, the Prudential Inquiry into Commonwealth Bank of Australia, evidence presented to the Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry, and proposals to give APRA expanded enforcement powers, particularly in superannuation. Mr Lonsdale led the Review, supported by a secretariat within APRA. Mr Lonsdale also utilised an Independent Advisory Panel comprising Dr Robert Austin, ACCC Commissioner Sarah Court and Professor Dimity Kingsford Smith to provide external perspectives and advice.

While APRA’s appetite for taking enforcement action is closely linked to a number of other components of its supervisory approach, the Review was focused on enforcement activity and not APRA’s wider operations

APRA Chair Wayne Byres

said APRA would implement all the recommendations, including:

adopting a “constructively tough” appetite to enforcement and setting it out in a board-endorsed enforcement strategy document;

ensuring APRA supervisors are supported and empowered to hold institutions and individuals to account, and strengthening governance of enforcement-related decisions;

combining APRA’s enforcement, investigation and legal experts in one strengthened support team, and ensuring resources are available to support the pursuit of enforcement action where appropriate; and

strengthening cooperation on enforcement matters with the Australian Securities and Investments Commission (ASIC).

Mr Lonsdale said the Review found APRA had, on the whole, performed well in its primary role of protecting the soundness and stability of institutions. But he said APRA could achieve better outcomes in the future by taking stronger action earlier where entities were not cooperative or open, and by being more willing to set public examples.

“APRA’s strong focus on financial risk has ensured the ongoing stability of Australia’s financial system, even during periods of financial and market stress, and protected the interests of bank depositors, insurance policyholders and superannuation members. But to remain effective, we must continue to evolve and improve, especially in response to the ways in which non-financial risks, such as culture, can impact on prudential outcomes.

“The recommendations of the Review will still mean that APRA as a safety regulator remains focused on preventing harm with the use of non-formal supervisory tools. However, APRA will be more willing to use the full range of its formal powers – such as direction powers and licence conditions – to achieve prudential outcomes and deter unacceptable practices,” Mr Lonsdale said.

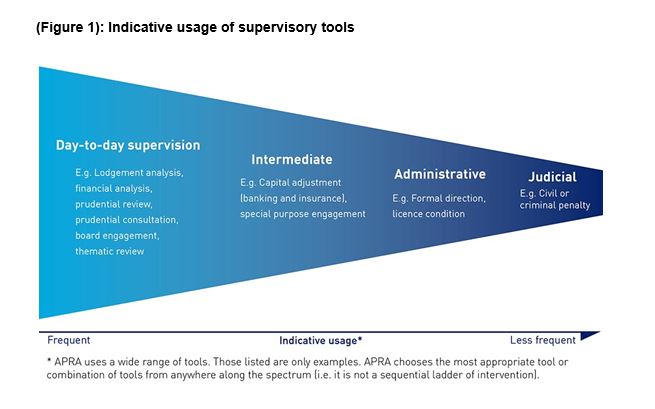

Mr Byres thanked Mr Lonsdale and the APRA Review team for delivering a valuable piece of work that would sharpen APRA’s ability to hold entities and their leaders to account. He said enforcement activity is not intended to be a separate or stand-alone function, but rather a set of tools that APRA supervisors would use more actively, particularly in the case of uncooperative institutions. (See Figure 1)

“Having joined APRA only last October, John brought a fresh set of eyes to the task of examining APRA’s historical approach to enforcement. The Review acknowledges that as a supervision-led prudential regulator, APRA’s primary focus will always be on resolving issues before they cause problems for depositors, insurance policyholders and superannuation members, rather than relying on backward-looking actions after harm has occurred. In most cases, we will continue to achieve this through non-formal tools.

“However, formal enforcement is an important weapon in our armoury when non-formal approaches are not delivering prudential outcomes. Particularly as our powers have recently been strengthened in a number of areas, the new Enforcement Approach will ensure we make use of those powers as the Parliament intended. That means that in future, APRA will be less patient with the time taken by uncooperative entities to remediate issues, more forceful in expressing specific expectations, and prepared to set examples using public enforcement to achieve general deterrence.

“With the release of APRA’s revised Enforcement Approach today, the new enforcement appetite comes into effect immediately,” Mr Byres said.

Mr Byres indicated support for the recommendations on legislative change, and that these would be referred to the Government for its consideration. He also welcomed the recent passage of the Treasury Laws Amendment (Improving Accountability and Member Outcomes in Superannuation Measures No 1) Bill 2019 as a useful complement to APRA’s renewed enforcement appetite.

The Panel, led by Graeme Samuel, currently undertaking a Capability Review of APRA will take into account APRA’s new Enforcement Approach in its work.

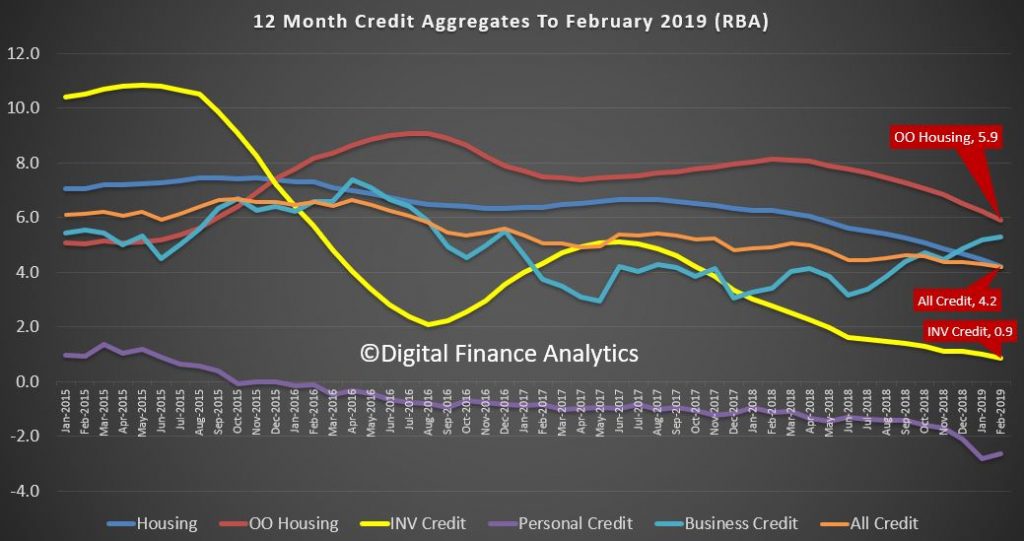

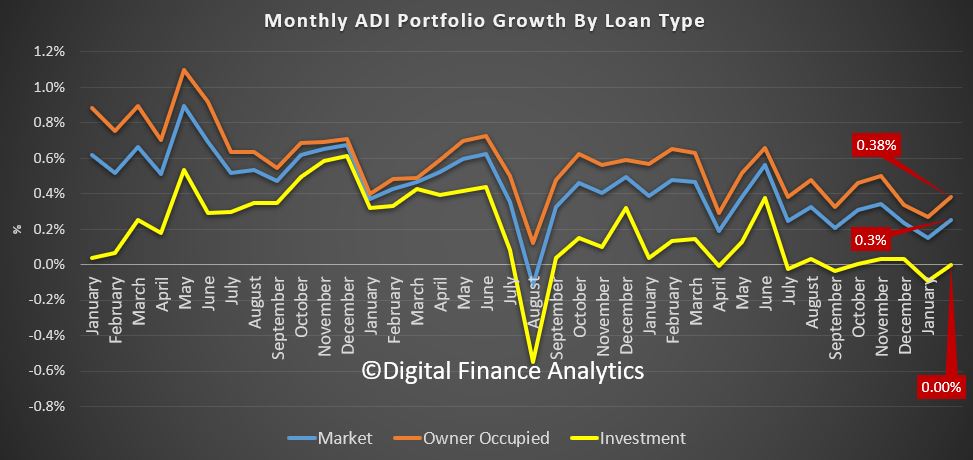

This is quite starkly shown in the RBA’s 12 month series, with total credit annualised growth now standing at 4.2%. Housing credit also fell to the same 4.2% level, from 4.4% a month ago. The fall continues. Within the housing series, lending for owner occupation fell below 6% – down to 5.9% and investment housing lending fell to 0.9% annualised.

The seasonally adjusted RBA data showed that last month total credit for housing grew by 0.31%, up $5.6 billion to $1.81 trillion, another record. Within in that owner occupied lending stock rose 0.42%, seasonally adjusted to $1.22 trillion, up $5.11 billion. Lending for investment property rose 0.09%, or $0.5 billion to $595 billion. Personal credit fell slightly, down 0.07% and business credit rose 0.42% to $960 billion, up $4.06 billion.

The APRA data revealed that ADI growth was lower than the RBA aggregates. Some of this relates to seasonal adjustments plus, as we will see a rise in non-bank lending. The proportion of investment loans less again to 33.3% of loans outstanding.

Total owner occupied loans were $1.11 trillion, up 0.38%, or $4.2 billion, while investor loans were $557 billion, flat compared with last month. This shows the trends month on month, with a slight uptick in February compared to January, as holidays end and the property market spluttered back to life. The next couple of months will be interesting as we watch for a post-Hayne bounce in lending and more loosening of the credit taps, but into a market where demand, is at best anemic.

The portfolio movements are interesting (to the extent the data is reported accurately!), with HSBC growing its footprint by more that one billion across both investor and owner occupied lending. Only Westpac, among the big four grew their investor loans, with ANZ reporting a significant slide (no surprise they said they had gone too conservative, and recently introduce a 10-year interest only investor loan). Macquarie and Members Equity grew their books, with the focus on owner occupied loans.

The overall portfolios did not vary that much, with CBA still the largest owner occupied lender, and Westpac the largest investor lender.

The 12 month investor tracker whilst obsolete in one sense as APRA has removed their focus on a 10% speed limit, is significant, in that the market is now at 0.6% annualised.

But the final part of the story is the non-bank lending. This has to be derived, and we know the RBA data is suspect and delayed. But the gap between the RBA and APRA data shows the trends.

Non Bank annualised owner occupied credit is growing at 17.6%, and investor lending at 4.8%. It is clear the non-banks, with their weaker capital requirements, and greater funding flexibility are making hay. Total non bank credit for housing is now around $142 billion or around 7.8% of housing lending. This ratio has been rising since December 2016, and kicked up in line with the tighter APRA rules being applied to the banks.

We have out doubts that APRA is looking hard enough at these lending pools, especially as we are seeing the rise of higher risk “near-prime” offers to borrowers who cannot get loans from the banks.

So to conclude the rate of credit momentum continues to ease – signalling more home prices ahead. The non-banks sector, currently loosely regulated by APRA is growing fast, and just the before the US falls around the GFC, risks are higher here. And finally, and worryingly, household debt is STILL growing… so more stress and financial pressure ahead.

The Australian Prudential Regulation Authority (APRA) has proposed updating its prudential standard on credit risk management requirements for authorised deposit-taking institutions (ADIs).

Credit risk refers to the possibility that a borrower will fail to meet their obligations to repay a loan, and is usually considered the single largest risk facing an ADI.

APRA has released a discussion paper proposing changes to Prudential Standard APS 220 Credit Quality (APS 220), which requires ADIs to control credit risk by adopting prudent credit risk management policies and procedures.

APS 220 was last substantially updated in 2006, and there has been significant evolution in credit risk practices since then, including more sophisticated analytical techniques and information systems. APRA’s plan to modernise the standard was prompted by its recent supervisory focus on credit standards, and also reflects contemporary credit risk management practices.

The discussion paper outlines APRA’s proposals in the following areas:

Credit risk management – The

revised APS 220 broadens its coverage to include credit standards and the

ongoing monitoring and management of an ADI’s credit portfolio in more

detail. It also incorporates enhanced Board oversight of credit risk and

the need for ADIs to maintain prudent credit risk practices over the

entire credit life-cycle.

Credit standards – The revised

APS 220 incorporate outcomes from APRA’s recent supervisory focus on

credit standards and also addresses recommendation 1.12 from the Final

Report of the Royal Commission in relation to the valuation of land taken

as collateral by ADIs.

Asset classification and

provisioning – The revised APS 220 provides a more consistent

classification of credit exposures, by aligning recent accounting standard

changes on loan provisioning requirements, as well as other guidance on

credit related matters of the Basel Committee on Banking Supervision.

To better describe the

purpose of the revised standard, APRA also proposes renaming it Prudential Standard APS 220 Credit Risk

Management.

The proposed reforms are due to be implemented from 1 July 2020, while an

accompanying prudential practice guide (PPG) and revised reporting standards

will be released for consultation later this year.

In a related development, APRA has also released a letter to industry

expressing concerns related to ADIs’ increasing exposure to funding agreements

with third party lenders, including peer to peer (P2P) lenders.

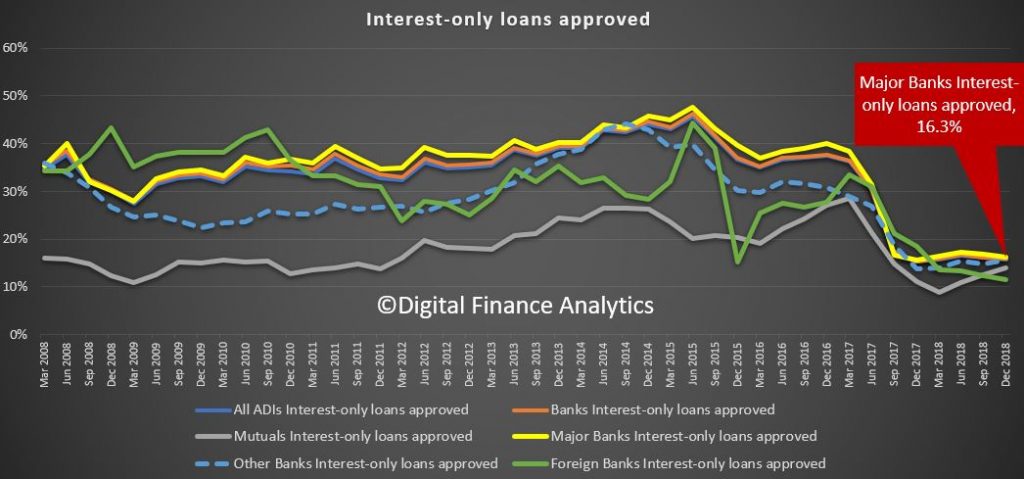

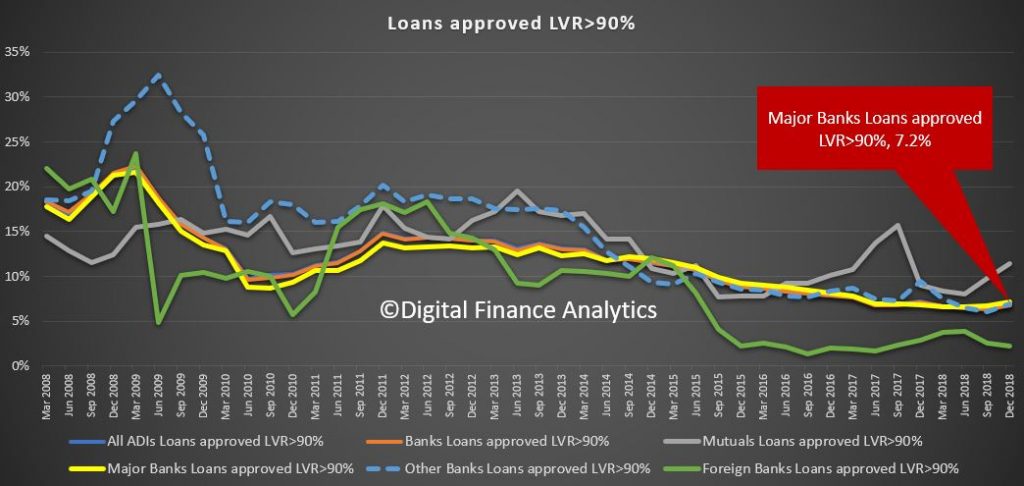

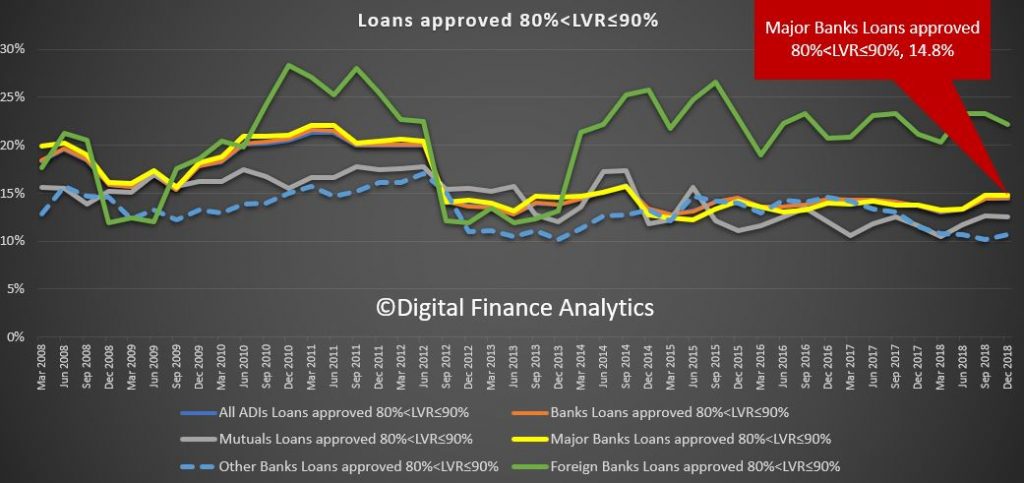

APRA released the latest quarterly property exposures data today to December 2018. The new loans flow data shows that owner occupied lending is still running at a pretty good clip, while new investor loans are sliding – and the share of all loans interest only, have dropped considerably.

The mapping between investment loans and interest only loans is probably more than coincidence, as we know the bulk of IO loans are for investors, but APRA does not [conveniently?] split them apart.

We can look at IO loan approvals by lender type. Major banks had 16.3% of their loans interest only, well down from their peak of 40%.

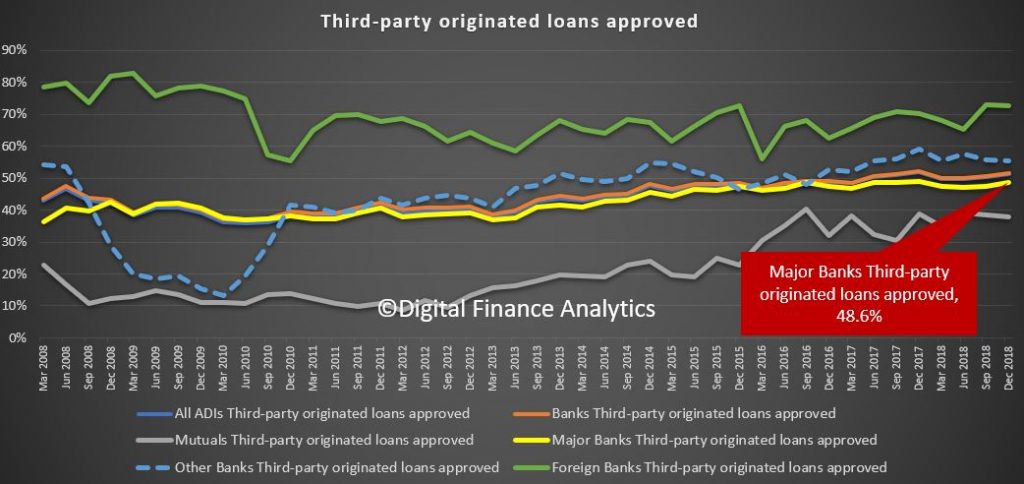

Mortgage brokers are still originating a significant share of new loans (even if volumes are lower). Foreign banks have the largest share via brokers, the majors are at 48.6%.

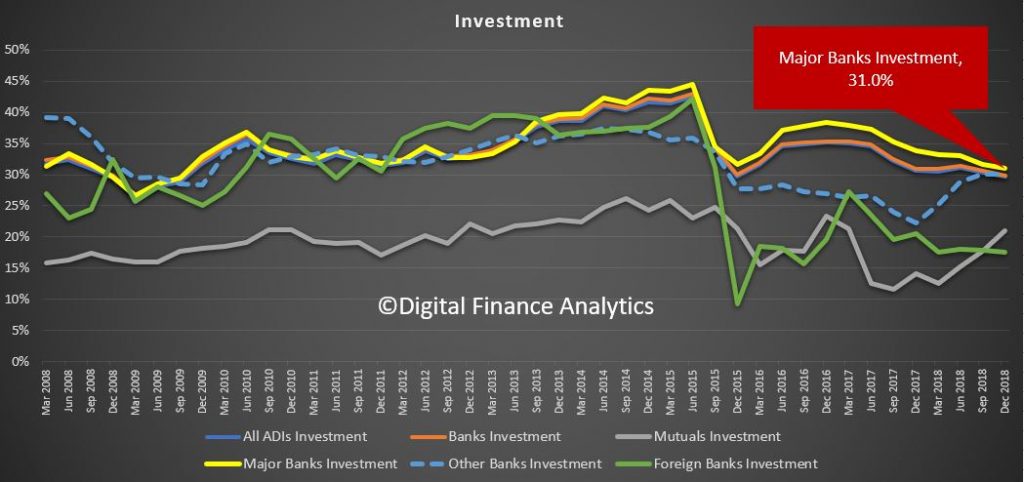

The proportion of investor loans being written has fallen, with major banks writing about 31% for investment purposes. Still a big number!

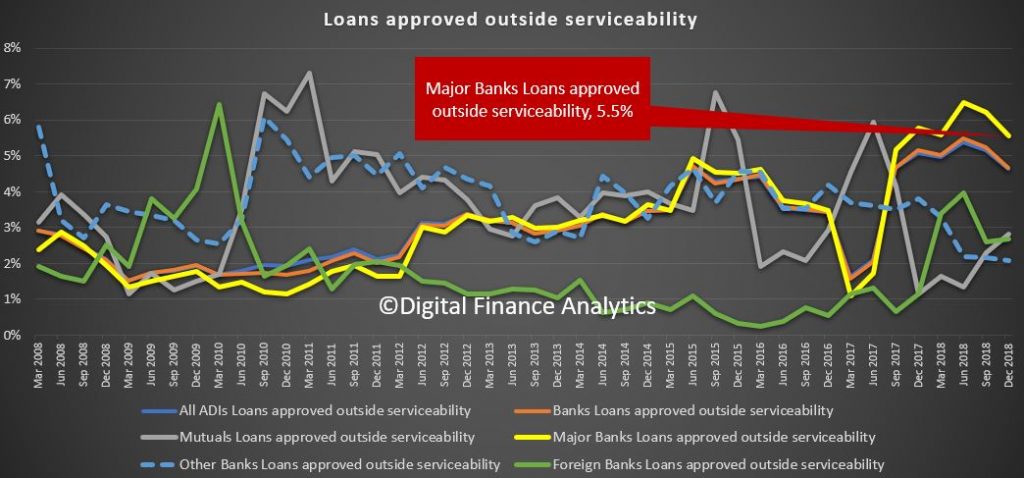

Loans outside serviceability are still high, reflecting tighter standards. Major banks are at 5.5% outside serviceability, down a little from past couple of quarters, but still a significant issue. Tighten the rules, then break the rules!

Finally, we can look at high LVR lending, important seeing as in some areas of Sydney prices are now down more then 20%. Over 90% LVR loans are still being written – 7.2% of all loans by major banks (so if prices fall another 10% ALL of these will be in negative equity. Also the trend is higher, especially for mutuals.

And the 80-90% LVRs are at 14.8% of all new loans from the major banks. Foreign banks are higher.

So a further fall of 20% would put more than 22% of new loans underwater.

These results suggest the banks are still lending excessively in the current environment. Expect more trouble ahead.

APRA’s Pat Brennan, Executive General Manager, Policy and Advice Division spoke at the 2019 KangaNews Debt Capital Markets Summit, Sydney

Bank capital (and liquidity) is the core of financial resilience, hence capital ratios are key indicators of financial strength. Bank boards, investors and regulators pay very close attention to these, the headline ratios and the underlying drivers, for reasons that are very obvious to this audience.

Reflecting the importance of financial strength,

APRA is in the process of updating the entire prudential framework for

capital in the banking industry. This began in 2014 with the Financial

System Inquiry recommendation for APRA to set requirements such that

Australian bank capital ratios are “unquestionably strong”, and

substantial progress has been made against this objective. More recently

at the end of 2017, the Basel Committee on Banking Supervision

finalised most of the post-global financial crisis (GFC) reforms,

finishing off in January of this year with the release of the final

market risk capital framework. In 2018 APRA began the public

consultation process as we sought to synthesise these two key drivers,

as well as introducing a variety of features that are specific to the

Australian industry.

Today I will provide an update on APRA’s

approach to risk-based capital requirements, then loss-absorbing

capacity (LAC), and then provide an update on what policy developments

APRA is working on behind the capital headlines.

Risk-based capital

A 10-year post-GFC capital build is near completion with

unquestionably strong capital ratios already attained by most banks.

Stress tests undertaken by both APRA and the IMF in recent years have

also found banks remaining above regulatory minimum requirements in very

severe stress scenarios.

While the overall amount of capital

that needs to be held by Australian banks has already been set in the

unquestionably strong benchmarks announced in July 2017, the allocation

of the precise amount of capital attributable to each source of risk is

being worked through as part of the revisions to the capital framework.

In February last year, APRA released an initial discussion paper that

proposed a number of revisions to the credit risk, operational risk and

market risk frameworks, including the adoption of a capital floor, which

will limit the capital benefit banks that use the internal

ratings-based approach (IRB) can obtain relative to those that use the

standardised approaches. These proposals focus primarily on improving

the risk sensitivity of the capital framework.

In August last

year, APRA also released a discussion paper on improving the

transparency, comparability and flexibility of the capital framework in

areas where APRA’s methodology is more conservative than minimum

international requirements. The proposals in that paper complement the

revisions to the capital framework by seeking to ensure that the capital

strength of Australian banks is appropriately understood by market

participants.

APRA expects to soon release its response to

revised capital requirements for credit risk and operational risk. In

relation to the former, the next phase of consultation will focus on the

treatment of residential mortgages for all banks, and other amendments

to the standardised approach to credit risk. Later this year, APRA will

release its full response to the revised credit risk requirements for

the IRB approach and its response to improving transparency,

comparability and flexibility. The outcome of this may lead to

significant presentational and calculation changes to a number of

prudential standards, although these would not affect the quantum of

capital required.

This stream of work is a multi-year process and

is likely to involve further rounds of consultation and quantitative

impact studies to enable APRA to assess the impact and better calibrate

the proposed changes. Given the need for extensive consultation, the

revised prudential standards are likely to be finalised in late 2020,

and are intended to commence in early 2022, consistent with the

international timetable agreed at the Basel Committee.

Loss-absorbing capacity and recapitalisation

Our work on building loss-absorbing and recapitalisation capacity

to deal with a bank failure or near-failure has been moving on a very

different timeline to risk-based capital, and deliberately so. The 2014

Financial System Inquiry recommended introducing LAC requirements in

Australia (which was consistent with APRA’s intent), adding that

international practices were still emerging at that time, and APRA

should follow these developments.

In November last year, APRA released the discussion paper Increasing the loss-absorbing capacity of authorised deposit-taking institutions to support orderly resolution.

In this paper we proposed increasing the Total Capital Requirement of

the major banks by between 4 and 5 per cent of risk-weighted assets,

with the expectation this would be mostly met through the increased

issuance of Tier 2 instruments. APRA intentionally proposed a simple

approach of using existing, well-understood capital instruments, given

they have been proven to work for their intended purpose – that is they

recapitalise a bank when needed.

Whilst APRA is still considering

submissions received and gathering additional information, and as such

we have not yet made any decisions on the proposals, I will offer a few

observations. The response we have received has been somewhat mixed. We

have been given clear feedback in a number of submissions that the

quantum of Tier 2 targeted, particularly at the higher end of the

calibration range consulted on, will test the likely bounds of investor

capacity. Submissions therefore challenged whether that calibration is

sustainable over time given debt markets will continue to experience

occasional periods of difficult issuance conditions. Some submissions

also questioned whether there are lower cost options to achieve the same

level of recapitalisation capacity, accepting these options are more

complex. On the other hand we have also received feedback from some

parties that using existing, proven capital instruments is a very good

idea.

In the debate about what is the best form of LAC, many

submissions concentrated on its form and understandably referred to the

variety of international approaches that have emerged. Submissions

offered informative perspectives on the relative merits of differing

forms of LAC from a capacity and efficiency perspective. Few, however,

reflected on the differing objectives and structures that have

influenced the divergence of international approaches.

Now is a good time to reflect that in many jurisdictions the chosen LAC approach was in direct response to their own, painful, lived experience through the GFC; with the reality of “Too Big to Fail” meaning authorities were faced with no choice but to bail-out troubled banks. In some jurisdictions this has led to a stated policy approach with the express, singular objective to never again require taxpayers to fund a bank bail-out. On the other hand, in other jurisdictions, including Australia, the objective is to protect the community from the potentially devastating broader impacts of financial crises. This is done firstly by reducing the probability of failure; and secondly by establishing sufficient recapitalisation capacity such that, should a failure or near-failure occur, the overall cost is minimised. This is consistent with the Financial System Inquiry recommendation that stated recapitalisation capacity should be “sufficient to facilitate the orderly resolution of Australian authorised deposit-taking institutions and minimise taxpayer support.”

These differing objectives guide

policy choices. Differing legislative and regulatory frameworks, and

institutional and corporate structures, around the globe also guide

choices and have played a role in influencing the divergence of

approaches adopted.

So for now we are thinking through options

and gathering additional information. APRA would still prefer a solution

that is on the side of simplicity, though at the same time we clearly

want to arrive at an approach that will work over time.

Whenever

APRA consults on a policy we undertake a genuine consultation process

and, for major policy such as this, it is an extensive process and all

submissions are carefully considered. In this case we have benefitted

from a high level of engagement with a broad range of stakeholders,

broader than is usually the case for APRA consultations, reflecting this

is new territory. At this point I cannot say when we will make public

our findings from the consultation, but given some years ago we

intentionally adopted the position of a follower of international

developments, we are now motivated to work through the considerations as

swiftly as possible.

Following finalisation of the LAC framework

APRA will build out other aspects of the prudential framework for

recovery and resolution.

And now, what is behind the headlines?

Without diminishing their importance, there is plenty that capital

ratios do not tell you. They don’t tell you how well a bank is run: if

its approach to risk management is sound, whether there is good

governance, and whether stakeholder interests are appropriately

balanced. Capital is no panacea as financial strength alone cannot

adequately mitigate against poor risk management or weak governance.

These are fundamental concerns for a prudential regulator. Capital

standards, including unquestionably strong benchmarks, are set on the

basis of at least sound risk management and governance being in place,

and so APRA has an ongoing supervisory and policy focus on non-financial

risks and drivers.

Cyber-risk, remuneration, accountability,

governance, risk management, recovery and resolution – these will

naturally become the greater part of APRA’s policy focus for the

forthcoming years. We are not lowering policy intensity on financial

risk and capital, but we are complementing and adding to this by

strengthening the prudential framework for non-financial risk.

Here is a quick overview of what to expect:

Late last year, APRA released the final version of Prudential Standard CPS 234 Information security,

which provides a clear set of requirements and expectations covering

information security, including cyber risk. We will very shortly be

supplementing this with a detailed practice guide.

In the next

quarter we will release for consultation an updated prudential standard

on remuneration. This follows the April 2018 Information Paper Remuneration practices at large financial institutions,

which reported on a thematic review APRA conducted where we found that

practices were not as robust as they should be. We have also learnt a

great deal from the CBA Prudential Inquiry and of course the Royal

Commission. The new standard will be stronger and be primarily focused

on outcomes. This will include that performance assessment must reflect

consideration of all relevant contributions to performance, including

risk management; banks will need to be transparent with APRA on how

remuneration decisions are made; and variable remuneration must be truly

variable in practice.

We will also have a significant focus on

governance and accountability. An extension of the Banking Executive

Accountability Regime (BEAR) to cover other prudentially regulated

industries has been a consideration since BEAR was first envisaged –

APRA has consistently supported this extension as the prudential

principles of BEAR apply equally across industries. Following the Royal

Commission, the BEAR extension will go even further, with a parallel

conduct accountability regime to be administered by ASIC. This is an

important development and APRA and ASIC will work closely to ensure the

parallel regimes work optimally. APRA will refresh its Governance and

Fit and Proper standards to not only more closely complement the

accountability regime, but to strengthen standards more generally; again

this will be in light of what we have learned through our supervisory

activity, through the CBA Prudential Inquiry and the findings of the

Royal Commission.

In the sphere of risk management, APRA will in the near future release for consultation a materially updated Prudential Standard APS 220 Credit Quality that

we will also rename to Credit Risk Management. Given credit is the most

material risk of the Australian banking sector we expect this will get

plenty of attention. On a slightly longer time frame, we are developing

an overarching operational risk standard and will consider changes to Prudential Standards CPS 220 Risk Management as our work of non-financial risk progresses.

In

conclusion, APRA has a comprehensive policy agenda both on bank capital

and non-financial risk. On the latter, this will draw on our

supervisory experience, the CBA prudential inquiry, the findings of the

Royal Commission and international developments. The Australian banking

system is well capitalised and APRA is supplementing that financial

strength by ensuring strong risk management and sound governance

practices are in place across the full spectrum of risks that banks

face.