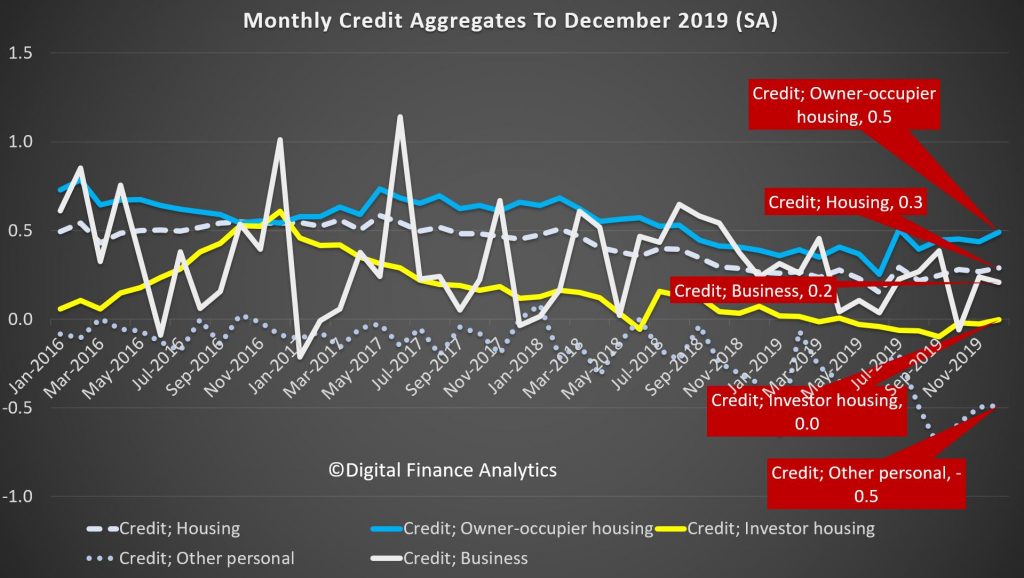

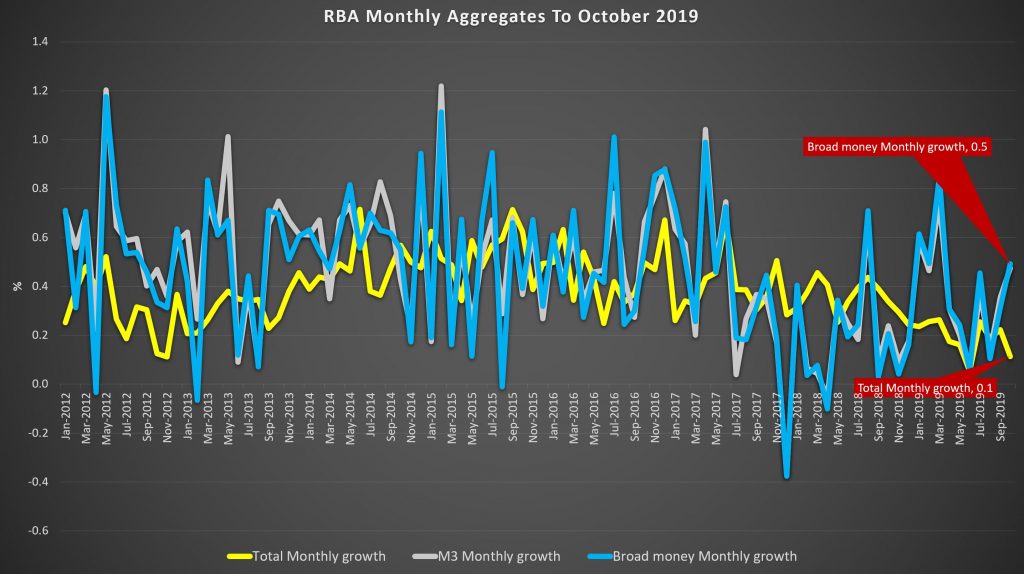

Looking at the RBA data first, over the past month housing credit stock (the net of new loans, repaid loans and existing loans) rose by 0.3%, driven by owner occupied housing up 0.5%, while investment loans slide just a little, but rounded to zero. Personal credit slid another 0.5% while business credit rose 0.2% compared with the previous month. These monthly series are always noisy, and they are also seasonally adjusted by the RBA, so there is plenty of latitude when interpreting them.

But overall, total credit grew by 0.2% over the month, while the broad measure of money rose just 0.1%.

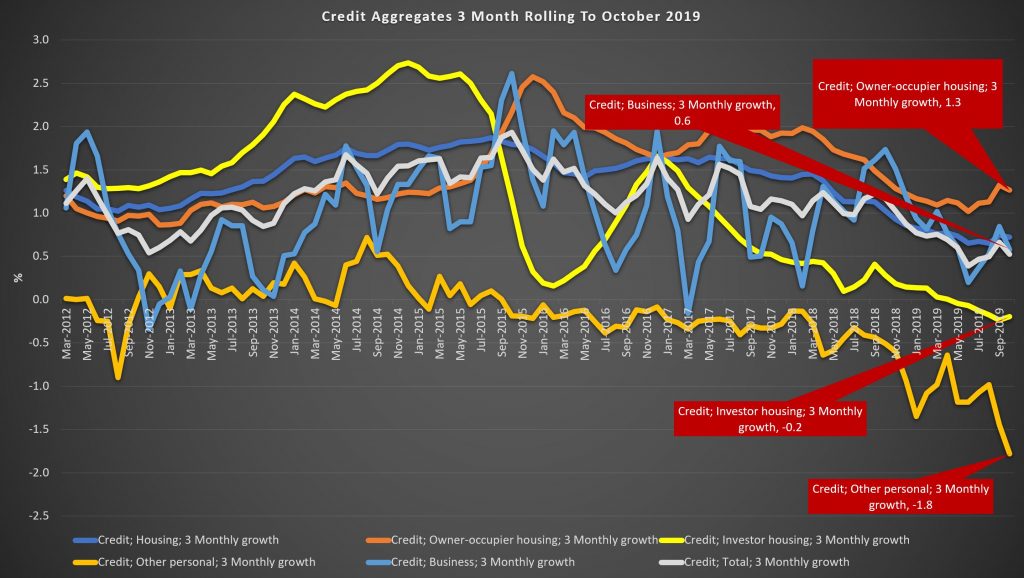

The three month derived series helps to spotlight the key movements over the past few years. Credit growth for owner occupation rose 1.4%, and it has been rising a little since the May election, and the loosening of lending standards by APRA, and lower rates later. Its low point was a quarterly rise of 1% a few months ago. Investment lending continues to shrink, at 0.1%, but the rate of decline has eased from September, again thanks to loser lending standards. However this also reflects a net loan repayment scheme that many households, in the current tricky environment are on. Personal lending is still shrinking, falling at 1.6%, though the rate of slowing is reversing from a low of minus 1.8%. Business credit is o.4%, but has been falling since October where it stood at 1.8%, reflecting a serious downturn in business confidence and demand for credit. For businesses, the economic backdrop has been a challenging one. The global economy is sluggish and household spending is soft. In this environment business investment in the real economy has lost momentum across the non-mining sectors – weighing on credit demand. Rolling total credit for 3 months is 0.6%, up from a low of 0.5% a couple of months back.

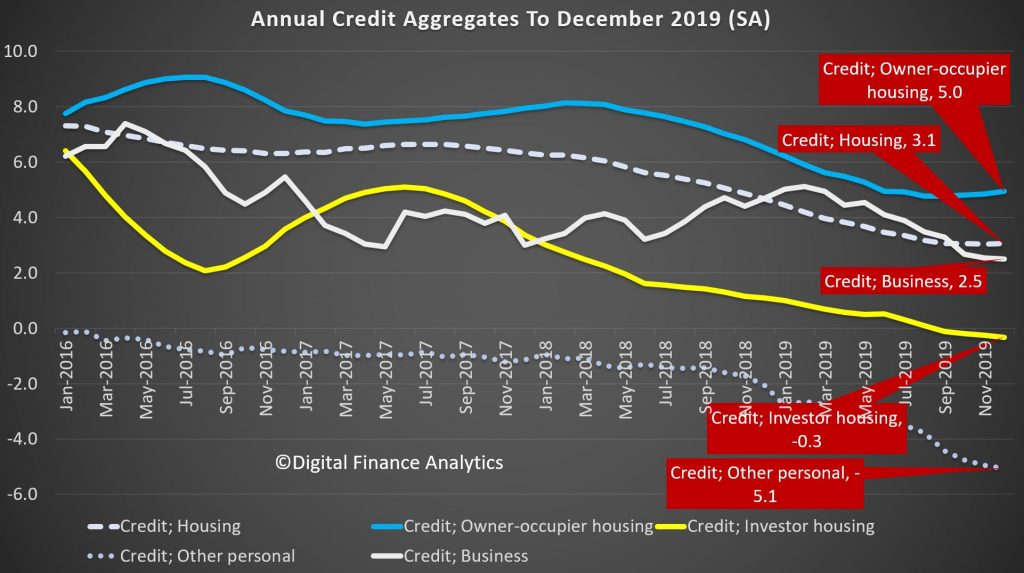

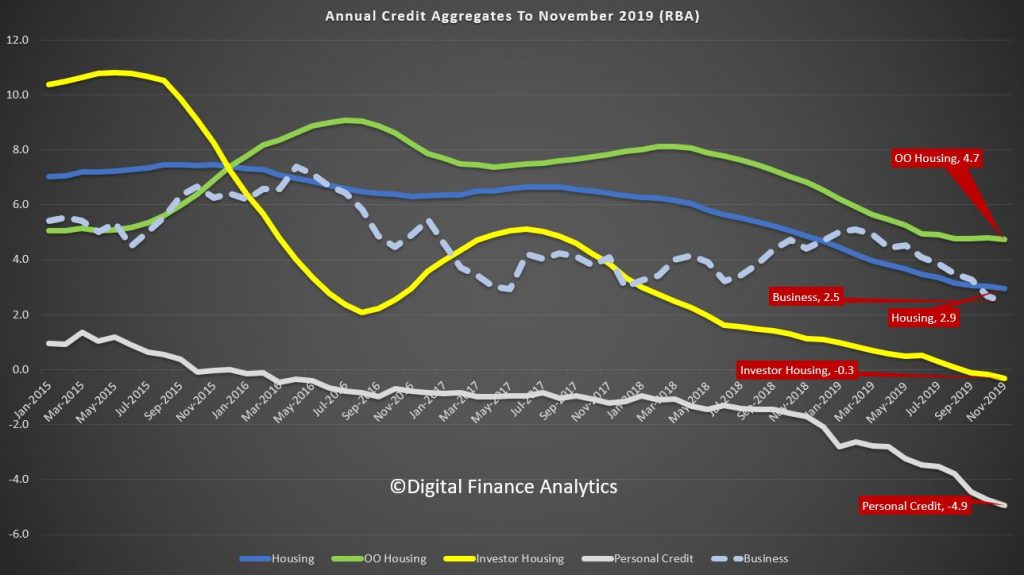

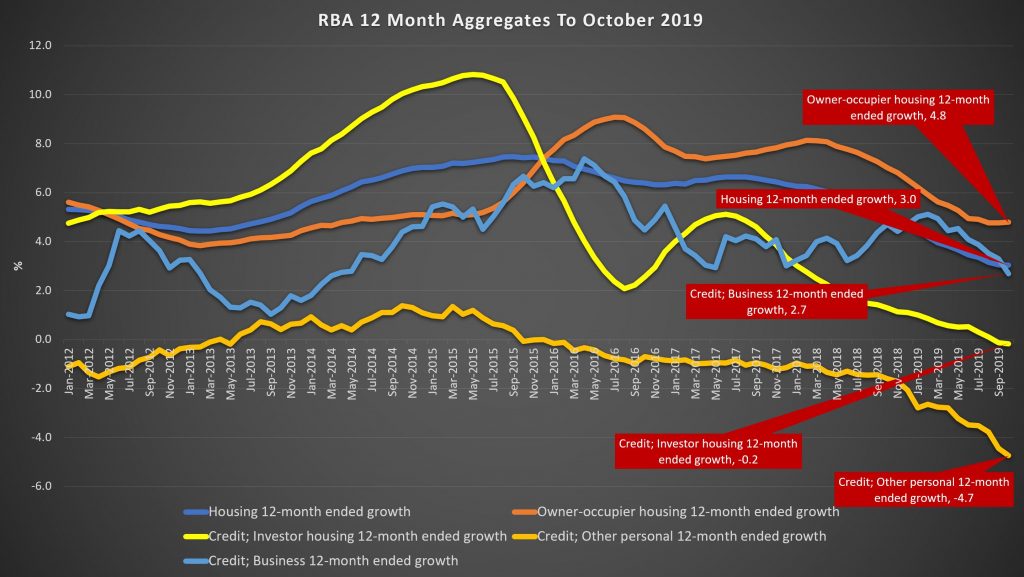

Turning to the annualised data series, housing credit is at 3.1% up from 3.03% last month. Annual owner occupied housing is up 5% from a low of 4.7% in August, while investor loans are down 0.3%, which is the largest fall we have ever seen. Personal credit is 5.1% lower, and that is another record low, while business credit grew by 2.5% on an annual basis, which is the lowest its been for years.

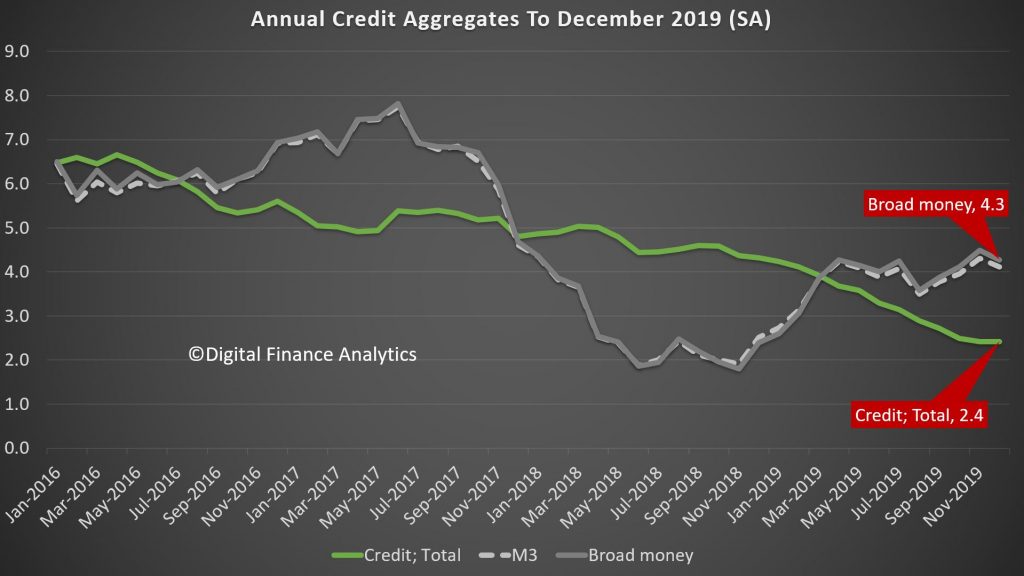

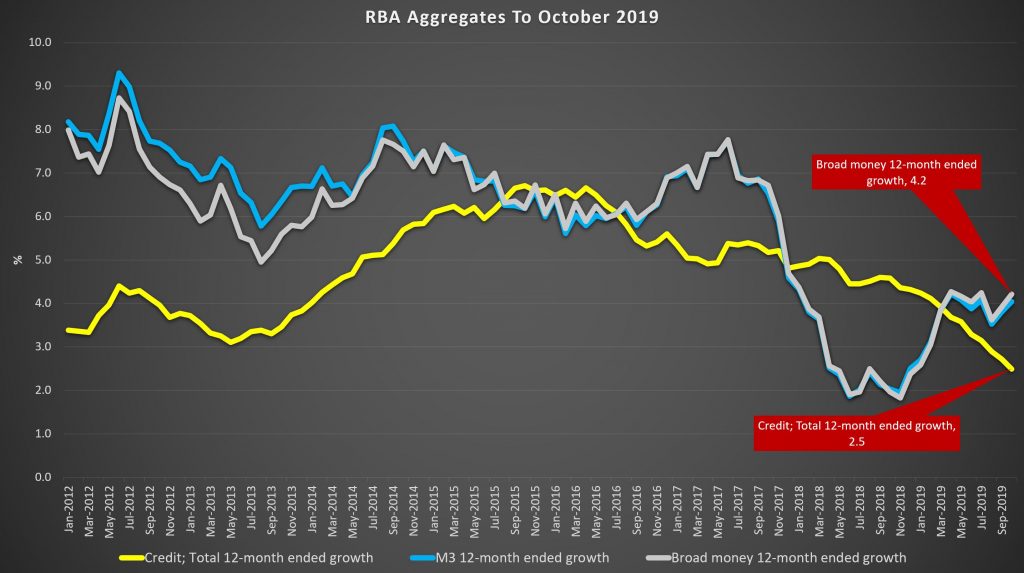

As a result, total credit grew 2.4%, which is the lowest level of growth since 2010, following the global financial crisis. Credit growth has progressively eased after peaking at 6.7% during the 2015/16 financial year. Key to the slowdown was the housing downturn as the cycle matured and lending conditions tightened. On the other hand, broad money is growing at 4.3%, and is significantly higher than last year, which we attribute to the positive terms of trade (thanks to iron ore prices and commodity volumes and RBA open market operations).

So while sentiment bounced after the May Federal election, which removed uncertainty around tax policy for the sector, as the RBA has lowered rates since June by a total of 75bps, with further cuts likely and APRA easing mortgage serviceability assessments; growth is anemaic, and of course sentiment is now in the gutter, thanks to the bushfires, coronavirus, and lack of income growth. While many analysts are predicting a bounce in credit in 2020, and a sentiment turnaround, pressure on global commodity prices and weak international tourism, as well as the drought are likely to take their toll.

We are also seeing more applications for mortgages being received, but also higher rejection rates, so we will see if this will really lead to stronger credit. And given such weak credit, we still question the veracity of the CoreLogic price series, which seems to exist in a different world. Our data supports much weaker average home price growth.

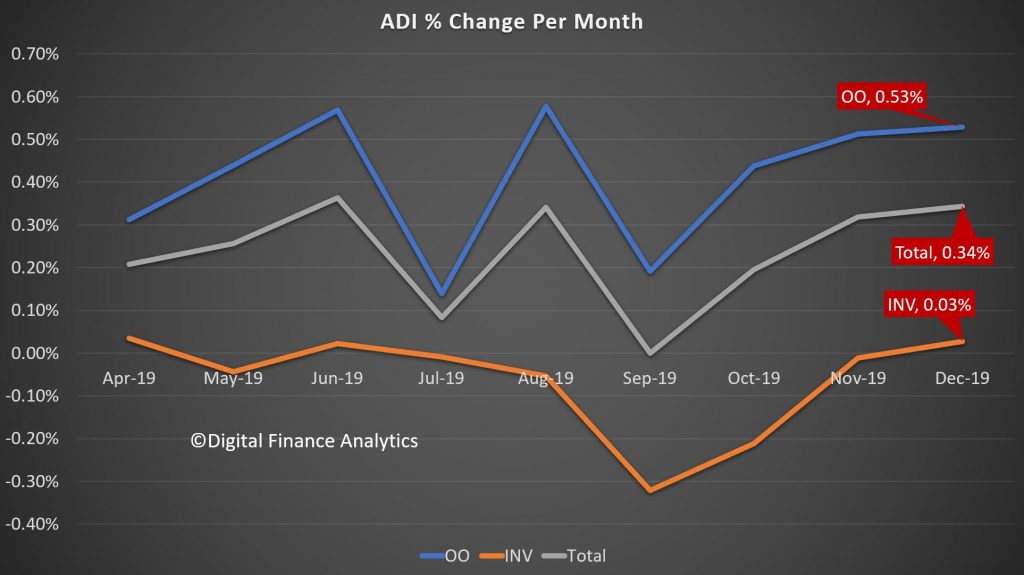

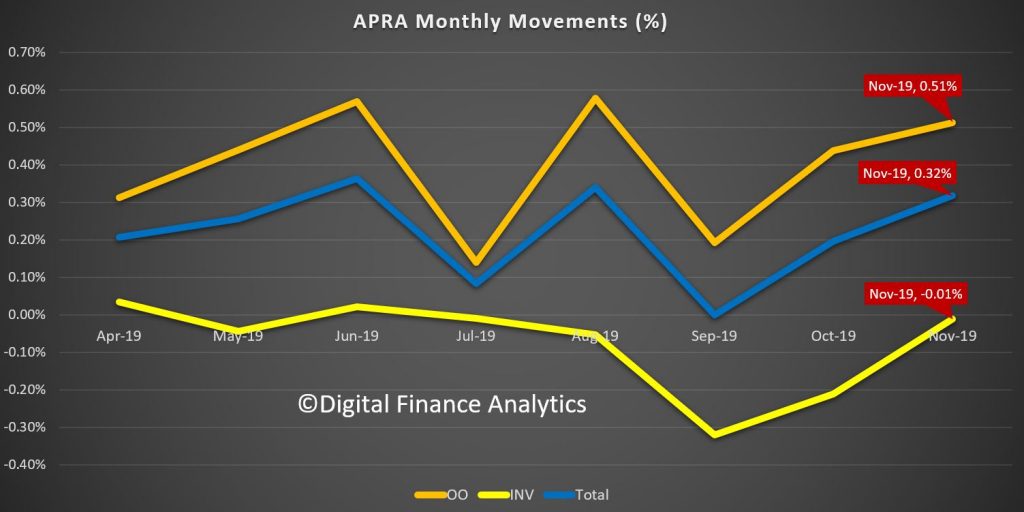

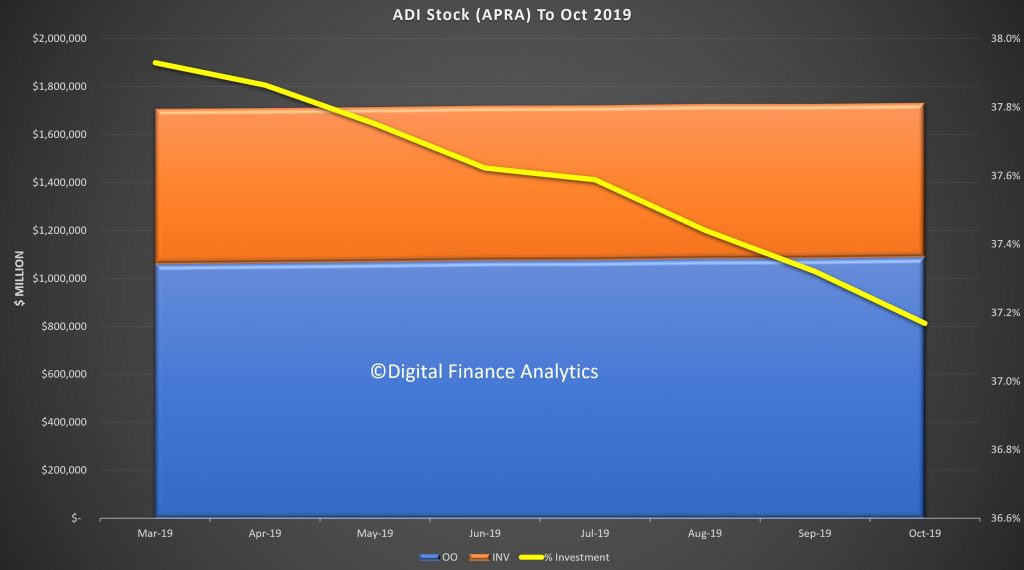

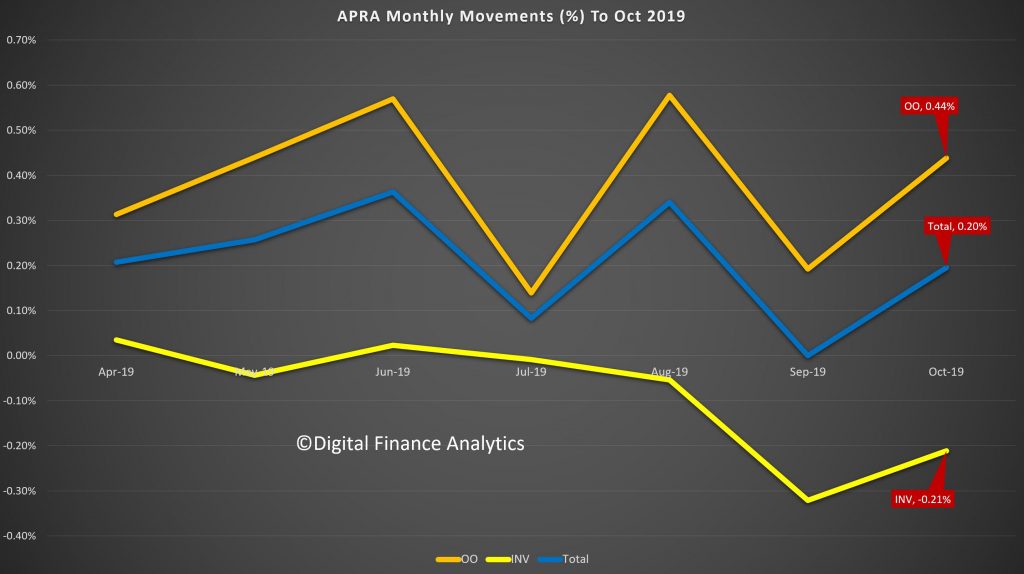

Turning to the APRA Bank series, the total value of mortgages lent (in original terms) grew by 0.34%, which is stronger than the market (0.3%), suggesting that the banks may be clawing back some business from the non-bank lenders, who have been quite active over the past couple of years. Within that owner occupied loans rose by 0.53% in the month, while investment loans grew 0.3%. The rate of growth remains slow.

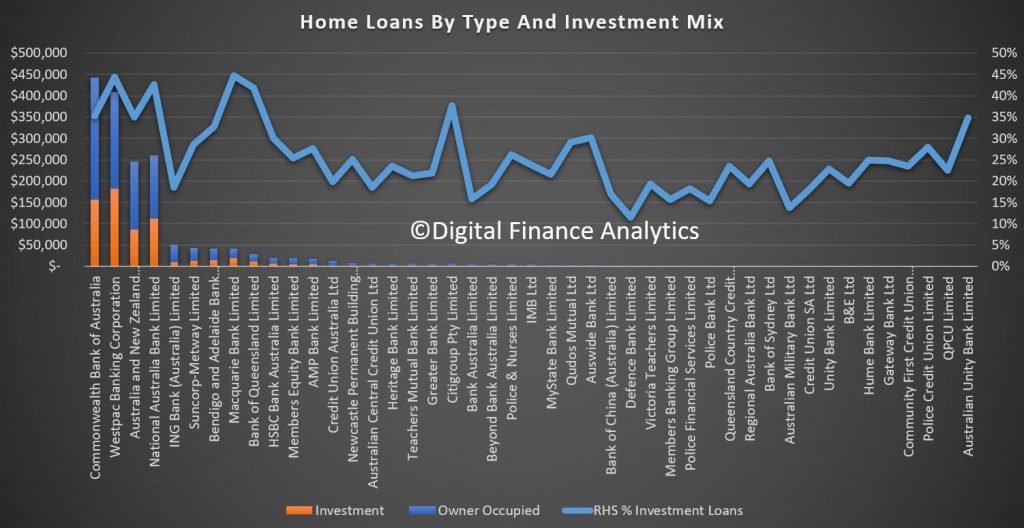

The total stock of loans did rise, up around $5 billion dollars to $1.09 trillion for owner occupied loans, and up only slightly to $644 billion, giving total exposures of $1.74 trillion, a record. The mix of investment loans fell to a low of 36.9%.

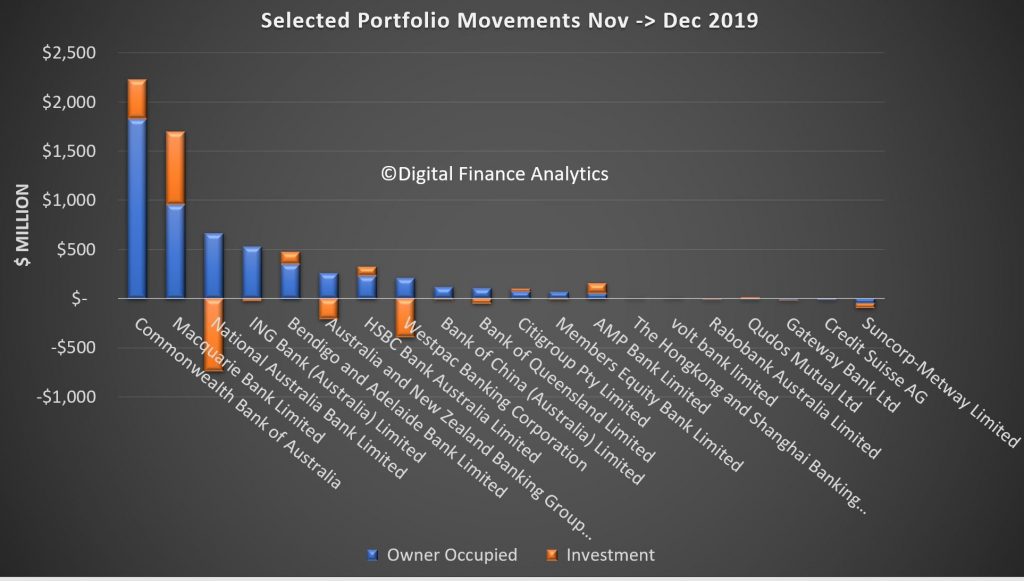

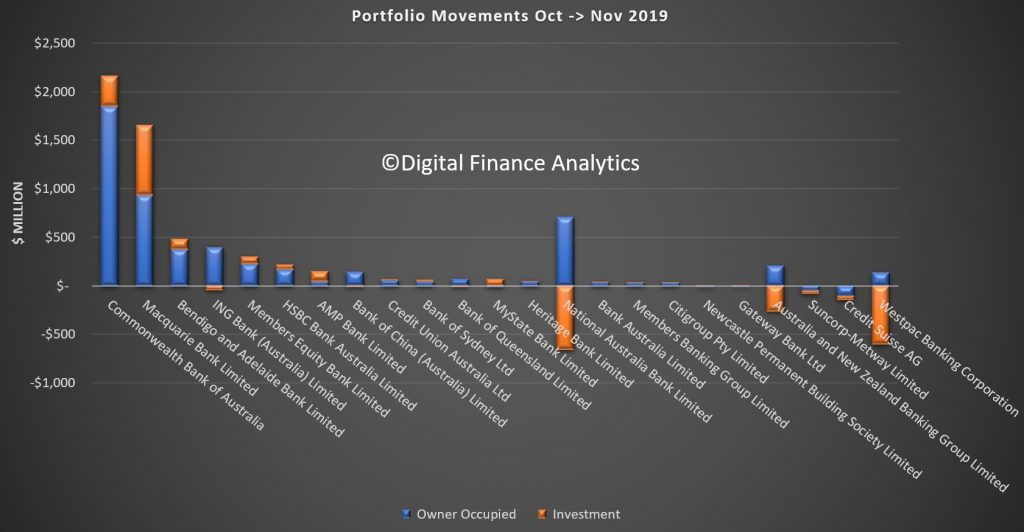

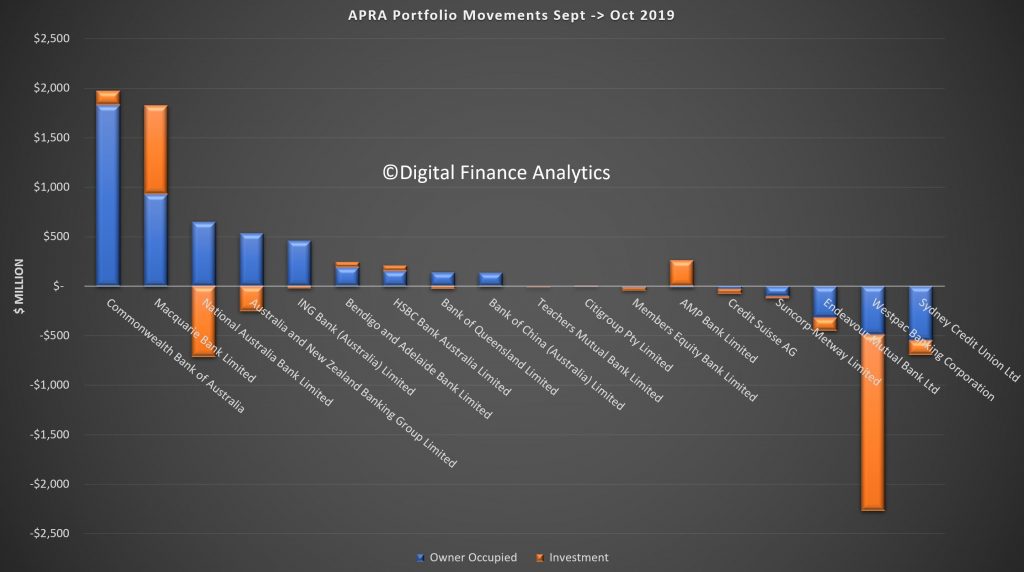

Finally we can examine the portfolio movements by individual lender, which reveals that, according to the data submitted by lenders (which may include some adjustments) CBA grew their portfolio the strongest, up more than $2.2 billion, including both owner occupied and investor loans, followed by Macquarie which continues to drive investor lending very hard, while NAB, Westpac and ANZ grew their owner occupied loans, while dropping their investor lending balances. Bendigo Bank, AMP and HSBC were also active in growing their investor loans. Neo-lender Volt Bank made an appearance in our selected list, while Suncorp dropped the value of both their owner occupied and investor loans. This highlights that lenders are steering quite different paths in their underwriting and marketing strategies. Time will tell whether the new loans being written are more risky.

And in closing, its interesting to note APRA’s release today saying that

The Australian Prudential Regulation Authority (APRA) will expand its quarterly property data publication to include new and more detailed statistics on residential mortgage lending.

In a letter to authorised deposit-taking institutions (ADIs) today, APRA confirmed the next edition of its Quarterly Authorised Deposit-taking Institution Property Exposures (QPEX) publication would include additional aggregate data on residential property exposures and new housing loan approvals.

The decision is part of APRA’s to move towards greater transparency, and will enable more in-depth market analysis by industry analysts, media and other interested parties.

The updated QPEX publication will also feature:

• reporting of additional sector-level statistics for the ‘Mutual ADI’ category; and

• clarified definitions for reported items, specifically for unreported loan-to-value ratios.

APRA Executive Director of Cross-Industry Insights and Data Division, Sean Carmody said: “APRA’s updated Corporate Plan commits us to increasing transparency of both our own operations and the industries we regulate. One of the key ways we can do that is by releasing more of the data we collect.

“With the ADI sector heavily reliant on commercial and residential property lending, enhancing QPEX will translate to greater transparency and sharper insights into one of the most crucial contributors to the economy.”

Consultation is continuing separately on a proposal for quarterly publication data sources to become non-confidential. This would mean that more of the underlying data may be disclosed to the public on a dis-aggregated basis. While this consultation remains open, APRA will continue to publish industry and peer group aggregate data, and mask data in QPEX where an individual entity’s confidential information could be revealed.

The next QPEX will be published on 10 March 2020 for the December 2019 reference period.

We believe that the dis-aggregated data should indeed be released – because sunlight remains the best disinfectant to quote Supreme Court Justice Louis Brandeis. Compared with the disclosures in other markets, Australia is so behind the times, on the pretext of confidentially. So we endorse the need for more granular data to help separate the lending sheep from the lending goats.

APRA has released their monthly banking stats to the end of November 2019. They are of course in the process of a major revision of these statistics, but we are now beginning to get some trend data down to the individual ADI level. The data is based on gross balances outstanding by owner occupied and investment loans, but it does not show where new loans were added, or loans repaid. So little flow data can be imputed.

Total owner occupied loans rose 0.51% or $5.58 billion dollars in November to $1.09 trillion dollars, while investment loans fell 0.01% or $75 million dollars to $643 billion dollars. The share of loans for investment purposes fell again to 37%.

The trend movements show some improvement relative to earlier months. Total loans rose 0.32% in the month, which would given an annualised 3.8%.

The RBA data released before Christmas showed that total loan growth over the past year for mortgages fell to the lowest ever (2.9%), which suggests that non-banks may be lending less now. But we cannot be sure of this.

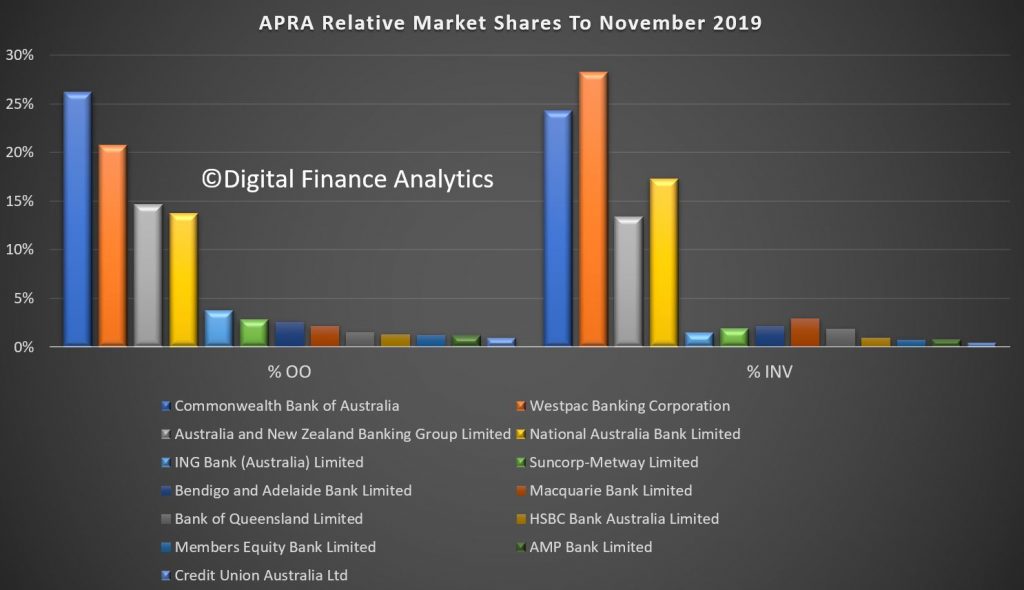

We can also look at individual lenders. The relative shares of the largest players hardly changed, with CBA the largest owner occupied lender, while Westpac has the largest share of investment loans.

However, the relative movements this month underscored divergent results from lenders. CBA and Macquarie both saw significant growth in loans in the month, with Macquarie writing net more investment loans than any other lender at $718 million dollars. Bendigo Bank and AMP Bank are also chasing investment lending. On the other hand, ING dropped their investment loan balances, alongside the other big lenders, with NAB down $661 million, ANZ down $263 million and Westpac down $602 million. Suncorp and Credit Suisse both dropped their owner occupied and investment loan portfolios.

Finally, the relative proportion of loans for investment purposes reveals that Macquarie has 44.8% of its loans for this purpose, Westpac at 44.5%, NAB at 42.6% and Citi at 37.7%. Bearing in mind investment loans are intrinsically more risky, this is worth watching.

So, some small uplift in net volume of loans, but not equally spread across the sector, which suggests different players have different underwriting settings.

And the growth in lending suggests the household debt ratio is set to continue to rise, despite its already stratospheric level.

The Australian Prudential Regulation Authority (APRA) has published a document outlining its governance arrangements, along with accountability statements for its senior executives.

The paper, titled Governance and Senior Executive Accountabilities, describes APRA’s internal governance and accountability arrangements and is supported by individual accountability statements for senior executive roles and an accountability map. The accountability statements cover all four APRA Members, as well as APRA’s six Executive Directors, APRA’s Chief Risk Officer and Chief Internal Auditor.

Today’s release responds to recommendation 6.12 of the Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry: that “each of APRA and ASIC should internally formulate and apply to its own management accountability principles of the kind established by the Banking Executive Accountability Regime (BEAR).”

APRA accepted the recommendation and committed to meeting it by 31 December 2019.

The Australian Prudential Regulation Authority (APRA) has today formally commenced an investigation into possible breaches of the Banking Act 1959 by Westpac Banking Corporation (Westpac).

APRA will focus on the conduct that led to the matters alleged last month by AUSTRAC, as well as the bank’s actions to rectify and remediate the issues after they were identified. The investigation will examine whether Westpac, its directors and/or its senior managers breached the Banking Act – including the Banking Executive Accountability Regime (BEAR) – or contravened APRA’s prudential standards.

Given the magnitude and nature of the issues alleged by AUSTRAC, APRA is aiming to ensure that fundamental deficiencies in Westpac’s risk management framework are identified and addressed and that Westpac and those responsible are held accountable as appropriate.

In addition, APRA will:

impose an immediate increase in Westpac’s capital requirements of $500 million, to reflect the heightened operational risk profile of the bank. This brings the total operational risk capital add-ons that Westpac is required to hold to $1 billion, following the increase announced by APRA in July 2019; and

initiate an extensive review program focused on Westpac’s risk governance. The review program will include risk management, accountability, remuneration and culture. An element of the review will be an examination of the steps Westpac has been taking to strengthen risk governance in recent years, including through its self-assessment.

APRA Deputy Chair Mr John Lonsdale said: “AUSTRAC’s statement of

claim in relation to Westpac contains serious allegations that question the

prudential standing of Australia’s second largest bank.

“While Westpac is financially sound, there are potentially substantial gaps in

risk governance that need to be closed.

“Given the nature of the matters raised by AUSTRAC, the number of alleged

breaches and the period of time over which they occurred, this will necessarily

be an extensive and potentially lengthy investigation.”

The investigation affords APRA the opportunity to exercise legal powers that

have been expanded and strengthened since 2017’s CBA Prudential Inquiry,

including enhanced investigative powers and the implementation of the BEAR in

2018.

APRA will conduct its investigation simultaneously with an investigation by the

Australian Securities and Investments Commission (ASIC), as well as AUSTRAC’s

legal proceedings, with each agency cooperating where appropriate.

The scope of APRA’s investigation is below.

Attachment – Scope of

APRA’s investigation into Westpac

The prudential matters that are the subject of APRA’s investigation are:

Whether Westpac, its directors, and/or its senior managers have contravened the Banking Act 1959 and the prudential standards by engaging in, and in the way they responded to, the conduct set out in and otherwise related to the AUSTRAC proceedings.

In considering possible contraventions of the Act and the prudential standards, the investigation will examine whether:

(a) Westpac’s governance, control and risk management framework was adequate; and appropriately implemented;

(b) Westpac’s accountability and remuneration arrangements were adequate, and appropriately implemented to effectively manage non-financial risks;

(c) there has been a failure to comply with accountability obligations under the Banking Executive Accountability Regime;

(d) there has been a failure to comply with the requirements of the prudential standards including Prudential Standard CPS 510: Governance, Prudential Standard CPS 520: Fit and Proper, and Prudential Standard CPS 220: Risk Management; and

(e) there was a failure to promptly notify APRA of any significant breaches and/or a breach of accountability obligations.

APRA remains in a low risk bubble, according to their paper today, which keeps the counter-cyclical buffer at 0. However they flag that may change ahead. I have to say this seems perverse, given the high debt levels and low economic performance and increased risks. Plain weird, and a million miles off the Reserve Bank NZ’s approach.

The Australian Prudential Regulation Authority (APRA) has decided to keep the countercyclical capital buffer (CCyB) for authorised deposit-taking institutions (ADIs) on hold at zero per cent, but has flagged the likelihood of a non-zero default level in the future.

The CCyB is an additional amount of capital that APRA can require ADIs to hold at certain points in the economic cycle to bolster the resilience of the banking sector during periods of heightened systemic risk. It has been set at zero per cent of risk-weighted assets since it was introduced in 2016.

In its annual information paper on the CCyB, APRA today confirmed it considers that a zero per cent CCyB remains appropriate at this point in time based on an assessment of the systemic risk environment for ADIs.

Among the factors APRA considered in making its decision were:

low credit growth;

minimal change in the risk profile of new housing lending;

movements in residential property prices, particularly recent growth; and

increased entity costs due to operational risk events and misconduct.

After carefully examining

these dynamics, APRA concluded that the current policy setting remains

appropriate.

In conjunction with the other agencies on the Council of Financial Regulators,

APRA will continue to closely monitor financial and economic conditions. APRA

reviews the buffer quarterly, and may adjust it if future circumstances warrant

this.

However, the information paper notes that APRA is also giving consideration to

introducing a non-zero default level for the CCyB as part of its broader

reforms to the ADI capital framework.

APRA Chair Wayne Byres said: “Given current conditions, and the financial strength

built up within the banking sector, a zero counter-cyclical buffer remains

appropriate.

“However, setting the countercyclical capital buffer’s default position at a

non-zero level as part of the ‘unquestionably strong’ framework would not only

preserve the resilience of the banking sector, but also provide more

flexibility to adjust the buffer in response to material changes in financial

stability risks. This is something APRA will consult on as part of the next

stage of the capital reforms currently underway.

“Importantly, this would be considered within the capital targets previously

announced – it does not reflect any intention to further raise minimum capital

requirements.”

APRA expects to commence the next stage of its ADI capital consultation in the

first half of next year. APRA’s revised capital framework is currently

scheduled to come into effect from 1 January 2022.

From the excellent James Mitchell, at The Adviser. If the prudential regulator was hoping to provide clarity on MySuper products it has failed miserably.

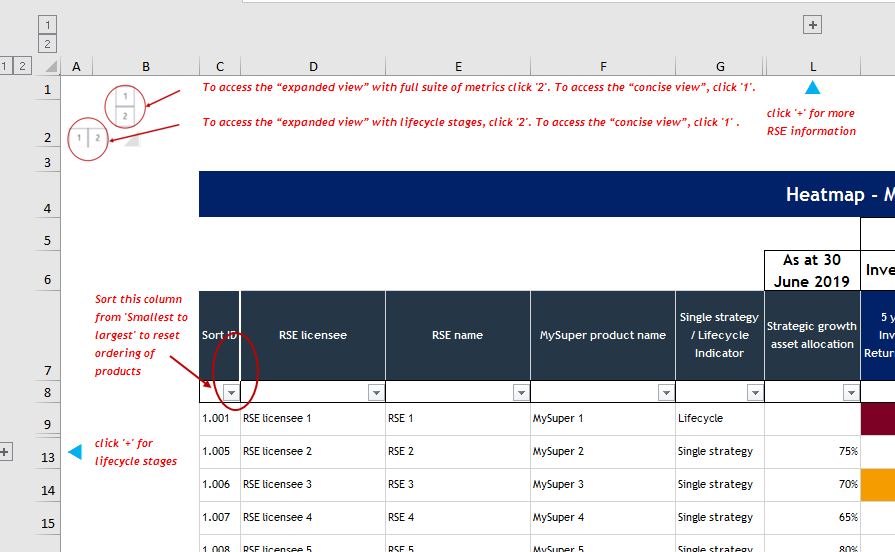

Call me ignorant, but when APRA announced the launch of its MySuper heatmap, I didn’t envision downloading an Excel spreadsheet and navigating multiple tabs in order to decipher what the hell I was looking at. If this monstrosity is intended to be fit for public consumption then the average Australian better have a financial adviser by their side, if for no other reason than to decode the thing.

Fortunately, the team who put the spreadsheet together included a “user guide” on tab 4 (see below). Crikey!

There

is also a colour legend and a glossary of definitions for terms such as

“strategic asset allocation” and “net investment return”.

My

fear is that the average Australian super member looking to compare

funds will struggle to comprehend what APRA’s heatmap actually means.

Particularly when you consider what the financial literacy of an average

Australian actually looks like.

Back

in August, Compare the Market and Deloitte Access Economics released the

second edition of The Financial Consciousness Index, which measures the

extent to which Aussies are conscious or aware of their ability to

affect and change their own financial outcomes, encompassing their

willingness to act, and the extent to which they are able to participate

in financial matters.

Australians

scored 48 per cent on average on the index, which means they are just

into the “conscious” band and out of the “it’s a blur” band.

Meanwhile,

ASIC’s 2018 Financial Capability initiative noted that two in three

Australians don’t understand the investment concept of diversification

and only 35 per cent know what their super balance is.

With

this in mind, it’s difficult to fathom how APRA’s overly complex Excel

spreadsheet is going to translate, let alone be used as a guide, to

everyday Australians.

FSC CEO Sally Loane warned against the misuse of the thing and said it should not be used to rank superannuation products.

“It

is really important to understand that the heatmaps are a point-in-time

analysis, which is a useful tool for APRA in its supervision

activities, but it doesn’t tell the whole story when it comes to

members’ retirement outcomes,” Ms Loane said.

“Particularly

for life cycle products, which adjust investment strategies over a

person’s lifetime, the headline numbers in the heatmap don’t reflect the

actual experience of a member in that fund, and could be misleading if

viewed in isolation.”

The FSC noted

that the heatmap may tell you that other funds have had higher returns

over five years, but if you’re close to retirement you might be far more

concerned with how your fund is managing the risks of a market downturn

to safeguard your retirement savings.

Some

of the heatmap’s other failings are that it doesn’t tell you how your

super has performed over your lifetime, it can’t tell you whether your

fund invests in accordance with your ethical and philosophical beliefs,

and it doesn’t tell you what additional services they offer to help you

manage your savings.

“If you have

concerns about whether your super fund is right for you, talk to your

fund or speak to a financial adviser,” Ms Loane said.

Ms

Loane said that while the FSC hoped APRA would continue to refine its

MySuper heatmap methodology, the proposal to extend the exercise to

choice products was highly problematic.

“The

broad variety of choice products in the market, the complexity and

bespoke nature of platforms and wraps where individuals choose their

investment strategies, and the lack of direct comparable data, [make] it

extremely difficult to translate heatmapping beyond MySuper and we urge

APRA to not only be cautious in proceeding with this exercise but to

engage deeply with industry,” she said.

The Australian Prudential Regulation Authority (APRA) has proposed substantially increasing the volume and breadth of data it makes publicly available on authorised deposit-taking institutions (ADIs), including banks, credit unions and building societies.

The move towards greater transparency and scrutiny of the banking sector is aimed at increasing accountability, supporting competition and lifting overall industry standards.

In a letter to industry today, APRA outlined plans to determine that all data collected for its quarterly ADI publications should be considered non-confidential, allowing it to be published. APRA currently publishes less than 1 per cent of the ADI data it collects due to legal restrictions contained within the Australian Prudential Regulation Authority Act 1998 (APRA Act). This change would allow APRA to significantly increase this figure.

From 2020, APRA proposes publishing:

entity-level ADI data related to currently published industry-level quarterly data;

remaining historical data in these forms that individual ADIs are required to provide APRA, which will be published with a three-year lag; and

commentary received by APRA from individual ADIs explaining material revisions to, or large movements in, their data.

The proposal supports

APRA’s strategic policy of increasing the transparency of data it collects, and

aligns with Government open data policies.

APRA’s Executive Director for Cross-Industry Insights and Data, Sean Carmody,

said: “APRA is committed to increasing transparency about the institutions and

industries we regulate.

“Under these proposed changes, APRA intends to publish – for the first time – a

range of information about individual ADIs, including their financial

performance and property exposures.

“As with the recent inclusion of data from credit unions and building societies

in our Monthly ADI Statistics publication, these changes are aimed at further

strengthening the ADI sector by enhancing accountability and encouraging

competition. They will also assist other regulatory agencies that rely on APRA

data, as well as analysts, policymakers and others who use our publications.”

Under the APRA Act, APRA must consult ADIs and their representatives, including

industry associations, before determining any new data to be non-confidential.

A 12 week consultation is now underway and concludes on 28 February 2020. APRA

is encouraging all interested parties to make submissions on issues including

what, if any, data should remain confidential.

APRA intends to consult on forms not included in this consultation at a later

date.

The end of the working month heralds another set of credit stats from both the RBA and APRA. The RBA reports via their Credit Aggregates, which is all credit stock in the system, while APRA reports on the banks (ADI’s) and also provides some individual lender loan stock data. And which ever way you look at it, credit growth is still anaemic, as the “great deleveraging” continues. And given the weak credit impulse, home prices may also be growing more slowly than many are claiming, though that is another story, for another day.

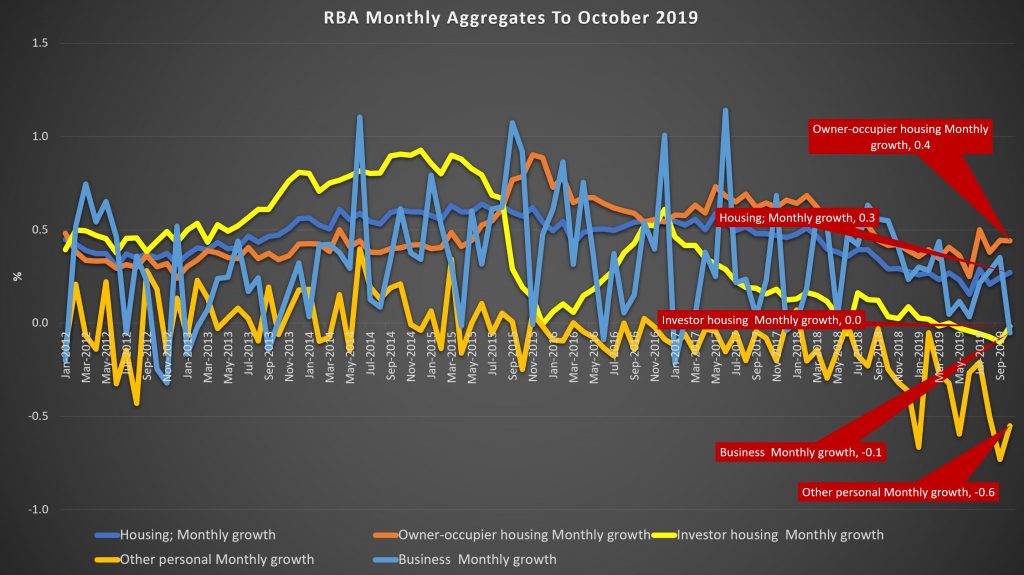

The RBA said that housing credit growth overall was 0.3% higher in October, compared with 0.2% in September. This translates to an annual rate of 3% to October (3.1% last month), compared with 5% just a year back.

Monthly owner occupied lending rose 0.4% while investor housing lending was flat. Personal credit fell another 0.6% in the month, and business lending was down 0.1%. As a result total credit rose just 0.1%, down from 0.2% last month. Broad money was higher though.

Over a rolling 3 months view, owner occupied credit grew 1.3% while investor credit was down 0.2%, other personal credit was down 1.8% and business credit was up 0.6%.

Looking across the rolling 12 month view, housing credit growth dropped from 3.1% to 3%, with owner occupied lending at 4.8% and investor lending down 0.2%. Business credit was 2.7% higher, and personal credit dropped by 4.7%.

As a result, total credit was just 2.5%, as lower as its been for many years, although broad money rose 4.2%.

APRA’s new data series continues to contain some surprises. Total lending stock by the banks rose to $1.73 trillion, up 0.2% in the month.

The share of investor loans continues to fall, to around 37.2%, and this is explained by investor loan stock falling by 0.21% in the month, compared with a rise of 0.44% for owner occupied loans. The series still looks a bit weird, so we wonder if there are still reporting issues.

The individual banks stocks of loans varied, with CBA extending their book (consistent with our industry research, as one of the easier lenders at the moment), along with Macquarie – both of which grew both investor and owner occupied pools. NAB and ANZ dropped investor loans, but extended owner occupied loans. But Suncorp and Westpac dropped BOTH investor and owner occupied loan balances (assuming the reporting is correct – lets see if we get a reversal next month).

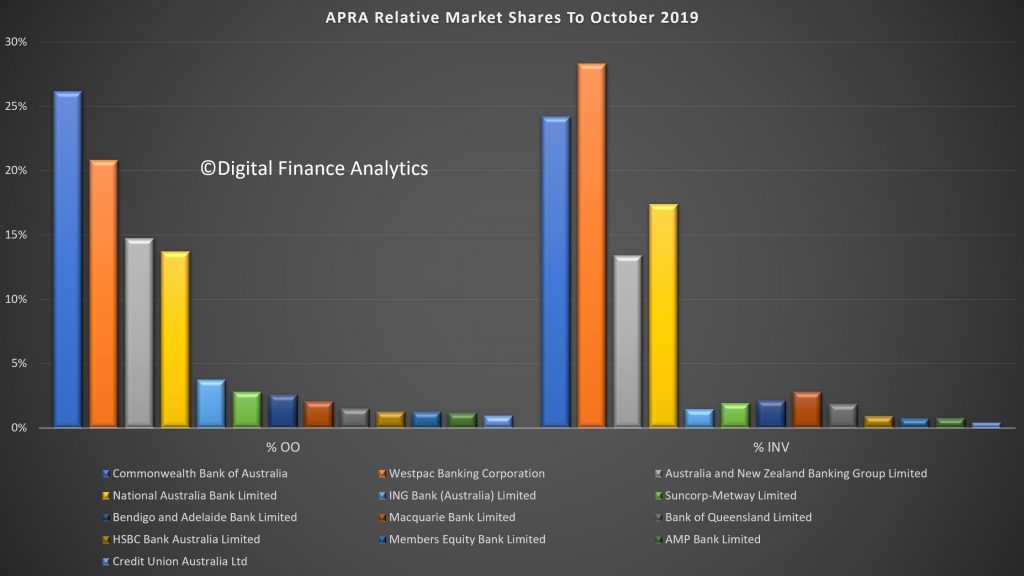

Finally, market shares hardly changed, with CBA the largest owner occupied lender and Westpac the largest investor loan provider.

Given the weak credit growth, this puts into sharp contrast the reported rises in home prices. We know transaction volumes remain low, but our industry contacts indicate a stronger pipeline of applications. Despite this the run-off of existing loans is translating to low net growth.

Even then, loan growth is still strong relative to income growth. But actually the most significant element is the fall in business credit, as more sectors come under pressure.

These results appear to be at odds with the RBA’s glass half full view of the economy, and may indicate more weakness in the GDP out-turn next week.

Blog")