Now Westpac has broken the dam, others are following, as expected. More will follow, especially late on a Friday afternoon…

Both regional banks, Suncorp and Adelaide Banks said that “challenging” market conditions have forced them to hike rates on variable rate mortgages across both owner-occupied and investor mortgage products by as much as 40 basis points.

Suncorp says rates on all variable rate home and small business loans will rise by 17 basis points and 10 basis points respectively, from September 14.

Adelaide Bank says rates for eight products across its range of principal and interest and interest-only owner-occupied and investor products will apply from September 7. Specifically, principal and interest-owner occupied and investment variable loans will be increasing by 12 basis points, interest-only owner occupied and residential investment loans will rise by 35 basis points and 40 basis and interest-only investment loans settled before January 1 will be increased by 12 basis points.

Lets be clear about what is happening here. Funding costs are indeed rising, as we show from the latest BBSW.

In addition some of the smaller lenders are lifting some deposit rates to try and source funding.

But the real story is the they are also running deep discounted rates to attract new borrowers, (especially low risk, low LVR loans) and are funding these by repricing the back book. This is partly a story of mortgage prisoners, and partly a desperate quest for any mortgage book growth they are capture. Without it, bank profits are cactus.

Once again customer loyalty is being penalised, not rewarded. Those who can shop around may save, but those who cannot (thanks to tighter lending standards, or time, or both) will be forced to pay more.

Seven lenders announced mortgage rates changes over the week ending 20 August, according to latest data from Canstar. In total, changes were made across more than 35 products, via Australian Broker.

Heritage bank was recorded making changes to its owner occupier and investment home loan products, changing its fixed rate products by decreases of 10 basis points to increases of 14 basis points. Heritage also recorded decreasing its Investment Discount Variable product by 10 basis points to a rate of 4.14%.

Meanwhile, Greater Bank increased both its owner occupier and investment variable rate products by 9 basis points. Goldfields Money reduced the standard home loan rate of its owner occupier product from 4.75% to 4.49%, and IMB dropped its accelerator – owner occupied 2 years rate from 3.82% to 3.59%. Community First CU lowered its “Accelerator Home Loan Inv True Value Var Hl – P&I 250k+” rate from 4.67% to 3.99%.

The average basic variable rates for the past week were:

Owner Occupier P&I Home Loans: 4.17%

Owner Occupier IO Home Loans: 4.64%

Investment P&I Home Loans: 4.58%

Investment IO Home Loans: 4.88%

However Australia’s largest member-owned bank CUA, made the largest increase, with interest rates up .25 percentage points across more than 20 products.

The increase applies to more than twenty P&I and interest-only variable home loan products, including the fresh start basic variable P&I which is now 4.32% (comparison rate 4.33%) for owner occupiers and 5.08% (comparison rate 5.13%) for investors.

It is an increase that Canstar group executive of financial services Steve Mickenbecker described as having the potential to become “a way of live”.

“The CUA move goes beyond what we have been seeing, and at 0.25% is the sort of increase that could become a way of life when the Reserve Bank eventually starts the upward move in the cash rate,” he said.

The bank’s chief sales officer, Paul Lewis said the rate hikes were not made lightly but were necessary given funding costs were expected to remain high in the coming year.

“CUA has absorbed these costs to date and we’ve delayed passing these costs on to borrowers. But over recent months, we’ve seen many other lenders have already reviewed interest rates in light of these higher funding costs.”

The Reserve Bank of Australia’s cash rate is currently at a historic low of 1.5% for a record 24th consecutive month, as the central bank has kept an unchanged economic growth forecast at a little over 3% in 2018 and 2019.

“Despite housing market headwinds from tighter credit conditions, the prospect of mortgage rates remaining reasonably stable should help to keep a floor under housing demand,” CoreLogic head of research Tim Lawless said in a statement.

CoreLogic data show that while the cash rate has remained unchanged for two years, the average standard variable mortgage rate has actually reduced by 5 basis points for owner occupiers and increased by 30 basis points for investors.

The U.S. housing market has garnered attention recently but for the wrong reason amid numerous signs of some weakening. Parts of the housing market have likely peaked while others haven’t, including new-home sales and construction, which pack the biggest GDP and employment punch.

Before assessing where housing is headed, it’s important to identify the possible culprits in the recent weakness in sales and construction. Common theories being tossed around blame the tax legislation that reduced the incentive to be a homeowner by increasing the standard deduction, lowering the deduction for a new mortgage, and capping the deductible amount of state and local taxes (which include property taxes) at $10,000 per year. More time is needed to assess the law’s impact on housing, since evidence is lacking. Sales of higher-priced homes, which would be most vulnerable, have been climbing. The tax legislation’s drag on housing will likely play out by reducing home sales and pushing some households to rent instead of buy, potentially putting upward pressure on rents.

We believe that affordability issues, mainly mortgage rates, are a more credible reason for housing’s recent slump. Affordability is a function of house prices, mortgage rates and income. Earlier this year, we noted that there was evidence that the housing market’s sensitivity to mortgage rates is increasing. The recent weakness in housing is consistent with this, since past increases in mortgage rates have been sufficient enough to be a drag.

To assess the impact, we ran through our U.S. macro model a scenario of a permanent increase in mortgage rates of 1 percentage point in the first quarter. That would be roughly the average of the gain during the taper tantrum and following the presidential election. The results show that the hit to residential investment is noticeable over the course of the subsequent year; real residential investment would be 7% lower than the baseline —enough to shave 0.1 to 0.2 percentage point off GDP growth for the year.

So far, mortgage rates have risen by 60 basis points this year, so the hit is smaller than our exercise, but it supports our view that higher interest rates are hurting housing.

Though there are headwinds, new-home sales and construction haven’t peaked, as fundamentals remain supportive. To estimate the underlying demand for new housing units, we broke it up into its main components, the trend in household formations, demand for second homes, and scrappage or obsolescence. The biggest source of demand is household formations, which have been running around 1.3 million per annum recently and this should continue over the next couple of years.

Demand for second homes tends to grow with the total number of housing units. We estimate that demand is running around 200,000 per annum. Housing units are scrapped from the housing stock each year because of demolition, disaster and disrepair. We estimate scrappage at 200,000 per year.

Even though underlying demand for new housing units is 1.7 million, housing starts should exceed that. Each year some housing units are started but never completed; assuming this is 1% of total housing starts—likely conservative—that would be an additional 17,000 starts. Underlying demand is about 25% below housing starts in the first half of this year. To close this gap over the next two years, would require homebuilding to rise 15% per annum. However, given the constraints facing builders this is unlikely. Alternatively, closing the gap in four years would require approximately an 8% gain per annum. Therefore, residential investment won’t be booming but it will be respectable.

The Productivity Commission report into Competition in The Financial Services Sector has shone a light on home loan pricing, and especially the fact that it is almost impossible for consumers to effectively compare products and prices. We think this is deliberate obfuscation by the industry. So today we look at home loan pricing section of the report in more detail.

The so called standard variable rate (SVR) is the starting point. This is an artificial price, an interest rate that each lender sets by taking into account their cost of funds, operating costs and target profit margins. Lenders make reference to their own SVR when pricing home loans and advertising home loan interest rates. They use it as their benchmark rate to which a margin may be added or (more usually) subtracted when making offers to consumers. Linking actual home loan interest rates to an SVR in this way allows lenders to easily increase or decrease prices on all variable rate loans on their books in response to changes in business or regulatory conditions.

The SVR provides a useful mechanism for each bank to control its entire book of variable rate mortgages while price discriminating between customers. While SVRs are individually set by each bank, they are public information and the SVRs set by different ADIs are closely related.

But the SVR is a source of misinformation for consumers The SVR is the advertised price of a home loan. But it is not the true market price, for almost anyone. Moreover, this ‘rate’ provides consumers with little useful information. It does not provide a meaningful price benchmark for the consumer regarding the actual price of home loans being offered in the market, as most home loans are priced below the SVR.

Almost no-one has to pay the SVR. In addition, customers might not have full information about the products and prices offered by other providers, preventing them from making an informed choice. For instance, transparency in the small business and home loan markets can be poor given the prevalence of unadvertised discounts to the standard variable rate, in many cases negotiated directly. Under these circumstances a customer will have difficulty determining the competitive price without incurring large search costs.

Looking at unpublished data on actual home loan interest rates, the PC found that, the overall discounting relative to the SVR is more prevalent among major lenders, discounting is slightly more widespread for loans issued to investors compared to owner-occupiers; this is more pronounced for non-major lenders. The shares of investor and owner-occupier loans at or below the SVR issued by non-major lenders have been similar in more recent years.

This strongly suggest there is no ‘discount’, just a hidden price that varies between consumers at the discretion of the lender. ASIC noted “that pricing and comparative pricing of mortgages is somewhat opaque at the moment, partly because the standard variable rate is not what a lot of people get, and it’s hard to know whether the discount you’re getting is the same as the discount other people are getting.”

These unpublished discretionary discounts can apply to a substantial portion of loans — for example, NAB submitted that, as at June 2017, discretionary pricing was being applied to up to 70% of new NAB-branded home loans. With the majority of successful home loan applicants offered a lower rate than the SVR, this suggests that the discretionary ‘discounts’ being offered by lenders, including those offered as part of a home loan package, are potentially being used to lull consumers into feeling good about accepting the offer without further negotiation on price or other aspects of the home loan.

In 2017 Deloitte noted that the long-term average discount on lenders’ back books was about 70 basis points. The ACCC reported that discounts on the headline interest rate on home loans by the four largest banks range from 78 to 139 basis points, over the period of 30 June 2015 to 30 June 2017. For major banks, the gap between SVRs and actual interest rates has increased over time. While only some of this gap is likely due to discounts on SVR, the gap nevertheless is in line with ASIC’s finding that, for most banks, the discount margin for home loans was larger in 2015 than in 2012. Similarly, RBA research found that interest rate discounts increased between 2014 and 2017, with home loan discounts higher for newer and larger loans.

In addition to most consumers paying below the SVR, it is difficult for consumers to reliably discover the actual price for the loan they anticipate seeking, as few of the discounts offered to consumers are public. While anecdotes, apps and websites abound, there is no benchmark against which to genuinely judge the market price. Information about individually-negotiated or discretionary discounts are usually not published. The ACCC noted that ‘lenders know the size of discounts they are prepared to offer and the type of borrowers they are prepared to offer them to but this information is not publicly available’.

Furthermore, since the decision criteria for discretionary discounts vary across lenders, borrowers may find it difficult to identify and assess the discounts for which they are eligible. But the potential savings from the total discounts are significant with borrowers potentially saving almost $4000 in the first year of the loan — highlighting the need for price transparency.

Despite the empirical evidence to the contrary, CBA sought to claim that the information available is indicative of the rate received. The PC says the “CBA’s linkage of advertised rates, comparison websites and the actual end rates paid by customers implies an ease of access to information that cannot be observed in practice”.

To the contrary, brokers in discussion with the Commission confirmed that consumers are generally only able to be certain of the actual size of their ‘discount’ once they have formally had their home loan application assessed. For a complex product, the idea of starting again, if the offer is unattractive, is a substantial barrier to pro-competitive customer behaviour (despite potentially being the best course of action). A consumer’s main focus is buying the property; the home loan facilitates this goal.

Next, bundling increases complexity of pricing. Many financial institutions offer package home loans: a bundle of products that usually includes a home loan, a transaction, offset or savings account, a credit card, and some types of insurance.

Consumers are attracted to home loan packages as lenders offer ‘discounts’ on the interest rate, including the SVR, or waive fees on some or all of the components of the package. However, bundling of a number of products into a home loan package can obscure the price of individual products making it difficult for consumers to assess the value of each individual component. It can also lock consumers into ongoing use of products that become less competitive over time as financial circumstances change).

The RBA said that “product bundling and a lack of transparency in the pricing of mortgages (with the prevalence of large unadvertised discounts in interest rates from advertised standard variable rates), are impediments to competitive outcomes”.

But this means that comparison rates are meaningless. The National Consumer Credit Protection Act requires that when advertising home loan products, lenders provide a comparison rate that includes the interest rate as well as most fees and charges. The purpose of comparison rates is to allow consumers to compare products with different fees and charges.

However, comparison rates are calculated using SVRs as the base interest rate. While comparison rates could potentially improve the competitiveness of the home loan market, they are only as useful as the interest rates on which they are based. As discussed above, for more than 90% of customers, SVRs (or the advertised rate) are not the market rate.

ASIC highlighted that the comparison rate is based on the advertised rate, not on the rate that people get when they either talk to a broker or a lender. So again, it’s not a very good guide as to whether the rate you are being offered is a good rate. It also doesn’t include other things that, you know, affect the cost of the loan like LMI, because the requirement is that a comparison rate include mandatory fees, but not contingent fees, and LMI, being a contingent fee is not included within the comparison rate.

The P&N Bank also noted the lack of relevance of the comparison rate: “While the home loan comparison rate methodology was a way of demonstrating comparability across product rates and fees, we acknowledge that it may not reflect real life scenarios based on borrower type, LVR, actual loan terms/amounts — or how pricing strategies are applied over the duration of that loan. And a submission from Home Loan Experts, a specialist mortgage broker, further noted the lack of understanding of comparison rates among consumers “We have not seen a customer use comparison rates or one that understands them. They are largely ignored by the industry and customers alike. For this reason, we recommend scrapping them altogether. And finally Canstar noted additional problems with the comparison rate — the assumptions used in formulating the rate are no longer representative of the lending market (including the loan.

SO when you are buying a home loan, the rate you get is frankly rigged, and you will never know whether you really ever got a good deal. That might help support bank profits, but once again consumers are being taken to the cleaners, and the regulators appear happy to support the poor customer outcomes. Frankly this is a disgrace,

ANZ has become the first big lender to cut its variable home loan rate for new customers, as the banks slug it out for business in a tightening market.

While banks including the CBA have cut fixed loan rates and offered “honeymoon deals” in recent weeks, the ANZ is the first to move on variable rates.

It comes at a time when there is upward pressure on interest rates as funding costs, particularly for smaller lenders, are rising.

The ANZ told mortgage brokers it was bringing down its basic principal and interest home rate for owner-occupiers by 0.34 percentage points to 3.65 per cent.

The ANZ offer only applies to new customers looking for a loan valued at 80 per cent or less than the value of their property.

Loan-to-value ratios above 80 per cent remain unchanged at 3.99 per cent.

Non-bank lenders growing market share rapidly

It comes at a time when small lenders have been eroding the market share of the Big Four banks.

While non-bank lenders hold less than 8 per cent of the mortgage market, their loan books have grown by about 14 per cent over the year, while growth at the Big Four is at a historically low level, a little over 1 per cent.

Ratecity research director Sally Tindall said it was a surprising move from ANZ to buck the rate-hike trend.

“It shows that the bank is competing hard to get new customers as non-banks threaten their market share,” Ms Tindall said.

“This comes at a time when the market was expecting ANZ to hike rates and not cut them and the [banking] royal commission has turned the playing field on its head.”

There are lower rates offered by the big banks in the market but they are generally so-called honeymoon deals that step up markedly after two or so years, or four years in the case of most fixed loan products.

Ms Tindall said the other three big banks were likely to come under pressure to follow ANZ’s lead or risk a further erosion of their market share.

Carefully targeted cut

Shaw and Partners bank analyst Brett Le Mesurier said ANZ’s move was carefully targeted.

“I was surprised by the extent of the reduction but ANZ has been courting the owner-occupier market for some time, and shunning the investment market relatively — most of their loan growth has been coming from Australian owner-occupier loans,” Mr Le Mesurier said.

He said there was little doubt that the differential between high-quality owner-occupier rates and investor loan rates was likely to increase.

“The banks are focusing on the below 80 per cent LVR [loan-to-value ratio] owner-occupier loans and that may well be because they expect the capital charges associated with those loans to reduce.

The bank is also cutting some of it fixed rate loans by up to 0.24 percentage points, following CBA’s move to cut fixed rates on various two and three-year fixed rate loans by 0.1 percentage points earlier this week.

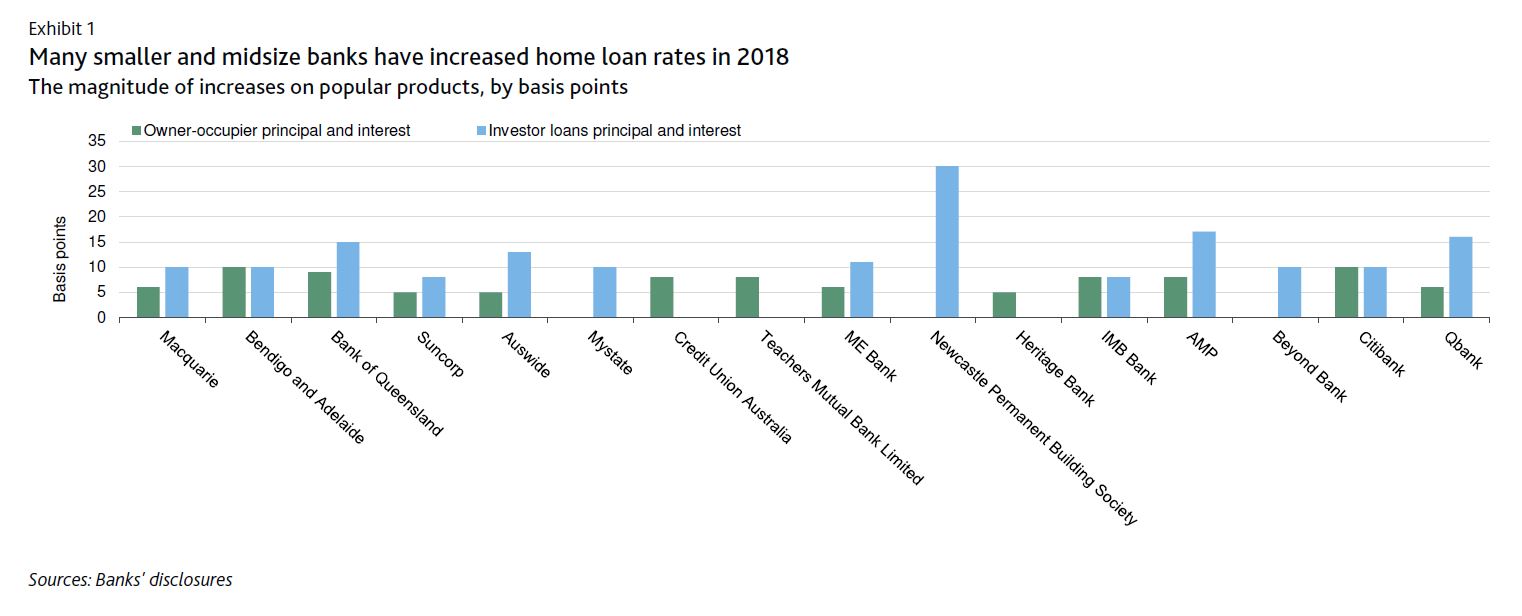

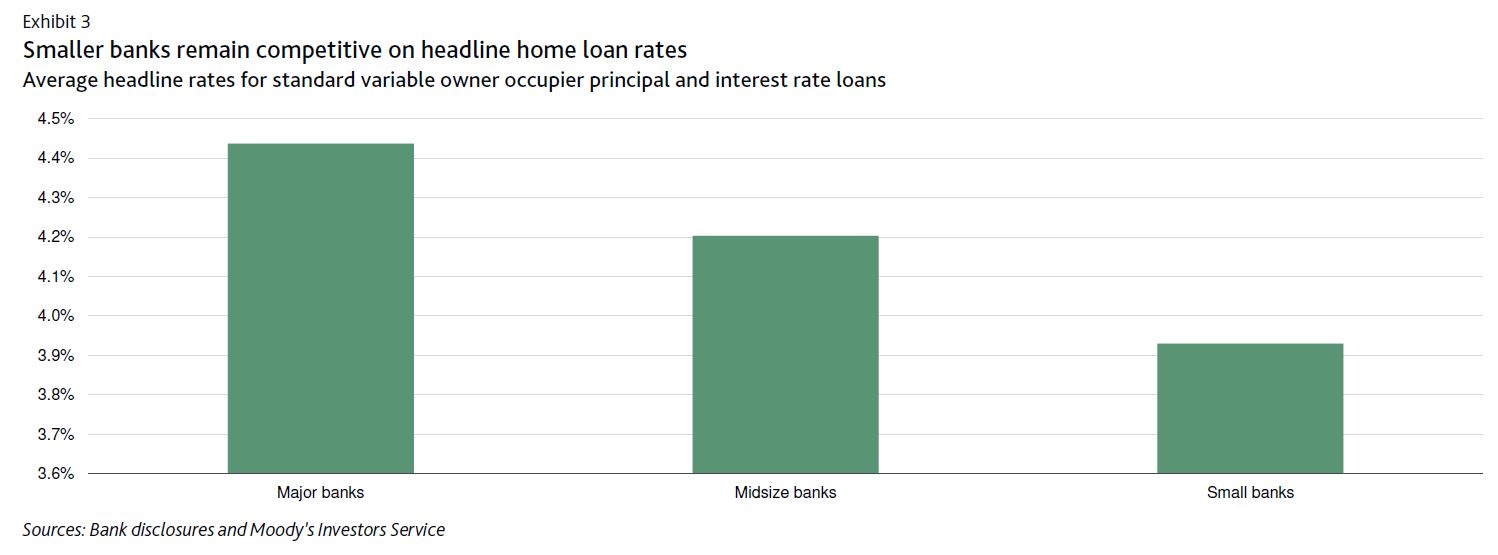

According to Moody’s , Australian regional banks Bendigo and Adelaide Bank and Teachers Mutual Bank Limited increased their home loan rates.

This follows a number of other small and midsize banks that have recently raised their home loan rates, taking the total to 16. The increase in rates is credit positive for these banks because it will help preserve their net interest margins amid higher wholesale funding costs and slower loan growth.

In contrast, Australia’s four-largest banks – Australia and New Zealand Banking Group Corporation, Commonwealth Bank of Australia, National Australia Bank Limited and Westpac Banking Corporation – have yet to raise their lending rates amid intense political scrutiny and against the backdrop of a probe by Australia’s Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry. Given that the four major banks have traditionally been the first-movers on headline home loan rates, we see smaller lenders’ willingness and ability

to increase rates as credit-positive evidence that they retain pricing power independent of the current challenges confronting the major banks.

To date, the rate increases have been concentrated in variable-rate home loan products, which are more popular in Australia than fixed-rate loans, at about 10 basis points for owner-occupier principal and interest loans, and higher for riskier products such as investor and interest-only loans.

Higher home loan rates will offset higher wholesale funding costs, with short-term funding costs being particularly affected.

Long-term debt issuance costs have increased proportionally less and, importantly, remain low by historical comparison. As such, the effect on banks’ weighted-average cost of long-term debt has thus far been muted. Positively, blended average deposit costs are marginally lower because banks have been paying lower rates on short-term deposits. The net effect varies by bank, according to various factors including their loan mix and funding profile. For instance, midsize listed banks have a moderately lower proportion of home loans and more short-term wholesale funding than smaller, predominantly mutual banks, which tend to have a higher concentration in home loans and are principally retail deposit-funded. As a consequence, the smaller banks may gain a little more profitability benefits from the latest round of rate increases. Following the rate increases, smaller banks still offer more favourable headline home loan rates than the major banks. However, the majors continue to offer significant discounts to attract the highest-quality borrowers at a time when system loan growth has slowed.

Despite the very high level of household leverage in Australia, we do not expect the current round of home loan rate moves to cause a sharp increase in loan delinquencies or credit costs. That is because labour market conditions, which are a strong indicator of mortgage performance, are likely to remain favourable, underpinned by solid economic growth forecasts. Additionally, the increases in home loan rates are small compared with the buffer built into home loan serviceability assessments. Australian lenders commonly assess borrowers’ repayment ability based on an interest rate floor of 7.25%, which is well above the average home loan rate of around 5.25% posted by Australian banks over the past three years. Moreover, collateral quality will remain strong, despite ongoing house price corrections in Sydney and Melbourne. The average loan-to value ratio for Australian bank home loan portfolios remains around 50%.

The big banks are under increasing pressure to move interest rates as more lenders make changes in response to increased costs.

Over the last week ten institutions have changed their interest rates to home loan products, with a total of 53 product level changes recorded.

While we have seen a number of rate increases over the last few weeks, despite the Reserve Bank of Australia (RBA) holding the cash rate, not all of the changes have been increases.

According to the information from comparison site Canstar, Yellow Brick Road made changes to all home loan types.

Mortgage House dropped its fixed rate investment products by 61 to 72 bps. It also made some changes to its owner occupier fixed rate products with interest rate decreases of 8 to 26bps.

Westpac also made changes this week. It increased its owner occupier fixed rate interest only home loans by 5 to 15bp.

Suncorp also made changes to its fixed rate products, decreasing the rates of its investment loans by 10 to 40bps.

Explaining the changes in interest rates, Steve Mickenbecker, group executive, financial services, at Canstar, said, “We are seeing a classic bit of churn that tends to happen at the top or bottom of a market.

“It has only just started in the last month or two, and we’re quite a while from seeing the end of it. The upward pressure is mounting, and at the same time the banks want to hold some competitive rates in the market.

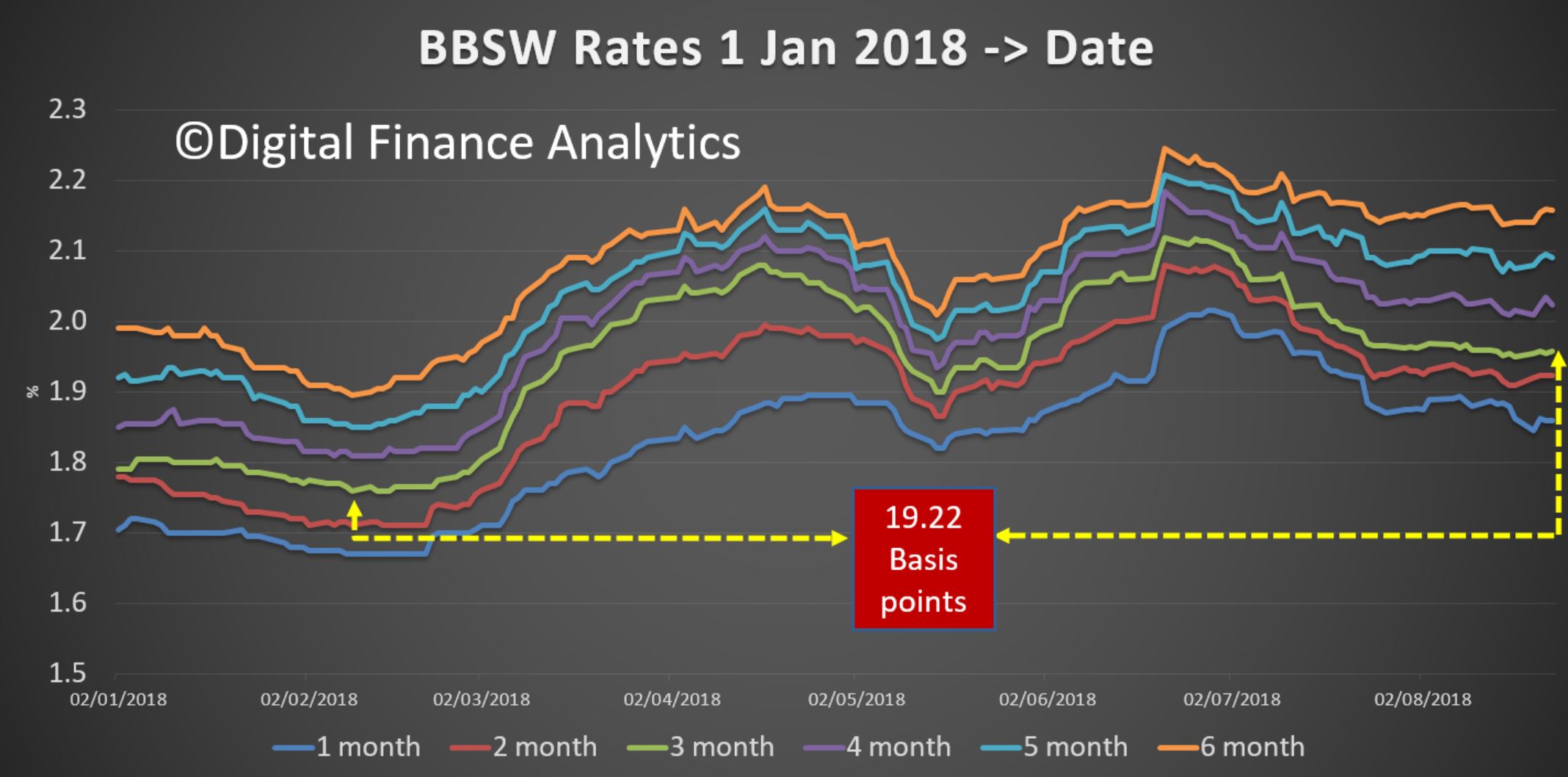

“With LIBOR and BBSW up 40 basis points in a month, it’s not surprising that we are seeing rate increases.

“The cost of wholesale funding is rising, which ultimately has to find its way through to home loan rates. At this stage it is the second-tier banks that have increased their variable rates by 8 to 10 basis points, not the big banks.

“The funding pressure sees some fixed rates rising, while other banks have moved down to maintain a competitive rate in the market for new business as they have increased their variable rates across the book for both the existing and new.”

While so far it has been the ‘second-tier’ banks changing variable rates, Mickenbecker said “big banks are under even more pressure”.

He added, “With around 80% of existing loans provided by the big four and the bulk in variable rates, any move in variable rates is going to flow through to most Australian borrowers.

“In the political world of banks through this Royal Commission, an increase is going to only increase the opprobrium. Westpac has moved interest only fixed rates up, reflecting that even the big lenders are feeling the funding pressure.

“But in terms of margin across the Westpac portfolio, the increase will hardly make a difference. With most big banks funding around 60 to 65% of their loan book through retail deposits, they have some buffer from wholesale funding increases.

“However, sooner or later they will have to move variable rates up. The timing might come down to when they feel they can face down the community.”

More banks have increased interest rates as the pressure of increased funding costs continues to mount.

Both Bendigo Bank and Teachers Mutual Bank Limited (TMBL) announced new rates. TMBL includes three banks: Teachers Mutual Bank, UniBank and Firefighters Mutual Bank.

While Bendigo has increased its variable interest rates for home owners, TMBL announced changes to its fixed rates for new customers to the group’s brands.

Bendigo has confirmed the changes are to absorb increasing funding costs.

Managing Director Marnie Baker said the changes reflect the increased cost of funding.

She said, “When setting interest rates our bank needs to consider many factors and carefully take into account the needs of our stakeholders including customers, shareholders, staff, partners and the broader community.

“Funding costs have been steadily increasing this year, and we’ve absorbed this cost impact to date. Today’s adjustment to the variable interest rates will assist in balancing this funding cost increase.

“We carefully balance the interests of our mortgage customers, those who earn money through deposits and those who invest in our Bank. We must ensure our pricing remains market competitive, provides the appropriate platform for sustainable growth and supports the hundreds of communities in which we operate.”

TMBL rates have increased on selected fixed rate home loan products.

The rates have been increased by 8, 9, and 9 basis points for 1, 2, and 3 year fixed rates respectively.

TMBL chief executive officer, Steve James, said, “These rate changes are the first increase in 12 months for fixed rates, and follow a decrease to our fixed rates last November.

“Any new members who join after these rate changes will still have access to a competitive market rate and great products, such as our 100% mortgage offset facility.”

Other banks to increase rates recently include AusWide, IMB, AMP, ING and Bank of Queensland.

Rate changes – Bendigo

Variable interest rates across home loans and lines of credit will increase for owner occupiers and investors as follows:

Owner occupier principal and interest loans will increase by 0.10% pa;

Owner occupier interest only loans will increase by 0.16% pa;

Investment loans will increase by 0.10% pa;

Lines of credit will increase by 0.10% pa.

The interest rate changes announced are effective Monday 23 July.

Customers on a residential variable interest rate with a $250,000 loan will see their repayments increase by $15.71 a month (principal and interest home loan over 30 years).

Rate changes – TMBL

The changes will affect owner-occupier, principal & interest, 1, 2 and 3 year fixed rate home loans.

The new rates are as follows:

1 Year Fixed rate OO P&I – 3.87% p.a.

2 Year Fixed rate OO P&I – 3.78% p.a.

3 Year Fixed rate OO P&I – 3.88% p.a.

The new rates are effective from Monday, 16 July 2018.

Ironic that in the past two weeks a number of smaller lenders, including Macquarie and Bendigio/Adelaide Bank all hiked their mortgage rates, the interbank rate has eased. A couple of weeks back it was above 32 basis points now its down to 25 basis points.

So does this mean the risk of mortgage rate hikes have also abated from the majors?

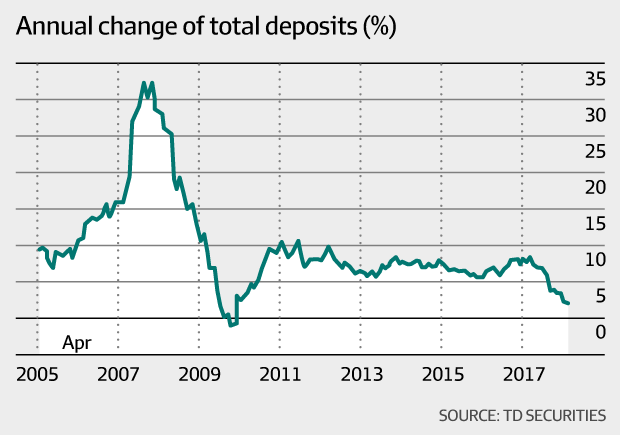

Not necessarily as according to the AFR today, investors are moving funds from deposits to offshore locations. The share of bank funding from deposits is falling, thus they will need “an estimated additional $70 billion of funding as superannuation funds shift out of cash into international assets while indebted households draw down on their savings”.

This additional funding is required to support continued mortgage loan growth.

The household savings ratio is also falling thanks to the need to service mortgage repayments.

The AFR concludes “The banks faced two choices in response to slowing deposit growth – either lift deposit rates, or increase their use of the capital markets to meet demand for credit as their loan books have swelled to $2.6 trillion”.

“Either measure should result in higher cost of bank funding”

In addition some of the smaller lenders are lifting some deposit rates to try and source funding.

In addition some of the smaller lenders are lifting some deposit rates to try and source funding.