The latest RBA Statement on Monetary Policy moves the dial a little in terms of expectations, but also is still predicting better economic outcomes down the track, if a little further away than originally expected (again).

By 2020, GDP could be somewhere between 1 and 5.5% – that should about cover it!

They call out risks relating to the amount of debt in the household sector, and the prospect of higher funding costs, and lower consumption should home prices fall. So there are a number of important items in the economic cross currents, and I am going to focus there today.

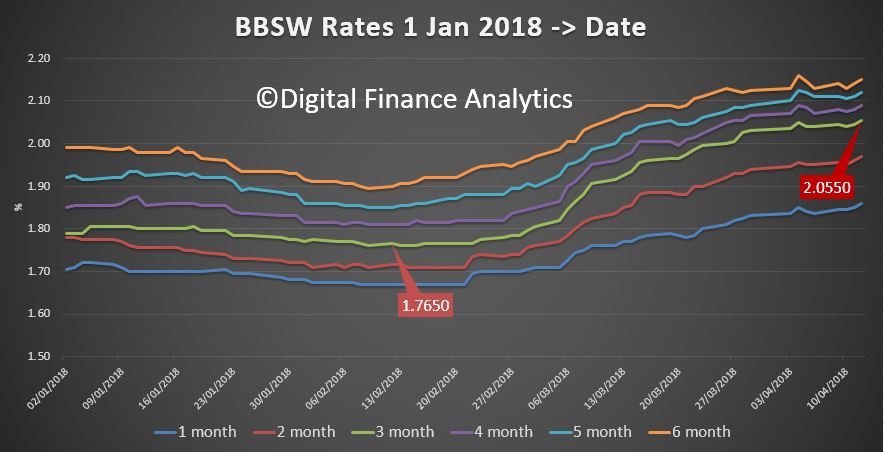

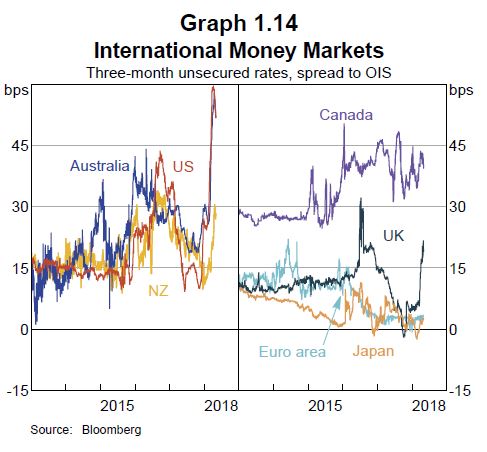

First, the highlight that US funding costs are on the rise, as US dollar money markets have increased.

They highlight that these developments have had a notable knock-on effect on Australian money markets. “In part, this is because Australian banks raise a portion of their funding in US markets to finance their domestic assets. So they have responded to higher US rates by seeking to borrow more in domestic markets, which has place upward pressure on rates in Australia. Similar effects, although less pronounced, can be seen on rates

in the United Kingdom and New Zealand. By contrast, banks in the euro area and Japan tend to raise funds in US dollar markets in order to fund US dollar assets, and so have less scope to substitute into domestic funding sources”.

“Higher bank bill swap (BBSW) rates affect bank funding costs in a number of ways. First, BBSW rates flow through to the rates banks pay on their new short- and long-term wholesale debt. In addition to this effect, bank bond

yields have increased by around 20 basis points since the start of the year.

Second, the higher BBSW rates increase some of the costs associated with hedging the risks on banks’ debt. Banks tend to issue fixed-rate bonds and then swap a sizeable share of these fixed interest rate exposures into floating rate exposures. This better aligns the interest rate exposure from their funding with their assets (which consist largely of variable interest rate loans). In doing this, the banks typically end up paying BBSW rates on their hedged liabilities, which flow through to the cost of funding.

Third, rates on wholesale deposits tend to be closely linked to BBSW rates, so the cost of these deposits is rising. Wholesale deposits include deposits from large corporations, pension funds and the government, and account for around 30 per cent of banks’ debt funding. Over the year to date, retail deposit rates have decreased slightly, mostly reflecting declines in the rates on online saving accounts. Most, but not all, of these decreases occurred

before the recent increase in BBSW”.

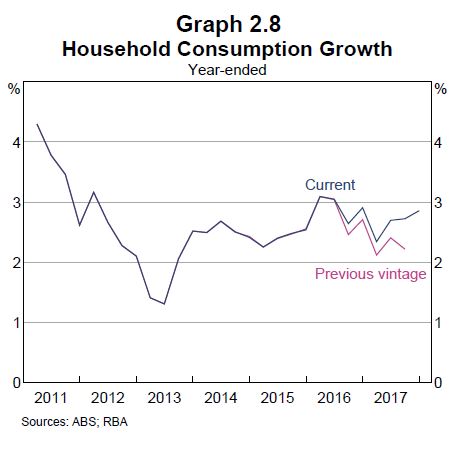

They suggest that “revisions” to the household consumption series shows a higher level of spend than previously thought. “Household consumption grew strongly in the December quarter and revisions to previous data

show that consumption growth held up better than previously thought in the second half of 2017 (Graph 2.8). Over the year, consumption grew by almost 3 per cent. Upward revisions to household consumption were particularly large for discretionary categories of expenditure, which tend to be more sensitive to household finances. Spending on overseas travel by Australian residents (which is classified as imports) was a major source of these revisions, while upward revisions to food and health expenditure

also lifted essential expenditure. More recent indicators suggest that household consumption growth was steady in early 2018: growth in retail sales held up in the first two months of the year. Measures of households’

sentiment towards their personal finances remain above their long-run averages, after increasing since the middle of 2017”.

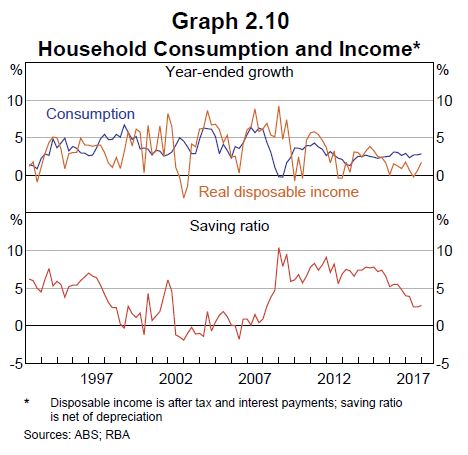

“Household consumption grew at a faster rate than household disposable income over 2017; the household saving ratio is reported to have declined, although it stabilised towards the end of the year as income growth picked up (Graph 2.10). Growth in real household disposable income was below average over 2017 at 1.7 per cent, largely because of low wages growth. The prospect of continued low growth in household income remains a key risk to the outlook for household consumption, especially given high levels of household debt. Slower growth in household net wealth, particularly in an environment of below-average income growth, adds to uncertainty about the outlook for consumption”.

“New dwelling construction declined by 5 per cent over 2017. This follows a few years in which new dwelling construction increased to high levels, supported by low interest rates, strong population growth and higher

housing prices in the eastern states. The recent decline in residential construction activity has been concentrated in detached housing, while higher-density construction activity has remained at high levels (Graph 2.14). Alterations and additions appear to have been less responsive to the cycle in new dwelling construction than in previous episodes”.

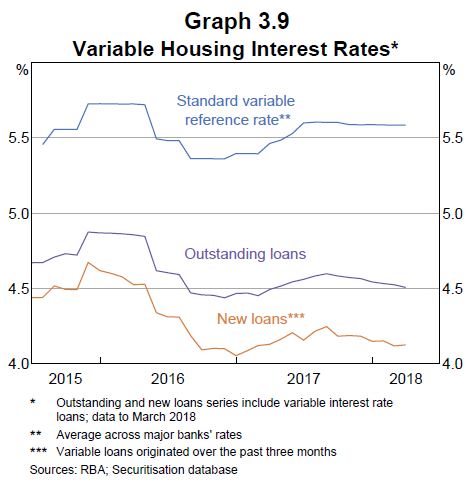

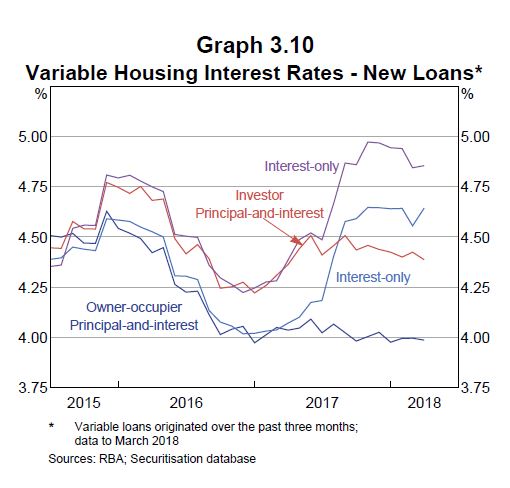

Turning to mortgage rates, they confirm that new loans tend to be at lower variable rates than the average for outstanding loans. Moreover, new IO borrowers continue to pay a premium above the interest rate on new principal-and-interest (P&I) home loans.

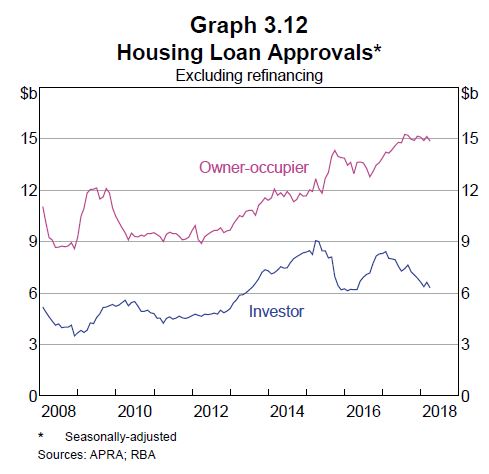

“The value of housing loan approvals (excluding refinancing) has continued to decline over recent months, to be 8 per cent below the recent peak in August 2017. This has been driven by investors, with owner-occupier approvals remaining relatively steady since mid 2017 (Graph 3.12). The decline in investor approvals has been primarily concentrated in New South Wales”. They reviewed interest only loans (again) and concluded that “Currently it appears that the share of borrowers who will not be able to afford higher P&I repayments and are not eligible to alleviate their situation by refinancing is small. Liaison with the banks suggests that there are a few borrowers needing assistance to manage the transition. Over the past year, some banks have reported in liaison that there has been a small deterioration in asset quality. For some borrowers this has tended to be only temporary as they take some time to adjust their financial affairs to cope with the rise in scheduled payments. For a small share of borrowers though, it reflects difficulty making these higher repayments. That share could increase in the event that an adverse shock led to a deterioration in overall economic conditions”.

The forecasts for domestic output growth are broadly similar to those presented in the February Statement. GDP growth is expected to strengthen a little over the next year or so as the drag from mining investment comes to an end and accommodative monetary policy provides ongoing support for sustained growth in household income and consumption, and non-mining business investment. However, the economy is not expected to encounter broad-based capacity constraints for some time.

“There is also uncertainty about how much any decline in spare capacity will build into wage pressures and inflation. Wages and employment growth are

key components of household income growth, and uncertainty about the outlook for household income growth translates into uncertainty about

household consumption and so GDP. Another key source of risk to consumption growth is that high levels of debt are likely to increase the

sensitivity of households’ consumption decisions to changes in their income or wealth.

Household indebtedness is high; and debt levels relative to income have edged higher because household credit growth has outpaced weak income growth over recent years. Steps taken by regulators to strengthen household balance sheets have led to a moderation in the growth in the riskier types of lending to households, but risks remain. Even if overall household indebtedness currently appears sustainable, a highly indebted household sector is likely to be more sensitive to changes in income, wealth or interest rates. For example, a highly indebted household facing weaker-than-expected growth in disposable income or wealth is more likely to respond by reducing consumption. Consumption growth may also be weaker for a time if indebted households choose to pay down debt more quickly rather than consume out of additional income.

Housing assets account for around 55 per cent of total household assets, so weaker housing prices could be a factor that leads to weaker consumption growth than is currently forecast. National housing prices have eased following several years of strong price growth. To date, the cooling of conditions in the established housing market does not appear to have dampened consumption growth. Although the earlier gains in national housing wealth may not have encouraged much additional consumption, it is possible that households’ consumption and saving decisions could be more sensitive to an easing in housing price growth.

Tighter lending standards could also affect the outlook for domestic growth. While APRA recently announced plans to remove the investor loan

benchmark, the change in dynamics in the housing market and the high level of public scrutiny of lending decisions could see some tightening in the

supply of credit. This could affect the outlook for consumption and dwelling investment”.

He highlighted ongoing low inflation and wages growth, despite a pick-up in business investment, as well as continuing high household debt, and the prospect that the next rate move will likely be up.

I am still amazed that household credit is still being allowed to run on at 3x income/cpi. So, I question his statement that “things now look less worrying than they were a while back” on this front! Household debt has NEVER been higher.

As you are aware, at our meeting today, the Board kept the cash rate unchanged at 1½ per cent. It has been at this level since August 2016 – that is for 21 months – which is the longest period without a change.

At today’s meeting, when we measured the pulse of the Australian economy, we assessed it to be stronger than a year ago. Business conditions are around their highest level for many years and the long-awaited pick-up in non-mining business investment is taking place. There has been a large pick-up in infrastructure spending in some states. The number of Australians with jobs has also grown strongly over the past year. The unemployment rate is lower than it was a year ago, although there has been little change for the past six months. Growth in consumer spending has been solid, although it is lower than it was before the financial crisis.

At our meeting today, we also discussed the latest inflation data, which showed that both CPI and underlying inflation were running marginally below 2 per cent. This was in line with our expectations and provides further confirmation that inflation has troughed, although it remains low. Strong competition in retailing is holding down the prices of many goods: for example, over the past year, the price of food increased by just ½ per cent, the price of clothing and footwear fell 3½ per cent and the price of household appliances fell 2½ per cent. Importantly, these outcomes are helping to offset some of the cost of living pressures arising from higher electricity prices, which nationally are up 12 per cent over the past year.

Another factor influencing recent inflation outcomes is the subdued growth in wages. Increases in wages of around 2 per cent have become the norm in Australia, rather than the 3–4 per cent mark that was the norm a while back. This is an issue we have been discussing around our board table for some time. While low growth in wages has helped boost employment, it has also put the finances of some households under strain, especially those who borrowed on the basis that their incomes would grow at the old rate. And in terms of the inflation target, it is difficult to see how a continuation of 2 per cent growth in wages is compatible with us achieving the midpoint of the inflation target – 2½ per cent – on a sustained basis. So from that perspective alone, a pick-up in wages growth over time would be welcome. Perhaps more importantly, sustained low wages growth diminishes the sense of shared prosperity that we have in Australia.

In our liaison with businesses, including here in Adelaide, many tell us about the very competitive environment in which they are operating. They tell us about how this competitive environment means that they have limited ability to pay bigger wage increases. At the same time, though, we are hearing a few more reports of larger increases in those areas where there is a shortage of workers with the necessary skills. After all, the laws of supply and demand still work. We also see evidence in the aggregate data that wages growth has troughed and we expect to see a further pick-up. This is likely to be a gradual process, though.

At today’s meeting, the Board also reviewed the staff’s latest forecasts for the economy. These will be published on Friday in our quarterly Statement on Monetary Policy. Those of you who are close readers of this document will notice some changes in this issue, as we seek to make the report more thematic.

The latest forecasts should not contain any surprises, with only small changes from the previous set of forecasts, issued three months ago. This year and next, our central scenario remains for the Australian economy to grow a bit faster than 3 per cent. This would be a better outcome than the average of recent years. If we are able to achieve this, we will make inroads into the remaining spare capacity in the economy and see a further modest decline in the unemployment rate. Inflation is expected to remain low, at around its current level for a while yet, before gradually increasing over the next couple of years, towards 2½ per cent. A key element here is the pick-up in wages growth that I just mentioned.

So, in summary, there has been progress in lowering unemployment and having inflation return to around the middle of the target range, and we expect further progress in these two areas over the next couple of years.

The other key point is that the progress we are making is only gradual: our central scenario is for a gradual pick-up in wages growth, a gradual lift in inflation, and a gradual reduction in the unemployment rate. While we might like faster progress, it is encouraging that things are moving in the right direction and are likely to continue to do so.

If this is how things turn out, it is reasonable to expect that the next move in interest rates will be up. This would reflect conditions in the economy returning to normal. In our discussions today, though, the Board again agreed that there was not a strong case for a near-term adjustment in the cash rate. This reflects our view that the progress in moving towards full employment and having inflation return to the middle of the target range is likely to be only gradual. The Board’s view is that while this progress is occurring, the best contribution we can make to the welfare of the Australian people is to hold the cash rate steady and for the Reserve Bank to be a source of stability and confidence.

Domestically, for some time, we have seen the main risk to be related to household balance sheets. For a while, trends in household credit were quite concerning. On this front, things now look less worrying than they were a while back, although the level of household debt remains very high, which carries certain risks. In terms of financing, we also discussed the potential for some tightening in financial conditions in Australia. In the United States, the cost of US dollar funding has increased for reasons not directly related to monetary policy and this increase is flowing through into higher money market rates in Australia. We expect some of this to be reversed in time, although it is difficult to tell by how much and when. It is also possible that lending standards in Australia will be tightened further in the context of the current high level of public scrutiny. We will continue to watch these issues carefully.

Absolutely no surprise that that RBA held the cash rate again today. And very little change of tune in the accompanying release. It looks like the cash rate will stay firmly where it is for some time to come.

At its meeting today, the Board decided to leave the cash rate unchanged at 1.50 per cent.

The global economy has strengthened over the past year. A number of advanced economies are growing at an above-trend rate and unemployment rates are low. The Chinese economy continues to grow solidly, with the authorities paying increased attention to the risks in the financial sector and the sustainability of growth. Globally, inflation remains low, although it has increased in some economies and further increases are expected given the tight labour markets. As conditions have improved in the global economy, a number of central banks have withdrawn some monetary stimulus and further steps in this direction are expected.

Long-term bond yields have risen over the past six months, but are still low. Equity market volatility has increased from the very low levels of last year, partly because of concerns about the direction of international trade policy in the United States. Credit spreads have also widened a little, but remain low. Financial conditions generally remain expansionary. Conditions in US dollar short-term money markets have, however, tightened over the past few months, with US dollar short-term interest rates having increased for reasons other than the increase in the federal funds rate. This has flowed through to higher short-term interest rates in a few other countries, including Australia.

The price of oil has increased recently, as have the prices of some base metals. Australia’s terms of trade are expected to decline over the next few years, but remain at a relatively high level.

The Bank’s central forecast for the Australian economy remains for growth to pick up, to average a bit above 3 per cent in 2018 and 2019. This should see some reduction in spare capacity in the economy. Business conditions are positive and non-mining business investment is increasing. Higher levels of public infrastructure investment are also supporting the economy. Stronger growth in exports is expected. One continuing source of uncertainty is the outlook for household consumption, although consumption growth picked up in late 2017. Household income has been growing slowly and debt levels are high.

Employment has grown strongly over the past year, although growth has slowed over recent months. The strong growth in employment has been accompanied by a significant rise in labour force participation, particularly by women and older Australians. The unemployment rate has declined over the past year, but has been steady at around 5½ per cent for some months. The various forward-looking indicators continue to point to solid growth in employment in the period ahead, with a further gradual reduction in the unemployment rate expected. Notwithstanding the improving labour market, wages growth remains low. This is likely to continue for a while yet, although the stronger economy should see some lift in wages growth over time. Consistent with this, the rate of wages growth appears to have troughed and there are reports that some employers are finding it more difficult to hire workers with the necessary skills.

Inflation remains low. The recent inflation data were in line with the Bank’s expectations, with both CPI and underlying inflation running marginally below 2 per cent. Inflation is likely to remain low for some time, reflecting low growth in labour costs and strong competition in retailing. A gradual pick-up in inflation is, however, expected as the economy strengthens. The central forecast is for CPI inflation to be a bit above 2 per cent in 2018.

The Australian dollar has depreciated a little recently, but on a trade-weighted basis remains within the range that it has been in over the past two years. An appreciating exchange rate would be expected to result in a slower pick-up in economic activity and inflation than currently forecast.

The housing markets in Sydney and Melbourne have slowed. Nationwide measures of housing prices are little changed over the past six months, with prices having recorded falls in some areas. In the eastern capital cities, a considerable additional supply of apartments is scheduled to come on stream over the next couple of years. APRA’s supervisory measures and tighter credit standards have been helpful in containing the build-up of risk in household balance sheets, although the level of household debt remains high.

The low level of interest rates is continuing to support the Australian economy. Further progress in reducing unemployment and having inflation return to target is expected, although this progress is likely to be gradual. Taking account of the available information, the Board judged that holding the stance of monetary policy unchanged at this meeting would be consistent with sustainable growth in the economy and achieving the inflation target over time.

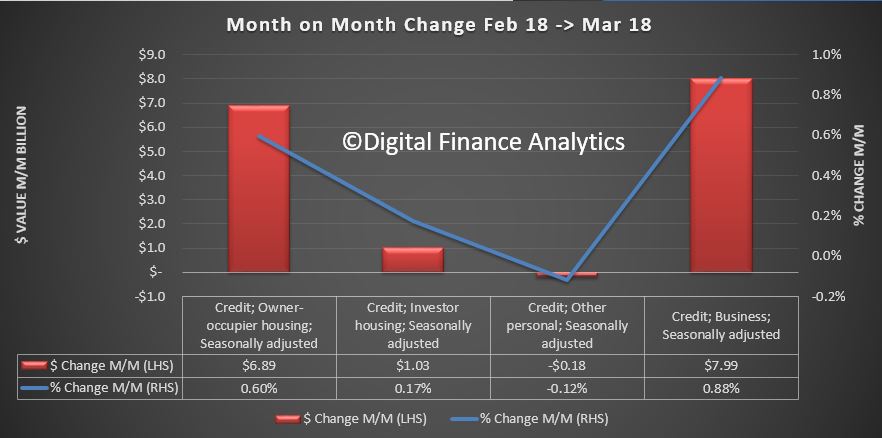

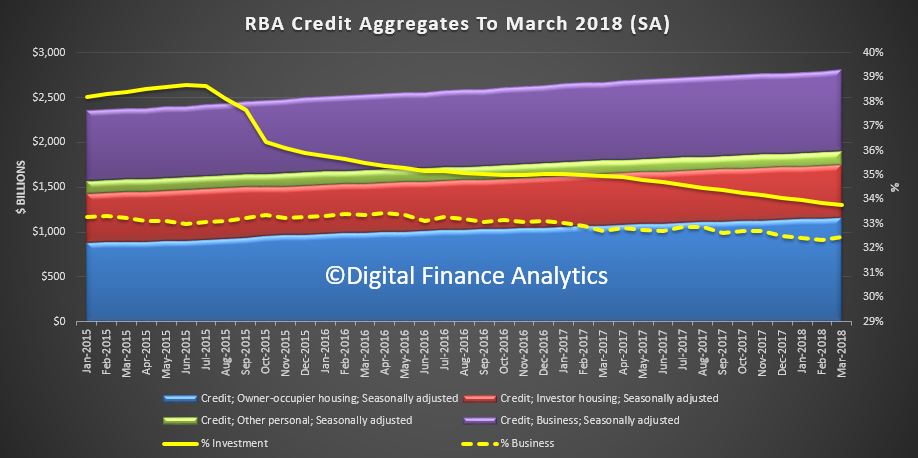

The RBA have released their credit aggregates to March 2018. Looking at the month on month movements, total owner occupied lending rose 0.6%, or $6.89 billion to $1,157.8 billion and investor mortgage lending rose 0.17% or $1.03 billion to $590.2 billion. So overall mortgage lending rose 0.46% in the month, up $7.92 billion (all seasonally adjusted) to $1.75 trillion. A record.

Personal credit fell 0.12%, down $0.18 to $152 billion. Business credit rose 0.88%, or $7.99 billion to $913 billion.

The trends show that the share of investment loans fell a little on the total portfolio to 33.8%, while business lending was 32.5% of all lending, up just a little.

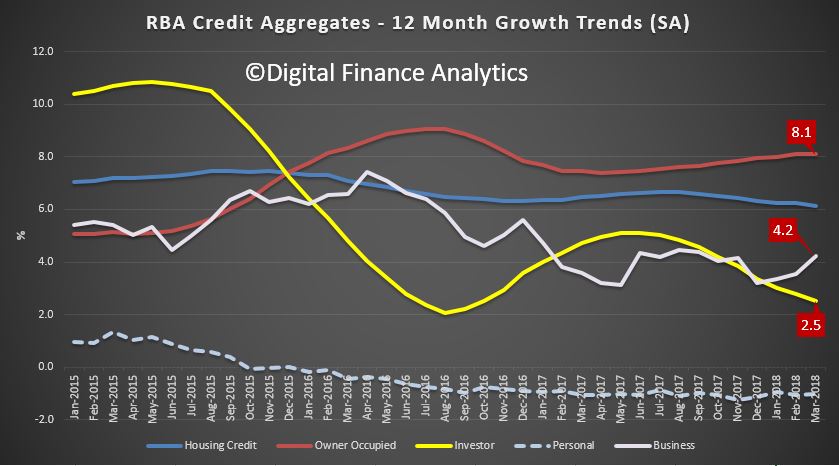

The 12 month average growth rates show that owner occupied loans rose 8.1%, while investment loans grew 2.5%. Business rose 4.2%, and personal credit fell again. Overall growth rates of credit for housing slide just a little to 6.1%. This is 3 times the rate of inflation and wage growth! Household debt therefore is still rising.

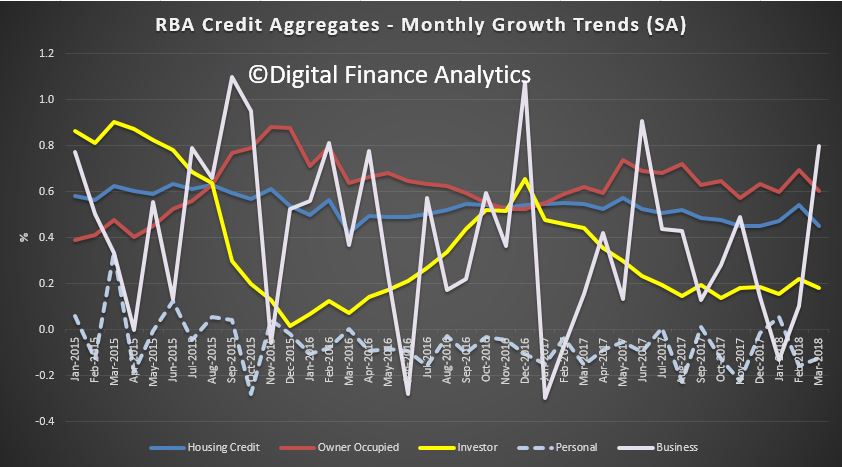

The noisy monthly data highlights how volatile the business lending trends are.

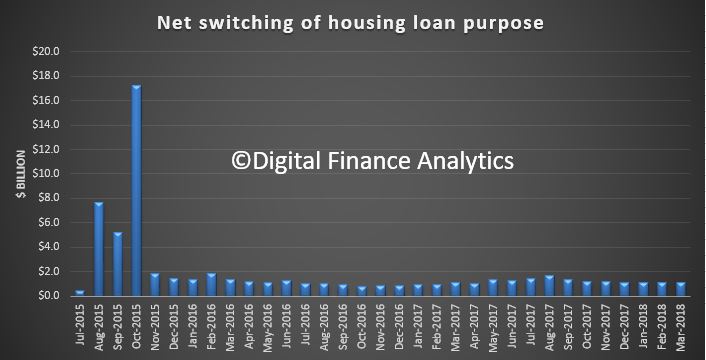

They also reported that the switching between investor and owner occupied loans continues to run at similar levels, after the hiatus in 2015.

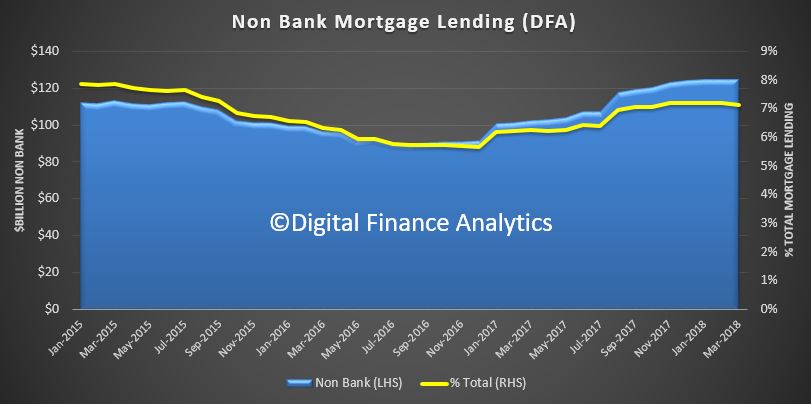

But set that aside, we have plotted the relative value of the mortgage pools at the total level, and the ADI level (not seasonally adjusted). The trend shows around 7% of lending is non-bank, up from 5.7% in 2017. In value terms this equates to $124 billion, up from $90 billion in 2016.

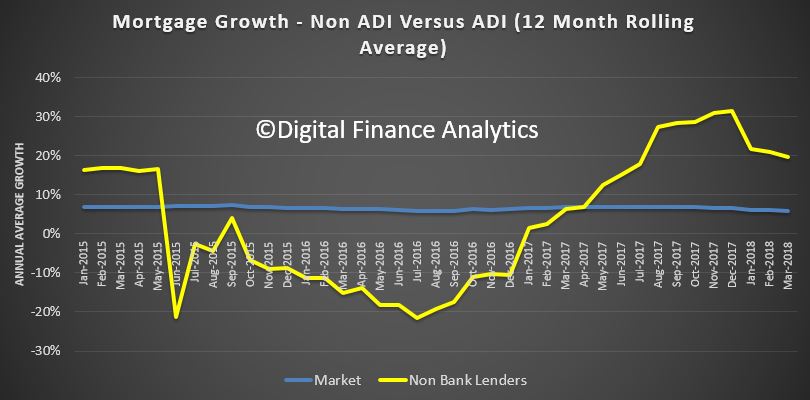

Another way to show the data is to look at the rolling 12 month growth trend. This shows that non-bank lending has been growing at up to 30% and significantly higher than the market at 5.94%.

So this is all playing out as expected. As the majors throttle back on new mortgage lending under tighter controls, the non-bank sector continues to pick up the slack. This is a concern as the regulatory environment for these lenders is weaker, with both ASIC and APRA now involved, ASIC from a responsible lending perspective and APRA from new supervision on the non-bank sector, despite their failure in the core banking sector. So we expect to see significant non-bank lending growth, ahead, which will stoke the current massively high household debts even higher.

The total loan mortgage growth is still significantly higher than income growth. This is not sustainable, and will lift mortgage stress higher again – our new data will be out in a few days.

This week’s Australian consumer price inflation figures revealed a 0.4% increase for the March quarter, and 1.9% for the last 12 months. The March quarter figure was below market expectations of 0.5%, and also the previous (December quarter) figure of 0.6%. Education prices were up 2.6% on the quarter, and health prices up 2.2% (or 4.2% for the year to March 2018).

Numerous central banks around the world have a similar approach. The basic idea is that a central bank can build a reputation over time to commit to monetary policy such that inflation lies in the band.

Now there are pros and cons to this approach to monetary policy, and it has its critics. But that is another tale for another day.

Just assuming that inflation targeting is the correct objective, how is the RBA doing? Well, one small hitch in the plan is that inflation has been outside the band for a long time now (basically since 2014), as the RBA’s own figures show.

Given the level of unemployment in Australia, low wages growth, and stubbornly low inflation, the RBA probably should have cut rates further a fair while back. But they seem, probably rightly, terrified of further fuelling a potential housing bubble.

Meanwhile, the credibility of their commitment to the inflation target withers. If only the regulation of our banking and finance sector had been better for the last, say, decade or two.

Speaking of such regulation, RBA assistant governor Chris Kent gave a speech Tuesday about the important issue of interest-only loans. Kent’s speech was significant because it followed up on remarks in the RBA minutes about the same issue that I discussed in this column last week.

It seems that the RBA “house view” on interest only loans is as follows. There could be a problem but the Australian Prudential Regulation Authority (APRA) stepped in and the banks have voluntarily tightened lending standards recently. Also because the average household with an interest only loan has a buffer of savings, everything will be fine. Nothing to see here.

I hope the RBA’s conclusion is right, but I know for sure that the reasoning is not. It’s actually the marginal household’s financial position and behaviour that matters, not the average household.

The average United States borrower with an adjustable-rate mortgage did not default in 2007, 2008 or 2009. But these mortgages were a huge contributor to the financial crisis, along with subprime mortgages.

Kent dutifully laid out the risks from interest only loans, saying:

Because there’s no need to pay down principal initially, the required payments are lower during the interest-only period. But when that ends, there is a significant step-up in required payments (unless the interest-only loans are rolled over).

Indeed, unless they can be rolled over. Which they can’t now because of APRA and the banks finally doing something.

Now, prices (interest rates) on interest only loans have gone up as part of the bank response. This has led a bunch of folks to shift to amortising loans, where the principal of the loan is paid down over the life of the loan. So those borrowers who haven’t shifted to these loans already, really don’t want to.

Maybe they can’t afford to because of the increased repayments, that can jump 30% or more per month.

So what does happen? First Kent says many borrowers save ahead of time, expecting a rise in repayments. Yes, the prudent ones.

But how many non-prudent borrowers have their been in the Australian property market in recent years? Hint: a lot.

Kent also points to borrowers who seek to refinance their interest only loan. But banks don’t really want to, and APRA doesn’t want to let them. And who is going to be able to? The safer borrowers who did save and so don’t really need to avoid amortisation. The risky borrowers can’t refinance.

Kent says some borrowers will have to cut their spending. Chuckle, chuckle. And the final option is to sell their house.

Sure, no problem, unless lots of folks want to do that all at once. Then it’s a fire sale that detonates the housing market.

I really do hope we escape the interest only debacle unscathed. But if we do it will be pure, dumb luck, not a consequence of good design or sound regulation.

It definitely doesn’t justify the RBA’s house view in Kent’s concluding remarks that:

The substantial transition away from interest-only loans over the past year has been relatively smooth overall, and is likely to remain so. Nevertheless, it is something that we will continue to monitor closely.

Perhaps a there should have been a little more monitoring before interest only loans got to be 40% of all loans and more than half of the loan book of one of our biggest banks.

Author: Richard Holden, Professor of Economics and PLuS Alliance Fellow, UNSW

Mortgages on interest-only terms have become an increasingly prominent part of Australian housing finance over the past decade. At their recent peak, they accounted for almost 40 per cent of all mortgages. While interest-only loans have a role to play in Australian mortgage finance, their value has limits.

Other things equal, interest-only loans can carry greater risks compared with principal-and-interest (P&I) loans. Because there’s no need to pay down principal initially, the required payments are lower during the interest-only period. But when that ends, there is a significant step-up in required payments (unless the interest-only loans are rolled over). This owes to the need to repay the principal over a shorter period; that is, over the remaining term of the loan. Also, because the debt level is higher over the term of the loan, the interest costs are also larger.

For housing investors, the key motivation for using an interest-only loan is clear. By enabling borrowers to sustain debt at a higher level over the term of the loan, interest-only loans maximise interest expenses, which are tax deductible for investors. They also free up funds for other investments.

For those purchasing a home to live in, there are other motivations for an interest-only loan. They provide a degree of flexibility when it comes to repayment. They can assist households to manage a temporary period of reduced income or heightened expenditure. That might occur, for example, when a household wants to work less in order to raise children, cover the cost of significant renovations or obtain bridging finance to buy and sell properties. They can also appeal to households without a steady flow of regular income, such as the self-employed. So there are understandable reasons why borrowers have taken out interest-only loans.

During interest-only periods, disciplined borrowers will be able to provision for future repayment of principal. They can accumulate funds in an offset or redraw account, or build up other assets. With sufficient saving over the interest-only period, the health of their balance sheet need be no different than it would have been with a P&I loan.

If, however, a borrower spends the extra cash flow available to them during the interest-only period (compared with the alternative of a P&I loan), they will need to make sizeable adjustments when that ends. They will have to either secure additional income by that time or reduce their consumption (or some combination of both). That will be more difficult and possibly come as a shock to the borrower if they haven’t planned for it in advance.

If the borrower has made no provisions and is unable to make the necessary adjustment, they may need to sell the property to repay the loan. Therein lies an additional risk inherent in interest-only lending. Moreover, the borrower’s ability to service the loan is not fully tested until the end of the interest-only period. If the borrower defaults, the potential loss for the lender will be larger than in the case of a P&I loan given that interest-only loans by design allow borrowers to maintain the debt at a higher level over the term of the loan.

That’s why, when providing interest-only loans, prudent lenders will carefully assess the borrower’s ability to make both interest and principal payments. Among other things, banks have to make their loan ‘serviceability assessments’ based on the status of the borrower’s income and expenditure at the time of origination. To help manage risks, lenders also typically limit the maximum interest-only period to five years.

The role of interest-only lending and its potential implications for financial stability have been of interest to the Reserve Bank for some time. The possible effects of the transition at the end of interest-only periods were discussed in the recent Financial Stability Review. I will come to that issue shortly, but first I want to review the regulatory responses to the strong growth of interest-only lending in recent years.

Tightening of Lending Standards

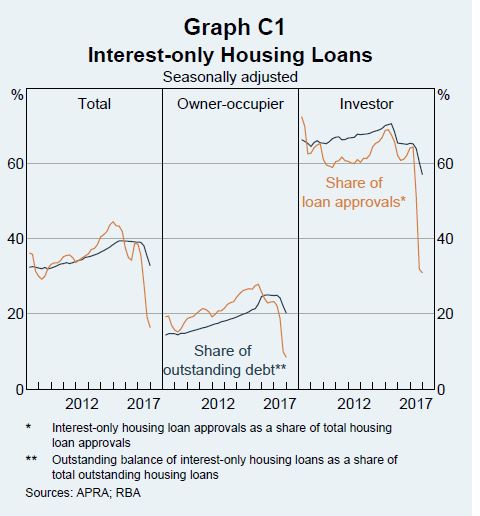

Interest-only loans had grown very strongly for a number of years in an environment of low mortgage rates and heightened competitive pressures among lenders. The share of housing credit on interest-only terms had increased steadily to almost 40 per cent by 2015 (Graph 1). The share of credit on interest-only terms has always been much higher for investors than owner-occupiers (consistent with the associated tax benefits for investors). But interest-only loans for owner-occupiers had also grown strongly.

Graph 1

In 2014, the Australian Prudential Regulation Authority (APRA) acted to tighten standards for interest-only loans, and mortgages more generally. APRA required serviceability assessments for new loans to be more conservative by basing them on the required principal and interest payments over the term of the loan remaining after the interest-only period. (Previously, some banks were assuming that the principal was being re-payed over the entire life of the loan, which was clearly a lower bar for the borrower to meet.) At about the same time, APRA acted to ensure that the interest rate ‘buffer’ used in the serviceability assessments for all loans was at least 2 percentage points above the relevant benchmark rate (with an interest rate floor of at least 7 per cent). Also, that test was required to include other, existing debt (which is often substantial for investors). The application of such a buffer in serviceability assessments implies that borrowers should be able to accommodate a notable rise in required repayments.

When APRA tightened loan serviceability requirements, it also limited the growth of investor lending (to 10 per cent annually). The share of interest-only loans in total housing credit then stabilised for a time at around 40 per cent, having increased steadily up to that point.

In early 2017, in recognition that continued strong growth of interest-only loans was contributing to rising risks, APRA further tightened standards on interest-only lending. Among other things, banks were required to limit new interest-only lending to be no more than 30 per cent of new mortgage lending. Banks were also required to tightly manage new interest-only loans extended at high loan-to valuation ratios (LVRs).

The Past Year or So

In response to those recent regulatory measures, the banks raised interest rates on investor and interest-only loans. From around the middle of 2017, the average interest rates on the stock of outstanding variable interest-only loans increased to be about 40 basis points above interest rates on equivalent P&I loans (Graph 2). Prior to that, there was little difference in interest rates on these loans.

Graph 2

The higher interest rates contributed to a reduction in the demand for new interest-only loans. In addition, because banks had raised interest rates on all of their (variable rate) interest-only loans, existing customers had an incentive to switch their loans from interest-only to P&I terms before their scheduled interest-only periods ended. Many took up that option.

The combination of higher interest rates and tighter lending standards contributed to the share of new loans that are interest-only falling comfortably below the 30 per cent limit. The stock of interest-only loans in total housing credit has also declined noticeably, from close to 40 per cent to almost 30 per cent.

This reduction in the stock of interest-only loans over the past year was substantial. It represented about $75 billion of loans (out of a total stock of interest-only loans of almost $600 billion in late 2016).

While many of the customers switching chose to do so in response to the higher rates on interest-only loans, there are likely to have been some borrowers who had less choice in the matter. Some borrowers may have preferred to extend their interest-only periods but may not have qualified in light of the tighter lending standards. We don’t have a good sense of the split between those borrowers that switched voluntarily and those that switched reluctantly. However, our liaison with the banks suggests that most borrowers have managed the transition reasonably well. Also, the share of non-performing housing loans over the past year remains little changed at relatively low levels. Moreover, the growth of household consumption has been sustained; indeed it picked up a touch in year ended-terms over 2017.

Given the large number of borrowers switching to P&I loans, it’s not surprising that scheduled housing loan repayments have increased over the past year (Graph 3). Meanwhile, unscheduled payments have declined. With total payments little changed, the rise in scheduled payments has had no obvious implications for household consumption.

Graph 3

The Next Few Years

So, many interest-only borrowers appear to have responded voluntarily to the pricing incentives and switched to P&I loans. This means that it is possible that the current pool of interest-only borrowers is a little more likely than usual to want to continue with their interest-only loans. For some of these borrowers, the decision not to switch to a lower interest rate P&I loan may reflect the higher required payments for such a loan.

Some commentators have gone so far as to suggest that when scheduled interest-only periods end, many borrowers will be forced onto P&I loans and will find it challenging to make the higher required payments. Commentators go on to suggest that such borrowers will either have to sell their property or reduce other expenditure significantly in order to service their loans.

In what follows, I’ll explore these concerns by providing some estimates of the effect of borrowers switching to P&I loans in the years ahead. I’ll focus my attention on the potential size of the change in households’ cash flows as well as the effect on the household sector’s consumption.

Around two-thirds of interest-only loans in the Reserve Bank’s Securitisation Dataset are due to have their interest-only periods expire by 2020 (Graph 4). That is consistent with interest-only periods typically being around five years. Only a small share of loans have interest-only periods of 10 years (or longer), with very few loans on these terms having been written (and securitised) since 2015. This is in line with the earlier measures to tighten lending standards.

Graph 4

Applying this profile of expiries to the total value of all interest-only loans suggests that about $120 billion of interest-only loans is scheduled to roll over to P&I loans each year over the next three years (Graph 5). This annual figure is equivalent to around 7 per cent of the stock of housing credit outstanding.

While the value of loans scheduled to reach the end of the interest-only periods appears large, it is worth emphasising that expirations of this size are not unprecedented. At the end of 2016, a similar value of loans was due to have their interest-only periods expire in 2017. What is different now, however, is that many households have already switched willingly in 2017 in response to pricing differentials, and lending standards were tightened further in recent years. This could affect the ability of some borrowers to extend their interest-only periods or to refinance to a P&I loan with a longer amortising period so as to reduce required payments on the loan.

Graph 5

To estimate the effect the expiry of interest-only periods, I’ll consider the case where all of the interest-only periods expire as scheduled. While extreme, this provides a useful upper-bound estimate of the effect of the transition ahead.

Consider a ‘representative’ interest-only borrower with a $400,000 30-year mortgage with a 5-year interest-only period. The left-hand side bar in Graph 6 shows the approximate interest payments (of 5 per cent) that such a borrower makes during the interest-only period. At the expiry of the interest-only period, required payments will increase by around 30–40 per cent (with an example shown in the bar on the right). (As shown in the graph, the interest rate applied to the loan is expected to be lower when it switches to P&I (by around 40 basis points) but this effect is more than offset by the principal repayments.)

Graph 6

The rise in scheduled payments amounts to about $7,000 per year for the representative interest-only borrower. This is a non-trivial sum for the household concerned.

But how big is this cash flow effect when summed up across all households currently holding interest-only loans? Again, I adopt the extreme assumption that all interest-only periods expire as scheduled over the coming few years. As a share of total household sector disposable income, the cash flow effect in this scenario is estimated be less than 0.2 per cent on average per annum over each of the next three years (Graph 7).

For the household sector as a whole, this upper-bound estimate of the effect is relatively modest. Even so, there are a number of reasons why the actual cash flow effect is likely to be even less than this. More importantly, the actual effect on household consumption is likely to be lower still. So let me step through the various reasons.

Graph 7

Savings

Many borrowers make provisions ahead of time for the rise in required repayments. It is common for borrowers to build up savings in the form of offset accounts, redraw balances or other assets. They can draw upon these to cover the increase in scheduled payments or reduce their debt. Others may not even need to draw down on existing savings. Instead, they can simply redirect their current flow of savings to cover the additional payments. In either case, such households are well placed to accommodate the extra required payments without needing to adjust their consumption very much, if at all.

As shown in the chart above, about half of owner-occupier loans have prepayment balances of more than 6 months of scheduled payments. While that leaves half with only modest balances, some of those borrowers have relatively new loans. They wouldn’t have had time to accumulate large prepayment balances nor are they likely to be close to the scheduled end of their interest-only period.

There are borrowers who have had an interest-only loan for some time but haven’t accumulated offset or redraw balances of substance. Offset and redraw balances are typically lower for investor loans compared with owner-occupier loans. That is consistent with investors’ incentives to maximise tax deductible interest. However, in comparison to households that only hold owner-occupier debt, there is evidence that investors tend to accumulate higher savings in the form of other assets (such as paying ahead of schedule on a loan for their own home, as well as accumulating equities, bank accounts and other financial instruments).

Refinancing

Another option for borrowers is to negotiate an extension to their interest-only period with their current lender or refinance their interest-only loan with a different lender. Similarly, they may be able to refinance into a new P&I loan with a longer loan term, thereby reducing required payments. Based on loans in the Securitisation Dataset, a large majority of borrowers would be eligible to alter their loans in at least one of these ways.

Any such refinancing will reduce the demands on a borrower’s cash flows for a time. However, it is worth noting that by further delaying regular principal repayments, eventually those repayments will be larger than otherwise.

Extra income or lower expenditures

What about borrowers who have not built up savings ahead of time or are unable to refinance their loans? The Securitisation Dataset suggests that such borrowers are in the minority. More importantly, most of them appear to be in a position to service the additional required payments. Indeed, the tightening of loan serviceability standards a few years ago was no doubt helpful in that regard.

Some fraction of interest-only borrowers may have used the reduced demands on their cash flows during the interest-only period to spend more than otherwise. However, the available data, and our liaison with the banks, suggest that there are only a small minority of borrowers who will need to reduce their expenditure to service their loans when their interest-only periods expire.

Sale of the property

Finally, some interest-only borrowers may have to consider selling their properties to repay their loans. Difficult as that may be – most notably for owner-occupiers – doing so could free up cash flow for other purposes. It would also allow them to extract any equity they have in the property. The extent of that can be gauged by estimating LVRs from the Securitisation Dataset. The LVRs of almost all of those interest-only loans (both owner-occupier and investor) are below 80 per cent (based on current valuations and including offset balances) (Graph 8). This reflects the combined effects of loan serviceability tests and the increase in housing prices over recent years.

Graph 8

Some risks remain

While the various estimates I’ve provided suggest that the aggregate effect of the transition ahead on household cash flows and consumption is likely to be small, some borrowers may experience genuine difficulties when their interest-only periods expire. The most vulnerable are likely to be owner-occupiers, with high LVRs, who might find it more difficult to refinance or resolve their situation by selling the property.

Currently, it appears that the share of borrowers who cannot afford the step-up in scheduled payments and are not eligible to alleviate their situation by refinancing is small. Our liaison with the banks suggests that there are a few borrowers needing assistance to manage the transition. Over the past year, some banks have reported that there has been a small deterioration in asset quality. For some borrowers this has tended to be only temporary as they take time to adjust their financial affairs to cope with the rise in scheduled payments. For a small share of borrowers, though, it reflects difficulty making these higher payments. That share could increase in the event that an adverse shock led to a deterioration in overall economic conditions.

Conclusion

Today, I have discussed some of the risks associated with interest-only loans, which imply that their value as a form of mortgage finance has limits. I have also presented rough estimates of the likely effect of the upcoming expiry of interest-only loan periods. The step-up in required payments at that time for some individual borrowers is non-trivial. For the household sector as a whole, however, the cash flow effect of the transition is likely to be moderate. The effect on household consumption is likely to be even less. This is because some interest-only borrowers will be willing and able to refinance their loans. Also, many others have built up a sufficient pool of savings, or will be able to redirect their current flow of savings to meet the payments, or have planned for, and will manage, this change in other ways.

Indeed, the substantial transition away from interest-only loans over the past year has been relatively smooth overall, and is likely to remain so. Nevertheless, it is something that we will continue to monitor closely.

Finally, the observation that the transition is proceeding smoothly is not an argument that the tightening in lending standards on interest-only loans was unwarranted; far from it. The tightening in standards starting in 2014 has helped to ensure that borrowers are generally well placed to service their loans. And the limit on new interest-only lending more recently has prompted a reduction in the use of those loans during a time of relatively robust growth of employment and still very low interest rates. In this way, it has helped to lessen the risk of a larger adjustment later on in what could be less favourable circumstances.

Given the range of issues already exposed by the Royal Commission into Financial Services Misconduct, including selling loans outside suitable criteria, fees from advice not given and other factors; we need to ask about the impact on the profitability of the banks and so share prices.

And all this is in the context of higher funding costs already hitting.

A number of international investors and hedge funds have placed shorts on the major banks, signalling an expectation of further falls in share price ahead, but the majors have already dropped by around 15% in the past year.

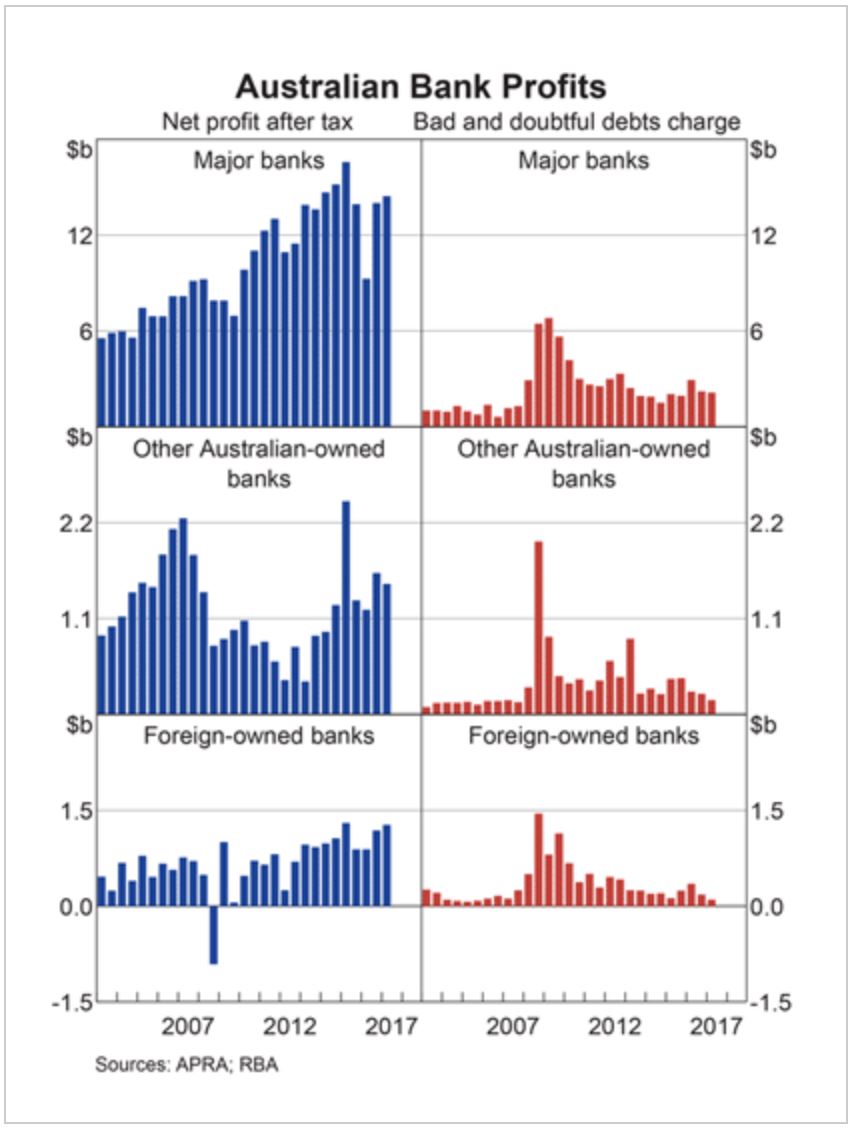

The recent RBA chart pack contained this picture on profitability. Bad and doubtful debts are very low, thanks to low interest rates. But that may change if rates were to rise, and “liar loans” are wide spread. There is no good data on the potential impact so far.

It is important to remember the Productive Commission recently called out that :

A quick survey of the banks from last year show that the return on equity – a measure of absolute profitability – or ROE range from 14.5% for CBA, 10.3% from NAB, 10.9% for ANZ and Westpac was 13.3% while AMP was 11.5%.

Looking overseas, US based Wells Fargo, which happens to be a key Warren Buffett holding, was 11.5% , the Bank of America earned less than 6.8% and Lloyds earns 4%. Barclays was -2.7%. In fact among western markets, only Canadian banks come close to our ROE’s – for example of Bank of Montreal was 11.3% but then they have the same structural issues that we do.

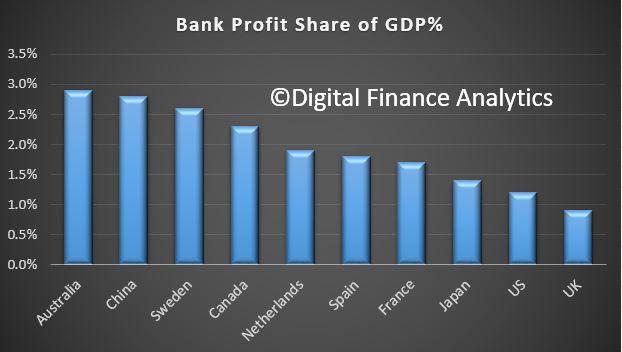

Data from news.com.au from 2016 shows the relative profit to GDP across several countries. Australia Wins.

That means 2.9 per cent of every $100 earned in Australia ends up as bank pre-tax profit, compared to the US and UK at $1.2 and 90 cents per cent respectively.

China is the highest after Australia at $2.80, Sweden $2.60 and Canada $2.30.

The Australia Institute also pointed to public money being used to secure the banking sector.

“Excessive profits provide a drag on the economy and hurt consumers who pay higher margins on bank products. The Reserve Bank found the big four banks enjoy an implicit government subsidy worth up to $4 billion dollars a year,”

The Royal Commission revelations have the potential to impact the market value of the banks as reflected in their share prices, and also raises questions about the financial stability of the entire system in Australia. APRA, in particular and the RBA have been (over?) focussed on financial stability, as the recent Productive Commission draft report highlighted.

Regulators have focused on a quest for financial stability prudential stability since the Global Financial Crisis, promoting the concept of an unquestionably strong financial system.

The institutional responsibility in the financial system for supporting competition is loosely shared across APRA, the RBA, ASIC and the ACCC. In a system where all are somewhat responsible, it is inevitable that (at important times) none are. Someone should.

The Council of Financial Regulators should be more transparent and publish minutes of their deliberations. Under the current regulatory architecture, promoting competition requires a serious rethink about how the RBA, APRA and ASIC consider competition and whether the Australian Competition and Consumer Commission (ACCC) is well-placed to do more than it currently can for competition in the financial system.

Over the next few days we will try to assess the potential impact ahead, from higher loss rates, lower fee income and potential fines and penalties. Then of course, there is the question, will these additional costs be passed on to investors and shareholders, or simply recovered from the current customer based by higher fees.

We expect banks to start making provisions for the revenue hits ahead. ANZ, for example, said their RC legal bill will be around $15 million. CBA made a $200 million expense provision for expected costs relating to currently known regulatory, compliance and remediation program costs, including the Financial Services Royal Commission.

To start the journey lets look at the relative performance of the banks’ share prices over the past year. Westpac share price is 16.8% lower compared with a year ago.

ANZ is down 16% over the same period

CBA has fallen 15.9% in the past 12 months.

and NAB’s share price dropped 14.2% over the same period.

In comparison, the ASX 200 is up 0.25% over the past year.

Among the regional banks, Bendigo Bank has fallen 16.6%

Bank Of Queensland has fallen 11.7% over the past year.

In contrast Suncorp is 0.74% higher

and Macquarie Group was up 19.5%. They of course have more than half their business offshore now.

Next time, we try to size the revenue hits ahead, and think about what that may mean for the banks and their customers.

An important post from Macrobusiness (MB) by the excellent Leith van Onselen which opens the can of worms which is the RBA’s Committed Liquidity Facility (a.k.a. Bank Safety Net or Unofficial Government Guarantee). Its all about the RBA’s version of QE!

He says:

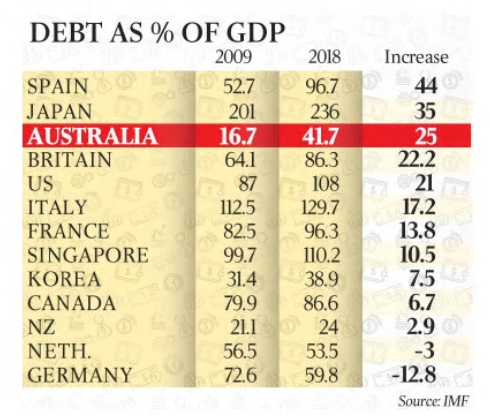

Figures from the International Monetary Fund (IMF) show that Australian government debt has risen faster than most other developed nations, increasing from 16.7% of GDP to an expected 41.7% this year – a jump of 25 percentage points. From The Australian:

The IMF report comes as Scott Morrison prepares to unveil next month’s budget, which will recycle improved company tax flows into personal income tax cuts while taking on more debt to finance infrastructure development. The Treasurer argues that the government is no longer borrowing to finance daily running costs but just to cover infrastructure and defence investments.

The mid-year budget update in December showed gross debt peaking at $591 billion in 2019-20, having hit $500bn in 2016-17. Gross debt stood at $319bn when the Coalition took office in 2013.

The IMF predicts this year will be the peak for Australian gross debt at 41.7 per cent of GDP, before a decline to 32.2 per cent over the next five years…

Although the IMF projects that Australia’s federal and state budgets will be back in surplus by 2020, it says there will be a continuing need to raise funds to roll over debts as they mature.

We think the projected return to surplus by 2020 is wishful thinking, given:

Commodity prices will likely fall, draining company profits, national income, and company tax revenue;

The housing downturn will dampen consumer spending, jobs and growth, draining company and personal income tax revenue; and

We are likely to see tax cuts offered from both sides in the upcoming federal election campaign.

Regardless, there is another important question that is rarely asked outside of MB: why is the Reserve Bank of Australia (RBA) persisting with the Committed Liquidity Facility (CLF) when there is now so much government debt on issue?

The CLF was established in late-2011 in order to meet the Basel III liquidity reforms. Below is the RBA’s explanation of the CLF [my emphasis]:

The facility, which is required because of the limited amount of government debt in Australia, is designed to ensure that participating authorised deposit-taking institutions (ADIs) have enough access to liquidity to respond to an acute stress scenario, as specified under the liquidity standard…

The CLF will enable participating ADIs to access a pre-specified amount of liquidity by entering into repurchase agreements of eligible securities outside the Reserve Bank’s normal market operations. To secure the Reserve Bank’s commitment, ADIs will be required to pay ongoing fees. The Reserve Bank’s commitment is contingent on the ADI having positive net worth in the opinion of the Bank, having consulted with APRA.

The facility will be at the discretion of the Reserve Bank. To be eligible for the facility, an ADI must first have received approval from APRA to meet part of its liquidity requirements through this facility. The facility can only be used to meet that part of the liquidity requirement agreed with APRA. APRA may also ask ADIs to confirm as much as 12 months in advance the extent to which they will be relying on a commitment from the Bank to meet their LCR requirement.

The Fee

In return for providing commitments under the CLF, the Bank will charge a fee of 15 basis points per annum, based on the size of the commitment. The fee will apply to both drawn and undrawn commitments and must be paid monthly in advance. The fee may be varied by the Bank at its sole discretion, provided it gives three months notice of any change…

Interest Rate

For the CLF, the Bank will purchase securities under repo at an interest rate set 25 basis points above the Board’s target for the cash rate, in line with the current arrangements for the overnight repo facility.

In light of the federal budget deficit projected to balloon out to nearly $600 billion, the question for the RBA is: shouldn’t the CLF be unwound and the banks instead be required to hold government bonds, as initially required under Basel III?

Bonds on issue are roughly triple that of when the CLF was first announced, so surely the RBA should amend the liquidity rules so that Australia’s ADIs are forced to purchase government bonds, so that the size of the CLF requirement decreases?

The most likely reason is because the RBA wants to keep open the option of bailing-out the banks. As noted by Deep T:

When there is capital flight due to official interest rate decreases, the RBA could and would step in and fund the banks’ funding shortfall from a loss of international investors using the Committed Liquidity Facility at rates below the banks’ international funding rates. The CLF used in these circumstances would be a form of quantitive easing and would have a dampening effect on mortgage rates by subsidising bank borrowing rates but could never be a lasting solution and only have limited effect in the long term. So yes, high cost international funding by the banks can easily be replaced by cheap RBA funding through a form of QE or money printing subsidising bank profits and banker bonuses.

The fact of the matter is the CLF represents another subsidy to the banks. The cost of the CLF is very low – i.e. 15bps pa – compared to the alternative. The CLF allows ADIs to originate mortgage assets and create RMBS rather than buying government bonds. The net spread on mortgage assets or RMBS compared to government bonds is much greater than 15bps pa, thus representing a significant direct subsidy to the banks.

MB reader, Jim, nicely dissected the lunacy of the CLF in a comment in 2016:

You’ve missed the real beauty of the CLF, and APS210

So the banks are forced to hold ‘as much as possible’ qualifying Tier 1 securities to meet their APS210 requirements. But… even with the large commonwealth government deficit, there still isn’t enough CGS to go round (CGS and TCorp bonds only qualify for Tier 1 securities under APS210).

Which is why the RBA invented the CLF. The CLF allows, no, it requires the banks to:

– hold their own securitised bonds on their balance sheet to qualify as ‘liquid assets’

– buy each other’s bonds to qualify as ‘liquid assets’

So, ANZ, CBA, NAB and WBC each have around $50bn of their own off balance sheet mortgages sitting back on their balance sheet to protect them against a ‘liquidity event’. Then they each have around $10bn each of each other’s bonds, so NAB holds around $50bn of WBC/ANZ/CBA bonds etc.

And if / when the liquidity shit hits the fan (e.g. foreigners stop buying the bank’s bonds), the banks can swap them into the RBA for a 15bps fee.

So the RBA will be forced to sit on about half a trillion dollars of Aussie bank paper ($100bn each plus a little more for CBA and WBC, plus Suncorp, Bendigo etc). Just think what THAT would do to your graph of yellow lines – more than double it in an instance.

So the CLF is not about government debt, its about bank debt, and how the RBA has bent over forward for the banks. Having worked in treasury at a Big 4, the CLF is the biggest joke under the sun – a guaranteed way to print money for the banks. This is why the fixed income desks at banks are always the best paying – those guys are paid to buy and hold bank bonds under APS210 requirements.

Do an investigation on how much REAL systemic debt is sitting in the banking system – the RBA has made itself lender of last resort to over $500bn worth of debt.

The bottom line is that with the stock of outstanding Commonwealth debt now so large (and still growing), the rationale for maintaining the CLF has evaporated. But don’t expect any action from the RBA, which wants to maintain the capability of bailing-out the banks via its own form of quantitative easing.

The Reserve Bank hosted a roundtable discussion on small business finance today, along with the Australian Banking Association and the Council of Small Business Australia. The roundtable was chaired by Philip Lowe, Governor of the Reserve Bank.

Small businesses are very important for the economy. They generate significant employment growth, drive innovation and boost competition in markets. Access to external finance is an important issue for many small businesses, particularly when they are looking to expand.

Our own SME survey highlights the problems SME’s face in getting finance in the face of the banks focus on mortgage lending. The latest edition of our report reveals that more than half of small business owners are not getting the financial assistance they require from lenders in Australia to grow their businesses.

The aim of the roundtable was to provide a forum for the discussion of small business lending in Australia. The participants included entrepreneurs from the Reserve Bank’s Small Business Finance Advisory Panel along with representatives from financial institutions, government and the financial regulators.

The challenges faced by small businesses when borrowing were discussed. The entrepreneurs highlighted a number of issues, including:

access to lending for start-ups

the heavy reliance on secured lending and the role of housing collateral and personal guarantees in lending

the loan application process, including the administrative burden

the ability to compare products across lenders and to switch lenders.

The participants discussed a range of ideas for addressing these challenges. Financial institutions shared their perspectives and discussed some of the steps that are being taken to address concerns of small business. The roundtable heard some suggestions about how to improve the accessibility of information for small businesses about their financing options. The roundtable also heard from the Australian Prudential Regulation Authority regarding the proposed revisions to the bank capital framework that relate to small business lending.

The roundtable discussed some other policy initiatives that are currently underway, including the introduction of comprehensive credit reporting and open banking. Participants agreed that these initiatives could help to improve access to finance, and the Reserve Bank will continue to monitor developments closely.

Background

The Small Business Finance Advisory Panel was established by the Reserve Bank in 1993 and meets annually to discuss issues relating to the provision of finance, as well as the broader economic environment for small businesses. The panel provides valuable information to the Reserve Bank on the financial and economic conditions faced by small businesses in Australia.

The Reserve Bank has previously hosted discussions on small business finance issues, including a Small Business Finance Roundtable in 2012 and a Conference on Small Business Conditions and Finance in 2015.

The Australian Banking Association, along with the Australian Council of Small business, representatives for member Banks and other stakeholders were also in attendance to bring their own perspective on the issues and to answer questions. The event was agreed to and organised at the end of last year.

Australian Banking Association CEO Anna Bligh said that the Roundtable was an important opportunity for Australia’s banks to listen first hand to the needs of small business.

“Small business is the engine room of the Australian economy, accounting for more than 40% of all jobs or around 4.7 million people,” Ms Bligh said.

“This Roundtable was an important step in building the relationship between banks, small businesses and their representatives.

“Banks are working hard to better understand the needs of business, their challenges and how they can work with them to help them achieve their goals,” she said.

There are a number of open issues worth considering. Most obvious is the question of the link between inflation targetting and financial stability. Would price level targetting offer a better alternative? Some argue this delivers predictability of the price level over a long horizon. Then there are questions about the correct level to target. More broadly, is it still relevant?

And in addition we would ask, as inflation targetting relies on the CPI dataset, are these telling the full story, or not?

It has been 25 years since Australia adopted an inflation-targeting regime as the framework for monetary policy. At the time of adoption, inflation targeting was in its infancy. New Zealand had announced its inflation target in 1989, followed by Canada and Sweden. The inflation-targeting framework was untested and there was little in the way of academic analysis to provide guidance about the general design and operational principles. Practice was very much ahead of theory.

Now 25 years later, inflation targeting is widely used as the framework for monetary policy. While there are differences in some of the features across countries, the similarities are more pervasive than the differences. And generally, the features of inflation-targeting frameworks have tended to converge over time.

It is interesting to firstly examine how the inflation-targeting framework in Australia has evolved over the 25 years. Secondly, it is also timely to reassess the appropriateness of the regime.

Open Issues

I have argued that the inflation target has delivered macroeconomic outcomes that have been beneficial for the Australian economy. I think a strong case can be made that it has contributed materially to better economic outcomes than the monetary frameworks that preceded it. I have also noted that the framework in Australia has not changed much over the 25 years of its operation, with the notable exception of communication.

So does that mean that the current configuration of the inflation target is the most appropriate or that even that is the most appropriate framework for monetary policy? What changes could be contemplated? Those questions are going to be addressed in other papers at this conference. But let me raise some here and discuss issues worth considering around each of them.

The first is the role of financial stability in an inflation-targeting framework. The Reserve Bank research conference last year considered this issue at some length. As I said earlier, financial stability is now articulated in the Statement on the Conduct of Monetary Policy. I talked about this issue at the Bank of England last year and Ben Broadbent is addressing it at this conference. One question that arises is how the financial stability goal interacts with the inflation target. Is it a separate goal that sets up potential trade-offs or is it aligned with the inflation-targeting goal? In the latter case, a potential reconciliation is the time horizon. When it materialises, financial instability is likely to be detrimental to inflation and unemployment/output: the global recession of 2008 and the subsequent slow recovery in a number of economies bears testament to the potential costs of financial instability (although here in Australia we didn’t experience this to as great an extent). So over some time horizon, potentially quite long, the inflation target and financial stability are aligned. But translating this into monetary policy implications over a shorter time horizon is a large challenge, which still seems to me to be far from resolved.

What about alternative regimes? Price level targeting is one that has been considered in some countries, including Canada, and has been proposed in the academic literature. One argument for a price level target is that it delivers predictability of the price level over a long horizon. It is not clear to me that this is something that is much valued by society. By revealed preference, the absence of long-term indexed contracts suggests that the benefits are not perceived to be high. I struggle to think of what contracts require such a degree of certainty. To me the benefits mostly derive from having inflation at a sufficiently low level that it doesn’t affect decisions. That supports an inflation target rather than a price level target. One important difference is that an inflation target allows bygones to be bygones, whereas a price level target does not. In a world where there are costs to disinflation (and particularly deflation), the likely small gains from the full predictability of the price level that comes with a price level target are not likely to offset the costs of occasional disinflations following positive price level shocks. Another challenge is how fast the price level should be returned to its target level. This presents both a communication and operational challenge as the speed is likely to vary with the size of the deviation.

While the argument at the moment is that a price level target allows the central bank to let the economy grow more strongly after a period of unexpectedly low inflation, again I do not think that practically this will deliver better outcomes than a flexible inflation target. That is an empirical question in the end which is worth testing.

The appropriate level of the inflation target is currently being debated in some parts of the world, including the US. The argument for a higher target rate of inflation is that it might reduce the risk of hitting the zero lower bound because a higher inflation rate would result in a higher nominal interest rate structure. In thinking about this, we should ask the question as to whether what we have seen is the realisation of a tail event in the historical distribution of interest rates (for a given level of the real interest rate).? While this event has now lasted quite a long time, if you thought it was a tail event, then you would expect the nominal rate structure to revert back to its historical mean at some point. If it is a tail event, and the world has just been unlucky enough to have experienced a realisation of that tail event, then there would not obviously be a need to raise the inflation target. We also need to question whether the real interest rate structure has shifted lower permanently, because of permanently lower trend growth say, which would also shift down the nominal rate structure and increase the likelihood of hitting the zero lower bound.

Also, as with price level targeting, in thinking about this question, it needs to be taken into account that it is highly beneficial to have the inflation target at a level where it doesn’t materially enter into economic decision-making. Two to three per cent seems to achieve that. We know that some number higher than a 2–3 per cent rate of inflation will materially enter decision-making, because we have had plenty of experience of higher rates of inflation that demonstrates that. How much higher though, we don’t really exactly know.

Another consideration in answering the question of whether the inflation target is at the right level is the range of policy instruments in the tool kit. Over the past decade, this tool kit has expanded in a number of central banks. For example, we now know that the zero lower bound is not at zero. Asset purchases have been utilised and these have included sovereign paper but also assets issued by the private sector. An assessment of the effectiveness of these instruments is still a work in progress. We also need to think about whether they are part of the standard monetary policy tool kit or whether they should only be broken out in case of emergency.

Nominal income targeting is another alternative regime to inflation targeting. I am not convinced that flexible inflation targeting of the sort practiced in Australia is significantly different from nominal income targeting in most states of the world. I also think that there are some quite significant communication challenges with nominal income targeting. Firstly, nominal income is probably more difficult to explain to people than inflation. Secondly, as a very practical matter, nominal income is subject to quite substantial revisions, which poses difficulties both operationally and again in communicating with the public.

Finally, one criticism of inflation targeting more generally is that central banks are fighting the last war. The fact that for a number of years now, inflation globally has been stubbornly low is not obviously the signal to declare victory over inflation and move on. Indeed, the declaration of victory may well be the signal that hostilities are about to resume and that inflation will shift up again. Moreover, even if victory can be declared that doesn’t mean you should go off to fight another war in another place without securing the peace. Inflation targeting can help secure the peace.

By 2020, GDP could be somewhere between 1 and 5.5% – that should about cover it!

By 2020, GDP could be somewhere between 1 and 5.5% – that should about cover it! They highlight that these developments have had a notable knock-on effect on Australian money markets. “In part, this is because Australian banks raise a portion of their funding in US markets to finance their domestic assets. So they have responded to higher US rates by seeking to borrow more in domestic markets, which has place upward pressure on rates in Australia. Similar effects, although less pronounced, can be seen on rates

They highlight that these developments have had a notable knock-on effect on Australian money markets. “In part, this is because Australian banks raise a portion of their funding in US markets to finance their domestic assets. So they have responded to higher US rates by seeking to borrow more in domestic markets, which has place upward pressure on rates in Australia. Similar effects, although less pronounced, can be seen on rates “Higher bank bill swap (BBSW) rates affect bank funding costs in a number of ways. First, BBSW rates flow through to the rates banks pay on their new short- and long-term wholesale debt. In addition to this effect, bank bond

“Higher bank bill swap (BBSW) rates affect bank funding costs in a number of ways. First, BBSW rates flow through to the rates banks pay on their new short- and long-term wholesale debt. In addition to this effect, bank bond They suggest that “revisions” to the household consumption series shows a higher level of spend than previously thought. “Household consumption grew strongly in the December quarter and revisions to previous data

They suggest that “revisions” to the household consumption series shows a higher level of spend than previously thought. “Household consumption grew strongly in the December quarter and revisions to previous data “Household consumption grew at a faster rate than household disposable income over 2017; the household saving ratio is reported to have declined, although it stabilised towards the end of the year as income growth picked up (Graph 2.10). Growth in real household disposable income was below average over 2017 at 1.7 per cent, largely because of low wages growth. The prospect of continued low growth in household income remains a key risk to the outlook for household consumption, especially given high levels of household debt. Slower growth in household net wealth, particularly in an environment of below-average income growth, adds to uncertainty about the outlook for consumption”.

“Household consumption grew at a faster rate than household disposable income over 2017; the household saving ratio is reported to have declined, although it stabilised towards the end of the year as income growth picked up (Graph 2.10). Growth in real household disposable income was below average over 2017 at 1.7 per cent, largely because of low wages growth. The prospect of continued low growth in household income remains a key risk to the outlook for household consumption, especially given high levels of household debt. Slower growth in household net wealth, particularly in an environment of below-average income growth, adds to uncertainty about the outlook for consumption”. “New dwelling construction declined by 5 per cent over 2017. This follows a few years in which new dwelling construction increased to high levels, supported by low interest rates, strong population growth and higher

“New dwelling construction declined by 5 per cent over 2017. This follows a few years in which new dwelling construction increased to high levels, supported by low interest rates, strong population growth and higher Turning to mortgage rates, they confirm that new loans tend to be at lower variable rates than the average for outstanding loans. Moreover, new IO borrowers continue to pay a premium above the interest rate on new principal-and-interest (P&I) home loans.

Turning to mortgage rates, they confirm that new loans tend to be at lower variable rates than the average for outstanding loans. Moreover, new IO borrowers continue to pay a premium above the interest rate on new principal-and-interest (P&I) home loans.

“The value of housing loan approvals (excluding refinancing) has continued to decline over recent months, to be 8 per cent below the recent peak in August 2017. This has been driven by investors, with owner-occupier approvals remaining relatively steady since mid 2017 (Graph 3.12). The decline in investor approvals has been primarily concentrated in New South Wales”.