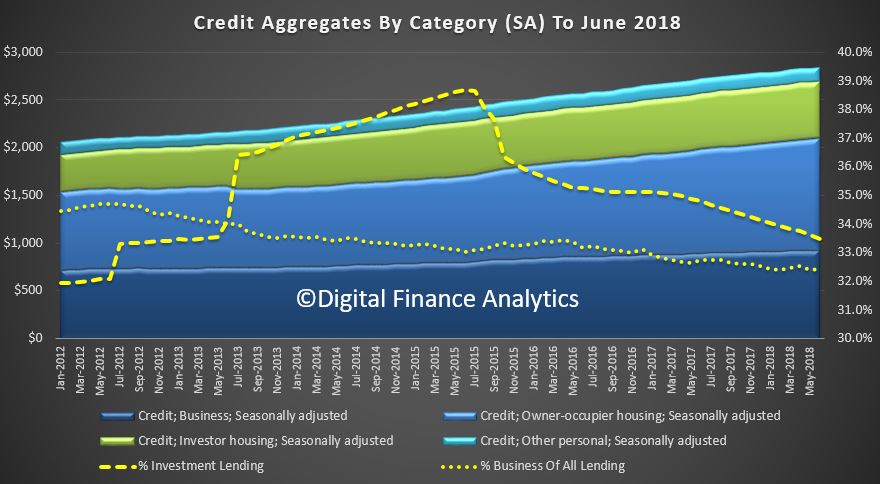

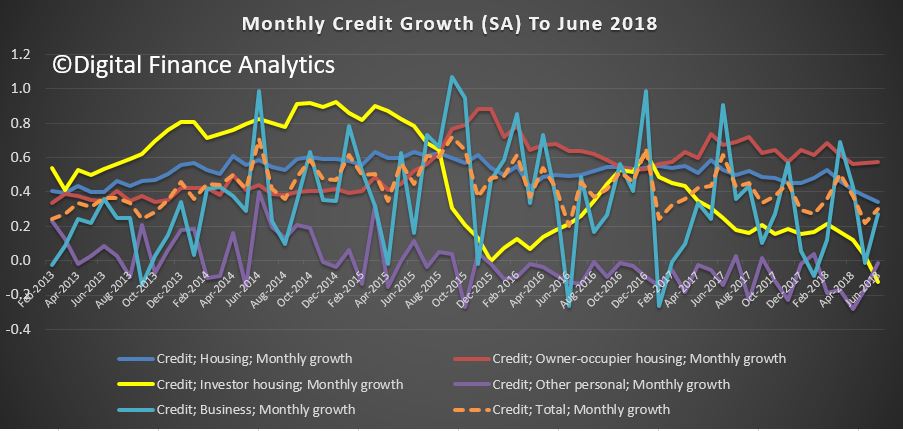

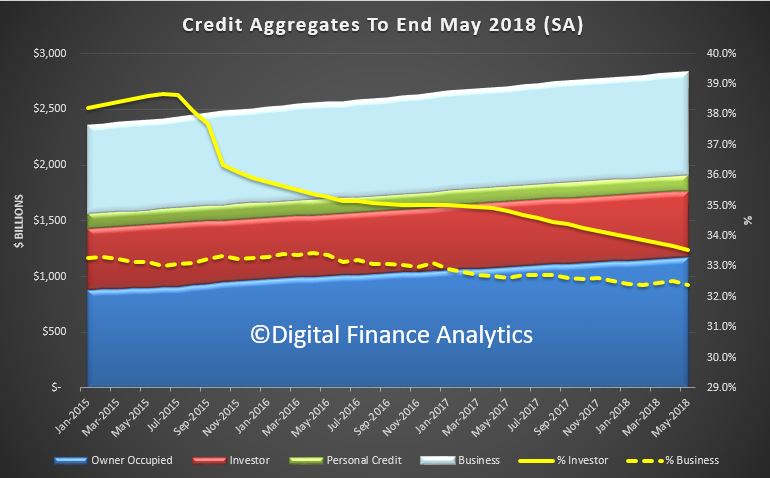

The RBA released their credit aggregates to June 2018 today. Overall credit grew 0.3% in the month to $2.84 trillion, up $9.7 billion. to a new record.

Within that, owner occupied housing lending rose 0.6% or $6.6 billion to $1.18 trillion, while investment lending fell $800 million, down 0.1% in seasonally adjusted terms, or rose $1 billion, up 0.2% in original terms. (I have no idea what adjustments the RBA makes, its not disclosed!).

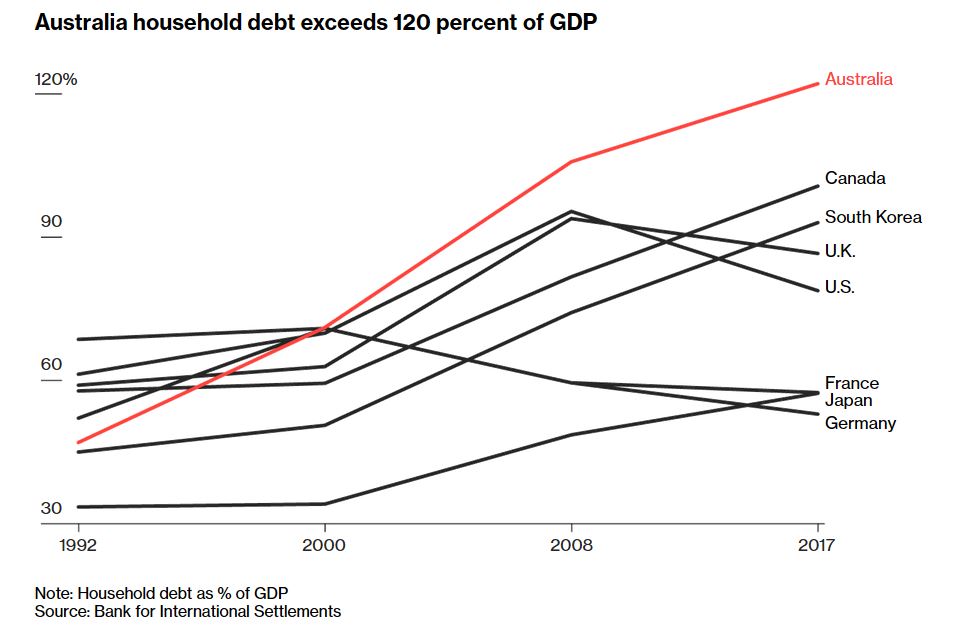

Investment lending fell to 33.5% of the portfolio. Total lending for housing is a new record $1.77 trillion, and remember this is at a time when housing debt to income is knocking on the 200 door, and we are one of the most in debt nations on the planet. Least we forget, loans need to be repaid, eventually!

Business lending in seasonal terms rose 0.4%, up $4.1 billion to $921 billion, and fell to 32.2% of all lending – we see a continued fall in the proportion of lending to business, as opposed for housing, which is not good.

Personal credit rose $600 million, up 0.4% in original terms or fell $300 million in seasonally adjusted terms down 0.2%.

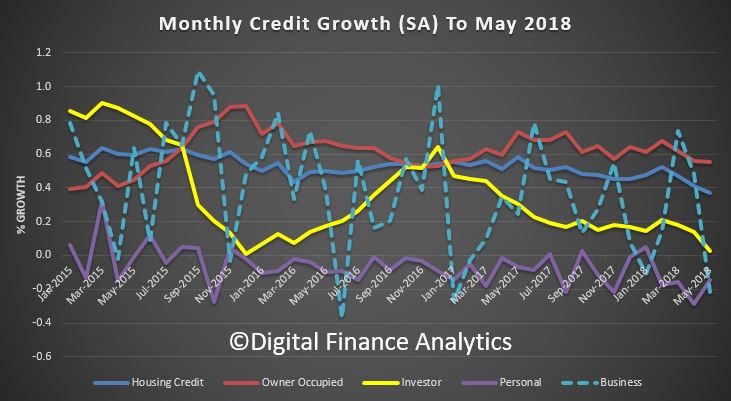

The monthly seasonally adjusted numbers highlight the slide in investor lending, and the stronger owner occupied lending.

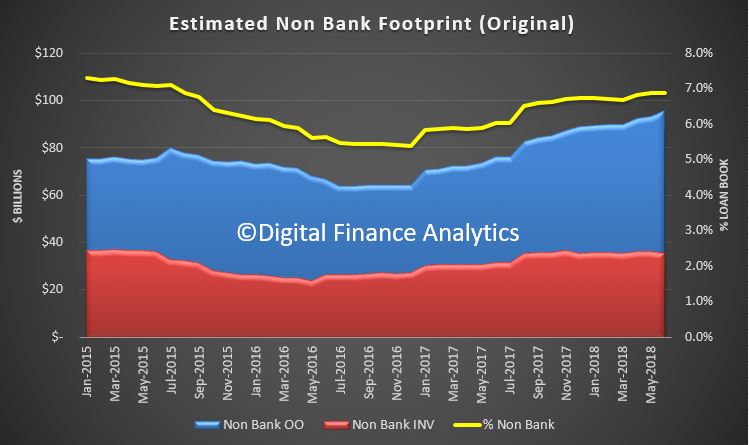

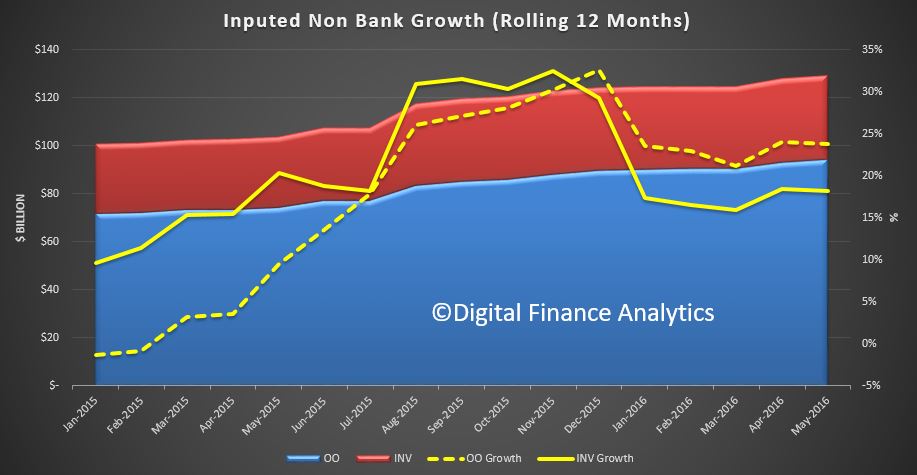

Finally, we also estimate the growth in on-bank lending, by taking the original RBA data, and comparing this with the ADI data from APRA also out today.

In essence, the relative share of home lending going to the non-banks is rising, to around 7% of all loans, and the bulk of the loans being written are for owner occupied borrowers.

A caveat here, as the non-bank segment of the data will always be a bit off, because there is less timely data captured from this small, but growing part of the market. Something which APRA needs to address.

So more of the old same old, same old, housing lending still growing way above inflation and wages, forcing housing debt higher, at the expense of business investment.

We have not fundamentally addressed the credit elephant in the room. Despite all the noise.

Perhaps the regulators would like to tell us, how much debt is too much? We clearly have not hit their pain threshold yet, despite the rising financial stress in many households.

When we released our mortgage stress report for June 2018, we said that the number of households exposed to risks is rising, and if rates were to increase then around 1 million of households will fall into stress and some may default, up from 970,000 now.

Members held a detailed discussion of the high level of household debt in Australia, informed by a special paper prepared for this meeting. Household debt has increased by more than household income over the preceding three decades in many countries, but particularly so in Australia. Two key drivers of this trend across countries have been the decline in nominal interest rates, predominantly reflecting lower inflation, and financial deregulation, both of which have increased households’ access to finance. Members noted that a distinguishing feature of the Australian housing market is that the bulk of dwellings are owned by the household sector. This has contributed to greater borrowing for housing by households in Australia compared with other countries, where the corporate sector owns a larger proportion of rental properties. Another feature of the Australian housing market that has contributed to greater borrowing by households is the higher cost of housing in Australia on account of a larger share of the Australian population living in urban centres, typically in large detached dwellings.

Survey data indicate that much of Australian household debt is owed by higher-income and middle-aged people, who tend to have more stable employment and often larger savings buffers. However, members recognised that a material share of household debt is held by lower-income households, which generally have higher debt relative to their income. Household assets in aggregate are valued at around five times the value of household debt and total assets exceed the value of debt for most households. Members noted, however, that most household assets are housing and superannuation, and that both of these are illiquid.

Members noted that high levels of household debt could affect economic outcomes. For example, households with high debt levels are more vulnerable to economic shocks and therefore more likely to reduce consumption in the face of uncertainty about their future income. Members also noted that changes in interest rates have a larger effect on disposable income for households with high debt levels, but that these households may be less inclined to borrow more at times when interest rates fall. Accordingly, members agreed that household balance sheets continued to warrant close and careful monitoring.

In fact our research says, yes, debt is a problem, and it is hitting many different types of household, including more affluent ones.

Our analysis of stress and defaults created a stir in the media, several radio and TV interviews, and some interesting discussions on social media.

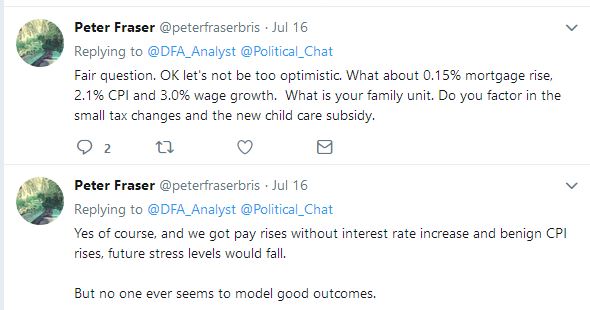

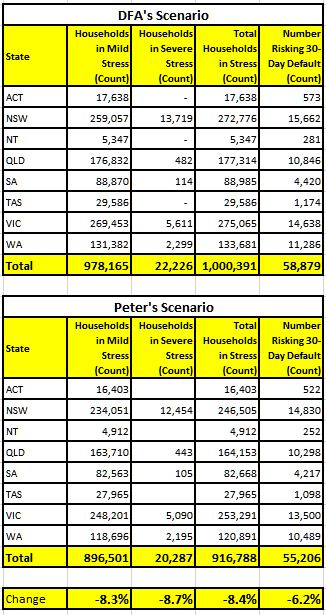

One of these, with Peter on Twitter led to a question about how we make our assessment and scenarios and our definitions of mortgage stress (cash-flow based). We include estimates of expected wages growth, inflation, cpi, interest rates etc.

So this led to a discussion where I volunteered to run a scenario using Peter’s parameters.

We also added in the tax changes and child care subsidy (in both scenarios). We do not impose a particular family structure, but capture that in our surveys (which aligns to the ABS census distribution).

So, we ran our model with a 3% wage growth, 2.1% CPI and small rise in mortgage rates. Stress levels would begin to fall, but will still be higher than since 2000, because of the greater leverage and debt burden.

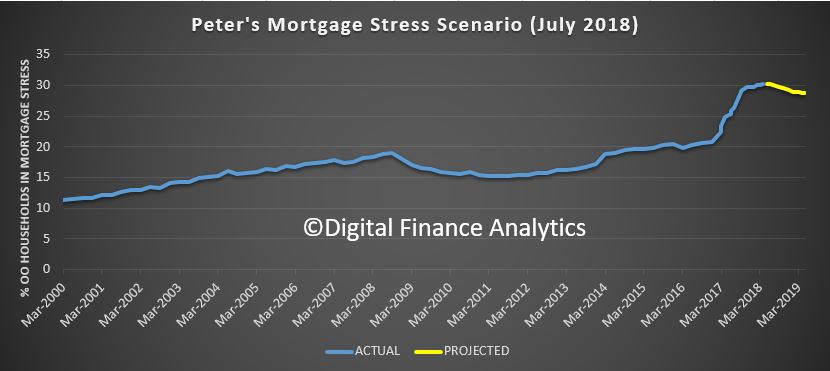

Here are the results, one year down the track.

So the impact of potential wages rises, in real terms is significant. A “good outcome!” However even then the risk in the system remains higher than we have been use to. Defaults reduced by 6% while stress fell by more than 8%.

Dwelling investment has gone from making a positive contribution to growth two years ago to being roughly flat over the year to March. In terms of our forecasts, dwelling investment is not expected to contribute much to growth over the next couple of years, but is expected to remain at a high level.

To understand the outlook, it is helpful to recognise that there isn’t a single national housing market. At the state level, there have been some similarities in the evolution of dwelling investment, but there have also been distinct differences (Graph 5).

Graph 5

One point of similarity is that the construction of higher-density apartments has been much more important than in the past, especially in the east-coast capitals. We have used our liaison program quite extensively to understand how to adapt our forecasting processes to take into account that the time taken for a building approval to progress to construction and the period of construction is longer and more variable for high-density projects than for detached dwellings. The liaison program, which includes organisations such as the UDIA and its members, has also allowed us to gain deeper insights into specific local factors, such as differences in planning rules and the emergence of capacity constraints in the housing construction sector.

One point of difference across states has been the timing of dwelling investment cycles. For New South Wales and Victoria, the level of dwelling investment has been broadly stable at a high level since 2016. In contrast there has been a decline in higher-density construction in Queensland since early 2017. In Western Australia, residential construction peaked in mid 2015, which was well after the end of the mining boom. These differences highlight the fact that there are different demand and supply forces at work across the states. Given time constraints, I am going to focus my attention on the demand side of the market.

An important driver of housing demand over the long run is the rate at which new households are being formed. This depends on population growth and changes in the average number of people who are living in each household. Household size declined steadily in Australia between 1960 and 2000 before levelling out, alongside declines in marriage and fertility rates and population aging. The natural increase in the Australian population has also declined over time due to demographic factors. In particular, lower fertility rates have offset increased life expectancy (Graph 6). Having said that, the rate of natural increase in Australia’s population remains higher than in most other advanced economies.

Graph 6

Immigration has also been a feature of the population growth story and it has certainly been the dominant influence on the swings in population growth over the past decade. The largest single category of net overseas migration has been people on temporary student visas (Graph 7). Prior to the financial crisis, a large share of these students were coming to Australia for vocational training courses. Following changes to visa requirements, student visa numbers initially dropped, but have picked up again in recent years, mostly due to an increase in students attending university. To put this into perspective, education now accounts for around 10 per cent of Australia’s total exports, which is in the same ball park as our rural exports. From the perspective of demand for housing, the important point is that most of these students have gone to Sydney and Melbourne.

Graph 7

Another interesting category is skilled workers. The net inflow of people on skill visas increased in response to demand for workers during the mining boom. Most of these workers went to Western Australia and Queensland. At the same time, net migration to Western Australia and Queensland from other states and New Zealand also increased. As the mining sector transitioned from the construction to the production phase of the mining boom, the demand for labour fell. The number of people on skilled visas fell and the inflow of people from New Zealand and other Australian states turned to an outflow.

As a consequence, there have been quite large differences in population growth at the state level, which have had direct effects on the demand for housing (Graph 8). Population growth is expected to remain strong, particularly in Victoria and New South Wales, and the net overseas migration component of this is expected to be driven by people on student visas.

Graph 8

On the supply side, the pipeline of residential construction that has been approved, but not completed remains high in New South Wales and Victoria (Graph 9). There is also a reasonable pipeline of work in Queensland, although it has already started to decline. Based on recent approvals data and expected demand conditions, this suggests that dwelling investment in New South Wales and Victoria will remain at a high level for a number of years. Liaison contacts have suggested to us that capacity constraints in the construction industry, particularly in New South Wales, will make it difficult for construction activity to increase.

Graph 9

Of course household formation and population growth are not the only drivers of housing demand. For example, interest rates and changes in lending standards can also influence how much households are willing and able to spend on housing. Another way to gauge the current balance of housing supply and demand is to look at housing price growth.

Over the past five years, housing price growth has been subdued in Brisbane and Perth (Graph 10). This is consistent with the fall in population growth coinciding with an increase in the supply of housing. In contrast, housing price growth has been strong until recently in Sydney and Melbourne, where population growth has been strong. Given that housing accounts for around 55 per cent of total household assets, we are paying close attention to these developments.

Graph 10

The Housing Market in the Illawarra Region

From a demand perspective, the Illawarra region has experienced a pick-up in population growth. Some of this has come from overseas students attending the University of Wollongong, and some has come from people migrating to the Illawarra region from Sydney. Although the Illawarra region is a little older, on average, than the rest of Australia and Sydney, it still has a large working-age population (Graph 11).

Graph 11

This is partly because its geographic proximity and transport infrastructure allow people living in Wollongong and the Illawarra region to commute to Sydney. Around 20 per cent of Wollongong workers commute at least 50 kilometres to work (Graph 12). This is one of the highest rates in the state. Unsurprisingly, five of the seven areas with higher shares of people commuting more than 50 kilometres are also within commuting distance of Sydney. Illawarra residents are also well placed to benefit from the fact that some of the fastest growing areas of Sydney are in south and south-west, including the proposed “aerotropolis” around the new airport at Badgery’s Creek. Access to these growth areas will be enhanced if some of the recently announced transport infrastructure plans are realised.

Graph 12

Although people from the Illawarra region can and do commute to Sydney, labour market conditions in the Illawarra region itself have also been strong recently (Graph 13). In combination, these factors mean that there has been strong employment growth for those living in the Illawarra region over the past five years and the unemployment rate is close to the average for New South Wales, which is, in turn, lower than the Australian unemployment rate.

Graph 13

Strong population growth and the economic prosperity associated with strong labour market outcomes have led to higher housing prices in the Illawarra region (Graph 14). Just as in Sydney, developers have responded to the higher prices, and dwelling investment in the region has increased. Also similarly to Sydney, there has been a debate about whether the infrastructure has been growing fast enough to accommodate the needs of an expanding population and the increase in construction that goes with that.

Graph 14

Conclusion

In summary, over the past couple of years, non-mining business investment has become a more important driver of growth in the Australian economy. This is a good thing because investment of this kind is necessary to ensure future productivity growth, which is ultimately what contributes to the economic prosperity and welfare of the Australian people. Infrastructure investment has been a part of this story.

At the same time, dwelling investment growth has eased off. Although dwelling investment is still expected to remain at a high level, particularly in New South Wales and Victoria, it is not likely to contribute much to growth over the next couple of years. Demand for housing remains strong because population growth is expected to stay strong. However, the housing story is different across states and across regions within states, partly because population trends differ. The effects of the mining investment cycle on population trends and housing markets in Western Australia is a clear-cut illustration of this point.

The data show that population trends and housing market developments in the Illawarra region are closely linked to those in Sydney, partly because the transport infrastructure allows people to live in the Illawarra region and commute to Sydney. Future transport infrastructure plans and the development associated with the Badgery’s Creek airport are likely to strengthen these ties. As always, the key to effective urban development is high-quality, transparent cost-benefit analysis of potential infrastructure projects informed by local knowledge. The UDIA has an important role to play here. The UDIA and its members, in Wollongong and elsewhere, also have an important role to play in macroeconomic policy by informing the Bank’s understanding of the factors at play in different housing markets through our liaison program.

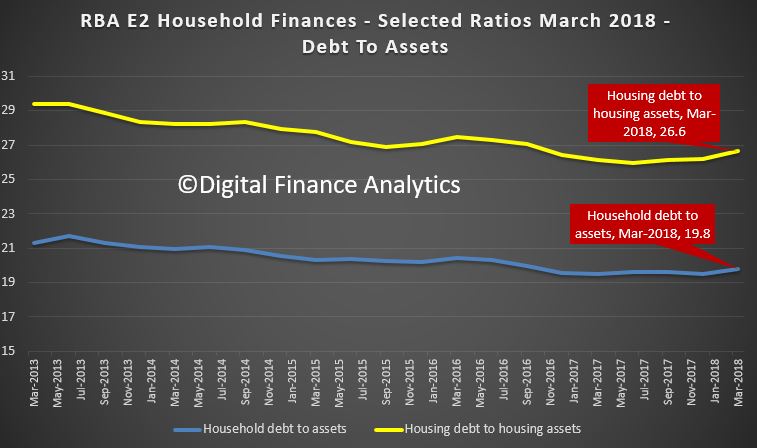

The RBA updated their E2 Household Finances – Selected Ratios to end March, released at the end of June. So they are yet to reflect the latest downturn in home prices and rising debt. But the trajectory is clear and should be ringing alarm bells.

First the ratio of household debt to housing assets and total assets is going up, reflecting mainly falls in property prices. The rate is accelerating, confirming that while debt is still rising, values are not. Expect more ahead.

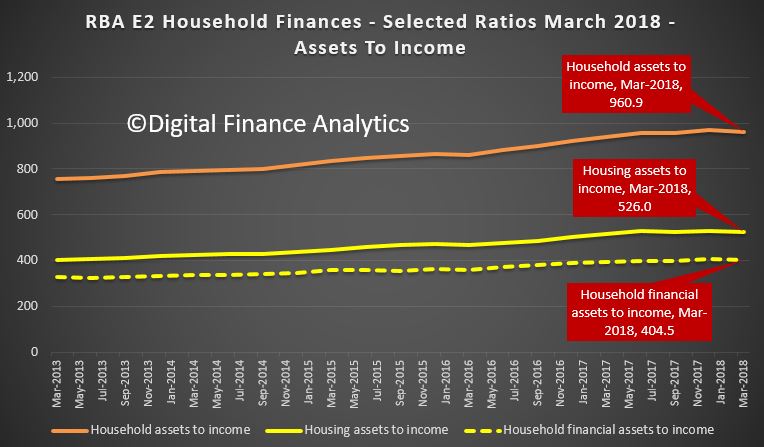

The ratios of assets to income are falling, having been rising for year, again reflecting falls in home prices. So while incomes are flat in real terms, asset values are falling faster.

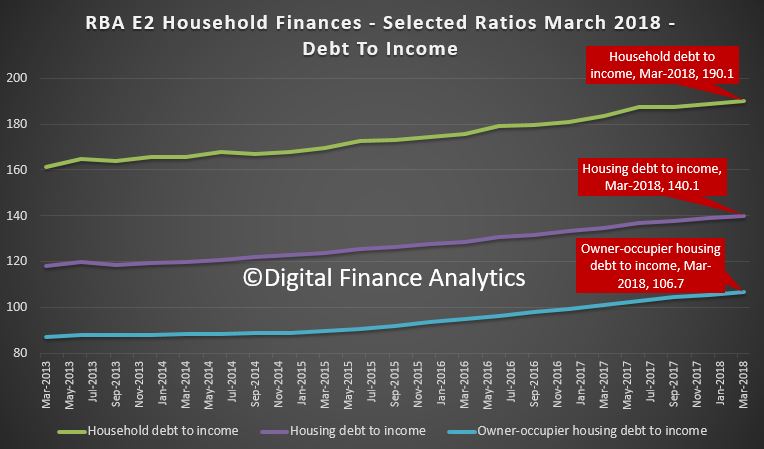

And finally, the killer, the household debt to income ratios continues higher, this despite the greater focus on lending quality, and reduced “mortgage power”. The household debt to income ratio is now at 190.1, the housing debt in income 140.1, and the owner occupied housing debt to income is 106.7. In fact this is moving up more sharply as lenders have focused on owner occupied lending.

Combined this shows the problems in the household sector. No surprise then that mortgage stress is going higher. We release the June data tomorrow.

Remember that the debt to GDP ratio is highest in Australia compared with other countries.

The RBA has released their monthly decision and no surprise, we remain at 1.5%. The tenor of the announcement, to me at least sounded less bullish, and I am sure the economists will the parsing the sentences for clues as to their next move. No hint of the next move being up!

To me it is simple, they would like to lift rates to more normal levels, but cannot thanks to high debt, and downside risks. They are stuck. I believe the next move will be down as the economy weakens (dragged down by the fading property market, rising interest rates internationally, and concerns about China’ economic dynamo). But not yet.

At its meeting today, the Board decided to leave the cash rate unchanged at 1.50 per cent.

The global economic expansion is continuing. A number of advanced economies are growing at an above-trend rate and unemployment rates are low. The Chinese economy continues to grow solidly, with the authorities paying increased attention to the risks in the financial sector and the sustainability of growth. Globally, inflation remains low, although it has increased in some economies and further increases are expected given the tight labour markets. One uncertainty regarding the global outlook stems from the direction of international trade policy in the United States. There have also been strains in a few emerging market economies, largely for country-specific reasons.

Financial conditions remain expansionary, although they are gradually becoming less so in some countries. There has been a broad-based appreciation of the US dollar. In Australia, short-term wholesale interest rates have increased over recent months. This is partly due to developments in the United States, but there are other factors at work as well. It remains to be seen the extent to which these factors persist.

The recent data on the Australian economy continue to be consistent with the Bank’s central forecast for GDP growth to average a bit above 3 per cent in 2018 and 2019. GDP grew strongly in the March quarter, with the economy expanding by 3.1 per cent over the year. Business conditions are positive and non-mining business investment is continuing to increase. Higher levels of public infrastructure investment are also supporting the economy. One continuing source of uncertainty is the outlook for household consumption. Household income has been growing slowly and debt levels are high.

Higher commodity prices have provided a boost to national income recently. Australia’s terms of trade are, however, expected to decline over the next few years, but remain at a relatively high level. The Australian dollar has depreciated a little, but remains within the range that it has been in over the past two years.

The outlook for the labour market remains positive. Strong growth in employment has been accompanied by a significant rise in labour force participation. The vacancy rate is high and other forward-looking indicators continue to point to solid growth in employment. A gradual decline in the unemployment rate is expected, after being steady at around 5½ per cent for much of the past year. Wages growth remains low. This is likely to continue for a while yet, although the stronger economy should see some lift in wages growth over time. Consistent with this, the rate of wages growth appears to have troughed and there are increasing reports of skills shortages in some areas.

Inflation is low and is likely to remain so for some time, reflecting low growth in labour costs and strong competition in retailing. A gradual pick-up in inflation is, however, expected as the economy strengthens. The central forecast is for CPI inflation to be a bit above 2 per cent in 2018.

Nationwide measures of housing prices are little changed over the past six months. Conditions in the Sydney and Melbourne housing markets have eased, with prices declining in both markets. Housing credit growth has declined, with investor demand having slowed noticeably. Lending standards are tighter than they were a few years ago, with APRA’s supervisory measures helping to contain the build-up of risk in household balance sheets. Some further tightening of lending standards by banks is possible, although the average mortgage interest rate on outstanding loans has been declining for some time.

The low level of interest rates is continuing to support the Australian economy. Further progress in reducing unemployment and having inflation return to target is expected, although this progress is likely to be gradual. Taking account of the available information, the Board judged that holding the stance of monetary policy unchanged at this meeting would be consistent with sustainable growth in the economy and achieving the inflation target over time.

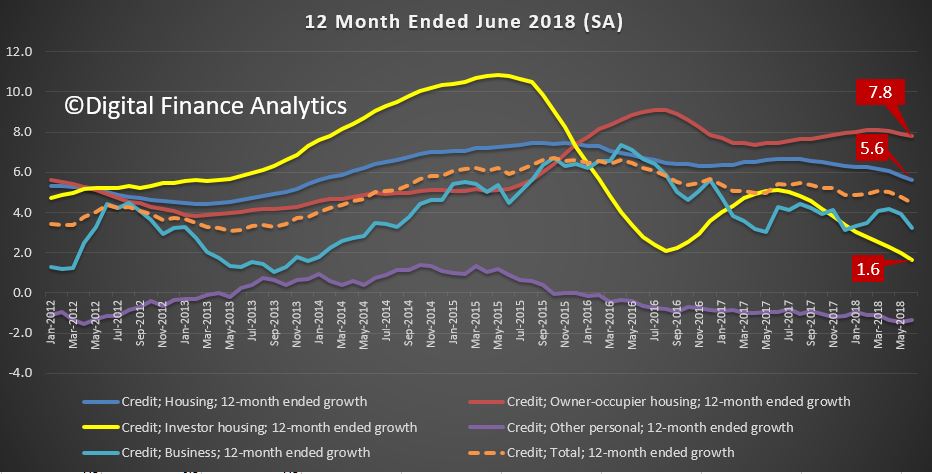

The RBA data shows that total housing lending rose 0.37% from last month, up $6.6 billion to $1.76 trillion. Within that, owner occupied housing rose 0.55% or $6.5 billion, and investment lending rose just 0.02% or $220 million. Personal credit fell again, and business lending fell 0.3% down $2.5 billion to $917 billion, all seasonally adjusted.

Investment lending made up 33.5% of all housing loans, down from 33.7% the previous month, and continues to slide, as expected. However the drop in business credit meant the proportion of commercial lending fell to 32.4% of all lending.

The monthly growth trends show the fall in business lending, and the fall-off in investor lending, all seasonally adjusted, which in the current environment may well be writing the volumes down too far.

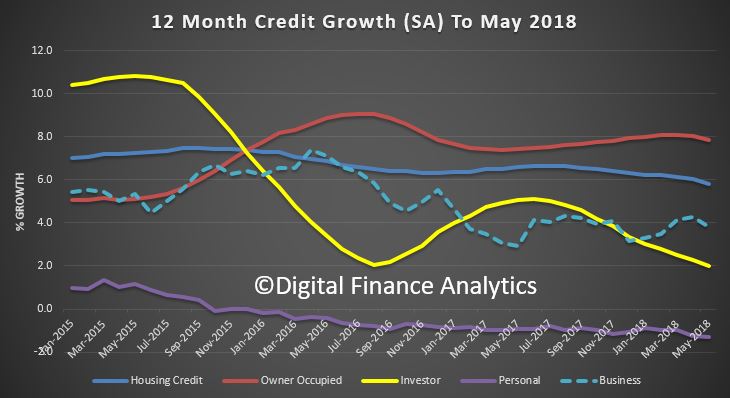

The 12 month rolling trend shows owner occupied housing still running at 7.9%, well above inflation and wage growth, while investor lending has a read of 2%, which is the lowest see since the RBA series started to be published in 1991. Have no doubt, investor lending is fading.

Personal credit dropped an annualised 1.3%, the largest fall since the fall out from GFC in 2009. Business lending was around 3.8% annualised and slid a little.

Finally, the non-bank contribution to lending growth can be imputed by subtracting the APRA ADI data from the RBA market data. This is an inexact science because of timing and coverage issues across the data. But it tells an interesting story, with non-bank growth rates sitting at around 20% for owner occupied loans and around 18% for investor loans, on a twelve month rolling basis. So we can see where some of the slack in the system is being taken up as non-banks flex their muscles. Regulation of this sector is a concern, as Moody’s highlighted recently. APRA has this responsibility, but how actively they are looking at this segment of the market, when data is so hard to acquire is a moot point. My guess is they are light on.

He described the basics of Crypto, with reference in particular to Bitcoin, compares it with money, and concludes that many of these shortcomings of cryptocurrencies stem from their design around trustless distributed ledgers and the costly proof-of-work verification method that is required in the absence of a trusted central entity. In contrast, in situations where there are trusted central entities in well-functioning payment systems, there may be little need for cryptocurrencies.

He then goes on to explore the implications for central banks.

The Bank has been watching developments in these areas for about five years. Currently, however, cryptocurrencies do not appear to raise any major concerns for the Bank given their very low usage in Australia. For example, it is hard to make a case that they raise any significant concerns for the Bank’s mandate to promote competition and efficiency and to control systemic risk in the payments system.

Nor do they currently raise any major issues for the Bank’s monetary policy and financial stability mandates. There are only very limited links from cryptocurrencies to the traditional financial sector. Indeed, many financial institutions have actively sought to avoid dealing with cryptocurrencies or cryptocurrency intermediaries. So, it is unlikely that there would be significant spillovers to the broader financial system if cryptocurrency holders were to suffer valuation losses or if a cryptocurrency system or intermediary was compromised.

But given all the interest in cryptocurrencies or private digital currencies, people have inevitably asked whether central banks should consider issuing digital versions of their existing currencies. I can give you an indication of the Bank’s preliminary thinking on this issue, as outlined in December by the Governor in a speech entitled ‘An eAUD?’.

Currently if households wish to hold money, they have two choices. They can hold physical cash, which is a liability of the Reserve Bank, or they can hold deposits in a bank (or credit union or building society), which is an electronic form of money and is a liability of a commercial bank that is covered (up to $250,000) by the Financial Claims Scheme. Both forms of money serve as a store of value and a means of payment (assuming the bank deposit is in a transaction account).

Most money is already ‘digital’ or electronic in form. Currency now accounts for only about 3½ per cent of what we call broad money. The remaining 96½ per cent is bank deposits, which we might call commercial bank digital money.

Furthermore, the use of cash by households in their transactions has been falling in recent years. This next graph shows there has been strong growth over an extended period in the use of cards and other forms of electronic payments. In contrast, the dots, which are from the Bank’s Consumer Payments Survey, show a significant fall in the use of cash. In 2007, cash accounted for nearly 70 per cent of the number of household transactions. Nine years later, this had fallen to 37 per cent.

Clearly, some households are moving away from cash and finding that electronic payments provided by banks better meet their needs. And this trend is likely to continue as the New Payments Platform (NPP), which launched recently, allows banks to offer better services to households – namely real-time electronic payments that give immediate value to the recipient, are easily addressed, are available 24/7 and carry lots more data than currently.

So the question is: ‘should the Reserve Bank introduce a new form of cash – an eAUD as the Governor called it – to give households an electronic payment instrument issued by the central bank for their everyday payments?’

Our current thinking is that there would not necessarily be all that much demand for an additional form of money in normal times, though this would presumably depend partly on design decisions such as the interest rate (if any) that would be paid on this money.

But to the extent that there was significant demand, particularly if this occurred at times of financial uncertainty with households switching out of the banking sector, there could be significant implications for the Bank’s financial stability mandate. There would also be implications for the structure of the financial sector – for example, it could result in reduced financial intermediation. We would need to think through these implications carefully.

So for the time being at least, consideration of a possible new electronic form of money provided by the Reserve Bank to households is not something that we are actively pursuing. Based on our interactions with our counterparts in other countries, it is also not front of mind for most other advanced economy central banks. An exception is Sweden, where the shift away from the use of cash is significantly more advanced than in Australia and elsewhere. Sweden’s Riksbank is studying the issues regarding the possible issuance of an e-krona and expects to report by late 2019.

However, as the Governor indicated in December, there might be a stronger case for considering a new form of central bank liability for use by businesses and financial institutions.

Here it is important to remember that the Reserve Bank already offers electronic balances to financial institutions in the form of Exchange Settlement Accounts (ESAs) at the Reserve Bank. These balances can be passed between financial institutions during the banking day, with the Bank keeping the official record (or the ledger) of account balances.[10] A key function of ESAs is that they provide banks with a risk-free liquid asset for settling payment obligations through the day, to prevent the build-up of large exposures that could threaten financial stability.

However, some stakeholders in the payments area – including some fintechs – have expressed the view that the introduction of another form of central bank balances could be quite transformative. They have suggested the issuance of a new form of digital money that would be accessible to businesses and could be passed around on a distributed ledger. They argue that the availability of another form of central bank settlement instrument could reduce risk and increase efficiency in business transactions. For example, it could allow the simultaneous exchange of money and other assets on blockchains. A central bank digital currency on a blockchain could potentially also enable ‘programmable money’, involving smart contracts and the simultaneous execution of complex, linked transactions.

Moving in this direction would involve two major changes to current arrangements: it would involve the introduction of a new form of settlement asset and it would presumably involve broader access to central bank money for non-bank institutions. Consideration of the first aspect will require an assessment of issues relating to the technology. Consideration of the second aspect would get into some of the issues that are relevant to thinking about giving households access to electronic central bank money, namely the implications for financial stability and the structure of the financial sector.

As we think more about a model along these lines we will be considering whether the benefits could be equally well facilitated by other means. For example, could there be commercial bank money on blockchains – say Bank X tokens, Bank Y tokens, and the like, rather than RBA digital settlement tokens? Indeed, some models have been sketched out whereby commercial banks would put aside ESA balances at the central bank or would put risk-free assets into special-purpose vehicles, and then issue credit-risk-free settlement tokens for use by their customers. We will also need to think about whether the possible use-cases that have been proposed really need central bank money on a blockchain, or if they might also be possible using other real-time payment rails – perhaps the NPP. At the moment, it does not appear that a strong case has emerged for us to provide this new form of central bank money, but we have an open mind.

RBA Assistant Governor (Economic) Luci Ellis spoke about the role of infrastructure from the perspective of someone involved in macroeconomic policy: the policy challenges and opportunities, the work of the G20 and role of infrastructure as not just an engine of growth but, more importantly, an enabler of growth.

What Is Infrastructure?

Before getting into that, it’s useful to define what we are talking about. When macroeconomists think about infrastructure, we think about the capital goods that provide public services. They are shared facilities that help economies function well. These include the structures – that is, the things produced by the construction industry that, unlike buildings, don’t have roofs. But there are also many other shared facilities that promote a well-functioning economy and society. One example of those other important pieces of infrastructure is the New Payments Platform that was launched recently. There are also important social infrastructures such as our legal system, or our frameworks for safeguarding children. But for the purposes of my talk, I will focus on the things that are tangible.

Within this class of tangible physical infrastructure, we can think of various kinds of physical assets. There is transport infrastructure, utilities providing electricity, gas and water, and communications infrastructure. Within each of these groups there are ‘hubs’ or centres, such as airports and railway stations for transport, power stations and reservoirs providing utilities, or telephone exchanges and satellites facilitating communication. Also within each group are ‘paths’ or distribution networks, such as the road and rail networks, power lines and telecommunications networks.

As you all well know, infrastructure of this kind can be provided by either the private or public sectors. The public sector might be involved for a number of reasons. One is that it is generally accepted that there are social benefits to providing these kinds of assets that are not fully captured by a profit-making provider. Without some provision by the state, such infrastructure will be under-provided. Another is the network nature of these facilities. Where there is a network, there is an element of monopoly power, and thus often a role for state regulation if not actually state ownership. At the very least, someone needs to set the rules of the game, whether that is the side of the road we drive on or the protocols used in telecommunications.

Despite the role of the state in the provision and management of these types of infrastructure, they are not ‘public goods’ in the textbook sense. Textbook public goods are non-rival and non-excludable: their benefits aren’t diminished by an extra person enjoying them and, in any case, you can’t prevent people from having those benefits. Clean air and a defence force fall into this category. By contrast, physical infrastructure can clearly suffer from congestion. It is also conceptually possible to exclude free riders from the use of the infrastructure, though this is more easily achieved in some cases than others. It is from these characteristics – congestion, excludability and the underlying monopoly network – that most of the policy challenges around infrastructure arise.

What Policy Challenges Does Infrastructure Pose?

Much like any business decision faced by private firms, decisions about infrastructure involve a lot of uncertainty. Businesses grapple with these questions every day. Should we build it? Is the market big enough? Where should we build it? What design and methods should we use? What price should we set?

It is tempting to think that physical infrastructure is no different. Many of the questions are the same. But there are differences, and the policy challenges around infrastructure stem from that. Firstly, infrastructure can be very long-lived, which compounds the uncertainty about future usage rates and congestion. Secondly, the network element of the infrastructure makes it especially difficult to forecast market size. Thirdly, the social benefits that spill over to the broader economy are harder to quantify than a forecast revenue stream.

All countries face the same challenges of providing enough infrastructure in the right places to serve the needs of their populations. So it is no surprise that infrastructure has been a recurring topic in the deliberations and work of the G20 group of major economies. Australia elevated the topic further during its presidency year in 2014. This year, the Argentine presidency has also included it as one of its key priorities and has re-convened the G20 Infrastructure Working Group, which met in Sydney earlier this month.

One typical challenge is risk management. Infrastructure risk takes many forms. There’s the risk that the project is not built efficiently, that investors are unwilling, that demand is too high – leading to congestion – or not high enough. There are risks that revenue can’t be collected as intended. There are risks that the construction isn’t resilient to natural disasters or just ordinary wear and tear.

Another typical challenge is financing. Most infrastructure assets cost a lot upfront to build, and their monetary return – if any – is only realised over a long period. This can still be an attractive payoff structure for private investors, depending on how the project is structured. Ensuring private sector participation in infrastructure finance has therefore been a priority of the G20.

A common thread in these challenges is that the nature of the risks and funding issues are very different in the ‘build phase’ than in the ‘run phase’, once the infrastructure is being used. This is true of any large construction project and, similarly, one solution can be to have different actors involved in the two stages.

What Policies Might Lessen These Challenges?

The good news is that, if we face common challenges, the solutions are also likely to be common. We can learn from each other. So there is value in sharing information about best practice across countries. For example, during Australia’s G20 presidency in 2014, a Global Infrastructure Hub (GI Hub) was announced, with an aim of, among other things, sharing guidance on best practices. If you think about it, the principles for designing a good road network or locating a railway line don’t really change according to where you live. There will be differences relating to legal frameworks or other national specifics, but most of what constitutes best practice will be universal.

To lessen the financing challenge, G20 authorities have been focusing on initiatives that can make infrastructure an attractive asset class. There is plenty of private sector financing looking for the stable long-term cash flows that certain kinds of infrastructure assets can provide, once they are built. The question is how to bring that financing to the projects that need it, especially in emerging market economies where the need seems to be greatest. Different countries have approached this topic differently (Chong and Poole 2013). The report ‘Roadmap to infrastructure as an asset class’, which G20 Finance Ministers and Governors endorsed in March, proposed several initiatives that should help, including to:

enhance project preparation so that projects are more ‘bankable’

align the risk of projects to the risk profile of investors

increase the data available on projects

promote quality infrastructure and good governance

improve local currency capital markets in emerging markets

explore the creation of standardised contracts for activities such as financing and risk sharing.

Some of these initiatives can work as collaborative efforts with the private sector. Others, such as aligning risks, may require more effective use of credit enhancement from the public sector or from supranational agencies, such as the multilateral development banks (MDBs). This is seen as a way of ‘crowding in’ private finance rather than have the MDBs fund the project themselves.

Here’s where the Australian experience might be instructive. As a central banker, I can look around the world and see that most countries have settled on the idea of having a specialist, independent agency to carry out the kinds of responsibilities that central banks usually have, such as setting monetary policy or running the payments system. The same is true for many kinds of financial regulation. It is less common to have an autonomous agency involved in analysing and assessing microeconomic policy. But in Australia, we do have something like that in the Productivity Commission. And similarly we have an independent statutory authority for assessing and prioritising infrastructure projects, Infrastructure Australia.

As a non-specialist it is not possible for me to quantify what difference this makes. But if common frameworks and rigorous, pre-emptive analysis help – and I believe they do – then Australia’s experience will surely be instructive for other economies wanting to improve their infrastructure.

What Is the Current State of Play in Australia?

In comparison to some countries, international research suggests that Australia is fairly well served by its current infrastructure.[4] But with a strongly growing population, we face a challenge of ensuring that the stock of infrastructure keeps pace with expanding needs. Utilities such as electricity and water, as well as transport links, need ongoing investment to accommodate a rising population.

This challenge has clearly been recognised and, over recent years, governments at both the state and federal level have been increasing infrastructure investment. As can be seen from this graph, public investment in communications infrastructure has increased with the rollout of the NBN. Transport infrastructure – road and rail – has increased even more sharply and is back close to the share of GDP it represented in the years immediately after the global financial crisis.

Graph 1

The recent federal budget foreshadowed additional infrastructure spending. More broadly, investment by the federal government is projected to increase over coming years. Most of the infrastructure spend is by state governments, however. This has already increased noticeably, particularly in the south-eastern states, and according to state budgets it is projected to increase further in the next couple of years. Much of this work is in urban transport projects, both road and rail.

Graph 2

Another area of infrastructure attracting substantial investment at the moment is renewable energy. The value of renewable generation projects slated for the next year or so is similar to the average of recent years’ total investment in electricity generation, distribution and transmission, a much broader set of activities. Most of the investment in renewables is by the private sector. These projects have become more attractive lately as the cost of the underlying technology has fallen. At the same time, the costs of fossil-based inputs to existing generation methods has risen, and so has the price of electricity. So renewable energy projects are becoming increasingly commercially viable. As such, it is an area where the private sector can provide the infrastructure.

And that is indeed what we are seeing. A range of data sources on both capital expenditure and financing show greatly increased activity recently (Graph 3). A few years ago, much of the investment in renewables was in small-scale rooftop solar. More recently, as the economics of these projects has changed, we are seeing more large-scale solar and wind projects being financed and built.

Graph 3

As I mentioned earlier, the risks and challenges of the build phase are very different from those in the run phase. There will be some areas, like renewables, where the private sector will be involved in both phases. In others, the execution and governance risks in the build phase don’t match investors’ desired risk profiles, but the revenue from the operation phase can do so. These kinds of projects will be good candidates for private ownership once construction is complete; some state governments are recycling the revenue from those sales to fund new infrastructure. And finally, there are projects where the social benefits are not easily captured as cash flow. It is important that these kinds of projects are not under-provided, just because they would not be profitable for the private sector to run.

Regardless of the exact approach to funding and management of construction, infrastructure investment can involve significant spillover benefits to the rest of the economy. The Bank has discussed these recently, and they bear repeating (RBA 2018). The direct spillovers derive from the incomes earned by the workers and firms doing the work; most of these projects are built by the private sector on behalf of the public sector. This income gets spent or invested, which in turn generates income for someone else and so on. At a time such as now, when there is still spare capacity in the economy, this ‘fiscal multiplier’ can result in overall demand rising by considerably more than the original spend on the project.

More broadly, and over a longer horizon, the economy benefits from a larger capital stock and the productivity benefits of infrastructure of this type. These are often hard to quantify even after the fact, but some examples might include: new export businesses enabled by the construction or expansion of an airport; higher productivity of logistics firms if their vehicles spend less time in traffic; and better health outcomes from reduced accident rates when roads are made safer.

It is these benefits that are worth focusing on, more than the raw contribution of the building work to GDP growth. As I’ve emphasised on an earlier occasion, it isn’t helpful to think of infrastructure as a new ‘engine of growth’, receiving the handover from the mining investment boom and, later, the apartment building boom (Ellis 2017). By its nature, infrastructure is justified by its contribution to the public good. It is not so much an engine of growth as an enabler of growth. But for this to be true, projects need to be rigorously assessed, carefully designed and appropriately timed. And for that to be possible, it helps if practitioners can learn from each other, for example through forums such as this one and, internationally, the initiatives of the G20.

Business lending in seasonal terms rose 0.4%, up $4.1 billion to $921 billion, and fell to 32.2% of all lending – we see a continued fall in the proportion of lending to business, as opposed for housing, which is not good.

Business lending in seasonal terms rose 0.4%, up $4.1 billion to $921 billion, and fell to 32.2% of all lending – we see a continued fall in the proportion of lending to business, as opposed for housing, which is not good. The monthly seasonally adjusted numbers highlight the slide in investor lending, and the stronger owner occupied lending.

The monthly seasonally adjusted numbers highlight the slide in investor lending, and the stronger owner occupied lending. Finally, we also estimate the growth in on-bank lending, by taking the original RBA data, and comparing this with the ADI data from APRA also out today.

Finally, we also estimate the growth in on-bank lending, by taking the original RBA data, and comparing this with the ADI data from APRA also out today. So more of the old same old, same old, housing lending still growing way above inflation and wages, forcing housing debt higher, at the expense of business investment.

So more of the old same old, same old, housing lending still growing way above inflation and wages, forcing housing debt higher, at the expense of business investment. We also added in the tax changes and child care subsidy (in both scenarios). We do not impose a particular family structure, but capture that in our surveys (which aligns to the ABS census distribution).

We also added in the tax changes and child care subsidy (in both scenarios). We do not impose a particular family structure, but capture that in our surveys (which aligns to the ABS census distribution). Here are the results, one year down the track.

Here are the results, one year down the track. So the impact of potential wages rises, in real terms is significant. A “good outcome!” However even then the risk in the system remains higher than we have been use to. Defaults reduced by 6% while stress fell by more than 8%.

So the impact of potential wages rises, in real terms is significant. A “good outcome!” However even then the risk in the system remains higher than we have been use to. Defaults reduced by 6% while stress fell by more than 8%. The ratios of assets to income are falling, having been rising for year, again reflecting falls in home prices. So while incomes are flat in real terms, asset values are falling faster.

The ratios of assets to income are falling, having been rising for year, again reflecting falls in home prices. So while incomes are flat in real terms, asset values are falling faster. And finally, the killer, the household debt to income ratios continues higher, this despite the greater focus on lending quality, and reduced “mortgage power”. The household debt to income ratio is now at 190.1, the housing debt in income 140.1, and the owner occupied housing debt to income is 106.7. In fact this is moving up more sharply as lenders have focused on owner occupied lending.

And finally, the killer, the household debt to income ratios continues higher, this despite the greater focus on lending quality, and reduced “mortgage power”. The household debt to income ratio is now at 190.1, the housing debt in income 140.1, and the owner occupied housing debt to income is 106.7. In fact this is moving up more sharply as lenders have focused on owner occupied lending. Combined this shows the problems in the household sector. No surprise then that mortgage stress is going higher. We release the June data tomorrow.

Combined this shows the problems in the household sector. No surprise then that mortgage stress is going higher. We release the June data tomorrow.

To me it is simple, they would like to lift rates to more normal levels, but cannot thanks to high debt, and downside risks. They are stuck. I believe the next move will be down as the economy weakens (dragged down by the fading property market, rising interest rates internationally, and concerns about China’ economic dynamo). But not yet.

To me it is simple, they would like to lift rates to more normal levels, but cannot thanks to high debt, and downside risks. They are stuck. I believe the next move will be down as the economy weakens (dragged down by the fading property market, rising interest rates internationally, and concerns about China’ economic dynamo). But not yet. Investment lending made up 33.5% of all housing loans, down from 33.7% the previous month, and continues to slide, as expected. However the drop in business credit meant the proportion of commercial lending fell to 32.4% of all lending.

Investment lending made up 33.5% of all housing loans, down from 33.7% the previous month, and continues to slide, as expected. However the drop in business credit meant the proportion of commercial lending fell to 32.4% of all lending. The 12 month rolling trend shows owner occupied housing still running at 7.9%, well above inflation and wage growth, while investor lending has a read of 2%, which is the lowest see since the RBA series started to be published in 1991. Have no doubt, investor lending is fading.

The 12 month rolling trend shows owner occupied housing still running at 7.9%, well above inflation and wage growth, while investor lending has a read of 2%, which is the lowest see since the RBA series started to be published in 1991. Have no doubt, investor lending is fading. Finally, the non-bank contribution to lending growth can be imputed by subtracting the APRA ADI data from the RBA market data. This is an inexact science because of timing and coverage issues across the data. But it tells an interesting story, with non-bank growth rates sitting at around 20% for owner occupied loans and around 18% for investor loans, on a twelve month rolling basis. So we can see where some of the slack in the system is being taken up as non-banks flex their muscles. Regulation of this sector is a concern, as Moody’s highlighted recently. APRA has this responsibility, but how actively they are looking at this segment of the market, when data is so hard to acquire is a moot point. My guess is they are light on.

Finally, the non-bank contribution to lending growth can be imputed by subtracting the APRA ADI data from the RBA market data. This is an inexact science because of timing and coverage issues across the data. But it tells an interesting story, with non-bank growth rates sitting at around 20% for owner occupied loans and around 18% for investor loans, on a twelve month rolling basis. So we can see where some of the slack in the system is being taken up as non-banks flex their muscles. Regulation of this sector is a concern, as Moody’s highlighted recently. APRA has this responsibility, but how actively they are looking at this segment of the market, when data is so hard to acquire is a moot point. My guess is they are light on.

He described the basics of Crypto, with reference in particular to Bitcoin, compares it with money, and concludes that many of these shortcomings of cryptocurrencies stem from their design around trustless distributed ledgers and the costly proof-of-work verification method that is required in the absence of a trusted central entity. In contrast, in situations where there are trusted central entities in well-functioning payment systems, there may be little need for cryptocurrencies.

He described the basics of Crypto, with reference in particular to Bitcoin, compares it with money, and concludes that many of these shortcomings of cryptocurrencies stem from their design around trustless distributed ledgers and the costly proof-of-work verification method that is required in the absence of a trusted central entity. In contrast, in situations where there are trusted central entities in well-functioning payment systems, there may be little need for cryptocurrencies.