The Royal Commission into Financial Services Misconduct, yesterday spent time with ANZ, and examined their expenses validation and verification processes, especially when applications were made via the broker channel.

Astonishingly, it appears that the bank may ignore the expense data from the broker as submitted (so the Commission asked why they capture the data at all!). Household Expenditure Measure (HEMs) figured in the discussion, as a test which was used by the bank in the assessment process. It will be interesting to see if the Commission views this approach is compliant with their responsible lending obligations.

It begs the question more broadly, are mortgages held by the banks supported by appropriate expense calculations? Some are saying that up to 40% of loans on book may have issues.

We also note that the “mortgage power” type calculators available on bank web sites to give an indication of a borrowers ability to get a mortgage, on average now gives a mortgage figure some 20% lower than a couple of years back.

So, many borrowers would not now get the mortgage they did then. Think about the implications for existing borrowers seeking to refinance, or to move from interest only loans to principal and interest loans!

There was also more data on lower auction clearance rates. Plus predicted falls in home prices, from Moody’s.

When you overlay the Commission findings, with the sales trends (deep discounts are now a feature of current sales, see above), it seems to me home prices are set for more falls in the months ahead.

We discussed this in our latest video blog.

More broadly, the Commission shows the massive repair job the banks have to do on their reputations and culture. No wonder their share prices are down. Of more significance are the structural risks to the economy, as households continue to struggle with over-committed budgets thanks to lax lending. This is unlikely to end well.

The purpose of the Commission was to remove uncertainty from the banking sector, but as it goes about its business, in fact the levels of concern are rising. It has royally back-fired!

But there is a good chance that customer outcomes will be enhanced as the consequences are digested. This would be an excellent outcome. But not an intended one.

CBA’s new CEO Matt Comyn has written to staff as the the blow touch is applied by the inquiry.

This week the Royal Commission into Misconduct in Banking, Insurance and Superannuation commenced hearings in Melbourne.

From the outset, we said that we were absolutely determined to be cooperative and open with the Commission. Unfortunately, as we heard on Tuesday, our first submissions did not meet the Commission’s expectations. This was never our intention and we will resubmit our information as soon as possible and ensure we have fully met the requests of the Commission. We will work to make sure this doesn’t happen again.

There will be cases highlighted next week where customers have been treated unfairly by us. In many cases, our actions have had a significant impact on the financial and emotional wellbeing of our customers. This is unacceptable.

Where we have made mistakes we must and will take responsibility for them, we will make things right for our customers, and not repeat the same mistakes. We will exceed our regulatory and compliance obligations, and enhance the financial wellbeing of every single customer we serve.

Together, we will make our bank better, and one we can all continue to be proud of.”

Today we examine the Mortgage Industry Omnishambles. And it’s more than just a flesh wound!

Welcome to the Property Imperative Weekly to 17th March 2018. Watch the video, or read the transcript.

In this week’s review of property and finance news we start with the latest January data from the ABS which shows lending for secured housing rose 0.14% or 28.8 million to $21.1 billion. Secured alterations fell 1%, down $3.9 million to $391 million. Fixed personal loans fell 0.1%, down $1.2 million to $4.0 billion, while revolving loans fell 0.06%, down $1.3 million to $2.2 billion.

Investment lending for construction of dwellings for rent rose 0.86% or $10 million to $1.2 billion. Investment lending for purchase by individuals fell 1.34%, down $127.7 million to $9.4 billion, while investment lending by others rose 7.7% up $87.2 million to $1.2 billion.

Fixed commercial lending, other than for property investment rose 1.25% of $260.5 million to $21.1 billion, while revolving commercial lending rose 2.5% or $250 million to $10.2 billion.

The proportion of lending for commercial purposes, other than for investment housing was 45% of all commercial lending, up from 44.5% last month.

The proportion of lending for property investment purposes of all lending fell 0.1% to 16.6%.

So, we are seeing a rotation, if a small one, towards commercial lending for more productive purposes. However, lending for property and for investment purposes remains quite strong. No reason to reduce lending underwriting standards at this stage or weaken other controls.

But this also explains the deep rate cuts the banks are now offering – even to investors – ANZ Bank and the National Australia Bank were the last of the big four to announce cuts to their fixed rates, following similar announcements from the Commonwealth Bank and Westpac. NAB has dropped its five-year fixed rate for owner-occupied, principal and interest home loans by 50 basis points, from 4.59 per cent to 4.09 per cent. The bank has also reduced its fixed rates on investor loans by up to 35 basis points, with rates starting from 4.09 per cent. And last week ANZ also dropped fixed rates on its “interest in advance”, interest-only home loans by up to 40 basis points, with rates starting from 4.11 per cent. Further, fixed rates on its owner-occupied, principal and interest home loans have fallen by 10 basis points, with rates now starting from 3.99 per cent. This fixed rate war shows our big banks are not pricing in a rate hike anytime soon.

But we think these offers will likely encourage churn among existing borrowers, rather than bring new buyers to the market. For example, the ABS housing finance data showed that in original terms, the number of first home buyer commitments as a percentage of total owner occupied housing finance commitments rose to 18.0% in January 2018 from 17.9% in December 2017 – and this got the headline from the real estate sector, but the absolute number of first time buyers fell, thanks mainly to falls of 22.3% in NSW and of 13.3% in VIC. More broadly, there were small rises in refinancing and investment loans for entities other than individuals.

The latest data from CoreLogic shows home prices fell again this week, with Sydney down for the 27th consecutive week, and their index registering another 0.09% drop, whilst auction volumes were down on last week. They say that last week, the combined capital city final auction clearance rate fell to 63.3 per cent across a lower volume of auctions with 1,764 held, down from the 3,026 auctions over the week prior when a slightly higher 63.6 per cent cleared. The weighted average clearance rate has continued to track lower than results from last year; when over the corresponding week 75.1 per cent of the 1,473 auctions sold.

But the strategic issues this week relate to the findings from the Royal Commission and from the ACCC on mortgage pricing. I did a separate video on the key findings, but overall it was clear that there are significant procedural, ethical and even legal issue being raised by the Commission, despite their relatively narrow terms of reference. They cannot comment on bank regulation, or macroprudential, but the Inquiries approach is to examine a series of case studies, from the various submissions they have received, and then apply forensic analysis to dig into the root causes examining misconduct. The question of course is, do the specific examples speak to wider structural questions as we move from the specific instances. We discussed this on ABC Radio this week.

From NAB we heard about referrer’s providing leads to the Bank, outside normal lending practices and processes, and some receiving large commissions, despite not being in the ambit of the responsible lending code. From CBA we heard that the bank was aware of the conflict brokers have especially when recommending an interest only loan, because the trail commission will be higher as the principal amount is not repaid. And from Aussie, we heard about their reliance on lenders to trap fraud, as their own processes were not adequate. And we also heard of examples of individual borrowers receiving loans thanks to poor conduct, or even fraud. We also heard about how income and expenses are sometimes misrepresented. So, the question is, do these various practices show up more widely, and what does this say about liar loans, and mortgage systemic risk?

We always struggled to match the data from our independent household surveys with regards to loan to income, and loan to value, compare with loan portfolios we looked at from the banks. Now we know why. In some cases, income is over stated, expenses are understated, and so loan serviceability is a potentially more significant issue than the banks believe – especially if interest rates rise. In fact, we saw very similar behaviours to the finance industry in the USA before the GFC, suggesting again we may see the same outcomes here. One other point, every lender is now on notice that they need to look at their current processes and back book, to test affordability, serviceability and risk. This is a big deal.

I will also be interested to see if the Commission turns to look at foreclosure activity, because this is the other sleeper. Mortgage delinquency in Australia appears very low, but we suspect this is associated with heavy handed forced sales. Something again which was apparent around the GFC.

More specifically, as we said in a recent blog, the role and remuneration models for brokers are set for a significant shakedown.

Turning to the ACCC report on mortgage pricing, this was also damming. Back in June 2017, the banks indicated that rate increases were primarily due to APRA’s regulatory requirements, but now under further scrutiny they admitted that other factors contributed to the decision, including profitability. Last December, the ACCC was called on by the House of Representatives Standing Committee on Economics to examine the banks’ decisions to increase rates for existing customers despite APRA’s speed limit only targeting new borrowers. The investigation falls under the ACCC’s present enquiry into residential mortgage products, which was established to monitor price decisions following the introduction of the bank levy. Here are the main points.

Banks raised rates to reach internal performance targets: concern about a shortfall relative to performance targets was a key factor in the rate hikes which were applied across the board. Even small increases can have a significant impact on revenue, the report found. And the majority of existing borrowers would likely not be aware of small changes in rates and would therefore be unlikely to switch.

A shared interest in avoiding disruption: Instead of trying to increase market share by offering the lowest interest rates, the big four banks were mainly preoccupied and concerned with each other when making pricing decisions. It shows a failure in competition (my words).

Reputation is everything: The banks it seems were very conscious of how they should explain changes. As it happens, blaming the regulators provides a nice alibi/

For Profit: Internal memos also spoke of the margin enhancement equating to millions of dollars which flowed from lifting investment loans.

New Loans are cheaper, legacy rates are not. Banks of course are offering deep discounts to attract new customers, funded by the back book repricing. The same, by the way, is true for deposits too.

The Australian Bankers Association “silver lining” statement on the report said they welcomed the interim report into residential mortgages, which clearly shows very high levels of discounting in the Australian home loan market. It’s clear that competition is delivering better deals for customers, shopping around works and Australians should continue to do so to get the best discounts on the advertised rate. But they are really missing the point!

We will see if the final report changes, but if not these are damming, but not surprising, and again shows the pricing power the major lenders have.

So to the question of future rate rises. The FED meets this week, and the expectation is they will lift rates again, especially as the TRUMP tax cuts are inflationary, at a time when the US economy is already firing. In a recent report Fitch Ratings said that Central banks are becoming less cautious about normalising monetary policy in the face of strong growth and diminishing spare capacity. They expect the Fed to raise rates no less than seven times before the end of next year. And while still sounding tentative, the European Central Bank is clearly laying firm groundwork for phasing out QE completely later this year. They now also expect the Bank of England to raise rates by 25bp this year.

Guy Debelle, RBA Deputy Governor spoke on “Risk and Return in a Low Rate Environment“. He explored the consequences of low rates, on asset prices, and asks what happens when rates rise. He suggested that we need to be alert for the effect the rise in the interest rate structure has on financial market functioning, and that investors were potentially too complacent. There are large institutional positions that are predicated on a continuation of the low volatility regime remaining in place. He had expected that volatility would move higher structurally in the past and this has turned out to be wrong. But He thinks there is a higher probability of being proven correct this time. In other words, rising rates will reduce asset prices, and the question is – have investors and other holders of assets – including property – been lulled into a false sense of security?

All the indicators are that rates will rise – you can watch our blog on this. Rising rates of course are bad news for households with large mortgages, exacerbated by the possibility of weaker ability to service loans thanks to fraud, and poor lending practice. We discussed this, especially in the context of interest only loans, and the problems of loan resets on the ABC’s 7:30 programme on Monday. We expect mortgage stress to continue to rise.

There was more discussion this week on Housing Affordability. The Conversation ran a piece showed that zoning is not the cause of poor affordability, and neither is supply of property. Indeed planning reform they say is not a housing affordability strategy. Australia needs a more realistic assessment of the housing problem. We can clearly generate significant dwelling approvals and dwellings in the right economic circumstances. Yet there is little evidence this new supply improves affordability for lower-income households. Three years after the peak of the WA housing boom, these households are no better off in terms of affordability. In part, this may reflect that fact that significant numbers of new homes appear not to house anyone at all. A recent CBA report estimated that 17% of dwellings built in the four years to 2016 remained unoccupied. If we are serious about delivering greater affordability for lower-income Australians, then policy needs to deliver housing supply directly to such households. This will include more affordable supply in the private rental sector, ideally through investment driven by large institutions such as super funds. And for those who cannot afford to rent in this sector, investment in the community housing sector is needed. In capital city markets, new housing built for sale to either home buyers or landlords is simply not going to deliver affordable housing options unless a portion is reserved for those on low or moderate incomes.

But they did not discuss the elephant in the room – booming credit. We discussed the relative strength of different drivers associated with home price rises in a separate, and well visited blog post, Popping The Housing Affordability Myth. But in summary, the truth is banks have pretty unlimited capacity to create more loans from thin air – FIAT – let it be. It is not linked to deposits, as claimed in classic economic theory. The only limit on the amount of credit is people’s ability to service the loans – eventually. With that in mind, we built a scenario model, based on our core market model, which allows us to test the relationship between home prices, and a series of drivers, including population, migration, planning restrictions, the cash rate, income, tax incentives and credit.

We found the greatest of these is credit policy, which has for years allowed banks to magic money from thin air, to lend to borrowers, to drive up home prices, to inflate the banks’ balance sheet, to lend more to drive prices higher – repeat ad nauseam! Totally unproductive, and in fact it sucks the air out of the real economy and money directly out of punters wages, but make bankers and their shareholders richer. One final point, the GDP calculation we use in Australia is flattered by housing growth (triggered by credit growth). The second driver of GDP growth is population growth. But in real terms neither of these are really creating true economic growth. To solve the property equation, and the economic future of the country, we have to address credit. But then again, I refer to the fact that most economists still think credit is unimportant in macroeconomic terms! The alternative is to continue to let credit grow well above wages, and lift the already heavy debt burden even higher. Current settings are doing just that, as more households have come to believe the only way is to borrow ever more. But, that is, ultimately unsustainable, and this why there will be an economic correction in Australia, and quite soon. At that point the poor mortgage underwriting chickens will come home to roost. And next time we will discuss in more detail how these scenarios are likely to play out. But already we know enough to show it will not end well.

The disparity between bank CEO pay and average weekly earnings is contributing to the uncompetitive nature of Australia’s economy, argues progressive think tank The Australia Institute.

The GFC+10: Executive Pay in Australia report released yesterday by the Australia Institute has scrutinised the pay packages of executives at Australia’s biggest companies 10 years on from the global financial crisis.

Homing in on banks, which had “been a particular focus of attention” in recent times, the report found NAB and Commonwealth Bank of Australia bosses respectively earned 108 and 93 times the average weekly earnings in 2017.

“Pay for the NAB CEO peaked in 2004 but even if we ignore that spike the data still show that CEO pay was increasing rapidly during the bulk of the 2000s, as people were expressing the most concern.”

For the chief executive of CBA at the time, the spike in pay was widest in the lead-up to the global financial crisis.

In fact, seven- or eight-figure remuneration packages were “likely to have played an important role in the global financial crisis” wherein chief executives risked long-term performance for short-term gains, the report said.

Such a significant gap in the earnings of average workers compared with top executives also reflected “to a large extent the uncompetitive nature of the modern Australian economy”.

“It has to be stressed that the issue of massive CEO pay is one associated with industry concentration and the dominance of big business in the Australian economy,” it said.

“According to tax office data 390,774 companies reported a positive income and declared taxable income of $281 billion, giving the ‘average’ company an income of $719,201 in 2015.

“An economy dominated by ‘average’ companies could never pay CEOs anything like the amounts going to the CEOs of the top Australian oligopolies and monopolies,” said the report.

While “growth in CEO pay was quite dramatic in the lead up to around 2007 or 2008” and had moderated since then, the report concluded remuneration for these top executives “remains excessive”.

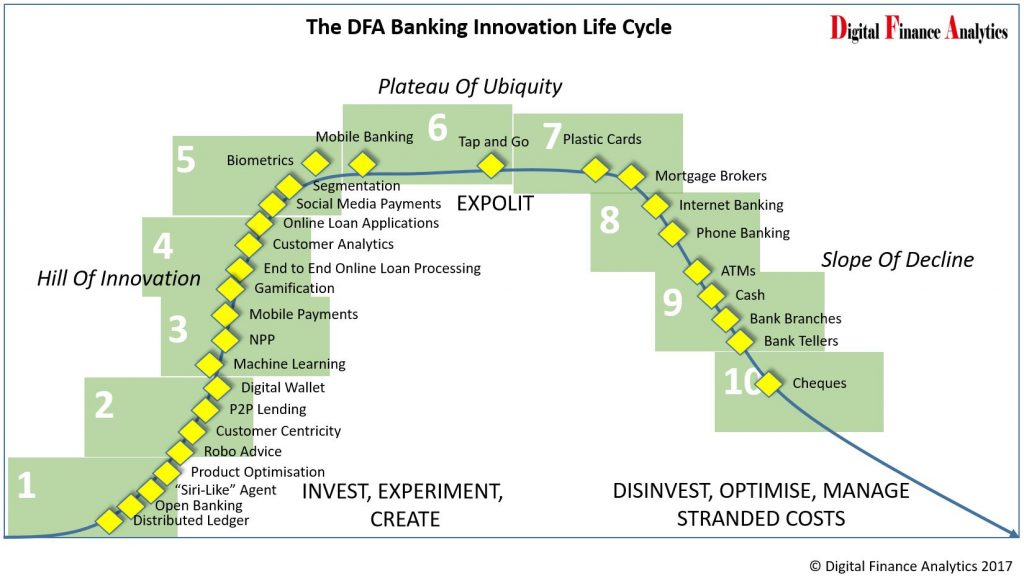

Given the tenor of the Royal Commission responsible lending inquiries this week, which focussed on the complexities of brokers and lenders complying with their responsible lending obligations, we believe the future will be distinctly digital. Our banking innovation life cycle road map calls this out.

To illustrate the point, there was a timely announcement from the Opica Group who have a new, and they claim Australia’s first responsible lending engine” (RELIE). This from The Adviser.

A new artificial intelligence-based expenses verification engine has been launched for brokers and lenders to ensure responsible lending and compliance obligations are met.

Billing the tech as “Australia’s first responsible lending engine” (RELIE), the Opica Group has launched the platform to help “protect any broker or lender from a breach of their responsible lending requirements”.

According to Opica Group founder Brett Spencer, the platform is needed because “lenders traditionally have been very quick to put blame on brokers for any application that goes sour”.

Mr Spencer said that following a tighter regulatory environment and “greater scrutiny being placed on our industry by regulators”, the group identified that “brokers needed something that provided them some protection”.

As such, it built the RELIE platform to enable brokers (and lenders) to perform a “RelieCheck” that could prove they had done the adequate checks into expenses and the consumer’s ability to service the loan.

How it works

The RELIE engine makes use of a specially built artificial intelligence engine, Sherlock™, which analyses a consumer’s banking and credit card transaction data over a period of 12 months and automatically provides “income verification, an understanding of the client’s mandatory expenditure, and therefore their ability to service a loan”.

According to the group, the key differentiator of the RELIE platform when compared to credit checks is that it uses machine learning to categorise transactions, allowing for the differentiation of transaction types, including mandatory versus discretionary expenditure and recurring versus one-off spending.

It also automatically highlights areas of concerns within the transaction data such as undisclosed debts, spikes in expenditure of high-risk categories such as gambling, and possible changes in life circumstances such childbirth.

Mr Spencer commented: “With the advancements in technology and legislation crackdown, we saw an opportunity to protect brokers and automate significant components of an applicant’s income and expense verification process…

“We believe that running a RelieCheck will protect any broker or lender from a breach of their responsible lending requirements.”

Speaking to The Adviser, Mr Spencer elaborated: “While a credit check simply looks at your credit worthiness, a RelieCheck looks at the consumer’s 365-day spending and income transactions and interrogates the data from a responsible lending perspective.

“It then presents back to the broker or lender a summary of exactly what, when and where an applicant’s income and expense are positioned.”

However, the Opica Group founder said that while the AI engine “does all the grunt work” to auto categorise and allocate spends to a range of buckets (such as mandatory versus discretionary expenses), the broker is able to review each category of spend and re-allocate expenses to a different category as part of their responsible lending discussions with the customers.

Each change made is then notated by the broker in order to meet their responsible lending requirements.

Revealing that the engine has been 16 months in the making, Mr Spencer said that the group wanted to “create a platform that a broker could use to protect themselves from any unintended breach of their responsible lending requirements”.

He added: “We also wanted to speed up the physically demanding process of paper-based statement reviews so that a broker could reduce the amount of time it takes to process a loan, and in the process providing a far greater service to the customer.”

Opica Group revealed that “early indications” have shown that by performing a RelieCheck on an applicant, a broker or lender could reduce processing times by approximately 90 minutes per application (when compared to manual assessment of the applicant’s banking and credit card transactions).

Mr Spencer concluded: “We want to create a new industry standard.

“Data is a commodity, but what you do with the data is the key ingredient.”

He added that he did not believe anyone else was thinking about “what we do with the data to aid the lending process”.

Opica Group is reportedly working with a number of aggregators and lenders to establish whether the engine could be integrated into their customer relationship management (CRM) systems. The service costs $15 (plus GST) per applicant for a broker account, or $10 (plus GST) per applicant for an aggregator or lender account.

CBA owned mortgage broker Aussie Home Loans does not have the capability to detect fraud committed by its brokers and instead waits until the banks detect scams and alert them as it does not have the resources.

The admissions were made by Aussie Home Loans general manager of people and culture Lynda Harris in a second day of questioning at the banking royal commission from counsel assisting Rowena Orr, QC.

It was revealed the company had recently bolstered the risk and compliance function at the broker to a total of nine employees.

Ms Harris was being questioned about the process behind the termination of an Aussie Home Loans broker Emma Khalil. Ms Khalil submitted multiple loan applications that were based on fake supporting documents including many from the same employer and with the same details.

“We don’t have that, we are reliant on the lenders to provide that expertise because ultimately they are the organisation that is approving the loans,” Lynda Harris said.

The fraud was not picked up until the client applied for a credit card with Westpac using different income details.

After the extent of the fraud committed by Ms Khalil was revealed, multiple internal emails between Aussie management revealed the broker was waiting for confirmation from Westpac before acting.

“If Westpac find that there was fraudulent activity on her part and revoke her accreditation, then that will be in breach of her contract and ultimately result in her termination from Aussie,” one such email read.

Ms Orr asked why Aussie was waiting to hear back from Westpac before terminating the employment of Ms Khalil despite identifying a number of suspect loans supported by similar or identical fake letters of employment.

“So Westpac – and in fact all large banks, have credit specialists and fraud teams that have the expertise to be able to determine fraud. We don’t have that, we are reliant on the lenders to provide that expertise because ultimately they are the organisation that is approving the loans,” Ms Harris said.

“What I want to put to you, Ms Harris, is that it’s not good enough, it’s not good enough that Aussie Home Loans outsources to a third party investigations of a fraudulent conduct made against one of its own employees. What do you say to that?” Ms Orr asked.

Ms Harris replied by saying that Ms Harris was not an employee of Aussie Home Loans and was in fact an independent contractor. She also said that company was not able to justify the expense.

Following an incredulous look from Ms Orr, Commissioner Ken Hayne sought clarification of the point

“It is open to me to conclude from your evidence from the time of the Khalil events and earlier, Aussie was of the view it was the role of the lender to investigate and determine whether there was fraud associated with one or more transactions?”

“Is it open to conclude from what you have told me that it remains Aussie’s view that it is for the lender and not Aussie to investigate and determine whether there was fraud associated with one or more transactions?”

Ms Harris explained the mortgage broker continued to invest in its systems and processes and hoped to develop a fulsome and rigorous process for the detection of anomalies in the loans submitted by its brokers.

She said the mortgage broker was developing a dashboard that would give it better visibility over its network however it was still in pilot phase.

Well, according to new research from Roy Morgan, home loan customer satisfaction with banks when using a mortgage broker was only 77.3%. This compares to 80.3% when home loans were obtained in person at a branch. So Banker is best….

Even among more recent home loans (held for under six years) satisfaction with going directly into branch was 81.7% compared to 78.7% for mortgage brokers. This is an important finding because it illustrates the potential impact that a third party can have on the satisfaction level of customers with their banks.

These results cover the six months to January 2018 and are from the Roy Morgan Single Source survey of over 50,000 consumers per annum, including over 12,000 mortgage holders.

Nearly all of the largest banks home loan customers have higher satisfaction with their bank when they obtained their loan in person at a branch, rather than through a mortgage broker. Home loan customers of Bendigo Bank who obtained their loan in person at a branch had the highest satisfaction with 92.6%, followed by Bankwest (87.3%) and St George (86.8%). The best of the big four was NAB with 82.4%, followed by ANZ (79.7%). All of the largest banks, with the exception of Westpac, had higher satisfaction when going direct rather than using mortgage brokers.

Home Loan Consumer Satisfaction: Obtained through Branch vs Mortgage Broker2 – Largest Home Loan Banks1

Source: Roy Morgan Single Source (Australia). 6 months to January 2018, n= 6,052 Base: Australians 14+ with home loan. 1. Based on largest number of home loans purchased at a branch. 2. Excludes other methods of obtaining home loans. 3. Includes brands not shown.

Satisfaction when using mortgage brokers was highest for St George with 85.6%, Bankwest (82.1%) and Suncorp Bank (82.0%). Each of the big four were below the market average (77.3%) for home loan customer satisfaction when using a mortgage broker, with the best of them being NAB (76.4%) and Westpac (75.7%).

Home loan customers go in person to branch

Despite many channels available to obtain home loans, over half (52.4%) of all current loans were sourced from going in person to a bank branch. This is well ahead of the 34.3% who purchased their loan through a mortgage broker. With these two channels accounting for 86.7% of the current market, it is important for banks to know how they perform in each in terms of customer satisfaction.

Method Used To Obtain Home Loan

Source: Roy Morgan Single Source (Australia). 6 months to January 2018, n= 6,052. Base: Australians 14+ with home loan

Other channels used to obtain home loans were, ‘in person with a mobile bank representative’ (8.7%, satisfaction 78.9%) and ‘over the phone’ (4.0%, satisfaction 80.3%).

In 2018, the way customers are banking in the Riverina and the surrounding areas has changed. Today, in response, NAB confirms changes to some of its branches in the area.

Video Player

Media error: Format(s) not supported or source(s) not found

NAB invests $1.6M to improve branches in the Riverina and surrounding areas in 2017 and 2018.

Following consultation with local teams, NAB can confirm Ardlethan, Lockhart, Grenfell, Culcairn, Boort, Barham and Euroa branches will close in June.

Customers in these towns can continue to do their banking at Australia Post offices, including making deposits up to $10,000 cash or withdrawals up to $2,000 per day.

NAB continues to back the Riverina through its other NAB branches across the region, sponsorships, including NAB AFL Auskick, and by funding and advocating for infrastructure so regional areas can grow.

Our business and agri bankers will continue to service the areas.

Locally, NAB is investing more than $1.6M into improving branches in Cowra, Seymour and Kerang, completed last year, and Tatura, Alexandra and Griffith, scheduled to be completed by September 2018, including installing and upgrading 32 ATMs in the area. Many of these ATMs are ‘Smart ATMs’, where customers can make deposits, check balances, and withdraw cash so customers can bank at their convenience.

As improvements are made to some branches, other branches in the area will be closing. Between 80-90% of NAB customers in Ardlethan, Lockhart, Grenfell and Culcairn are using other branches in the area such as Temora, Wagga Wagga, Young and Holbrook. Similarly approximately 85% of customers using Euroa, Boort and Barham are using other branches .

NAB General Manager, Retail, Paul Juergens, explained the decision was a difficult one to make and was only made after careful consideration.

“While our branches continue to be an important part of what we do at NAB, the way our customers are banking has changed dramatically in recent years,” Mr Juergens said.

“Increasingly we find that our customers are banking at other branches, or prefer to do their banking online, on the phone, or through our mobile app.

“In the locations we are closing, more than 80% of our customers are also using our other NAB branches in the area.

“Importantly, we are continuing to support the Riverina and surrounding areas, including a $1.6M investment into other branches in the area as well as through local sponsorships.”

Mr Juergens emphasised that NAB wants to continue to help our customers with their banking.

“Over the coming weeks, we’ll be spending time with our customers explaining the different banking options available to them, including online banking and banking through Australia Post.

“We know that some NAB customers still like to bank in person, which is why we have a strong relationship with Australia Post offices, which offer banking services on NAB’s behalf.

“At Australia Post, NAB customers can do banking like check account balances, pay bills and make deposits up to $10,000 cash or withdrawals up to $2,000 per day.”

NAB is working with our local branch employees to discuss their next steps.

“When we make changes to our branches, we make every effort to find opportunities for our local teams at other branches in our network, and often this is possible. If we can’t find opportunities, we help our employees through The Bridge, our industry leading program where employees are provided up to six months of career coaching as they decide what’s next for them – whether that be retirement, pursuing a new career or starting a small business.”

The Australian Banking Association welcomes today’s ACCC interim report into residential mortgages, which clearly shows very high levels of discounting in the Australian home loan market. It’s clear that competition is delivering better deals for customers, shopping around works and Australians should continue to do so to get the best discounts on the advertised rate.

The report itself states that “an overwhelming majority of borrowers with variable rate residential mortgages at the Inquiry Banks were paying interest rates significantly lower than the relevant headline rate” (the advertised rate). Discounts on home loans ranged between .78% and 1.39% below the relevant headline interest rate.

The advertised variable discount rate for home buyers today is 4.5%, close to the lowest ever recorded.

Data from APRA(1) and Canstar further illustrates there is strong competition in the home loan market, with over 140 providers, offering over 4,000 home loan products. Truly a vast and competitive market for Australians to choose a home loan.

Other evidence shows that Australians are taking advantage of this competitive market and are shopping around. Research by Galaxy shows that:

3 million people had switched banks over the last three years.

Of those who had switched banks over the last three years, two-thirds (68 per cent) found that switching was an easy process.

The opaque pricing of discounts offered on residential mortgage rates makes it difficult for customers to make informed choices and disadvantages borrowers who do not regularly review their choice of lender, a report by the ACCC has found.

The ACCC’s Residential Mortgage Price Inquiry is monitoring the prices charged by the five banks affected by the Government’s Major Bank Levy: Australia and New Zealand Banking Group Limited (ANZ), Commonwealth Bank of Australia (CBA), Macquarie Bank Limited, National Australia Bank Limited (NAB), and Westpac Banking Corporation.

The Inquiry’s interim report, out today, reveals signs of less-than-vigorous price competition, especially between the big four banks.

“We do not often see the big four banks vying to offer borrowers the lowest interest rates. Their pricing behaviour seems more accommodating and consistent with maintaining current positions,” ACCC Chairman Rod Sims said.

“We have seen various references to not wanting to ‘lead the market down’, to have rates that are ‘mid-ranked’ and to ‘maintain orderly market conduct’.”

The ACCC has found that discounts are a major factor in the interest rates customers are paying. Banks offer varying levels of discounts, both advertised and discretionary, but the latter are not always transparent to consumers.

The criteria used by different banks for determining the total discount offered to borrowers includes many factors, such as the individual borrower’s characteristics, their value or potential value to the bank, and their ability to negotiate.

During the two years to June 2017, the average discount across the five banks under review on variable interest rate loans was 78-139 basis points off the relevant headline interest rate.

“The discounting by the big banks lacks transparency and it’s almost impossible for customers to obtain accurate interest rate comparisons without investing a great deal of time and effort. But the potential savings from these discounts are immense,” Mr Sims said.

The report also found the average interest rates paid for basic or ‘no frills’ loans are often higher than for standard loans at the same bank.

“We think many customers who opted for ‘basic’ or ‘no frills’ loans thinking they are saving money would be surprised to learn they might actually be paying more.”

The report’s other key findings include:

existing residential mortgage borrowers paid significantly higher interest rates than new borrowers at the same bank. Between 30 June 2015 and 30 June 2017, existing borrowers on standard variable interest rate residential mortgages at the big four banks were paying up to 32 basis points more (on average) than new borrowers,

the large majority of borrowers are paying lower interest rates than the relevant headline interest rate, and

the bank with the lowest headline rate is not always the bank with the lowest average rate paid by borrowers.

“These findings suggest that many bank customers would likely benefit from either switching mortgage providers, or approaching their bank for a better rate and indicating they are prepared to switch to get one,” Mr Sims said.

“It seems existing customers are not being rewarded for their loyalty; in fact they are worse off. For example on a $375,000 residential mortgage, a new borrower paying an interest rate that was 32 basis points lower would save approximately $1200 in interest over the first year of a loan.”

“This is a significant saving,” Mr Sims said.

In addition to examining the way banks make their mortgage pricing decisions, the ACCC’s Residential Mortgage Pricing Inquiry final report will detail if the banks have adjusted their pricing in response to the Government’s Major Bank Levy.

As at November 2017, the five banks stated no specific decisions had been made to adjust residential mortgage prices in response to the Major Bank Levy.

Indeed, one bank considered whether the costs could be passed on to customers and suppliers at a range of different time periods, including after the end of the ACCC inquiry.

The ACCC’s final report will examine these issues further.

Background

On 9 May 2017 the Treasurer, the Hon. Scott Morrison MP, issued a direction to the ACCC to inquire into prices charged or proposed to be charged by Authorised Deposit-taking Institutions (ADIs) affected by the Major Bank Levy in relation to the provision of residential mortgage products in the banking industry in Australia. The Major Bank Levy came into effect from 1 July 2017, and the Inquiry will consider residential mortgage prices for the period 9 May 2017 until 30 June 2018.

The ACCC’s interim report examines the motivations, influences, and processes behind the residential mortgage pricing decisions of the five banks during the period 1 July 2015 to 30 June 2017.

The ACCC is reporting on this period in order to have a baseline against which to compare pricing decisions for the review period set by the Treasurer.

The ACCC will continue to examine the banks’ mortgage pricing decisions and how they have dealt with the Major Bank Levy through to 30 June 2018.

The ACCC has used its compulsory information gathering powers to obtain documents and data from the five banks on their pricing of residential mortgage products. The ACCC has supplemented its analysis of the documents and data supplied by the five banks with data from the Reserve Bank of Australia (RBA), Australian Prudential Regulation Authority (APRA) and the Australian Bureau of Statistics (ABS).

This inquiry is the first task of the ACCC’s Financial Services Unit (FSU), which was formed as a permanent unit during 2017 following a commitment of continuing funding by the Australian Government in the 2017-18 Budget. Alongside the ACCC’s role in promoting competition in financial services through its enforcement, infrastructure regulation, open banking, and mergers and adjudication work, the FSU will monitor and promote competition in Australia’s financial services sector by assessing competition issues, undertaking market studies, and reporting regularly on emerging issues and trends in the sector.

Astonishingly, it appears that the bank may ignore the expense data from the broker as submitted (so the Commission asked why they capture the data at all!). Household Expenditure Measure (HEMs) figured in the discussion, as a test which was used by the bank in the assessment process. It will be interesting to see if the Commission views this approach is compliant with their responsible lending obligations.

Astonishingly, it appears that the bank may ignore the expense data from the broker as submitted (so the Commission asked why they capture the data at all!). Household Expenditure Measure (HEMs) figured in the discussion, as a test which was used by the bank in the assessment process. It will be interesting to see if the Commission views this approach is compliant with their responsible lending obligations.

Source: Roy Morgan Single Source (Australia). 6 months to January 2018, n= 6,052 Base: Australians 14+ with home loan. 1. Based on largest number of home loans purchased at a branch. 2. Excludes other methods of obtaining home loans. 3. Includes brands not shown.

Source: Roy Morgan Single Source (Australia). 6 months to January 2018, n= 6,052 Base: Australians 14+ with home loan. 1. Based on largest number of home loans purchased at a branch. 2. Excludes other methods of obtaining home loans. 3. Includes brands not shown.