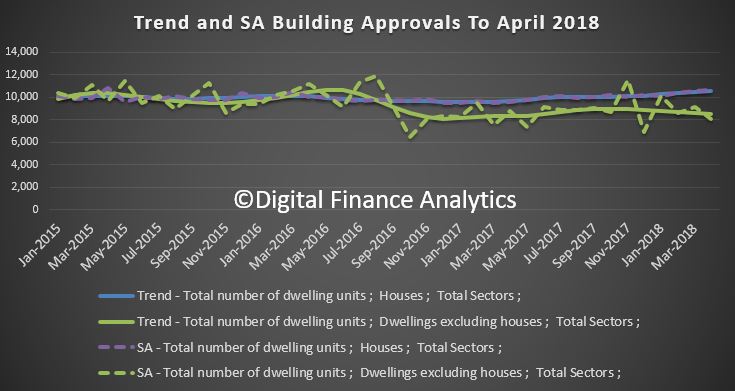

The ABS reports that the number of dwellings approved in Australia fell by 0.1 per cent in April 2018 in trend terms. We see a fall in units, somewhat offset by a rise in houses approved. The seasonally adjusted numbers show a more significant drop.

“The total dwellings series has been relatively stable for the past eight months, with around 19,000 dwellings approved per month,” said Justin Lokhorst, Director of Construction Statistics at the ABS. “The strength in approvals for houses is being offset by weakness in semi-detached and attached dwelling approvals.”

Among the states and territories, dwelling approvals fell in April in Tasmania (3.7 per cent), Victoria (2.3 per cent) and Western Australia (2.2 per cent) in trend terms.

Dwelling approvals rose in trend terms in the Australian Capital Territory (14.8 per cent), the Northern Territory (6.7 per cent), South Australia (1.7 per cent), New South Wales (0.9 per cent) and Queensland (0.7 per cent).

In trend terms, approvals for private sector houses rose 0.9 per cent in April. Private sector house approvals rose in Queensland (1.6 per cent), Victoria (1.5 per cent) and New South Wales (0.6 per cent), but fell in Western Australia (0.9 per cent) and South Australia (0.4 per cent).

In seasonally adjusted terms, total dwellings fell by 5.0 per cent in April, driven by a 11.5 per cent decrease in private sector dwellings excluding houses. Private sector houses rose 0.1 per cent in seasonally adjusted terms.

The value of total building approved fell 0.7 per cent in April, in trend terms, and has fallen for six months. The value of residential building fell 0.5 per cent while non-residential building fell 1.0 per cent.

The HIA managed to put a positive spin on the results saying “Detached House Approvals Strongest in 15 Years”.

The performance of the detached house building market is remarkable. The volume of house approvals during the three months to April was 9.9 per cent higher than a year ago – a time when it was already elevated,” said Shane Garrett, HIA’s Senior Economist.

Strong demand for new houses is being sustained by healthy rates of population growth – itself a product of robust labour markets in Australia’s largest cities. While it’s a virtuous circle for detached house building at the moment, there are risks on the horizon.

As the property market rotates, and demand slackens, property developers with a stock of newly built, or under construction dwellings – mostly high-rise apartments are trying tactics from deep discounting, cash bribes, or 100% mortgages to persuade people to buy. Remember there are around 200,000 units coming on stream over the next year or two and demand is falling.

Building approvals are also slowing. There is an air of desperation.

So we were interested to see (thanks to a tip off from our community) a WA initiative which was recently announced by Apartments WA – “Backed by the foundations of the BGC Group – Western Australia’s largest residential home builder and largest private company, we make your buying journey a seamless process from finding you the right apartment, assisting with obtaining finance, right through to settlement and key handover”.

Finance is provided by Perth based Harrisdale Pty Ltd trading as The Loan Company. They hold a financial service licence.

There are few details on the Preposit site, and we have no idea of the financial arrangements below the surface. So we suspect any prospective buyer should ask some hard questions about the overall risks and real effective costs. Remember that they are not an Authorised Depository Institution, so any money “saved” with them for a deposit could be at risk.

I put in a call to the company, who said they would call back to discuss “Preposit”, but they never did!

The Apartments WA exclusive product allows you to move into an apartment immediately, then begin to make weekly payments that are stored away for you until you’ve saved your deposit.

Apartments WA Sales Manager Chad Toquero said Preposit addresses one of the biggest stumbling blocks in home ownership – the deposit.

“Preposit appeals to all buyers who can afford the loan repayments but are finding it difficult to save for a deposit – there is nothing else like this in the market and Preposit appeals to those looking to buy and those who are currently renting but want to own their own home in the future.”

Apartments WA have also partnered with Loan Co to offer their clients access to a wide range of lenders. As each person’s financial circumstance, and thus borrowing capacity is different, Loan Co will work with each individual to pre-qualify them for a loan upfront. Preposit just allows the buyer to live in the property, while saving for their deposit.

This new way of purchasing is flexible, negotiable and customised to suit the needs of every individual.

Mr Toquero believes Preposit has the potential to make home-ownership become a reality for more people.

“We want Preposit to make home ownership easier for those who want to take advantage of the property market now and their only hurdle is saving for a deposit,” he said.

“The only catch is you have to be able to afford your mortgage repayments and pre-qualify for a loan.

“As long as you can afford the repayments but don’t quite have the deposit right now, we can get you into one of our apartments.”

Here is their FAQ.

What is Preposit ?

Preposit is a unique initiative created by Apartments WA to help people save for their deposit, whilst being able to live in the apartment at the same time.

So how does it work?

We help you find your dream apartment and then introduce you to our finance experts to work out how much you can afford to borrow. The difference between the purchase price and what you can borrow is the deposit you’ll need to save. Once you receive finance pre-approval to purchase the apartment, we give you the keys to move in and you start saving for your deposit in weekly payments. We then store away these payments away until your deposit amount is achieved, which we give back to you as your deposit toward purchasing the apartment.

Is there a minimum amount required to qualify for Preposit?

No. Everyone’s individual situation is different, and we’ll work through finding the best solution for you.

What properties is Preposit applied to?

We have a range of apartments in selected areas across Perth currently available.

Is this a Government Scheme or Shared Equity?

No. Apartments WA understands that saving for a deposit is one of the biggest hurdles when looking to buy a property. And we want to help.

Sounds too good. What’s the catch?

There’s no catch. You agree to purchase the property upfront, and then get to move in whilst you save for your deposit. Once you’ve reach your deposit amount, you settle on the apartment and then its yours.

How do i know if i eligible?

Complete our enquiry form and we’ll give you a call.

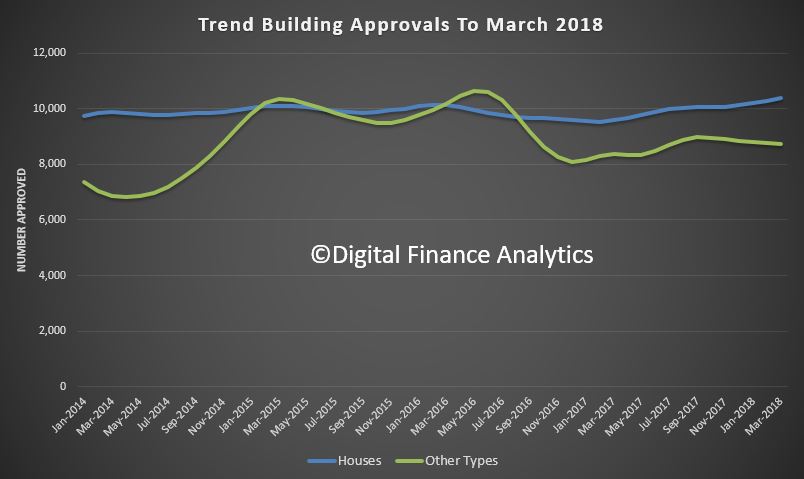

The number of dwellings approved in Australia rose in March 2018 in trend terms, with a 0.2 per cent rise.

This is being driven by approvals for private sector houses, which have now risen for 13 consecutive months. They are now at their highest level since 2003, in trend terms.

Approvals for private sector houses rose 0.8 per cent in March. Private sector house approvals rose in Victoria (1.8 per cent) and Queensland (1.5 per cent), but fell in Western Australia (2.1 per cent) and New South Wales (0.2 per cent). Private house approvals were flat in South Australia.

But units continue to fall, so overall the biggest trend increase in dwelling approvals in March was in the Australian Capital Territory (28.0 per cent), followed by the Northern Territory (5.3 per cent) and Queensland (2.3 per cent).

There were falls in trend terms in Western Australia (6.7 per cent), Tasmania (4.8 per cent), Victoria (0.5 per cent), New South Wales (0.2 per cent) and South Australia (0.1 per cent).

In seasonally adjusted terms, total dwellings rose by 2.6 per cent in March, driven by a 6.1 per cent increase in private sector dwellings excluding houses. Private sector houses rose 1.1 per cent in seasonally adjusted terms.

The value of total building approved fell 0.6 per cent in March, in trend terms, and has fallen for six months. The value of residential building rose 0.4 per cent while non-residential building fell 2.5 per cent.

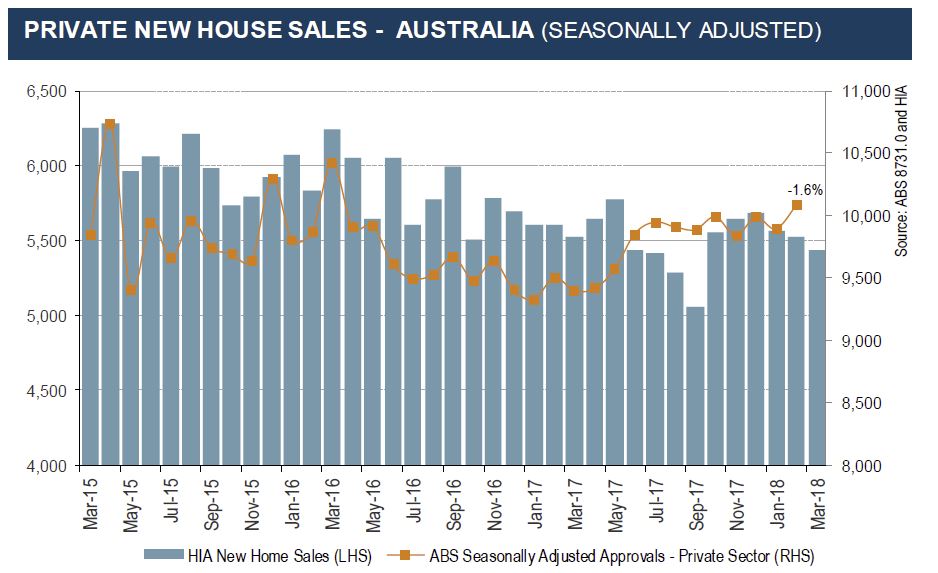

The HIA New Home Sales report – a monthly survey of the largest volume home builders in the five largest states – provides an early indication of trends in the residential building industry.

During March 2018, new house sales declined in three of the five markets covered by the report. The largest reduction in house sales occurred in South Australia (-11.4 per cent), followed by NSW (-10.2 per cent) and Victoria (-7.2 per cent). Two states bucked the overall trend, with the largest increase in new house sales in Western Australia (+26.2 per cent) and more measured growth occurring in Queensland (+2.7 per cent).

“Detached house sales fell again in March – meaning that declines have occurred in each of the first three months of 2018,” commented HIA Senior Economist Shane Garrett.

“New detached house sales were down by 2.0 per cent during March following a 0.7 per cent fall in February,” added Mr Garrett.

“The reduction in new house sales in Sydney and Melbourne is likely to be the result of tighter lending policies for investors being imposed by APRA.

“There has been a welcome increase in first home buyers participation which has partially offset the fall in investor involvement in the market.

“Economic recovery is underway in Queensland and WA – and these two states were the only ones to see new house sales rise during March. Detached house building has always been of considerable importance in these two markets.

“HIA’s new house sales index is a leading indicator of activity on the ground. Based on today’s results, new house building activity is likely to move lower on a national basis over the next few months,” concluded Shane Garrett.

More data showing the impact of the fleeing of property investors on the property market. We suspect the decline will continue as credit rules are tightened.

The HIA begs for no further constraints on this sector of the market, but with one third of loans for investment purposes, it is still too high. Remember the Bank of England got twitchy at 16%.

“Investors have been the target of a number of regulatory interventions and we are now seeing this impact on residential building activity,” said HIA Senior Economist, Geordan Murray.

The ABS today released building activity data for the final quarter of 2017. Detached house commencements increased by 0.7 per cent over the December 2017 quarter, while starts for other dwelling types (predominantly apartments) declined by 11.2 per cent.

“The decline in multi-unit dwelling starts has dragged down the total number of new home starts during the final quarter of 2017. The total number of dwellings starts fell by 5.0 per cent in the December 2017 quarter and was down by 8.3 per cent on the level recorded a year earlier,” added Mr Murray.

“In contrast to the decline in multi-unit starts, the resilience of the detached house market continued to shine through. The number of detached house starts during the December quarter of 2017 increased by 0.7 per cent over the quarter and was up by a similar amount compared with the level of a year ago.

“Despite the soft starts result in the quarter, the pipeline of multi-unit activity remains quite large. There were still over 150,000 multi-unit dwellings under construction at the end of the 2017, which is only slightly below the 155,000 level at the peak of the cycle. There are a further 33,800 dwellings in projects that have been approved and are yet to start work, this is a record high.

“The combination of falling commencements and the build-up of dwellings in projects awaiting commencement is somewhat concerning. It is likely to indicate a slowdown in pre-sales activity. New projects will not commence construction until they achieve a satisfactory level of pre-sales.

“Pre-sales to investors, both domestic and from overseas, have been important for many multi-unit developments. With additional taxes on foreign investors and regulators clamping down on investor lending, investors have retreated from the market.

“If we see investors return to the market and the approved projects continue to progress through to work on the ground then residential building work could potentially make a stronger contribution to economic growth this year than we are expecting.

“Now is not the time to impose additional taxes or constraints on investors,” concluded Geordan Murray.

Australia has record levels of supply of new properties but despite various government interventions, housing still remains unaffordable for many.

Our study found the government could use more direct methods to deliver homes for people on low and moderate incomes, while leveraging the market. These methods, widespread across the United Kingdom and in major cities of the United States, are known as “inclusionary planning”.

This includes requiring developers to make a financial contribution towards affordable housing, or to dedicate completed dwellings, as part of the development approval process.

We studied the outcomes of inclusionary planning programs in parts of the United States and the United Kingdom, and more recent approaches in South Australia and New South Wales.

What techniques can ensure affordable housing in the mix

“Inclusionary zoning”, a common type of inclusionary planning, was first developed in the United States to counteract land use rules which excluded the lower end of the property market. For example, where rules would only permit large homes on single allotments.

Some states in the US have also adopted “anti-snob” laws. Under these laws, developers whose schemes include affordable housing can bypass local zoning controls, if an area has insufficient affordable housing for those on low and moderate incomes.

More recently, inclusionary planning programs are being used in many US cities in a bid to ensure that transport and infrastructure investment does not price out or displace lower income renters.

There are now more than 500 inclusionary planning schemes operating in municipalities across the US. Some require developers to include affordable housing as part of development in a particular zone (usually a fixed percentage of units or floor space).

For example inclusionary planning programs in the city of San Francisco, California (population of around 830,000) generate around 150–250 affordable units per year (around 12% of the city’s total supply).

Other schemes allow variations to planning rules in return for affordable housing. These variations might permit additional density in certain areas or waive certain requirements that would normally apply or expedite the development assessment process.

Other schemes require financial contributions from developers to offset the impact of a project on affordable housing demand or supply.

These programs provide a way for governments to ensure affordable housing for lower income residents even in rapidly gentrifying neighbourhoods.

How this plays out in England and Scotland

In England and Scotland, the supply of affordable housing is negotiated through the planning process. The general expectation is that 20 to 40% of new housing developments will be affordable. But proportions of affordable housing are allowed to vary on a case by case basis in light of the housing market and the costs of undertaking the development.

The main methods for this in England are section 106 agreements. These agreements, which come under the Town and Country Planning Act 1990, specify the amount and type of affordable housing to be provided as part of a development.

Section 106 agreements have steadily gained traction since the 1990s. Between 2005–16, 83,790 affordable dwellings were secured through these agreements in England. This included 9,640 new dwellings in 2015–16.

Section 106 agreements have resulted in different types of affordable housing, including social housing, discounted home ownership, share equity schemes and affordable rental housing (offered at 20% less rent than for comparable properties in the same local housing market).

Our study found that when inclusionary planning model requirements are predictable and applied in a consistent way, developers accept them because they can factor costs into the price paid for land.

We also found most models work in conjunction with other government funding or subsidies, extending the value of this funding by reducing the cost of land for social or affordable housing.

What usually happens in Australia

Only the South Australia and New South Wales governments have similar types of planning schemes in Australia, although there are signs that other states may follow.

The SA government’s inclusionary planning target, announced in 2005, aims for 15% of significant new housing developments to be affordable.

By 2016 more than 2,000 affordable homes had been built and a further 3,476 homes committed. This amounts to about 17% of new housing supply in South Australia.

In NSW, inclusionary planning schemes only deliver affordable rental housing.

In the mid 1990s an inclusionary zoning scheme pilot was introduced to Pyrmont and Ultimo. This scheme was then extended to Green Square.

These schemes require that developers dedicate 0.8 to 3% of the floor area of developments for affordable housing, or that a monetary contribution be made in lieu of direct affordable housing provision.

However, to date, the NSW state government and many in the development sector have favoured voluntary mechanisms (such as density bonuses for providing affordable housing) over mandatory ones to supply affordable rental housing.

For our study, we estimated the volume of affordable housing delivered through voluntary planning agreements and state policy giving a density bonus for affordable housing inclusion by examining individual development approval records.

We found that voluntary measures have so far delivered about 1,300 dwellings or between 0.5 to 1% of Sydney’s housing supply between 2009 and 2017.

How viable is inclusionary planning?

We found that voluntary planning incentives can encourage affordable housing, but as part of incremental residential development, within the existing planning framework.

However, affordable housing should be mandated when land is rezoned for residential development, when planning rules are varied for particular projects, or following major infrastructure investment.

Inclusionary planning can’t replace government funding in providing housing for those on the lowest incomes. However, inclusionary planning schemes can reduce land costs and ensure that affordable homes are well located near jobs and services.

Authors: Nicole Gurran, Professor of Urban and Regional Planning, University of Sydney; Catherine Gilbert, Research Assistant and PhD Candidate, Urban Housing Lab, University of Sydney

The HIA has released a new report peddling the same old message. Just build more. This despite the fact that vacancy rates are rising, we have 150,000 new units coming on stream in the next year or so, and the root cause of the affordability problem is NOT population growth, but poor credit policy. You can read more about the truth about housing affordability here.

“Australia needs to build in more than 230,000 homes every year if we are to address our current housing affordability challenge,” stated Tim Reardon, HIA’s Principal Economist.

HIA has released a Report, “Housing Australia’s Future”, which presents a number of scenarios based on future population growth and wages growth to estimate the number of new homes required avoid exacerbating the housing affordability challenge.

“Over the past 15 years Australia’s housing market has been dominated by a persistent undersupply of housing – the underlying cause of the rapid acceleration in prices and ultimately Australia’s housingaffordability crisis.

“The excessive cost of supplying new housing lies at the core of the affordability challenge. This has been recognised by a number of key organisations including the RBA and the Productivity Commission; and federal and state Treasury’s have identified the supply of housing as the key problem.

“In 2016 Australia built a record number of 230,000 new homes and we will need to maintain this rate of annual supply for the next thirty years, if we are to meet future housing needs.

“The enormous pent up demand for housing in metropolitan areas is now being met and for the first time in 15 years the supply of new housing is in balance with the demand for new housing.

“Housing affordability will not be solved by amending negative gearing, capital gains tax or imposing punitive charges on foreign investors.

“Such measures increase taxation on housing and further raise the cost of new supply, which is already excessive and inefficient.

“Meaningful action needs to include all three tiers of government, working with industry, to ensure the delivery of affordable residential housing,” concluded Mr Reardon.

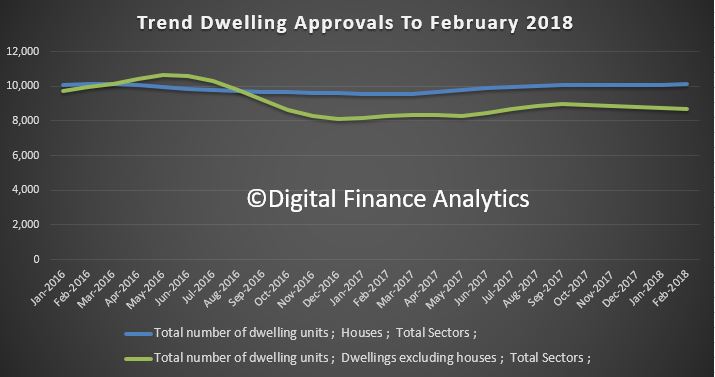

The number of dwellings approved in Australia fell for the fifth straight month in February 2018 in trend terms with a 0.1 per cent decline.

Approvals for private sector houses have remained stable at around 10,000 for a number of months. But unit approvals have fallen for five months.

Overall, building activity continues to slow from its record high in 2016. And the sizeable fall in the number of apartments and high density dwellings being approved comes at a time when a near record volume are currently under construction. If you assume 18-24 months between approval and completion, then we still have 150,000 or more units, mainly in the eastern urban centres to come on stream. More downward pressure on home prices.

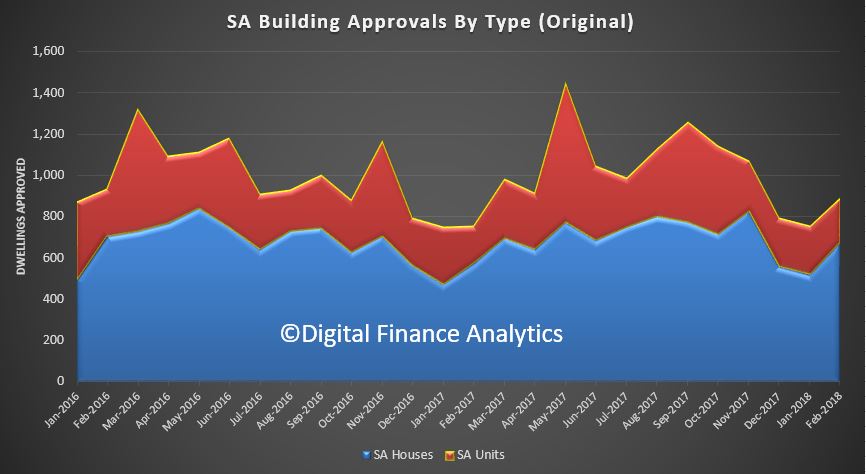

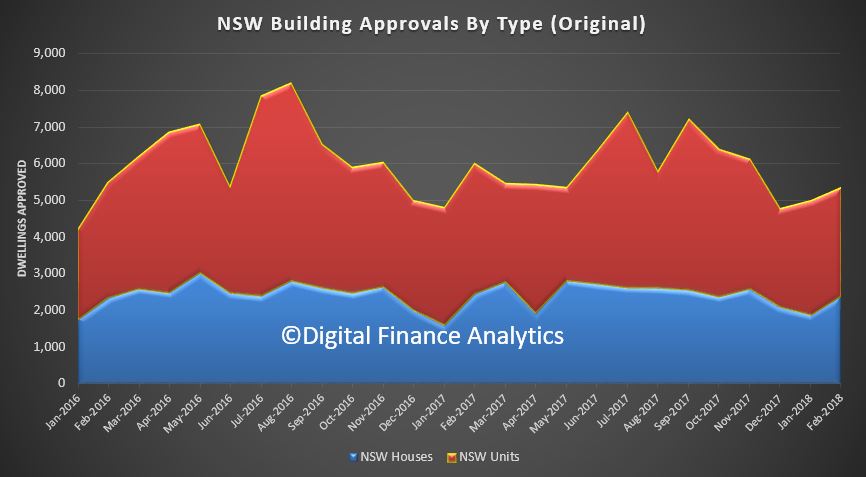

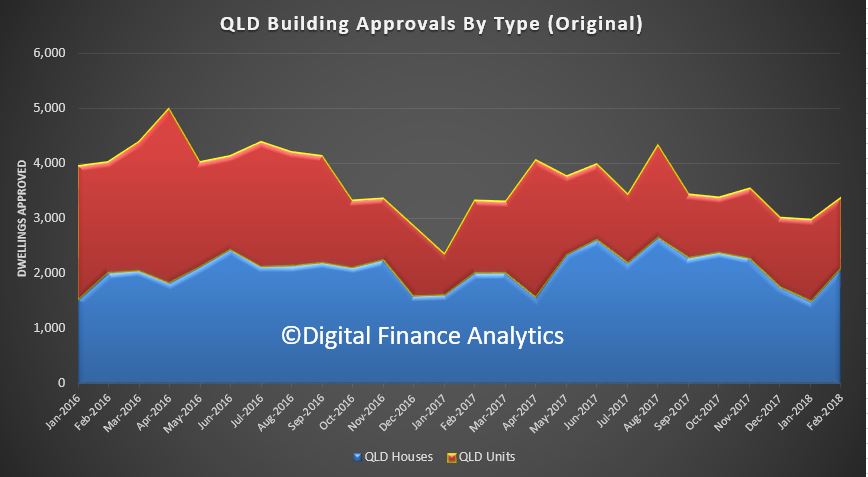

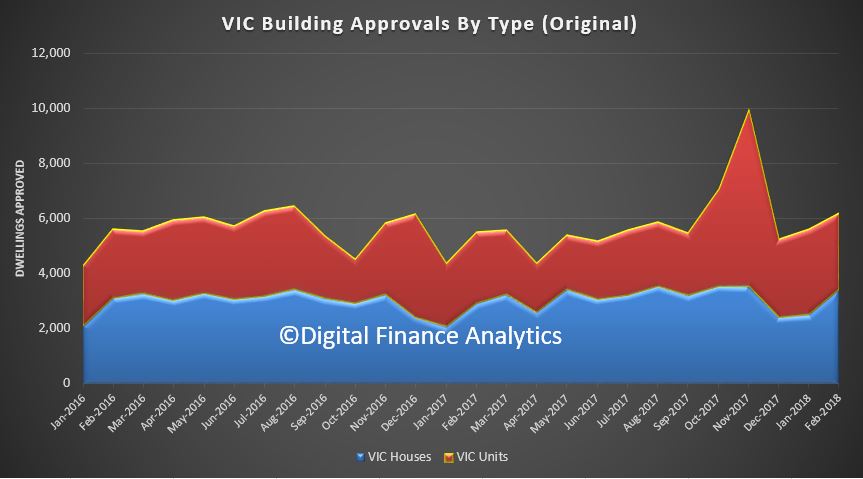

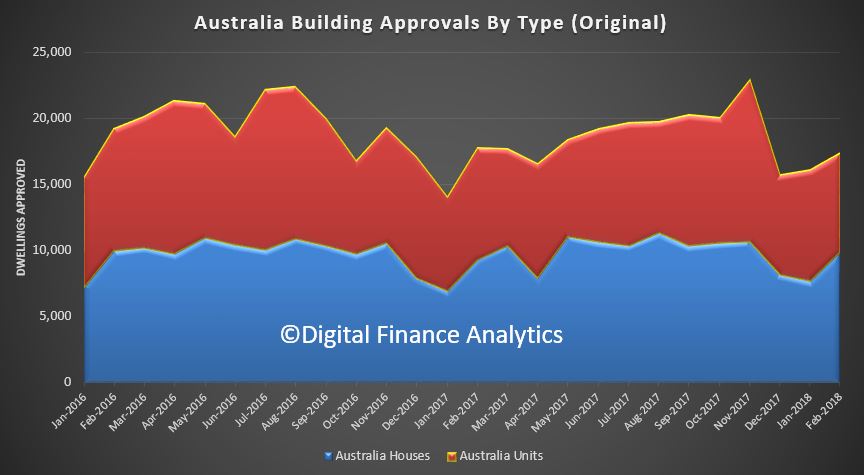

Here is the data displayed in original terms. Whilst house approvals remains relatively stable, unit approvals are more volatile. This is explained by the changing demand profile as overseas investors and local investment property purchasers retreat. As we discussed recently, this is thanks to tighter lending standards making mortgages more difficult to come by, lower capital growth making investment property less attractive, and stronger controls on overseas investors, both in terms of moving capital to purchase, and local regulations and tighter supervision.

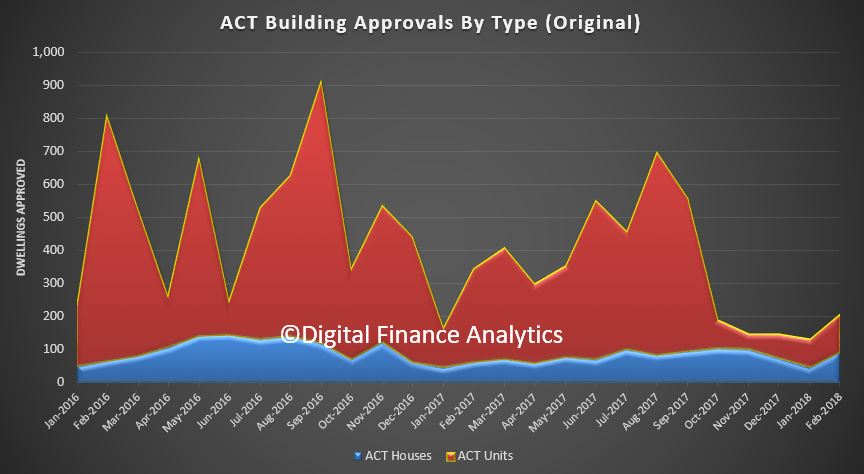

We can then look across the individual states, as there are significant variations. Among the states and territories, the biggest trend decrease in dwelling approvals in February was the Australian Capital Territory down 18.7 per cent,

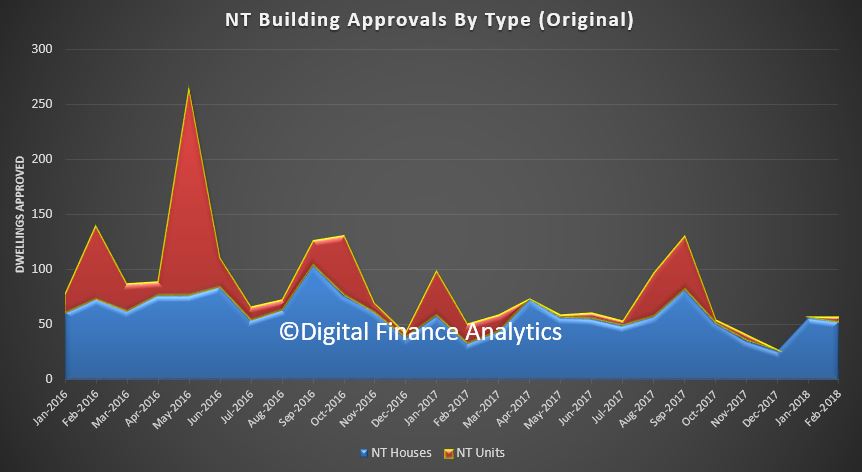

followed by the Northern Territory (down 7.2 per cent),

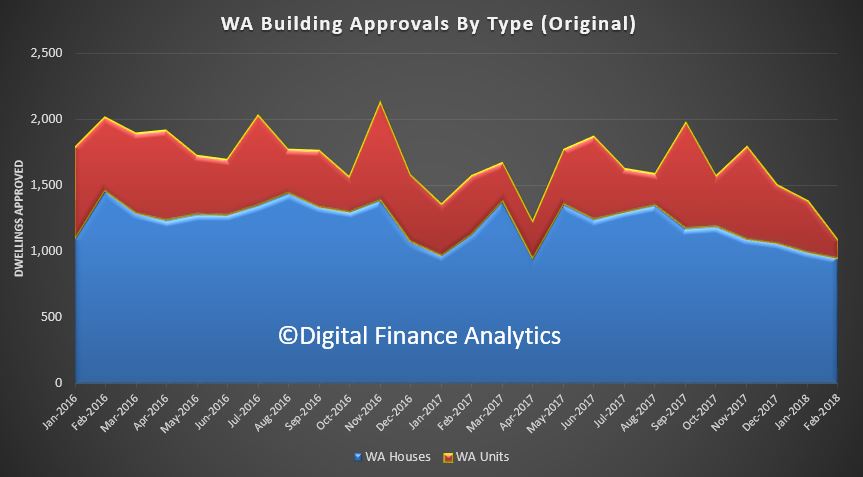

Western Australia (down 4.4 per cent),

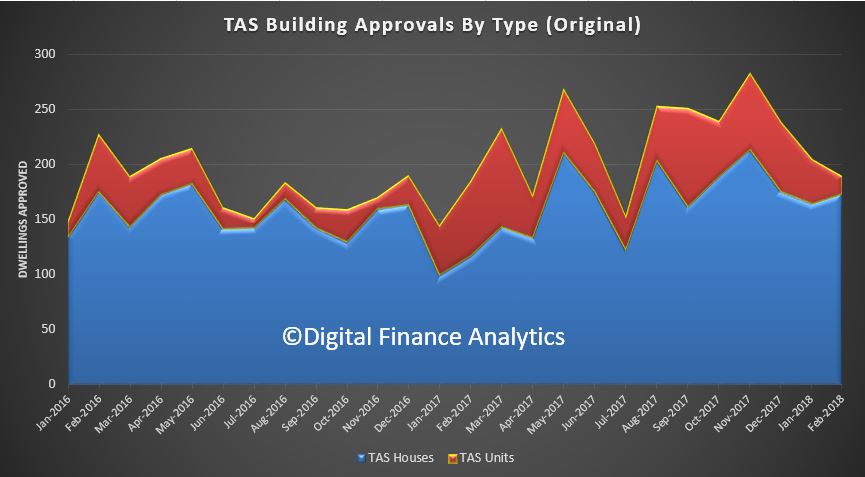

Tasmania (down 3.4 per cent)

and South Australia (down 1.2 per cent).

There were small increases in trend terms in New South Wales (1.0 per cent),

Queensland (0.9 per cent)

and Victoria (0.1 per cent).

Approvals for private sector houses rose 0.2 per cent in trend terms in February. Private sector house approvals rose in Victoria (1.1 per cent) and New South Wales (0.8 per cent), but fell in Queensland (1.1 per cent), South Australia (1.1 per cent) and Western Australia (0.5 per cent).

The value of total building approved fell 1.1 per cent in February, in trend terms, and has fallen for five months. The value of residential building fell 0.1 per cent while non-residential building fell 2.9 per cent.

Welcome to the Property Imperative Weekly to 31st March 2018.

Watch the video or read the transcript.

In this week’s review of property and finance news we start with the latest CoreLogic data on home price movements.

Looking at their weekly index, after last week’s brief lift, values fell 0.17% in the past week and as a result Sydney home values have now declined by a cumulative 4.2% over the past 29-weeks, with values also down 4.1% over the past 34 weeks. Sydney’s quarterly growth rate remains firmly negative, down 1.8% according to CoreLogic and annual growth is also down 2.2%.

More granular analysis shows the most significant falls in higher value property, and also in high-rise apartments. Our own analysis, and feedback from our followers is that asking prices are falling quite consistently now, and the same trend is to be see in Brisbane and Melbourne, our largest markets. This despite continued strong migration. We see two trends emerging, more people getting desperate to sell, so putting their property on the market, and having to accept a deeper discount to close a sale.

As we showed this week in our separate videos on the latest results from our surveys, down traders in particular are seeking to release capital now, and there are more than 1 million who want to transact. On the other hand investors are fleeing, though some are now also being forced to sell thanks to the switch from interest only to more expensive principal and interest loans.

This is all consistent with the latest auction results, which Corelogic also reported. They said that volumes last week broke a new record with 3,990 homes taken to auction across the combined capital cities in the lead up to Easter, which exceeded the previous high of 3,908 over the week ending 30th November 2014. The preliminary clearance rate was reported at 65.5%, but the final auction clearance rate fell to 62.7 per cent last week, down from 66.0 per cent across 3,136 auctions the previous week. Over the same week last year, 3,171 auctions were held, returning a significantly stronger clearance rate (74.5 per cent).

CoreLogic said that Melbourne’s clearance rate last week was 65.8 per cent across 2,071 auctions, making it the busiest week on record for the city. In comparison, there were 1,653 auctions held across the city over the previous week, returning a clearance rate of 68.7 per cent. This time last year, 1,607 homes were taken to auction, and a clearance rate of 78.9 per cent was recorded. Sydney was host to 1,383 auctions last week, the most auctions held across the city since the week leading up to Easter 2017 (1,436), while over the previous week, 1,093 auctions were held. The clearance rate for Sydney fell to 61.1 per cent, down from 64.8 per cent over the previous week, while this time last year, Sydney’s clearance rate was a stronger 75.8 per cent.

Across the smaller auction markets, auction volumes increased week-on-week, however looking at clearance rates, Adelaide (64.6 per cent) and Canberra (69.1 per cent) were the only cities to see a slight rise in the clearance rate over the week.

The Gold Coast region was the busiest non-capital city region last week with 87 homes taken to auction, while Geelong recorded the highest clearance rate at 79.7 per cent across 75 auctions.

Given the upcoming Easter long weekend, auction volumes are much lower this week with only 540 capital city auctions scheduled; significantly lower than last week when 3,990 auctions were held across the combined capital cities.

The next question to consider is the growth in credit. As we discussed in a separate blog, credit for housing, especially owner occupied mortgages is still running hot. The smoothed 12 months trends from the RBA, out last Thursday, shows annualised owner occupied growth registering 8.1%, up from last month, investor lending falling again down to 2.8% annualised, and business credit at just 3.6%

Looking at the relative value of lending, in seasonally adjusted terms, owner occupied credit rose 0.71% to $1.15 trillion, up $8.08 billion, while investment lending rose 0.12% to $588.3 billion, up just 0.69 billion. Business lending rose 0.17% to $905 billion, up 1.55 billion and personal credit fell 0.15%, down 0.22 billion to $152.2 billion.

Note that the proportion of investment loans fell again down to 33.9%, and the proportion of business lending to all lending remained at 32.4%, and continues to fall from last year. In other words, it is owner occupied housing which is driving credit growth higher – if this reverses, there is a real risk total credit grow will run into reverse. Again, we see the regulators wishing to continue to drive credit higher, to support growth and GDP, yet also piling on more risks, when households are already terribly exposed. They keep hoping business investment and growth will kick in, but their forward projections look “courageous”. Remember it was housing consumption and Government spending on infrastructure which supported the last GDP numbers, not business investment.

Now, let’s compare the total housing lending from the RBA of $1.74 trillion, which includes the non-banks (though delayed, and partial data), with the APRA $1.61 trillion. The gap, $130 billion shows the non-bank sector is growing, as historically, the gap has been closer to $110 billion. This confirms the non-bank sector is active, filling the gap left by banks tightening. Non-banks have weaker controls on their lending, despite the new APRA supervision responsibilities. This is an emerging area of additional risk, as some non-banks are ready and willing to write interest only and non-conforming loans, supported by both new patterns of securitisation (up 13% in recent times) and substantial investment funds from a range of local and international investors and hedge funds.

Once again, we see the regulators late to the party. This continues the US 2005-6 playbook where non-conforming loans also rose prior to the crash. We are no different.

The ABS released more census data this week, and focussed on the relative advantage and disadvantage across the country. Ku-ring-gai on Sydney’s upper north shore is Australia’s most advantaged Local Government Area (LGA). Another Sydney LGA, Mosman, which includes the affluent suburbs of Balmoral, Beauty Point and Clifton Gardens, has also been ranked among the most advantaged. In fact, SEIFA data shows the 10 most advantaged LGAs in Australia are all located around the Northern and Eastern areas of Sydney Harbour and in coastal Perth.

The most disadvantaged LGA is Cherbourg, approximately 250 kilometres north-west of Brisbane (QLD), followed by West Daly (NT). The 10 most disadvantaged LGAs in Australia can be found in Queensland and the Northern Territory.

The latest data has found that more than 30 per cent of people born in China, South Africa and Malaysia live in advantaged areas and less than 10 per cent reside in disadvantaged areas. Meanwhile, 40 per cent of Vietnamese-born live in disadvantaged areas and only a small proportion (11 per cent) live in advantaged areas.

People of Aboriginal and/or Torres Strait Islander origin are more likely to live in the most disadvantaged areas with 48 per cent living in the bottom fifth most disadvantaged LGAs, compared to 18 per cent of non-Indigenous people. Overall, only 5.4 per cent of Aboriginal and/or Torres Strait Islander people live in areas of high relative advantage compared with 22 per cent of non-Indigenous people.

What the ABS did not show is that there is a strong correlation of those defined as advantaged to valuable real estate – home price rises have both catalysed the economic disparities across the country, and of course show the venerability that more wealthy areas have should home prices fall further. The paper value of property is largely illusory, and of course only crystallises when sold.

The HIA reported that new home sales declined for the second consecutive month during February 2018 overall, but the markets were patchy, based on results contained in the latest edition of their New Home Sales report – a monthly survey of the largest volume home builders in the five largest states.

Despite the fact that the overall volume of sales declined during February, reductions only occurred in two of the five states covered by the HIA New Home Sales Report – the magnitude of these reductions outweighed the increases which took place elsewhere. The largest fall was in Queensland (-16.3 per cent) with a 9.9 per cent contraction recorded in WA. The largest increase in sales was in NSW (+11.7 per cent), followed by SA (+10.3 per cent) and Victoria (+4.8 per cent).

Finally, we walked through our survey results in a series of separate videos, but in summary, the latest release of the Digital Finance Analytics Household Survey to end March 2018, helps to explain why we think home prices are set to fall further by drawing on our 52,000 sample, from across Australia.

This chart, which looks across our property segments, shows that both portfolio property investors (who hold multiple properties) and solo investors (who hold one, or perhaps two) intentions to transact are tanking, down 8% since December 2017. This is because credit is less available, capital growth has stalled, and in fact only the tax breaks remain as an incentive! This decline started in 2015, but is accelerating. Remember that around one thirrd of mortgages are for investment purposes, so as this demand dissipates, the floor on prices starts to shatter.

Whilst there are offsetting rises from down traders (who are seeking to release capital before prices fall further) and first time buyers (who are being “bribed” by first owner grants) there is a significant net fall in demand. This pattern is seen across the country, but is most prevalent in our two biggest markets of Sydney and Melbourne.

Refinancing is up a little, thanks to the attractive discounts being offered by many lenders, and the prime driver is to reduce monthly repayments, as currently household finances are under pressure. We release the latest mortgage stress analysis in a few days.

And if you want to think about the consequences of all this, then watch our commentary on the Four Scenarios which portrays how the property and finance sector may play out, and compare the comments from APRA with those in Ireland in 2007 in our latest video blog – they are eerily similar, and we all know what happened there!

The outlook for finance and property in Australia in decidedly uncertain.

Governments can encourage more affordable housing by targeting first home buyer subsidies to specific locations and housing types, a new report finds. It also suggests incentivising developers and builders to create smaller houses with more cost-efficient designs.

The report is based on the housing market in Perth, Western Australia, and shows that historically building single houses as opposed to units or town houses is a more effective way of delivering affordable housing on the city fringes.

The report examined housing affordability through individual transaction records over a six year sample period. It compared prices between established and new housing, showing that new land and building developments play important roles in supplying affordable housing options.

New dwellings comprise 13% of single house transactions and 33% for dwellings such as apartment or townhouses. Although new dwellings like apartments provided some affordable housing options, in general they are selling at a premium over existing houses.

Australia’s largest cities, like Perth, are stretched to the limit of land supply and infrastructure for affordable housing. The most infrastructure exists in city centres where houses are expensive.

Over the past two decades Perth has grown rapidly. Between 2001 and 2016 the population increased by 46.7%, the largest proportional increase of any Australian capital city. The make-up of the housing market is similar to other capitals: 68% of the housing stock is single houses, 20% other dwellings and 11% vacant.

Levels of home ownership are generally consistent with the national pattern: 62% of housing is owned outright or mortgaged, and 24% rented.

House prices have grown rapidly. From 1999 to 2016 house prices grew at an average annual rate of 8.4%; other dwellings grew 9%. Both sectors report the highest annual increases for all Australian capital cities over this period.

How can governments help?

The challenge in Australia’s housing market is supplying an adequate range of affordable new dwelling types within a range of suitable locations – both inner city and outer suburban choices.

Clusters of cheaper housing on the urban fringe and more expensive inner-city development suggest new building activity is confined to specific locations. These are defined by the price the constructor or buyer is willing to pay.

Housing policy in Australia has relied on market outcomes to determine aesthetic and economic characteristics of housing in our cities. Government intervention has mainly been through zoning, predominantly at local levels. More recently there’s also been stimulus at state and federal levels for first home buyers through various deposit subsidy schemes.

Subsidy schemes have been important in helping first home buyers bridge the deposit gap. Incentives have included cash payments and stamp duty relief.

In some states additional payments have been made for new building and for purchases in specific locations. But the Perth study indicates that some of these subsidies are becoming ineffective.

Standard “one type fits all” subsidies are limiting first home buyers’ choices of location and housing type.

The solution to this problem is to make subsidy schemes more flexible to nudge first home buyers towards affordable locations. This would even out the supply of affordable houses from areas where housing is densely clustered in certain locations.

Policy would also need to take into account the needs of different demographics in certain locations. Housing requirements of young singles are obviously different than for young families.

Effective policy would also need to take into account the types of housing finance available for first home buyers. One example is the WA government’s Keystart loans which help eligible people to buy their own homes through low deposit loans and shared equity schemes.

These types of schemes include shared ownership with the government owned housing authorities and include existing and newly built homes in a variety of locations.

But it’s not all up to state governments. The problems of lack of land supply and infrastructure are the same in all Australian capital cities. The federal government could play a more prominent role through infrastructure grant funding in changing the location choice of buyers and variation of affordable housing types at a national level.

Author: Greg Costello, Associate Professor, Curtin University

We can then look across the individual states, as there are significant variations. Among the states and territories, the biggest trend decrease in dwelling approvals in February was the Australian Capital Territory down 18.7 per cent,

We can then look across the individual states, as there are significant variations. Among the states and territories, the biggest trend decrease in dwelling approvals in February was the Australian Capital Territory down 18.7 per cent,