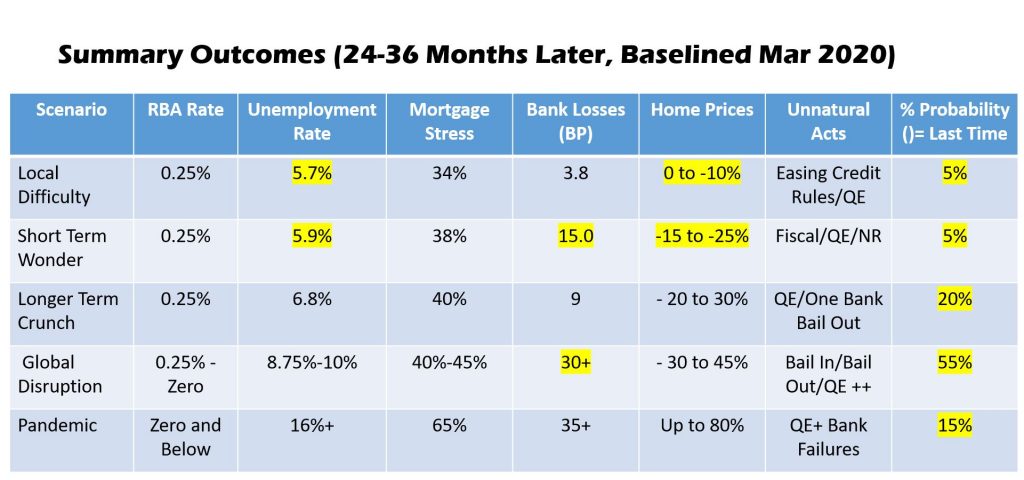

We have updated our scenarios, driven from our core market models.

The drivers are rising unemployment, and business failure thanks to the impact of the virus. We discussed these scenarios in our live stream event last night. This is the full version with live chat. The show starts formally at 32 minutes.

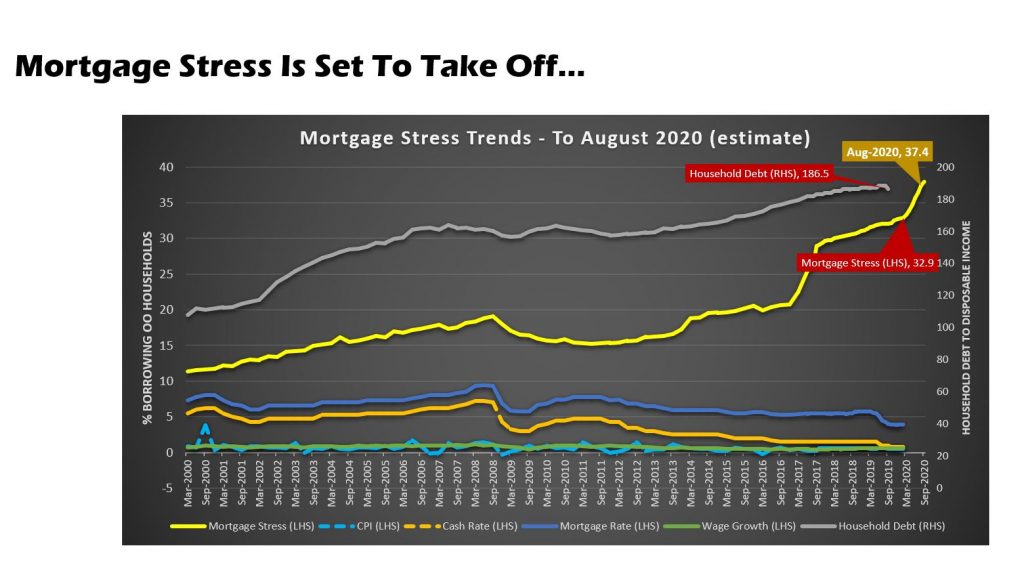

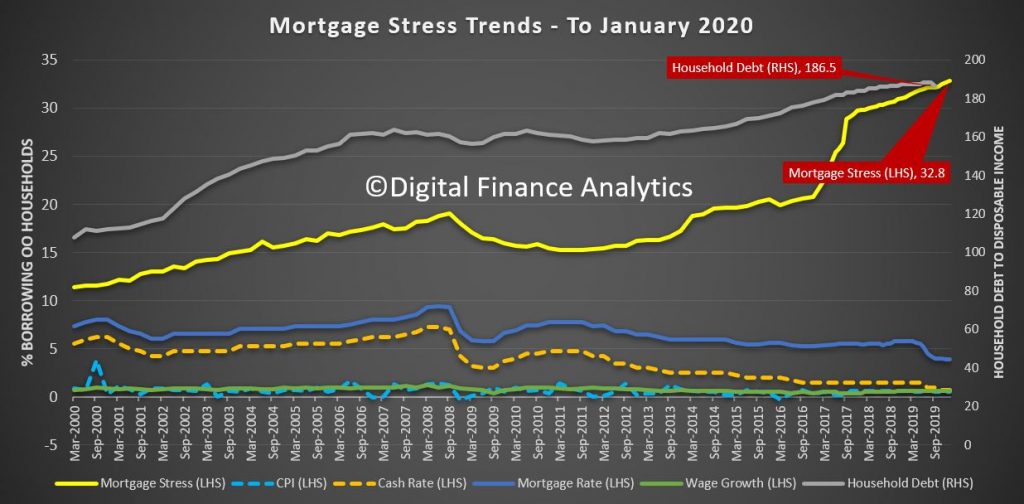

We estimate that mortgage stress is set to rise significantly in the months ahead as household cash-flows are interrupted.

Alternatively we have also released a shorter edited version, without chat here:

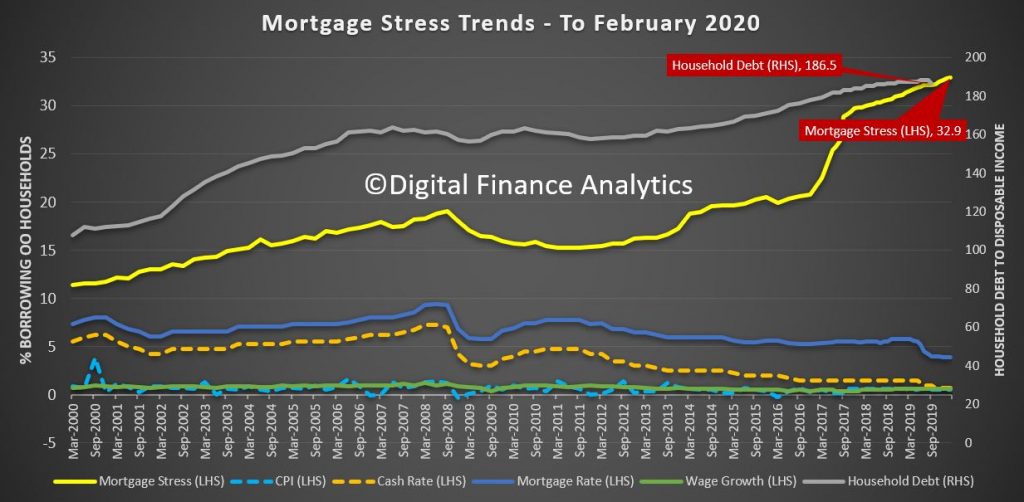

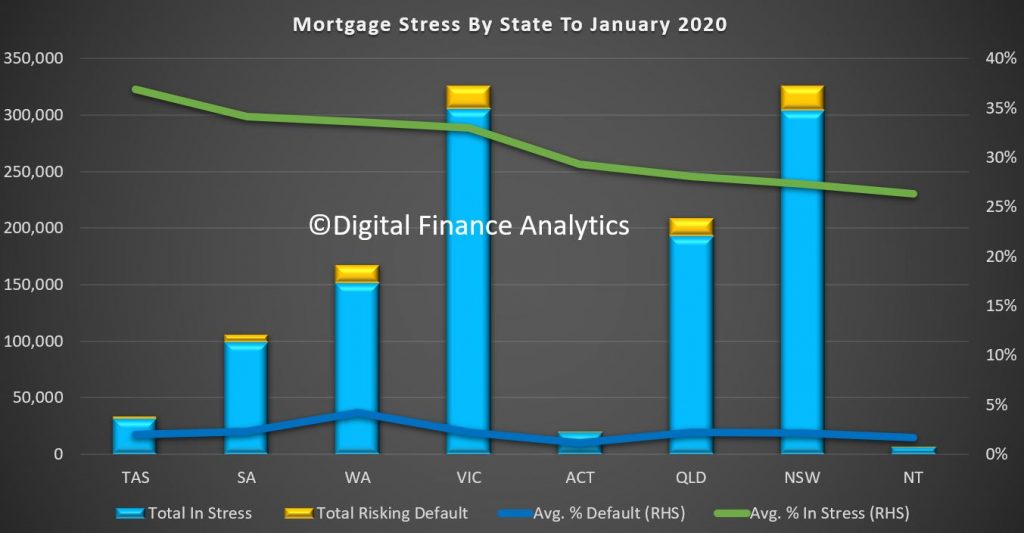

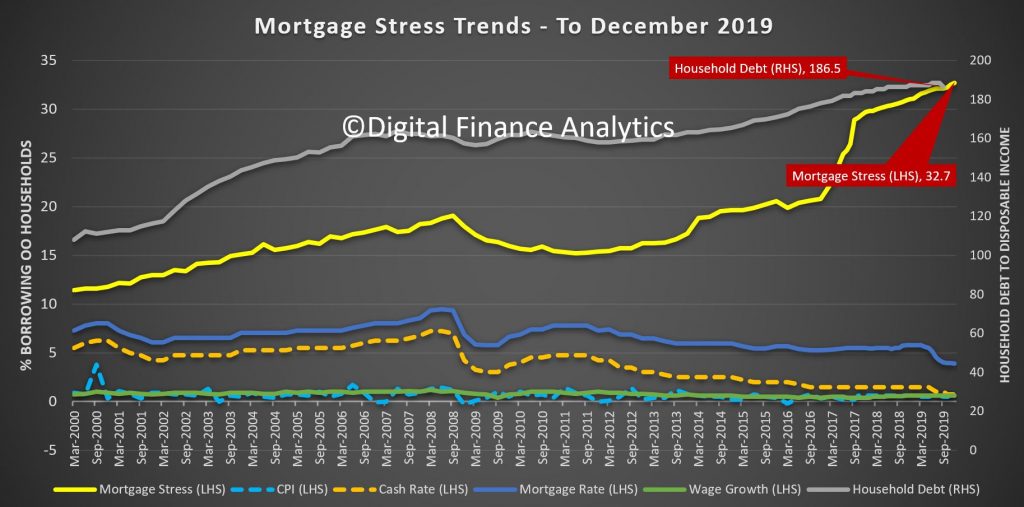

The official story is that lower interest rates are translating to reduced financial stress in the community. The true story, as revealed in the latest edition of our mortgage stress analysis is that more households are up against it, with a record 32.9% of mortgages households wrestling with cash flow issues. This translates to 1.08 million households in stress, and more than 82,000 risking default in the months ahead.

Many households are chasing their tails, in that while mortgage repayments are dropping – for some, rising living costs and flat real incomes are compounding their financial pressures. There was a sharp downturn in take home pay, thanks to bushfires and the virus is beginning to hit businesses, (who in turn are less able to pay and retain staff, especially those on “flexible” contracts).

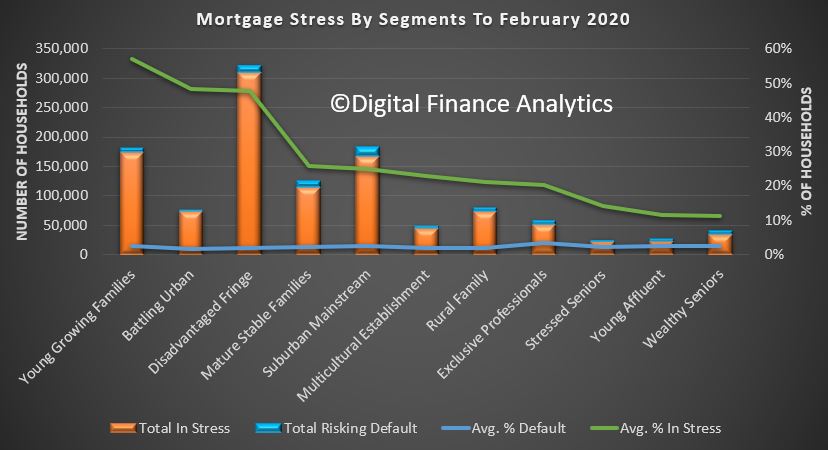

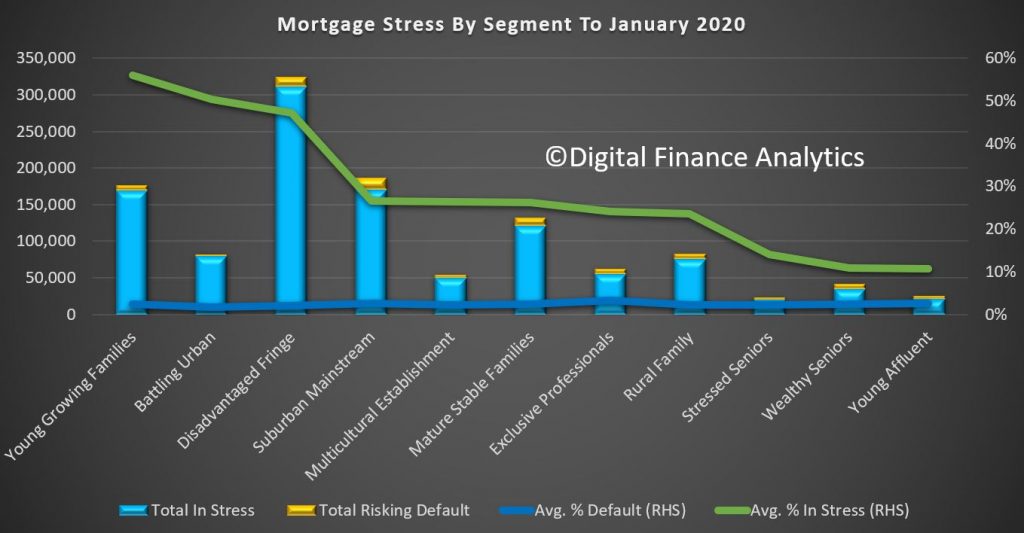

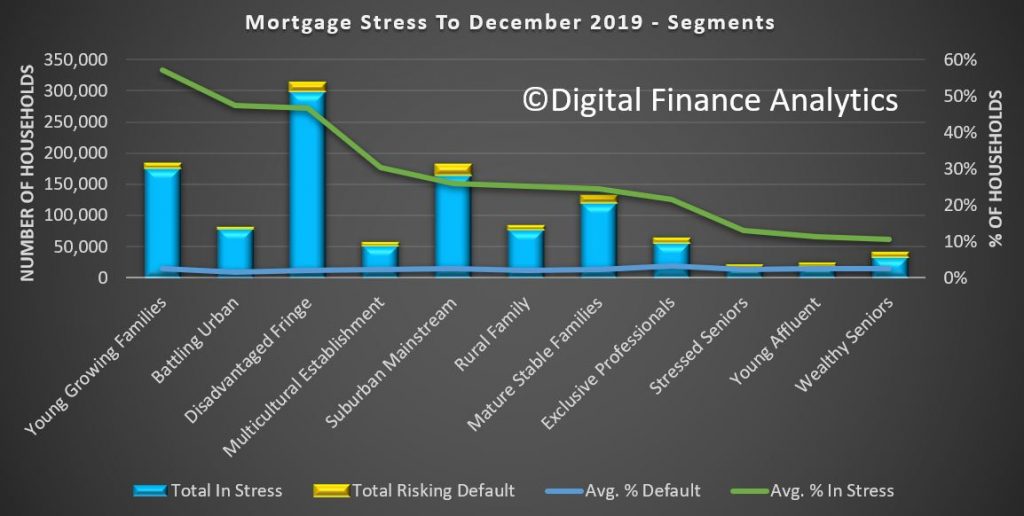

Across our master household segments, the highest proportion of households under pressure are “Young Growing Families”, which includes many recent first time buyers, “Battling Urban” – those older households living in the main urban corridors, and “Disadvantaged Fringe” households, those living in the often new fringe developments are also at the top of the list. That said, stress takes no prisoners, in that even some wealthy households, and more mature families are also under pressure.

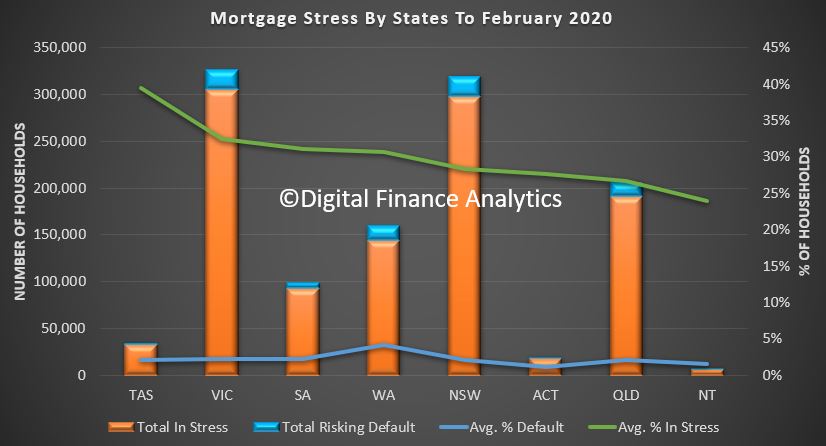

Across the states, the highest proportion of households are in Tasmania, where the recent run up in prices, against high costs and low wages is a nasty cocktail. As yet though defaults remain low here. Western Australia has a significantly higher level of defaults, because the financial pressures have been running for years. The largest counts of stressed households are located in Victoria and New South Wales, with Queensland also seeing a further rise. Defaults are expected to rise again.

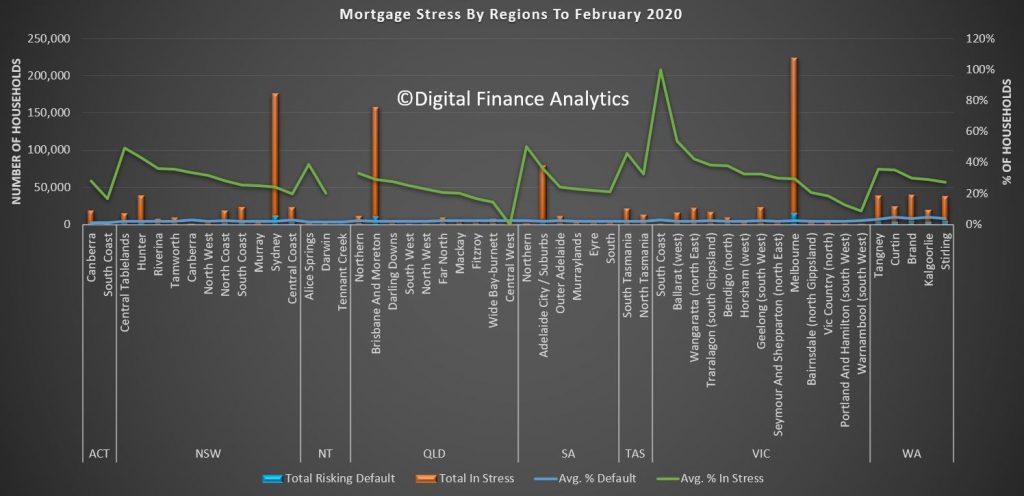

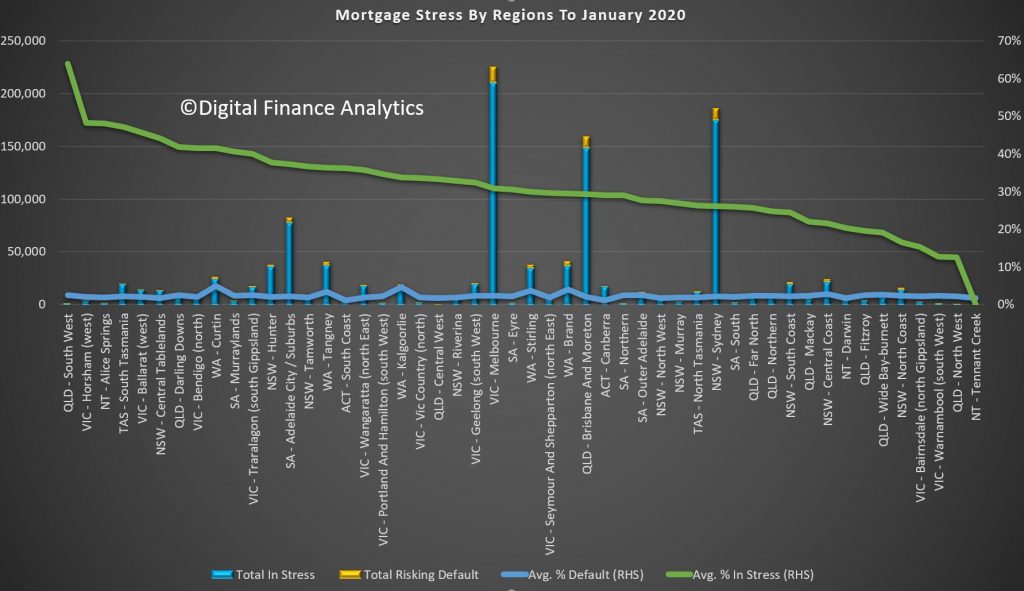

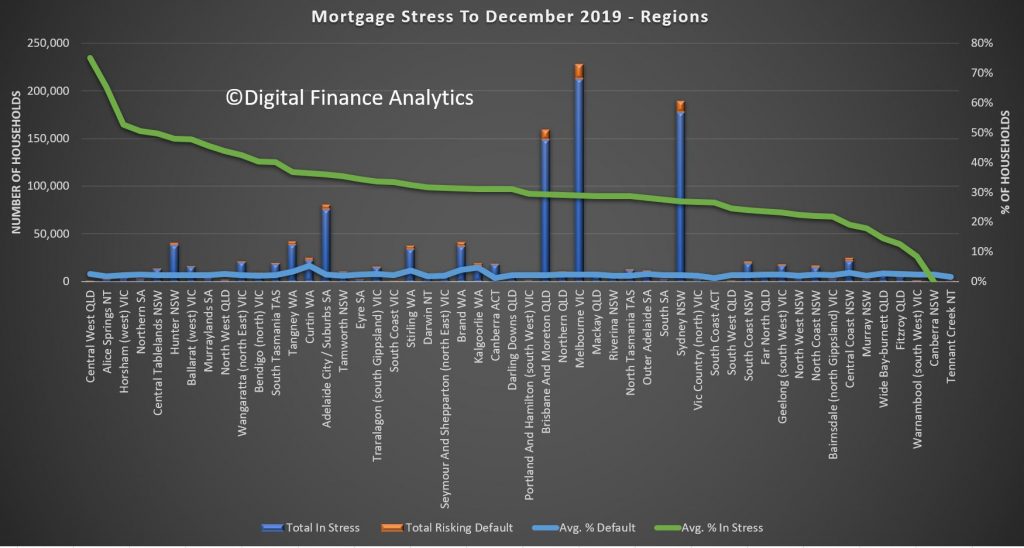

Across the regions, there are considerable variations, with a significant spike in some areas following the recent bushfires.

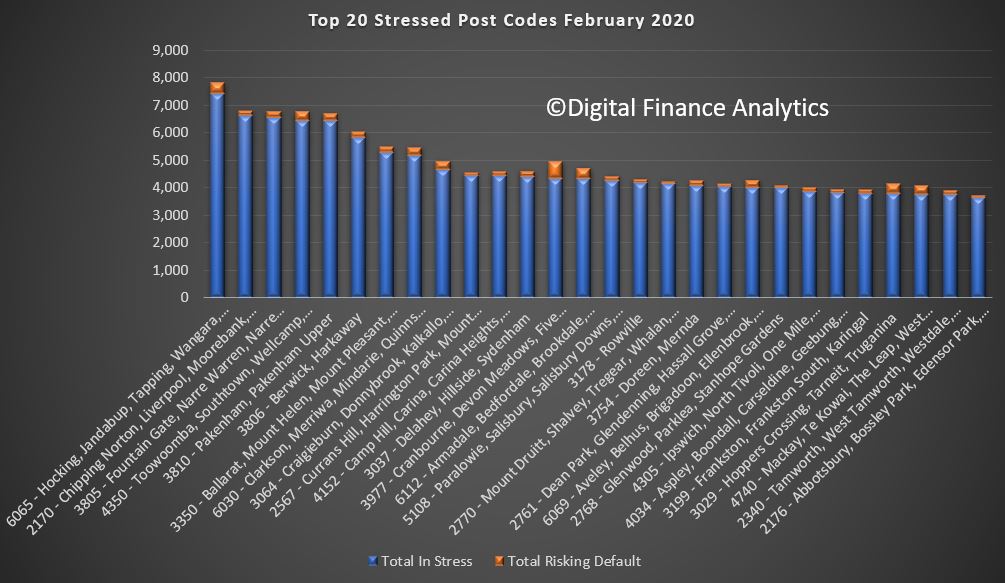

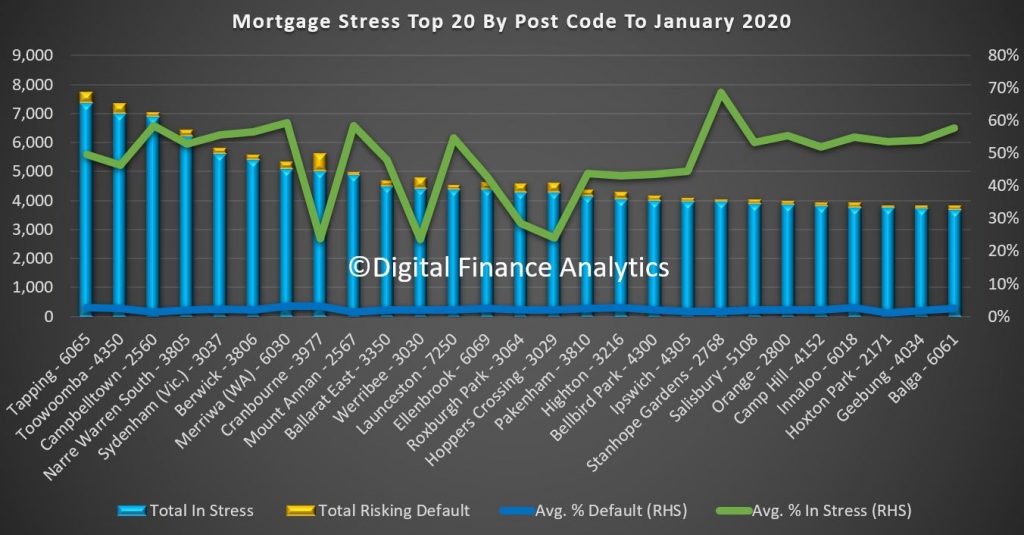

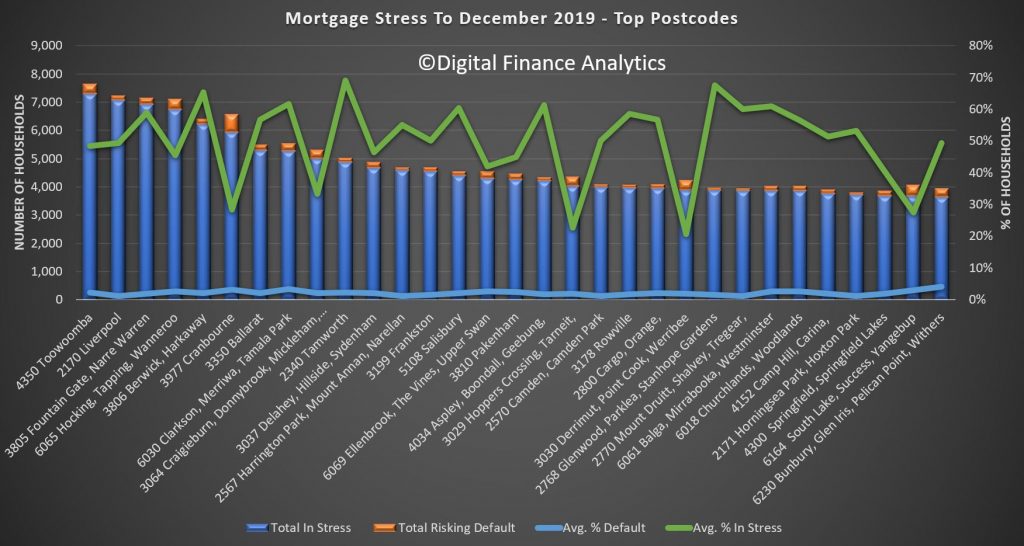

The top 20 post codes reveals that WA post code 6065 which includes Tapping and Hocking tops the list this month, with more than 7,000 households impacted. Liverpool, 2170, in New South Wales, Narre Warren 3805 in Victoria and Toowoomba 4350 in Queensland are all at the top of the list. The common theme here is significant and recent higher density development, large mortgages and over priced real estate (and supported by insufficient infrastructure).

As always we remind households that maintaining a cash flow record is an essential tool to managing a household budget – there are good tools available on ASIC’s Money Smart Web Site. Less than half of the households surveyed know their financial status. Careful prioritisation, and repaying higher interest debts first often makes the most sense, especially when wages growth will remain sluggish (and before the economic impact of the virus really hits). Finally, refinancing may provide short term relief, but without a change in behaviour this will not be long lasting.

The ACCC just released their 21st report into the Private Health Insurance Sector, which analyses key competition and consumer developments and trends in the private health insurance industry to 30th June 2019 that may have affected consumers’ health cover and out-of-pocket expenses. This report also continues the ACCC’s focus on adequate private health insurer communications to their consumers, including on detrimental policy changes, as well as potential emerging issues in the use of consumer data.

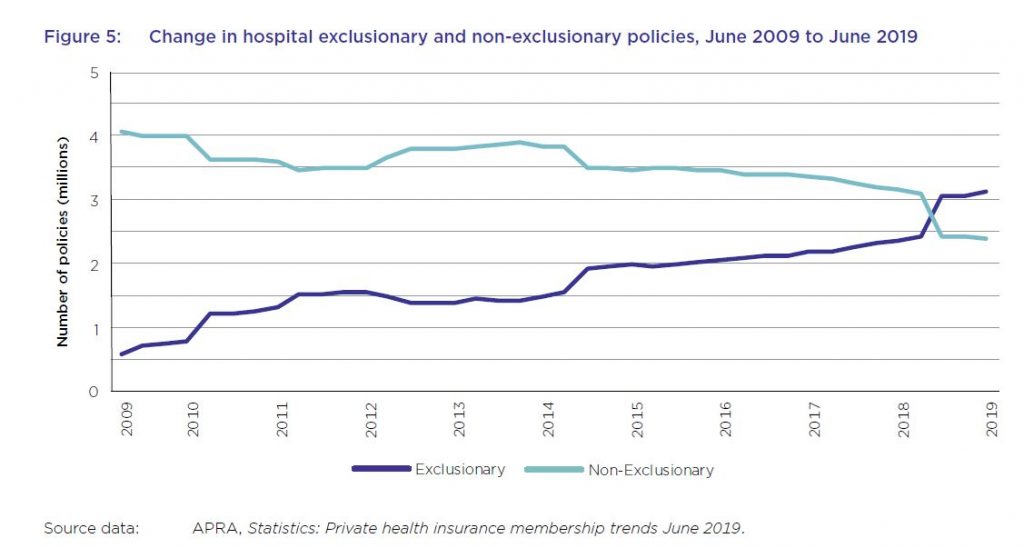

And in summary the system is unwell. Private health insurance premiums rise faster than income despite growing exclusions. For the first time, the majority of hospital treatment policies held by Australians now contain exclusions with more than 57 per cent of policies containing exclusions, up from about 44 per cent in the previous year. This chimes with our household surveys which shows more younger people are jettisoning their policies, or not signing up in the first place. This is a wicked problem, as more sick people as a total proportion are within the system, meaning that costs are becoming more concentrated.

Plus, the ACCC notes that consumer data collected by private health insurers and other businesses, for example through wellbeing apps and rewards schemes, can be used for a number of purposes such as targeted marketing, including from third parties.

Key industry data used and relied upon by the ACCC includes industry statistics and data collected by the Australian Prudential Regulation Authority (APRA) and private health insurance complaints data from the Private Health Insurance Ombudsman (PHIO).

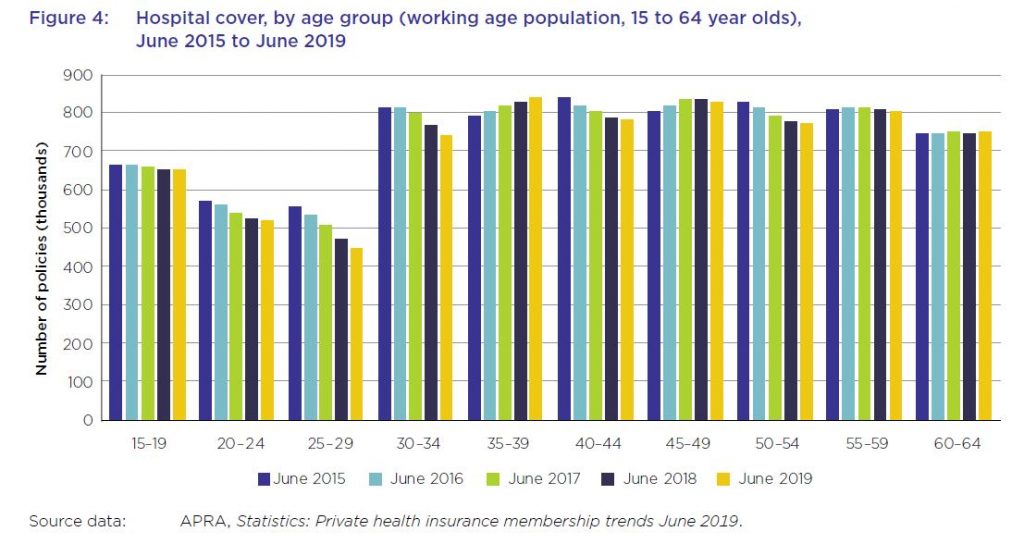

As at 30 June 2019, 13.6 million Australians, or 53.6 per cent of the population, had some form of private health insurance. This represents a membership reduction of 0.6 per cent from June 2018 (54.2 per cent). The Australian population grew by 396 722, or almost 1.6 per cent, during this period. The decline is sharpest among younger age groups.

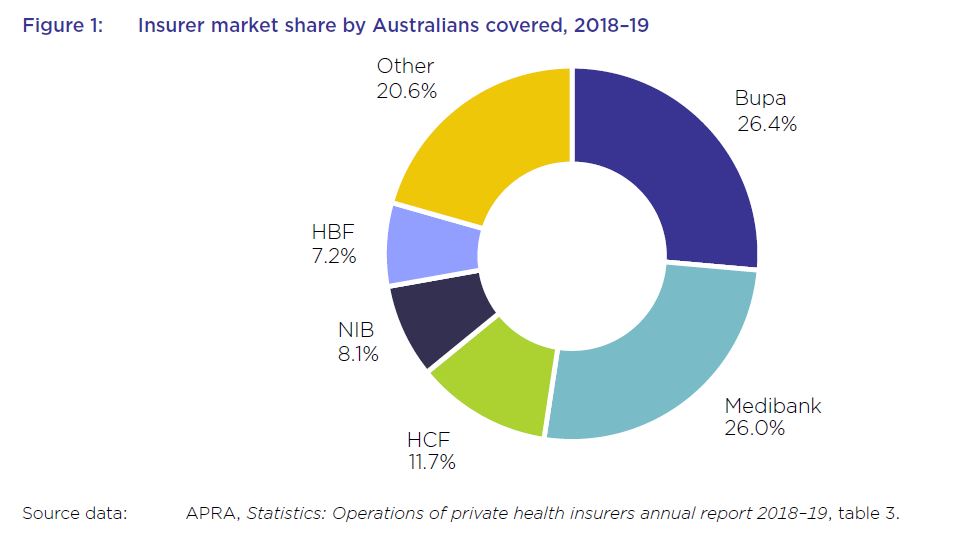

The five largest health insurers have a combined market share of almost 79.5 per cent and contributed to almost 77.5 per cent of total health fund benefits paid in 2018–1915, with Bupa and Medibank contributing 26.7 per cent and 25 per cent respectively.

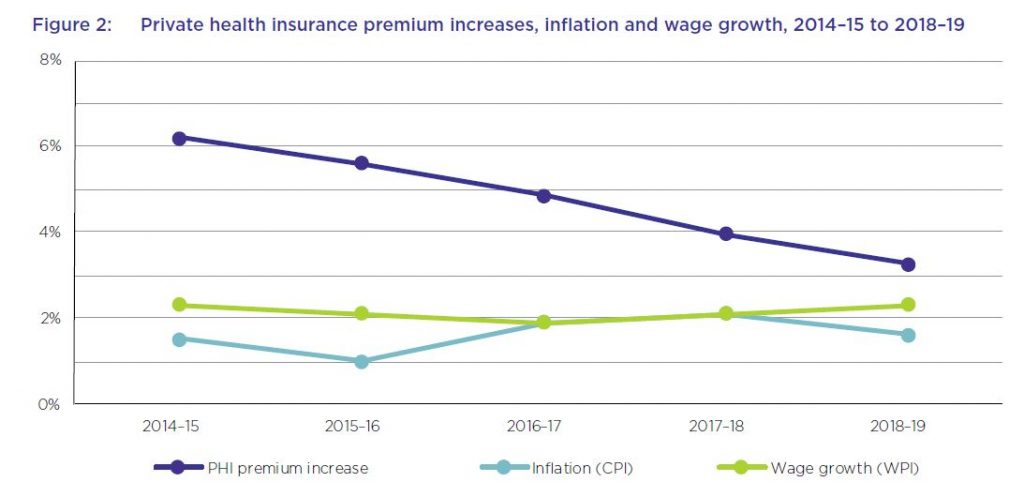

The average premium increase of 4.8 per cent per year over this period has been higher than the average annual growth in the wage price index (2.1 per cent) and the consumer price index (1.6 per cent) over the same period. While the rate of the average yearly premium increases has been decreasing each year over the past five years, and was 3.25 per cent in 2018–19, the average industry premium change for 2020, to take effect on 1 April 2020, will be 2.92 per cent – still well above wages growth.

From June 2018 to June 2019, the proportion of hospital policies held with exclusions increased by almost 14 per cent. For the first time, the majority of policies held now have exclusions.

The number of exclusionary policies held increased by over 650 000 from June 2018 to September 2018, with an equivalent reduction in non-exclusionary policies during the same period. APRA’s statistics did not indicate the reasons for this rise in the number of exclusionary policies during the reporting period. However, analysis by Silvester and others has suggested that less expensive exclusionary policies may appeal both to existing policyholders whose policies have become unaffordable, as well as to young people buying health insurance to avoid LHC loading and the Medicare levy surcharge.

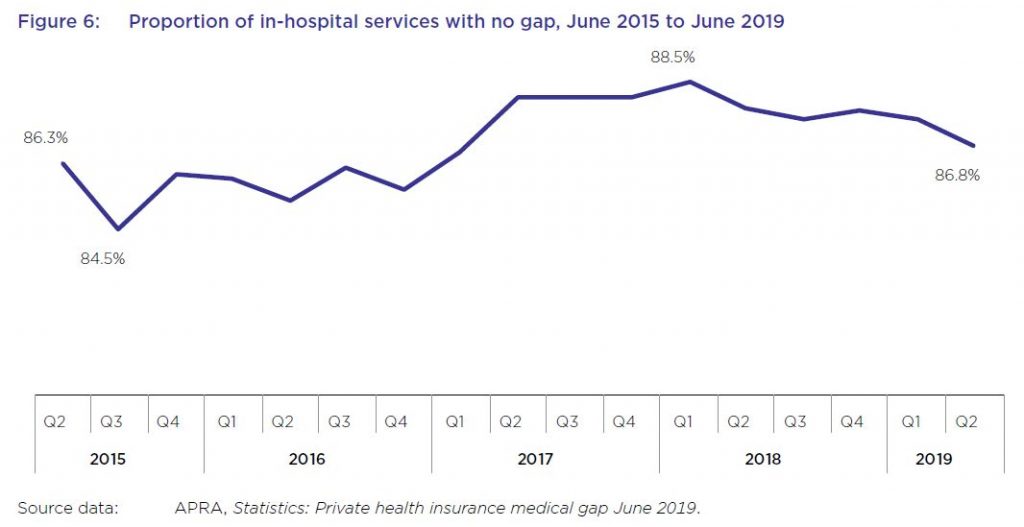

While most in-hospital services are delivered with no gap payments required from patients, this rate has varied in recent years, from a low of less than 85 per cent of services not requiring a gap payment in September 2015, to almost 89 per cent in March 2018, before falling again to under 87 per cent in June 2019.

From June 2018 to June 2019, the average gap expense incurred by a consumer for hospital treatment was $314.51, an increase of 1.9 per cent from the previous year, as shown in table 8. Average gap payments for extras treatment increased by almost 4 per cent to $49.20 over the same period.

A YouGov survey from late 2019 found that, after the cost of premiums and a perceived lack of value for money, out-of-pocket costs were a leading reason given by respondents for no longer holding private health insurance.

Several health insurers offer rewards schemes for their members, some of which involve the use of fitness tracking apps and devices to record activities such as steps and sleep. Some of these apps operate in conjunction with companies other than health insurers. For example, the health insurers MO Health and GMHBA are both partnered with the life insurer AIA Australia Limited, and use the AIA Vitality program issued by AIA.

HCF has also entered into a partnership with Flybuys where new HCF members can collect Flybuys points based on their annual health cover premiums. Qantas, which offers health insurance issued by NIB, also offers frequent flyer points for members who download the Qantas Wellbeing app and undertake certain activities. Its Qantas Wellbeing Program Terms and Conditions state that members must link a tracking device to record their physical activity, and that as members, they consent to Qantas: “collecting, using and disclosing any personal information including health and Wellbeing information submitted by the Member through joining or use of the Wellbeing Program or collected by Qantas through the Tracking Device or the Qantas Wellbeing App”.

Although Australians can receive benefits from rewards and discounts offered by health insurers and other organisations that collect consumer data, the ACCC is concerned that few consumers are fully informed of, fully understand, or can effectively control, the scope of data collected when they sign up for, or use, such services.

While the community rating system for private health insurance in Australia prohibits insurers from charging different private health insurance premiums to individual consumers based on health and other factors, the ACCC notes that the consumer data collected by wellbeing apps and rewards schemes could be used for a number of other purposes, including for targeted marketing (including from third parties), and potentially to create insights that could be shared with or sold to third parties.

The system will continue to be under pressure – and we think the model is frankly broken.

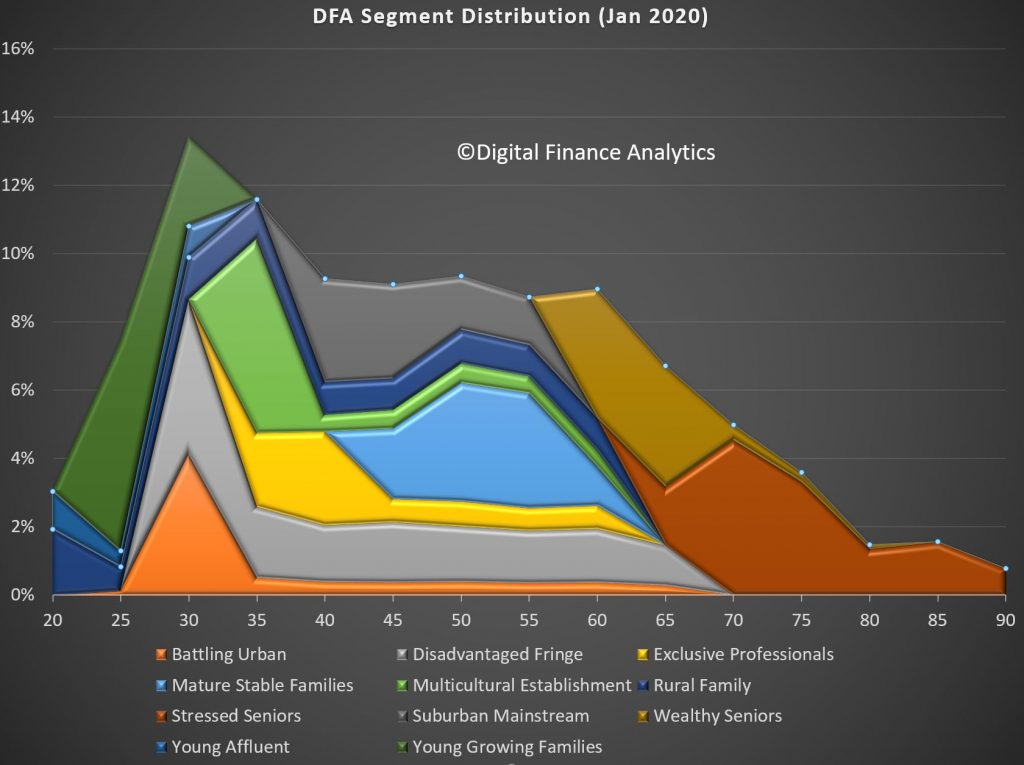

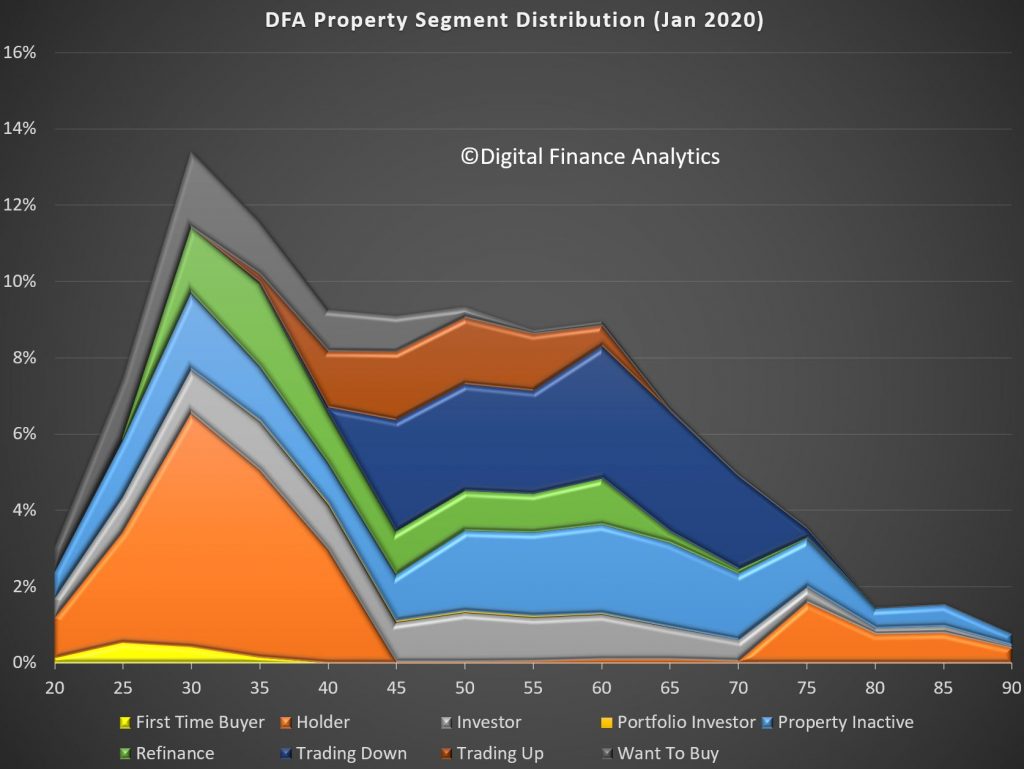

In response to a question, we are publishing a couple of analytic slides which shows the relationship between DFA household and property segments and age bands.

Our segments are derived from multi-factorial analysis but do have an age related dimension also. You can read more here.

The latest results from our household surveys to end the end of January reveals that mortgage stress continues to push higher with 32.8% of households now impacted, representing more than 1.1 million borrowing households. In addition expectations of defaults are up to more than 83,400 over the next 12 months.

These results are of no surprise, given the ongoing pressure on incomes and rising costs, despite somewhat lower mortgage rates for some borrowers. The banks of course are deeply discounting rates for new loans, but many borrowers are unable to access these “cheap” deals and are stranded on more expensive rates.

Whilst some households who are not stressed continue to pay mortgages down ahead of time (which is why many claim all is well in mortgage-land), the hard fact is that one third of households are facing ongoing financial pressures. These households are not reducing their debt, rather in some cases they are turning to additional finance to try and bridge the cash-flow gap. Or they are raiding savings if they have them, and are putting more on credit cards.

We analyse mortgage stress in cash-flow terms. If a household is paying out more each month including the mortgage repayments, compared with income received, they are in stress. This is not defined by a set proportion of income going on the mortgage. They may have assets they could sell, but nevertheless in cash-flow terms they are underwater.

Mortgage stress continues to be visible across most of our household segments, with more than half of young growing families exposed (56%), and this includes a number of recent first time buyers.

Those in the urban fringe, especially on new estates are also exposed (50%) but the largest cohort are in the disadvantaged fringe, where incomes are below average as well. More than 300,000 households in this group are exposed, comprising 47.2% of all household in this segment.

Stress also appears in our more mainstream groups, though at a lower level, and we also see our most affluent segments over-leveraged, with 24% of Exclusive Professionals (the most affluent group) and 10.7% of Young Affluent households impacted. In fact our predicted bank losses are more extreme in these groups, as they have larger mortgages and multiple properties.

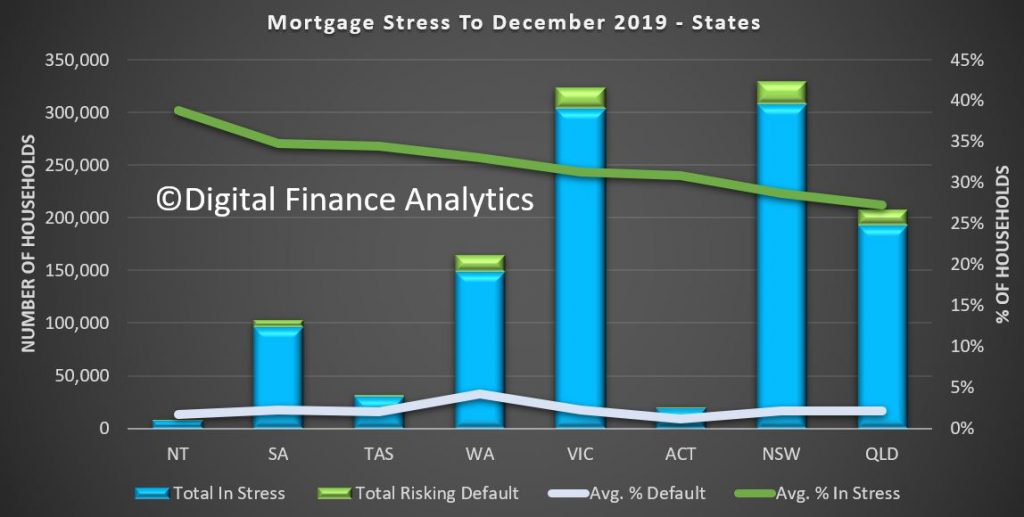

Across the states, 36.9% of households in Tasmania are registering as stressed, which equates to 31,700 households exposed, followed by South Australia at 34.1% (99,700) and Western Australia at 33.6% or 152,000 households. In TAS and SA prices have remained elevated relative to income and housing affordability continues to deteriorate. Victoria has more than 305,000 household in stress, or 32.9%, while Queensland has 193,000 (28.1%) and New South Wales 304,000 (27.3%). The highest rate of default (a forward-looking estimate over the next 12 months) is in WA at 4.2%, while the national average is 2.2%.

Across the regions, Regional Queensland, Horsham (VIC), Alice Springs and the Southern Half of Tasmania recorded the highest proportion exposed. But the main urban centres of Melbourne, Sydney, Brisbane and Adelaide had the highest counts. Default rates were highest in Curtin WA at 5% and Brand WA (4%). This is driven by multiple years of poor economic performance across the state and underscores that mortgage stress is a precursor to defaults, which tend to occur significantly later. The majority are still working, though income is under pressure. Given current economic headwinds and settings, we expect defaults to continue to rise.

Finally, across the most stressed post codes, WA 6065, which includes Tapping, Wangara and Wanneroo recorded 50% of households in stress, or 7,360 households, followed by Queensland postcode 4350, the area around Toowoomba with 7,000 households in stress, NSW post code 2560, the area around Campbelltown with 6,900 households in difficulty, or 59% of households, and then Victorian post code 3805, the area around Narre Warren, with 6,200 households in stress, which is equivalent to 53% of households.

Most of these areas are fast-growing highly developed suburbs, often on the fringes of our major centres, with many relatively newly built properties on small lots, and often with little local infrastructure. As a result, a significant proportion of income goes on transport costs, and so despite many households having above average incomes, their larges mortgages and high expenses are putting them under continued severe pressure.

Finally, a couple of comments for those in stress, bearing in mind many we survey seem unaware of their plight, because they do not maintain a cash flow. So step one is to draw up a cash flow of money in and money out – ASIC’s Money Smart web site has some excellent tools. Next prioritise spending, and focus on repaying high interest debt (like credit card debt). Third, be cautious of refinancing and restructuring as while this may provide a short term path to relief, unless households in difficulty change their behaviour, it will not be a long-term fix. And finally, do not count on income growth ahead, as given the current economic conditions across the country, we expect wages to remain lower for longer.

And this is a warning too to those contemplating the new first owner incentives. Be conservative in your cash flow estimates, do not count on automatic income acceleration. This would be a path to mortgage stress sooner rather than later.

We plan to publish some stress geo-mapping in a later post.

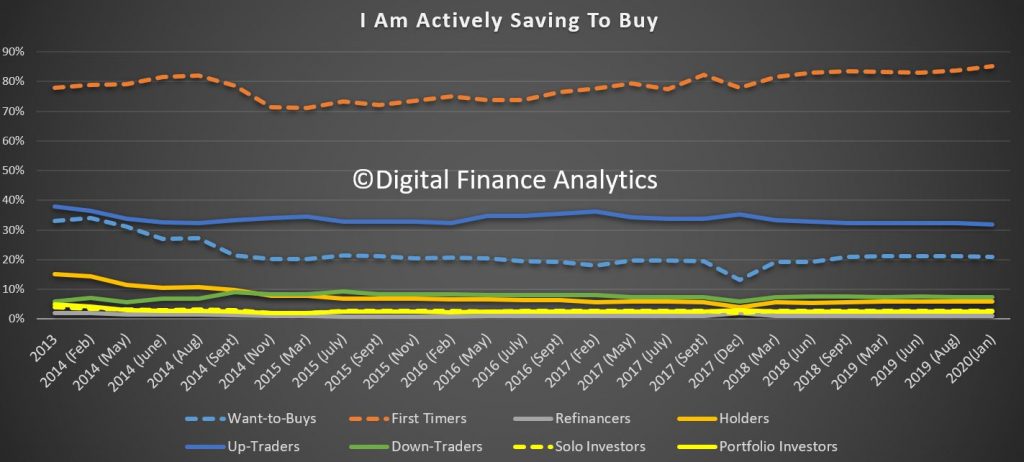

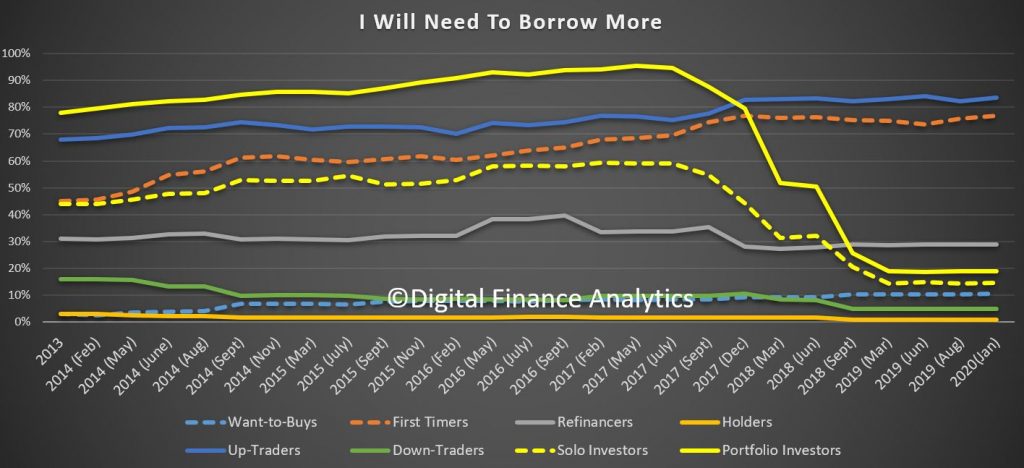

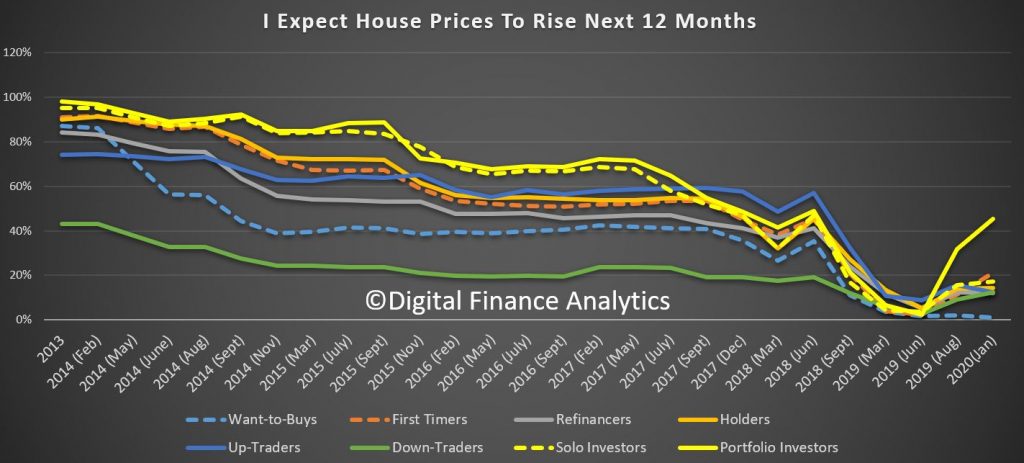

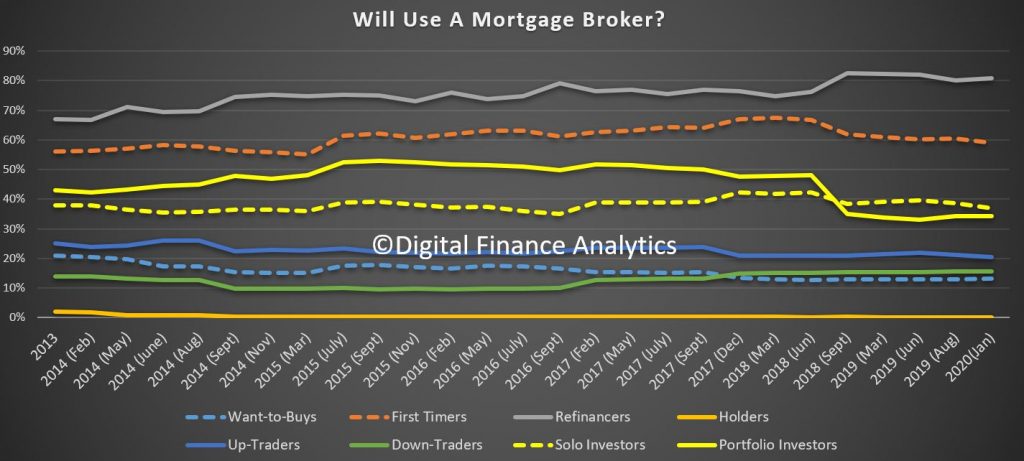

We are releasing the latest data from our household surveys to January 2020 relating to segmented buying intentions and home price expectations. This is using data from our rolling 52,000 households nationally.

In overview, households have got the memo from the Government, that home prices are expected to rise – and this is influencing their forward expectations and buying intentions; to an extent. However, high prices and the significant debt burden, along with no income growth, and overall financial pressures are working against this intent. And property investors remain on the side-lines while first time buyers are lining up to take advantage of the Government scheme which has just commenced. There are 10,000 guarantees available now, and a further 10,000 in the next financial year. Not enough to meet demand.

As normal we will begin with our cross segment comparisons, before looking in more detail at the highlights of specific groups.

The intention to transact in the next 12 months is supported by two segments, first time buyers and down traders. The former are trying to get into the market for the first time, the latter are trying to exit the market to release capital. There are net more exits than entrants, so this suggests a supply demand disequilibrium. Investors remain sidelined.

We find that first time buyers and want-to-buys are savings hard, though lower interest rates are making the task harder. Up traders (people planning to up-size) are also saving, but at a slightly slower rate.

The intention to borrow is an important measure as it drives prospective mortgage growth ahead. The survey results suggests demand will be anemic and be driven by first time buyers and up traders, rather than investors. Not enough to suggest a significant lending recovery, yet.

Price growth expectations are rising, led by property investors, up 14% from September, and first time buyers up 10%. Other segments appear less convinced however.

Across the segments, the preference for using a mortgage broker remains close to longer run averages.

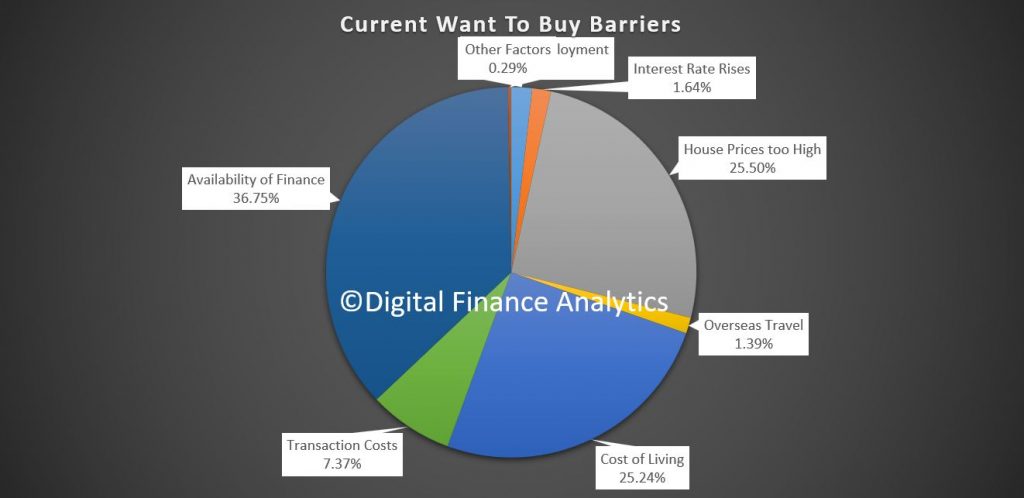

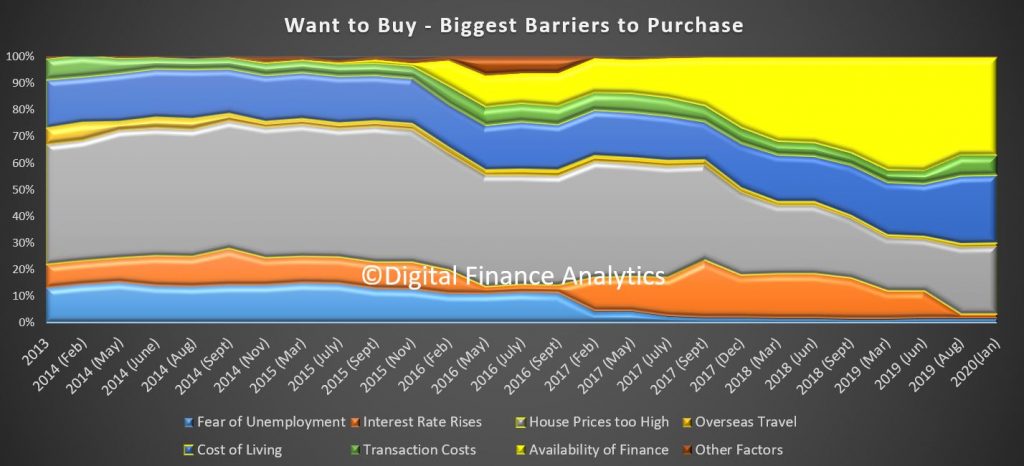

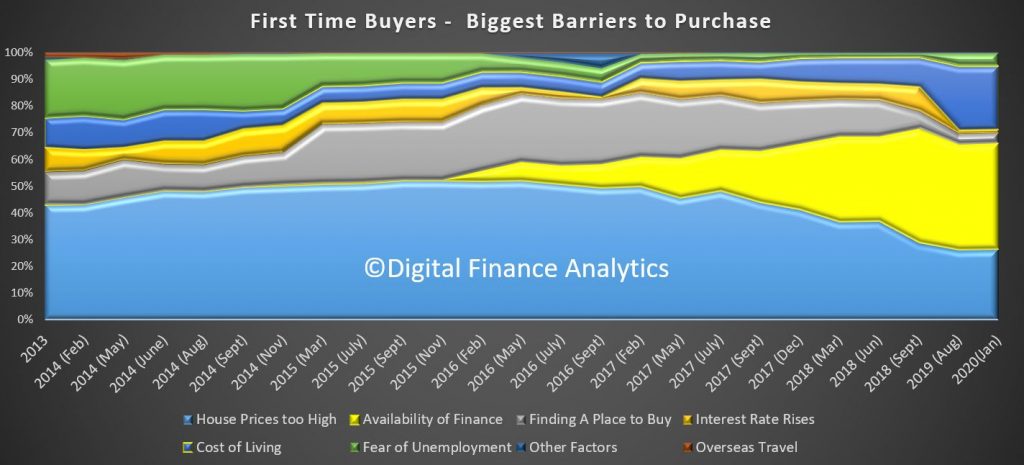

Now, looking in more detail at the segments, those 500,000 households wanting to buy are largely limited by access to finance (37%) (often because their incomes are insufficient or uncertain), that prices are too high (26%), high costs of living (25%) and transaction costs, like stamp duty, LMI premiums, and legal costs (7%).

In trend terms, the availability of finance has eased, down from 43% to 37%, while high home prices and rising costs of living have become a more significant barrier recently.

Turning to first time buyers, there are around 350,000 households who are actively saving with an intention to buy when they can, and the count has been rising in the past few months, partly thanks to the announced Government-back deposit scheme, which is discussed recently in our post: First Time Deposit Scheme: Fish Or Fowl? Loan approvals are running around 10,000 per month, so only a small proportion of the first time buyer pool will be able to take advantage of the scheme, which may put upward pressure on property in the target zones! 22% intend to use the scheme, so more than the guarantees available.

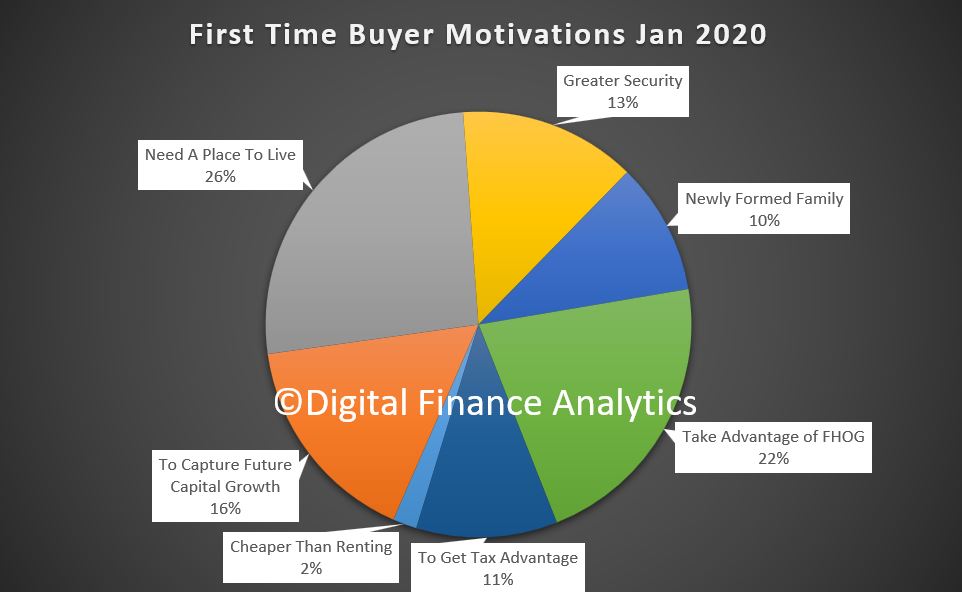

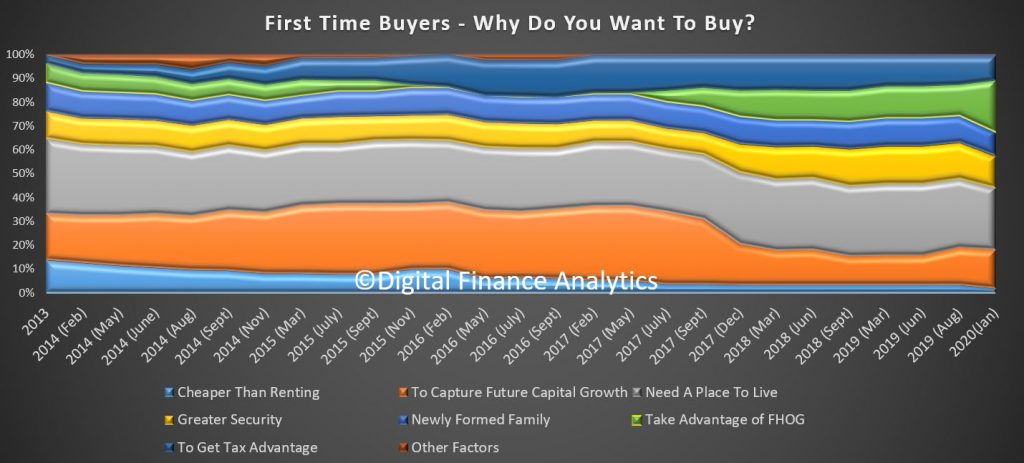

First time buyers are motivated by needing a place to live (26%), with greater security than renting (13%) and to capture future capital growth (16%), or tax advantages (11%). Around 10% transact as part of a newly formed family.

The trends highlight the impact of the new Government scheme, and the rising expectations of future capital gains, compared with a few months ago.

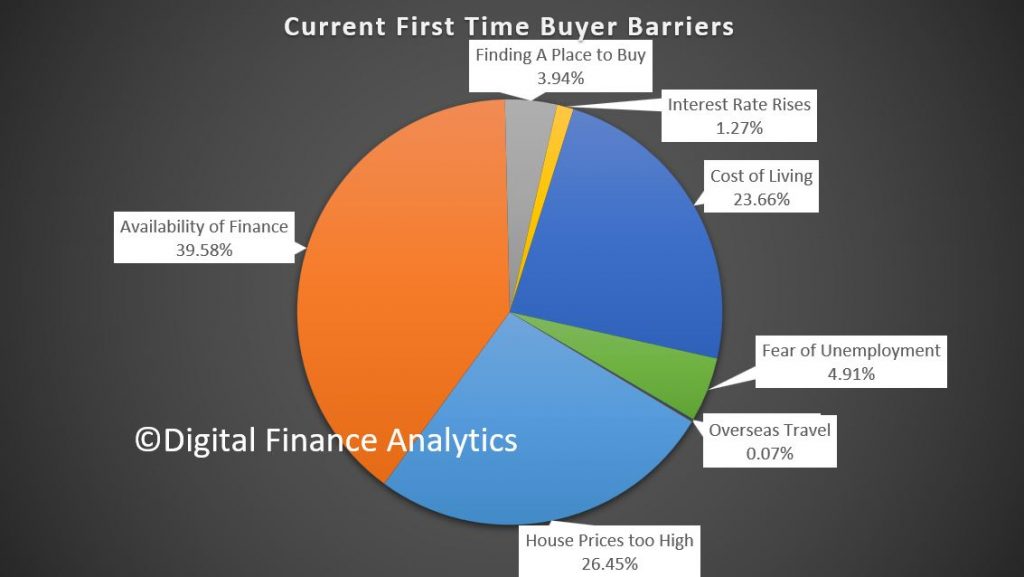

But first time buyers are still facing considerable barriers, including availability of finance (40%), prices too high (26%) and pressure from costs of living rises (24%). Property availability and fear of rising interest rates have both dissipated.

The trends highlight how finance availability remains an issue, and home price concerns are rising again, while there has been a big spike in costs of living in recent times. So many will struggle to buy.

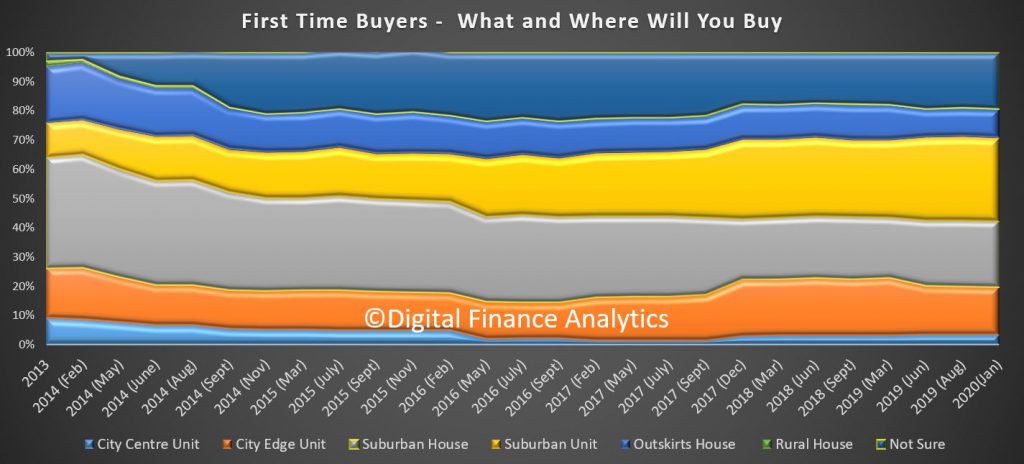

We also see a greater focus on purchasing houses rather than units, a reflecting on the bad publicity in recent times relating to the poor quality of construction and flammable cladding issues.

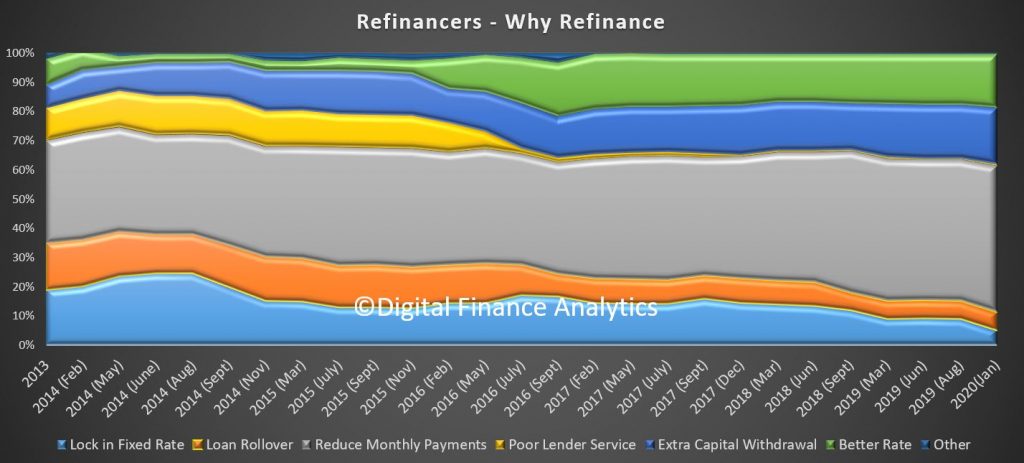

Turning to refinancing, we see the primary motivation is to reduce monthly costs (50%) , capital extraction (19%) and seeking a better rate (19%). Intention to lock in a fixed rate has fallen to 5%, on the expectation that rates will fall further ahead.

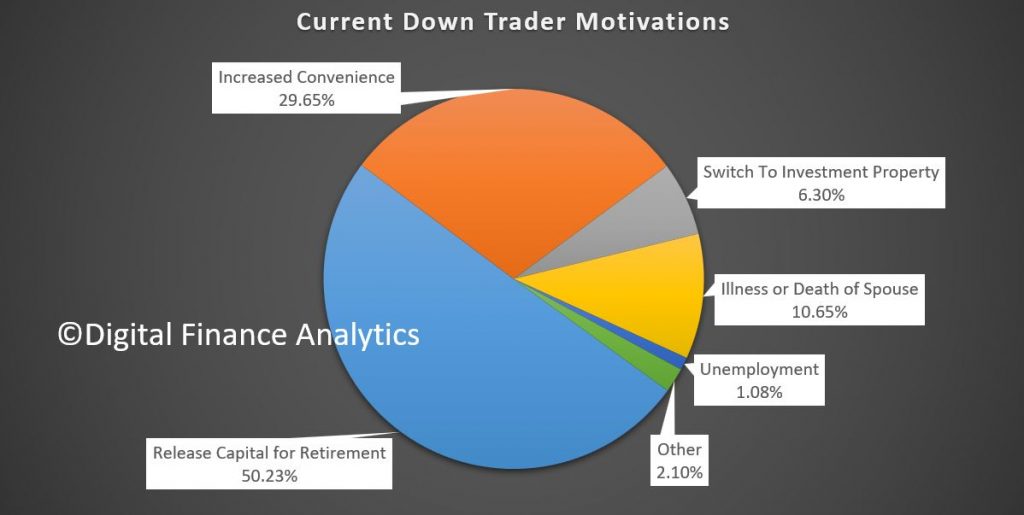

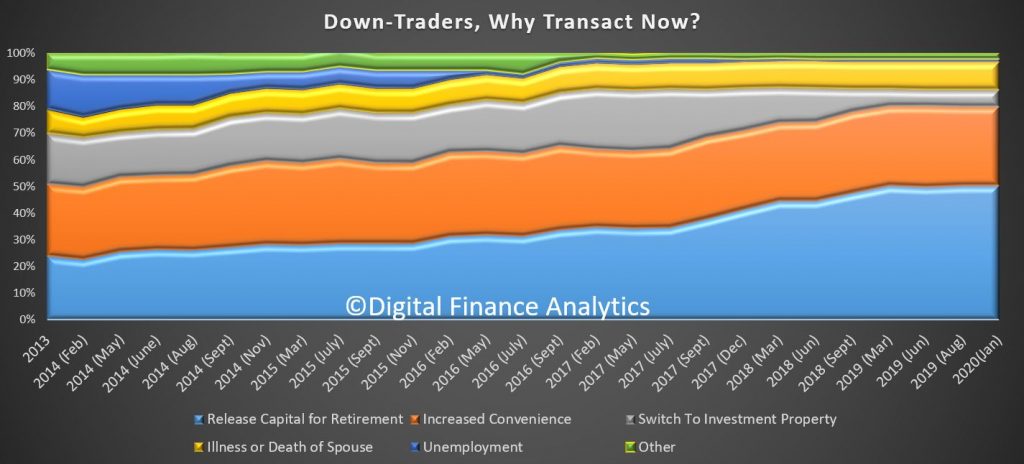

Among those seeking to sell and release capital – and perhaps buy a smaller place – our down trader segment, with more than 1.2 million are in this category, and 56% are hoping to transact. The main drivers are to release capital (56%), increased convenience (30%) and illness or death of spouse (11%).

In trend terms, interest in investment property remains at a low 6%, compared with 23% back in 2017.

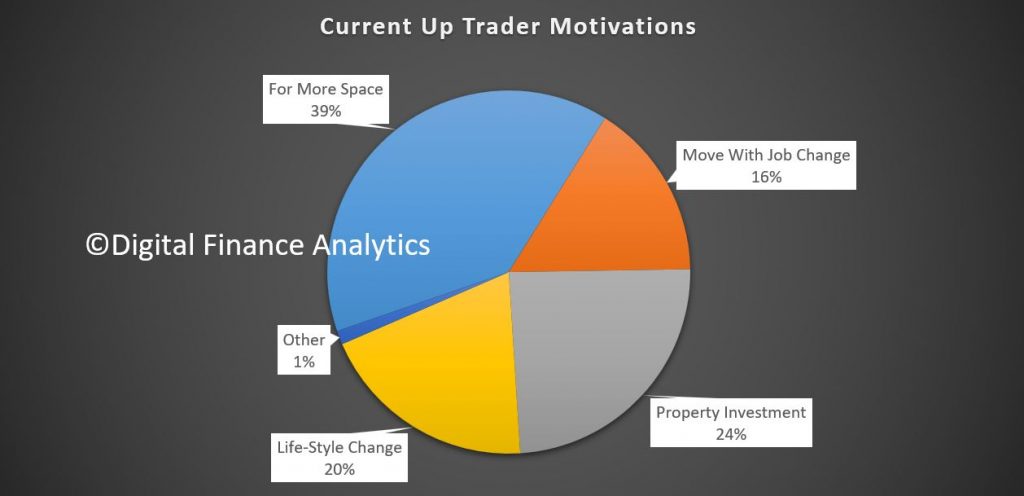

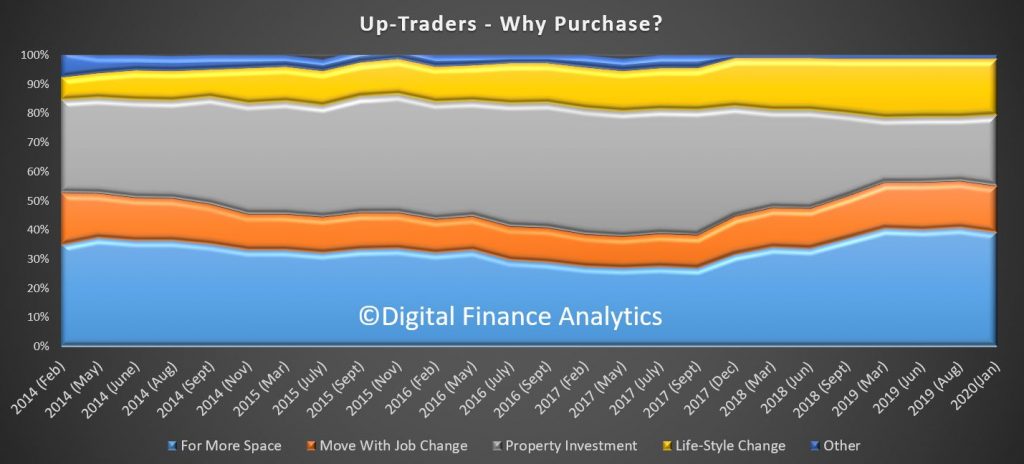

Up traders remain active but there are around 500,000 actively in this category. The main motivations are a desire for more space (39%), life-style change (20%), and job change (16%). 24% are driven by the expectation of future capital growth.

The trend tracker shows the property investment driver is weaker now, while more space and life-style are stronger drivers.

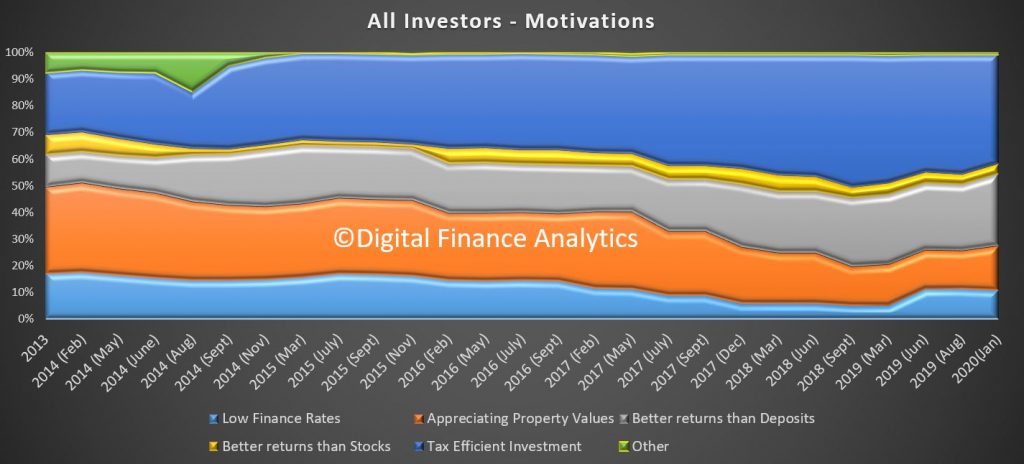

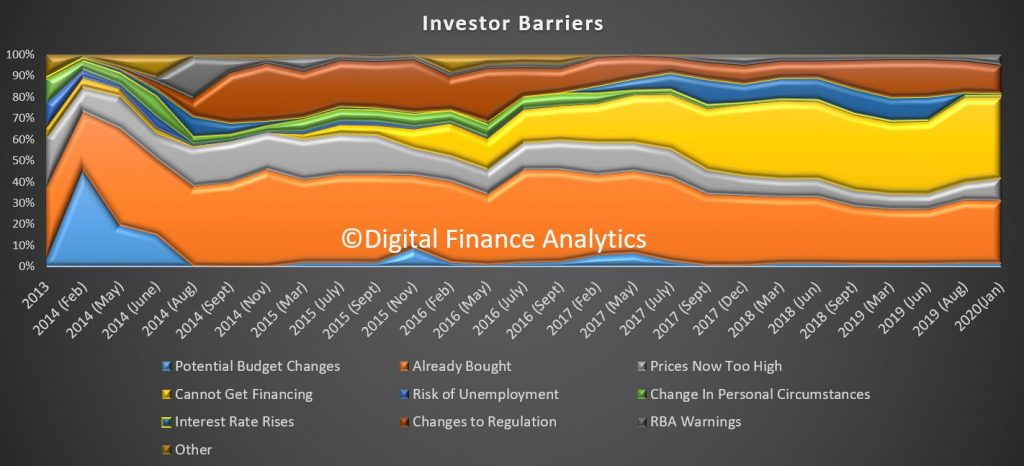

Turning to property investors, tax efficiency features as the strongest driver at 41%, down from 50% back in 2018. Better returns than deposits rose to 27%, reflecting the recent cash rate cuts. Low finance rates also feature at 11% and appreciating property values at 17%, higher than a few months ago. Within the investor segments, portfolio investors (those with multiple investor properties) are most hopeful of capital growth.

Barriers for investors include they have already bought property (30%), they cannot get financing (38%), down 2% from September, and changes to regulation (13%), including tighter rules on income and cost assessments.

There are around 1.3 million property investors, and many remain on the sidelines, due to low rentals, higher vacancy rates, and financial pressures. Of course the switch from interest only loans continues to bite too.

So, in summary, while there are some signs of interest in property, the segments really active are primarily first time buyers, and those trading down and up. There are more sellers than buyers in these groups, so if investors remain on the sidelines, we doubt prices can continue to drive higher, unless mortgage lending really accelerates (who would borrow?) or rules on loan serviceability are loosened further. The first time buyer deposit scheme will not be sufficient to turn the market around, though it may help some builders to shift newly completed or vacant property in the short term.

Nevertheless, households appear more bullish about future home price growth than a few months back – despite the fact the levers of growth appear disconnected from reality judging by these survey results.

We are releasing the results of our rolling household surveys, which were completed before the latest round of bushfires started raging. Nevertheless, the results are a concern because the total number of households registering as financially stressed rose again, to 32.7% of borrowing households. This represent 1.1 million households across the country and a predicted default count of 83,220, despite lower cash rates, and some deeply discounted mortgages.

Stress is assessed in cash-flow terms, and when money in is not sufficient to cover the costs of the mortgage and other regular outgoings, the household is flagged as stressed. Granted they may have the capability to tap into deposits, pull down on credit cards, or even sell property, but on a regular basis they are in strife. We find a significant gap between those we assess as at risk, and those who believe they do have financial difficulty. Many adopt the head in the sand approach and hope things will improve, but given the current economic outlook, we think that is a courageous stance to take.

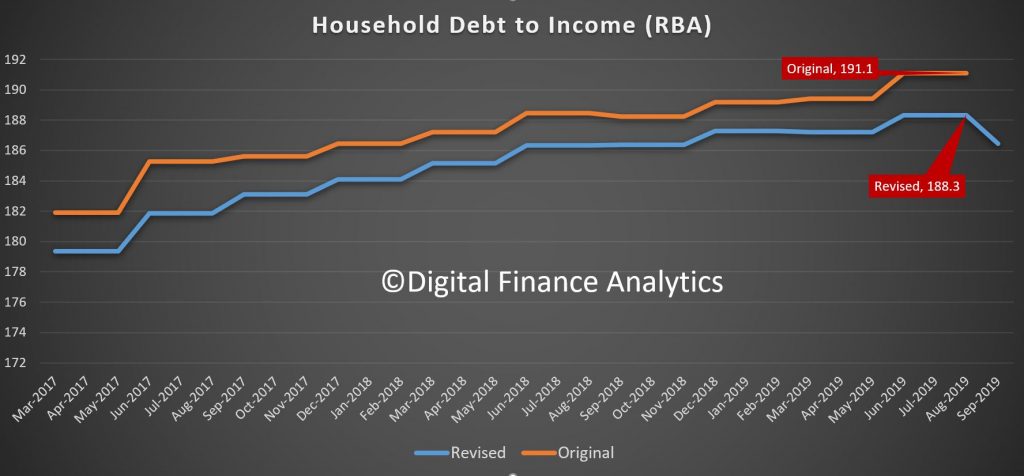

The RBA reported their E2 Selected Household ratios to September just before Christmas and weirdly, the entire debt to income ratio series was restated lower, not just the current quarter, but back through the series. As a result the average debt to income ratio dropped from 191 to a still high 186.5. We always have a issue with this series because it includes small business and households without borrowings, but the downshift in the series is quite significant, and unexplained. I have written to the RBA asking for an explanation. Note this is not the first time the series has been revised down, yet they do not include any explanation in the dataset.

Across the states, NT, SA and TAS recorded the highest proportion of households in difficulty, though WA has the highest default probability risk over the next 12 months at 4.2%, whereas the three most populous states, VIC, NSW and QLD sat at 2.2%. Victoria proportionally to New South Wales has a higher mortgage stress reading.

Among the DFA household segments, 57% of young growing households are in mortgage stress, and within this group there is a large cohort of first time buyers. 2.5% of these households risk default in the next 12 months.

47.5% of battling urban households are also in mortgage stress, and 1.7% risk default ahead. Many of these households occupy properties in the urban fringe, often on newish high density estates. The largest cohort is the disadvantaged fringe group, with 300,000 households in stress and 13,00 risking default. Stress continues to build in our more affluent segments too, with young affluent households at 11.3%, or 4,400 households and exclusive professionals at 21.5% in stress and 3.4% risking default. Losses from this exclusive group are expected to be as high as $1 billion dollars, and is the most value exposed group from a lender perspective.

Across the regions, the Central West of Queensland has 75% of households in stress, but only 300 households, followed by Alice Springs at 65% with around 2,000 households exposed.

In the larger urban centres Adelaide has 35.9% of households exposed, which equates to 75,000 households, followed by Brisbane and Moreton Bay at 29.2% or 148,000 household, Melbourne at 28.9% or 213,000 households and Sydney at 26.9% with 178,000 households under stress.

And across the top post codes, Toowoomba 4350, is the highest count at 7,300 households, or 48%, followed by Liverpool 2170 at 49% or 7,080 households, Fountain Gate and Narre Warren 3805 with 6,918 households or 59% and in WA Hocking, Tapping and Wanneroo with 45% of households equating to 6,732.

Given the current economic settings we expect stress to continue to rise. And shortly we will be looking at the latest household financial confidence index from DFA, which continues to highlight challenging times for more and more households.

But in closing, as I often say, households would do well to draw up a cash flow, to identify money in and money out, determine which spending is essential and prioritise accordingly. And remember, if you are in financial difficulty banks have an obligation to assist, so go talk to them, early. Avoid the head in the sand posture, as it leaves other parts horribly exposed!!

Following our recent update on household mortgage stress, it’s important to broaden our scope into other areas of household financial stress. Just as mortgage defaults rise, power disconnections rise too.

In this report Mitch Grande examines the evidence. Mitchell is a recent Graduate of Politics, Philosophy, Economics (Honours) at the University of Wollongong and is concerned with Australian public policy, and especially energy policy.

Disconnections:

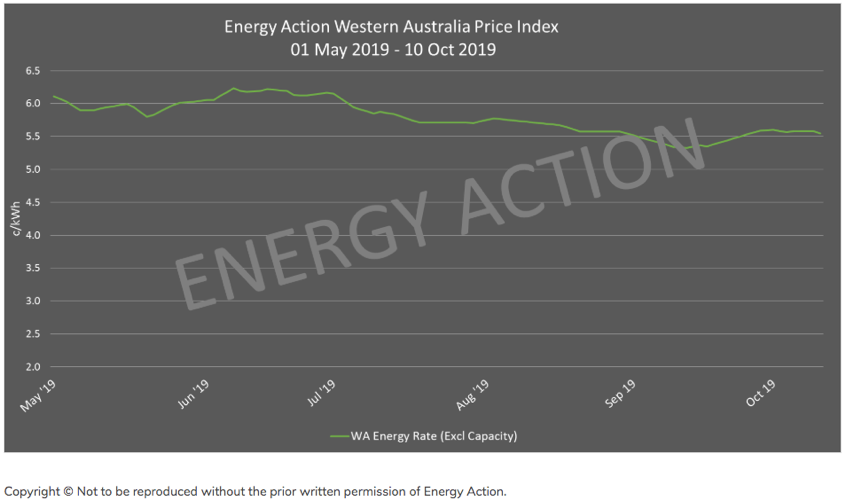

The ABC recently published an article on Western Australia’s record number of

households having their power shut off. For measure, WA’s mortgage stress has

reached 34.3% (145,000), as local economic conditions continue to deteriorate. We

suspect mortgage stress is well correlated with households being disconnected

from their power supply and compounding cost of living pressures through power

bills.

The

article spoke of one 1 in 60 WA households being cut off following unpaid

bills. WA’s state-corporations and largest retailers, Synergy and Horizon

Power, stated that over 22,000 customers had their power shut off in the past

year. This is a two-fold increase in state disconnections in the last three

years. The article cites year-on-year increases to the average WA electricity

bill of +11% (2017), +7% (2018), and +1.75% (2019); while salaries at best

increased +1%. It is important to note that WA is not included in National

Energy Market operations and trading, and as such, the government regulates

Synergy and Horizon Power’s prices of residential and larger customers, setting

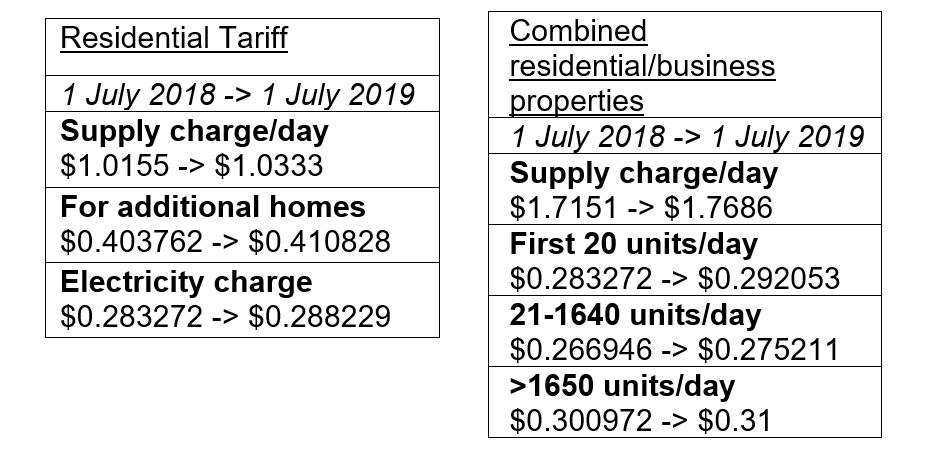

the fees and charges annually in the budget. Most recent changes are as follows:

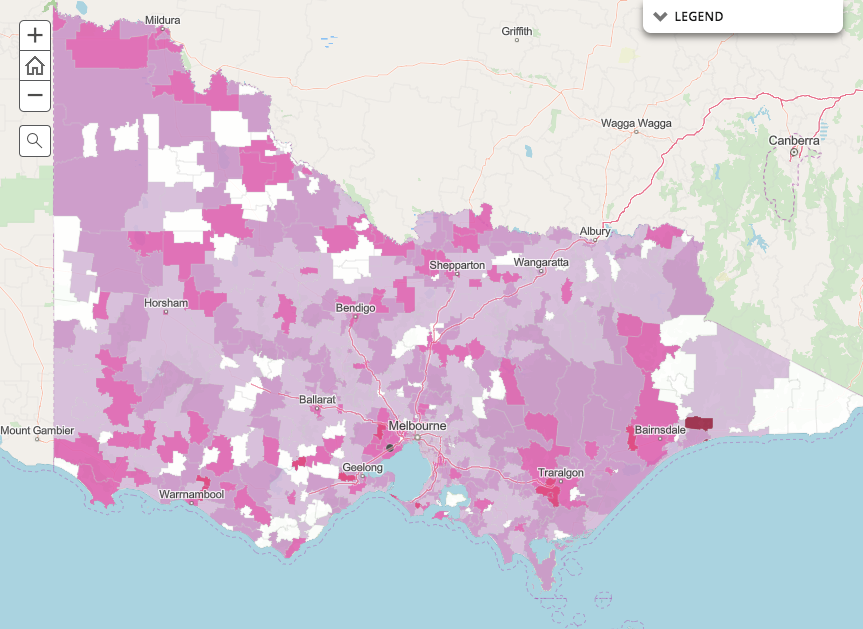

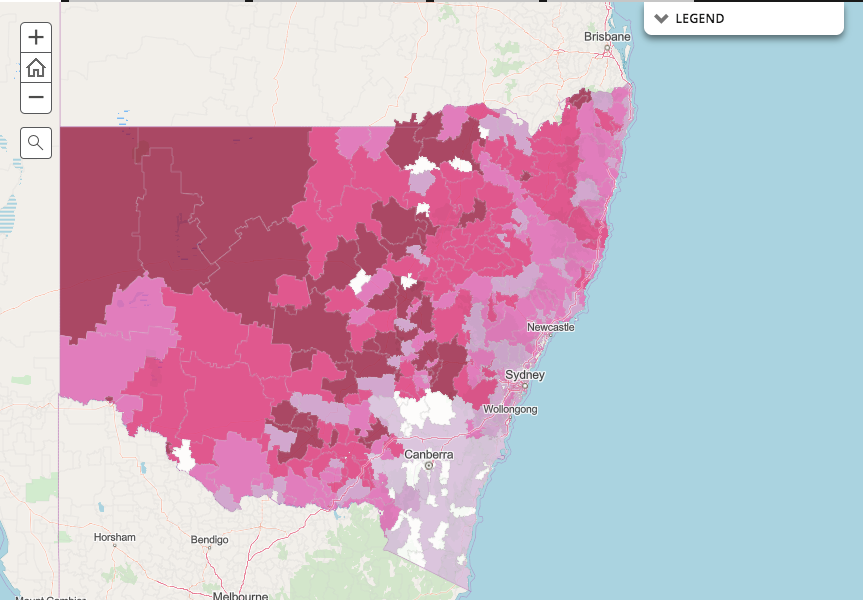

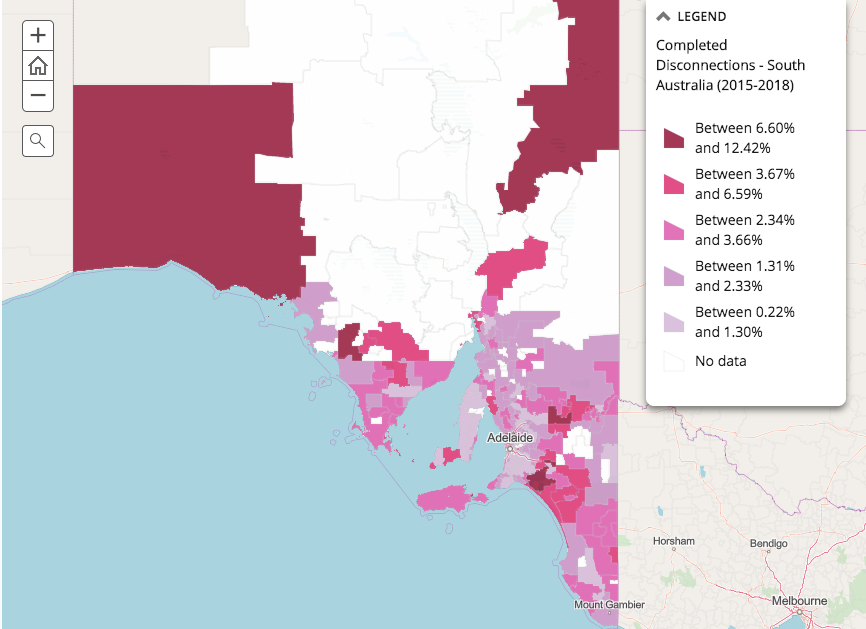

Other research on household energy stress by Alviss consulting with St Vincent de Paul, which does not include Western Australia, examined disconnection data for Victoria, New South Wales, Queensland, and South Australia. In short, their research found many regional and rural hubs at risk, as these postcodes, especially in the last three years, have experienced the most disconnections. The reason behind the regional cost profile is burgeoning network costs, with polls and wires being old, inconsistent, and ‘gold-plated’ over much longer distances than metro customers.

The

Alviss report categorises two types of disconnections: raised disconnections

and completed disconnections. However, the ABC report on WA only speaks to

“power being shut off”, so it is hard to compare the data uniformly. Nevertheless

both reveal the same story of financial hardship in small rural postcodes, perhaps

struggling with the agrarian shift and general economic stressors of poor

revenue poor wages, high costs, and burdens. Both the ABC article and Alviss

report speak to these at-risk households entering stress spirals, in which

regional folk are ‘too proud to seek help’ in either welfare or drug and alcohol

abuse.

The

average postcode profile consisted of lower local incomes, higher unemployment

rates, and relatively more housing affordability issues. A such, the average at

risk household was demographically older, had less economic opportunities, and

lower incomes.

State-by-state

the Alviss report found that:

Victoria had 43.8% of reported customers face

raised and/or completed disconnections.

Werribee (3030) topped the table with 10,424

raised and 5,097 completed.

NSW had 36.7% of its customers face raised

and/or completed disconnections.

Orange

(2800) had the most with 17,902 raised and 6,435 completed.

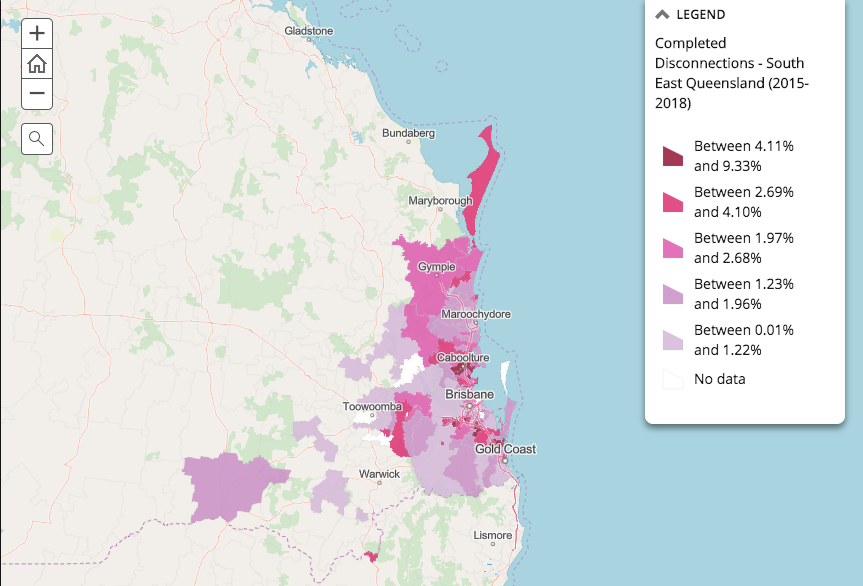

South East QLD had 30.3% of its customers face

raised and/or completed disconnections.

Caboolture (4510) had 7,587 raised and 2,541

completed.

But Logan (4114) had the highest completed with

2,552 of 7,152 raised.

SA had 30.2% of its customers face raised

and/or completed disconnections.

Salisbury (5108) had 3,956 raised and 952

completed.

But Elizabeth North (5113) had highest

completed with 1,524 of 3,953 raised.

This points to larger lingering issues in SA in

which more than 10 of the top 30 disconnected postcodes are middle suburbs

(5085, 5112, 5113, and 5114).

The

higher completion of disconnection rates reflects far greater then understood

financial hardship, retailers more readily disconnecting households, and

networks being more readily and efficiently able to disconnect consumers. Here

at DFA we have the data available to investigate this financial hardship,

through the survey data on mortgage stress.

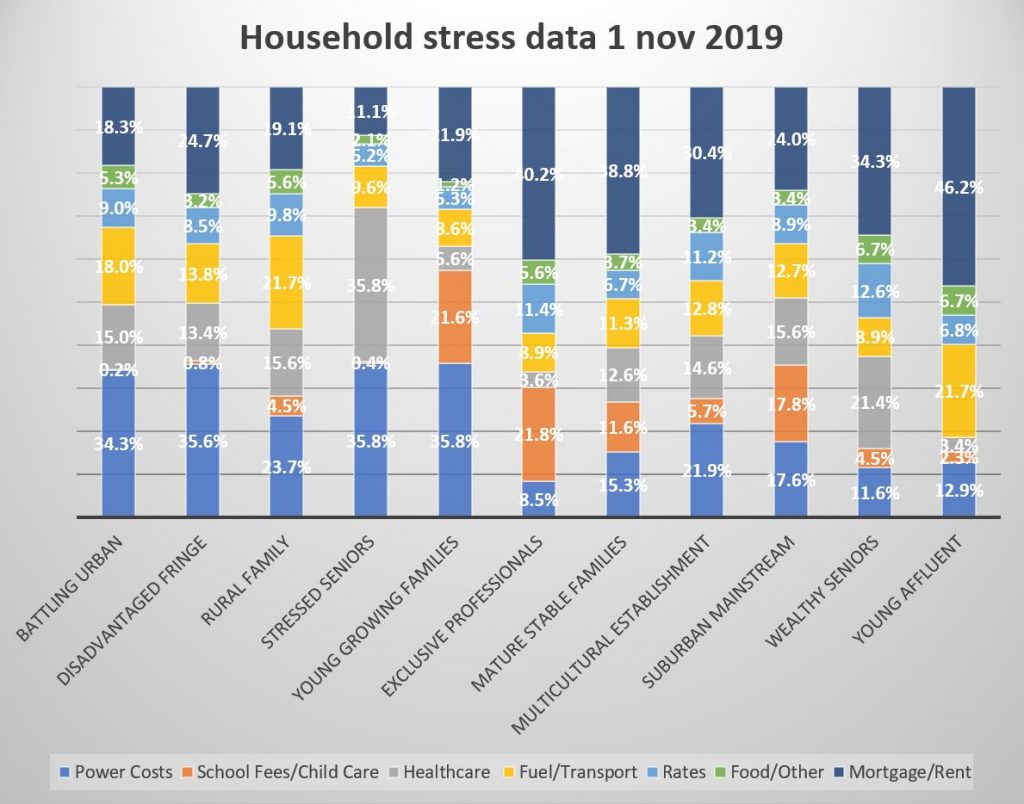

DFA survey data breakdown:

From our

most recent DFA survey data, those most affected by power costs include:

the Battling Urban (34.3% surveyed);

the Disadvantaged Fringe (35.6%);

Rural Families (23.7%);

Stressed Seniors tied between power costs

(35.8%) and healthcare costs (35.8%); and

Young Growing Families (35.8%).

This

comes, largely, as we might expect, with young families in growing urban areas,

seniors and those in regional areas struggling with cash flow, and pockets of

disadvantaged and battling segments overburdened by power costs. The

distribution of these segments is largely consistent with the Alviss data,

particularly in Rural New South Wales and the Battling Urban of South

Australia.

All of

these segments (except rural families) whose power costs were the largest

stressor had mortgage/rent stress as their next most outstanding strain with:

Battling Urban (18.3%);

Disadvantaged Fringe (24.7%);

Stressed Seniors (sans healthcare cost (35.8%))

with (11.8%); and

Young Growing Families (21.9%); while

21.7% of Rural Families had fuel and transport

costs as their next highest stressor, whereas mortgage/rent costs affected

19.1%.

In the

other segments, which surveyed a higher cost than power costs, the distinction

is clear:

40.2% of Exclusive Professionals had higher

mortgage/rent cost stress than power costs (8.5%) with the next highest portion

reporting school fees/childcare (21.8%);

Mature Stable Families surveyed higher stress

from mortgage/rent costs (38.8%) than power costs (15.3%) which was their next

highest;

Multicultural Establishments had higher

mortgage/rent stress (30.4%) which was higher than power costs (21.9%), the

next highest result;

the Suburban Mainstream surveyed 24.4%

mortgage/rent costs compared to power costs (17.6%), where their next highest stressor

is school fees/childcare (17.8%);

Wealthy Seniors with (34.3%) mortgage/rent

costs, followed by healthcare (21.4%); and finally

Young Affluent in mortgage/rent costs (46.2%)

followed by their next highest, power costs (12.9%).

These

segments, too, largely come as no surprise with Mature Stable Families not

facing disadvantage, unlike the inner-city postcodes of South-East Queensland.

Or, Wealthy Seniors facing some degree of housing affordability in Rural or

Regional Victoria.

AEMC, AER, and Canstar:

A 2018 Australian Energy Market Commission (AEMC)

report modelled that in the next

two years emerging wind and solar capacity will drive down residential

wholesale prices by $55, offsetting marginal increases in the supply chain like

coal plant retirements, burgeoning network costs, and minor environmental

costs. The 2019 national weighted average consumption level for

residential consumers was estimated at 4,596 kWh per year. And at this

consumption level, the national average annual residential bill in 2017-18 was

$1,384 exclusive of good and services tax (GST) and $1,522 inclusive of GST.

However,

the lived reality for many households, on average, far exceeds these averages. One

way we can be certain of this is the Australian Energy Regulator’s own data on

disconnections: for NSW, SA, QLD, the ACT, and Tasmania 70,000 residential

customers had their supply disconnected between 2017 and 2018. These

disconnections are seasonally dependent, however more uniformly than we might

expect: there are slightly more disconnections raised in autumn (27.8%) and

summer (26.6%) than in spring (23.0%) and winter (22.6%). And then from the

more recent Alvis report and ABC WA article, we find that renewables easing the

wholesale price is not being felt – especially by regional and rural

households. To be clear, the private development of renewables is making enormous

strides in the alleviation of power costs, however, the rather incongruent

policy leadership in a number of other spaces is directly counteracting this.

By

taking a quick glance at Canstar, average annual bills are anywhere from $80 to

$370 greater than the AEMC’S estimates for the same average consumption – and

have increased.

Despite

the AEMC claiming observable declines in average household prices, postcodes

and households across the National Energy Market experience higher real bills

due to sluggish wages and are themselves burdened by inconsistent policy

frameworks that fail to implement meaningful market-based solutions or improve

the cost of living. The fact of the matter is that household disconnections in

all states is increasing.

Recently, the AEMC published their annual report for 2018-2019, which showed that consumers who are willing and able, have engaged in consumer-side uptake of solar PV and batteries. This is causing a positive decentralisation of energy grids (e.g. microgrids, peer-to-peer, virtual powerplants) and alleviation of power prices. In short:

“The technology revolution offers opportunities

and benefits for customers to take control of how they buy, sell and use

energy. Over time, this should allow for greater utilisation of the existing

stock of generation and network capacity, lowering average costs for all

consumers.”

However,

this is not without its challenges. The AEMC signal to a more complicated shape

of daily consumer demand and daily generator supply due to the decentralised

frequency and voltage; the necessity of a new power system management in

replacing old and inadequate capacity; getting proper connectivity to new

remote wind and solar projects; and the ever-elusive unpredictability of

weather patterns on day-to-day demand. As well, those households who are unable

to purchase household solar and/or batteries are beginning to be left behind,

worsening bad market conditions.

In all,

these challenges can be adequately met with coordinated and purposeful

investment in solar/battery integration and security. For instance, improving

grid access to those least-cost sources; fixing security challenges present in

the system, like network infrastructure; or maintaining incentives vis-à-vis

the needs of the system, like decentralised control of household’s bills with

smart technologies all will alleviate prices.

The Federal Governments’ Policy Angle

Going

into the election, the Coalition alluded to three policy options in order to

lower power prices: removing standing offers (dubbed a loyalty tax);

underwriting new reliable investment (painstakingly trying not to call it

subsidies); and ‘big stick’ divestment policies aimed at big gen/retailers who

either ‘price game’ or stray from Angus Taylor’s ‘reliable’ mantra. Rather

critically:

“The Coalition’s

fixation on energy prices is no doubt politically effective, as it both appeals

to people’s hip pockets and works as a scare campaign against taking action on

climate change. But it also obscures another significant, and not unrelated,

economic reality.”

Coming

from an ACCC report that “the standing offer is no longer working as it was

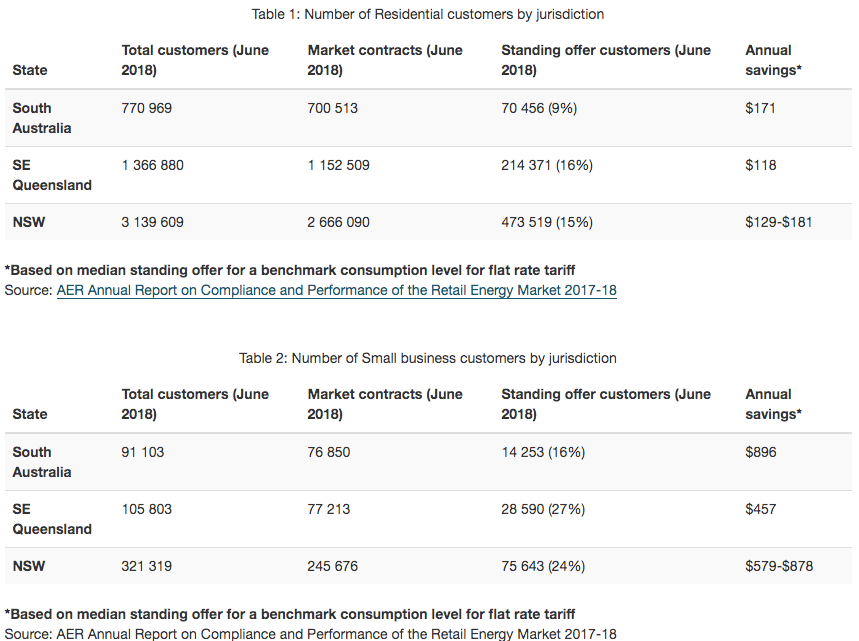

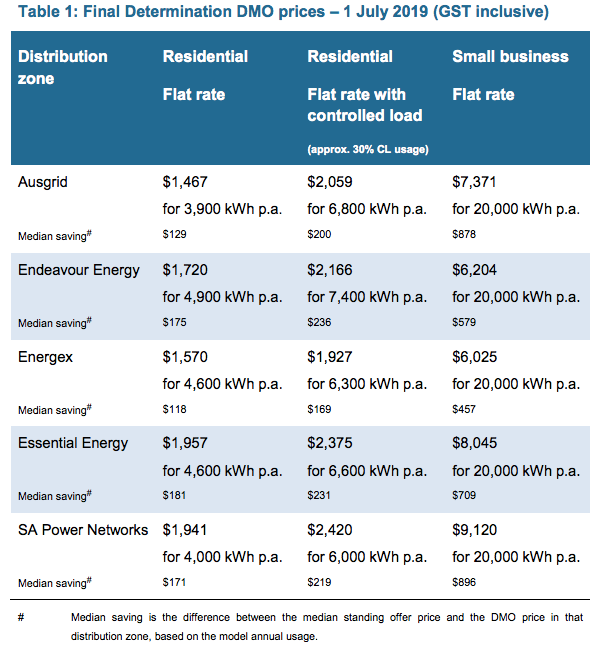

intended and [that it] is causing financial harm to consumers…” the government claimed that: “On 1 July 2019, 800,000 Australian families

and small businesses will benefit from lower electricity prices by moving to

default market offer electricity contracts saving households up to $481 in

South Australia and up to $663 in NSW and South East Queensland. Households changing to default market offers

from standing offer tariffs will save up to $481 in South Australia and $663 in

NSW and South-East Queensland…”

Not only

is this marginal in the grand scheme of energy consumers, it has required an

equalisation across the entire NEM. That is, people on “confusing discounts”

will have those reduced in order to maintain retail profits, stating: “customers

on standing offers and market offers that were above the default offer would be

better off, customers on lower priced market offers would be worse off”. The

AEMC and ACCC’s own data showed that the percentage of consumers on standing

offers was declining rapidly and organically.

“All

jurisdictions are likely to have less than 10 per cent of residential customers

on standing offers within the next two years. The Commission also notes that

there exists a segment of the market (approximately two to four per cent of all

residential customers) who are on standing offers for only a short period when

they move house or create a new connection and have not yet selected a market

offer.”

The

Government signalled to “savings built on price cuts of up to 15 per cent

secured by the Morrison Government for more than 500,000 families and small

businesses from 1 January 2019 – and our ban on sneaky late payment fees that

will save some customers up to $1,000 a year…” in that “small Businesses

changing to default market offers from standing offers will save up to $457 in

South-East Queensland, $878 in NSW and $896 in South Australia.” Despite this,

disconnections and household power costs stress have uniformly risen.

The

government and the ACCC urged consumers to still shop around for market offers

that are almost always cheaper than these default market offers.

“In particular, higher proportions of rural and small

business customers remain on standing offers. In contrast, the percentage of

hardship customers on standing offers is approximately half that of all other

residential customers.”

This is

coupled with underwriting new “reliable” generation, expected to reduce NEM

wholesale prices by a quarter by 2021 – however, whether the government is

subsidising the right wholesale generation capacities is another question

entirely (they’re not). As well, the government has introduced the Energy

Assistance payments to welfare recipients which emphasises a price safety net:

“banning retailers from offering confusing discounts, protecting customers in

financial hardship and requiring energy retailers to notify customers when

their discounts are about to finish or change.”

The

government appears more concerned with tinkering with peoples’ demand (a la the

first home buyers’ scheme). In doing so they are inflating average demand

profiles, not managing the market-wide issues in supply.

Being

seven months after the election, and five months since the default market

offers were introduced, the AEMC optimistically signalled to wholesale price

easing countered by burgeoning costs in the network and retail profiting – whereas,

on average, the consumers’ bill has increased in the eyes of financial

comparison cites and segments of the population surveyed by DFA report higher power

cost stress.

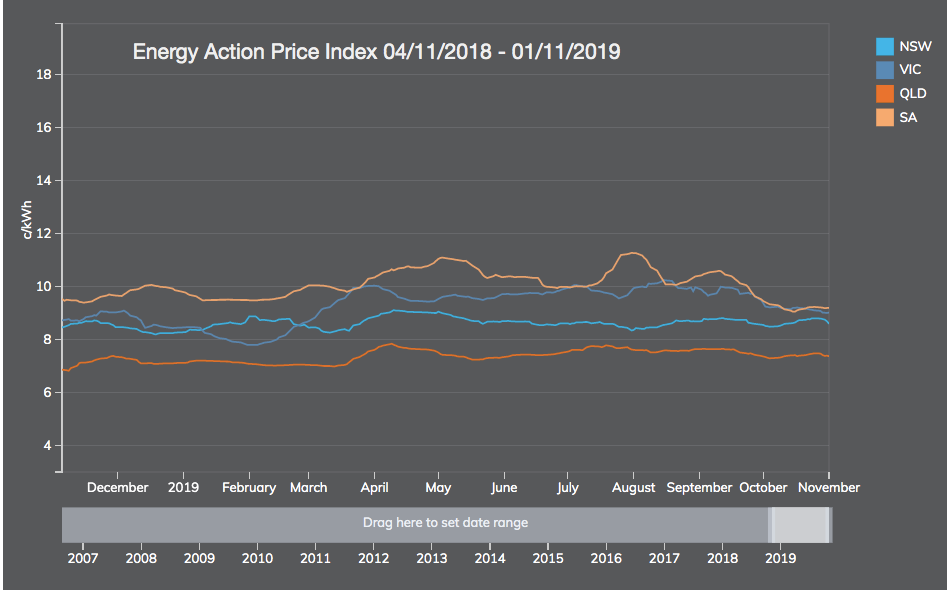

The

optimism is not lost in the media: with David Crowe, just in September, writing a piece stating that bills are falling

$130 a year thanks to the Morrison governments’ “industry crackdown.” Crowe

writes: “The price rules came into effect on July 1 and have already cut the

standard offers for electricity customers, with some NSW households saving $130

a year. Some Victorian customers have seen their offers fall by medians of $310

to $430 depending on the retailer.” But immediately, Crowe states that not all

customers are going to have reduced bills, just those that were on existing standing

offers – meaning that those on existing discounted retail rates have since had

their bills increased to equalise the burden. Whether this is observable in the

mass of disconnection figures or household stress is uncertain.

In the face of this optimism is the reality that power costs continue to burden

a majority of segments in Australia and average bills continue to rise, as ad

hoc policies have all but decreased the average bill. This is mainly because of

the new policy directions under Taylor and Morrison, which deal more in threats

and subsidies than they do in proper market-based or evidence-based

policymaking. The governments new direction fails to address the largest

inflators of household power costs, which are the overinvested gold-plated

regulated asset base, burgeoning wholesale costs from aging coal-fired power,

and extraordinary retail costs/profits – the latter of which the ACCC and AEMC reject, simply because ‘the market is competitive’. In

that same report, the ACCC and AEMC flag the long-term risks due to legislating

default market offers, including:

increased risk to retailers driving higher

financing and overall costs

lower levels of innovation leading to less

available products and services

higher barriers to entry and changes to

consumer behaviour resulting in decreased competition.

AEMC

were happy with retail competition (2019), for the market’s improved

simplicity, stable price deals, and removing confusing offers creating “a more

engaged market that is responding positively to greater product innovation and

bundling – and producing positive outcomes.”

5. Final Remarks

As a

portion of average household expenditure, electricity costs have risen to 50%

from 2006 to 2016. The ABS found 10% of those surveyed reported difficulty in

paying bills in 2015-2016. In 2013, ABS also found 10% “chose” to restrict

heating and cooling. These figures alone reaffirm the DFA thesis that Australia

is experiencing poor wage growth, underemployment, low productivity, record

levels of private debt. And when this is applied to poor innovation in the

energy sector, a maintenance of minerals-based growth, and a reluctance to

properly do what is needed

Across

all household types, less are able to pay electricity/gas. There is a negative

association between net wealth and indicators of energy-related financial

stress 1st quintile ‘chose’ to restrict heating / cooling. Renters

and mortgage holders are at observably greater risk of energy-related financial

stress, ‘choosing’ to forgo consumption. Solar panels substantially reduce their

difficulties, however, it is only available to those who can afford it, while

those who can’t are left to the market.

As the

DFA data shows, the surveyed segments are divided along two key groups: those

with Young Families in growing urban areas, Seniors and those in regional areas

struggling with cash flow, and pockets of disadvantaged and battling segments who

are overburdened by power costs. And on the other hand, those Exclusive

Professionals, Mature Stable Families, Multicultural Establishment, Suburban

Mainstream, Wealthy Seniors and the Young Affluent who are more burdened by

mortgage/rent costs.

In summary,

summer bodes very poorly, with shocks from old coal-fired power very likely spiking

prices unpredictably along outdated yet gold-plated interconnectors. Any price

movements across states, such as a brown out, through the NEM will be

infectious, as interconnectors deteriorate and fail to distribute new renewable

projects of higher efficiency. Existing coal generation is increasingly

unreliable and expensive, as the fleet continues to retire, and governments

fail to make investment into sufficient new generation or systems reliability. The

policy void in wholesale and gas markets will mean that higher prices and

system risk will continue, as the market and industry signals for proper

investment and legislative certainty.