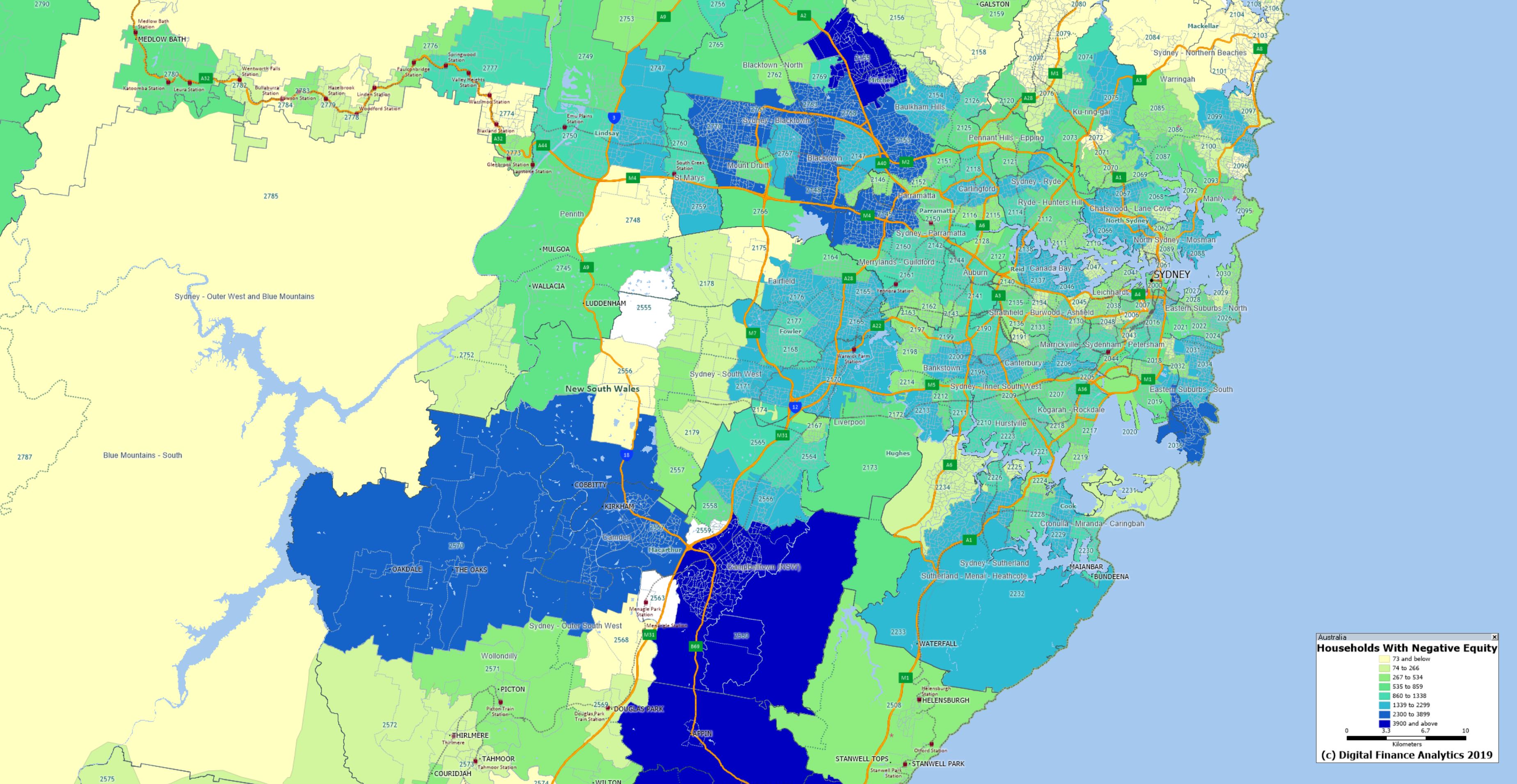

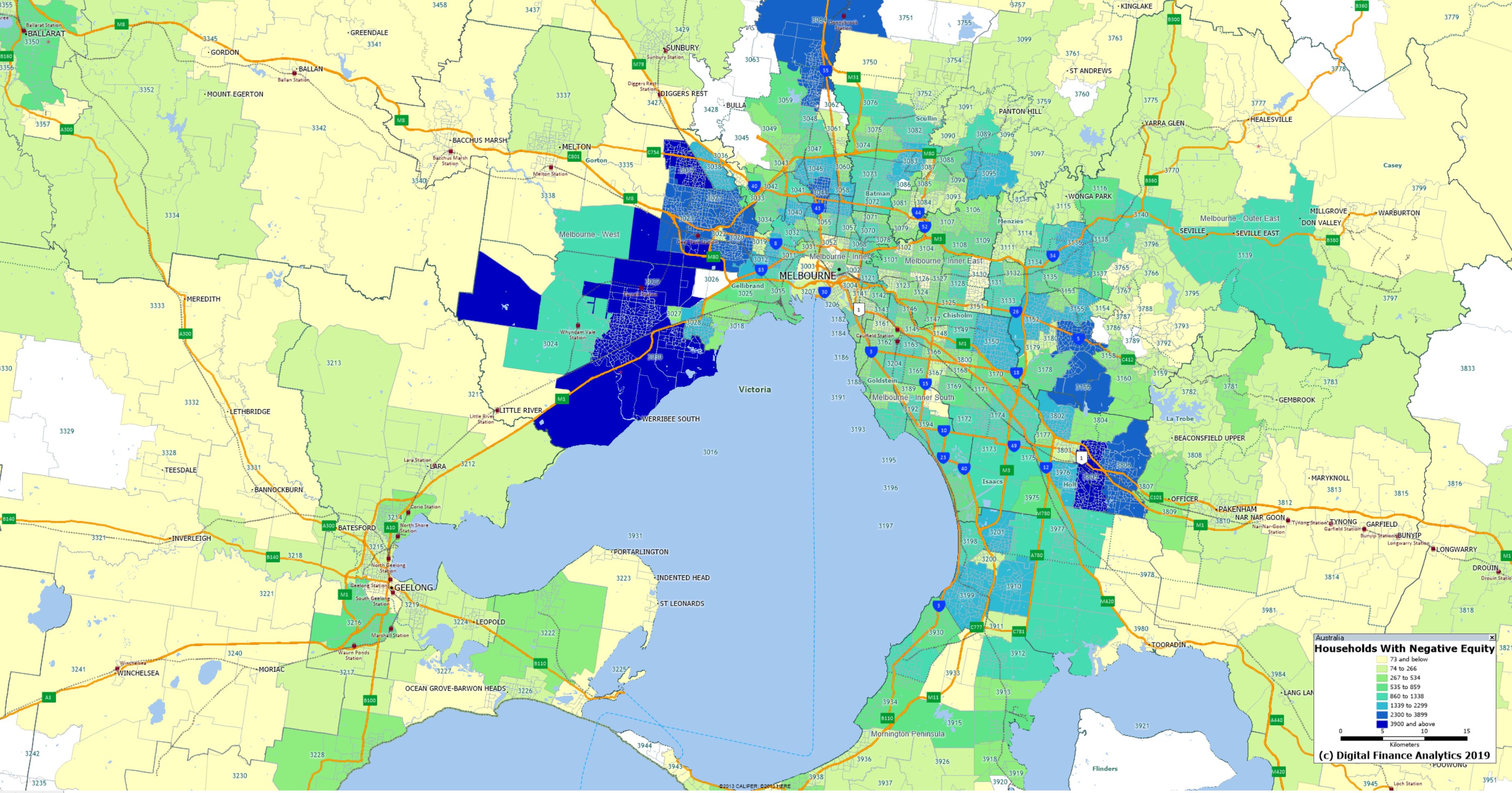

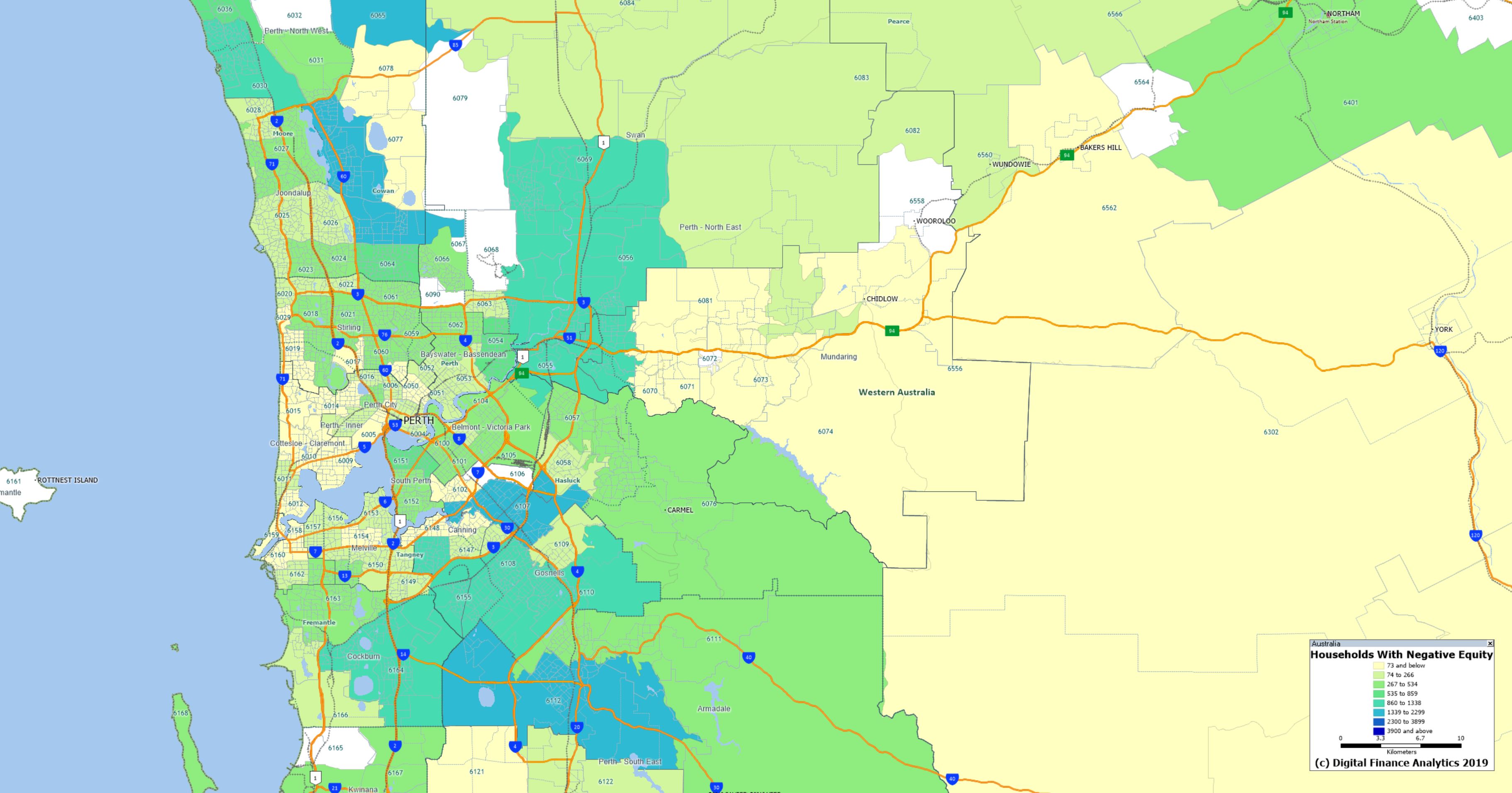

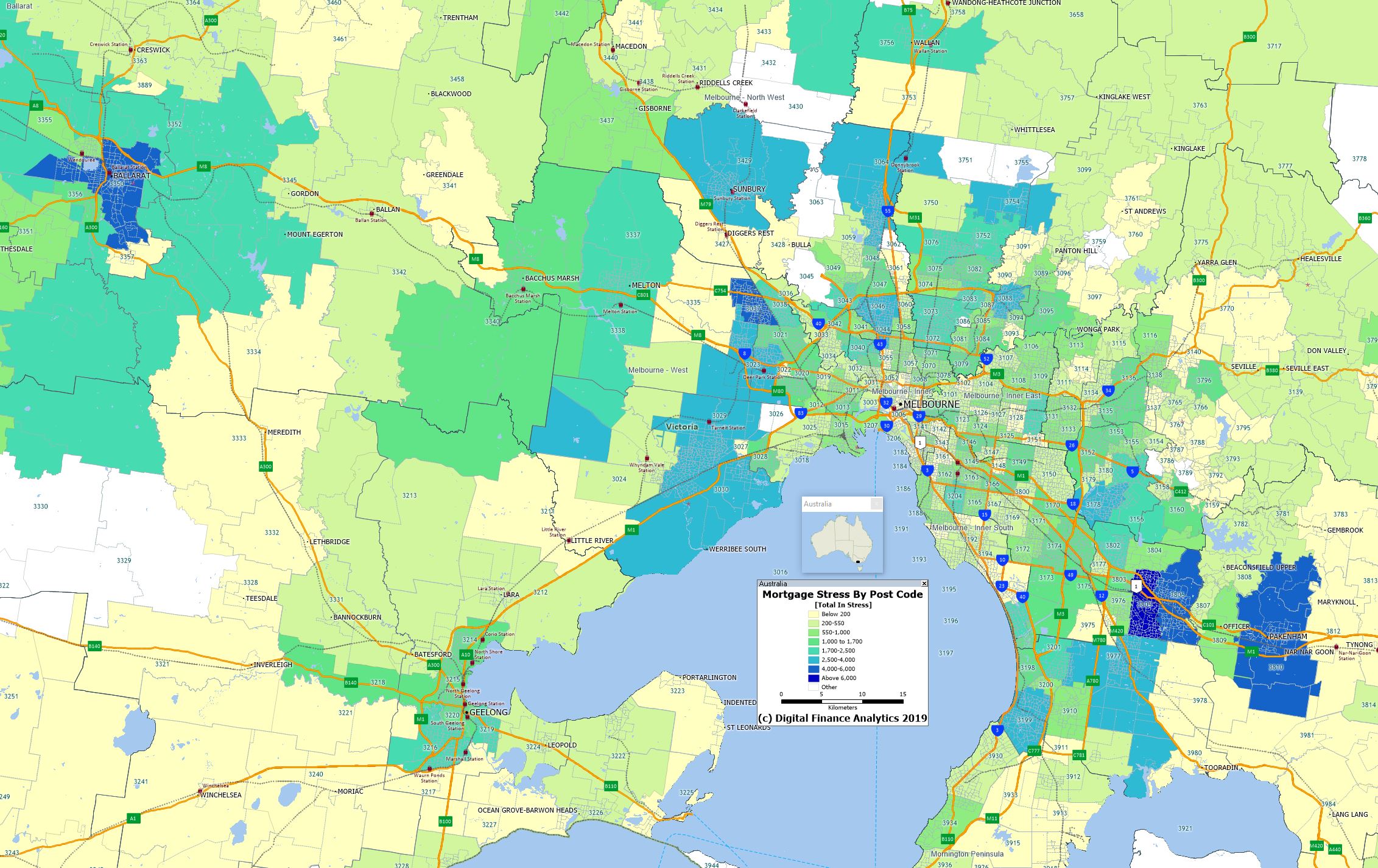

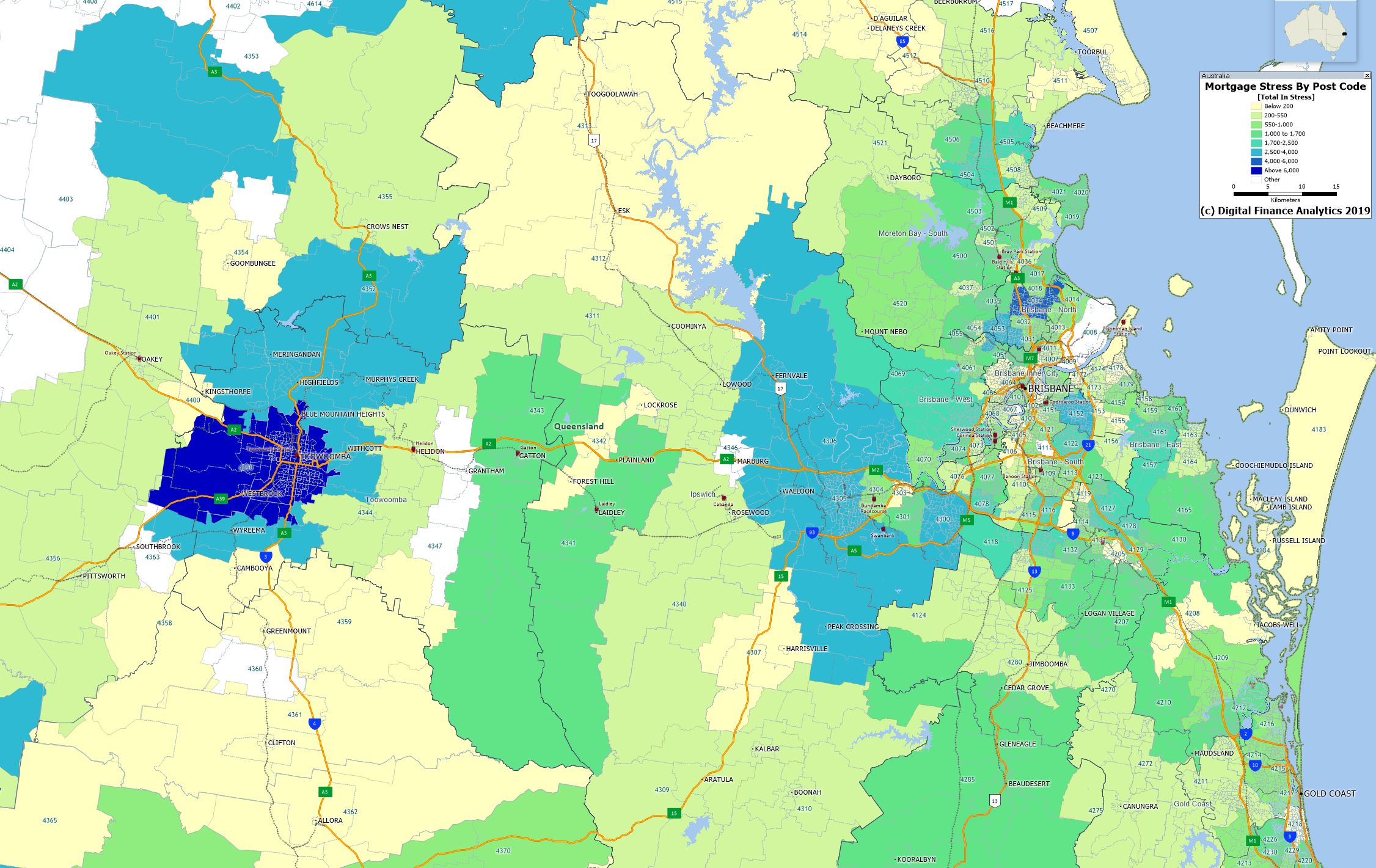

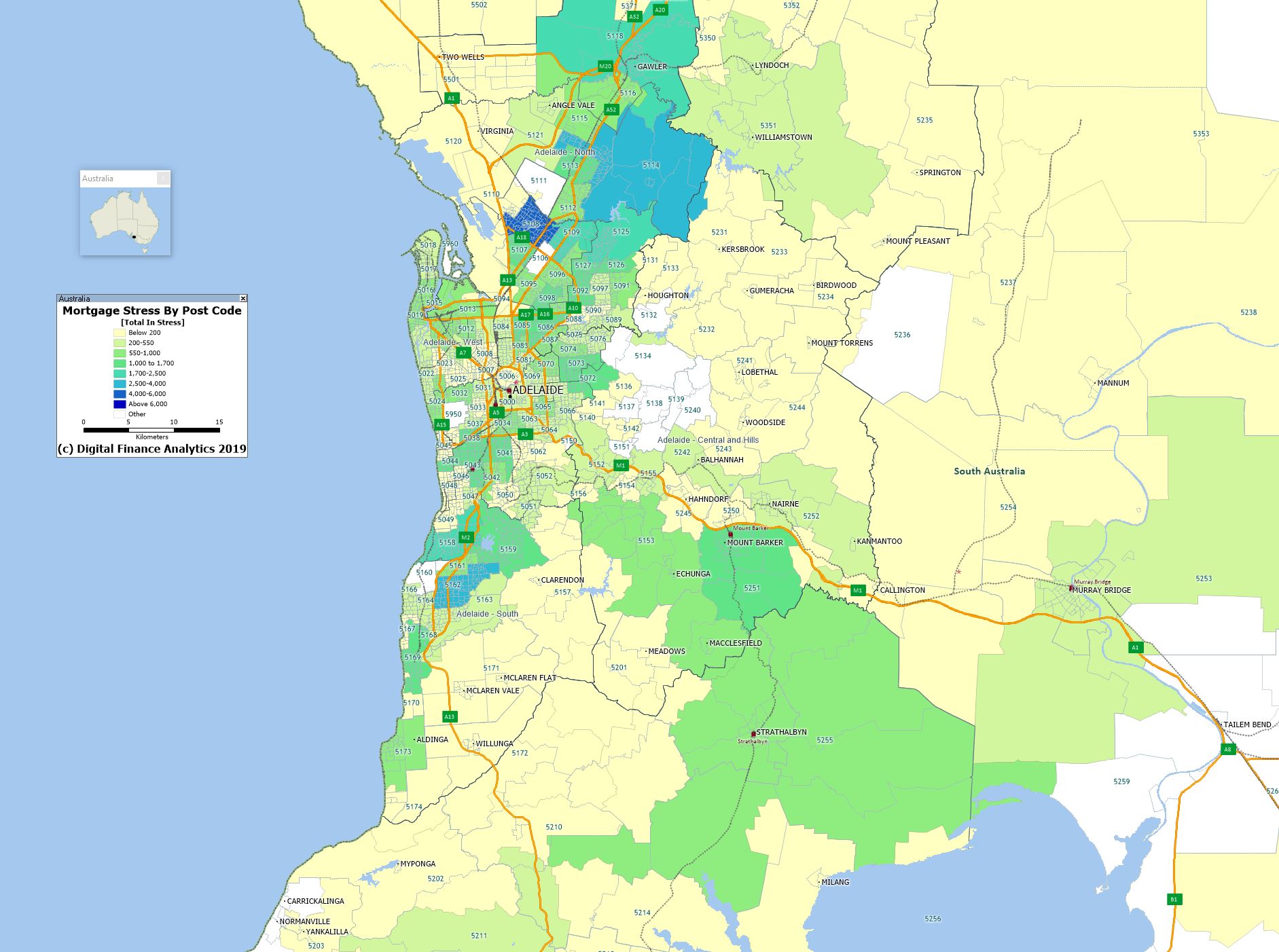

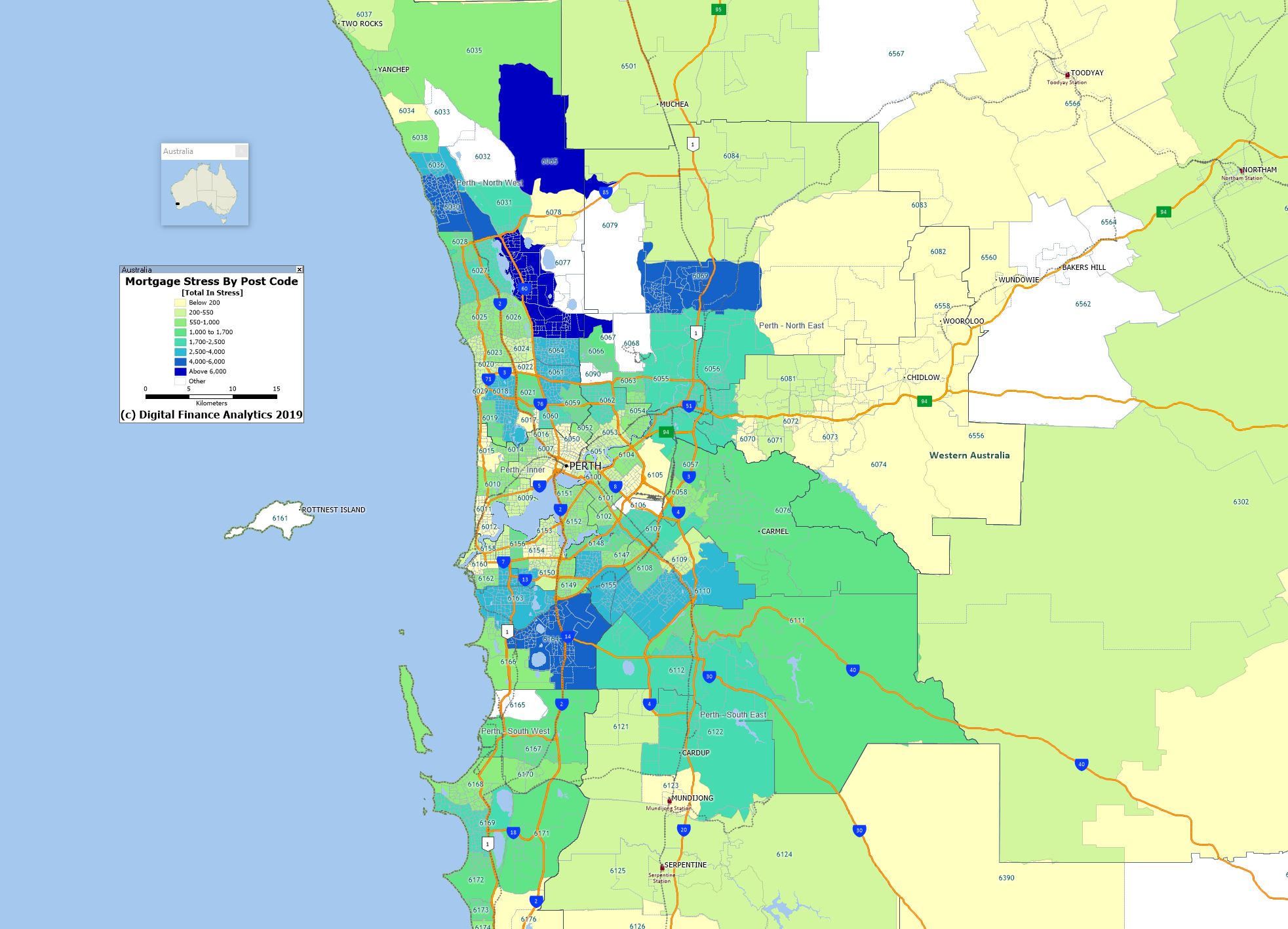

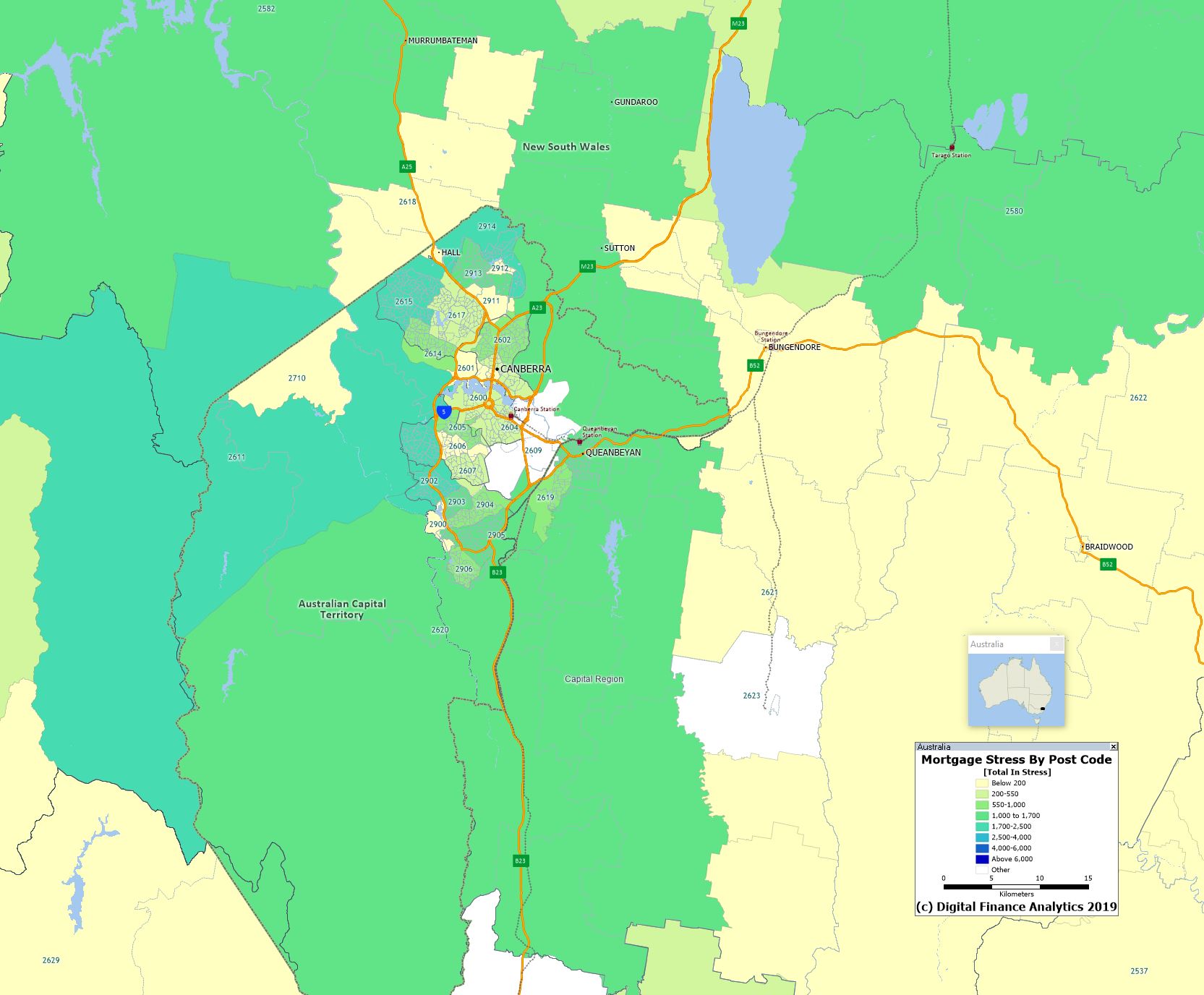

Following 7/30’s report last night I have received a number of requests for access to the maps. So here are the high resolution versions for Sydney, Melbourne and Perth. If they are reproduced elsewhere, please attribute DFA.

As discussed in my video, this is based on the number of households in each post code recording at least one property in negative equity – where the current mortgage (net of any offset accounts) in greater than the estimated current forced sale value plus sale costs. The analysis is based on results from our 52,000 household surveys nationwide.

A quick reminder we are running our live event tomorrow, where we update our property and finance scenarios and answer questions from the audience in real time. You can send questions beforehand, via the DFA blog, or in the live chat on during the session.

Here is a direct link to the event (where you can set a reminder).

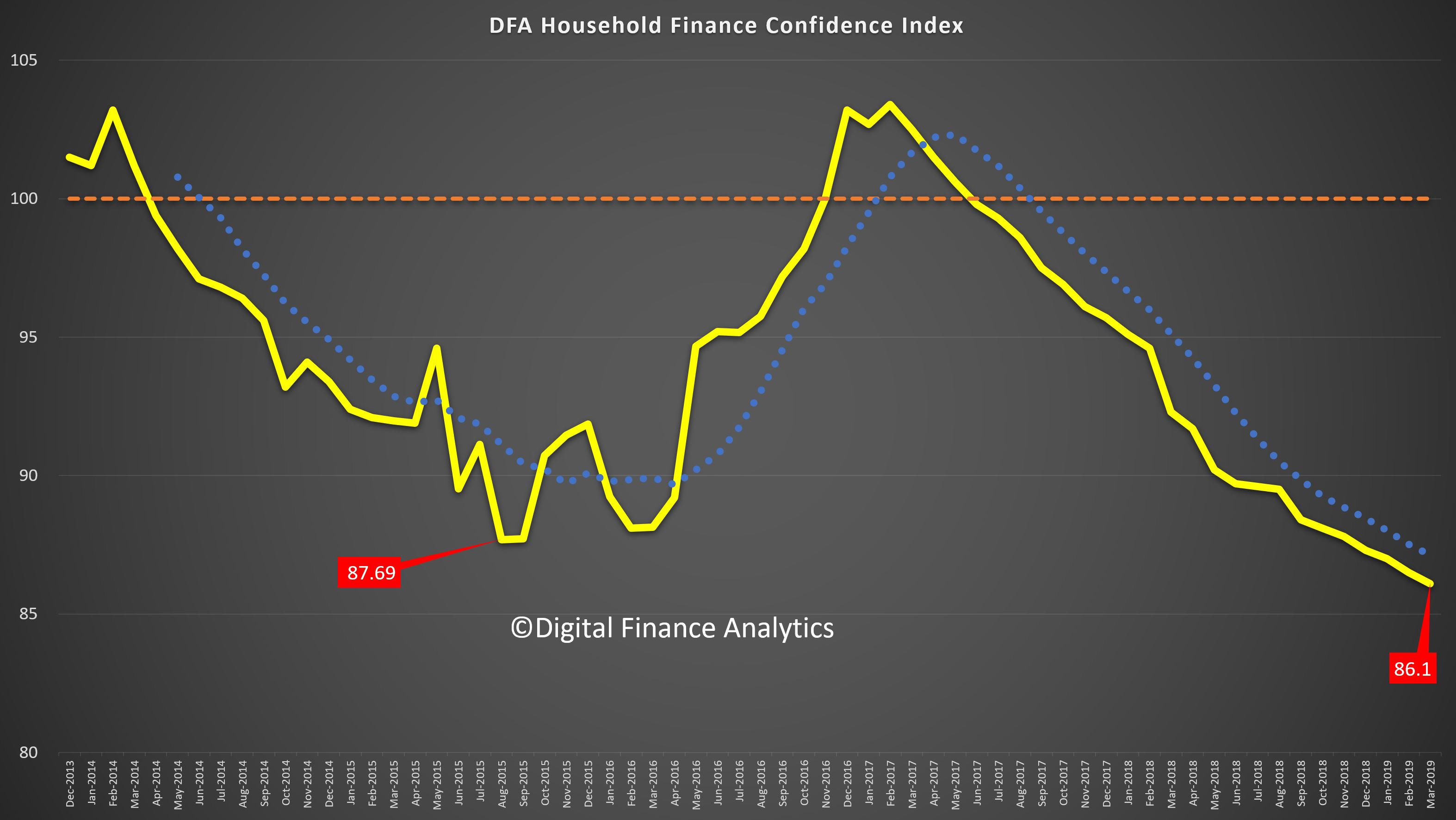

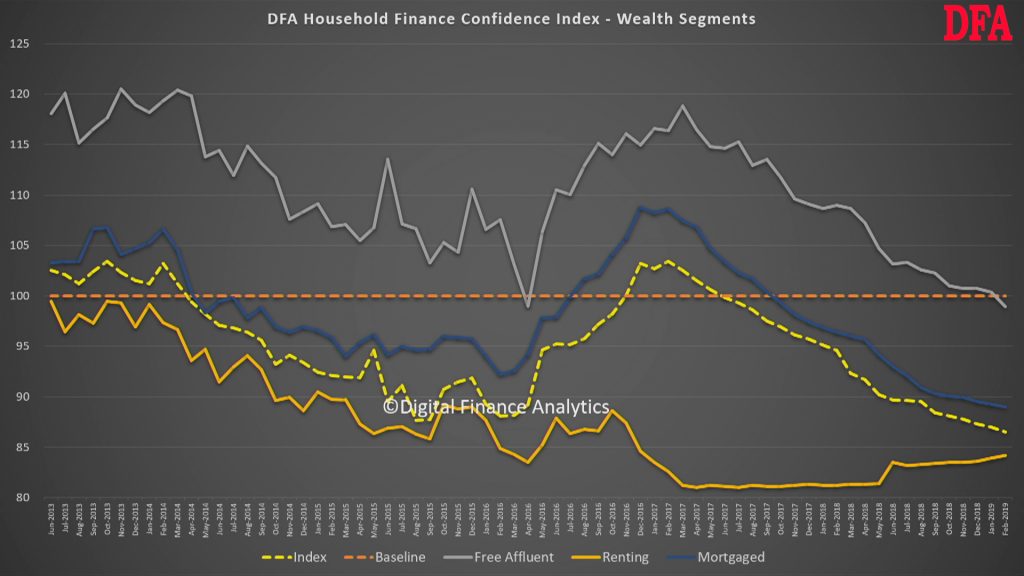

DFA has released the March 2019 Household Financial Confidence Index, which is based on our rolling 52,000 household surveys.

The index reached a new low this past month as the weight of issues on many household’s shoulders pile up. The index fell to 86.1, well below the 100 neutral setting.

This video discusses our findings.

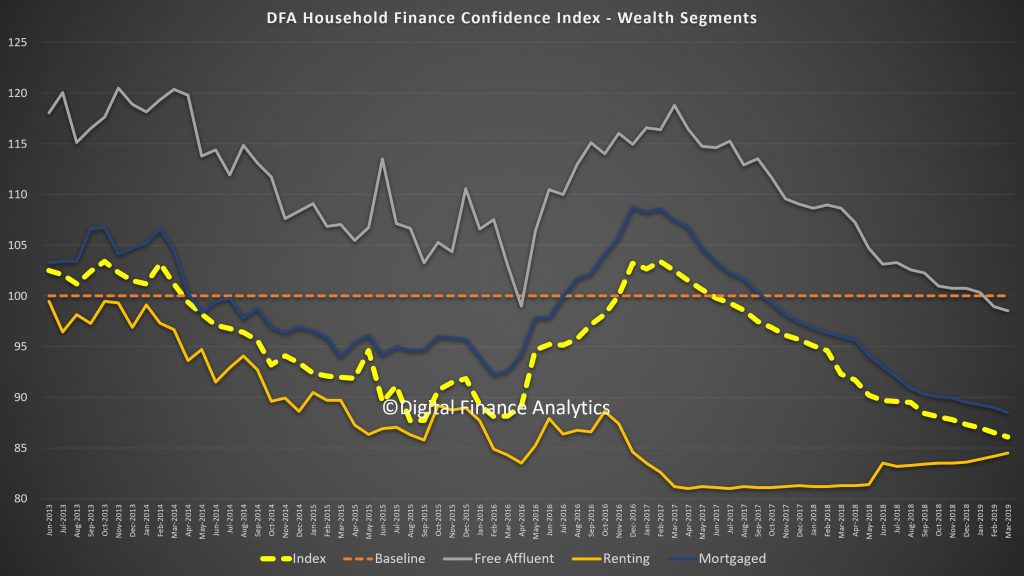

But in essence, all household segments, using our wealth lens, now sit below neutral, with those households with mortgages continuing to track lower, together with those who own property but are mortgage free. In fact the only segment showing a rise is the renting cohort, who see their rents in some centres (especially Sydney) on the decline. We find more among the Free Affluent segment, which is more aligned to the incumbent government, questioning their economic management.

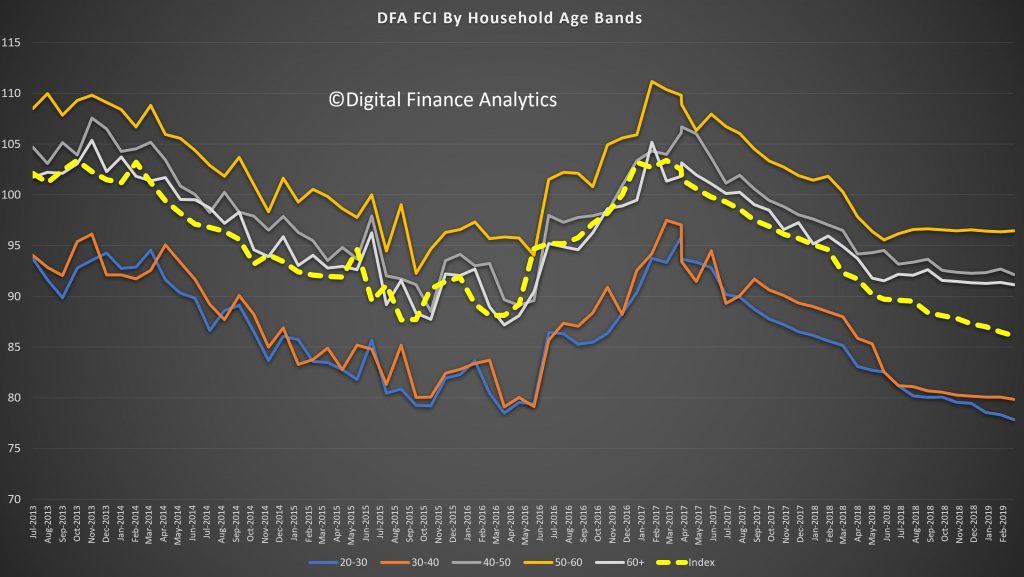

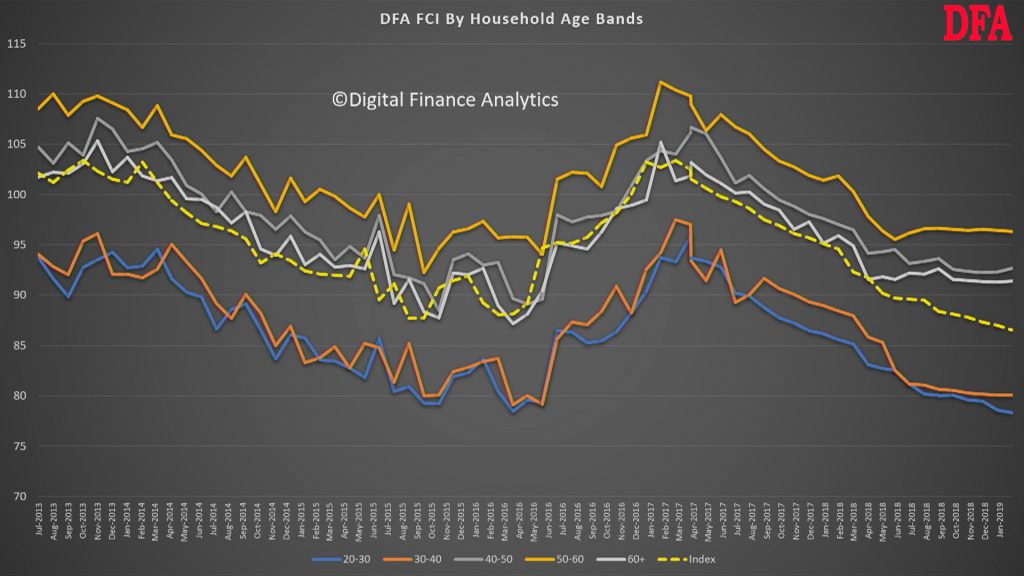

Across the age bands, younger households are more negative, and this highlights some of the inter-generational tensions which we suspect will be played up in the yet to be announced election campaign. In fact, households in the 50-60 year band are most confident (thanks to lower mortgages, bigger savings and controlled costs).

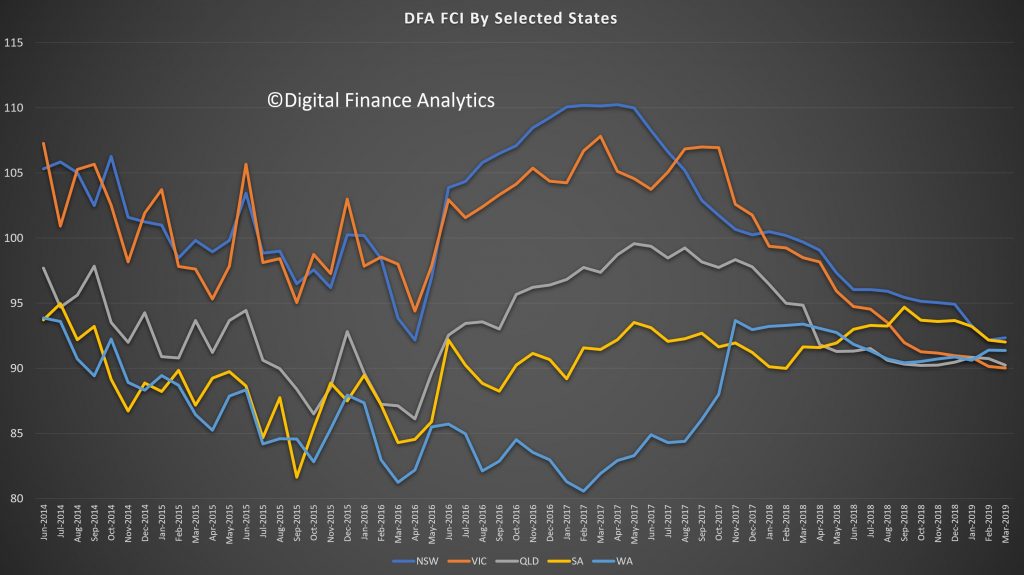

We also see the state indices have consolidated below the neutral setting, as the confidence from households in NSW and VIC are eroded. Much of this is connected with falling home prices.

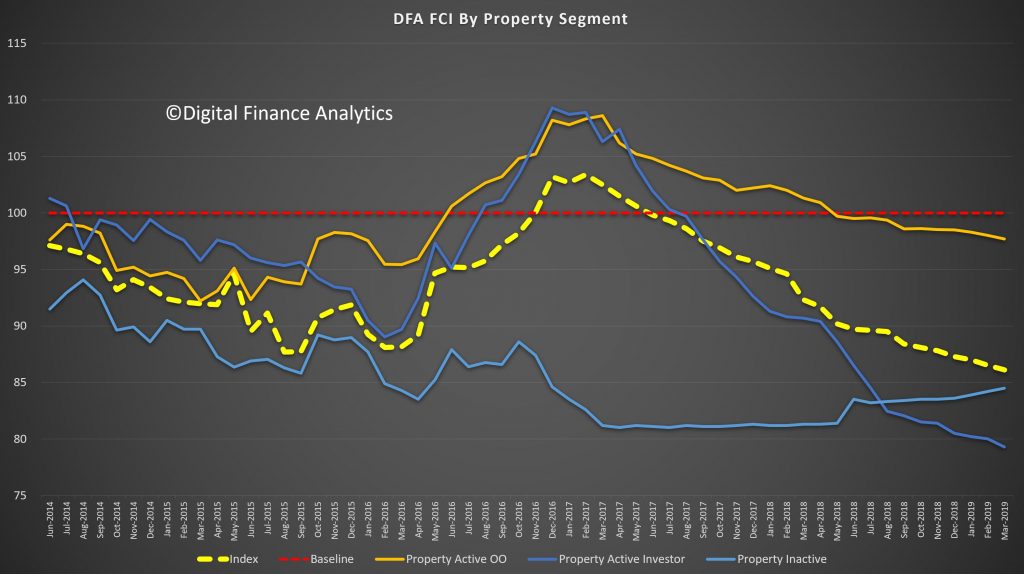

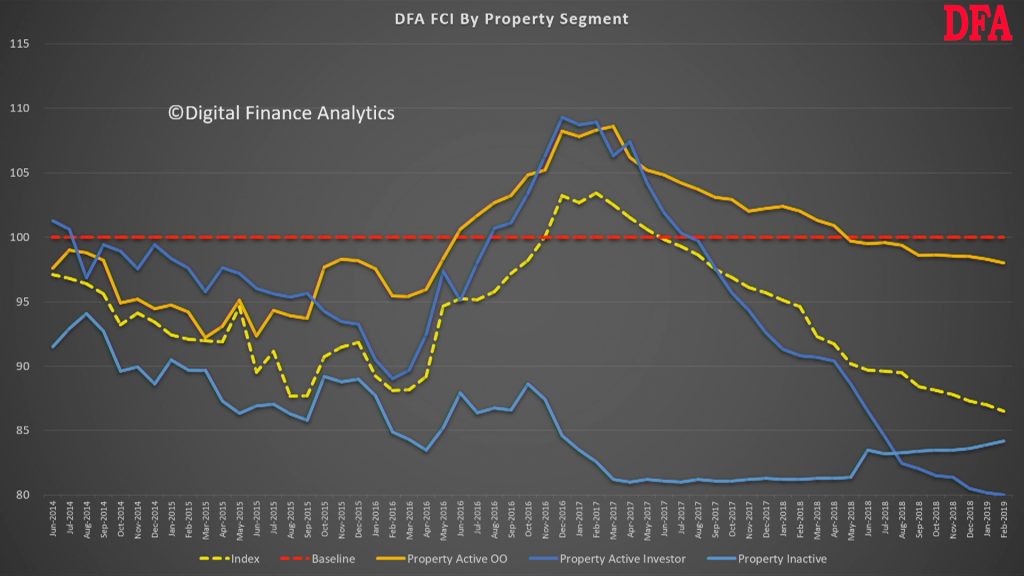

Across our property segmentation, property investors remain the most concerned, with falling home prices, the switch from interest only lending, lower net rental yields and the risks from changes to negative gearing and capital gains all playing in. On the other hand renters are finding some less expensive rentals now, and greater supply. Owner Occupied households are more positive, but still below neutral. This may mark the end of the great property-owning bonanza, at least for now.

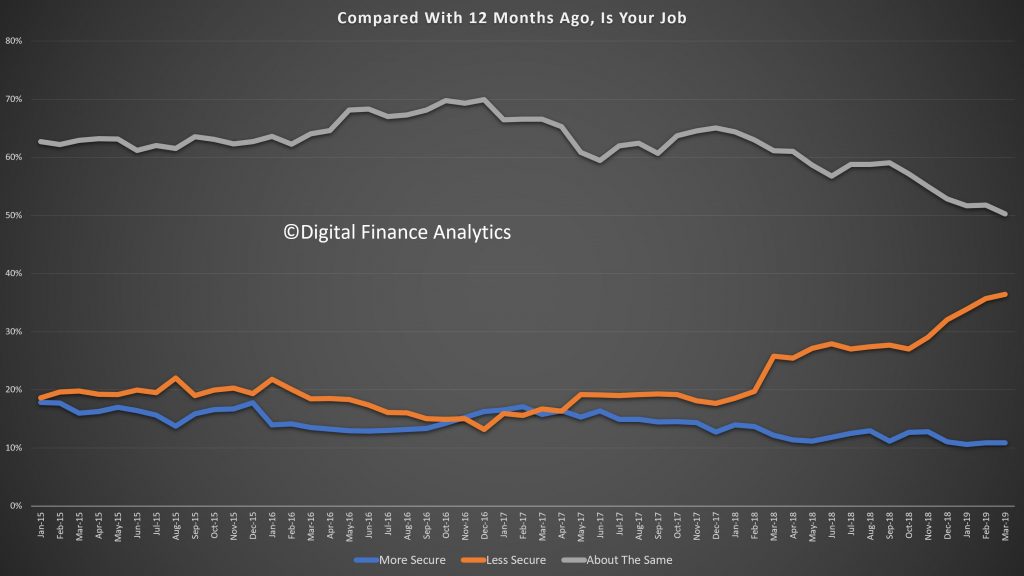

Looking across the moving parts of the index, more households are feeling insecure about their job prospects, thanks to pressure in the construction, retail and real estate sectors.

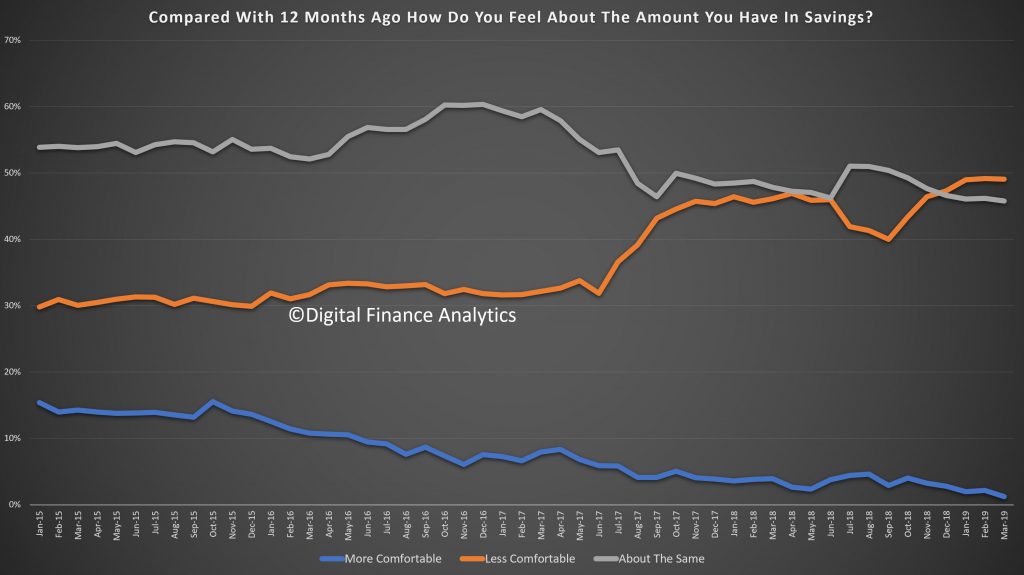

Savings are under pressure from first continued low bank deposit rates, and second, the need to raid savings to keep the household budget in balance. Share values did improve in the month, which offset some of the gloom.

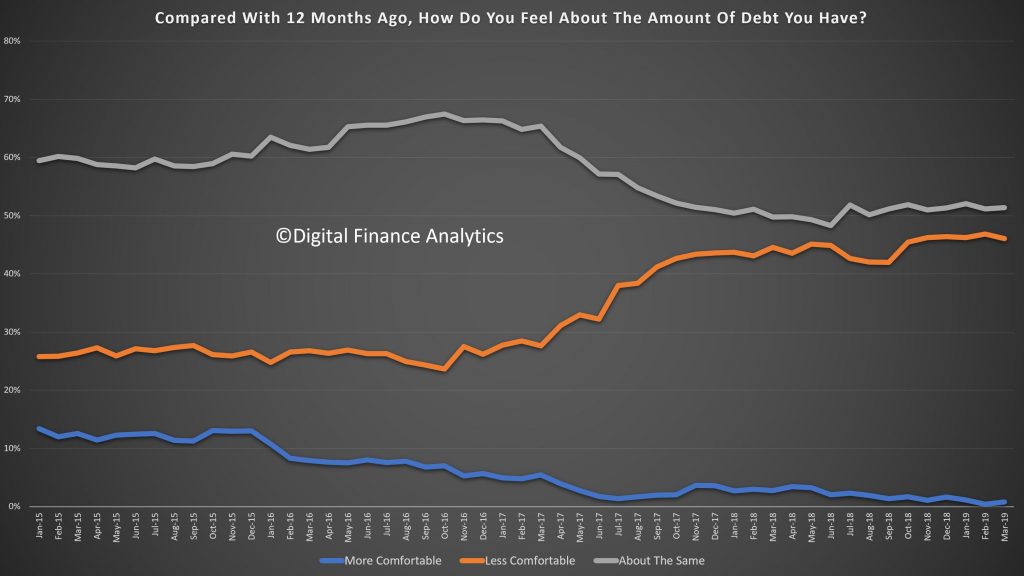

Households are felling the pressure of the high debt (and as the IMF recently showed not just among affluent households). Just under half are now less comfortable with their debt than a year ago, a trend which started to rise in early 2017.

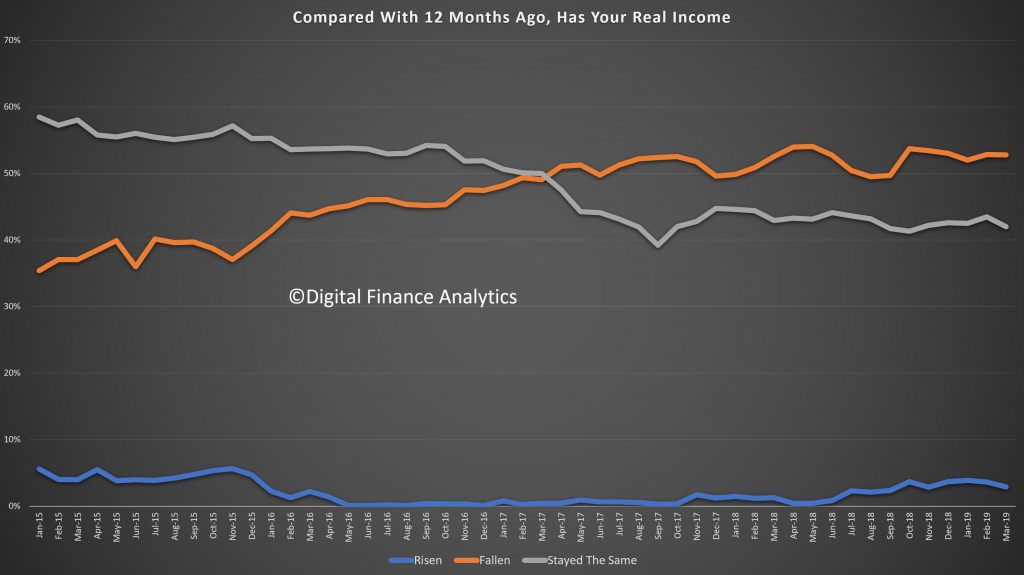

Incomes, in real terms, remain under pressure, with those in the public sector experiencing small rises, but many in the private still in negative territory. More than half say, in real terms, incomes have fallen over the past year.

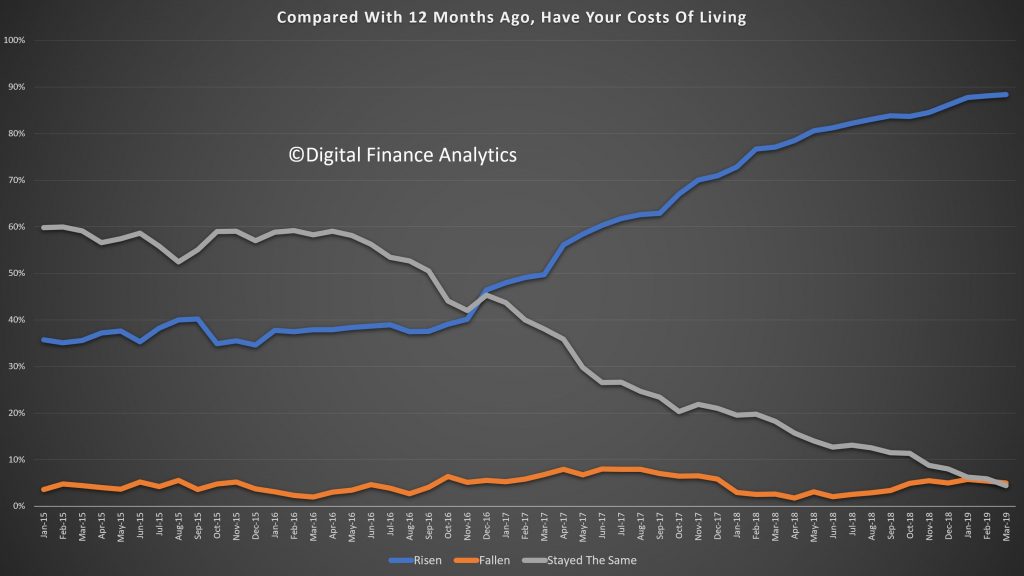

Costs continue to rise, with power prices, healthcare, health insurance, and child care all registering. Plus we are seeing more fallout from the drought which is also impacting some food costs. Nearly 90% of households said their costs are higher than a year ago.

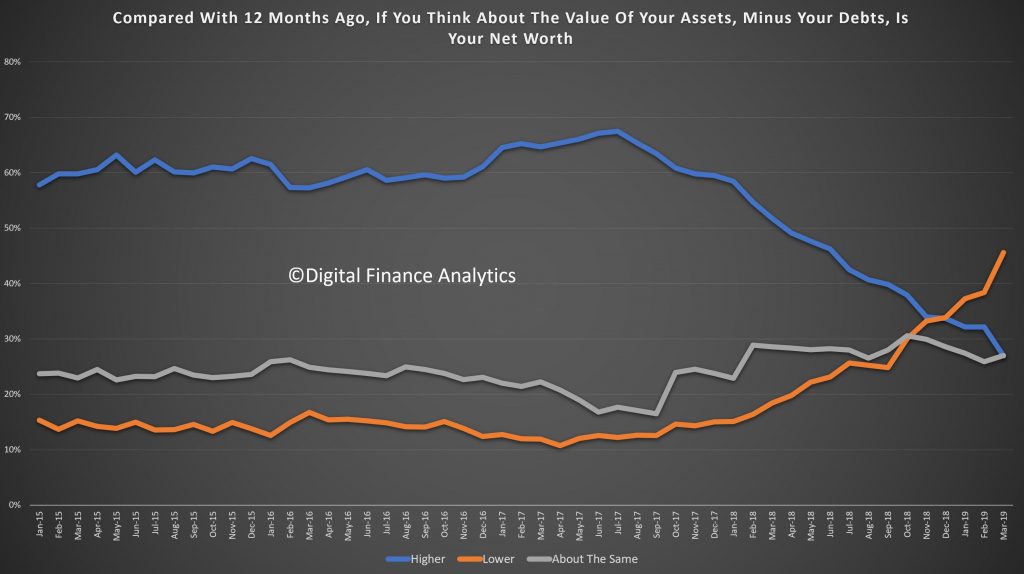

Finally, we put this all together in our assessment of net worth (assets minus loans etc). 45% of households say their net worth is lower, reflecting falls in the property sector, some lower share prices, and diminishing savings. Not a good look in the run up to an election!

There is little evidence of anything which will change the momentum. Rate cuts and handouts to households may provide some short-term relief, but the economic settings are not correct to reverse the trend. So expect more bad news ahead.

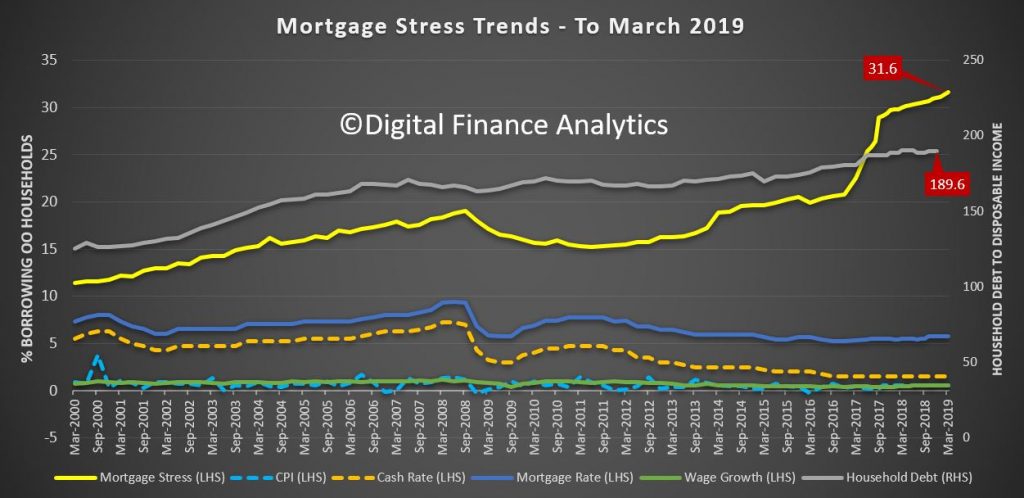

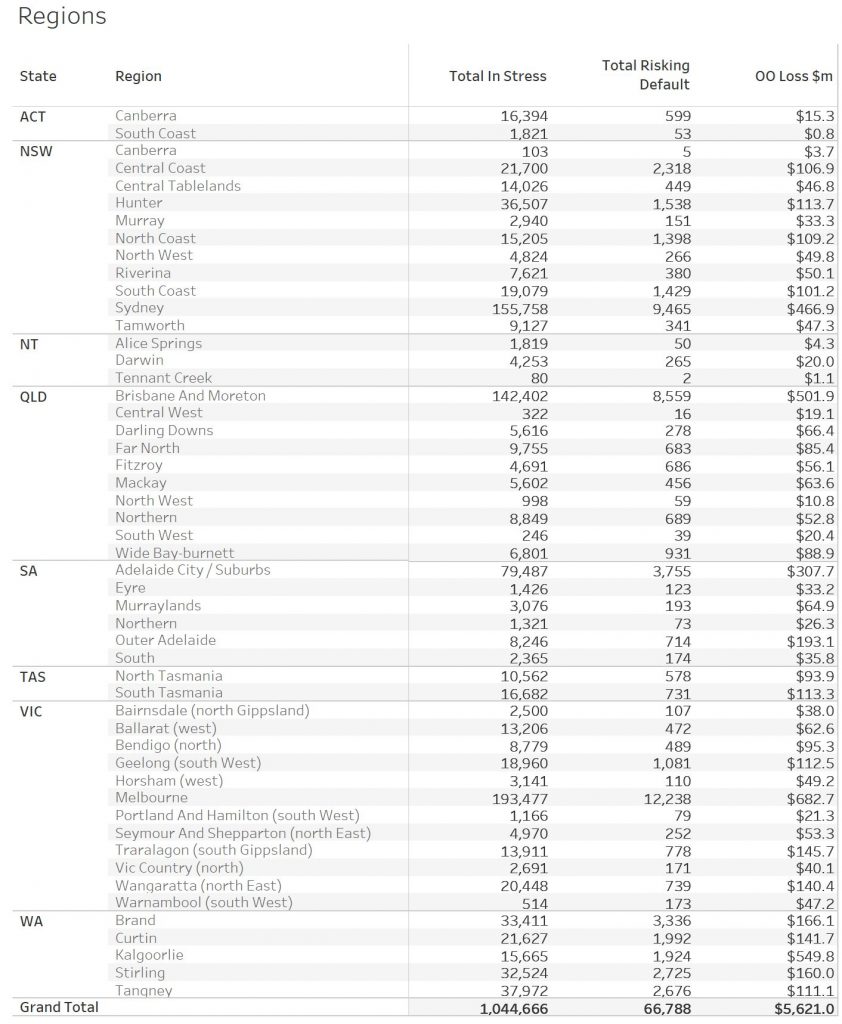

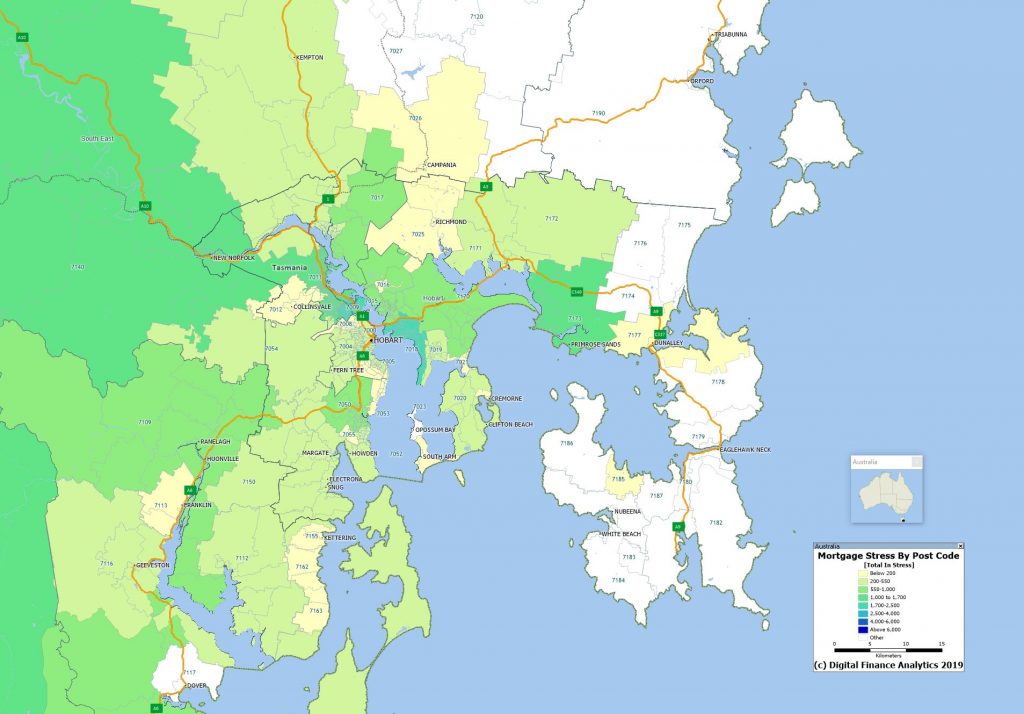

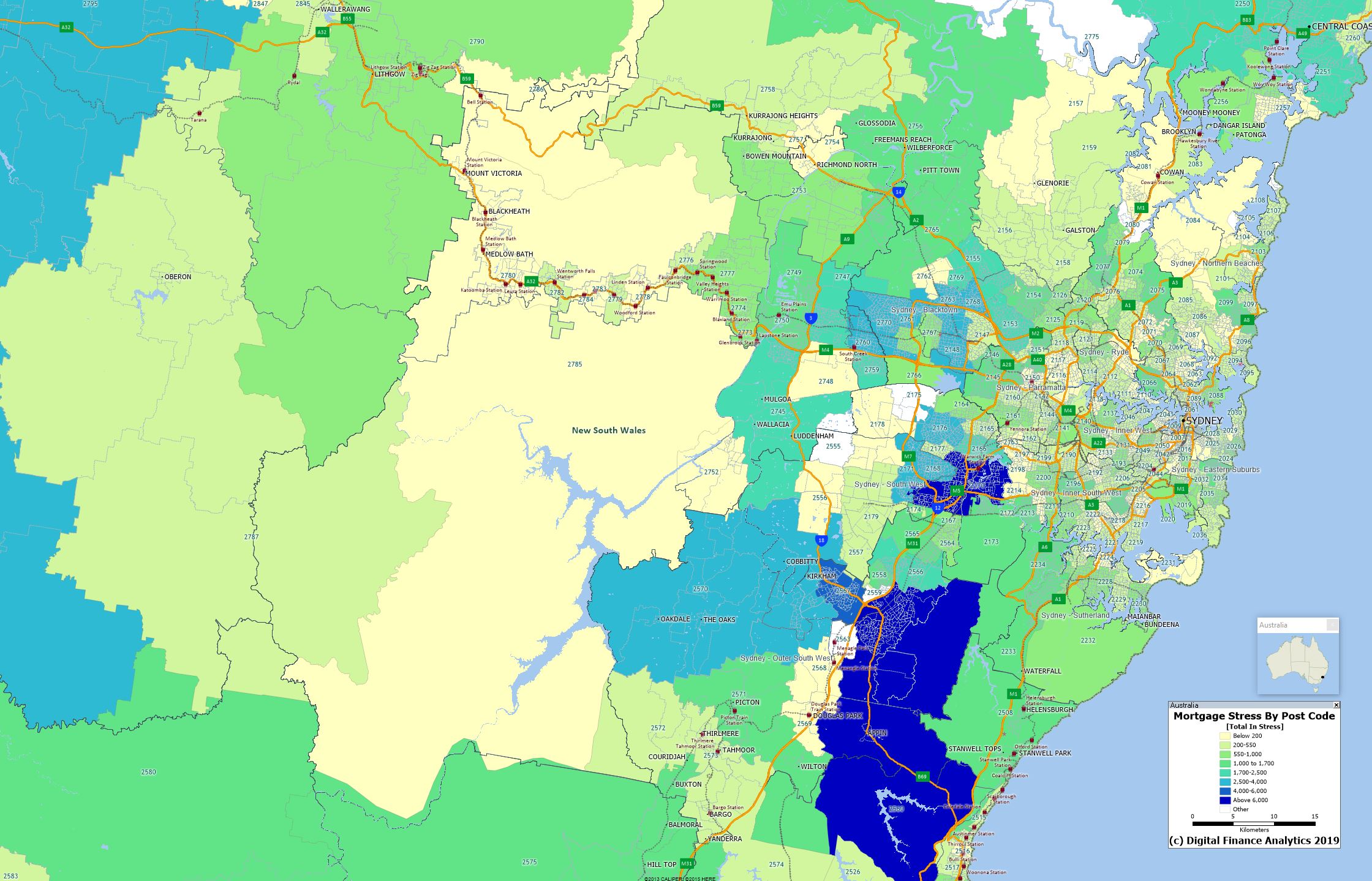

Digital Finance Analytics (DFA) has released the March 2019 mortgage stress and default analysis update. It’s the continuing story of pressure on households as ongoing wages growth is not offsetting costs of living, and mortgage repayments and total debt continues to rise.

Note: Later in the month we will release mapping showing the percentage of households in stress across postcodes (as opposed to the number estimated to be in stress). We generally avoid this data view because a raw percentage calculation can easily be distorted by postcodes with low counts of borrowing household, but then we have had several requests for this alternative view.

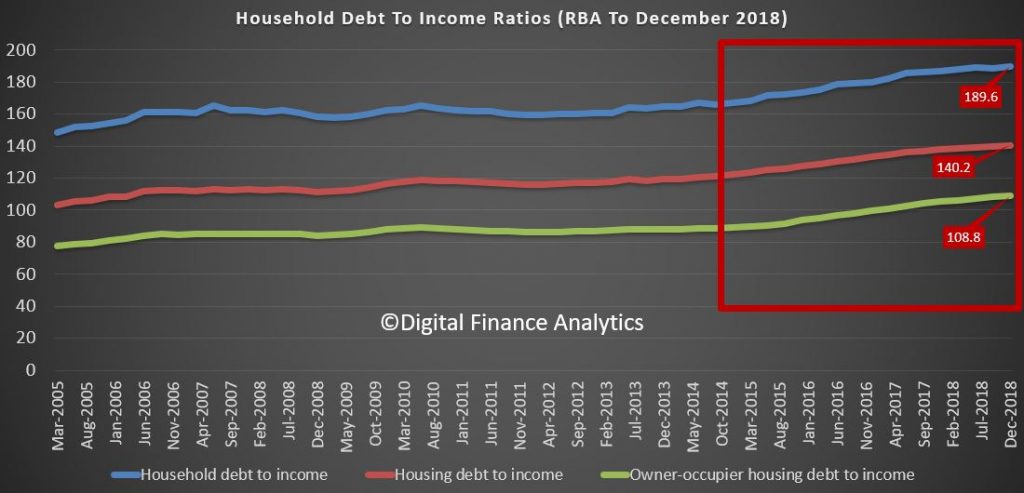

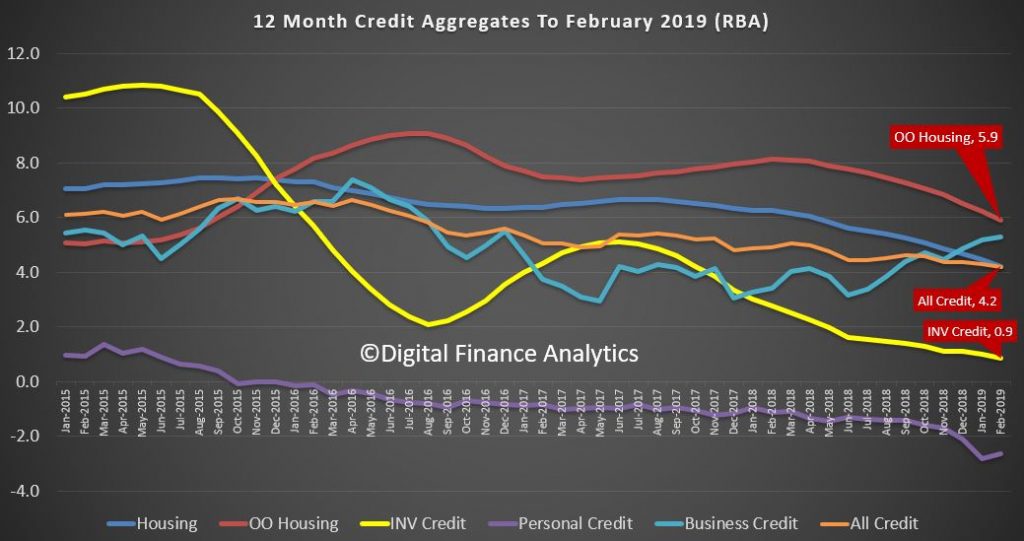

The latest RBA data on household debt to income to December rose to 189.6[1], and remains highly elevated. Plus, the housing debt ratio continues to climb to a new record of 140.2, according to the RBA. This shows that household debt to income is still increasing.

This is confirmed by the latest

financial aggregates recently released by the RBA, with owner occupied lending

still growing significantly faster than inflation at 5.9%.

This high debt level, in the

context of broader financial pressure, helps to explain the fact that mortgage

stress continues to rise. Across Australia, more than 1,044,666 households are estimated

to be now in mortgage stress (last month 1,036,214), another new record. This

equates to more than 31.6% of owner-occupied borrowing households. In addition,

more than 27,775 of these are in severe stress. We estimate that more than 66,700

households’ risk 30-day default in the next 12 months, up 800 from last month. This

is as the impact of flat wages growth, rising living costs and higher real

mortgage rates hit home. Bank losses are

likely to rise a little ahead.

Our analysis uses the DFA core

market model which combines information from our 52,000 household surveys,

public data from the RBA, ABS and APRA; and private data from lenders and

aggregators. The data is current to the end of March 2019. We analyse household

cash flow based on real incomes, outgoings and mortgage repayments, rather than

using an arbitrary 30% of income.

Households are defined as

“stressed” when net income (or cash flow) does not cover ongoing costs. They

may or may not have access to other available assets, and some have paid ahead,

but households in mild stress have little leeway in their cash flows, whereas

those in severe stress are unable to meet repayments from current income. In

both cases, households manage this deficit by cutting back on spending, putting

more on credit cards and seeking to refinance, restructure or sell their

home. Those in severe stress are more

likely to be seeking hardship assistance and are often forced to sell.

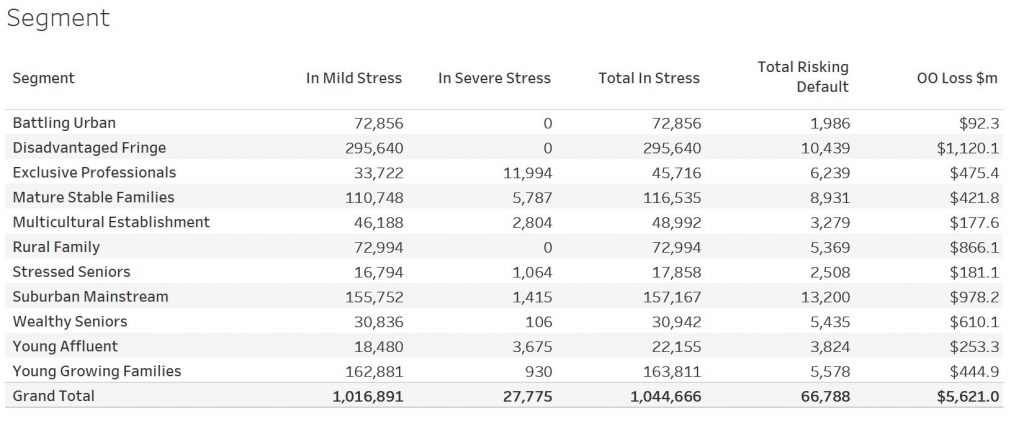

The forces continue to build, despite reassurances that household finances are fine. This is because we continue to see an accumulation of larger mortgages compared to income whilst costs are rising, and incomes remain static. Housing credit growth is running significantly faster than incomes and inflation and continued rises in living costs – notably child care, school fees and electricity prices are causing significant pain. Many households are depleting their savings to support their finances.

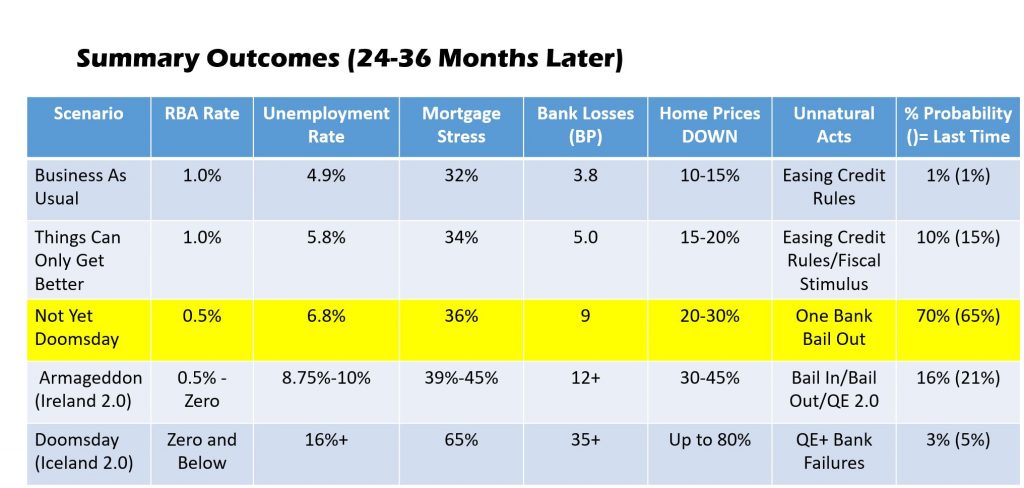

Probability of default extends our

mortgage stress analysis by overlaying economic indicators such as employment,

future wage growth and cpi changes. Our

Core Market Model also examines the potential of portfolio risk of loss in

basis point and value terms. Losses are likely to be higher among more affluent

households, contrary to the popular belief that affluent households are well

protected. This is shown in the segment

analysis below:

Stress by the numbers.

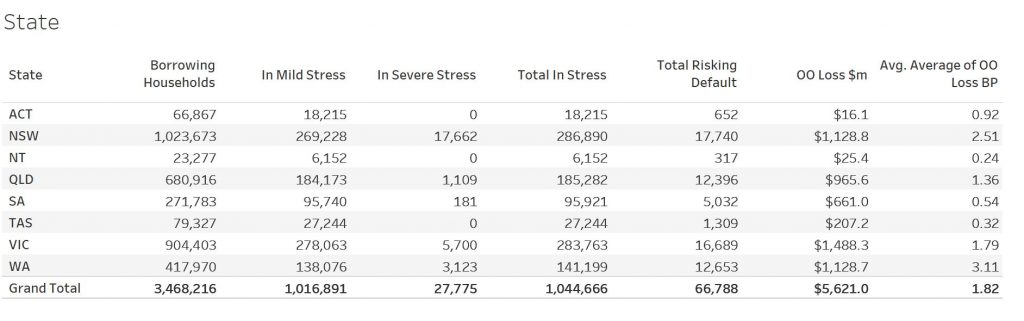

Regional analysis shows that NSW has

286,890 households in stress (286,469 last month), VIC 283,753 (278,091 last

month), QLD 185,282 (185,424 last month) and WA has 141,199 (139,142 last month).

The probability of default over the next 12 months rose, with around 12,600 in

WA, around 12,400 in QLD, 16,700 in VIC and 17,700 in NSW.

The largest financial losses

relating to bank write-offs reside in NSW ($1.1 billion) from Owner Occupied

borrowers) and VIC ($1.49 billion) from Owner Occupied Borrowers, though losses

are likely to be highest in WA at 3.1 basis points, which equates to $1,045

million from Owner Occupied borrowers.

A fuller regional breakdown is set out below.

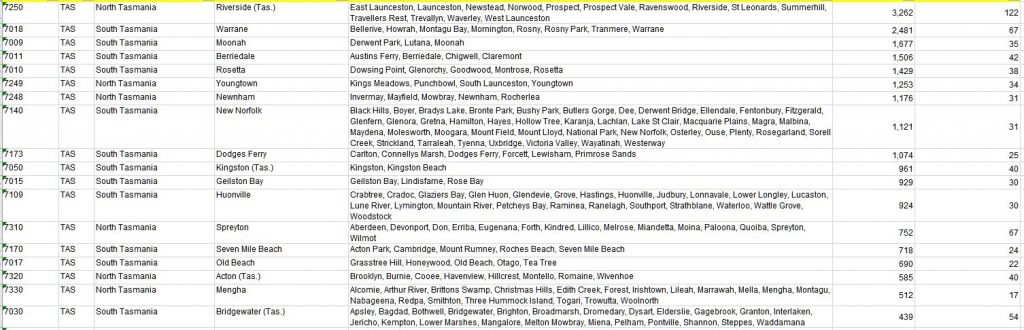

Here are

the top postcodes sorted by number of households in mortgage stress.

Handling

Mortgage Stress

Households who are in financial difficulty should not ignore

the signs. Though many do. And trying to refinance to solve the problem often

ends up just postponing the inevitable.

We think there are some simple steps households can take:

Step one is to draw up a budget, so you can see where the

money is coming and going. From our research, only half of households have any

budget. This means you can then make decisions about what is most important,

and what can be foregone. Select and prioritise.

Step two is to talk with your lender, as they have a legal

obligation to assist is case of hardship. Yet many households avoid having that

conversation, hoping the problem will cure itself. I have to say, in the

current low-income growth, high cost environment, that is unlikely. And remember rates are likely to rise at some

point.

Step three. Work out what would happen if mortgage rates rose

by say half or one percent. Pass that across your budget and examine the

impact. Then you will really know where you stand. Then plan accordingly.

[1]

RBA E2 Household Finances – Selected Ratios December 2018

You can request our media release. Note this will NOT automatically send you our research updates, for that register here.

[contact-form to=’mnorth@digitalfinanceanalytics.com’ subject=’Request The March 2019 Stress Release’][contact-field label=’Name’ type=’name’ required=’1’/][contact-field label=’Email’ type=’email’ required=’1’/][contact-field label=’Email Me The March 2019 Media Release’ type=’radio’ required=’1′ options=’Yes Please’/][contact-field label=”Comment If You Like” type=”textarea”/][/contact-form]

Note that the detailed results from our surveys and analysis are made available to our paying clients.

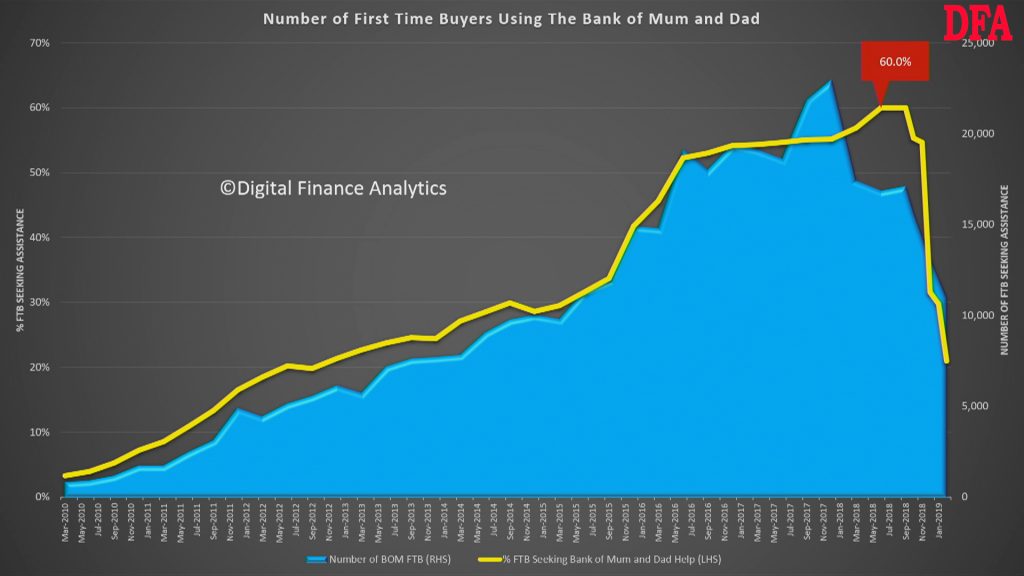

Latest data released today from the DFA household surveys shows that a smaller number of potential first time buyers are now getting help from their parents to buy property.

This video explains what is going on.

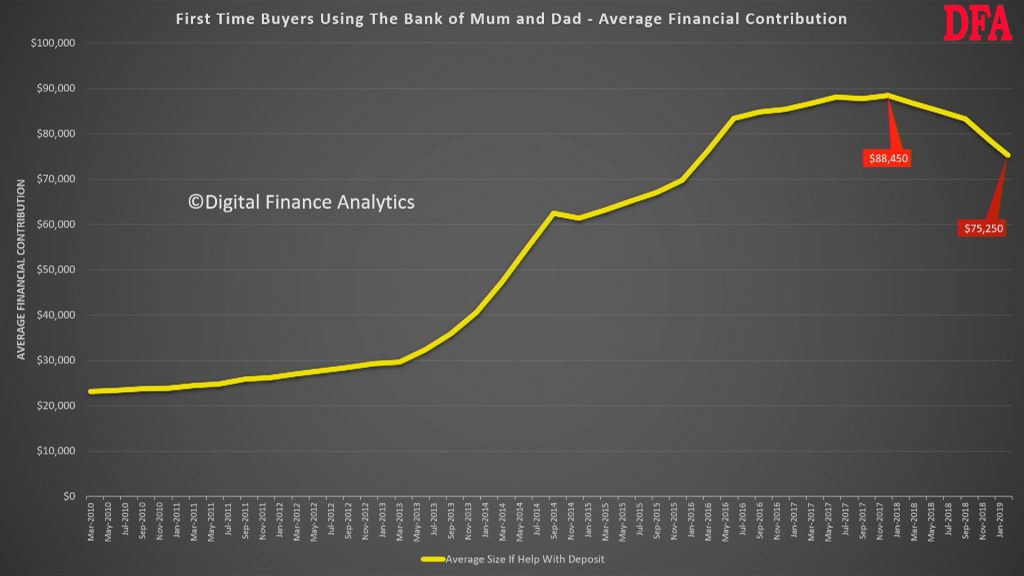

At its height 60% of first time buyers were getting help from their parents, but this has now dropped to 20%. In addition the value of that help has fallen from around $88,000 to around $75,000, on average.

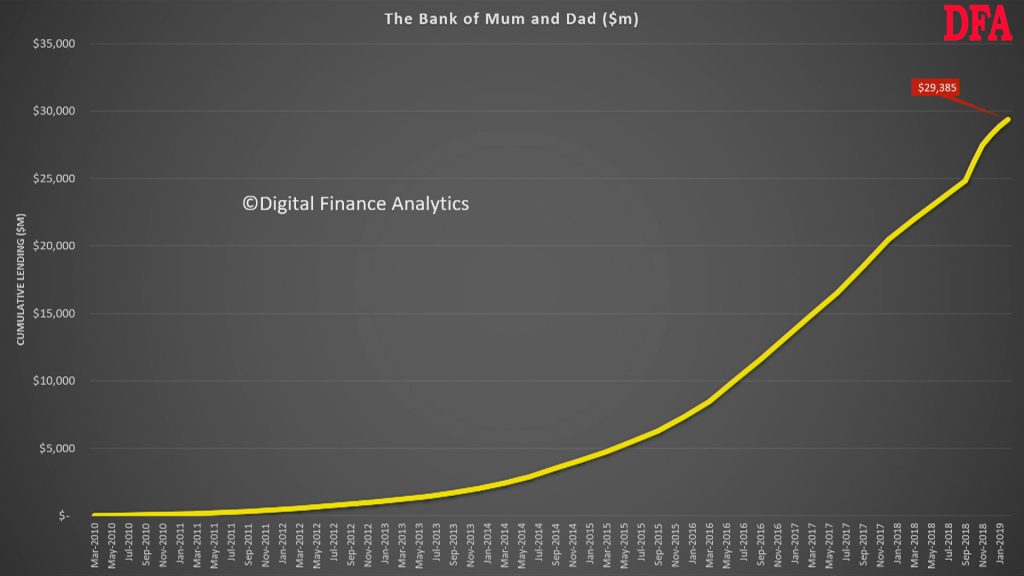

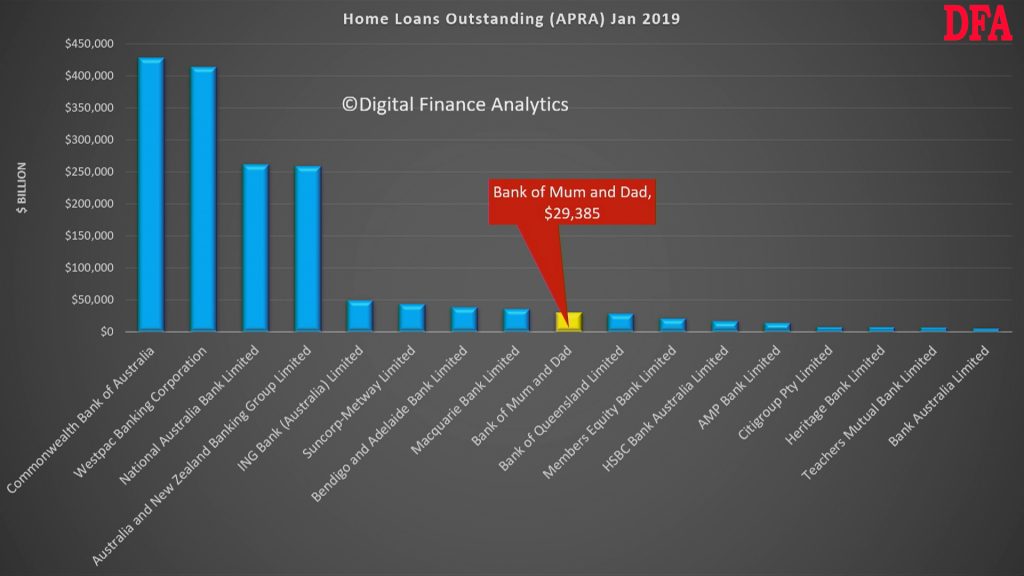

That said the total amount lent by the Bank of Mum and Dad is approaching $30 billion.

This puts the Bank of Mum and Dad among the top-10 lenders in Australia, based on the latest APRA data, in terms of loan stock.

Three drivers explain these changes. First parents are more concerned in a falling market about the equity in their property, when facing into retirement. The “ATM” has run dry. They cannot afford to pass money down the generation now.

Second despite some incentives, such as those in the Northern Territories, announced recently, many first time buyers are preferring to wait, rather than buy into a falling market and risk loosing their deposits. Plus we know that those who get help from parents are twice a likely to default in the subsequent 5 years compared with those who saved.

Third, banks are reluctant to lend, and a seagull payment is not regarded well, compared with a record of regular savings. Some lenders have stopped lending to borrowers with a Bank of Mum and Dad deposit.

Thus we think the momentum we saw last year is slowing and the Bank of Mum and Dad may be a less important factor ahead.

Some parents may decided to help pay monthly mortgage payments instead as this is a more flexible alternative and does not risk capital.

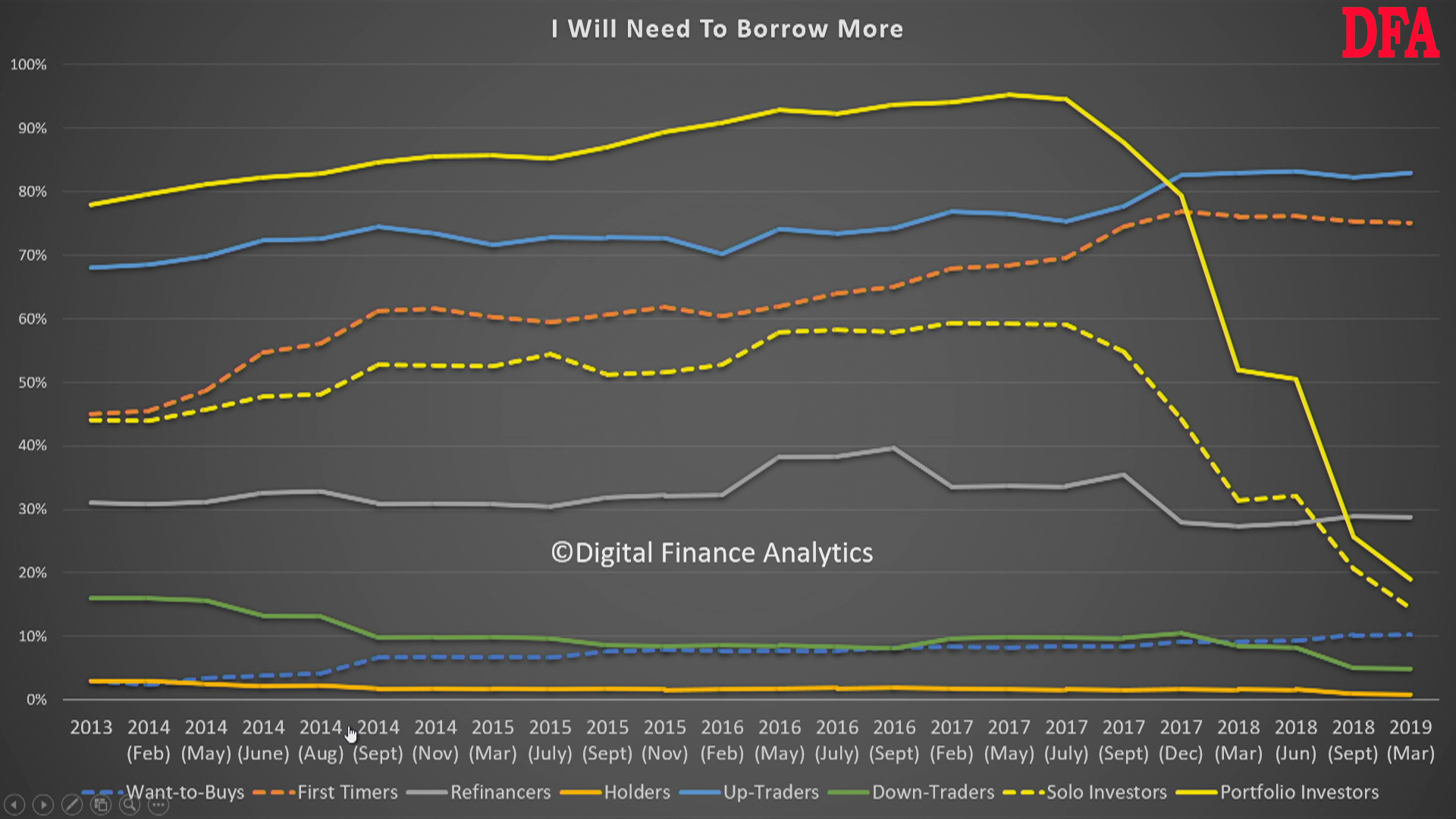

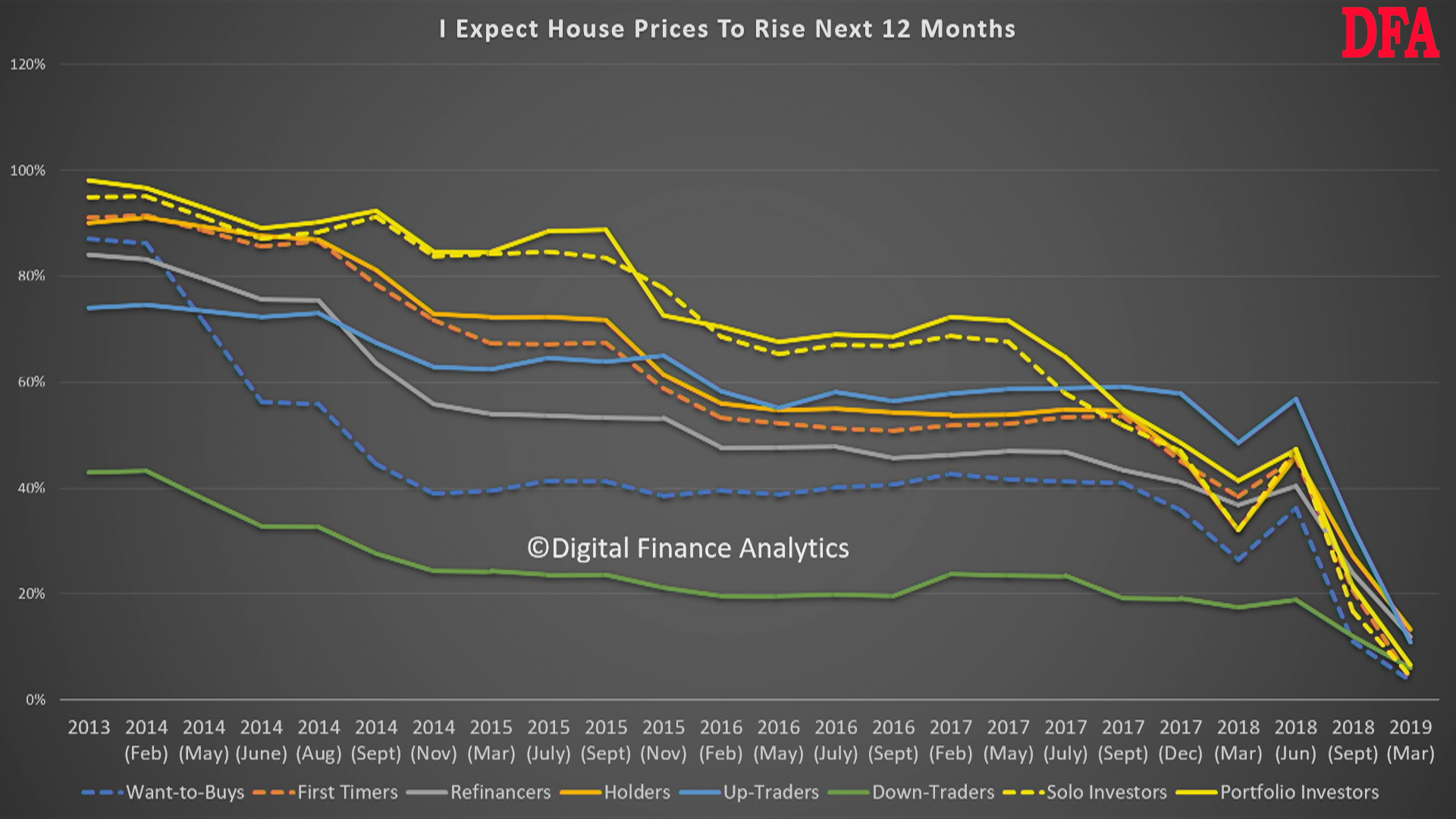

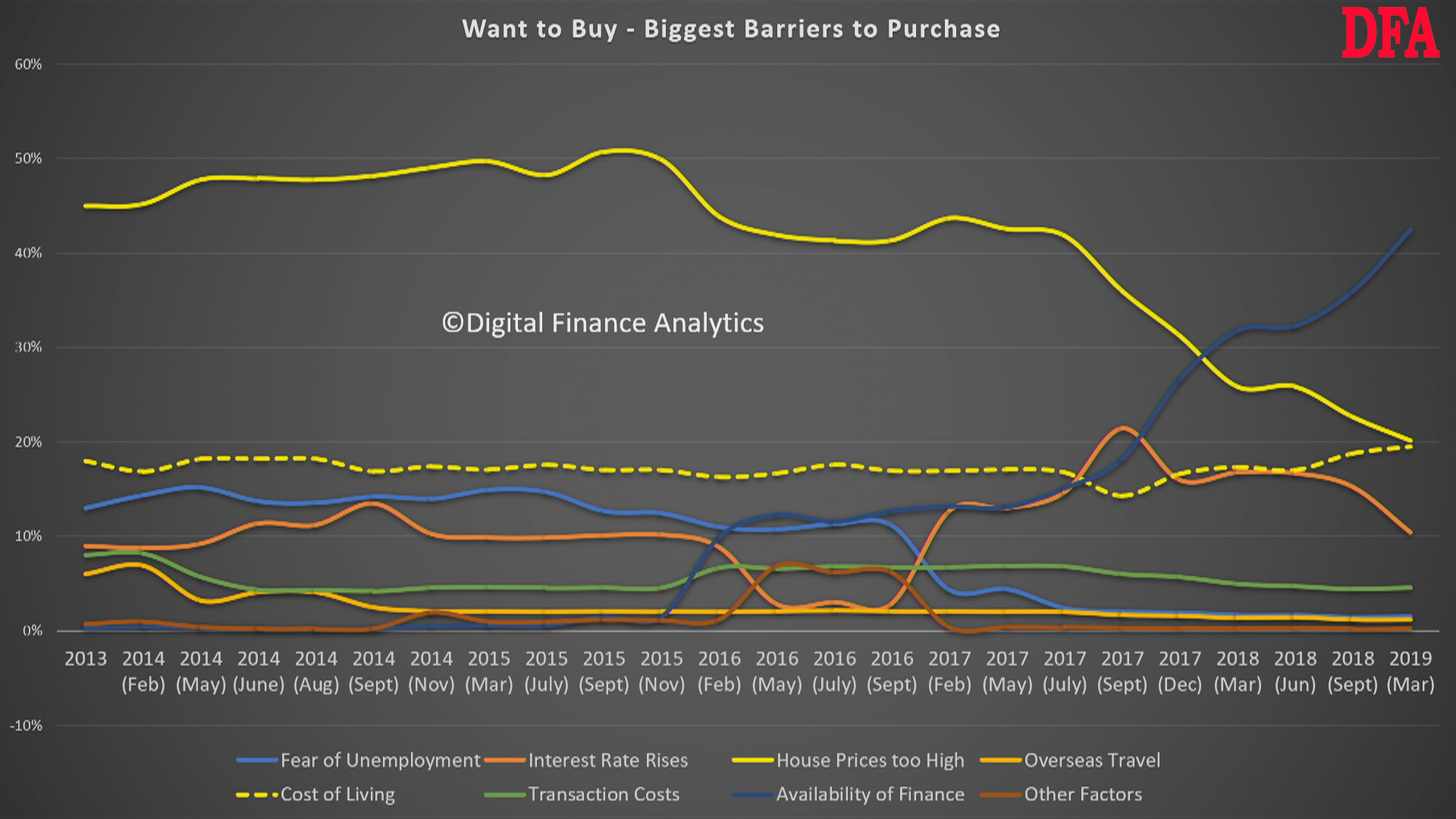

We have released the latest edition of our household surveys, looking specifically their attitude to property transactions and expectations. And overall demand, and intention to transact have tanked. More evidence of a weaker market ahead.

Our video provides a complete analysis of the results, but here are the main points.

Intention to transact continues to fall, as property investors continue to step away from the market. Down Traders and First Time Buyers remain active, as do those seeking to Refinance; but overall expect lower numbers of transactions ahead.

As a result, demand for credit is also likely to fall further, as investors walk. Up Traders and First Time Buyers are the main cohorts likely to want a loan, plus some refinancing.

Home price expectations are diving, across all segments, these are the lowest results I have ever seen in the data series. This is a significant shift compared with even 18 months ago. People think property is likely to fall further.

Looking at the barriers to transacting, there are some common themes emerging. Those wanting to buy are being constrained by the lack of available finance. Rising costs of living are also not helping.

First Time Buyers are also finding getting a loan tougher as underwriting standards have tightened. High prices as a barrier have slid a little.

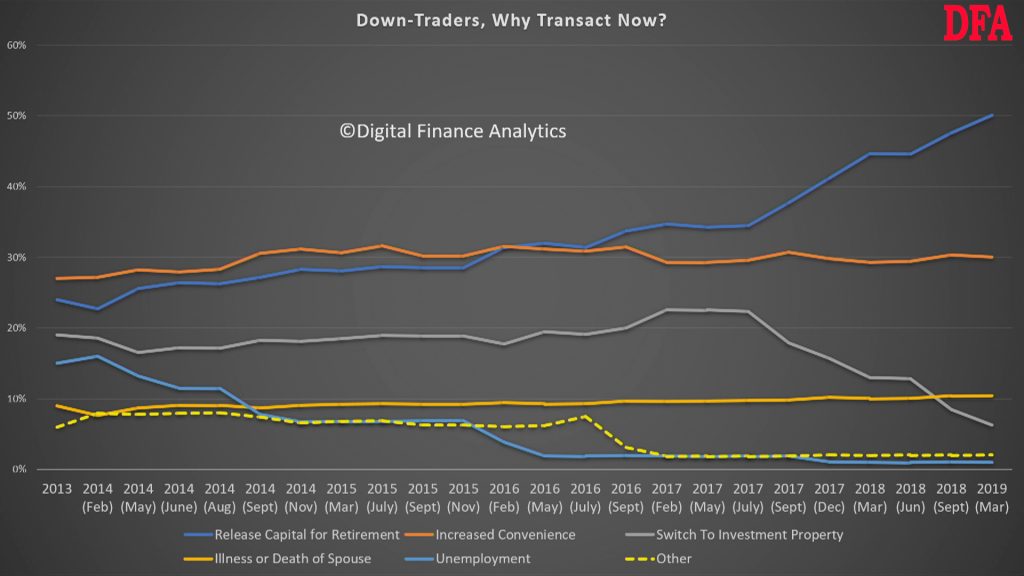

Down Traders are seeking to release equity before prices slide further. This is a big cohort and they are becoming more desperate to sell.

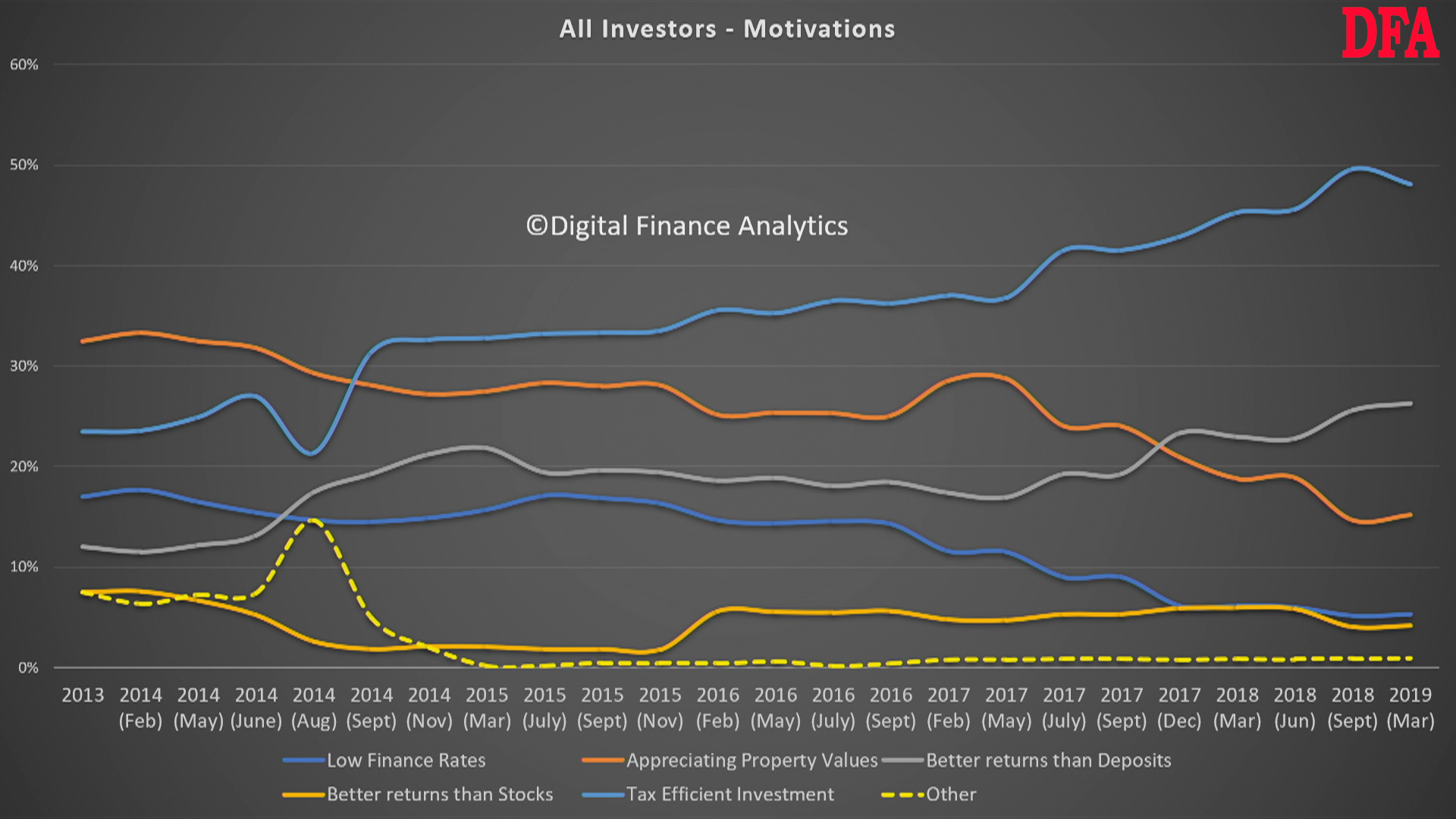

Investors are less convinced by future capital appreciation. Its mainly now tax efficiency which they cling to. Some will be forced to sell, but many are sitting on the sidelines and waiting to see how this plays out.

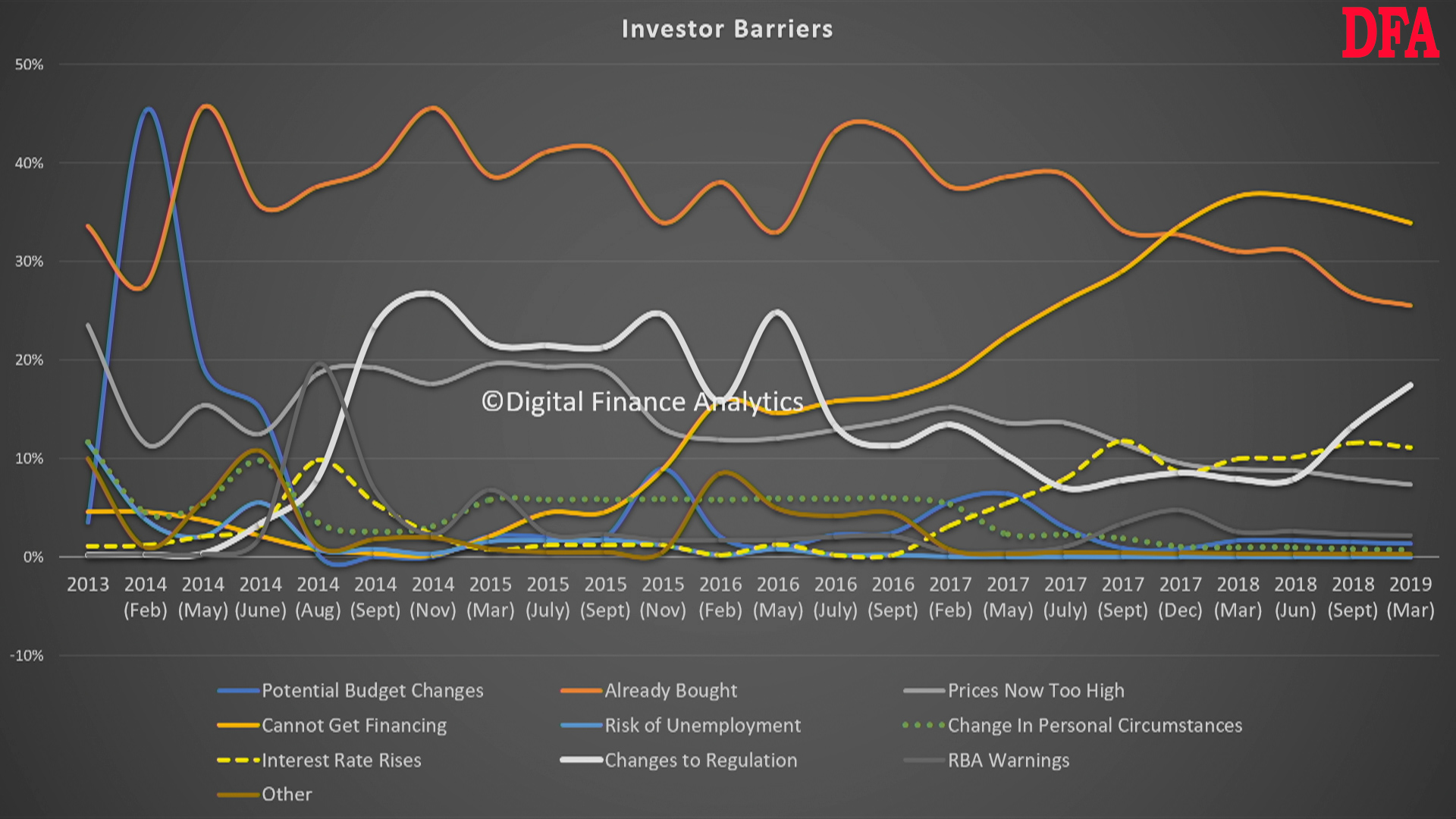

And barriers now include concerns around regulatory changes and finance avaliability.

So in summary there is nothing here which suggests any type of recovery in home prices. The collapse in prices has already been sufficient to put many households off from future purchases, and those who need finance are finding it hard to get funds. More falls to come.

Nothing here changes our scenarios. More falls. Period.

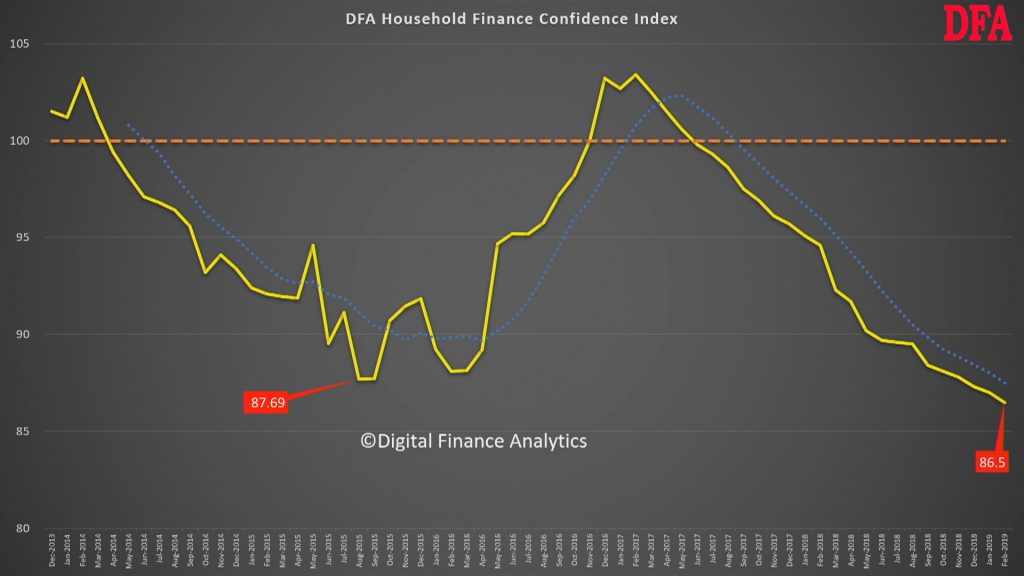

The latest from our household surveys reveals a further fall in household confidence, with the data to end February 2019.

The overall index fell to 86.5, the lowest since we have run the series.

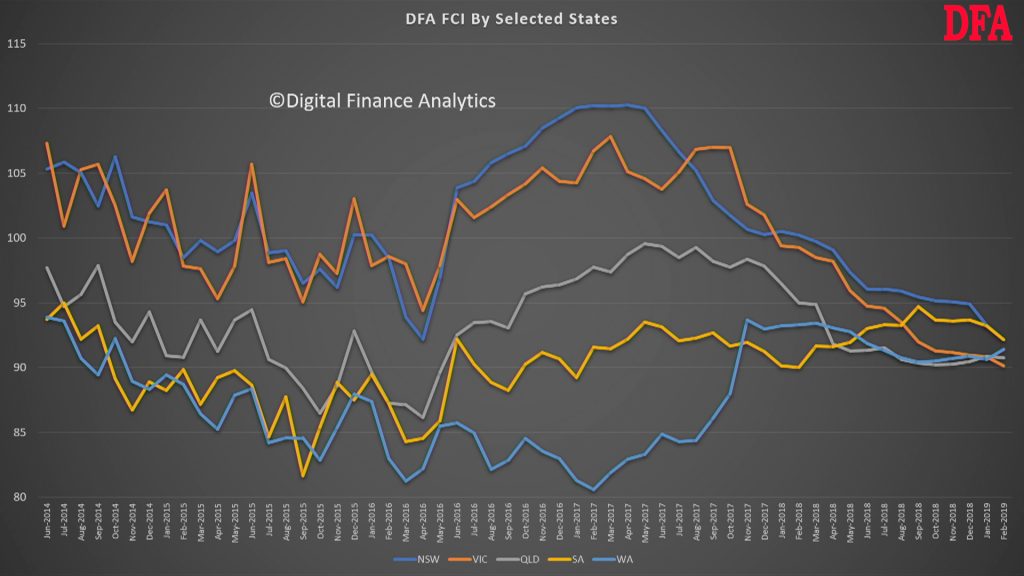

The state indices have converged at a level below the neutral setting.

The age groups continue to show younger households are less confident, thanks to low wages growth, high costs and rents or mortgage repayments. Some older groups remain more confident.

Property investors continue to struggle, though owner occupied owners are relatively more confident, even if below the neutral setting.

And all wealth segments are now in negative territory.

We review the moving parts in the index in the video above.

We released a series of updated mortgage stress maps this week. However we received a number of requests for higher resolution versions, which although uploaded were not displayed on some platforms.

So here are the direct links to the source JPG files. You should be able to view them direct in your browser, or even download them. They show the heat maps in each region.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}