Wisr is Australia’s only ASX listed marketplace lender and a fintech pioneer in the rapidly growing Australian consumer finance market. The company is is increasing its personal loan limits following increased borrower demand, strong institutional lender support and continued improvement to loan evaluation.

As of this week, Wisr will increase its personal loan limit from $35,000 up to $50,000, with a comparative interest rate up to 5% p.a. lower than the four major banks.

Loans will be available for any worthwhile purpose over three or five years, with a comparison rate of 9.36% p.a. for borrowers with a strong credit rating. The neo-lender also offers no early repayment or exit fees.

Chief executive officer Anthony Nantes said, “We have never been in a stronger position to help more Australians achieve a fairer financial future. During the past six months we’ve seen increasing borrower demand, continued strong support from institutional lenders and improvements to our lending platform.

“[The] announcement means creditworthy Australian borrowers now have more choice, to do bigger, more exciting things, and the opportunity to potentially make significant savings through lower interest rates and lower fees when compared to a personal loan from a traditional big bank.”

The move follows a period of strong personal lending growth for the company. Wisr announced record loan growth earlier this year, with originated loans growing by 42% in FY18 Q3 when compared with the previous quarter. It was the company’s largest quarter in loan originations since it began in 2014.

During the same period the company also announced ongoing improvement to its automated loan evaluation platform. The gross annualised loss rate for the loan book up to the quarter ending 31 March 2018 had also been below 2%.

Salvini has responded to the refugee crisis by saying that Italy needs “a mass cleaning – home by home, street by street, neighbourhood by neighbourhood”. Grillo, meanwhile, has championed the idea of celebrating “V-Days” – short for the Italian vaffanculo (the various English translations all begin with an expletive and end with either “off” or “you”) – taking aim at the political elite as part of an eccentric grab bag of largely anti-capitalist policy ideals.

Setting aside the bizarre prospect of a coalition between the far right and the loopy left, as a prospective government the pair do not bode well for Italy or Europe. Although officially disavowing any move to exit the Eurozone, they almost surely would have sought to do so. That would have triggered an automatic exit from the European Union, perhaps inevitably nicknamed “Quitaly”.

Italy, and the European experiment with it, might have bled out slowly.

But when Italian President Sergio Mattarella refused to allow the putative coalition to form government in its currently proposed form, all hell broke loose.

With a second election now on the cards, the spread on two-year Italian bonds quickly jumped to around 300 basis points over German bonds. That’s the market suggesting a staggering risk of default.

Yesterday Mattarella tried to calm things down by suggesting that he could appoint an interim technocratic government, giving Salvini and Five Star’s current leader, Luigi Di Maio, more time to produce a list of ministers that he could live with.

That’s probably the right thing to do, but it’s tough to get the toothpaste back in the tube. The markets are spooked. It will take a lot more than the prospect of securing a coalition government between two lunatic-fringe parties bent on getting Italy out of the euro to calm things down.

Greece is the word

Italy is Europe’s third-largest economy and it has public debt of €2.3 trillion. A bank run on the Italian economy, similar to what happened in Greece in 2015, would be a cataclysm that would likely be impossible to stop without Italy exiting the euro.

The seeds of Italian populism were fairly predictable in the wake of the great recession. Italy’s unemployment rate doubled to more than 12% and is still at 10.9%. Youth unemployment peaked at a 42.7% in 2014 and remains around 35%. GDP fell by more than 7% per year at an annualised rate and only turned positive in 2014. Real GDP is still below its 2007 level. Italy’s current GDP growth of 1.5% is the lowest in the Eurozone.

The question is what to do about it. Radical spending promises that can’t possibly be fulfilled without totally blowing the government’s books are not the answer. Having them delivered by an unstable government comprised of a loose coalition of warring tribes is less encouraging still.

On the other hand, fresh elections will just spook the markets even more.

Right now, Mattarella’s proposed technocratic government looks like the least worst option. There is an open question about how long it should govern for, but a reasonable starting point would be three years. That might give it time to get the Italian economic ship back upright. Enough time to take some tough decisions. This, of course, simply cannot be guaranteed under the constitution, so all Mattarella can do is install it and hope that the prospect of stability becomes self-reinforcing.

That is the kind of government that former Greek finance minister Yanis Varoufakis would hate, given his fierce resistance to the austerity imposed on Greece by its creditors. And I’m sure it will take about five seconds for me to be labelled a Washington Consensus, IMF-loving neoliberal for suggesting it. It would certainly attract plenty of criticism in Italy, given the strong anti-establishment sentiment that created this crisis in the first place.

But, to use the language of bankruptcy, the bottom line is that Italy is in political and economic Chapter 11. It is broke. It’s not technically insolvent just yet. But it will be, as they say in debt contracts, “but for the passage of time”.

It’s time to bring in the receivers to restructure. There needs to be serious microeconomic and labour-market reform, of the kind Emmanuel Macron is trying to implement in France. There also needs to be some attempt to get the debt under control. Lowering the interest rate through increased confidence would be a good start.

This would also help the rest of Europe. Perhaps there is some hope that German Chancellor Angela Merkel would be grateful, and thus more amenable to assistance measures for Italy. She certainly could not be less well disposed to help out than at present.

Author: Richard Holden, Professor of Economics and PLuS Alliance Fellow, UNSW

Misconduct exposed by the banking Royal Commission is the tip of the iceberg, with the catastrophic consequences of Australia’s broken financial sector yet to be revealed, according to a Deakin University corporate law expert.

Deakin Law School’s Professor Gill North, who has a background as a chartered accountant and financial analyst, as well as doctorate in law, said the Royal Commission would not fully address the broader impact of financial misconduct.

“Australians are horrified now by what they’re learning from the Royal Commission, but news on the finance sector is set to get much worse, with likely catastrophic consequences,” Professor North said.

“Systemic risks across the financial sector are already much higher than most people realise, and these risks are being exacerbated by the concentration of the sector, lax lending standards, high levels of household debt, and the heavy reliance of the economy on the health of the residential property market.

“As levels of household debt and financial stress rise, disparities between those who have considerable income, savings and wealth buffers and those who don’t will only become starker.

“The true resilience of the financial institutions, their consumers, and the broader economy will be tested and put under extreme pressure at some point – much of Australia is in for a bumpy and uncomfortable ride.”

Professor North is co-director of the analyst firm Digital Finance Analytics and has worked in senior executive positions at multinational corporations and investment banks in major financial centres including London, Tokyo, New York and Sydney.

She said the Royal Commission was shining a light on the most powerful corporations in Australia, but the investigation so far had been predominantly restricted to the most significant examples of non-compliance with the law by the largest financial institutions.

“The dirty linen of these entities and the practices they’ve gotten away with for many years are finally being effectively challenged,” Professor North said.

“The Commission is expected to have a profound and long-lasting impact on the sector, however the many governance and systemic concerns that flow from the identified misconduct are unlikely to be fully examined and addressed.”

Professor North said the Commission’s recommendations could include changes to consumer lending, while opening the door to future litigation.

“Changes to the consumer credit regimes under the National Consumer Protection Act are inevitable, including the way loan brokers can be remunerated and the processes used by lenders to verify information provided by consumers and intermediaries,” she said.

“The Commission has provided additional information and admissions that corporate regulator ASIC could use in actions against lenders, credit assistance providers, financial advisers, and directors.

“But future litigation in this space won’t be limited to regulators – actions by consumers who were issued loans or provided financial advice in breach of the law are likely to accelerate, and become a flood of litigation as the circumstances in Australia deteriorate and household financial stress levels climb to new records.”

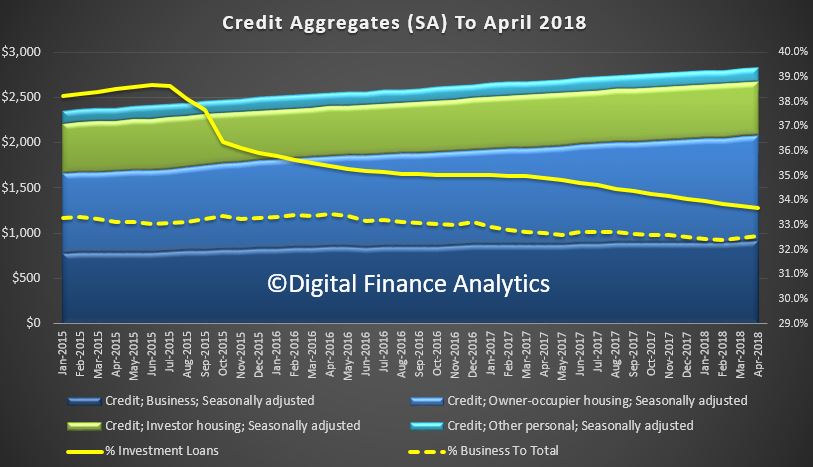

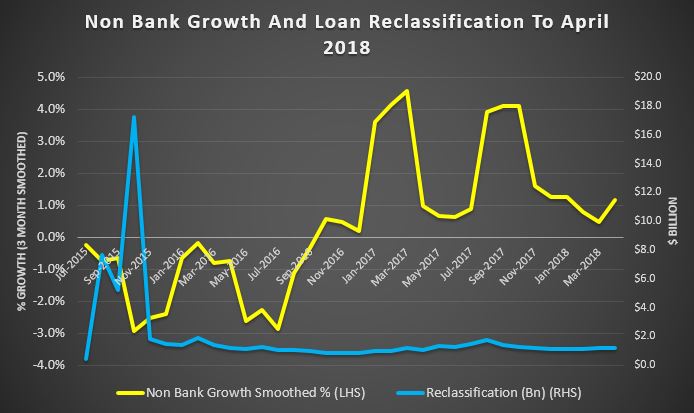

The RBA has released their credit aggregates to April 2018. Total mortgage lending rose $7.2 billion to $1.76 trillion, another record. Within that, owner occupied loans rose $6.4 billion up 0.55%, and investment loans rose 0.14% up $800 million. Personal credit fell 0.3%, down $500 million and business lending rose $6.3 billion, up 0.69%.

Business lending was 32.5% of all lending, the same as last month, and investment mortgage lending was 33.7%, slightly down on last month, as lending restrictions tighten.

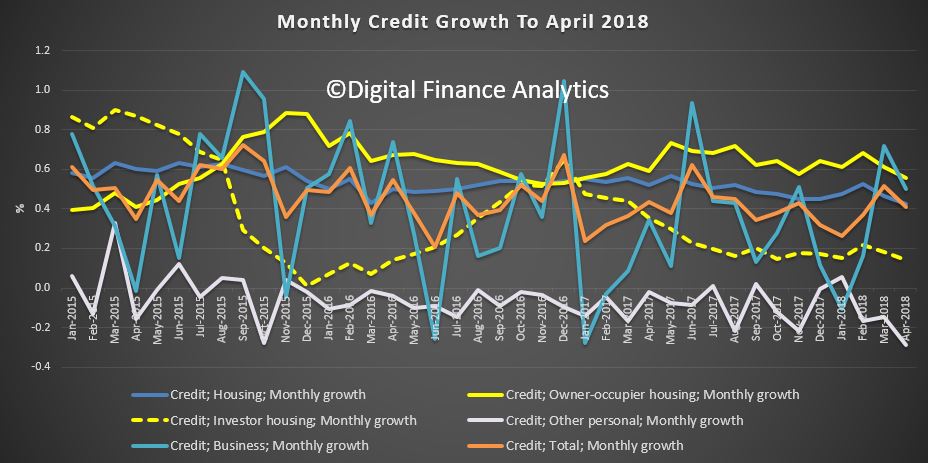

The monthly trends are noisy as normal, although the fall in investor property loans is visible and owner occupied lending is easing.

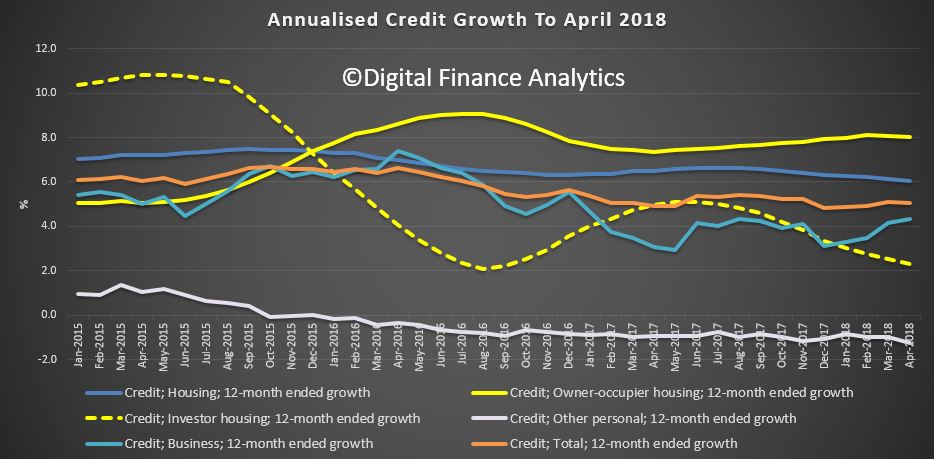

But the annualised stats show owner occupied lending still running at 8%, while business lending is around 4% annualised, investment lending down to 2.3% and personal credit down 0.3%. On this basis, household debt is still rising.

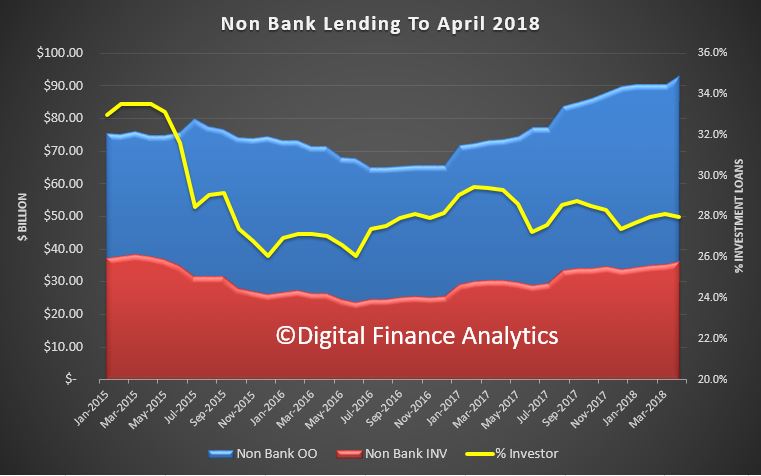

One interesting piece of analysis we completed is the comparison between the RBA data which is of the whole of the market and the APRA data which is bank lending only.

Now this is tricky, as the non-bank data is up to three months behind, and only covers about 70% of the market, but we can get an indication of the relative momentum between the banks and non banks.

We see that non-bank lending has indeed been growing, since late 2016. The proportion of loans for property investors is around 28%, lower than from the banks. Back in 2015, the non-bank investor split was around 34%.

The percentage growth from the non-bank sector appears stronger than the banks. Across all portfolios, loan reclassification is still running at a little over $1 billion each month.

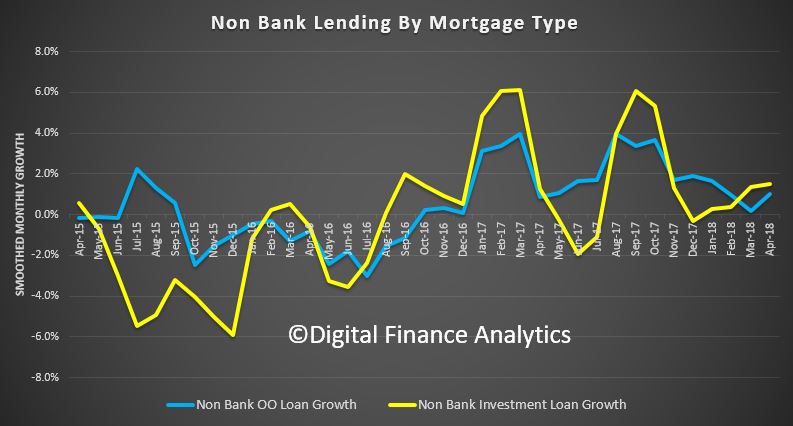

Finally if we look at the relative growth of owner occupied and investment loans in the non-bank sector we see stronger investment lending in the past couple of months. Bank investment property lending actually fell on April according to APRA stats.

As expected, as banks throttle back their lending, the non-banks are filling some of the void – but of course the supervision of the non-banks is a work in progress, with APRA superficially responsible but perhaps not actively so.

We would expect better and more current non-bank reporting at the very least APRA, take note!

At first blush the news at home and abroad appears to be steering us towards our most risky – scenario 4 outcome, where global financial markets are disrupted and home prices fall by 20-40 percent or more as confidence wains.

Some would call this GFC 2.0. So let’s looks at the evidence.

In Australia, as we predicted, a massive class action lawsuit is being planned on behalf of “Australian bank customers that have entered into mortgage finance agreements with banks since 2012”.

Law firm Chamberlains has been appointed to act in the planned class action lawsuit, which has been instructed by Roger Donald Brown of MortgageDeception.com in the action that aims to represent various Australian bank customers that are “incurring financial losses as a result of entering into mortgage loan contracts with banks since 2012”.

As the AFR put it – Lawyers’ representing up to 300,000 litigants are planning an $80 billion action against mortgage lenders, mortgage brokers and financial regulators in a class action that would dwarf previous actions. Roger Brown, a former Lloyds of London insurance broker, said he already has about 200,000 borrowers ready to join the action and has $75 million backing from UK and European investors. There has been a scam, he said about mortgage lending to Australian property buyers. “But the train has hit the buffers and there needs to be recompense.

As we discussed before, if loans made were “unsuitable” as defined by the credit legislation, there is potential recourse. This could be a significant risk to the major players if it gains momentum. And more will likely join up if home prices fall further and mortgage repayments get more difficult. But we think individuals must take some responsibility too!

Next, we now see a number of the major media outlets starting to blame the Royal Commission for the falls in home prices, tighter lending standards and even damage to the broader economy. Talk about shoot the messenger. The fact is we have had years of poor lending practice, and poor regulation. But the industry and regulators kept stumn preferring to enjoy the fruits of over generous lending. The Royal Commission is doing a great job of exposing what has been going on. In fact, the reaction appears to be that what had been hidden is now in the sunshine, and it is true the sunlight is the best disinfectant. Structural malpractice is being exposed, some of which may be illegal, and some of which certainly falls below community expectations. But let’s be clear, it’s the poor behaviour of the banks and the regulators which have placed us in this difficult position. Hoping bad lending remans hidden is a crazy path to resolution. At least if the issues are in the open they stand a chance of being addressed.

But it is also true that just a lax lending allowed households to get bigger mortgages than they should, and bid home prices higher, to be benefit of the banks, and the GDP out-turn, the reverse is also true. Tighter lending will lead to less credit being available, which in turn will translate to lower home prices, and less book growth for the banks. But do not lay this at the door of the Royal Commission. They are actually doing Australia a great service, in a most professional manner.

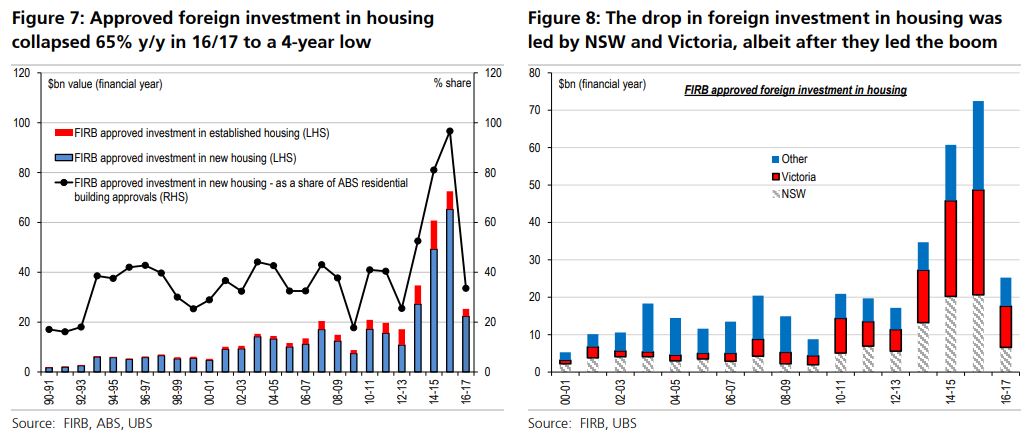

But that does not stop the rot. UBS came out today with an update saying that the housing market is slowing, with house prices falling and credit conditions tightening. Given the number of headwinds the market is facing; many investors are now questioning whether the housing correction could become disorderly. We expect credit growth to slow sharply and believe the risk of a Credit Crunch is rising.

They walk through the main areas, including tighter lending, interest only loans and foreign buyers. Specifically, they highlight that approved foreign investment in housing is down -65%. The Foreign Investment Review Board just released data for 16/17. The value of approvals to buy residential housing collapsed 65% y/y to $25bn in 16/17, the lowest level since 12/13, and mostly reversing the prior ‘super boom’. The fall was across both new (-66% to $22bn) and established housing (-59% to $3bn) – led by total falls in NSW (-66% to $7bn) and Victoria (-61% to $11bn.

They say that the collapse in 16/17 may be overstated because of the introduction of application fees in Dec-15 – meaning the fall in transactions is less pronounced. But, there is still likely to have been a drop in transactions, reflecting more structural factors including – the lift in taxes on foreigners; domestic lenders tightening standards for foreign buyers (effectively no longer lending against foreign sources of income or collateral); as well as tighter capital controls especially from China.

Their base case is for a small fall in prices ahead, and assumes house prices fall by 5%+ over the coming year and that bad and doubtful debts increase only modestly given the current very benign credit environment. but they also talk about a downside scenario which reflects a more disorderly correction in the housing market (ie a Credit Crunch) and could result in approximately 40% reduction in major bank share prices. This is likely due to credit growth falling more substantially, by ~2-3% compound and credit impairment charges rising significantly as the credit cycle turns. This scenario would put pressure on bank NIMs. Litigation risk from class actions for mortgage misselling is also a tail risk. Dividends would need to be cut in this scenario. Given the leverage in the banking system, accurately predicting the extent of a downturn is very difficult, as was seen in 2008.

And the reason they still hold to their milder view is the expectation that the Government will step in to assist, and slow the implementation of recommendations from the Royal Commission. To quote Scott Morrison on 2GB radio on 23d March.

If banks stop lending, then what do people think that is going to mean for people starting businesses or getting loans or getting jobs or all of this. In the budget papers, the Treasury have actually highlighted this as a bit of a risk with the process we are going through. We have got to be very careful. These stories are heartbreaking, I agree, but we have to be also very cautious about, well, how do we respond to that. What is the right reaction to that? Is it to just throw more regulation there which basically constipates the banking and financial industry which means that people can’t start businesses and people can’t get jobs, people can’t get home loans. Or do we want to move to a smarter way of how this is all done and I think in the era of financial technology in particular there are some real opportunities there. We are going to continue to listen and carefully respect the royal commission, not prejudge the findings, but be very careful about any responses that are made because this can determine how strong an economy we live in over the next ten years and whether people get jobs and start businesses.

But in essence, expect some unnatural acts from the Government to try to keep the bubble going a little longer. All bets are off the other side of the election.

And the third risk, and the one which takes us closest to GFC 2.0 is what is happening in Italy. I am not going to go back over the history, but after months of wrangling, Italy’s political crisis has a hit an impasse, with new elections now increasingly likely. The country faces an institutional crisis without precedent in the history of the Italian republic. Its implications extend well beyond Italy, to the European Union as a whole.

Since an election on March 4, there have been endless vain attempts to form a government – with the likely outcome changing every 24 hours. By mid-May, the Five Star Movement (M5S) and the League, both populist parties, had come together to draft a programme for government featuring tax cuts and spending plans. But it sent shivers down the spines of those contemplating Italy’s public debt – running at over 130% of GDP – and threatened the stability of the eurozone.

The appointment of Carlo Cottarelli, a former official from the International Monetary Fund, as prime minister on May 28 was merely a stop-gap measure until fresh elections in the autumn. His government will almost certainly fail to win the necessary vote of confidence required of all incoming governments upon taking office. This means that it will be unable to undertake any legislative initiatives that go beyond day-to-day administration.

ITALY’S president, Sergio Mattarella had originally planned to put a former IMF economist, Carlo Cottarelli, at the head of a government of technocrats, tasked with steering the country back to the polls after the summer. But Mr Mattarella was reportedly considering changing tack after meeting Mr Cottarelli on May 29th amid growing evidence of support in parliament for an earlier vote. Not a single big party has declared its readiness to back Mr Cottarelli’s proposed administration in a necessary vote of confidence.

So the president is expected to decide on May 30th whether to call a snap election as early as July in an effort to resolve a rapidly deepening political and economic crisis that has sent tremors through global financial markets. There was also concern that the populist parties could win a bigger parliamentary majority in the new election, creating a bigger risk for the future of the eurozone.

In a sign of investors’ concern, the yield gap between Italian and German benchmark government bonds soared from 190 basis points on May 28th to more than 300. The governor of the Bank of Italy, Ignazio Visco, warned his compatriots not to “forget that we are only ever a few steps away from the very serious risk of losing the irreplaceable asset of trust.”

The yield on two-year debt has risen from below zero to close to 2% and Italy’s 10-year bond yields, which is a measure of the country’s sovereign borrowing costs, breached 3 per cent on Tuesday, the highest in four years. At the start of the month they were just 1.8 per cent. Italy’s sovereign debt pile of €2.3 trillion is the largest in the eurozone

The Italian stock market was also down 3 per cent on Tuesday, and has lost around 13 per cent of its value this month.

But these movements need to be put in some context. The Italian stock market is still only back to its levels of last July, after experiencing a strong bull run since later 2016.

In 2011 and 2012 Italian bond breached 7 per cent and threatened a fiscal crisis for the government in Rome. Yields are still some distance from those extreme distress levels.

George Soros was quoted in the FT:

The EU is in an existential crisis. Everything that could go wrong has gone wrong,” he said. To escape the crisis, “it needs to reinvent itself.” Mr Soros said tackling the European migration crisis “may be the best place to start,” but stressed the importance of not forcing European countries to accept set quotas of refugees. He said the Dublin regulation — which decides which nation is responsible for processing a refugee’s asylum status, largely based on which country the individual first enters — had put an “unfair burden” on Italy and other Mediterranean countries, “with disastrous political implications.” While austerity policies appeared initially to have been working, said Mr Soros, the “addiction to austerity” had harmed the euro and was now worsening the European crisis. US president Donald Trump’s exit from the nuclear arms deal with Iran and the uncertainty over tariffs that threaten transatlantic trade will harm European economies, particularly Germany’s, he said, while a strong dollar was prompting “flight” from emerging market economies. “We may be heading for another major financial crisis,” he said. Meanwhile, years of austerity policies had led working people to feel “excluded and ignored,” sentiment that had been exploited by populist and nationalistic politicians, said Mr Soros. He called for greater emphasis on grassroots organisations to meaningfully engage with citizens.

To play devil’s advocate, if Italy were to leave the Eurozone, the Lira would drop, hard. Most probably Italy would default on debt, and this would hit the Eurozone banks hard, especially those in German and French banks will be hit hard and they are saddled with about half the outstanding debt. Just like in the GFC a decade back, global counter-party bank risk will rise, and this time sovereign are involved, so it may go higher. The US Dollar will run hot, and there will be a flight to quality, tightening the capital markets, lifting rates and causing global stocks and commodities to crash, possibly a recession will follow.

In Australia, the dollar would slide significantly, fuelling stock market falls and a further drop in home prices, leading to higher levels of default, and recession, despite the Reserve Bank cutting rates and even trying QE.

Now the financial situation in Italy at the moment, a far cry from the height of the eurozone crisis in 2012, when it really did look possible that weaker member states would be imminently forced to default and the single currency would collapse. Then, that situation was finally defused when the head of the European Central Bank, Mario Draghi, announced he would do “whatever it takes” to stop this break up happening, unveiling an emergency programme of backstop bond buying by the central bank. This reassured private investor that they would, at least, get their money back and bond yields in countries like Italy and Spain fell back to earth, ending the risk of a destructive debt spiral.

But the latest deadlock in Rome is nevertheless the biggest crisis in the eurozone since Greece last threatened to leave in 2015. And Italy is a much larger economy than Greece. If the third largest country in the bloc exited the euro, it is doubtful the single currency would survive.

Falling bank shares dragged down Europe’s main share markets. At the close the UK’s FTSE 100 fell almost 1.3%, while Germany’s Dax was down 1.5% and France’s Cac 1.3% lower. “It’s a market that is totally in panic”, said a fund manager at Anthilia Capital Partners, who noted “a total lack of confidence in the outlook for Italian public finances”. And the chief economic adviser at Allianz in the US said: “If the political situation in Italy worsens, the longer-term spill overs would be felt in the US via a stronger dollar and lower European growth.”

So whether you look locally or globally its risk on at the moment, and we are it seems to me teetering on the edge of our Scenario 4. This will not be pretty and it will not be quick. I see that slow moving train wreck still grinding down the tracks, with no way out.

The New Zealand Reserve Bank has issued their latest financial stability report. They say that New Zealand’s financial system remains sound. Household debt is firmly in the frame as the biggest potential risk!

The banking system holds sufficient capital and liquidity buffers, guided by our prudential regulatory requirements. These buffers reduce New Zealand banks’ exposure to adverse shocks.An ongoing driver of financial soundness is the conduct and culture of banks and insurance companies. These features are being jointly reviewed by the Financial Markets Authority and ourselves, and we will report our findings over coming months. The financial system vulnerabilities are much the same as we discussed in our previous Financial Stability Report.

Household mortgage debt remains high. However, financial risk has lessened with both lending and house price growth slowing in the last 12 months – in part due to our imposition of loan-to-value (LVR) ratio restrictions. This more subdued lending growth needs to be further sustained before we gain sufficient confidence to again ease the LVR restrictions.

However, the banks says the high level and concentration of household sector debt in New Zealand is the largest single vulnerability of the financial system. Some households are vulnerable to developments that reduce their debt servicing capacity, such as higher interest rates or a change in financial circumstances. Households with severe debt servicing problems could default on their loans, creating losses for lenders. If debt servicing problems were widespread, weaker consumption and investment could reduce incomes and contribute to an economic downturn. This could threaten financial stability by causing households and businesses to default, and by reducing the value of assets against which banks have lent, such as houses.

The high level and concentration of household sector debt in New Zealand is the largest single vulnerability of the financial system. Some households are vulnerable to developments that reduce their debt servicing capacity, such as higher interest rates or a change in financial circumstances. Households with severe debt servicing problems could default on their loans, creating losses for lenders. If debt servicing problems were widespread, weaker consumption and investment could reduce incomes and contribute to an economic downturn. This could threaten financial stability by causing households and businesses to default, and by reducing the value of assets against which banks have lent, such as houses.

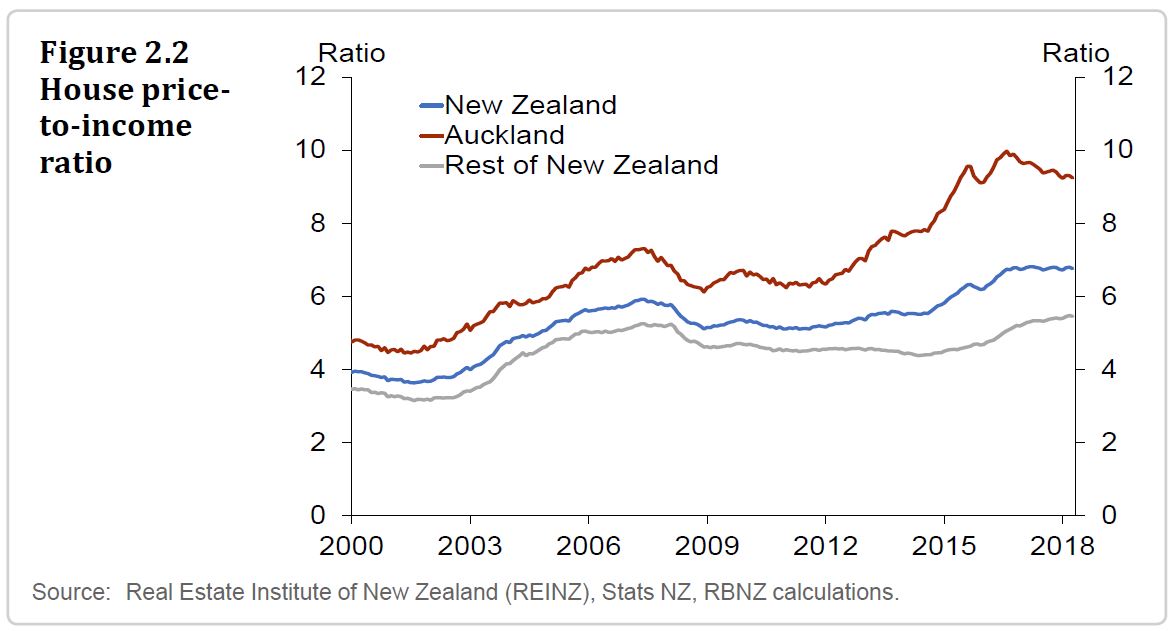

The rise in household debt since 2012 has coincided with a sharp rise in house prices, particularly in Auckland (figure 2.2). The simultaneous rise in household debt and house prices could partly reflect a self-reinforcing cycle, where bank lending has boosted house prices and, in turn, higher house prices have supported more bank lending, by increasing the value of homeowners’ collateral. But this cycle can also operate in reverse, driving down bank lending and house prices. This negative interaction can amplify the financial stability impact of a household income shock, by lowering collateral values and reducing households’ ability to service their existing debts by increasing their borrowing.

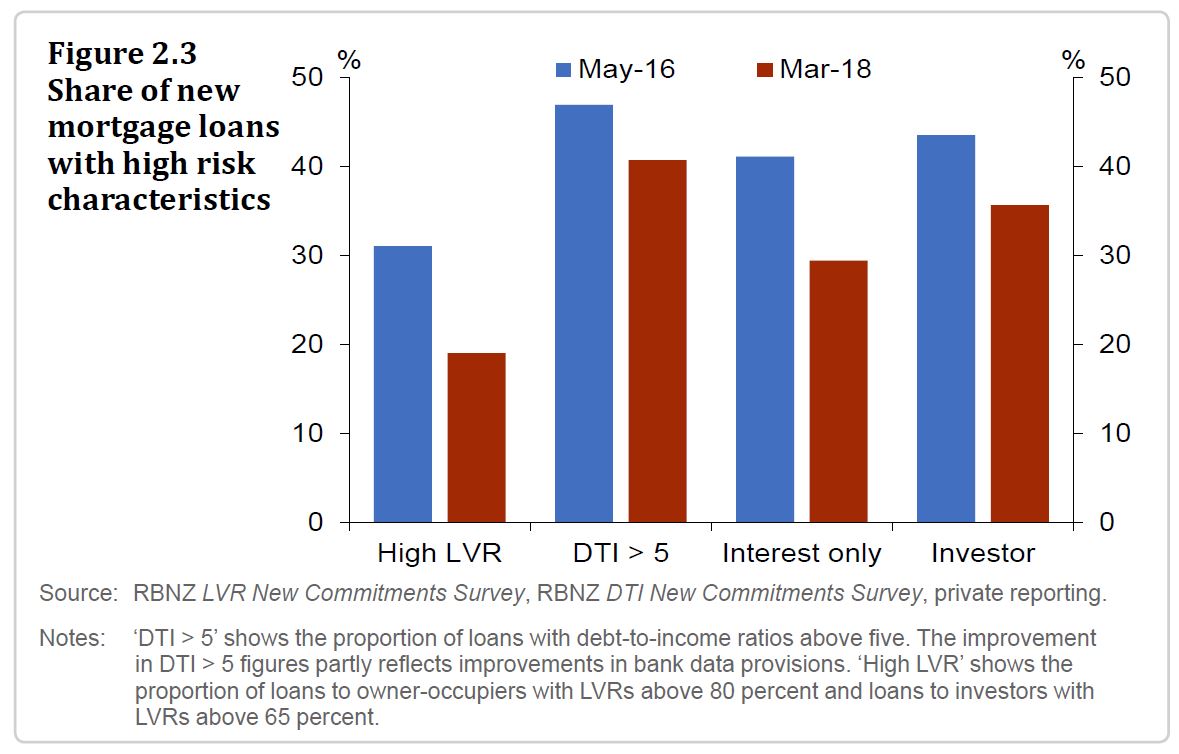

In the past two years, concerns about vulnerabilities in the household sector have caused a tightening in bank lending standards to the sector. This is partly the result of the Reserve Bank tightening its restrictions on new mortgage lending, particularly to investors, at high loan-tovalue ratios (LVRs) in October 2016.1 It also reflects actions by banks to tighten lending standards, such as the use of higher household living cost assumptions when assessing borrowers’ ability to service loans. As a result, a lower proportion of banks’ new mortgage loans have high risk characteristics than in 2016.

However, the share of new lending with high risk characteristics is still concerning. The proportion of new mortgage lending to borrowers with debt-to-income ratios above five is high compared to international peers, such as the UK. Households with this level of indebtedness are

particularly vulnerable to even modest changes in income or interest rates.

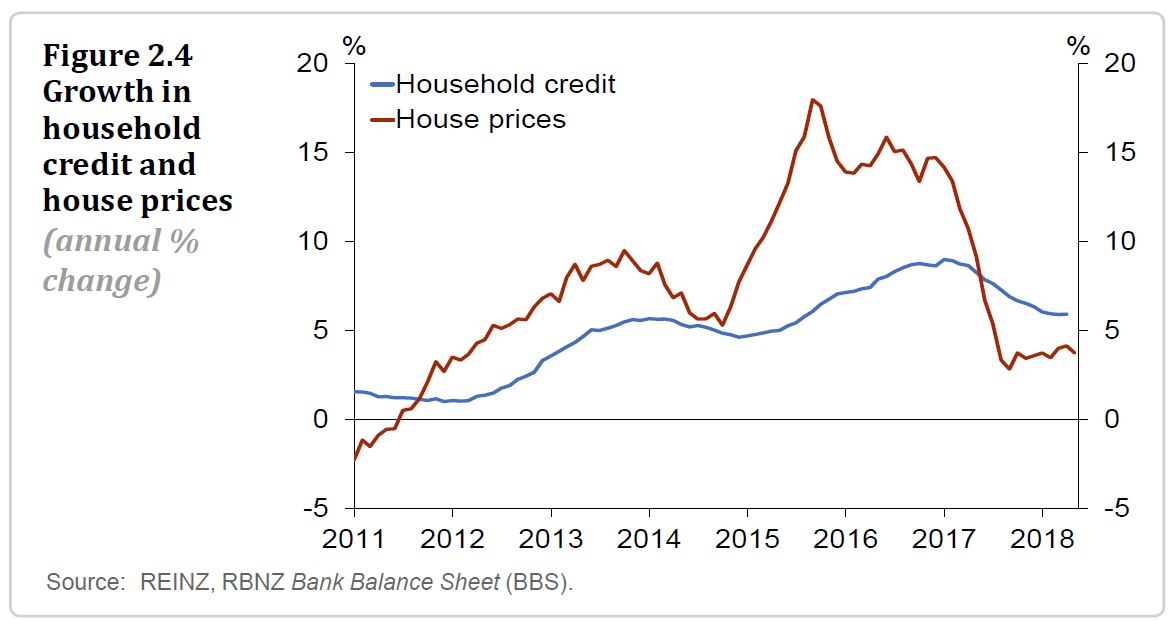

The tightening in lending standards has contributed to the annual growth rate of household credit slowing to 6 percent, slightly above the rate of income growth (figure 2.4). This has coincided with a slowdown in national house price growth, to 4 percent in the year to April. The

decline in house price inflation partly reflects the announcement and implementation of government policies (such as KiwiBuild, the extension of the bright-line test and plans for ‘loss ring-fencing’). But low mortgage rates and high net migration continue to support house prices.

The growth rates of household debt and house prices have been fairly stable over the past six months. Combined with tighter bank lending standards, this suggests the financial system’s vulnerability to household debt has not changed materially since the previous Report.

Ultimately, continued stabilisation, or a further reduction, in the growth rates of household debt and house prices, will be required before the risk to the financial system is normalised. Bank lending standards will have an influence over both. Currently, banks expect to keep their lending standards relatively tight for the rest of 2018.

In a similar vein, the dairy farming sector remains highly indebted. Most dairy farms are currently cash-flow positive, but remain vulnerable to any possible downturn in dairy prices and agriculture shocks. Reducing this bank lending concentration risk requires more prudent lending practices.

The high dairy-farm indebtedness, and the fact that LVRs were necessary, reflects that banks’ allocative efficiency – eg deciding how much to lend to whom – can be impaired due to the pursuit of short-term, rather than longer-term, profits.

The report also commented on the Australia Economy:

The Australian economy is growing steadily. But vulnerabilities have risen in recent years, particularly in the household sector, which carries a relatively high level of debt. House prices also appear stretched in some cities. Regulators have responded in a number of ways, including by requiring banks to conduct more rigorous loan serviceability assessments. These changes, coupled with a broader improvement in lending standards and an easing in housing market conditions, have improved the outlook for risks in the Australian household sector. But the Australian financial system remains vulnerable to developments that could weaken households’ ability to service their debts.

Perhaps originally a banks was a safe place for people with money to store it, and people who needed funds to obtain them. Simple. But when I worked for the big banks there was an increasing focus on boosting shareholder returns by financial engineering and acquisition, and this included expanding into areas such as wealth management, insurance and advisory businesses. The big institutional investors loved the returns from non-organic growth partly thanks to tax breaks available on restructuring costs on the way through. Focus in customers, and on enabling them to achieve their financial goals was a poor second. The industry had become an end in itself! One reason why I left the industry.

But that expansion is now in full reverse, and this is likely to hit returns to investors and change the shape of the industry in the years ahead. Perhaps bigger is not necessarily better. Perhaps it’s time to get back to the roots of banking.

The Royal Commission into Financial Services Miscount continues to highlight the structural issues which lay under the surface in financial services. For example, how can mortgage brokers or financial advisers, employed by a bank, recommend a product from that same bank, when they receive commissions when so doing. There are inherent conflicts which are not to the benefit of the customer This is vertical integration, when advice, product sales and product manufacturing all live under the same roof.

Or consider horizontal integration, where a bank owns ever more of what’s called a share of wallet, by expanding into insurance and wealth management. They can cross sell in theory, and accumulate vast amounts of customer intelligence across the board. In practice it’s much harder, thanks to cultural differences across divisions, management complexity, and consumers often want diversity not uniformity. In fact, though already we have seen a bevy of break-ups and sell-offs in a quest for capital efficiency. NAB, for example will be selling off their MLC wealth management business, marking the end of their mass-market wealth experiment. They will retain their upper end JBWere business as part of their Private Bank, for the most affluent customers. Other players are also divesting wealth businesses, partly because they never really generated the value expected, (and frittered away shareholder funds in the process) and because of the higher risks thanks to the FOFA “Best Interests” requirement.

The Productive Commission Draft report on superannuation released today, makes the point that a quarter of households are being poorly served by the current superannuation system, and the retail funds – those owned by many of the major banks, are charging more and returning less. They recommend a significant number of changes, which if implemented could enhance the benefits to savers, and remove many of the snouts from the trough. The big operators, including the big banks, though, will hate it.

But there are other conflicts too – for example the sector analysts within the banks on one hand claim to operate behind Chinese walls within their institutions, but we wonder whether their observations on the economy and housing market are truly independent. If an analyst employed by one of the big banks really thought the housing market would crash, would they spell this out (and risk a significant re-rating of their own entity)? We suspect this is why many of the analysis have only become recently mildly negative, despite the evidence building towards a more substantial correction. There are a few thought leaders who are ahead of the curve, but also a swag of followers, wanting to stay in the pack.

And then there are risks within banking from organisations who mix the more speculative aspects of trading and funding from the core banking operations – the meat and potato services like holding deposits and making loans, in fact at the moment, as we have discussed before, banks can create loans on demand, thanks to their ability to use a range of financial instruments – it has little to do with deposits. This by the way is counter to what most economists would claim. The derivatives market is, in a word, gigantic – with a “notional amount” of $500 trillion which is 25 times the GDP of the US and about 7 times global GDP, though other have estimated it at $1.2 quadrillion on the high-end. Other market analysts estimate the derivatives market at more than 10 times the size of the total world gross domestic product. Whichever way you look at it, it’s big.

Given the significant exposures to derivatives in the system globally and held by the large financial institutions, the risks are significant and growing. Remember in 2007 it was derivatives which led the way to the broader collapse in the financial system, and we have more exposure today.

Finally, the old argument that scale is required for efficiencies sake is mainly humbug, with smaller organisations often nimbler, less encumbered by legacy systems and more efficient – bigger is not necessarily better.

It is likely the Royal Commission, in their interim report will be discussing disaggregation options within the banks. On the other hand, it is also as likely that the Banks are already lobbying Canberra to deflect any potential breakups, claiming scale and stability and autonomy should be king. But as the Productivity Commission recently argued, the interests of customers are left far behind. Structural changes are needed.

So what are the break-up options worth considering?

One option to fix the Banking System would be to bring in a Glass-Steagall type regime. Glass-Steagall emerged in the USA in 1933, after a banking crisis, where banks lent loans for a long period, but funded them from short term, money market instruments. Things went pear shaped when short and long term rates got out of kilter. So The Glass-Steagall Act was brought in to separate the “speculative” aspects of banking from the core business of taking deposits and making loans. Down the track in 1999, the Act was revoked, and many say this was one of the elements which created the last crisis in the USA in 2007.

Now the Citizens Electoral Council of Australia CEC (an Australian Political Party) has drafted an Australian version of the Glass-Steagall act, and Bob Katter has announced that he will try to bring the legislation as a Private Member’s Bill called The Banking System Reform (Separation of Banks) Bill 2018. And Bob Katter has form here, in taking the lead in Parliament on Glass-Steagall, as he did on the need for a Royal Commission into the banks in 2017.

The 21st Century Glass-Steagall Act has been updated to prohibit commercial banks from speculating in the specific financial products that caused the 2008 global financial crisis, which didn’t exist in 1933, such as financial derivatives. These updates are reflected in the Australian bill. Aside from specific practices, the overriding lesson of the 2008 crash is that commercial banks should not mix with other financial activities such as speculative investment banking, hedge funds and private equity funds, insurance, stock broking, financial advice and funds management. The banks have gone far beyond traditional banking, into other financial services and speculating in derivatives and mortgage-backed securities. Consequently, they have built up a housing bubble, which is heading towards a crash and an Australian financial crisis.

The bill also addresses the question of the role and function of APRA, the financial regulator, which we believe has a myopic fixation on financial stability at all costs, never might the impact on customers, as the recent Productivity Commission review called out.

A few points worth making. First there is merit in the Glass-Steagall reforms, and I recommend getting behind the initiative, despite the fact that it will not fix the current problem of the massive debt households have. There is an online petition you can sign, and draft letters you can send to your MPs.

Remember that Banks were able to create loans thanks to funding being available from the capital markets, and so bid prices up. Turn that off, and their ability to lend will be curtailed ahead, which is a good thing, but the existing debts will remain. Now some are concerned about the CEC, and its motives. The CEC, is an Australian federally registered political party which was established in 1988. From 1992 onward the CEC joined with Lyndon H. LaRouche. But my point is, if you need a horse, and a horse appears, ride the horse and worry less about which stable it came from. I applaud the CEC for driving the Glass Stegall agenda.

But to deal with the debt burden we have, there are some other things to consider. For example, at the moment the standard mortgage contract gives banks full recourse — if you default the bank can not only sell the property, but also get a court judgment to go after your other assets and even send you bankrupt. In the USA some states have non-recourse loans, and recent research showed that borrowers in these non-recourse states are 32 per cent more likely to default than borrowers in recourse states. This is because if the outcome of missing your mortgage payments is losing pretty much everything you own and being declared bankrupt, you will do just about anything possible to keep paying your home loan. And banks will be more likely to make riskier loans when they have full recourse. So I wonder if we should consider changes to the recourse settings in Australia, which appear to me to favour the banks over customers, and encourage more sporty lending.

Then, there is the idea of changing the fundamental basis of bank funding, using the Chicago Plan. You can watch our video “Popping The Housing Affordability Myth” where we discuss this in more detail and “It’s Time for An Alternative Finance Narrative” where we go into more details. Essentially, the idea is to limit bank lending to deposits they hold, and it offers a workout strategy to deal with the high debt in the system and remove the boom and bust cycles. This is not a mainstream idea at the moment, but I think the ideas are worthy of further exploration. This is something I plan to do in a later post and look at how a transition would work. I believe that down the track we have to find a way to unwind all the unaffordable debt which is out there, the alternative is a generation or two of debt slaves, great for the Banks, not great for society. The excesses of the past 20 years have to be fixed. The Chicago Plan offers one mitigation path, there are others, including a so-called loan Jubilee.

But we need to go further and ask whether the Central Banks around the world are truly looking after our best interests or the banks, in the name of financial stability. For example, it is the Basel Capital rules, established by the Bankers Banker, the Bank for International Settlement, which makes lending for mortgages so much more capitally efficient compared with lending for productive business purposes, in the name of credit risk and stability. But to my mind these rules are part of the problem, and the tweaks they make to adjust the risk sensitivity (in consultation with the big banks) does not really address the underlying issues.

Indeed, some will point to the strong links between big business, big banks and the central bankers (and something of a revolving door between big banks and politics. All of which may work against the best interests of the community.

So it seems to me we need some fresh thinking to break out of our current dysfunctional banking models. Today, they may support GDP results as they inflate home prices more, but we are at the point where households a “full of debt”. So we see higher risks in the system – even the RBA recently called out risks relating to the amount of debt in the household sector, and the prospect of higher funding costs, a credit crunch, and lower consumption should home prices fall. And the latest data shows that prices are falling in the major centres now, and auction results continue lower. I believe that the RBA’s business as usual approach will lead us further up the debt blind alley. Which is why we need more radical reform in the banking system and the regulators if we are to chart a path ahead.

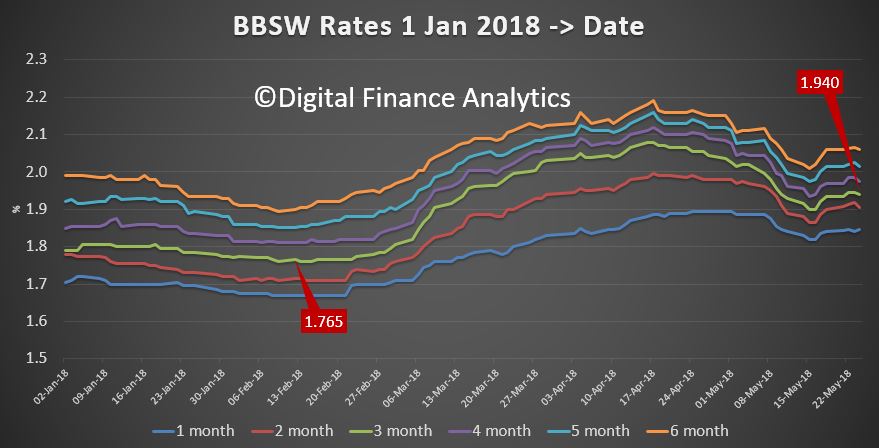

The latest charts on the Bank Bill Swap Rate shows that rates eased slightly from the peaks reached in April 2018. But we also see a move higher again in the past week, so the trajectory may still be up ahead.

In practice, the gap between the lowest and highest rates for the 3 month series peaked at 32 basis points, but is now back to 17.5 basis points. Still up, but it perhaps puts less pressure on bank margins as a result.

Welcome to our latest summary of finance and property news to the 26th May 2018 with a distinctively Australian flavour.

Watch the video, listen to the podcast, or read the transcript.

I had a number of interesting discussions with people who follow our analysis of the property market this past week. One in particular which stood out was from Melbourne who told me that in February 2017 he decided to sell his home, and got an indication it would sell conservatively for 1.3 million dollars. After a delay he took it to auction in August 2017 and struggled to see $1.25 million. But that property is now worth $1.15m a $150,000 drop from Feb 2017 to May 2018 or 11%. He also told me that back in 2017 he could have got a mortgage of $980,000, but now, on the same financial basis he can only access $670,000 today.

That in a nutshell is what is happening in the major markets, with people’s mortgage borrowing power being curtailed, and as a result home prices are falling. And they will fall further.

We had a bevy of analysts revising down their forecasts for future home prices this week. It is tricky to determine the extent of any fall ahead, and most predictions will of course be wrong. But the more significant factor in play is the significant change in the atmospherics around the housing sector. More are going negative. And when the largest lender in Australia signals they expect a fall, even a mild one, this is significant.

Recently Morgan Stanley said it is predicting property prices could fall by about 8% in 2018, and lending by more than a third. Morgan Stanley suggests there’ll not only be further price weakness in the months ahead, but also the likelihood of renewed softening in building approvals. It says these two factors will likely weigh on household consumption and building activity, seeing Australian economic growth decelerate, rather than accelerate, this year.

CBA has also gone negative on housing, now forecasting a mild correction. Gareth Aird, senior economist at CBA says that Australian residential property prices have fallen over the past six months. Additional declines appear likely over the next 1½ years due to a further tightening in lending standards, a continued lift in supply, potentially higher mortgage rates and more rational price expectations from would-be buyers. But he says a hard landing, however, looks unlikely and “is not our central scenario”.

We discussed this analysis in more detail in our recent release “Another Bank Goes Negative On Housing” which is still available. And remember CBA is the largest mortgage lender for owner occupied loans. Until recently they were bullish on prices, so this reversal is significant.

And UBS, who called the top of the market earlier than most, says macroprudential tightening ‘phase 3’, is a ‘game changer’ that will materially further tighten credit ahead, with higher living expense assumptions & debt to-income limits cutting borrowing capacity ~30-40%. Indeed, they says, housing is already weakening more quickly than our bearish view, with home loans dropping by ~10% since Aug-17, before the full Royal Commission impact. We have shifted our base case towards our ‘credit tightening scenario’, where home loans falls ~20%, credit growth drops to ~flat, prices fall persistently, & the RBA holds for longer. This coupled with record housing supply in coming years & a slump in foreign buyers sees us downgrade our house price outlook to fall 5%+ over the next year; below our prior 0 to -3% y/y. They conclude that housing activity will correct & prices to fall; still with downside risk: We still expect commencements, activity & prices to have an ongoing ‘downturn’ until at least 2019 – with downside risk from a ‘credit crunch’ scenario amid regulatory tightening & the Royal Commission. But housing should not ‘crash’ without (unexpected) RBA rate hikes or higher unemployment. So that’s ok then…

CoreLogic added some colour to the question of home prices by assessing home price growth across each decile, which confirms that values have fallen fastest at the premium end of the market. The broad trend findings in the CoreLogic May Decile Report showed that values have been falling on an annual basis across the 10th decile (the premium end of the market), while all other valuation deciles enjoyed positive (albeit restrained) growth over the twelve months to April 2018. National dwelling values were 0.2% higher over the 12 months to April 2018 – the slowest annual rate of growth since values fell -0.3% over the 12 months to October 2012. Analysing deeper at a decile level, it was only the most expensive 10% of properties that recorded a fall in values over the year (-4.3%) and all other sectors recorded annual growth greater than 0.2%.

In Sydney the most expensive decile, have fallen 7.2% over the past year, while in Melbourne the same decile fell just 2.4%. In contract the cheapest 10% of houses rose 1.5% in Sydney, and 11.9% in Melbourne over the past year. This is thanks partly to first home buyer stamp duty concessions implemented by both state governments from 1 July 2017. But be warned, if Perth is any guide, the top of the market falls first, but other sectors soon follow. This is one reason why we continue to hold the view prices will drop further than many analysts are predicting.

The credit tightening is real, borrowing power is being reduced, and investors are voting with their feet. We continue to see investors planning to exit the market before prices fall further. If you want further evidence, look no further than the latest auction clearance rates. CoreLogic says the combined capital city auction market continues to soften throughout 2018; while volumes have remained relatively steady over each of the last 3 weeks the weighted average clearance rate has continued to decline. Last week, the combined capitals returned a final auction clearance rate at a record year-to-date low of 56.8 per cent, the last time clearance rates were tracking at a similar level was in early 2013. With 2,100 homes taken to auction last week almost half of these failed to sell, over the same period last year the clearance rate was a much higher 73.1 per cent across 2,824 auctions.

In Melbourne, the final auction clearance rate increased last week across a slightly lower volume of auctions, with 62 per cent of the 1,033 auctions reported as selling, up on the previous week when the final clearance rate across the city dropped below 60 per cent (59.8 per cent- 1,099 auctions).

Sydney’s final auction clearance rate fell to 54 per cent last week, the lowest recorded since late 2017, with 672 homes taken to auction which was lower than the week prior when 787 auctions were held and a higher 57.5 per cent cleared.

Across the remaining auction markets, Adelaide was the only capital city to see a rise in clearance rate last week with volumes also increasing across the city.

This trend is set to continue with CoreLogic currently tracking 2,164 auctions, increasing slightly on last week’s final figures which saw 2,100 auctions held. Sydney is expected to see the most notable difference in volumes this week; increasing by 15 per cent on last week with a total of 775 homes scheduled for auction. Australia’s other largest auction market Melbourne is set to host 1,064 auctions this week, remaining somewhat consistent on the 1,033 auctions held last week at final results. In any case there are doubts about the auction stats, as we discussed in “Auction Results Under the Microscope”.

Across the smaller auction markets, Tasmania is the only other auction market to see a rise in week-on-week volumes, with Adelaide and Perth down more than 30 per cent on last week, while Brisbane and Canberra’s volumes are down to a lesser degree.

When compared to activity last year, both volumes and clearance rates were tracking considerably higher, with 2,885 auctions held on this same week one year ago when the success rate of auctions were tracking consistently above the 70 per cent mark throughout the first half of 2017; a much different trend to what we are currently seeing.

All the indicators are for more falls.

As the property market rotates, and demand slackens, property developers with a stock of newly built, or under construction dwellings – mostly high-rise apartments are trying tactics from deep discounting, cash bribes, or 100% mortgages to persuade people to buy. Remember there are around 200,000 units coming on stream over the next year or two and demand is falling. So we were interested to see (thanks to a tip off from our community) a WA initiative which was recently announced by Apartments WA – “Backed by the foundations of the BGC Group – Western Australia’s largest residential home builder and largest private company, we make your buying journey a seamless process from finding you the right apartment, assisting with obtaining finance, right through to settlement and key handover”.

I have been following the latest rounds of hearings at the Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry, which is exploring lending for small businesses.

It’s been quite dramatic, with stories of business owners with impossible dreams, walking into commercial ventures which had a limited chance of success. The banks on the stand appear to have made procedural mistakes, and when things go wrong often went for the jugular to cover their losses. This included relying on guarantees even if it meant selling the guarantors property, and the case studies included sad stories of people losing their homes. This included a disabled pensioner, blind and riddled with medical problems; her daughter, a budding small business operator. Or an ambitious woman trying her hand at running a pie shop with the hope of retiring early.

But the way the story is presented is only half the story. Yes, the banks failed in their duties on occasions, but on the other hand many businesses need finance if they are to start, and banks want to lend. What is really going wrong?

My theory is there small businesses are not get access to the advice they need to make a balanced assessment as to the viability of their operation. By default, they assume if the bank provides funding then the business must be viable – but this is not necessarily so. The bank is only concerned with protecting their loan, and ensuring they can cover the risk of loss – this is not the same as considering the business in the round. We discussed this analysis in more detail in our recent release “The Problem With Small Business Lending”. And remember about 53 per cent of the nation’s 2.2 million small to medium businesses need finance to continue trading.

The Australian Financial Review reported on our recent research on the Bank of Mum and Dad funding business start-ups. More than 33,000 business owners are estimated to have seed finance – or ongoing financial support – from loans that are secured with their parents’ home, analysis of home ownership and borrowing numbers reveals. The average cash injection is about $56,000 but loans typically range from few hundred dollars to more than $1 million, the analysis reveals. But while the number of parents providing direct cash support to their siblings’ business is increasing there has been a big fall in the number willing to put their houses on the line. That’s because of increased understanding that a lender could foreclose if there a default, which means parents’ best intentions risk the threat of homelessness by prodigal sons or daughters, according to financial advisers. said the number of parents guaranteeing a loan with their homes has fallen by about 8 per cent in the past year. This is because of the greater focus on financial advice and a better understanding of the risks involved with a guarantee, plus thanks to the strong rises in property there is more equity in a property.

Next, we look at the latest from the US where the adjustments to the Dodd-Frank Act (DFA) – sound familiar?) are expected to be signed into law next week. The changes ease the capital and regulatory requirements for smaller institutions and custody banks by raising the systemic threshold to $250 billion from $50 billion for enhanced prudential standards (EPS), reduce stress testing requirements and modify applicability of proprietary trading rules (the Volcker Rule). The legislation reduces regulations for U.S. small to mid-size banks in particular, while only providing de-minimis regulatory relief to the largest U.S. banks. The change to the systemic threshold reduces the number of banks subject to heightened regulatory oversight to 12 from 38. Regulators will still have discretion to apply EPS to banks with $100 billion-$250 billion in assets. Banks above $250 billion in assets would not see much benefit from the legislation.

Fitch Ratings says stress testing has provided discipline for banks and is an important risk governance practice that is considered in its rating analysis. The elimination or meaningful reduction of stress testing would likely have negative ratings implications. And this at a time when debt is very high.

Moody’s says the return of a 3% 10-year Treasury yield is making itself known in the housing industry. Markets have already priced in a loss of housing activity to the highest mortgage yields since 2011. They conclude that just as it is overly presumptuous to predict the nearness of a 4% 10-year Treasury yield, it is premature to declare an impending top for the benchmark Treasury yield. Thus far in 2018, the 11% drop by the PHLX index of housing-sector share prices differs drastically from the accompanying 3% rise by the market value of U.S. common stock. In addition, the CDS spreads of housing-related issuers show a median increase of 78 bp for 2018-to-date, which is greater than the overall market’s increase of roughly 23 bp. Finally, 2018-to-date’s -1.97% return from high-yield bonds is worse than the -0.13% return from the U.S.’ overall high-yield bond market. Despite the lowest unemployment rate since 2000, the sum of new and existing home sales dipped by 0.7% year-over-year during January-April 2018. All this shows the impact on the housing sector as rates rise.

The highest effective 30-year mortgage yield in seven years has depressed applications for mortgage refinancings. For the week-ended May 18, the MBA’s effective 30-year mortgage yield reached 5.01% for its highest reading since the 5.04% of April 15, 2011. The effective 30-year mortgage yield’s latest fourweek average of 4.95% was up by 63 bp from the 4.32% of a year earlier. March 2018’s 7% yearly drop by the NAR’s index of home affordability showed that the growth of after tax income was not rapid enough to overcome the combination of higher home prices and costlier mortgage yields. March incurred the 17th consecutive yearly decline by the home affordability index. The moving three-month average of home affordability now trails its current cycle high of the span-ended January 2013 by 23%.

And according to the latest from The St.Louis Fed On The Economy Blog, individuals who were in financial distress five years ago were about twice as likely to be in financial distress today when compared with an average individual. They argued that financial distress is not only quite widespread but is also very persistent. They show that the share of households with past financial distress increased from approximately 6.6 percent in 1998 to 12.2 percent in 2016. They conclude that households that have encountered an episode of financial distress in the past are 1.5 times more likely to delay payment today, compared to average households.

Why is this US data relevant to us? Well first, the debt levels in the US are significantly lower than here as home prices relative to income are lower there. We have more households in financial difficulty as a result. Second, the higher rates are likely to impact local funding costs here, which will put pressure on local banks funding costs, and third, higher rates will further tighten credit availability, and as in the US, this is likely to impact the construction sector – so expect to see more unnatural acts to try to attract buyers into a falling market – to which I reply, caveat emptor – let the buyer beware!

Finally, the latest data from S&P Global Ratings using their Mortgage Performance Index (SPIN) to March 2018 shows a rise in arrears – they increased to 1.18% in March from 1.16% in February and there was a significant hike in 90+ defaults. WA and NT continue their upward trends, both above 2% and rising. Home loan delinquencies fell in New South Wales, Queensland, South Australia, and the Australian Capital Territory in March. Of note, mortgage arrears in South Australia appear to have turned a corner; the state’s March 2018 arrears of 1.35% are well down from a peak of 1.81% in January 2017. This reflects a general improvement in economic conditions in South Australia, in line with national trends. Western Australia remained the state with the nation’s highest arrears, sitting at 2.37% in March.

But S&P says say arrears more than 90 days past due made up around 60% of total arrears in March 2018, up from 34% a decade earlier. This shift partly reflects a change in the reporting of arrears for loans in hardship that came in response to regulatory guidelines. Even accounting for this, however, there has been a persistent rise in this arrears category, though the level of arrears overall remains low. And I recall Wayne Byers recent comment to the effect that at these low interest rates, defaults should be lower!

The pressure on households is set to continue. The crunch is getting nearer.

Congressional passage of financial reform legislation easing the Dodd-Frank Act (DFA) for smaller and custodial banks is not likely to be a near-term ratings issue but could be negative for some banks’ credit profiles over the long term, if it results in significantly reduced capital levels, Fitch Ratings says.

The congressional legislation, which is widely expected to be signed into law by the president as early as this week, eases the capital and regulatory requirements for smaller institutions and custody banks. Fitch views robust regulation and capital as supportive of bank creditworthiness.

Key attributes of the legislation raise the systemic threshold to $250 billion from $50 billion for enhanced prudential standards (EPS), reduce stress testing requirements and modify applicability of proprietary trading rules (the Volcker Rule). The legislation reduces regulations for U.S. small to mid-size banks in particular, while only providing de-minimis regulatory relief to the largest U.S. banks. The change to the systemic threshold reduces the number of banks subject to heightened regulatory oversight to 12 from 38. Regulators will still have discretion to apply EPS to banks with $100 billion-$250 billion in assets. Banks above $250 billion in assets would not see much benefit from the legislation.

The biggest potential change to regulatory and capital requirements is for banks under $100 billion in assets, exempting them from DFA stress test requirements. From Fitch’s perspective, stress testing has provided discipline for banks and is an important risk governance practice that is considered in its rating analysis. The elimination or meaningful reduction of stress testing would likely have negative ratings implications.

Technically, the Fed’s CCAR process is not considered EPS and therefore the lower $50 billion proposed threshold isn’t applicable to CCAR, which applies to banks over $50 billion in assets. However, exempting banks with under $100 billion in assets from stress testing requirements makes it likely the Fed would align its CCAR testing requirements with Congress’ new thresholds. Banks with over $250 billion in assets would still be required to run CCAR; however, banks between $100 billion and $250 billion in assets would be subject to periodic rather than annual stress testing requirements.

Trust and custody banks would benefit from the potential carve out of central bank deposits to their supplementary leverage ratios, allowing for increased leverage. However, the joint banking regulators’ notice of proposed rulemaking (NPR) on the enhanced supplementary leverage ratio (eSLR) noted the proposed recalibration of the eSLR was contingent on the capital rules’ current definitions of tier 1 capital and total leverage exposure, which is being significantly altered by this legislation. The NPR specifically stated: “Significant changes to either of these components would likely necessitate reconsideration of the proposed recalibration as the proposal is not intended to materially change the aggregate amount of capital in the banking system.” The regulators’ response to this definition change only for the custody banks remains unclear. Ultimately, how much custody banks increase their leverage will also dictate ratings implications.

Banks with less than $10 billion in assets would be exempt from Volcker Rule restrictions on speculative trading, and banks originating less than 500 mortgages annually would be exempt from some of the record-keeping requirements of the Home Mortgage Disclosure Act. The Volcker Rule exemption would not aid large banks that must still demonstrate compliance with the rule. The legislation would also require U.S. regulators to consider certain investment-grade municipal securities as high-quality liquid assets for liquidity coverage calculations.