Across the eight capital cities, house values are set to decline 7.7% in 2019, a sharper correction than apartments which are forecast to see a 4.3% hit, says Moody’s. Via Property Observer.

House prices have declined over 9% since their peak in late 2017,

while apartment values are down around 6% from the peak, according to

CoreLogic.

House values in Sydney declined 5.5% in 2018 and are forecast to fall

a further 9.3% in 2019. Apartment values are set to decline 5.9% in

2019.

Melbourne’s house price decline has been more accelerated than

Sydney’s, and its sharp downturn is reflected in the forecast for its

house values in 2019.

Moody’s suggest values will decline 11.4% across Great Melbourne, with apartments to fall 5%.

The worst is over for Brisbane, according to Moody’s, with house values to see a correction in 2019.

There will be strength in East Brisbane, offset by declines elsewhere.

There’s also good news for the Brisbane apartment market, Moody’s forecast. Values are tipped to recover 0.9% in 2019.

It’s not such good news for Perth, where house values are like to decline 7.6% in 2019.

Adelaide’s housing market will continue its stable run, with house values forecast to rise 1% in 2019 after a 1.9% gain in 2018.

The latest amendments passed into law last week extends the capital raising capabilities of mutuls in Australia, via mutual capital instruments (MCIs), which Moody’s rates as “credit positive”.

However, we are concerned by the extension of “financialisation” into the mutual sector, the potential higher risks it introduces as players compete for returns to investors, and the complexity of the financial markets they have to engage in. This could be a disaster.

Frankly, this just continues the journey away from meat and potato banking and is a further illustration of the myopic views of the regulators, especially APRA.

Rather than extending these additional capital channels, we need banking structural reform to contain the over-risky sector. This is the wrong strategy at the wrong time (especially as the housing sector tanks).

Anyhow, this is what Moody said:

On 4 April, Australia’s parliament passed the Treasury Laws Amendment (Mutual Reforms) Bill 2019, which amends the Corporations Act 2001 to allow mutually owned institutions to issue capital instruments. The development is credit positive for mutuals because it will enhance their ability to support growth, invest in technology innovation and, over time, will also strengthen their competitiveness.

In particular, the amended Act introduces a definition of a “mutual entity;” clarifies that demutualisation rules can only be triggered by an intended demutualisation and not by other acts such as capital raising; and creates mutual capital instruments (MCIs) that are specific to the mutual industry to raise equity capital.

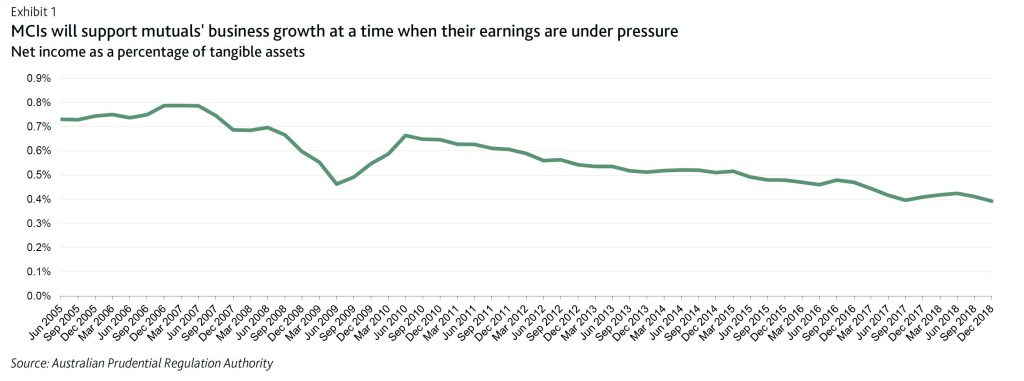

MCIs will provide mutuals with an additional capital channel to respond to growth opportunities, supplementing the retained earnings they have relied on to date. This additional capital channel is particularly important for mutual authorised deposit-taking institutions (mutual ADIs, which include mutual banks, building societies and credit unions) at a time when their profitability is under pressure. Pressure on profitability stems from competition for lower-risk owner-occupier mortgages with principal and interest repayments, the mutuals’ core products. This elevated competition stems from a number of factors including reduced overall loan growth; a reduced demand for investor mortgage loans in the face of potential changes to negative gearing and capital gains taxes; and tightened underwriting criteria at the major commercial banks as a result of public scrutiny during Australia’s Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry.

Additional capital options will also help mutual ADIs build the scale and efficiency they need for technology investment, which is particularly important at a time when banking services are rapidly becoming technology-based. Compared with mutual ADIs, the large commercial banks have more resources to develop or acquire innovative products, digitise processes and integrate new technologies into their business models. Technology-driven financial firms (fintechs) are seeking entry to banking, while the Australian Prudential Regulation Authority (APRA) has established a framework that allows new entrants to begin operating at an earlier stage in their licensing process than previously. These new entrants are currently small and subject to regulatory constraints in taking deposits and making loans. In most cases they have not yet built up a retail customer base of meaningful size. However, they could grow to challenge incumbents, particularly small-scale ones like the mutual ADIs, over time.

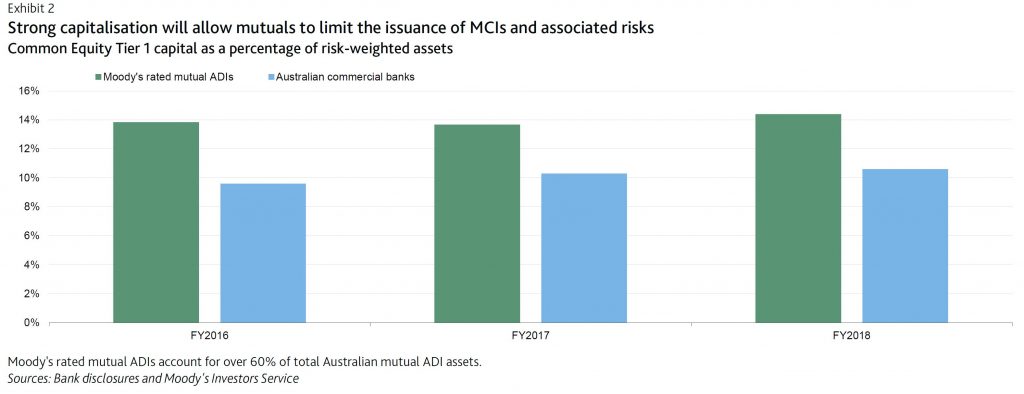

We do not expect mutual ADIs to swiftly ramp up their issuance of MCIs because their already-strong capitalisation and the current low loan growth environment are likely to reduce their need for additional capital. Mutual ADIs’ average Common Equity Tier 1 (CET1) capital ratio is well above that of the major commercial banks, which is itself strong by international standards. Moreover, APRA has set a 25% cap on the inclusion of MCIs in CET1 capital and has also capped the annual distribution of profit to holders of MCIs at 50% of a mutual institution’s net profit after tax for the year in question.

The prospect that the issuance of MCIs will remain limited will reduce the risk that mutual ADIs will significantly increase their risk profiles in an attempt to generate greater dividend returns for MCI holders. Mutuals will need time to amend their constitutions and build market recognition for MCIs. The experience of mutual banking peers in the UK also suggests that the process will be gradual. In the UK, mutuals have been allowed to issue core capital deferred shares, similar to MCIs, under the Building Societies (Core Capital Deferred Shares) Regulations 2013, but few have done so to date. We expect that Australian mutual ADIs that already have a strong investor base in the debt market to be in a better position to issue MCIs.

Moody’s says on 2 April, the US Federal Reserve Board, the Federal Deposit Insurance Corporation, and the Office of the Comptroller of the Currency proposed a rule that would require US global systemically important bank (GSIB) holding companies and advanced-approaches banking organizations1 to hold additional capital against investments in total loss absorbing capacity (TLAC) debt. The additional capital required for investments in TLAC debt would reduce interconnectedness between large banking organizations and the systemic effect of a GSIB’s failure, a credit positive for the US banking system.

The credit-positive proposal would require companies to deduct from their regulatory capital any investment in their own regulatory capital instrument which includes TLAC debt, any investment in another financial institution’s regulatory capital instrument, and investments in unconsolidated financial institutions’ capital instruments that would qualify as regulatory capital if issued by the banking organization itself (subject to a certain threshold). The deductions intend to discourage banks from investing in the regulatory capital instruments of another bank and improve the largest banks’ resiliency to stress and ensure a more efficient bank resolution process.

The proposal also includes additional required disclosures about TLAC debt in bank holding companies’ public regulatory filings, which would increase transparency.

The TLAC rules were first proposed in 2015 and finalized in December of 2016. However, in 2016 when the TLAC rules were finalized, regulators needed more time to determine the rule’s regulatory capital treatment for investments in certain debt instruments such as TLAC issued by bank holding companies.

On 19 March, the Haut Conseil de la Stabilité Financière (HCSF), the French macroprudential authority, announced it would increase banks’ countercyclical capital buffer on their exposures to French counterparties to 0.50% from 0.25% by no later than 2 April 2020.

The increase, the first since the HCSF established the buffer in June 2018 to stem the potential for excessive credit growth, raises banks’ capital requirements, a credit positive, says Moody’s.

The countercyclical capital buffer was introduced with Articles 136-140 of the European Union’s (EU) Capital Requirement Directive IV (CRD IV) to build up extra capital in boom periods and pre-empt the credit risks that accumulate during economic upswings. The buffer applies to all French, EU and European economic area banks’ that have exposures to French counterparties.

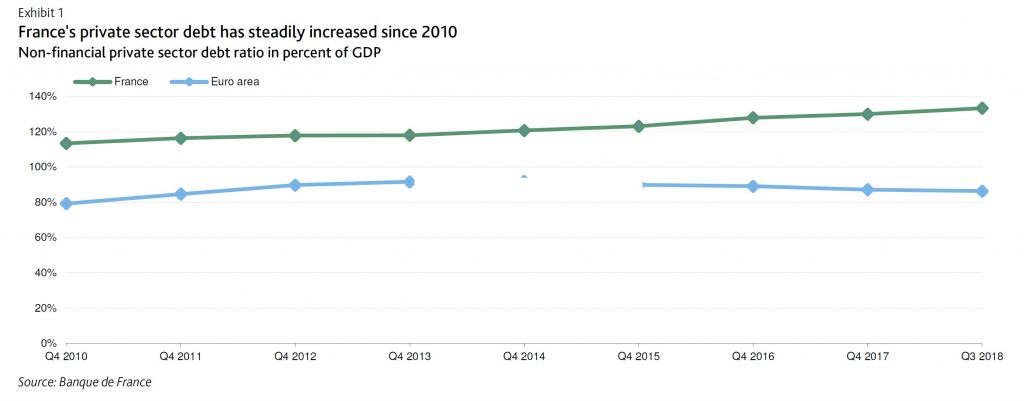

Last Monday’s increase aims to dampen continuing credit growth : non-financial private sector debt increased to 133.3% of GDP as of third-quarter 2018 (one of the highest levels in the EU) from 131.0% as of first-quarter 2018 and 113.4% at year-end 2010.

Since 2016 credit to corporates and households has increased at a 4%-6% annual rate amid relaxed lending standards (especially on housing loans with higher loan-to-value ratios and longer maturities), rising house prices and increasing leveraged buyout transactions (up 3.6% in February 2019 compared to February 2018). Moreover corporate debt issuance also drove the increase in indebtedness, in particular at large corporates, which prompted the HCSF to express some concern.

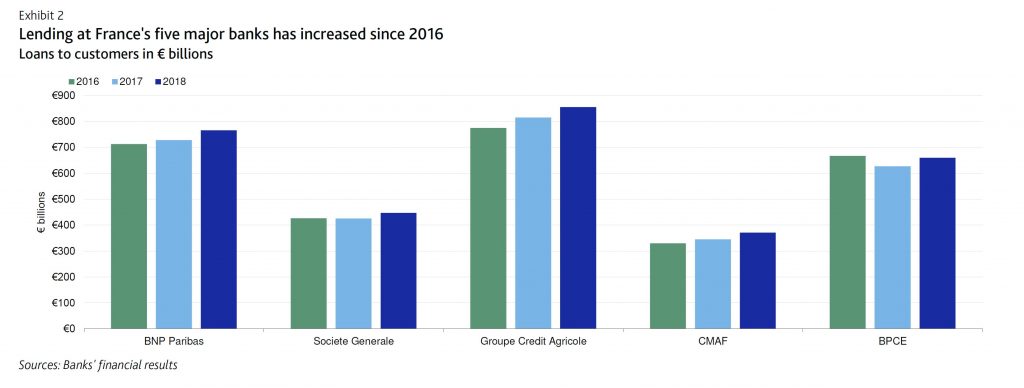

Total lending (domestic and international) among France’s five major banks – BNP Paribas, Societe Generale, Credit Agricole S.A., Banque Federative du Credit Mutuel, BPCE – grew 5.6% year over year as of year-end 2018, with bank loans to SMEs growing a robust +6.3% for the same period.

Additionally, France’s credit-to-GDP gap (measuring the difference between the credit-to-GDP ratio and its long-term trend) was 2.7 percentage points in fourth-quarter 2018, versus the euro area average of negative 12.4 percentage points at the same time.

The HCSF’s decision will be submitted to the ECB on a non-objection basis and will be adopted before 2 April 2019 for an effective implementation of this requirement a year later (April 2020).

The 2018 decision to set a CCyB at 0.25 % has not resulted in a more moderate lending growth at French banks hence the decision to tighten it at 0.50%. It remains to be seen whether or not a higher capital add-on will be successful in materially curbing lending at banks. If not successful the official sector may consider tightening the 0.5 % CCyB once again.

We assign a one-notch downward adjustment for credit conditions in France’s macro profile, which reflects the macro- risks faced by banks, to account for the material growth of private sector indebtedness in France since 2015 and the risk that a too rapid rise in corporate and household debt could eventually increase the vulnerability of borrowers to an economic downturn.

Many European have imposed much higher countercyclical capital buffers, up to 2.5% (for example, Sweden). The growing use of CCyBs in European countries – 11 countries have resorted to this prudential measure – points to a potential accumulation of excessive credit risk throughout the region.

According to Moody’s, on 14 March, the European Parliament voted in favor of a regulation setting minimum loan loss provisioning requirements for nonperforming loans (NPLs). The European Union (EU) regulation aims to prevent the excessive accumulation of soured loans, a scenario that unfolded in several European countries during the global financial crisis. The new rules, which will become effective in the coming weeks, will be credit positive for EU banks.

All European banks will be subject to the same prudential standards. Until now, banks’ provisions were driven by two factors; accounting rules, which were recently amended to make them more prudent and forward-looking (IFRS 9), and supervisory expectations, which the euro-area banking supervisor, the Single Supervisory Mechanism’s (SSM), in March and July 2018 made more explicit by providing qualitative and quantitative guidance.

However, the SSM’s quantitative guidance on NPL coverage (the so-called addendum) has been criticised because the SSM is not empowered to set rules; regulation is the joint responsibility of the European Council (of governments) and the European Parliament.

The new regulation will operate as a backstop to the accounting standard IFRS 9, which can be interpreted in different ways in different jurisdictions. The SSM will continue to have influence over banks’ provisioning decisions in rare instances that it considers the NPL regulation does not provide appropriate coverage.

The regulation directs minimum provisions (prudential provisions) on loans according to a prescribed timetable. The volume of provisions required may vary from the amount computed under IFRS 9 accounting standards.

The new rules categorize banks’ loans as unsecured and secured loans. For secured loans the regulation differentiates between immovable collateral such as property (the highest quality) and other eligible credit protection (the lowest quality). For unsecured loans that move into the NPL category, no provisions would be required for the first two years; a minimum provision of 35% of the outstanding amount would be required during the third year; and 100% coverage should be in place before the end of the fourth year. This final timetable is slightly longer than that originally proposed (100% after two years of nonperformance).

For secured loans, provisioning follows a longer timetable. For loans with the highest quality immovable collateral, the timetable spans nine years, beyond which NPLs must be 100% covered by provisions. For loans with the lowest quality collateral, 100% coverage must be in place by the end of the seventh year after a sound loan is moved to the NPL category.

The new rules will not tackle the outstanding stock of NPLs, but we expect them to have an effect over time. NPLs still are a large proportion of banks’ loans portfolios in several EU countries, including Italy, where we estimate they comprise 10% of total loans. The scope of the NPL regulation, however, is restricted to new loans EU banks extend from the date of implementation. Consequently EU banks’ provisioning decisions on legacy NPLs will still be driven by IFRS 9 accounting rules and guidance from the SSM.

Nevertheless, we expect the SSM’s approach to legacy NPLs will mirror the new regulation, and at some point banks will find it untenable to maintain two parallel provisioning policies.

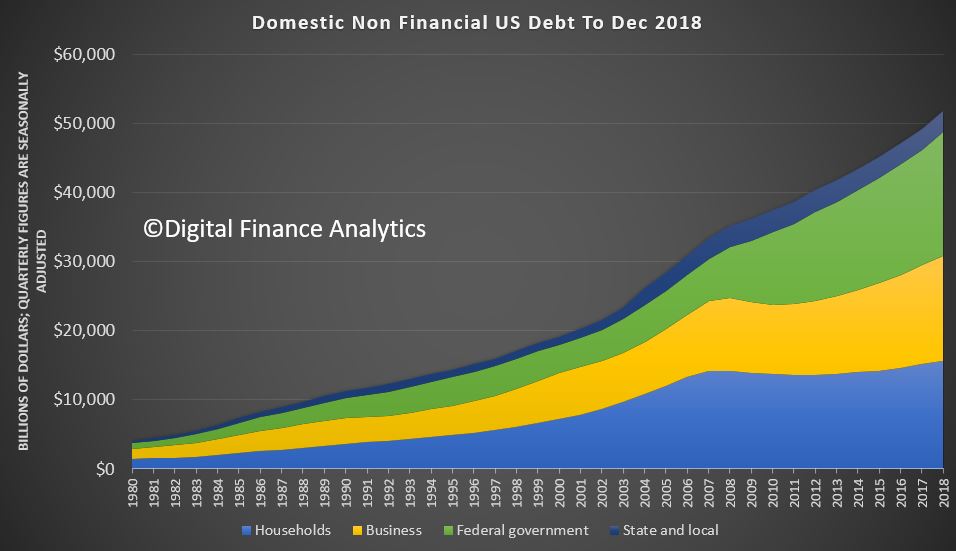

Moody’s says that US debt continues to rise (with strongest growth in the public sector) and a powerful enough external shock could force U.S. benchmark interest rates up to levels that shrink business activity considerably.

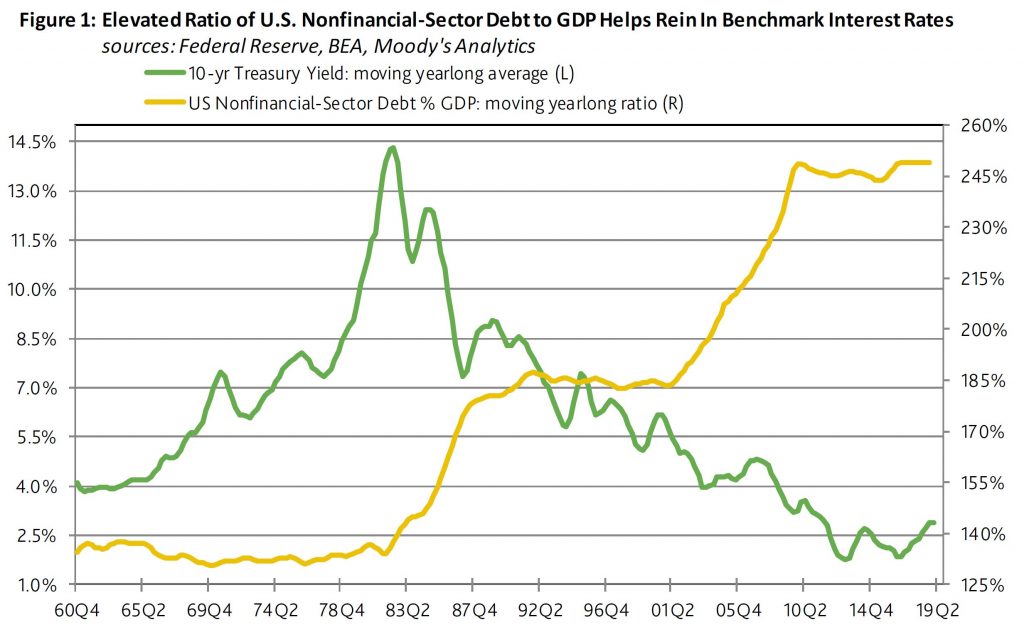

The latest version of the Federal Reserve’s “Financial Accounts of the United States” was released on March 7. As of 2018’s final quarter, the total outstandings of private and public nonfinancial-sector debt grew by 5.1% year-to-year to a record high $51.796 trillion. The year growth rate of the broadest estimate of U.S. nonfinancial-sector debt has slowed from second-quarter 2018’s current cycle high of 5.6%. Since the end of the Great Recession, the 3.9% average annualized rise by nonfinancial-sector debt has slightly outpaced nominal GDP’s accompanying 3.7% average annual increase.

By contrast, during 2002-2007’s upturn, the 8.1% average annualized advance by nonfinancial-sector debt was much faster than nominal GDP’s comparably measured growth rate of 5.3%. As a result, the moving yearlong ratio of total nonfinancial-sector debt to GDP climbed from the 197% of 2001’s final quarter to the 225% of 2007’s final quarter. Because of the current recovery’s much slower growth of debt vis-a-vis GDP, debt barely rose from second-quarter 2009’s 243% to fourth-quarter 2018’s 249% of GDP.

Today’s near record high ratio of nonfinancial-sector debt to GDP limits the upside for benchmark interest rates. Just as highly leveraged businesses exhibit a more pronounced sensitivity to higher benchmark interest rates, highly leveraged economies are likely to slow more quickly in response to an increase by benchmark rates. Relatively low interest rates do much to lessen the burden implicit to a comparatively high ratio of debt to GDP.

Nevertheless, a powerful enough external shock could force U.S. benchmark interest rates up to levels that shrink business activity considerably. Under this scenario the Fed would be compelled to hike rates in defense of the dollar exchange rate despite how a deterioration of domestic business conditions requires lower rates.

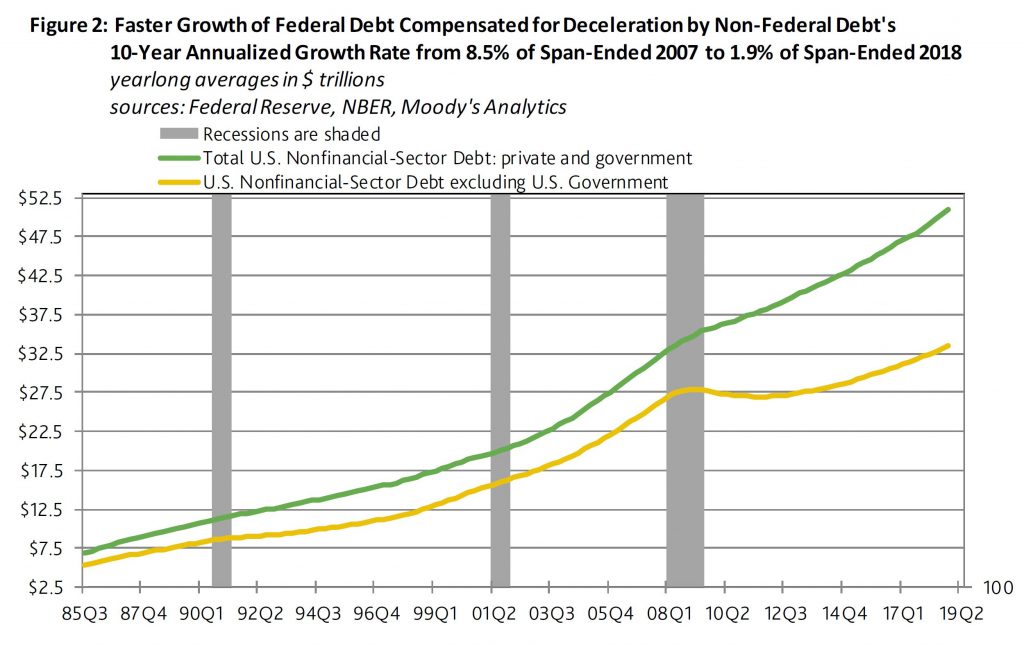

The federal government has dominated the growth of total nonfinancial-sector debt during the current business cycle upturn. In terms of moving yearlong averages, U.S. government debt’s 9.3% average annualized surge has well outrun the accompanying 2.2% growth rate for the sum of private and state and local government nonfinancial-sector debt.

Regarding 2018’s final quarter, the outstandings of U.S. government debt advanced by 7.6% annually to $217.865 trillion. By comparison, household-sector debt rose by 3.1% to $15.628 trillion, nonfinancial corporate debt increased by 6.5% to $9.759 trillion, unincorporated business debt grew by 4.9% to $5.485 trillion, while state and local government debt shrank by 1.7% to $3.060 trillion. Thus, fourth quarter 2081’s U.S. nonfinancial-sector debt excluding the obligations of the federal government grew by a modest 3.9% annually. Over the past 10-years, the faster growth of federal government debt compensated for the sluggish debt growth of non-federal borrowers.

More evidence of the peeling back of US bank disclosure, which may reduce the incentive for bank managements to continually improve their capital and risk management processes.

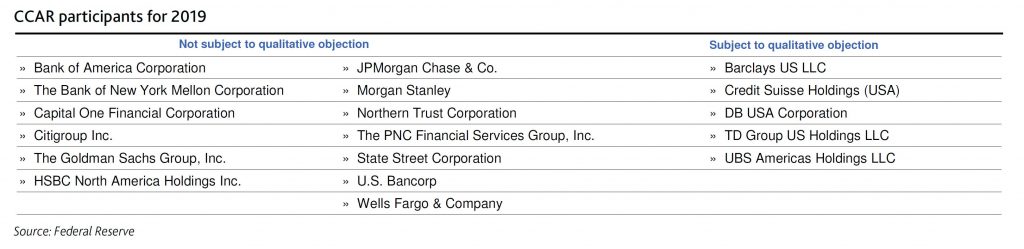

On 6 March, Moody’s says the US Federal Reserve Board (Fed) announced the elimination of the qualitative objection in its 2019 Comprehensive Capital Analysis and Review (CCAR) for most stress test participants. Only five banks, all US subsidiaries of foreign banks, will remain subject to qualitative objection in the current stress tests cycle. In the past, the Fed has used the qualitative objection to address deficiencies in banks’ capital-planning process. Its elimination is credit negative because it reduces public transparency around the quality of banks’ internal capital and risk management processes.

Under the revised rules, a bank must participate in four CCAR cycles before it qualifies for exemption from a potential qualitative objection in future years. If a firm receives a qualitative objection in its fourth year, it will remain subject to a possible qualitative objection until it passes. For most of the five firms still subject to the qualitative objection, their fourth year will be the 2020 CCAR cycle. In total, 18 firms are subject to this year’s CCAR exercise, with five of them subject to a possible qualitative objection.

All five firms subject to the qualitative assessment in 2019 are foreign-owned intermediate holding companies (IHCs), most of which were first subject to the Fed stress tests on a confidential basis in 2017. If the IHC has a bank holding company subsidiary that was subject to CCAR before the formation of the IHC, then the IHC is not considered the same firm for the purpose of the four-year test.

The Fed noted that since CCAR was implemented in 2011, most firms have significantly improved their risk management and capital planning process. Going forward, its capital-planning assessments will be through the regular supervisory process. The Fed highlighted as an example the new rating system for large financial institutions, which will assign component ratings of a firm’s capital planning and positions. However, these ratings will be confidential supervisory information and unavailable to the public unless the deficiencies are so severe that they warrant formal enforcement action. The new process replaces an independent comparative assessment.

The lack of public disclosure may also reduce the incentive for bank managements to continually improve their capital and risk management processes, which the CCAR qualitative review encouraged.

As previously announced, 17 large and non-complex bank holding companies, generally with $100-$250 billion of consolidated assets, will not be subject to CCAR in 2019 because of the Economic Growth, Regulatory Relief, and Consumer Protection Act (the EGRRCPA), which became law in May 2018. They will next participate in 2020. Most of these banks were removed from the qualitative objection in 2017 and the Fed will only object to their capital plans if they fail to meet one of the minimum capital ratios under the stress scenarios on quantitative grounds.

The Fed’s announcement was incorporated with its release of instructions for the 2019 CCAR cycle. The Fed also provided information on allowable capital distributions for those firms whose CCAR cycle was extended to 2020. For those banks, the Fed published letters that address each bank’s individual 2019 capital plans. The Fed pre-authorized the firms to distribute, net of any issuance of capital, up to the sum of:

The additional capital the firm could have distributed in CCAR 2018 and remained above the minimum requirements; plus

Capital accretion (change in capital ratios since CCAR 2018); plus

its already approved capital distributions for first-quarter 2019 and second-quarter 2019; minus

its actual distributions for first-quarter 2019 and planned distribution for second-quarter 2019

This plan is also credit negative because it permits capital distributions based on last year’s results, which incorporated a modestly less stringent severely adverse scenario than the 2019 stress test, and it also fails to incorporate any interim changes in the banks’ risk profiles. If any of the 17 banks wants to distribute more than its maximum pre-authorized amount, it may submit a capital plan to the Fed by 5 April 2019 and will be subject to the 2019 CCAR supervisory stress test.

Most major banks chose to use the so called advanced risk weighted approach to calculate the amount of capital they are required to hold as part of the Basel III frameworks against loans they write. This is an immensely complex (many would say over complex) and myopic approach to managing the risks in the banking system. But even then, who reviews and checks the approaches used, the calculations made and so the risk status of each bank?

Certainly the regulators do not have the time and resources to check each one in detail, so they tend to take the results on face value. So it was interesting to note that on 4 March, the secretary general of the Basel Committee on Banking Supervision (BCBS) suggested that entrusting external auditors with some responsibility for checking banks’ calculations of their risk-weighted assets (RWAs) would reduce the risk of errors and regulatory arbitrage.

External auditors would add another line of defense and enhance the accuracy and reliability of banks’ calculations of their Common Equity Tier 1 (CET1) ratios, a credit positive.

According to Moody’s, RWAs constitute the denominator of banks’ CET1 ratios and are commonly calculated by large banks themselves based on their own data. Because they are based on regulatory rather than accounting concepts, external auditors are not commonly entrusted with certifying whether banks’ calculations of RWAs are accurate.

RWA calculations are subject to the scrutiny of supervisors who have often expressed concerns about banks’ internal estimates of their RWAs. This lack of trust has led to many initiatives: in December 2017, the BCBS introduced input and output floors as a means to limit the benefit that banks can obtain from calculating model-based RWAs (the so-called Basel IV framework).

The input floors are minimum thresholds imposed on parameters used in internal models. The output floor adds an overlay of constraint whereby the maximum benefit from implementing internal models is limited to 72.5% of the calculation derived from the new standardized approach. However, this new framework will only apply starting in January 2022 and the output floor will be phased in through January 2027.

Along the same vein, the European Central Bank recently embarked on a multiyear endeavor aimed at checking the quality of banks’ internal models (referred to as targeted review on internals models, or TRIM) and instructed many banks to fix identified shortcomings which often resulted in additional RWAs.

Supervisors to some extent rely on auditors’ verification of financial statements to conduct their own prudential analysis. Beyond this, auditors vet banks’ internal credit risk models under International Financial Reporting Standard No. 9 (IFRS 9), and those models are closely linked to prudential capital models. External auditors already play a role in banks’ data and processes that are critical for the computation of RWAs.

Additionally, some supervisors already commission external auditors to undertake specific work as a means to complement and inform their supervisory work. Within the European Union, supervisors in an estimated 10 countries require external auditors to provide comfort on capital, solvency and other ratios.

However, the formal validation of RWAs and capital ratios remains outside the scope of the audit. There has been no official decision by the BCBS as to whether the relationship between supervisors and external auditors should be standardized. Entrusting external auditors with a mandatory responsibility to certify CET1 ratios in addition to their usual remit would be a bold step if this initiative were to be spearheaded by the BCBS in its role as global standard setter. It remains to be seen whether a sufficiently large consensus will emerge among BCBS members; some supervisors might be reluctant to empower external auditors with such a critical mandate.

To be sure, external auditors’ certification of CET1 ratios would not be a panacea. Calculating RWAs is a complicated process, particularly at banks that rely on risk-modelling techniques. External auditors are unlikely to be able to address all shortcomings that the supervisory community has wrestled with for years (e.g., accuracy and consistency of RWAs), even if the auditors’ involvement would add a useful line of defense to ensure the accuracy of RWAs.

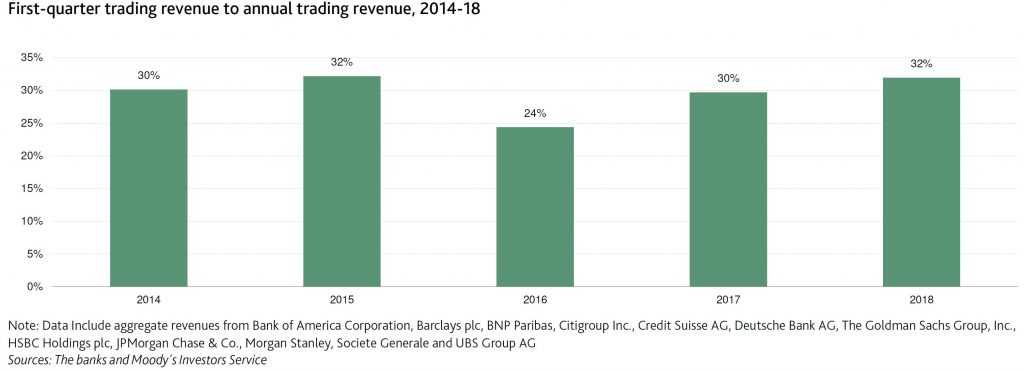

On 26 February, JPMorgan Chase & Co. at its Investor Day became the latest bank to caution that trading revenue would fall in first-quarter 2019, guiding to a year-over-year decline in core trading revenue in the mid-teen-percent range. JPMorgan has one of the world’s largest and most diverse trading operations and therefore may be more resilient than firms of smaller scale and scope, says Moodys.

A double-digit decline in trading revenue in the typically busy first quarter would be credit negative for banks with extensive market making operations, including Bank of America, Barclays, Citigroup, Credit Suisse, Deutsche Bank, Goldman Sachs, Morgan Stanley and UBS.

Economic fundamentals, technical market factors and sentiment are the primary drivers of capital markets volumes and volatility. Nevertheless, trading revenue also often displays seasonality. The first quarter is typically the strongest quarter of the year for marketmakers, driven by busy issuance calendars and strong interest by investment and portfolio managers to put money to work as a new performance period begins. By contrast, the third and fourth calendar quarters are often the weakest – owing to holiday day counts, buy-side and sell-side vacations and occasionally by reduced activity – as protecting annual performance increases in importance for certain portfolio managers.

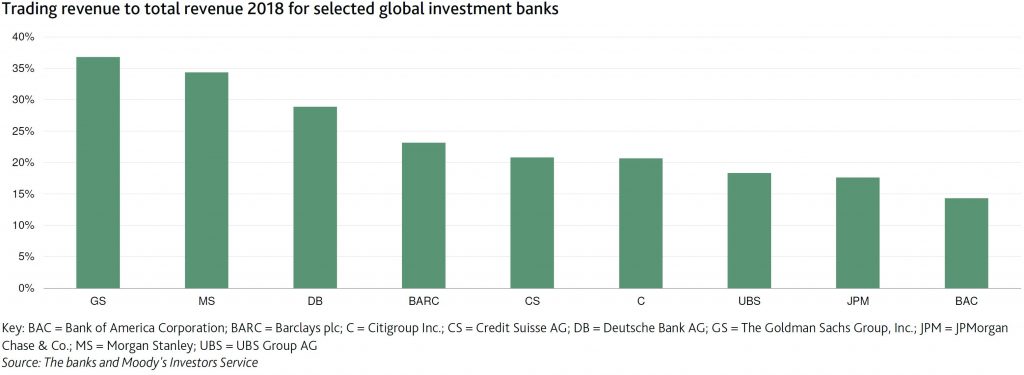

The vulnerability of individual banks to a shrinking trading wallet depends on the scale and diversification of their trading businesses and the diversification of their business mix. Diversification of a trading business can have asset class, product, customer and geographic dimensions. Firms with diversified trading operations will trade equities, fixed income, currencies and commodities (FICC) – making markets in cash and derivative products while offering financing and securities lending capabilities. Firms with the greatest client and geographic diversification deal with corporates, real money and leveraged investors, governments and other financial institutions in major market centers around the globe. Managing such expansive trading operations is definitely a challenge, but such a platform provides two distinct advantages: scale and the opportunity to monetize a greater share of customer flows.

Soft first-quarter trading revenue would follow a challenging fourth-quarter 2018 trading environment for the industry. Managements of trading operations are always trying to answer the vexing question of which declines are cyclical and which are structural. The question has become ever more pressing with FICC revenue down roughly 20% across the industry since 2014. The most durable firms tend to combine scale, diversification and expense flexibility to navigate cycles and preserve real optionality toward global capital markets that deepen and widen over time. Firms with less resilient business models may face tougher reengineering choices if the industry wallet remains depressed in 2019.

Perhaps one reason among many, why Goldman’s stocks have fallen more than 25% over the past year? 37% of revenue was from trading operations in 2018!

On 14 February, JPMorgan Chase & Co. announced that it has created and tested the JPM Coin, a new digital representation of US dollars redeemable at a 1:1 ratio in fiat currency, this despite CEO Jamie Dimon having slammed bitcoin as a fraud in the past .

The JPM Coin is for now a pilot offered to select client banks, broker-dealers and other corporations.

Would JPM Coin simply be a digital currency, rather than a cryptocurrency? If JP Morgan’s new coin operates privately and is only used for money transfers between the lender and its clients, it would not operate on a public network in the same way that cryptocurrencies such as bitcoin or ethereum do.

In addition to this, cryptocurrencies operate on public networks that anyone can join without permission and while in this case, it means that the many computers working together on the shared ledger is said to improve security (according to a recent Motherboard article), JPM coin will run on a blockchain network called Quorum, which requires permissions and users must be approved by JP Morgan.

Moodys says that although still at an early stage, the digital coin breathes some life back into blockchain technology, which was criticized during 2018 for falling short of proving tangible use cases. For value to be exchanged among participating members over a blockchain, a unit of account in digital format is needed. Consequently, the JPM Coin is designed to allow the bank’s clients to transfer value between participating members. The exchange from fiat to JPM Coin and vice versa would be done at a value equivalent to $1.00, but it promises to be instantaneous, reducing settlement time. Given that JPM Coin is currently offered only to JPM’s institutional clients, should the test prove successful, it could motivate new clients to join the JPM platform to benefit from its features. It is not clear how, or if, JPM will make the feature available to non-JPM clients.

The offering can potentially help the bank expand its ecosystem, allowing firms seeking instant value transfer to use this highly sought feature in the global movement of money and payments in securities transactions.

At its investor day last year, JPM guided for around $10.8 billion in technology spend for 2018. The combination of a highly profitable franchise and a dedication to technology reinforces JPM’s ability and willingness to innovate and defend its core payment franchises against disruptive threats.

Although a first-mover among US banks in the creation and testing of a digital coin, JPM Coin’s concept is not unlike fiat-backed “stable coins” that exist within the cryptocurrency sphere. Examples of stable coins include Tether and Coinbase’s USDC, which operate as digital coins designed to bypass the volatility inherent among cryptocurrencies. However, volatility is not the only risk that the JPM Coin promises to avoid: it also sidesteps counterparty risk. Stable coins offered by start-up crypto exchanges and platforms offer digital coin redemptions back into fiat currencies. However, a transfer back into fiat is only possible to the extent the platforms are capable of supporting the redemptions, which exposes the holders of stable coins to counterparty risk. Common concerns around the platforms’ creditworthiness revolve around the lack of confidence that the digital coin is in fact backed by an inventory of fiat currencies.

An ecosystem sponsored by JPM, with a counterparty risk rating of Aa1(cr) may garner higher trust than competing ecosystems. Operational risks have also plagued start-up digital currency exchanges that have often faced bankruptcy (Mt Gox, QuadrigaCX), fraud (Bitconnect) or cyberattacks (Coincheck).

In October 2017, JPM launched the Interbank Information Network (IIN), which currently has 157 banks signed up. The IIN is designed to facilitate the transfer of information using blockchain technology and aims to reduce costs for correspondent banks when dealing with wholesale payments, particularly when it comes to sharing of information to resolve payment delays. While IIN addresses information sharing, JPM Coin is designed to test the actual transfer of value.