APRA has released their monthly banking statistics for ADI’s to April 2018. And now we are really seeing the tighter lending standards biting. In fact, Westpac apart, all the majors have reduced their investor property lending.

APRA reports for each lender the net total balance outstanding at the end of each month and by looking at the trends we see the net of loan roll offs and new loans. This is important, as we will see.

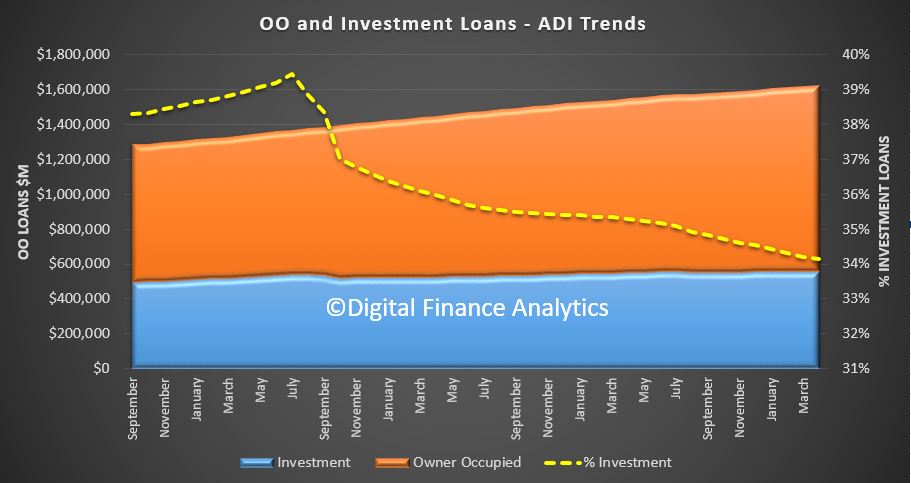

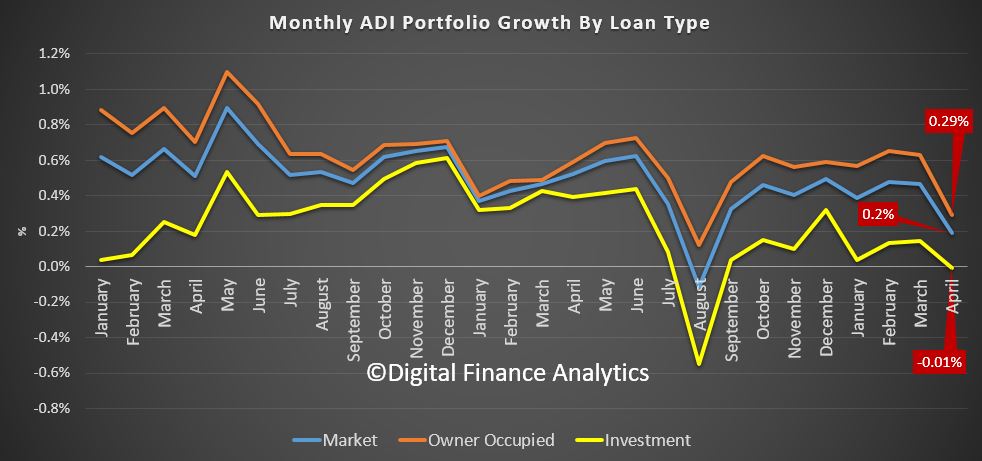

At the aggregate level, total lending for mortgages from ADI’s rose 0.2% in the month, up $3.0 billion to $1.62 trillion. Within that owner occupied loans grew by 0.29% or $3.1 billion to $1.07 trillion while investment loans fell slightly, down 0.01% of $42 million. As a result the relative share of investment loans fell to 34.14%.

The trend movement highlights the significance of the fall (the August 2017 point is an outlier thanks to reclassification), this is the weakest result for years. At an aggregate level, over 12 months this would translate to a rise of just 2.3%, significantly down from the 5-6% range of recent months.

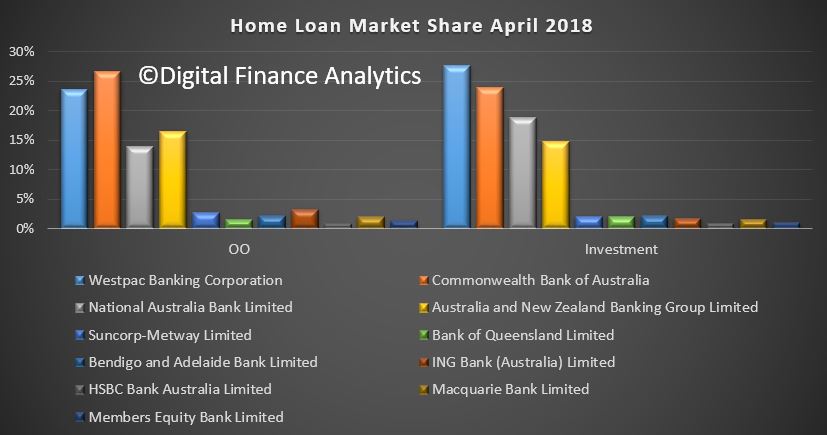

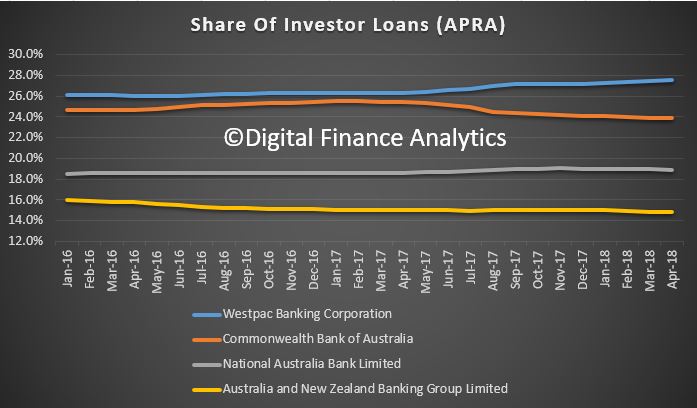

Turning to the individual market shares, at the aggregate level there was little change, other than Westpac’s share of investor loans grew to 27.6%, up from 26.1% in January 2016

Here is the trends from the big four. Westpac has continued to increase share of investor loans. CBA has fallen away the most significantly.

There has been almost no shift in owner occupied loan shares.

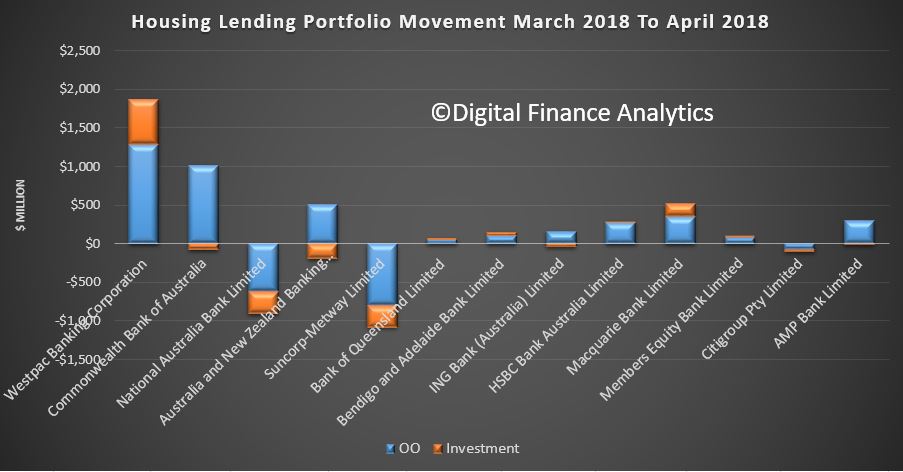

The monthly changes in value tell the story, with Westpac and Macquarie growing the value of their portfolios, across both owner occupied and investment lending. We see falls in net investor lending elsewhere.

We conclude that Westpac executed a different strategy in terms of mortgage origination compared with its competitors. They may be offering selective discounts to attract particular types of business, or they may have different lending standards, or both.

It is quite possible we will see other lenders trying to compete relative to Westpac in the investment loan domain ahead, as lending growth is needed to sustain profitability. But demand is also falling, so we expect lending momentum to continue to weaken, with the consequential impact on home prices and bank profitability. We are entering credit crunch territory!

At first blush the news at home and abroad appears to be steering us towards our most risky – scenario 4 outcome, where global financial markets are disrupted and home prices fall by 20-40 percent or more as confidence wains.

Some would call this GFC 2.0. So let’s looks at the evidence.

In Australia, as we predicted, a massive class action lawsuit is being planned on behalf of “Australian bank customers that have entered into mortgage finance agreements with banks since 2012”.

Law firm Chamberlains has been appointed to act in the planned class action lawsuit, which has been instructed by Roger Donald Brown of MortgageDeception.com in the action that aims to represent various Australian bank customers that are “incurring financial losses as a result of entering into mortgage loan contracts with banks since 2012”.

As the AFR put it – Lawyers’ representing up to 300,000 litigants are planning an $80 billion action against mortgage lenders, mortgage brokers and financial regulators in a class action that would dwarf previous actions. Roger Brown, a former Lloyds of London insurance broker, said he already has about 200,000 borrowers ready to join the action and has $75 million backing from UK and European investors. There has been a scam, he said about mortgage lending to Australian property buyers. “But the train has hit the buffers and there needs to be recompense.

As we discussed before, if loans made were “unsuitable” as defined by the credit legislation, there is potential recourse. This could be a significant risk to the major players if it gains momentum. And more will likely join up if home prices fall further and mortgage repayments get more difficult. But we think individuals must take some responsibility too!

Next, we now see a number of the major media outlets starting to blame the Royal Commission for the falls in home prices, tighter lending standards and even damage to the broader economy. Talk about shoot the messenger. The fact is we have had years of poor lending practice, and poor regulation. But the industry and regulators kept stumn preferring to enjoy the fruits of over generous lending. The Royal Commission is doing a great job of exposing what has been going on. In fact, the reaction appears to be that what had been hidden is now in the sunshine, and it is true the sunlight is the best disinfectant. Structural malpractice is being exposed, some of which may be illegal, and some of which certainly falls below community expectations. But let’s be clear, it’s the poor behaviour of the banks and the regulators which have placed us in this difficult position. Hoping bad lending remans hidden is a crazy path to resolution. At least if the issues are in the open they stand a chance of being addressed.

But it is also true that just a lax lending allowed households to get bigger mortgages than they should, and bid home prices higher, to be benefit of the banks, and the GDP out-turn, the reverse is also true. Tighter lending will lead to less credit being available, which in turn will translate to lower home prices, and less book growth for the banks. But do not lay this at the door of the Royal Commission. They are actually doing Australia a great service, in a most professional manner.

But that does not stop the rot. UBS came out today with an update saying that the housing market is slowing, with house prices falling and credit conditions tightening. Given the number of headwinds the market is facing; many investors are now questioning whether the housing correction could become disorderly. We expect credit growth to slow sharply and believe the risk of a Credit Crunch is rising.

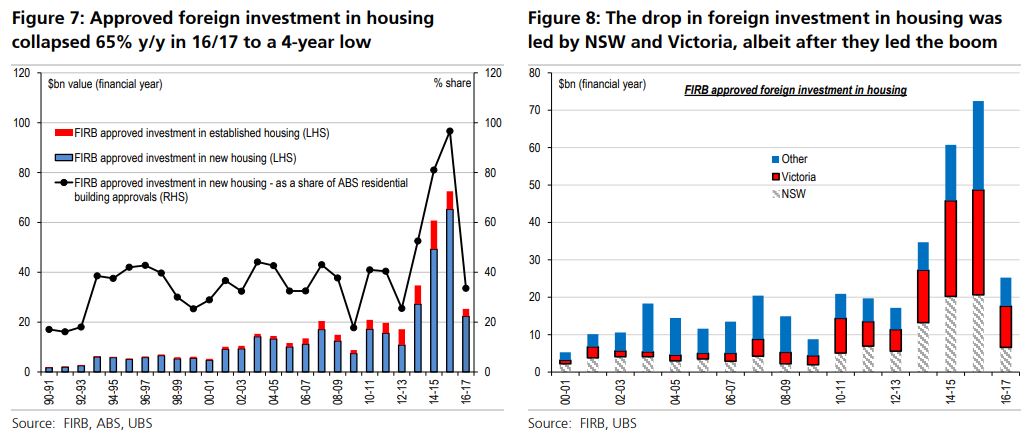

They walk through the main areas, including tighter lending, interest only loans and foreign buyers. Specifically, they highlight that approved foreign investment in housing is down -65%. The Foreign Investment Review Board just released data for 16/17. The value of approvals to buy residential housing collapsed 65% y/y to $25bn in 16/17, the lowest level since 12/13, and mostly reversing the prior ‘super boom’. The fall was across both new (-66% to $22bn) and established housing (-59% to $3bn) – led by total falls in NSW (-66% to $7bn) and Victoria (-61% to $11bn.

They say that the collapse in 16/17 may be overstated because of the introduction of application fees in Dec-15 – meaning the fall in transactions is less pronounced. But, there is still likely to have been a drop in transactions, reflecting more structural factors including – the lift in taxes on foreigners; domestic lenders tightening standards for foreign buyers (effectively no longer lending against foreign sources of income or collateral); as well as tighter capital controls especially from China.

Their base case is for a small fall in prices ahead, and assumes house prices fall by 5%+ over the coming year and that bad and doubtful debts increase only modestly given the current very benign credit environment. but they also talk about a downside scenario which reflects a more disorderly correction in the housing market (ie a Credit Crunch) and could result in approximately 40% reduction in major bank share prices. This is likely due to credit growth falling more substantially, by ~2-3% compound and credit impairment charges rising significantly as the credit cycle turns. This scenario would put pressure on bank NIMs. Litigation risk from class actions for mortgage misselling is also a tail risk. Dividends would need to be cut in this scenario. Given the leverage in the banking system, accurately predicting the extent of a downturn is very difficult, as was seen in 2008.

And the reason they still hold to their milder view is the expectation that the Government will step in to assist, and slow the implementation of recommendations from the Royal Commission. To quote Scott Morrison on 2GB radio on 23d March.

If banks stop lending, then what do people think that is going to mean for people starting businesses or getting loans or getting jobs or all of this. In the budget papers, the Treasury have actually highlighted this as a bit of a risk with the process we are going through. We have got to be very careful. These stories are heartbreaking, I agree, but we have to be also very cautious about, well, how do we respond to that. What is the right reaction to that? Is it to just throw more regulation there which basically constipates the banking and financial industry which means that people can’t start businesses and people can’t get jobs, people can’t get home loans. Or do we want to move to a smarter way of how this is all done and I think in the era of financial technology in particular there are some real opportunities there. We are going to continue to listen and carefully respect the royal commission, not prejudge the findings, but be very careful about any responses that are made because this can determine how strong an economy we live in over the next ten years and whether people get jobs and start businesses.

But in essence, expect some unnatural acts from the Government to try to keep the bubble going a little longer. All bets are off the other side of the election.

And the third risk, and the one which takes us closest to GFC 2.0 is what is happening in Italy. I am not going to go back over the history, but after months of wrangling, Italy’s political crisis has a hit an impasse, with new elections now increasingly likely. The country faces an institutional crisis without precedent in the history of the Italian republic. Its implications extend well beyond Italy, to the European Union as a whole.

Since an election on March 4, there have been endless vain attempts to form a government – with the likely outcome changing every 24 hours. By mid-May, the Five Star Movement (M5S) and the League, both populist parties, had come together to draft a programme for government featuring tax cuts and spending plans. But it sent shivers down the spines of those contemplating Italy’s public debt – running at over 130% of GDP – and threatened the stability of the eurozone.

The appointment of Carlo Cottarelli, a former official from the International Monetary Fund, as prime minister on May 28 was merely a stop-gap measure until fresh elections in the autumn. His government will almost certainly fail to win the necessary vote of confidence required of all incoming governments upon taking office. This means that it will be unable to undertake any legislative initiatives that go beyond day-to-day administration.

ITALY’S president, Sergio Mattarella had originally planned to put a former IMF economist, Carlo Cottarelli, at the head of a government of technocrats, tasked with steering the country back to the polls after the summer. But Mr Mattarella was reportedly considering changing tack after meeting Mr Cottarelli on May 29th amid growing evidence of support in parliament for an earlier vote. Not a single big party has declared its readiness to back Mr Cottarelli’s proposed administration in a necessary vote of confidence.

So the president is expected to decide on May 30th whether to call a snap election as early as July in an effort to resolve a rapidly deepening political and economic crisis that has sent tremors through global financial markets. There was also concern that the populist parties could win a bigger parliamentary majority in the new election, creating a bigger risk for the future of the eurozone.

In a sign of investors’ concern, the yield gap between Italian and German benchmark government bonds soared from 190 basis points on May 28th to more than 300. The governor of the Bank of Italy, Ignazio Visco, warned his compatriots not to “forget that we are only ever a few steps away from the very serious risk of losing the irreplaceable asset of trust.”

The yield on two-year debt has risen from below zero to close to 2% and Italy’s 10-year bond yields, which is a measure of the country’s sovereign borrowing costs, breached 3 per cent on Tuesday, the highest in four years. At the start of the month they were just 1.8 per cent. Italy’s sovereign debt pile of €2.3 trillion is the largest in the eurozone

The Italian stock market was also down 3 per cent on Tuesday, and has lost around 13 per cent of its value this month.

But these movements need to be put in some context. The Italian stock market is still only back to its levels of last July, after experiencing a strong bull run since later 2016.

In 2011 and 2012 Italian bond breached 7 per cent and threatened a fiscal crisis for the government in Rome. Yields are still some distance from those extreme distress levels.

George Soros was quoted in the FT:

The EU is in an existential crisis. Everything that could go wrong has gone wrong,” he said. To escape the crisis, “it needs to reinvent itself.” Mr Soros said tackling the European migration crisis “may be the best place to start,” but stressed the importance of not forcing European countries to accept set quotas of refugees. He said the Dublin regulation — which decides which nation is responsible for processing a refugee’s asylum status, largely based on which country the individual first enters — had put an “unfair burden” on Italy and other Mediterranean countries, “with disastrous political implications.” While austerity policies appeared initially to have been working, said Mr Soros, the “addiction to austerity” had harmed the euro and was now worsening the European crisis. US president Donald Trump’s exit from the nuclear arms deal with Iran and the uncertainty over tariffs that threaten transatlantic trade will harm European economies, particularly Germany’s, he said, while a strong dollar was prompting “flight” from emerging market economies. “We may be heading for another major financial crisis,” he said. Meanwhile, years of austerity policies had led working people to feel “excluded and ignored,” sentiment that had been exploited by populist and nationalistic politicians, said Mr Soros. He called for greater emphasis on grassroots organisations to meaningfully engage with citizens.

To play devil’s advocate, if Italy were to leave the Eurozone, the Lira would drop, hard. Most probably Italy would default on debt, and this would hit the Eurozone banks hard, especially those in German and French banks will be hit hard and they are saddled with about half the outstanding debt. Just like in the GFC a decade back, global counter-party bank risk will rise, and this time sovereign are involved, so it may go higher. The US Dollar will run hot, and there will be a flight to quality, tightening the capital markets, lifting rates and causing global stocks and commodities to crash, possibly a recession will follow.

In Australia, the dollar would slide significantly, fuelling stock market falls and a further drop in home prices, leading to higher levels of default, and recession, despite the Reserve Bank cutting rates and even trying QE.

Now the financial situation in Italy at the moment, a far cry from the height of the eurozone crisis in 2012, when it really did look possible that weaker member states would be imminently forced to default and the single currency would collapse. Then, that situation was finally defused when the head of the European Central Bank, Mario Draghi, announced he would do “whatever it takes” to stop this break up happening, unveiling an emergency programme of backstop bond buying by the central bank. This reassured private investor that they would, at least, get their money back and bond yields in countries like Italy and Spain fell back to earth, ending the risk of a destructive debt spiral.

But the latest deadlock in Rome is nevertheless the biggest crisis in the eurozone since Greece last threatened to leave in 2015. And Italy is a much larger economy than Greece. If the third largest country in the bloc exited the euro, it is doubtful the single currency would survive.

Falling bank shares dragged down Europe’s main share markets. At the close the UK’s FTSE 100 fell almost 1.3%, while Germany’s Dax was down 1.5% and France’s Cac 1.3% lower. “It’s a market that is totally in panic”, said a fund manager at Anthilia Capital Partners, who noted “a total lack of confidence in the outlook for Italian public finances”. And the chief economic adviser at Allianz in the US said: “If the political situation in Italy worsens, the longer-term spill overs would be felt in the US via a stronger dollar and lower European growth.”

So whether you look locally or globally its risk on at the moment, and we are it seems to me teetering on the edge of our Scenario 4. This will not be pretty and it will not be quick. I see that slow moving train wreck still grinding down the tracks, with no way out.

As we predicted, a massive class action lawsuit is being planned on behalf of “Australian bank customers that have entered into mortgage finance agreements with banks since 2012”.

If loans made were “unsuitable” as defined by the legislation, there is potential recourse. This could be a significant risk to the major players if it gains momentum. But we think individuals must take some responsibility too!

As the AFR put it –

Lawyers’ representing up to 300,000 litigants are planning an $80 billion action against mortgage lenders, mortgage brokers and financial regulators in a class action that would dwarf previous actions.

…Roger Brown, a former Lloyds of London insurance broker, said he already has about 200,000 borrowers ready to join the action and has $75 million backing from UK and European investors.

“There has been a scam,” he said about mortgage lending to Australian property buyers. “But the train has hit the buffers and there needs to be recompense,” he said.

Law firm Chamberlains has been appointed to act in the planned class action lawsuit, which has been instructed by Roger Donald Brown of MortgageDeception.com in the action that aims to represent various Australian bank customers that are “incurring financial losses as a result of entering into mortgage loan contracts with banks since 2012”.

The law firm is currently calling on bank customers to join the class action, led by Stipe Vuleta, if they have “incurred financial losses due to irresponsible lending practices”.

The MortgageDeception site says:

Those who have entered into loans with banks to purchase residential properties since 2011 are about to encounter difficulties. Since 1995, banks in the United Kingdom, Ireland, Australia and New Zealand have been making massive and obscene profits from providing finance to property purchasers. These banks have cared little about the lending practices adopted by them, and reckless lending has brought about huge and unsustainable increases in property prices.

These lending practices are now leading to problems for both intending buyers and existing owners of property.

We believe that the banking industry and its regulators have intentionally turned a blind eye to the irresponsible lending that has been taking place.”

For Australian bank customers that have entered into mortgage finance agreements with banks since 2012, we have appointed the leading Canberra-based law firm of Chamberlains, www.chamberlains.com.au, to act in the planned class action lawsuit. The partner in charge is Mr Stipe Vuleta.

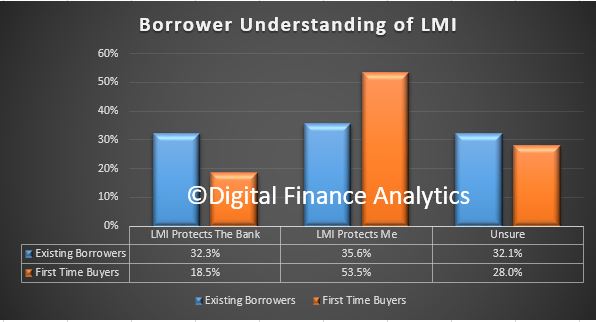

More than two in five prospective home buyers have admitted to not understanding Lenders Mortgage Insurance (LMI), according to new data.

This chimes with our research on the topic of LMI from our own surveys. In fact the confusion varies by type of buyer, and who is protected. First Time Buyers are a particular concern. See our previous post “Is Lenders Mortgage Insurance a Good Thing“.

Mortgage Choice and CoreData’s new Evolving Great Australian Dream 2018 whitepaper found 42.1% of respondents said they were not sure what LMI was, yet a third (32%) said they would need to pay it in order to get into the property market.

“Our data found that a majority of home buyers are in the dark when it comes to Lenders Mortgage Insurance and what it entails,” Mortgage Choice Chief Executive Officer Susan Mitchell said.

“According to our survey, only 32.1% of prospective buyers accurately stated that LMI is designed to protect the lender if a borrower can’t repay their mortgage.

“Another 8.2% of respondents thought LMI protected the borrower, while 17.6% believed it protected both the borrower and the lender,” said Ms Mitchell.

The research found that 44.8% of women did not to understand what LMI was, compared to 37.35% of men.

Buyers aged 29 and under (47.3%) were the most likely not to know what LMI was, while the 50 to 59 age group (40.75) had the highest proportion of buyers who knew what LMI was.

On a state by state comparison, Victoria (46%) had the highest proportion of buyers who did not know what LMI was, followed by Queensland (40%) and Western Australia (39.6%). NSW buyers topped the states when it came to correctly defining LMI at 34.6%.

Ms Mitchell said it was concerning that such a large proportion of Australians had either a limited or no understanding of LMI and that mortgage brokers can play an educational role for borrowers.

“For many first home buyers, LMI is likely to be a cost they have to pay to get into the property market, particularly if they do not have a deposit that is at least 20% of the purchase price,” she said.

“The reality is that saving for a home deposit is a major challenge for first home buyers and this has been the result of strong price growth over the last few years.

“According to CoreLogic, the median dwelling value in Australia is $554,605, and for a first home buyer to avoid LMI, they would need to save $110,921 for a 20% deposit and they would still need to have additional funds to cover costs such as legal fees and stamp duty.

“That is quite large sum to save and it only increases if a buyer is looking in cities such as Sydney and Melbourne.

“While LMI on the surface seems like a fee to be avoided, it does have the benefit of helping a buyer purchase a home with a smaller deposit, thereby allowing them to get onto the property ladder sooner rather than later.

“A buyer can choose to delay their property purchase to save a sufficient deposit, but the reality is property prices have risen consistently and the longer they delay, the more likely they are to miss an opportunity.

“Ultimately, in the long run, LMI is a fairly small expense in the overall cost of purchasing a home.”

Ms Mitchell said first home buyers could avoid LMI altogether if they were able to receive some sort of financial boost or a have a guarantor on their loan.

“First home buyers can avoid LMI by having a parent or family member go guarantor on their home loan, which then allows them to purchase without a 20% deposit” she said.

“In the case of the latter, it is important to note that lenders may require that any monetary gift must be held in an account for at least three months before home loan approval. Also, a lender may still require a borrower to demonstrate that they have 5% genuine savings.”

Ms Mitchell said it was important for first home buyers to have a good understanding of the purchase process.

“If you’re a first home buyer, you should speak to a mortgage broker who can guide you through the process of purchasing a property, from getting the best rate as part of the home loan application, through to settlement.

“They can explain the various options and costs involved, including LMI, thereby ensuring that you can confidently achieve your goal of home ownership,” concluded Ms Mitchell.

“As property prices continue to relax there has never been a better time for first home buyers to purchase. Therefore, it’s essential they have a clear understanding of LMI so that they know how it affects their ability to get into the market.”

A credit crackdown among the big four banks has been a blessing for the non-ADI sector, with lenders seeing a significant boost in prime mortgage flows. We discussed this a few weeks back.

Credit has been tightening since 2014 and a raft of measures have been introduced to stem the flow of investor loans, interest-only mortgages and foreign buyers.

“A lot of that is narrowing what is prime credit for a bank,” Fitch Ratings’ head of APAC, Ben McCarthy, told the group’s 2018 Credit Insights Conference in Sydney on Wednesday.

“As the bank prime market gets smaller, things that were prime last year will end up in the non-bank space.

“Talking to some of the issuers just recently, some of them have commented on the potential outcomes for them as an individual lender. Non-banks are telling me that their volumes are increasing, but not in the areas that you might think. Interest-only volumes are falling and investor loans are relatively stable.”

Australia’s RMBS market is dominated by the non-banks, which rely on securitisation and warehouse funding to grow their books and continue lending.

In 2017, securitisation issuance was at its highest since the GFC. Last year saw $36.9 billion of RMBS issuance, of which $14.7 billion came from the non-banks. Only $8 billion of issuance was made up of non-conforming loans.

The strength of the non-bank sector has attracted US investors. Last year, KKR snapped up the Pepper Group, Blackrock purchased an 80 per cent stake in La Trobe Financial and private investment firm Cerberus Capital Management, L.P. acquired the APAC arm of Bluestone Mortgages.

With a bolstered balance sheet, Bluestone was recently able to edge closer to the prime mortgage space by introducing a new product and lopping 225 basis points off its rates.

Last month, the non-bank lender entered the near-prime space and made significant rate cuts to the Crystal Blue portfolio, which comprises full and alt doc products geared to support established self-employed borrowers (with greater than 24 months trading history) and PAYG borrowers with a clear credit history.

Speaking of the move, Royden D’Vaz, head of sales and marketing at Bluestone Mortgages, said: “The recent acquisition of the Bluestone’s Asia Pacific operations by Cerberus Capital Management has enabled a number of immediate opportunities to be realised — most notably the assessment of our full range of products and to ensure they fully address market demands.

“We’re now in an ideal position to aggressively sharpen our rates based on the new line of funding and pass on the considerable net benefit to brokers and end users alike.”

With many anticipating a significant slowdown in bank credit growth, driven by the evidence given during the Hayne royal commission, non-banks look well positioned to capture a greater slice of the prime and near-prime markets.

“Non-banks are becoming a bigger part of the market,” Fitch Ratings’ Mr McCarthy said. “That trend will increase.”

Australian mortgage marketplace HashChing is launching its own branded home loans for the first time, claiming to offer some of the lowest rates in Australia, and one of the fastest approval times on the market available through the mortgage brokers.

They say this is an opportunity for Australians to access highly competitive deals that are independent of the big four and large financial institutions, whose shady lending practices have been recently exposed by the Royal Commission.

Mandeep Sodhi, CEO of HashChing, said that securing a competitive rate with the banks is a stressful experience for most Australian borrowers.

“Even a slight difference in an interest rate can cost the average homeowner thousands of dollars each year,” said Mr Sodhi.

“That’s why so many Australians access the market through a mortgage broker, but finding a broker that aligns with their interests can also be challenging. This is what motivated us to launch HashChing and what has motivated us to offer competitive home loans through our platform.”

The new home loan product, which can only be accessed by HashChing mortgage brokers, gives borrowers access to approval within an impressive 24 hours, one of the fastest approval times available to Australians through the mortgage brokers.

“Timing can be the difference between owning your own dream home or missing out on the opportunity of a lifetime. The big banks typically take 4 to 5 days to complete an approval process, so we’re confident we can offer a service in this area that they cannot compete with.

“On top of that, our core business is offering instant access to the top rated mortgage brokers in any area who do all the legwork at no cost to borrowers, meaning we now offer a front to back mortgage service with some of the most competitive deals on market.”

HashChing started to initially solve the pain point of finding a community rated local broker in the area. The move to offer home loans through the platform is part of the greater expansion plans for HashChing, which is currently raising $5 million through crowdfunding platform Equitise.

HashChing is independent of the big banks and has chosen to undertake crowdfunding as a means to raise money while staying independent of any ownership by the banks. The funds will help to improve and expand the company’s current business activities and enable it to continue looking for ways to improve on the home loan process and offer better rates to borrowers.

Mr Sodhi said: “One of the main reasons we chose equity crowdfunding was because we wanted to stay independent. Unlike many other online mortgage platforms who are backed by a lender, we are and will continue to stand separate from the banks. We want our customers to become shareholders in HashChing and help us deliver the simple and effective end-to-end home loan journey that Australia is currently lacking.

“We look for ‘win-win’ opportunities, whereby if our customers do well, we do too – and vice versa. One such opportunity is allowing customers to own a piece of HashChing and benefit from any success we have. We’ve built this business on the ability to put more money back into the pockets of homeowners and not the banks, and this crowdfunding opportunity extends that vision to give our loyal customers and everyday Australians an opportunity to invest in a fast-growing disruptive start-up that they believe in.”

HashChing is Australia’s first online marketplace allowing consumers to access great home loan deals without having to shop around. Completely free to consumers, HashChing connects customers directly with verified mortgage brokers who further negotiate better rates from lenders, saving valuable time and money.

Equitise is an online equity crowdfunding platform connecting start-ups and high growth businesses, with a broad range of investors. We help businesses grow and thrive in a simple, intuitive and social way by disrupting the investment marketplace and removing the traditional funding barriers and costs.

Cloud-based digital mortgage platform Athena Home Loans has closed a Series A raise of $15 million with investment backing from Macquarie Bank, Square Peg Capital, Apex Capital and Rice Warner.

Athena, founded by former NAB executives Nathan Walsh and Michael Starkey, pulled in a $3 million seed round in June 2017 and has now set its sights on disrupting the $1.7 trillion Australian mortgage market.

Speaking to The Adviser, co-founder and CEO Nathan Walsh noted that Athena plans to bypass the banks, offering super fund-backed mortgages directly to borrowers through its cloud-based digital portal.

“We know that the big banks are very constrained by customer pain points that are caused by ageing technology in the manual, paper-based processes, and we know there’s a real opportunity to improve on that,” Mr Walsh said.

Chief operating officer Michael Starkey claimed that Athena’s super fund-backed investment model would also allow it to offer lower interest rates than its competitors.

“By investing in home loans directly with Athena, super funds can cut the spread between what mortgage borrowers pay and investors receive,” Mr Starkey said.

“In countries such as the Netherlands, where pension systems are similarly advanced, the impact of this model is already evident.”

Mr Walsh added: “The potential savings for a typical Australian family switching from the big four banks to Athena could be as much as $100,000 over the life of the average loan.”

Mr Walsh also noted that Athena aims to settle $100 million in home loans this year, which the CEO said equated to approximately 200 home loans.

The Athena chief went on to say that the online lender plans to ramp up its offerings once it is established in the marketplace.

“We see a big opportunity [for brokers] here,” Mr Walsh continued.

“Next year, [it’s] game on; we really see a big opportunity. It’s a big market and we’re very keen about giving all Australians access to a better deal on their home loan.”

No immediate plans for the broker channel

Mr Walsh revealed to The Adviser that while Athena has no immediate plans to originate home loans through the broker channel, it could be an option in the future.

“[We’re] a direct model, so consumers are going direct to [Athena] and opening accounts directly, but we do know that, clearly, mortgage brokers are an important part of the market and we’ll consider that in our roadmaps for the long term,” the CEO said.

“[We] are considering those options, so I think those are probably things for future discussions.

“At this stage, we’re really focusing on our launch, which is targeting our direct channel.”

Compliance with responsible lending obligations

Mr Walsh also insisted that Athena would ensure it’s complaint with responsible lending obligations, saying that a “huge part” of the build phase has been “the ongoing process of design, legal and compliance review, to really make sure that we’re stepping through each stage of that journey.”

The CEO said: “[We want to] make sure we’re providing those really important protections, but at the same time, managing the complexities so it is a process that borrowers feel comfortable using digital channels. And that’s a really big part of the design thinking that’s gone into building that.”

Square Peg co-founder joins Athena board

As part of Square Peg Capital’s investment, co-founder Paul Bassat is set to join the Athena board.

“We are thrilled to be joining Athena’s journey,” Mr Bassat said.

“This is a great example of the type of team we love to back — smart, driven and focused on solving an important problem.

“The win-win model that Athena offers to investors and borrowers has huge potential to disrupt the way home loans are originated, serviced and funded in Australia.”

NAB’s wholesale funder and distributor of white label home loans – Advantagedge – has announced that, as of today, it will require NSW mortgagors to sign mortgage documents on paper.

They said that until relevant legislation regarding the need for wet signatures on mortgage documents is amended in NSW, it would send a paper copy of the mortgage documents to customers to be wet-signed and witnessed.

NAB-owned white label provider Advantedge has said that it is updating its digital mortgage process for NSW customers, and is now requesting that mortgage documents be wet-signed by customers and witnesses.

Formerly, Advantede could accept electronically submitted mortgage documents without a paper copy. However, from Monday, 7 May, it will require NSW-based customers to sign mortgage documents issued in NSW on paper and to be witnessed.

It has said that it will post (or send by encrypted email to print depending on customer preference) mortgage documents for customers to sign with a witness, and return to its settlement agents, MSA National.

Despite this, Advantedge will continue to issue NSW mortgage documents electronically so there will be no delays with settlement.

It added that should the mortgage documents be submitted electronically, Advantedge would still process these “as normal” but would also send a paper copy of the mortgage documents to customers to be wet-signed and witnessed.

Advantedge clarified that the following documents can still be sent and signed electronically:

Letter to Borrower(s)

Loan Contract

Loan and Settlement Authority

Direct Debit Request

Business Purpose Declaration

Loan Terms and Conditions Booklet

Credit Guide

Borrower’s Guide to Construction Loans

MSA National’s Estimated Costs Statement

NSW mortgage documents issued prior to Monday, 7 May 2018, will be accepted without a wet signature.

Those issued after this date may still be submitted electronically but will need to be accompanied by a paper-signed and witnessed mortgage document.

Advantedge told The Adviser that, until relevant legislation regarding the need for wet signatures on mortgage documents is amended in NSW, it would send a paper copy of the mortgage documents to customers to be wet-signed and witnessed.

It added that this change only applied to Advantedge (and not NAB), as it involves the execution of mortgages.

Indeed, NAB announced just last week that it had launched DocuSign in the broker channel, allowing customers to sign their mortgage documents from anywhere and on any device.

NAB general manager of broker distribution Steve Kane said that this is another example of NAB’s ongoing commitment to improving the customer experience and to supporting brokers.

“By giving brokers the ability to have customers digitally sign their upfront documents, we are making the home loan process simpler, easier and more convenient,” Mr Kane said.

“We have eliminated the delays that can come with requiring a physical signature, for example, and we are confident this new tool will go a long way to help create a more streamlined process for brokers and for customers.”

I’ve said before that the next downturn will, ironically, be triggered by regulation. Recent developments show this could soon play out.

This we week we’ve seen ANZ chief Shayne Elliott and RBA governor Philip Lowe both admit that lending is becoming more difficult.

On Tuesday, Elliott said that tighter controls around customer living expenses — an issue given extensive coverage during the first week of the Hayne royal commission – would slow lending down.

“It is also possible that lending standards in Australia will be tightened further in the context of the current high level of public scrutiny. We will continue to watch these issues carefully,” Mr Lowe said.

Exactly what these will look like remains to be seen, but the banking regulator expects ADIs to develop their own portfolio limits on the proportion of new lending at “very high” debt-to-income levels.

The problem with things like forensic evidence of customer living expenses and tighter restrictions on mortgage lending is that they will reduce credit availability.

About 10 months ago I wrote that “mortgages are the second largest pool of assets in Australia after superannuation. Messing with that could have serious implications. Particularly at a time when property price growth is moderating.

“The risk is that measures designed to strengthen the system could inadvertently weaken economic growth, consumer sentiment and the propensity for Australians to continue spending.”

That observation was made following the 2017 budget, when it was revealed that APRA’s powers would extend to the non-banks.

Former Pepper CEO Patrick Tuttle told me that such action would “accelerate a credit crunch” and a sharp correction in house prices.

But the stakes are higher now and the risks to mortgage growth have intensified. Customer living expenses are at the centre of this, but I doubt common sense will prevail when it comes to regulation and tighter policies.

Over the last few weeks I’ve spoken to a number of mortgage brokers, head groups and lenders about this issue.

On the record, they see more granular data around living expenses as a positive development. Off the record, they can’t stand the idea and anticipate a significant drop in volume.

One broker put it to me plain and simple: when a person gets a mortgage, they change their living expenses accordingly. They stop spending on rent, reduce their entertainment budget and work harder for that job promotion. In other words, they adapt to their new financial position.

Australians have a solid track record of paying down their mortgages. Arrears rates range from 0.76 per cent (ACT) to 2.5 per cent (WA).

While there have been no systemic problems in the Australian mortgage market, the banking royal commission is doing a great job of promoting a financial services industry rife with misconduct and risky behaviour. Which it is, to some extent, but how risky are the mortgages currently being written?

Are the banks tightening their lending policies because of risks, or is it simply a PR play to appease the regulators and the royal commission?

Either way, we can expect a reduction in credit availability and brace ourselves for what the knock-on effects of that will be.

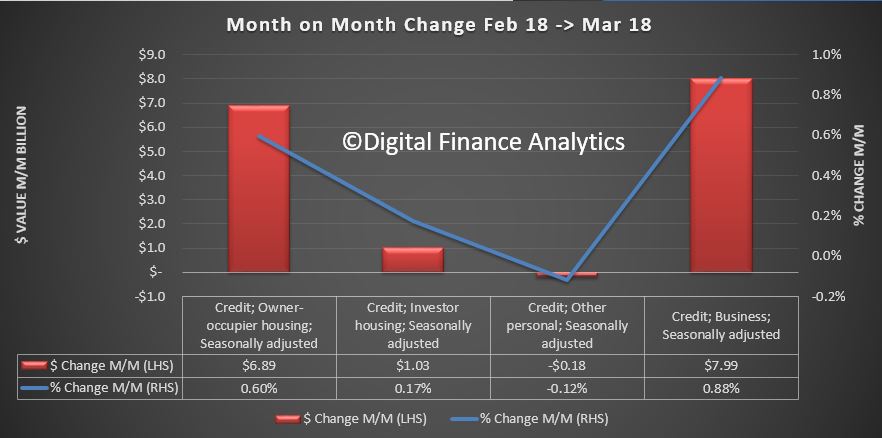

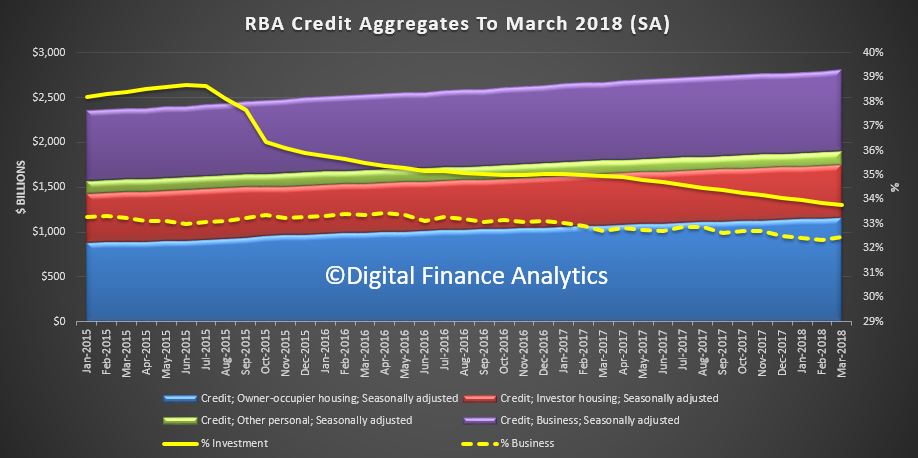

The RBA have released their credit aggregates to March 2018. Looking at the month on month movements, total owner occupied lending rose 0.6%, or $6.89 billion to $1,157.8 billion and investor mortgage lending rose 0.17% or $1.03 billion to $590.2 billion. So overall mortgage lending rose 0.46% in the month, up $7.92 billion (all seasonally adjusted) to $1.75 trillion. A record.

Personal credit fell 0.12%, down $0.18 to $152 billion. Business credit rose 0.88%, or $7.99 billion to $913 billion.

The trends show that the share of investment loans fell a little on the total portfolio to 33.8%, while business lending was 32.5% of all lending, up just a little.

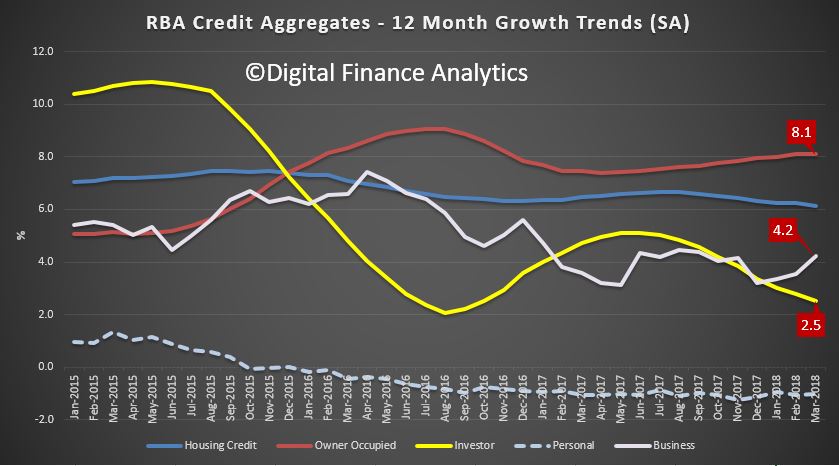

The 12 month average growth rates show that owner occupied loans rose 8.1%, while investment loans grew 2.5%. Business rose 4.2%, and personal credit fell again. Overall growth rates of credit for housing slide just a little to 6.1%. This is 3 times the rate of inflation and wage growth! Household debt therefore is still rising.

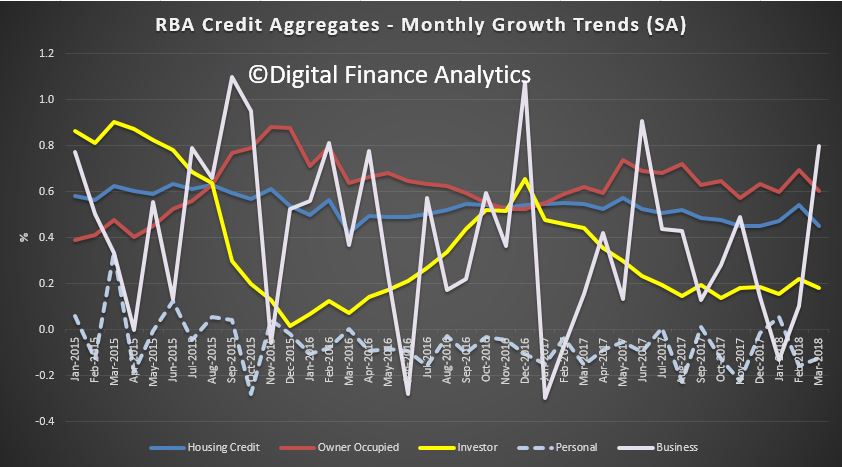

The noisy monthly data highlights how volatile the business lending trends are.

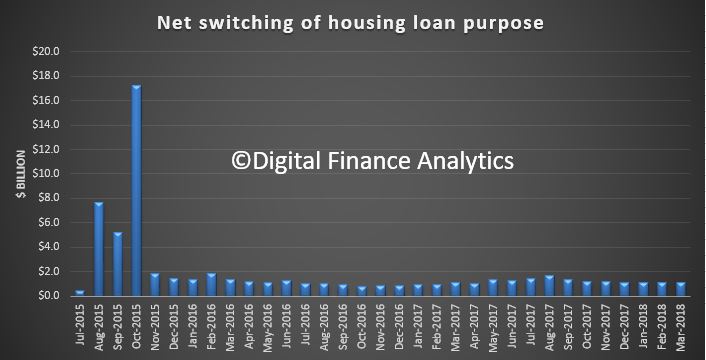

They also reported that the switching between investor and owner occupied loans continues to run at similar levels, after the hiatus in 2015.

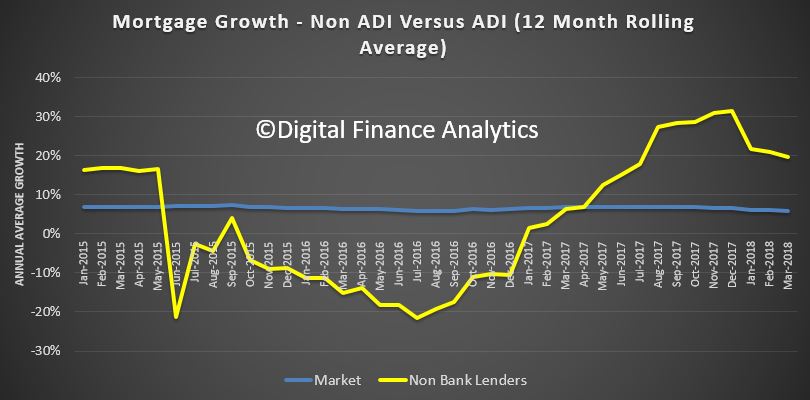

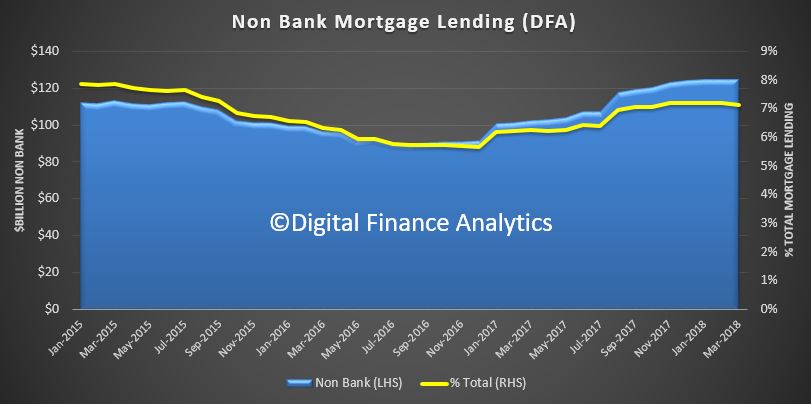

But set that aside, we have plotted the relative value of the mortgage pools at the total level, and the ADI level (not seasonally adjusted). The trend shows around 7% of lending is non-bank, up from 5.7% in 2017. In value terms this equates to $124 billion, up from $90 billion in 2016.

Another way to show the data is to look at the rolling 12 month growth trend. This shows that non-bank lending has been growing at up to 30% and significantly higher than the market at 5.94%.

So this is all playing out as expected. As the majors throttle back on new mortgage lending under tighter controls, the non-bank sector continues to pick up the slack. This is a concern as the regulatory environment for these lenders is weaker, with both ASIC and APRA now involved, ASIC from a responsible lending perspective and APRA from new supervision on the non-bank sector, despite their failure in the core banking sector. So we expect to see significant non-bank lending growth, ahead, which will stoke the current massively high household debts even higher.

The total loan mortgage growth is still significantly higher than income growth. This is not sustainable, and will lift mortgage stress higher again – our new data will be out in a few days.

The trend movement highlights the significance of the fall (the August 2017 point is an outlier thanks to reclassification), this is the weakest result for years. At an aggregate level, over 12 months this would translate to a rise of just 2.3%, significantly down from the 5-6% range of recent months.

The trend movement highlights the significance of the fall (the August 2017 point is an outlier thanks to reclassification), this is the weakest result for years. At an aggregate level, over 12 months this would translate to a rise of just 2.3%, significantly down from the 5-6% range of recent months. Turning to the individual market shares, at the aggregate level there was little change, other than Westpac’s share of investor loans grew to 27.6%, up from 26.1% in January 2016

Turning to the individual market shares, at the aggregate level there was little change, other than Westpac’s share of investor loans grew to 27.6%, up from 26.1% in January 2016 Here is the trends from the big four. Westpac has continued to increase share of investor loans. CBA has fallen away the most significantly.

Here is the trends from the big four. Westpac has continued to increase share of investor loans. CBA has fallen away the most significantly. There has been almost no shift in owner occupied loan shares.

There has been almost no shift in owner occupied loan shares. We conclude that Westpac executed a different strategy in terms of mortgage origination compared with its competitors. They may be offering selective discounts to attract particular types of business, or they may have different lending standards, or both.

We conclude that Westpac executed a different strategy in terms of mortgage origination compared with its competitors. They may be offering selective discounts to attract particular types of business, or they may have different lending standards, or both.