The number of small business customers signing onto loans through marketplace lenders has increased more than 500% over the past year, but experts say scrutiny must be put on the alternative finance sector now to ensure smaller operators get the best deal.

The Australian Securities and Investments Commission (ASIC) released its 2017 survey of marketplace lending practices this week, crunching the numbers of 12 key lenders in Australia. Marketplace lending covers a range of models, including peer-to-peer systems and other structures where investors put up funds on which they get returns when consumers and businesses borrow.

In 2015-16, ASIC’s survey of the sector put the total value of loans through this kind of model at $156 million, but that figure has doubled over the past year to now sit at $300 million. Total borrowers for the year jumped from 7,448 last year to 18,746 this year.

The pool of small business borrowers through these schemes has historically been small, but over the past 12 months there was a 509% increase, from 33 SME borrowers in 2015-16 to 201 in 2016-17. Seventy-seven percent of these business loans carried interest rates of between 12% and 16%.

Business customers borrowed $47 million through marketplace lending platforms in 2017, compared with $26 million in the year prior, according to the report.

The numbers come as regulators and Australia’s Small Business Ombudsman continue to focus on the challenges SMEs are currently experiencing when applying for finance from the big banks. In an era where property is hard to secure in Australia, Kate Carnell has told SmartCompany young business owners face big challenges ahead when applying for a bank business loan.

While options like marketplace lending provide an alternative to small businesses, Carnell has raised concerns that these models don’t always make it clear what businesses are signing up for.

The small business and fintech communities have started discussions to address these concerns, with Carnell, Fintech Australia chief executive Danielle Szetho and independent banking consultant and founder of thabankdoctor.org, Neil Slonim, holding a roundtable on the issue of transparency in SME lending this week.

Slonim tells SmartCompany that while the pool of business borrowers using marketplace lending is still very small, conversations must be had about it and alternative finance models more broadly.

“The main thing businesses need to understand is that borrowing through one of these models is different from borrowing through a bank,” he says.

The larger lenders have less room to move on their loan terms and are often “more transparent” when it comes to fees than their newer fintech competitors, Slonim says, while alternative lenders can find it “difficult to convey the true cost” of a loan.

He says it’s important to find a balance when discussing these concerns with fintech companies, because areas like marketplace lending will be valuable for small businesses into the future.

“It’s a really important sector, it needs to be encouraged, but there does need to be more self regulation and the regulators. In particular, ASIC will come in if they’re not satisfied there’s progression [on regulation],” he says.

These discussions will be a long-term process, with the Small Business Ombudsman, Fintech Australia and thebankdoctor.org planning on releasing a report in February 2018 with recommendations for establishing guidelines for interest rates and fees from alternative lenders.

Trade financing deep tech startup, Trade Ledger, has made it onto the APAC CIOoutlook “Top 25 FinTech Companies 2017” list after just 5 months with its unique digital banking platform for business banks and alternative lenders, who were previously unable to address the challenging SME sector without high expected losses. See our Fintech Spotlight Series note on the firm.

The list recognises promising fintech companies in the Asia-Pacific region that have not only demonstrated the use of technological innovation to solve an urgent and sizeable problem, but who have also shown an ability to commercialise their innovation for rapid adoption and scale.

“Trade Ledger was always intended to be a global end-to-end platform. The working capital problem we are solving is common to businesses and banks everywhere in the world,” said Martin McCann, CEO and Co-Founder of Trade Ledger.

“Finance providers have never been able to accurately leverage quality operational supply chain data to determine business lending risk, due to not having digital data access or suitable technology for credit assessment technology.

“As a result, most of the world’s SMEs are considered too risky for credit, when the truth is actually that credit modelling and underwriting processes are simply designed for multinationals and large corporations, not for our smaller SMEs.

“The unfortunate reality is that despite their smaller size, these SMEs represent an enormous chunk of the global lending opportunity: neglecting this important segment has resulted in a business loan undersupply to the tune of AU$90 billion each year in Australia, and AU$2.7 trillion globally.

“This essentially represents the size of the unaddressed opportunity for any business lenders wishing to use the Trade Ledger technology,” concluded Martin McCann.

Over 500 companies were assessed by the APAC CIOoutlook research team for inclusion in the final 25 fintech companies list.

These companies were all considered to be at the forefront of tackling market challenges and building technologies that greatly benefited other firms in the finance industry.

However, those who made the final cut stood out from their peers in terms of technological innovation, the size and urgency of the problem they solved, and their commercial prowess in bringing their technology to market.

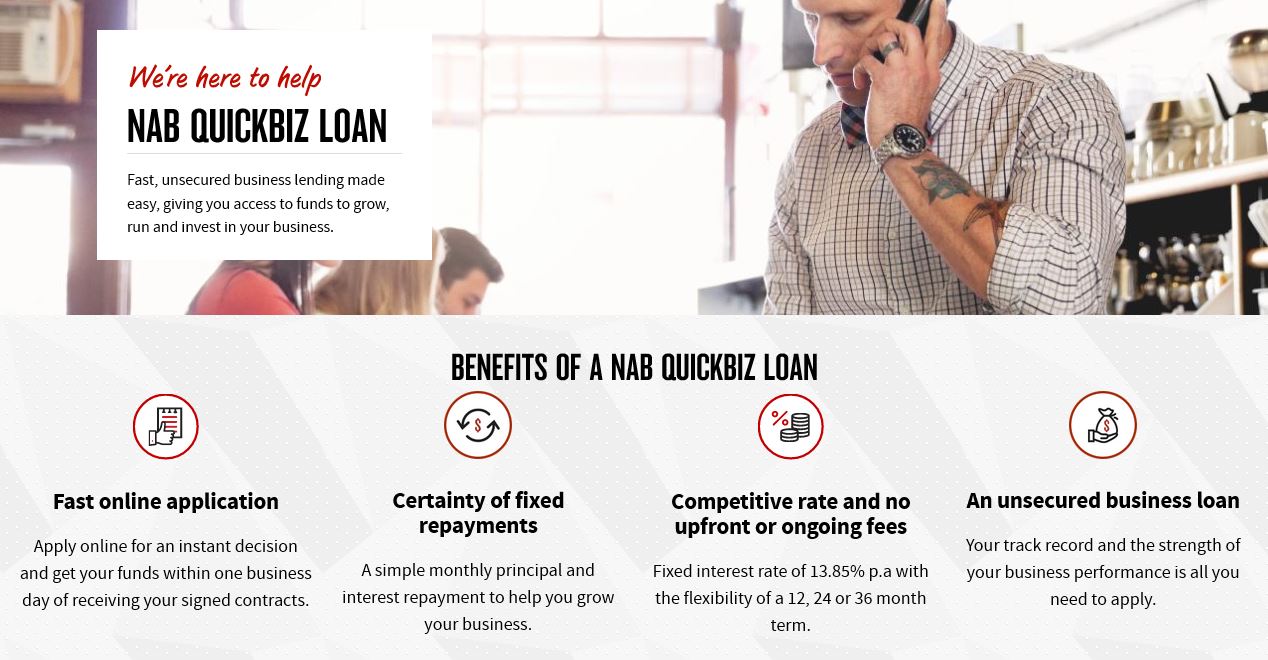

In a nod to the emerging Fintech SME lending sector, NAB today announced $100,000 unsecured lending for Australian small business owners to grow and expand, backing the strength of their business without the need for security requirements such as property or cash, with a decision is around 10 minutes. As we discussed recently, getting funding for SME ex. security is tough.

The rates look highly competitive at 13.85% relative to many of the other Fintech alternatives.

Customers apply via a fast and simple digital application process, with conditional credit approval granted in minutes. Once application contracts are signed and returned, cash is delivered within 24 hours.

Executive General Manager Business Direct and Small Business Leigh O’Neill said NAB recognises that fast and easy access to funds is critical for small businesses as they grow.

“There is often a perception that access to credit is difficult without a property or other major asset to secure against. That’s why we’ve responded by placing more emphasis on the strength of the business rather than traditional physical bricks and mortar, and we’re doing this at a fair and competitive price,” Ms O’Neill said.

NAB is the only Australian bank to have developed in-house an unsecured online lending tool without a third party referral involved. QuickBiz first launched in June 2016, initially up to $50,000.

The new $100,000 QuickBiz loan is an extension to NAB’s existing unsecured, self-service digital financing facilities, which includes an overdraft and credit card, all unsecured and capped at $50,000 for eligible customers.

“Six months after a QuickBiz loan application, just under half of our customers grew their business turnover by greater than 10 percent. This confirms we have an important role to play by offering finance to businesses with good prospects- it’s the the kick-start they need.”

“Small businesses are the backbone of the Australian economy. We need all parts of the economy – big business, government and industry – to get behind them to move the country forward.”

NAB’s Unsecured Solutions Fast Facts:

Unsecured QuickBiz loan, up to $100,000 available for eligible Australian SMEs

Direct connectivity to Xero or MYOB data, or simple financial upload from any accounting package

Application and decision in under 10 minutes

Competitive and transparent annualised interest rate charges, 13.85 % – no hidden surprises

For more information on the entire QuickBiz product suite (loan, overdraft) and Low Rate NAB business cards),

Christopher Kent, RBA Assistant Governor (Financial Markets), spoke at the 30th Australasian Finance and Banking Conference on The Availability of Business Funding, a subject which was featured in the recent RBA Bulletin.

While his speech covered the gamut of business finance, his comments on small business are important. He acknowledged the need for, and difficulty of getting funding in this sector. Something we have highlighted in our SME Report series, and which are still available. Whilst alternative lenders (Fintechs for example) have a role to play, (and there is massive opportunity in the SME sector in our view), most SME’s still go to the banks, where they have to pay more, for poor products and service. Indeed, if you are a business owner seeking to borrow, without a property to secure against, the options are limited. This is because the banks’ view is, correctly, unsecured risks are higher than secured, and in any case, they prefer to lend to mortgage holders more generally, as the capital required to do so is lower. Therefore many SME’s are at a structural disadvantage, and often end up having to pay very higher interest rates, if they can get finance at all.

There is much to do, in my view, to address the funding needs of SMEs, and this is a critical requirement if we are to seen sustained real economic growth. As Kent suggests, perhaps Open Banking will assist, eventually!

The challenge of obtaining finance has been a consistent theme of the Small Business Finance Advisory Panel. In this context, it is important to distinguish between two types of small businesses. First, there are the many established small businesses that are not expanding. Their needs for external finance are typically modest. Second, there are small businesses that are in the start-up or expansion phase. They are not generating much in the way of internal funding. Accordingly, those businesses have a strong demand for external finance. I’ll focus my comments on the issues relevant to this second group of small businesses.

I should emphasise again that access to finance for small businesses is important because they generate employment, drive innovation and boost competition in markets. Indeed, small businesses in Australia employ almost 5 million people, which is nearly half of employment in the (non-financial) business sector. They also account for about one-third of the output of the business sector.

Compared with larger, more established firms, smaller, newer businesses find it difficult to obtain external finance since they are riskier on average and there is less information available to lenders and investors about their prospects. Lenders typically manage these risks by charging higher interest rates than for large business loans, by rejecting a greater proportion of small business credit applications or by providing credit on a relatively restricted basis.

The reduction in the risk appetite of lenders following the global financial crisis appears to have had a more significant and persistent effect on the cost of finance for small business than large business. After the crisis, the average spread of business lending rates to the cash rate widened dramatically. The increase was much larger and more persistent, though, for small business loans (Graph 9). In part, this increase owed to the larger increase in non-performing loans for small businesses than for large business lending portfolios (Graph 10). It’s not clear, however, whether the increase in interest rates being charged on small business loans relative to those charged on large business loans (over the past decade or so) reflects changes in the relative riskiness of the two types of loans.[11]

Graph 9

Graph 10

Over recent years, there has been strong competition for large business lending, which has resulted in a decline in the interest rate spread on large business loans. Part of the competition from banks for large business loans has been driven by an expansion in activity by foreign banks. Large businesses also have access to a wider array of funding sources than small businesses, including corporate bond markets and syndicated lending.

In contrast, competition has been less vigorous for small business lending. Indeed, some providers of small business finance were acquired by other banks or exited the market following the onset of the crisis. Also, the interest rates on small business loans have remained relatively high. This difference in competitive pressures is evident in the share of lending provided to small business by the major banks, which is relatively high at over 80 per cent. This compares with a share of around two-thirds in the case of large businesses. Small businesses continue to use loans from banks for most of their debt funding because it is often difficult and costly for them to raise funds directly from capital markets.

The RBA’s liaison has highlighted that if small business borrowers are able to provide housing as collateral, it significantly reduces the cost and increases the availability of debt finance. Lenders have indicated that at least three-quarters of their small business lending is collateralised and they only have a limited appetite for unsecured lending. However, there are a number of reasons why entrepreneurs find it difficult to provide sufficient collateral for business borrowing via home equity:

they may actually not own a home, or have much equity in their home if they are relatively young;

similarly, they may not have sufficient spare home equity if they’ve already borrowed against their home to establish a business and now want to expand their business;

and even if they have plenty of spare home equity, using their homes as collateral concentrates the risk they face in the event of the failure of the business.

Many entrepreneurs have limited options for providing alternative collateral, since banks are far more likely to accept physical assets (such as buildings or equipment), rather than ‘soft’ assets, such as software and intellectual property.

Given the higher risk associated with small businesses, particularly start-ups, equity financing would appear to be a viable alternative to traditional bank finance. However, small businesses often find it difficult to access equity financing beyond what is issued to the business by the founders. Small businesses have little access to listed equity markets, and while private equity financing is sometimes available, its supply to small businesses is limited in Australia, particularly when compared with the experience of other countries (Graph 11). Small businesses also report that the cost of equity financing is high, and they are often reluctant to sell equity to professional investors, since this usually involves relinquishing significant control over their business.

Graph 11

Innovations Improving Access to Business Finance

There are several innovations that could help to improve access to finance by: providing lenders with more information about the capacity of borrowers to service their debts, and connecting risk-seeking investors with start-up businesses that could offer high returns.

Comprehensive credit reporting

Comprehensive credit reporting will provide more information to lenders about the credit history of potential borrowers. The current standard only makes negative credit information publicly available. When information about credit that has been repaid without problems also becomes available publicly, the cost of assessing credit risks will be reduced and lenders will be able to price risk more accurately; this may enhance competition as the current lender to any particular business will no longer have an informational advantage over other lenders. It may also reduce the need for lenders to seek additional collateral and personal guarantees for small business lending, particularly for established businesses. Indeed, the use of personal guarantees is more widespread in Australia than in countries that have well-established comprehensive credit reporting regimes, such as the United Kingdom and the United States.

For several years, the finance industry has attempted to establish a voluntary comprehensive credit reporting regime in Australia. Participation has so far been limited.[13] However, several of the major banks have committed to contribute their credit data in coming months. The Australian Government has announced that it will legislate for a mandatory regime to come into effect mid next year.

Open banking

The introduction of an open banking regime should make it easier for entrepreneurs to share their banking data (including on transactions accounts) securely with third-party service providers, such as potential lenders. When assessing credit risks, lenders place considerable weight on evidence of the capacity of small business borrowers to service their debts based on their cash flows. For this reason, making this data available via open banking would reduce the cost of assessing credit risk. A review is currently being conducted with a view to introducing legislation to support an open banking regime.

Large technology companies

Technology firms can use the transactional data from their platforms to identify creditworthy borrowers, and provide loans and trade credit to these businesses from their own balance sheets. This could supply small innovative businesses that are active on these online platforms with a new source of finance. Amazon and Paypal are providing finance to some businesses that use their platforms. For example, Amazon identifies businesses with good sales histories and offers them finance on an invitation-only basis. Loans are reported to range from US$1 000 to US$750 000 for terms of up to a year at interest rates between 6 and 14 per cent. Repayments are automatically deducted from the proceeds of the borrower’s sales.

Alternative finance platforms

Alternative finance platforms, including marketplace lending and crowdfunding platforms, use new technologies to connect fundraisers directly with funding sources. The aim is to avoid the costs and delays involved in traditional intermediated finance.

While alternative financing platforms are growing rapidly, they are still a very minor source of funding for businesses, including in Australia. The largest alternative finance markets are in China, followed by the United States and the United Kingdom. But even these markets remain small relative to the size of their economies (Graph 12).

Graph 12

Marketplace lending platforms provide debt funding by matching individuals or groups of lenders with borrowers. These platforms typically target personal and small business borrowers with low credit risk by attempting to offer lower cost lending products and more flexible lending conditions than traditional lenders. Data collected by the Australian Securities and Investments Commission indicate that most marketplace lending in Australia is for relatively small loans to consumers at interest rates comparable to personal loans offered by banks (Graph 13).

Graph 13

It is unclear whether marketplace lending platforms are significantly reducing financial constraints for small businesses. Unlike innovations such as comprehensive credit reporting, which have the potential to improve the credit risk assessment process, marketplace lenders do not have an information advantage over traditional lenders. As a result, they need to manage risks with prices and terms in line with traditional lenders. Nevertheless, these platforms could provide some competition to traditional lenders, particularly as a source of unsecured short-term finance, since they process applications quickly and offer rates below those on credit cards.

Crowdfunding platforms have the potential to make financing more accessible for start-up businesses, although their use has been limited to date. Crowdsourced equity funding platforms typically involve a large number of investors taking a small equity stake in a business. As a result, entrepreneurs can receive finance without having to give up as much control as expected by venture capitalists. Several legislative changes have been made to facilitate growth in these markets, including by allowing small unlisted public companies to raise crowdsourced equity.

We have highlighted the fact that Young Home Buyers have been turning to the Bank of Mum and Dad to fund their transaction, on average to the tune of more than $85,000; despite the risks of eroding their parent’s retirement savings.

Now the Australian Small Business and Family Enterprise Ombudsman has released a study into factors impacting small to medium enterprise investment. And the Bank of Mum and Dad figures again; another sign of inter-generational wealth shifting and the two tier “have and have nots”.

Speaking at the Institute of Public Accountants national conference on the Gold Coast, Ombudsman Kate Carnell said barriers to investment included access to capital, red tape and energy prices.

Ms Carnell said removing barriers to investment would give small businesses confidence to grow and boost jobs.

Despite recent claims by bank executives that lending to small firms is booming, Ms Carnell said this wasn’t the case for borrowers who don’t have equity in property.

“Traditional bank loans are backed by real property mortgages and although alternatives are emerging, they are not currently mature and affordable,” she said.

“Young aspiring small business operators are particularly disadvantaged and increasingly rely on their parents to provide seed finance.”

Ms Carnell said this meant the “Bank of Mum and Dad” was often called on to help young entrepreneurs.

“This offers convenience and flexibility, but it puts people’s retirement savings at risk,” she said.

“It also raises social equity issues in that the children of affluent parents have greater opportunities to buy and grow businesses.”

Ms Carnell said a government-backed guarantee scheme could be the answer, similar to the British Business Bank.

The Ombudsman’s study also takes aim at red tape, saying past reduction efforts have largely been “window dressing”.

Ms Carnell said a successful pilot in Parramatta to make compliance requirements seamless should be extended to other areas.

“It was found there were more than 50 pieces of regulation which applied to setting up a hospitality business in Parramatta and that the regulation meant it took up to 18 months to commence trading,” she said.

“Regulation wasn’t removed, but was instead sped up and made invisible. Information provided once was used to automatically complete forms in other areas of bureaucracy.

“This is a smart way of using systems and technology to relieve regulatory burdens on business.”

Prospa, Australia’s number one online lender for small business, has announced the delivery of more than half a billion dollars into the economy, providing loans to over 12,000 small businesses across the country.

Now in its sixth year, Prospa has scaled rapidly, today placing second in the AFR Fast 100 for 2017 thanks a 239 per cent average revenue growth since 2013-14. The AFR’s Fast 100 ranks the fastest growing companies in Australia, and in previous years has included the likes of Atlassian, Lonely Planet, SEEK and WebJet.

2017 has been been a bumper year for Prospa, having secured over $50m in equity and debt funding. The firm announced a $25m equity round led by AirTree and Square Peg in February (the largest deal of its kind in Australia at the time), which was followed by an additional $20m debt funding line from Silicon Valley-based Partners For Growth in July.

Over the past twelve months, the company has doubled the size of its loan book, and also grown its team by more than 50 per cent to 150 people from 33 countries. Recent key hires include Damon Pezaro ex Domain as Prospa’s first Chief Product Officer, and Rebecca James ex ME Bank, as Chief Marketing and Enterprise Officer.

Prospa also became the first fintech to win a Telstra Business Award, being named a New South Wales state winner in 2017, as well as being named Employer of Choice in the AON Hewitt Best Employers Program 2017.

Greg Moshal, co-founder and joint CEO of Prospa, comments, “For over five years, we’ve been transforming the way small business owners experience finance. Before Prospa, small business owners simply couldn’t access finance unless they had an asset to put up as security, and they certainly couldn’t do it in a fast easy way from the convenience of their own workplace. We’ve now provided over half a billion dollars in loans to small businesses, and there’s obviously a real need there. We’re now focusing on finding more ways to provide quick, easy access to capital: how, where and whenever it suits our customers.”

Beau Bertoli, co-founder and joint CEO of Prospa adds, “As we scale up, we’re taking a long term view on our growth plans. Awareness of fintech is at all time high, and the sector is at a tipping point in Australia. Regulatory uncertainty is being addressed through consultation and fast decision-making by Treasury, and we’re confident this will help kickstart the next wave of innovation and growth. We’re genuinely excited about the future.”

As a long term Prospa investor and Board member, Avi Eyal, Partner at UK-based Entrée Capital commented, “Prospa has had exceptional growth over the past four years, led by two of the best CEOs in tech today, Greg Moshal and Beau Bertoli. The team is world class and together they are the clear leaders in the Australian fintech market. We are proud to have Prospa in our portfolio.”

Danielle Szetho, CEO of FinTech Australia, commented: “We congratulate Prospa on this important achievement. Prospa’s incredible growth is a great reflection of our recent results from the EY FinTech Australia Census, which shows that fintech companies have tripled their median revenue since 2016, and that the industry overall is rapidly maturing.

This strong revenue growth is happening because fintech companies such as Prospa are providing new and innovative services that delight their customers, compared to the previous offerings from traditional financial services institutions.”

Small businesses are warned to get across their obligations when managing customer databases and sending email communications, after internet provider TPG was fined $360,000 this month for failing to process “unsubscribe” requests from customers.

The Australian Communications and Media Authority (ACMA) confirmed last Friday that TPG Internet received the infringement notice after an investigation prompted by customer complaints revealed the company’s “unsubscribe” function was not working as required in April 2017.

Customers complained that despite having hit the “unsubscribe” button after receiving electronic promotions from TPG, and withdrawing consent to receive such material, they kept getting these messages.

ACMA found TPG’s systems weren’t processing the requests properly in the month of April, meaning the company breached subsection 16(1) of the Spam Act 2003, which relates to sending messages to customers without their consent.

The Act makes it compulsory for businesses sending electronic communications to include “a functional unsubscribe facility”.

“This is a timely reminder to anyone who conducts email or SMS marketing to make sure the systems they have for maintaining their marketing lists are working well,” ACMA chair Nerida O’Loughlin said in a statement.

The communications authority has marked consent-based marketing strategies as an area of top priority.

However, director of CP Communications Catriona Pollard tells SmartCompany that in her experience discussing email and electronic content with businesses, too many are not aware of are rules for collecting data and communicating with customers.

“I would suggest there is a high percentage of people who haven’t ever read the Spam Act and don’t have any information about what they can and can’t do,” she says.

Aside from the risks of fines, Pollard says from a brand perspective, this lack of knowledge can mean companies might really infuriate customers.

“People hate spam, and I think businesses are often more focused on building up their database than on how people will see them,” she says.

Unsubscribes are unavoidable, so make sure the function works

Pollard warns businesses never to do things like “hide the unsubscribe button”, explaining unsubscribe requests are “part and parcel” of sending any digital communication, and businesses must take that on board.

Companies will see regular unsubscribe requests from customers, but even so, “email marketing is still one of the most powerful marketing tools,” Pollard says.

Director of InsideOut PR, Nicole Reaney, observes businesses are often keen to use low-cost formats like email to build a user base, but they still have to follow legislative requirements and make sure customers have consented to getting this information.

“It’s extremely tempting for businesses to utilise the very affordable and efficient platform of digital media with direct emails and text messages. However, it does place them in a position of exposure if there was no prior relationship or consent to the contact,” she says.

Pollard says for smaller operators, one way to get bang for buck is to focus on writing informative and useful content for your audience. That way, regardless of some people hitting the unsubscribe, a business will be engaging with those who most want that kind of information.

“Writing really good copy is really effective. It’s not just thinking about blasting information out to your database,” she says.

SmartCompany contacted TPG Internet for comment but did not receive a response prior to publication.

The Australian Taxation Office has put the hard word on ride-sharing drivers and the wider gig economy, reminding drivers working for platforms like Uber about the importance of meeting their GST obligations next tax time.

The tax office determined in 2015 that ride-sharing and ride-sourcing drivers should be classified in the same way as taxi drivers for GST purposes, meaning they must register for an Australian Business Number and for the GST even if they are under the $75,000 threshold.

However, the tax office says the message isn’t getting through, with ATO assistant commissioner Tom Wheeler saying in a statement that the tax office has notified over 120,000 ride-sharing drivers over the past 18 months regarding their tax obligations.

“We know that most drivers do the right thing, and we are now focusing attention on the minority of drivers that are not currently meeting their obligations,” Wheeler said in a statement this morning.

“Our message to taxpayers is that if you have a ride-sourcing enterprise you must get an Australian Business Number and register for GST as soon as you start driving. You also need to include the income on your tax return at tax time.”

Wheeler notes the ATO is sourcing information “directly” from banks and facilitators, and warns “we know who you are, and we know if you aren’t correctly meeting your obligations”.

“This isn’t a black economy issue,” says Lisa Greig, SME and start-up tax specialist at Perigee Advisers.

“The money’s going through Uber and into a bank account, [and] it will be found.”

Companies should remind workers of GST obligations

Wheeler says if ride-sharing drivers who have not registered for GST continue to ignore the ATO’s prompts, the tax office will register the drivers itself and then backdate the registration to their first ride-sharing payment.

“[The drivers] will be required to lodge and pay all outstanding tax obligations. Penalties and interest may also be applied,” he says.

Greig tells SmartCompany she believes many of these outstanding cases would be drivers who maybe did a few trips for a ridesharing app over a couple of weeks, made around $60 dollars, and then haven’t driven again.

“Those people still have to be registered for GST,” she says.

Businesses who employ a significant number of these ride-sharing type contractors – such as Uber – should have a “duty of care” to inform workers of their GST obligations, believes Greig.

SmartCompany understands Uber drivers are directed to the ATO’s ride-sharing information page and notified of their obligation as part of the signup process, but Uber is unable to sign them up when a driver registers on the platform, because Uber not a registered tax agent.

Other companies working with similar types of contractors should take a similar course in informing them about GST obligations, because companies should make it “as simple as possible” for workers.

However, one reason the ATO is having to chase people now might come down to the slackness of the drivers, Greig says, suggesting that signing up for an ABN and GST would likely take less time than signing up to drive with Uber.

“People who forget to register for GST are like those people who forget an old bank account has $2 of interest in it when it comes to tax time.”

Looking to the future of tax reporting, Greig says it won’t be surprising if Uber driving income is automatically detected by the tax office in future.

“But with where this is all going, in the future all your ride-sharing data will just get populated in MyTax come tax time and you won’t have to worry.”

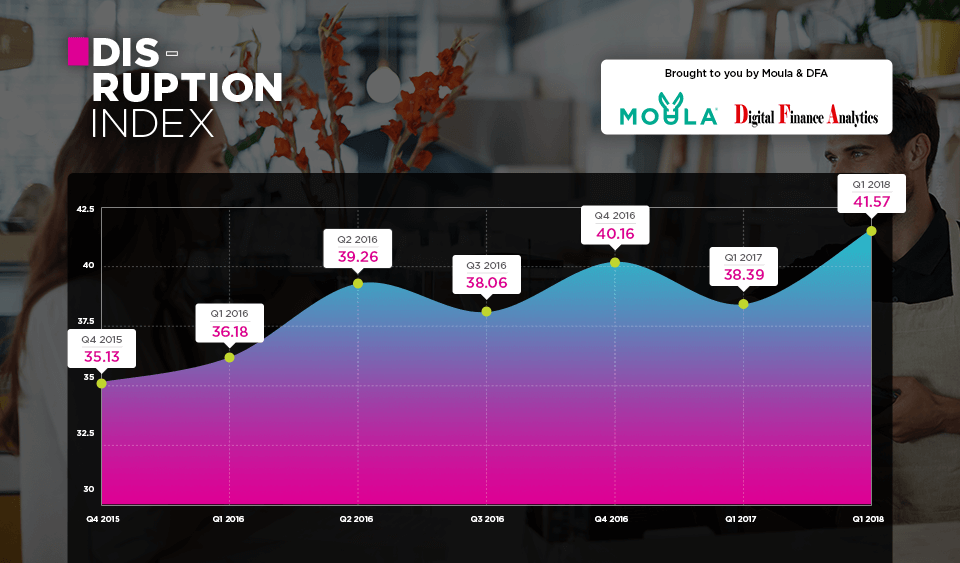

The latest edition of the Disruption Index has just been released, and it is 41.57, up from 38.29 last quarter. This is good news for Fintechs in that the SME community is adopting digital faster than ever.

The Financial Services Disruption Index, which has been jointly developed by Moula, the lender to the small business sector; and research and consulting firm Digital Finance Analytics (DFA).

Combing data from both organisations, we are able to track the waves of disruption, initially in the small business lending sector, and more widely across financial services later.

The index tracks a number of dimensions. From the DFA Small business surveys (52,000 each year), we measure SME service expectations for unsecured lending, their awareness of non-traditional funding options, their use of smart devices, their willingness to share electronic data in return for credit, and overall business confidence of those who are borrowing relative to those who are not.

Moula data includes SME conversion data, the type of data SME’s share, the average loan amount approved, application credit enquiries, and speed of application processing.

Here are some of the highlights:

Business Confidence

SME Business Confidence of those borrowing is on the up, reflecting stronger demand for credit, with the indicator jumping a healthy 15.8%, however, the amount of “red tape” which firms have to navigate is a considerable barrier to growth.

Knowledge of Non-bank Financial Providers

Awareness of new funding options continues to rise if slowly, creating a significant marketing opportunity for the new players, and a potentially larger slice of the pie.

Business Data

Greater willingness to share data and use of cloud-based services continue to rise. One-third of businesses have data held within the cloud, including accounting, customer management, invoicing, human resource, and tax management. We see variations across the segments in their use of these services. Of the businesses applying for funding, almost 90% now provide some form of electronic data via online loan application and are clearly comfortable in doing so (suggesting security concerns are less of a deterrent than the incentive of the speed of application and execution).

Average Loan Size

Average loan size continues to move upwards to register above $40k for the first time, indicating that better businesses are embracing alternative finance arrangements. More than likely, these businesses have traditional banking relationships, but either choose (or are forced to) look elsewhere for liquidity.

The Financial Services Disruption Index, which has been jointly developed by Moula, the lender to the small business sector; and research and consulting firm Digital Finance Analytics (DFA).

The Financial Services Disruption Index, which has been jointly developed by Moula, the lender to the small business sector; and research and consulting firm Digital Finance Analytics (DFA).