On 1 July, legislation in Denmark took effect that will trigger the inaugural issuance of Danish public housing covered bonds (almene realkreditobligationer) as a new asset class, says Moody’s.

These new covered bonds will be issued out of newly established capital centres with the sole purpose of funding mortgage loans granted to public housing companies (almen boligforening). As is the practice in the Danish covered bond market, assets serving as security for covered bonds must be segregated into independent cover pools, referred to as capital centres in mortgage banks. The Danish government guarantees in full the mortgage loans as well as the public housing covered bonds.

The law is credit positive for potential investors in public housing covered bonds because their credit risk will be lower than in existing mortgage covered bonds. Although investors in both types of covered bonds benefit from recourse to the issuing mortgage bank and a pool of good quality mortgage assets, only public housing covered bonds benefit from a state guarantee in case the issuer fails to fulfil its obligations.

Today, public housing loans benefit from a municipality’s partial guarantee of the loan, but under the new framework such loans will benefit from the federal government’s guarantee covering the full loan amount. In 2017, Danish municipalities guaranteed on average the most risky 62% of mortgage loans. Under the new model, the government will charge a guarantee commission from the mortgage banks. The mortgage banks, owing to the government’s full guarantee, will have lower capital requirements and lower over- collateralisation requirements for the covered bonds that are set in Denmark at 8% of risk-weighted assets.

Denmark’s public housing covered bonds will be issued by mortgage banks via frequently held auctions and tap sales. For the issuance of public housing covered bonds, banks shall obtain bids for purchases from Denmark’s central bank on behalf of the Danish government before the bonds are sold to others, which reduces funding execution risk for the public housing companies and the mortgage banks. According to the Danish central bank, the government will purchase DKK42.5 billion of public-sector covered bonds in 2018, corresponding to the total of new loans and refinancings of existing loans. The government will bid at a rate corresponding to the yield on government bonds.

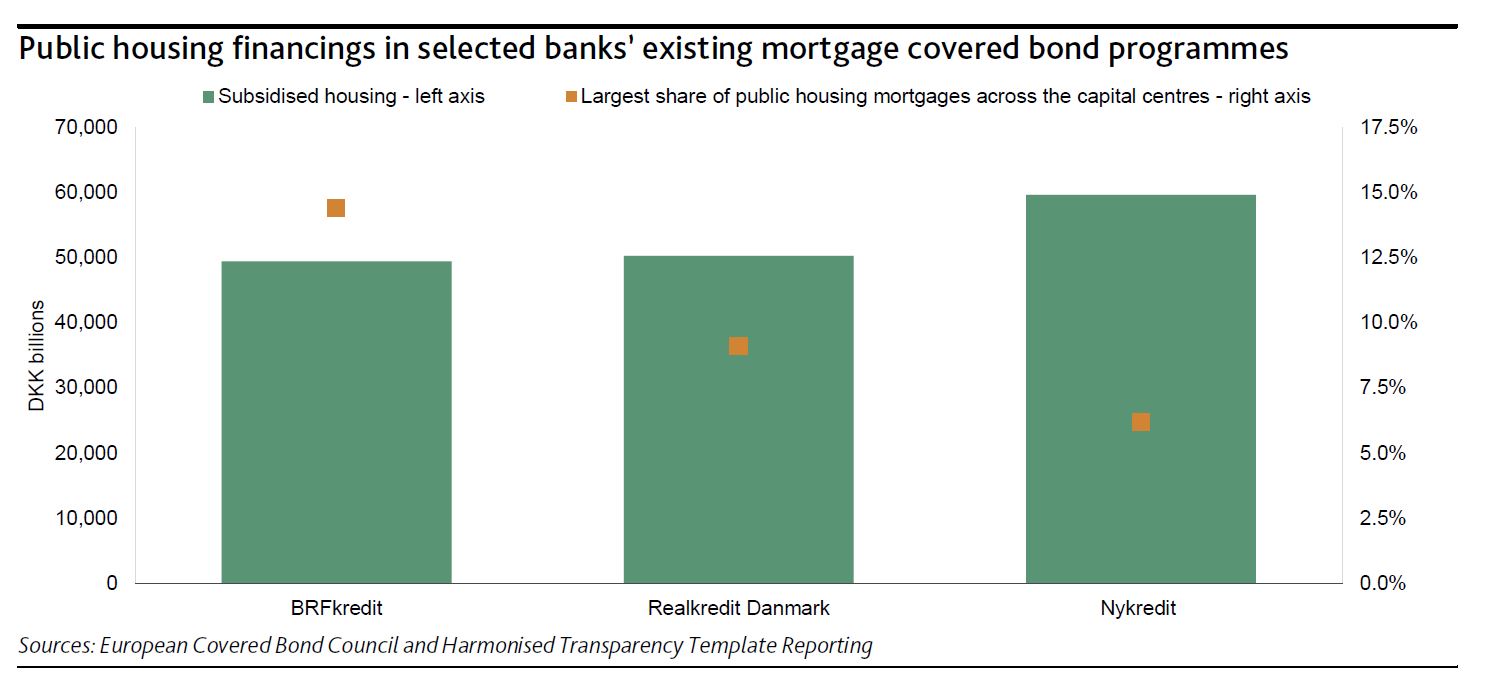

We expect a quick migration of public housing loans to the newly established capital centres in order to benefit from the government guarantees. This will lead to an increased level of prepayments and refinancings in the existing capital centres. The public housing sector has subsidised loans totalling around DKK180 billion that are largely financed by existing capital centres that issue mortgage covered bonds.

Nykredit Realkredit A/S, Realkredit Danmark A/S (part of Danske Bank) and BRFkredit A/S (part of Jyske Bank) are active lenders in this sector, each currently lending DKK50-DKK60 billion to the public housing sector. Despite the public housing loans being refinanced into the new capital centres, the risk characteristics of the capital centres will not change materially because the share of public housing loans is often small and in active capital centres does not exceed 15% as shown in the exhibit.

ASIC has accepted a variation to an enforceable undertaking provided by National Australia Bank Limited (NAB) relating to its wholesale spot foreign exchange (FX) business.

The variation imposes additional undertakings after an independent expert’s report identified significant deficiencies in NAB’s remediation program developed as part of the original EU, accepted in December 2016 (refer: 16-455MR).

Under the original EU, NAB was required to develop a program of changes to its existing systems, controls, monitoring, training and supervision of employees within its spot foreign exchange business to prevent, detect and respond to certain types of conduct. The program and its implementation was to be assessed by an independent expert.

In accordance with the EU, NAB provided its program of changes on 28 November 2017. On 29 March 2018, the independent expert reported on NAB’s spot foreign exchange program noting significant deficiencies regarding its:

Governance, Risk Management and Compliance Framework

Policies and Procedures

Risk Management Practices

Human Resource Management.

The independent expert also concluded that it was unable to complete the expert assessment of the program’s effectiveness required by the EU because NAB has made incomplete progress in designing items to be included in the program.

The expert’s report states ‘progress in developing the program has been slow’ and that the program ‘appears to have evolved iteratively during 2017, rather than through a well-defined process. For instance, there appears to have been no comprehensive risk assessment across NAB’s Spot FX business against the EU requirements and relevant regulatory standards and guidance.’

The variation of the EU imposes an additional undertaking on NAB to prepare an updated program that adequately addresses all required components. This updated program will then be subjected to further assessment by the independent expert. After these new undertakings are satisfied, NAB will be able to progress with the undertakings in the original EU.

Commissioner Cathie Armour said, ‘ASIC is disappointed with the delay in the development and assessment of a remediation program to address the conduct outlined in the EU. However, we are pleased that the process has been sufficiently robust to ensure any ongoing deficiencies have been identified and are being addressed, with oversight by an independent expert. ASIC’s ultimate objective is to ensure NAB has effective mechanisms in place to adequately train, monitor and supervise its employees to provide financial services efficiently, honestly and fairly’.

The wholesale spot FX market is an important financial market for Australia. It facilitates the exchange of one currency for another and thus allows market participants to buy and sell foreign currencies. As part of its spot FX businesses, NAB entered into different types of spot FX agreements with its clients, including Australian clients.

Spot foreign exchange refers to foreign exchange contracts involving the exchange of two currencies at a price (exchange rate) agreed on a date (the trade data), and which are usually settled two business days from the trade date.

“We welcome the feedback received from the independent expert in its initial report, which has helped us identify areas where we can do better to implement the program of changes,” Mr Gall said.

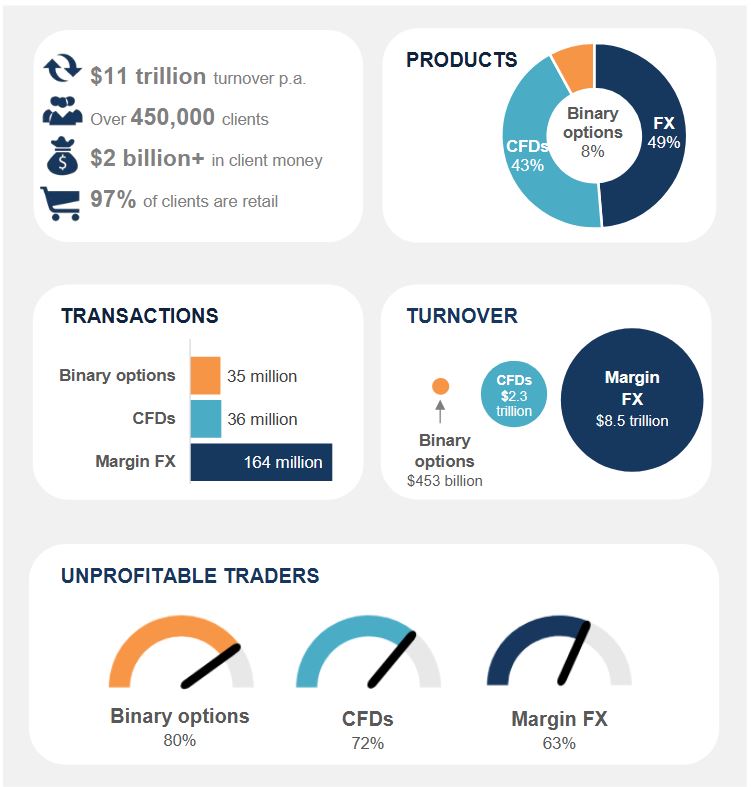

ASIC has called on participants in the retail over-the-counter (OTC) derivatives sector to improve their practices after recent ASIC activities showed their conduct fell short of expectations.

The products offered by retail OTC derivatives issuers in Australia include binary options, margin foreign exchange and contracts for difference.

A recent review of 57 retail derivative issuers identified a number of risks associated with the products offered to retail investors by OTC derivatives issuers.

Our review found that client losses in retail OTC derivatives trades seemed high, with the percentage of unprofitable traders being up to 80% for binary options, 72% for CFD traders and 63% for Margin FX traders. ASIC will examine this area further as part of its ongoing focus on the sector.

ASIC’s recent supervisory activities have also revealed sector-wide concerns about certain practices.

The most concerning practices ASIC has identified during in its supervision of the sector and highlighted in our recent reviews include:

actual client profits being inconsistent with marketing materials

a lack of transparency around pricing

risk management practices that relied on the use of client money were outdated and needed to be reviewed

some referral arrangements that may be in breach of conflicted remuneration requirements and referral selling prohibitions

some issuers that were providing wholesale services or allowing third parties to ‘white label’ their products did not have adequate risk management practices and operational capital to supervise counterparties and support their exposures.

Binary options may be the least transparent in terms of underlying pricing, strike prices and payout structures.

To address these risks, ASIC has called on issuers to:

review and update their risk management and client money practices; and

assess whether their arrangements with counterparties and referrers meet their AFS licence obligations.

ASIC Commissioner Cathie Armour said, ‘The retail OTC derivatives sector in Australia is an active and growing market, with an annual turnover of $11 trillion and over 450,000 investors. The integrity of the retail OTC derivatives sector is a key focus for ASIC. ASIC expects licensed issuers to conduct themselves appropriately and ensure consumers trade in retail OTC derivatives with a clear understanding of the products and the risks to which they’re exposed. We will be working with issuers to raise industry standards and improve compliance with their Australia financial services licence obligations.’

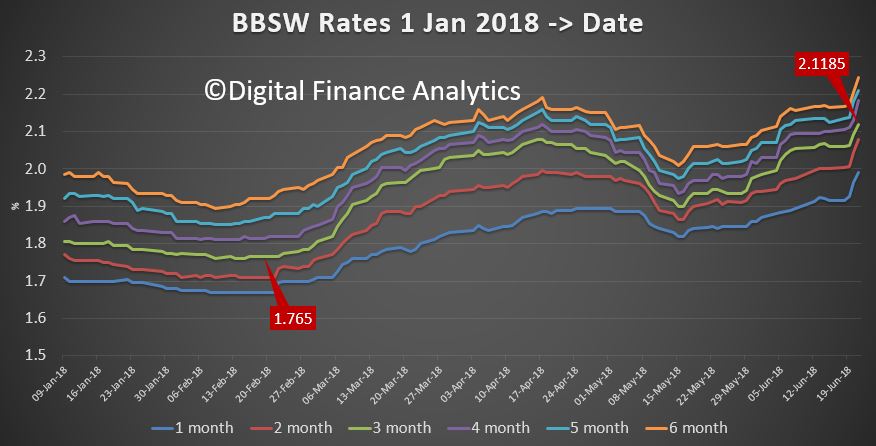

The benchmark BBSW rate has moved higher again, with the 3 month series now at a high of 2.1185; up ~36 basis points from February.

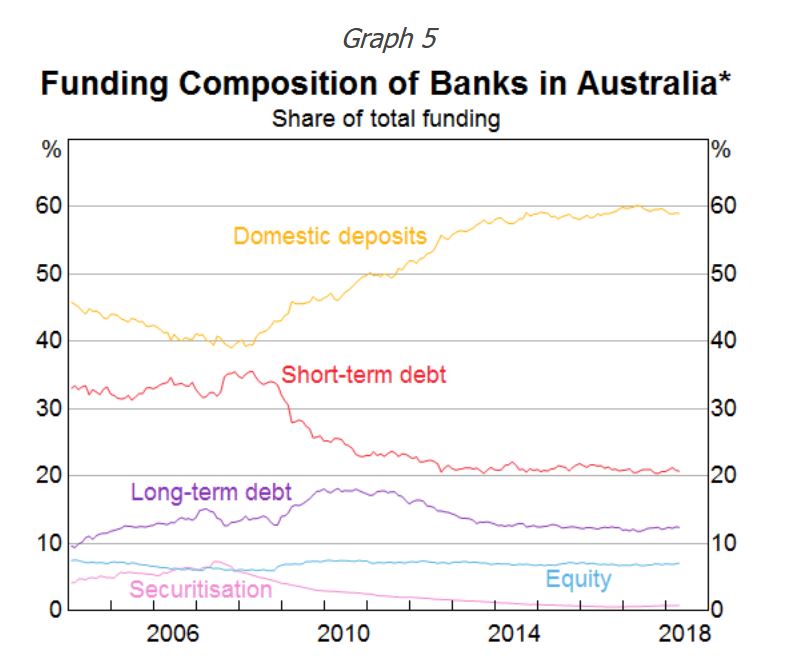

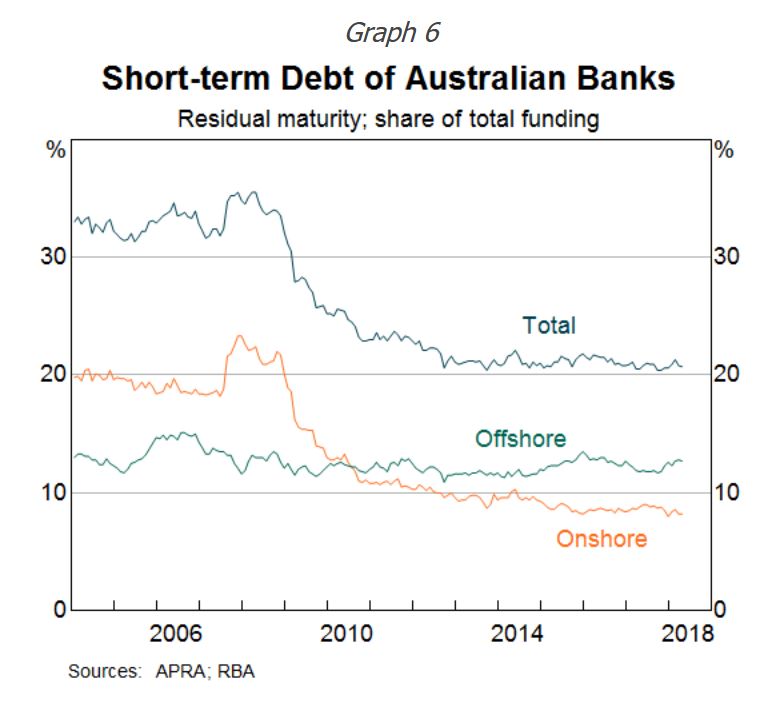

We know that around 20% of bank funding is from short term sources, according to the RBA.

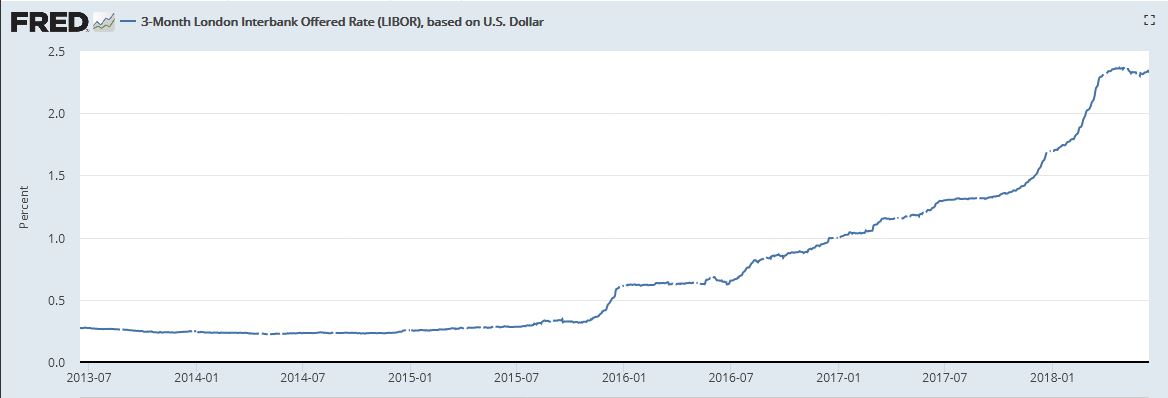

Of that, more is sourced offshore than onshore. Both overseas rates – as typified by the US LIBOR …

… and the local BBSW rates as we looked at before, suggest a hike in mortgage rates is coming. In fact more smaller lenders quietly lifted their rates last week, following Suncorp, ME Bank and others.

IMB Bank said from 22 June, its standard variable interest rate will increase by 0.08 per cent for new and existing home loan customers and Auswide has also lifted with increases of five basis points (0.05%) for owner occupied home loans and thirteen basis points (0.13%) for investment home loans and residential lines of credit, effective 27th June.

Unless the majors follow suite, expect their profits to drop, and returns of bank deposit to fall further.

Near-term global growth prospects remain robust despite rising trade tensions and political risks, but US inflation risks are rising, says Fitch Ratings in its new Global Economic Outlook (GEO).

Accelerating private investment, tightening labour markets, pro-cyclical US fiscal easing and accommodative monetary policy are all supporting above-trend growth in advanced economies. In emerging markets (EMs), China’s growth rate is holding up better than expected so far this year in the face of slowing credit growth; Russia and Brazil continue to recover, albeit slowly; and the rise in commodity prices is supporting incomes in EM commodity producers.

“Global trade tensions have risen significantly this year, but at this stage the scale of tariffs imposed remains too small to materially affect the global growth outlook. A major escalation that entailed blanket across-the-board geographical tariffs on all trade flows between several major countries would be much more damaging,” says Brian Coulton, Fitch’s Chief Economist.

Populist political forces continue to create policy risk and increase the threat of rising tensions within the eurozone that could adversely affect the outlook for investment, a key driver of growth last year. At this stage, we have made only a modest downward revision to our eurozone investment forecast for this year (to 3.3% from 3.9% in March), but a further escalation in uncertainty represents an important downside risk.

A much sharper-than-anticipated pick-up in US inflation remains a key risk to the global outlook. The decline in US unemployment – to 3.8% in May – is becoming more important to watch, and we forecast the rate to hit a 66-year low of 3.4% in 2019. A wide array of indicators of US labour market tightness suggest it is now only a matter of time before sharper upward pressures on US wage growth start to be seen.

“An inflation shock in the US could bring forward adjustments in US and global bond yields and sharply increase volatility, harming risk appetite. In particular, it could lead to a rapid decompression of the term premium, which remains negative for US 10-year bond yields. In combination with a likely aggressive Fed response, this would be disruptive for global growth,” adds Coulton.

Global growth forecasts remain unchanged since our March GEO, at 3.3% for 2018 and 3.2% for 2019. Nevertheless, 2018 growth forecasts have been revised down for 10 of the 20 economies that make up the GEO, with the eurozone seeing a 0.2pp downward revision, the UK a 0.1pp downward revision and Japan a 0.3pp downward revision. Brazil and South Africa have seen sizeable markdowns, and our Russia and Indonesia forecasts have also been lowered. These have been offset by 0.1pp upward revisions to the US and China and a stronger outlook for Poland and India in 2018.

For 2019, there have been fewer forecast changes, with the notable exception of Turkey, where recent currency turmoil and interest rate hikes are set to take a heavy toll on domestic demand. The US 2019 growth forecast has been raised by 0.1pp, and China’s 2019 outlook has been upgraded by 0.2pp following better-than-expected recent momentum.

Fitch still forecasts a total of four Fed rate hikes in 2018, followed by three more next year. Recent pronouncements from ECB officials suggest that the Asset Purchase Programme (APP) will be phased out in 2018, but also appear to imply that purchases will be scaled down between September and the end of the year rather than stopping abruptly after September. This is significant for the likely timing of the first ECB rate hike in 2019. ECB forward guidance has stated that rate hikes will not take place until “well after” the end of asset purchases, which the bank has clarified to mean quarters rather than years. A December 2018 end-date for the APP would imply rate hikes in 3Q19 or 4Q19. On this basis, we have revised our forecast of ECB rate hikes to just one increase in 2019, from two hikes before.

Global monetary policy normalisation and upward pressures on the US dollar have likely been contributing to the rise in financial market volatility witnessed so far this year. Both these global trends look set to stay.

The European Central Bank said it plans to remove accommodative policy but the euro zone monetary authority had yet to discuss when interest rates would be raised.

The ECB decided to cut its monthly asset purchase program in half to €15 billion at the beginning of October and noted that it was expected to end in December – although reinvestment of proceeds will be maintained. They indicated that interest rates were likely to be on hold for an extended period of time.

“The Governing Council expects the key ECB interest rates to remain at their present levels at least through the summer of 2019 and in any case for as long as necessary to ensure that the evolution of inflation remains aligned with the current expectations of a sustained adjustment path,” the ECB said in its policy decision.

Reiterating that point in the press conference’s question and answer period, president Mario Draghi stressed the “at least through the summer of 2019” and added that “we did not discuss if and when to raise rates.”

The euro, which turned negative against the dollar when the decision was published, extended losses after those remarks.

Weaker short-term growth, stronger inflation

The ECB also updated its economic projections and predicted weaker growth along with stronger inflation for this year.

“June 2018 Eurosystem staff macroeconomic projections for the euro area foresee annual real GDP increasing by 2.1% in 2018, 1.9% in 2019 and 1.7% in 2020,” Draghi announced. The 2018 growth forecast was cut from the 2.4% expansion predicted in March.

“The latest economic indicators and survey results are weaker,” Draghi explained, “but remain consistent with ongoing solid and broad-based economic growth.”

Overall, Draghi stated that the risks surrounding the euro area growth outlook remain broadly balanced.

However, he admitted that “uncertainties related to global factors, including the threat of increased protectionism, have become more prominent (and) the risk of persistent heightened financial market volatility warrants monitoring.”

With regard to price stability, the ECB now forecasts annual inflation of 1.7% through 2020, compared to the March projections of 1.4% for this year and next. The estimate for 2020 remained unchanged.

Draghi explained that the changes were made because the ECB felt that progress towards a sustained adjustment in inflation “has been substantial so far”.

“With longer-term inflation expectations well anchored, the underlying strength of the euro area economy and the continuing ample degree of monetary accommodation provide grounds to be confident that the sustained convergence of inflation towards our aim will continue in the period ahead, and will be maintained even after a gradual winding-down of our net asset purchases,” he added.

Welcome to the Property Imperative weekly to 9th June 2018, our digest of the latest finance and property news with a distinctively Australian flavour.

Watch the video, listen to the podcast, or read the transcript.

Today, a story. In the great city of Ghor, all the inhabitants were blind. A king and his entourage arrived nearby. He brought his army and camped in the desert. He had a mighty elephant, which he used to increase the people’s awe. The populace became anxious to see the elephant, and some sightless from among the blind community ran like fools to find it. As they did not even know the form or shape of the elephant, they groped sightlessly gathering information by touching some part of it. Each thought that he knew something, because he could feel a part… The man whose hand had reached the ear of the elephant, said “It is a large, rough thing, wide and abroad, like a rug.” And the one who had felt the trunk said: “I have the real facts about it. It is like a straight and hollow pipe, awful and destructive.” The one who had felt its feet and legs said” it is mighty and firm, like a pillar.” Each had felt one part of many. Each had perceived it wrongly…

The parable of the three blind men and the elephant makes the point that depending on where you feel, or look, you get a very different view of what’s currently going on, and so too with the economy.

For example, superficially, the latest GDP numbers released this week by the ABS were good news, showing 1.0% growth in real GDP over the quarter and a 3.1% rise over the year. The Treasurer was effusive. But below the spin, things are not so clear cut. In fact, net exports drove most of the growth because the terms-of-trade which measures the prices received for Australia’s exports relative to the prices paid for imports rose by 3.3% over the quarter in seasonally adjusted terms and by 1.6% in trend terms. However, over the year it fell by 2.6% seasonally adjusted and by 0.7% in trend terms. And these movement could be one offs. We were fortunate. Quarterly final demand, which excludes export volumes, rose by 0.6% over the March quarter, driven largely by VIC (+1.9%) and NSW (+0.7%).

But, on a more relevant per capita basis, real GDP rose by just 0.7% over the quarter and was up by 1.5% over the year and real national disposable income per capita also rose by 1.5% over the quarter and was up 0.9% over the year. And most importantly for Australian workers, average compensation per employee rose by just 1.6% in the year to March, and remained negative by 0.3% after adjusting for inflation (1.9%). It was 0.4% in the quarter. Plus, the household savings ratio continued to fall, down another 0.2% to 2.1% – the lowest reading in the post-GFC era. And what consumption there was went to necessities like electricity and fuel.

So my take is that while there is a glow of headline growth above 3%, in truth, its mainly migration led, plus a convenient shift in export prices, and a rise in government investment. Private sector business investment is sluggish, and households continue to reel from low wages growth and rising costs as signalled by falling savings, and a rise in debt. Not such a good story then.

This is confirmed by the retail turnover figures, also out this week. The ABS data, rose 0.3 per cent in April 2018 following a similar rise the previous month. Compared to April 2017 the trend estimate rose 2.6 per cent, above income growth. Across the categories, food retailing was up 0.4%, household good up 4%, other retailing 0.2%, Cafes and takeaway food 0.1%, department stores down 0.1%, clothes and footwear down 0.2%. Across the states, the trends were strongest in NT up 0.7%, ACT up 0.6%, NSW and VIC up 0.4%, TAS up 0.2%, QLD 0.1% and SA fell 0.1%.

Elsewhere on the elephant, we reported that Mortgage Stress Notched Up Again in May 2018. You can watch our Video “Mortgage Stress Updated – May 2018” where we discuss the details and walk though to top 10 most stressed postcodes across the country. Across Australia, more than 966,000 households are estimated to be now in mortgage stress (last month 963,000). This equates to 30.2% of owner occupied borrowing households. In addition, more than 22,600 of these are in severe stress, up 1,000 from last month. We estimate that more than 56,700 households risk 30-day default in the next 12 months. We expect bank portfolio losses to be around 2.7 basis points, though losses in WA are higher at 5 basis points. We continue to see the impact of flat wages growth, rising living costs and higher real mortgage rates.

The post code with the highest count of stressed households, was NSW post code 2170, the area around Liverpool, Warwick Farm and Chipping Norton, which is around 27 kilometres west of Sydney. There are around 27,000 families in the area, with an average age of 34. There are 6,974 households in mortgage stress here. The average home price is $805,000 compared with $385,000 in 2010. 64% of properties are standalone houses, while 22% are flats or apartments. The average income here is $5,950. 36% have a mortgage, which is above the NSW average of 32% and the average repayment is about $2,000 each month, so the average proportion of income paid on the mortgage is more than 33%.

The RBA left the cash rate on hold again this week, no surprise, of course. But the pressure on rates are on the rise due to the rising borrowing costs in the USA, and as reflected in the bond markets, and the local BBSW. Credit Suisse did a good job of dissecting the problem and they estimate that banks have something like a 0.5% – or 50 basis point gap in funding thanks to the changes in the rates. We discussed this in our video So, How Much Pressure on Bank Margins Now and look the RBA’s recent outing where they sought to explain away the pressure on rates. But Credit Suisse concludes:

The key issue is that the pipeline of out of cycle rate hikes is growing, with no end in sight until the RBA resolves the pricing mystery in the interbank market. There is too much pipeline pressure for adjustment to be borne by just one lever of credit creation, because interbank spreads are so persistently, and mysteriously wide. But recent commentary and the lack of responsiveness of interbank spreads to liquidity injections suggests to us that the Bank is no closer to resolving the mystery than it was in April, when it first noted tightening. The sheer depth of the pipeline of out of cycle rate hikes due to elevated funding pressures is beyond what policy makers are currently envisaging. To be sure, Banks do not have to hike rates out of cycle, or limit pass through of potential RBA rate cuts to end borrowers. They could cut deposit rates. Or they could take a hit to profitability, effectively passing on the funding pressure to shareholders rather than borrowers. But interestingly: 1. RBA work suggests that there are non-linearities in pass through when cash rates fall, precisely because deposit rates are already so low. As the cash rate falls, the relative cost of low/no interest fixed deposits increases. Substitution out of higher yielding deposits into low/no interest fixed deposits offsets this increase in relative cost – but there is a limit to the offset once the cash rate falls too far. 2. If margins take a hit, or are likely to take a hit, potentially banks could tighten lending standards even more aggressively than they currently are doing. Interestingly, interbank credit spreads currently point to a much sharper fall in loan approvals than our proprietary credit conditions index, based on publicly available data on bank lending standards. In other words, the growth shock from incremental credit tightening may be just as bad, if not worse, than out of cycle rate hikes, or lack of pass through. The issue is that corporate credit spreads are unusually low in comparison with interbank credit spreads.

And UBS discussed whether banks are likely to be able to pull out from their current market price falls. Australian banks they say…

have now underperformed the Australian market on a rolling 3-year timeframe and the sectors PE discount to market ex-resources has widened to the most since 2008. They rightly argue that bank profitability and share market performance is all about credit growth, and indeed the high growth in loans helped offset the fall in interest rates in the past couple of years. They conclude “UBS’s work on the prospect of a tightening credit cycle (see Credit Crunch? Seven factors to consider) suggests the ability to rebound from the current earnings lull will be very difficult, even if one subscribes to a “soft landing” scenario for house prices, credit growth and the economy. Credit growth should at a minimum grind lower over coming years. Bank NIMs are likely to be under at least moderate pressure (given BBSW trends) while bad debts at absolute best will be a neutral influence. The muted earnings outlook suggests that one can subscribe to a soft landing for housing and the economy amid tighter credit but still adhere to a strategic underweight in the sector. Of course a sharper credit slowdown will compound the headwinds for the sector.

And the fact is, so far the RBA has never started a tightening cycle at a time when dwelling prices are declining, until now.

So we hold to our view that mortgage rate pressure is on, and that will put more pressure on home prices which continue to fall. The bellwether is of course the auction clearance rates, which CoreLogic reported as now hitting a final weighted average last week of 46.91%. The signs are clear as we head into winter that fewer properties are being sold, more are being passed in and the number for sale, is growing by the day. SQM Research said this week

We continue to see a shortage of properties available for sale in Hobart. But elsewhere, the story is different, with greater supply now evident in most capitals compared to a year ago, leading to slowing growth in property asking prices as supply increases. We are also seeing more property being listed in Melbourne compared to a year ago, which has taken pressure off asking property prices for houses and units, which fell over the month. Even in Hobart, price growth has slowed despite the ongoing shortage of properties for sale there.

Corelogic’s Index shows that in Sydney, values fell by 0.11% last week and average values have fallen declined by 4.8% over the past 39-weeks. But this is an average, and some more expensive properties are more than 15% down now from their peaks. Auction clearances in Sydney’s mortgage belt – which runs in a ring from the southern beaches though Canterbury-Bankstown, Parramatta and the North West – have collapsed deep into the 30%s.

Melbourne fell by another 0.07%, and dwelling values have now also declined by 1.7% over the past 27 weeks, but is still positive by 1.9% over the past year. Two points to make here, first again the top of the market is moving sharply lower, and second, we think Melbourne is 6 to 9 months behind the Sydney trajectory, but is firming in the same direction. We are in correction territory now, and falls will accelerate. And frankly as Sydney and Melbourne contain the bulk of the population and property, what happens in these two states will set the tone elsewhere.

And the ACCC is going after ANZ, plus Deutsche Bank and CitiGroup’s investment banking arms alleging they engaged in cartel-like behaviour relating to a share placement in 2015. We discussed this in our post “Now Investment Banking Is Under The Microscope”, available on YouTube or via Podcast.

And talking of YouTube, we ran our first livestreaming Q&A session last Tuesday, with a couple of hundred people joining in. You can watch the 1:20 programme on replay on YouTube including the live chat, or listen to the podcast version. Thanks to everyone who joined in, and for those who sent questions in advance. I have to admit, we did not cover them all, so I will plan an extra offline session to answer some of the outstanding questions in the next few days. We will plan another live Q&A session in a couple of months, so watch out for that too.

Before we finish, a quick scan of the global financial markets – as I have received feedback that this part of the weekly reviews are well received.

First then, U.S. stock markets rose more than 1% this week but gains were held back in the latter part of the week somewhat as focus shifted to escalating trade tension between the U.S. and its key allies as the G7 summit got underway. U.S. President Trump refused to back down from his tough stance on tariffs, as he vowed to “fight” for the United States, and criticised allies, accusing them of imposing massive tariffs and creating non-monetary barriers. Tech was also one the stories of the week after coming under pressure on Thursday and Friday as Facebook and Apple fell. Apple fell nearly 1% Friday on reports the iPhone maker warned its supply chain to make fewer parts for iPhones in the second half of 2018 amid expectations for lower sales. Shares of Tesla rallied sharply this week after CEO Elon Musk said it is “quite likely” Tesla will hit a weekly Model 3 production rate of 5,000 cars by the end of June. The S&P 500 closed more than 1% higher for the week at 2,779.03.

Crude oil prices posted a third straight weekly loss after settling lower Friday on concerns about ongoing U.S. output after data showed the number of U.S. oil rigs continued to climb. Oil price action was choppy for most of the week as OPEC members attempted to allay fears the oil cartel would lift limits on production curbs at its June 22 meeting. U.S. oil output, meanwhile, continued to rise as the Energy Information Administration said Wednesday U.S. oil output rose to a record 10.8 million barrels per day. Oil prices were also limited by a weekly Energy Information Administration report showing U.S. crude supplies unexpectedly rose by 2.072 million barrels in the week ended June 1. Crude futures settled 22 cents lower on Friday as data showed U.S. oil rigs continued to climb, pointing to signs of growing domestic output.

The US dollar posted its first weekly loss in four weeks despite expectations the Federal Reserve will hike rates next week for the second time this year. 33.8% of traders expect the FED to hike rates for a fourth time at its December meeting, up from under 30% last week. The Federal Reserve will also release its summary of economic projections outlining expectations for key measures of the U.S. economy including inflation, interest rates, unemployment and GDP. The dollar was held back by a resurgent euro as European Central Bank policymakers stoked expectations the ECB would tighten monetary policy sooner rather than later. The dollar rose 0.12% to 93.54 against a basket of major currencies on Friday.

Locally, the Aussie Dollar held at 76 cents to the US dollar.

Gold prices bounced back from a weekly slump as dollar weakness encouraged buying, which was tentative, however, with a widely expected Fed rate hike on the horizon. Gold prices were unable to capitalise on rising geopolitical tensions as U.S. President Donald Trump went into the G7 meeting expecting a frosty reception after lashing out at Canada and the European Union. Gold appeared to be in ‘wait-and-see’ mode through the week as trading was restricted to a narrow range ahead of the Fed rate decision and the release of the central bank’s economic estimates.

Bitcoin seesawed its way to end the week roughly unchanged as regulatory uncertainty continued to weigh on sentiment despite signs of increasing institutional demand for the popular cryptocurrency. A report this week that Wall Street giant Fidelity was eyeing a move into the crypto space, planning to create products that would push the market for bitcoin to the “next level,” attracted a muted reaction. Bitcoin rose to a high of $7,777.4, testing a price level which some have identified as resistance – price levels that trigger selling – before paring gains. On the regulatory front, SEC chief Jay Clayton said this week, bitcoin was not a security, and further clarified the U.S. financial watchdog’s position on initial coin offerings, or ICOs. Demand for cryptocurrencies modestly improved as data showed the total crypto market cap rose to about $342 billion, at the time of writing, from about $329 billion a week ago.

And so back to the elephant analogy. There are a number of lumps and bumps across the US economy which suggests that pressure is building. For example, the flatter US yield curve underscores the lift in short term rates, and there is more to come. Higher rates mean that individuals and corporations will have to pay more. This chart shows the growth in US personal debt and the fall in savings, a trend which have grown in the past decades. Debt has never been higher, and savings is through the floor.

And remember that the US Government will have to pay more for their debt. This is important because the US Government is financing almost 25% of US GDP, and you have to ask whether this is sustainable.

But we still expect US rates to move higher, putting more pressure on local rates here. And there are simply no signs yet of any improvement in wages, as costs go on rising. Meantime the tighter lending controls and lack of sales momentum will see prices fall further, and by the way ANZ was the latest to forecast bigger falls, so more are joining the chorus – but the question is still extent and timing. Our modelling suggests we will see more severe falls, and we will be discussing this in upcoming posts

But the bottom line is compared with what we have seen so far, more falls must be expected, with all the downstream consequences which follow.

At first blush the news at home and abroad appears to be steering us towards our most risky – scenario 4 outcome, where global financial markets are disrupted and home prices fall by 20-40 percent or more as confidence wains.

Some would call this GFC 2.0. So let’s looks at the evidence.

In Australia, as we predicted, a massive class action lawsuit is being planned on behalf of “Australian bank customers that have entered into mortgage finance agreements with banks since 2012”.

Law firm Chamberlains has been appointed to act in the planned class action lawsuit, which has been instructed by Roger Donald Brown of MortgageDeception.com in the action that aims to represent various Australian bank customers that are “incurring financial losses as a result of entering into mortgage loan contracts with banks since 2012”.

As the AFR put it – Lawyers’ representing up to 300,000 litigants are planning an $80 billion action against mortgage lenders, mortgage brokers and financial regulators in a class action that would dwarf previous actions. Roger Brown, a former Lloyds of London insurance broker, said he already has about 200,000 borrowers ready to join the action and has $75 million backing from UK and European investors. There has been a scam, he said about mortgage lending to Australian property buyers. “But the train has hit the buffers and there needs to be recompense.

As we discussed before, if loans made were “unsuitable” as defined by the credit legislation, there is potential recourse. This could be a significant risk to the major players if it gains momentum. And more will likely join up if home prices fall further and mortgage repayments get more difficult. But we think individuals must take some responsibility too!

Next, we now see a number of the major media outlets starting to blame the Royal Commission for the falls in home prices, tighter lending standards and even damage to the broader economy. Talk about shoot the messenger. The fact is we have had years of poor lending practice, and poor regulation. But the industry and regulators kept stumn preferring to enjoy the fruits of over generous lending. The Royal Commission is doing a great job of exposing what has been going on. In fact, the reaction appears to be that what had been hidden is now in the sunshine, and it is true the sunlight is the best disinfectant. Structural malpractice is being exposed, some of which may be illegal, and some of which certainly falls below community expectations. But let’s be clear, it’s the poor behaviour of the banks and the regulators which have placed us in this difficult position. Hoping bad lending remans hidden is a crazy path to resolution. At least if the issues are in the open they stand a chance of being addressed.

But it is also true that just a lax lending allowed households to get bigger mortgages than they should, and bid home prices higher, to be benefit of the banks, and the GDP out-turn, the reverse is also true. Tighter lending will lead to less credit being available, which in turn will translate to lower home prices, and less book growth for the banks. But do not lay this at the door of the Royal Commission. They are actually doing Australia a great service, in a most professional manner.

But that does not stop the rot. UBS came out today with an update saying that the housing market is slowing, with house prices falling and credit conditions tightening. Given the number of headwinds the market is facing; many investors are now questioning whether the housing correction could become disorderly. We expect credit growth to slow sharply and believe the risk of a Credit Crunch is rising.

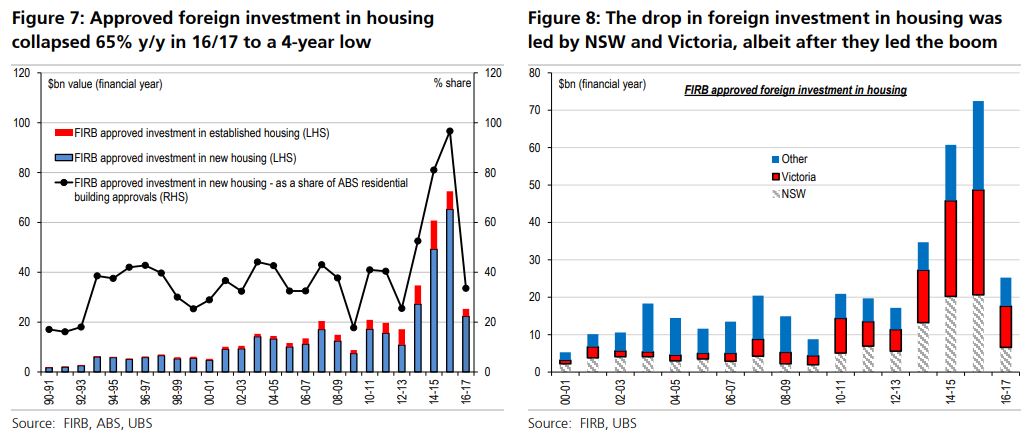

They walk through the main areas, including tighter lending, interest only loans and foreign buyers. Specifically, they highlight that approved foreign investment in housing is down -65%. The Foreign Investment Review Board just released data for 16/17. The value of approvals to buy residential housing collapsed 65% y/y to $25bn in 16/17, the lowest level since 12/13, and mostly reversing the prior ‘super boom’. The fall was across both new (-66% to $22bn) and established housing (-59% to $3bn) – led by total falls in NSW (-66% to $7bn) and Victoria (-61% to $11bn.

They say that the collapse in 16/17 may be overstated because of the introduction of application fees in Dec-15 – meaning the fall in transactions is less pronounced. But, there is still likely to have been a drop in transactions, reflecting more structural factors including – the lift in taxes on foreigners; domestic lenders tightening standards for foreign buyers (effectively no longer lending against foreign sources of income or collateral); as well as tighter capital controls especially from China.

Their base case is for a small fall in prices ahead, and assumes house prices fall by 5%+ over the coming year and that bad and doubtful debts increase only modestly given the current very benign credit environment. but they also talk about a downside scenario which reflects a more disorderly correction in the housing market (ie a Credit Crunch) and could result in approximately 40% reduction in major bank share prices. This is likely due to credit growth falling more substantially, by ~2-3% compound and credit impairment charges rising significantly as the credit cycle turns. This scenario would put pressure on bank NIMs. Litigation risk from class actions for mortgage misselling is also a tail risk. Dividends would need to be cut in this scenario. Given the leverage in the banking system, accurately predicting the extent of a downturn is very difficult, as was seen in 2008.

And the reason they still hold to their milder view is the expectation that the Government will step in to assist, and slow the implementation of recommendations from the Royal Commission. To quote Scott Morrison on 2GB radio on 23d March.

If banks stop lending, then what do people think that is going to mean for people starting businesses or getting loans or getting jobs or all of this. In the budget papers, the Treasury have actually highlighted this as a bit of a risk with the process we are going through. We have got to be very careful. These stories are heartbreaking, I agree, but we have to be also very cautious about, well, how do we respond to that. What is the right reaction to that? Is it to just throw more regulation there which basically constipates the banking and financial industry which means that people can’t start businesses and people can’t get jobs, people can’t get home loans. Or do we want to move to a smarter way of how this is all done and I think in the era of financial technology in particular there are some real opportunities there. We are going to continue to listen and carefully respect the royal commission, not prejudge the findings, but be very careful about any responses that are made because this can determine how strong an economy we live in over the next ten years and whether people get jobs and start businesses.

But in essence, expect some unnatural acts from the Government to try to keep the bubble going a little longer. All bets are off the other side of the election.

And the third risk, and the one which takes us closest to GFC 2.0 is what is happening in Italy. I am not going to go back over the history, but after months of wrangling, Italy’s political crisis has a hit an impasse, with new elections now increasingly likely. The country faces an institutional crisis without precedent in the history of the Italian republic. Its implications extend well beyond Italy, to the European Union as a whole.

Since an election on March 4, there have been endless vain attempts to form a government – with the likely outcome changing every 24 hours. By mid-May, the Five Star Movement (M5S) and the League, both populist parties, had come together to draft a programme for government featuring tax cuts and spending plans. But it sent shivers down the spines of those contemplating Italy’s public debt – running at over 130% of GDP – and threatened the stability of the eurozone.

The appointment of Carlo Cottarelli, a former official from the International Monetary Fund, as prime minister on May 28 was merely a stop-gap measure until fresh elections in the autumn. His government will almost certainly fail to win the necessary vote of confidence required of all incoming governments upon taking office. This means that it will be unable to undertake any legislative initiatives that go beyond day-to-day administration.

ITALY’S president, Sergio Mattarella had originally planned to put a former IMF economist, Carlo Cottarelli, at the head of a government of technocrats, tasked with steering the country back to the polls after the summer. But Mr Mattarella was reportedly considering changing tack after meeting Mr Cottarelli on May 29th amid growing evidence of support in parliament for an earlier vote. Not a single big party has declared its readiness to back Mr Cottarelli’s proposed administration in a necessary vote of confidence.

So the president is expected to decide on May 30th whether to call a snap election as early as July in an effort to resolve a rapidly deepening political and economic crisis that has sent tremors through global financial markets. There was also concern that the populist parties could win a bigger parliamentary majority in the new election, creating a bigger risk for the future of the eurozone.

In a sign of investors’ concern, the yield gap between Italian and German benchmark government bonds soared from 190 basis points on May 28th to more than 300. The governor of the Bank of Italy, Ignazio Visco, warned his compatriots not to “forget that we are only ever a few steps away from the very serious risk of losing the irreplaceable asset of trust.”

The yield on two-year debt has risen from below zero to close to 2% and Italy’s 10-year bond yields, which is a measure of the country’s sovereign borrowing costs, breached 3 per cent on Tuesday, the highest in four years. At the start of the month they were just 1.8 per cent. Italy’s sovereign debt pile of €2.3 trillion is the largest in the eurozone

The Italian stock market was also down 3 per cent on Tuesday, and has lost around 13 per cent of its value this month.

But these movements need to be put in some context. The Italian stock market is still only back to its levels of last July, after experiencing a strong bull run since later 2016.

In 2011 and 2012 Italian bond breached 7 per cent and threatened a fiscal crisis for the government in Rome. Yields are still some distance from those extreme distress levels.

George Soros was quoted in the FT:

The EU is in an existential crisis. Everything that could go wrong has gone wrong,” he said. To escape the crisis, “it needs to reinvent itself.” Mr Soros said tackling the European migration crisis “may be the best place to start,” but stressed the importance of not forcing European countries to accept set quotas of refugees. He said the Dublin regulation — which decides which nation is responsible for processing a refugee’s asylum status, largely based on which country the individual first enters — had put an “unfair burden” on Italy and other Mediterranean countries, “with disastrous political implications.” While austerity policies appeared initially to have been working, said Mr Soros, the “addiction to austerity” had harmed the euro and was now worsening the European crisis. US president Donald Trump’s exit from the nuclear arms deal with Iran and the uncertainty over tariffs that threaten transatlantic trade will harm European economies, particularly Germany’s, he said, while a strong dollar was prompting “flight” from emerging market economies. “We may be heading for another major financial crisis,” he said. Meanwhile, years of austerity policies had led working people to feel “excluded and ignored,” sentiment that had been exploited by populist and nationalistic politicians, said Mr Soros. He called for greater emphasis on grassroots organisations to meaningfully engage with citizens.

To play devil’s advocate, if Italy were to leave the Eurozone, the Lira would drop, hard. Most probably Italy would default on debt, and this would hit the Eurozone banks hard, especially those in German and French banks will be hit hard and they are saddled with about half the outstanding debt. Just like in the GFC a decade back, global counter-party bank risk will rise, and this time sovereign are involved, so it may go higher. The US Dollar will run hot, and there will be a flight to quality, tightening the capital markets, lifting rates and causing global stocks and commodities to crash, possibly a recession will follow.

In Australia, the dollar would slide significantly, fuelling stock market falls and a further drop in home prices, leading to higher levels of default, and recession, despite the Reserve Bank cutting rates and even trying QE.

Now the financial situation in Italy at the moment, a far cry from the height of the eurozone crisis in 2012, when it really did look possible that weaker member states would be imminently forced to default and the single currency would collapse. Then, that situation was finally defused when the head of the European Central Bank, Mario Draghi, announced he would do “whatever it takes” to stop this break up happening, unveiling an emergency programme of backstop bond buying by the central bank. This reassured private investor that they would, at least, get their money back and bond yields in countries like Italy and Spain fell back to earth, ending the risk of a destructive debt spiral.

But the latest deadlock in Rome is nevertheless the biggest crisis in the eurozone since Greece last threatened to leave in 2015. And Italy is a much larger economy than Greece. If the third largest country in the bloc exited the euro, it is doubtful the single currency would survive.

Falling bank shares dragged down Europe’s main share markets. At the close the UK’s FTSE 100 fell almost 1.3%, while Germany’s Dax was down 1.5% and France’s Cac 1.3% lower. “It’s a market that is totally in panic”, said a fund manager at Anthilia Capital Partners, who noted “a total lack of confidence in the outlook for Italian public finances”. And the chief economic adviser at Allianz in the US said: “If the political situation in Italy worsens, the longer-term spill overs would be felt in the US via a stronger dollar and lower European growth.”

So whether you look locally or globally its risk on at the moment, and we are it seems to me teetering on the edge of our Scenario 4. This will not be pretty and it will not be quick. I see that slow moving train wreck still grinding down the tracks, with no way out.

The Federal Court has determined ASIC failed to prove Westpac manipulated the bank bill swap rate, but the judge found the bank engaged in unconscionable conduct, via InvestorDaily.

Justice Beach of the Federal Court has handed down a 643-page judgement on a civil court case brought by ASIC that alleged Westpac manipulated the bank bill swap rate (BBSW).

In his judgement, Justice Beach found ASIC has “not made out its case against Westpac” concerning market manipulation or market rigging.

However, he did find that Westpac engaged in unconscionable conduct under s12CC of the ASIC Act on four occasions (6 April 2010, 20 May 2010, 1 and 6 December 2010) “by trading Prime Bank Bills in the Bank Bill Market with the dominant purpose of influencing yields and where BBSW is set”.

Westpac was also found to have contravened paragraphs 912A(1)(a), (c), (ca) and (f) of the Corporations Act, which relate to the obligations of financial services licensees to operate efficiently, honestly and fairly.

ASIC did not make out its case in respect to any of its other claims, said the judgement.

In his summary, Justice Beach said Westpac had failed to take “reasonable steps” to ensure its representatives did not engage in trading in Prime Bank Bills with the “sole or dominant purpose of manipulating the BBSW”.

“Further, in my view Westpac failed to ensure that its traders were adequately trained not to engage in trading with such a sole or dominant purpose,” said the judgement.

“This should have been reinforced and stipulated to them orally and in writing. In those circumstances, Westpac also contravened s 912A(1)(f).”