Misconduct exposed by the banking Royal Commission is the tip of the iceberg, with the catastrophic consequences of Australia’s broken financial sector yet to be revealed, according to a Deakin University corporate law expert.

Deakin Law School’s Professor Gill North, who has a background as a chartered accountant and financial analyst, as well as doctorate in law, said the Royal Commission would not fully address the broader impact of financial misconduct.

“Australians are horrified now by what they’re learning from the Royal Commission, but news on the finance sector is set to get much worse, with likely catastrophic consequences,” Professor North said.

“Systemic risks across the financial sector are already much higher than most people realise, and these risks are being exacerbated by the concentration of the sector, lax lending standards, high levels of household debt, and the heavy reliance of the economy on the health of the residential property market.

“As levels of household debt and financial stress rise, disparities between those who have considerable income, savings and wealth buffers and those who don’t will only become starker.

“The true resilience of the financial institutions, their consumers, and the broader economy will be tested and put under extreme pressure at some point – much of Australia is in for a bumpy and uncomfortable ride.”

Professor North is co-director of the analyst firm Digital Finance Analytics and has worked in senior executive positions at multinational corporations and investment banks in major financial centres including London, Tokyo, New York and Sydney.

She said the Royal Commission was shining a light on the most powerful corporations in Australia, but the investigation so far had been predominantly restricted to the most significant examples of non-compliance with the law by the largest financial institutions.

“The dirty linen of these entities and the practices they’ve gotten away with for many years are finally being effectively challenged,” Professor North said.

“The Commission is expected to have a profound and long-lasting impact on the sector, however the many governance and systemic concerns that flow from the identified misconduct are unlikely to be fully examined and addressed.”

Professor North said the Commission’s recommendations could include changes to consumer lending, while opening the door to future litigation.

“Changes to the consumer credit regimes under the National Consumer Protection Act are inevitable, including the way loan brokers can be remunerated and the processes used by lenders to verify information provided by consumers and intermediaries,” she said.

“The Commission has provided additional information and admissions that corporate regulator ASIC could use in actions against lenders, credit assistance providers, financial advisers, and directors.

“But future litigation in this space won’t be limited to regulators – actions by consumers who were issued loans or provided financial advice in breach of the law are likely to accelerate, and become a flood of litigation as the circumstances in Australia deteriorate and household financial stress levels climb to new records.”

From Guest Blogger Alex Petrovic – currently working as finance content contributor.

Australia’s gig economy has been on the rise for a number of years, and new data by the Australian Bureau of Statistics (ABS) reveals that the number of workers considered to be part of this economy is still growing. From Deliveroo to Uber and Upwork, people are increasingly turning to jobs that offer a better work-life balance.

But what does this mean for gig economy workers seeking a home loan? With more Australians becoming self-employed, demand from these borrowers is set to increase, and lenders will need to adapt to meet their needs.

The rise of the gig economy

Gig economy work is growing around the world, not just in Australia. With the spread of mobile internet connectivity and platform websites such as 99designs, Airtasker, and Freelancer, people can now work from anywhere they like, whether that’s at home or from their local café.

It’s an attractive option for many people who are seeking a better work-life balance, yet doing short spells of contract work or completing work for a range of employers can make things more challenging when it comes to securing a home loan.

The difficulty of securing a home loan

Following the global financial crisis, self-employed borrowers faced even more significant challenges securing a mortgage. When you’re your own boss, income isn’t always steady, and without a history of up to three years’ worth of accounts or payslips, it can be far more difficult to obtain verification.

Banks became far less willing to lend to those they regarded as being riskier than your more traditional borrower with a standard income. For a potential borrower with enough savings and income to pay their deposit and keep up with repayments, being refused merely for having a non-standard income can be incredibly frustrating.

While self-employment has been on the rise for some time, securing a home loan is still proving difficult for many Australians. In fact, a recent survey revealed that one in five have been turned down for a loan, and of these, 26% were declined because they were self-employed or working part-time.

What is perhaps more worrying, is that more than half of those who were declined for a loan at a bank were not aware that other options are available. Non-bank lenders can help sole traders when it comes to securing a mortgage. By assessing applications on a case-by-case basis and having a more flexible approach to the type of documentation they can use to conduct their lending assessments, they may be able to help where other lenders cannot.

This flexibility isn’t just about giving borrowers other options; using documentation such as accountant letters, bank statements, and business activity statements can actually provide lenders with a more current picture than some traditional forms of documentation might.

While some may have concerns that these types of lenders will charge much higher interest rates, what you’ll find is that they actually offer very competitive rates. For example, the lowest interest rate from Commonwealth bank is 3.79%, although rates do vary depending on the loan to valuation ratio (LVR).

Time for a change

What the larger financial institutions have done is essentially create a void by only focusing on one type of customer. Old style policies must be adapted to suit newer generations and those working in the gig economy.

Banks should follow the lead of non-bank lenders, who offer a more flexible approach and look at the whole picture of an individual’s circumstance to gain a better understanding of potential borrowers. There is no need to loosen lending criteria; it’s about staying current and helping this underserviced market find a solution that meets their needs.

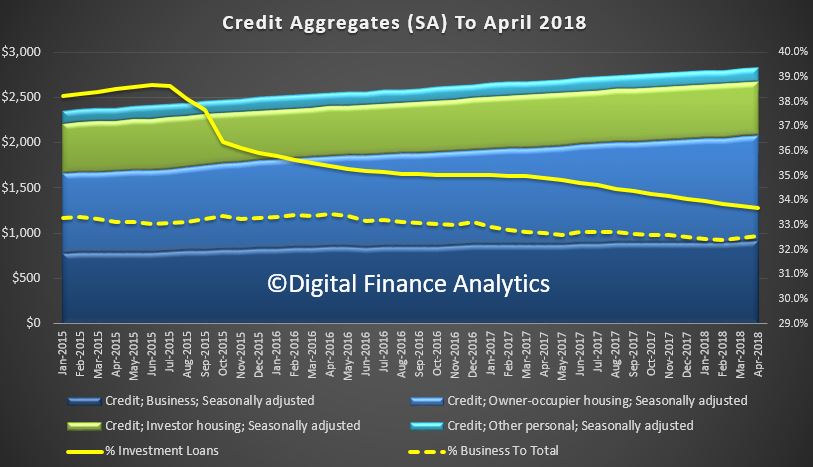

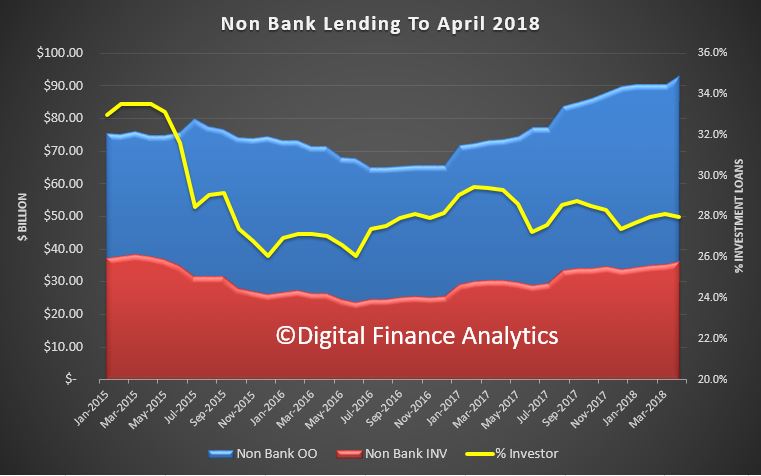

The RBA has released their credit aggregates to April 2018. Total mortgage lending rose $7.2 billion to $1.76 trillion, another record. Within that, owner occupied loans rose $6.4 billion up 0.55%, and investment loans rose 0.14% up $800 million. Personal credit fell 0.3%, down $500 million and business lending rose $6.3 billion, up 0.69%.

Business lending was 32.5% of all lending, the same as last month, and investment mortgage lending was 33.7%, slightly down on last month, as lending restrictions tighten.

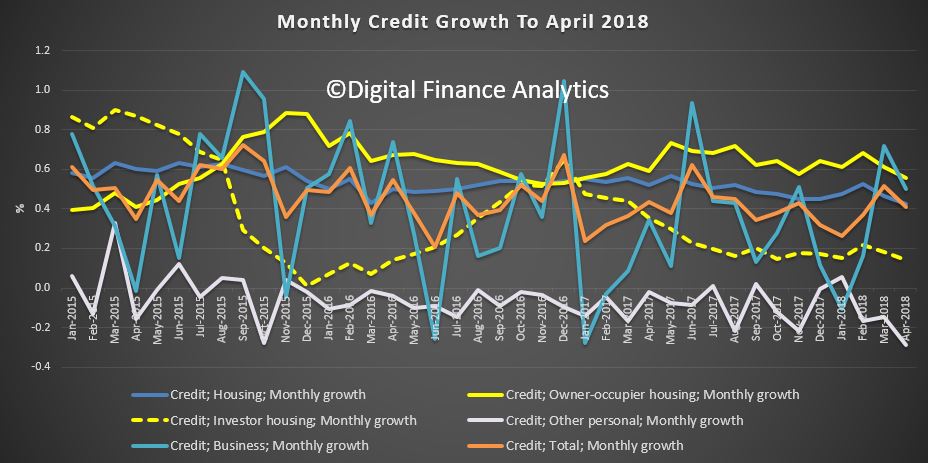

The monthly trends are noisy as normal, although the fall in investor property loans is visible and owner occupied lending is easing.

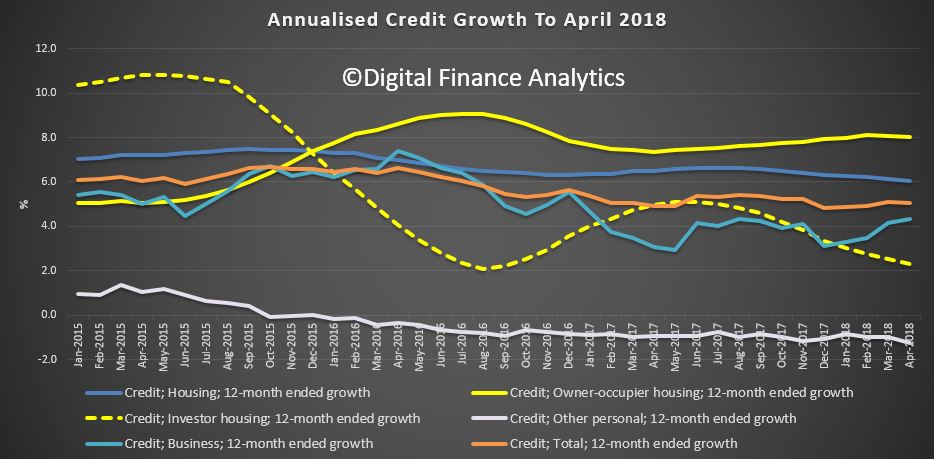

But the annualised stats show owner occupied lending still running at 8%, while business lending is around 4% annualised, investment lending down to 2.3% and personal credit down 0.3%. On this basis, household debt is still rising.

One interesting piece of analysis we completed is the comparison between the RBA data which is of the whole of the market and the APRA data which is bank lending only.

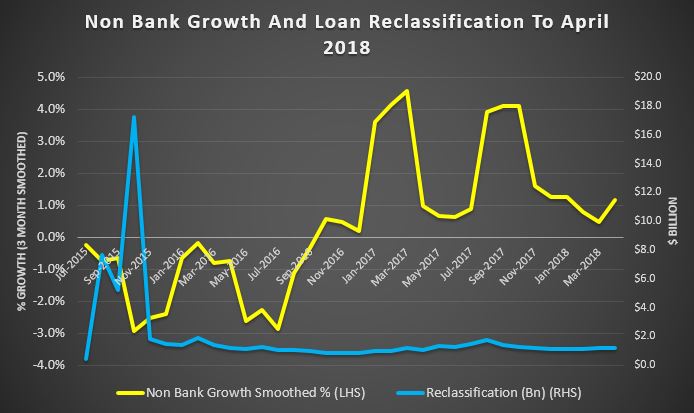

Now this is tricky, as the non-bank data is up to three months behind, and only covers about 70% of the market, but we can get an indication of the relative momentum between the banks and non banks.

We see that non-bank lending has indeed been growing, since late 2016. The proportion of loans for property investors is around 28%, lower than from the banks. Back in 2015, the non-bank investor split was around 34%.

The percentage growth from the non-bank sector appears stronger than the banks. Across all portfolios, loan reclassification is still running at a little over $1 billion each month.

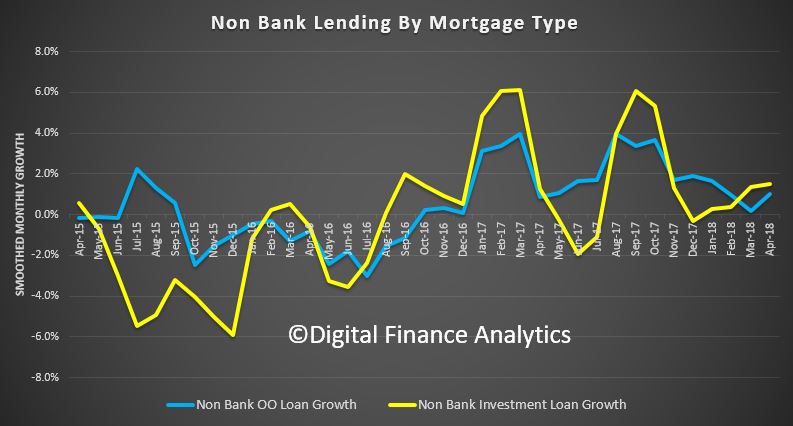

Finally if we look at the relative growth of owner occupied and investment loans in the non-bank sector we see stronger investment lending in the past couple of months. Bank investment property lending actually fell on April according to APRA stats.

As expected, as banks throttle back their lending, the non-banks are filling some of the void – but of course the supervision of the non-banks is a work in progress, with APRA superficially responsible but perhaps not actively so.

We would expect better and more current non-bank reporting at the very least APRA, take note!

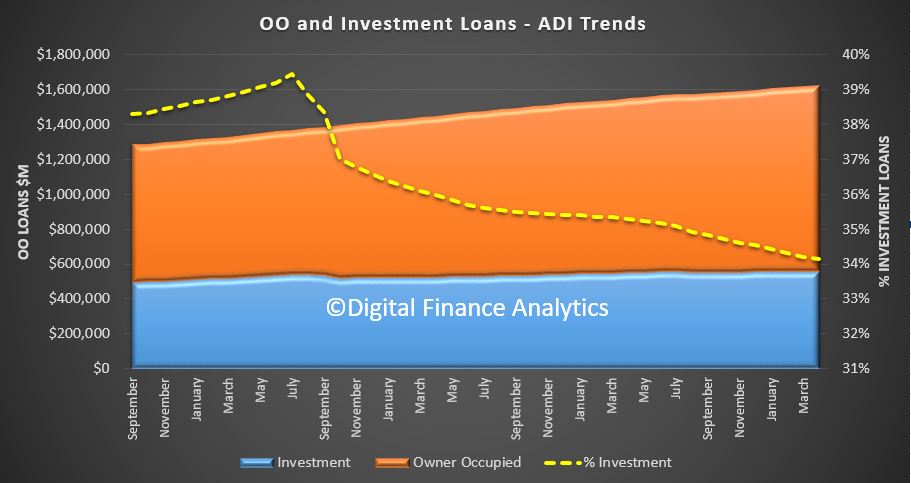

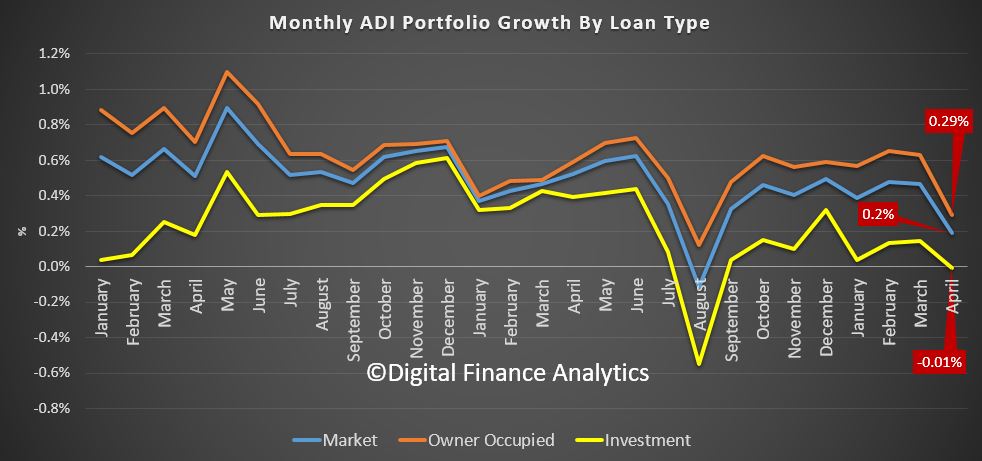

APRA has released their monthly banking statistics for ADI’s to April 2018. And now we are really seeing the tighter lending standards biting. In fact, Westpac apart, all the majors have reduced their investor property lending.

APRA reports for each lender the net total balance outstanding at the end of each month and by looking at the trends we see the net of loan roll offs and new loans. This is important, as we will see.

At the aggregate level, total lending for mortgages from ADI’s rose 0.2% in the month, up $3.0 billion to $1.62 trillion. Within that owner occupied loans grew by 0.29% or $3.1 billion to $1.07 trillion while investment loans fell slightly, down 0.01% of $42 million. As a result the relative share of investment loans fell to 34.14%.

The trend movement highlights the significance of the fall (the August 2017 point is an outlier thanks to reclassification), this is the weakest result for years. At an aggregate level, over 12 months this would translate to a rise of just 2.3%, significantly down from the 5-6% range of recent months.

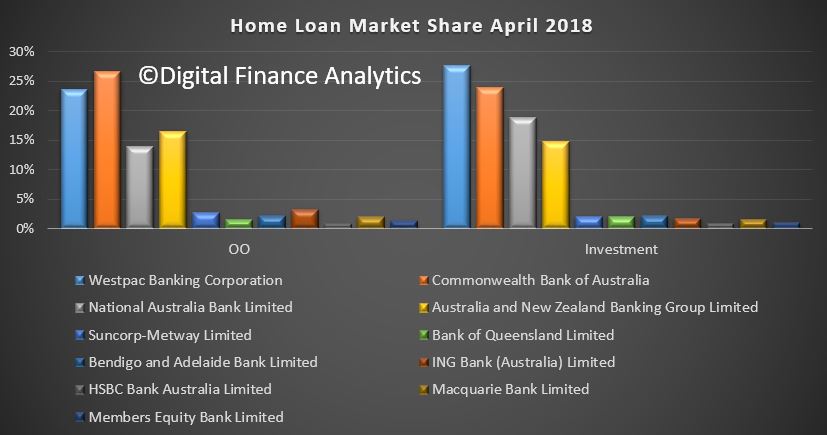

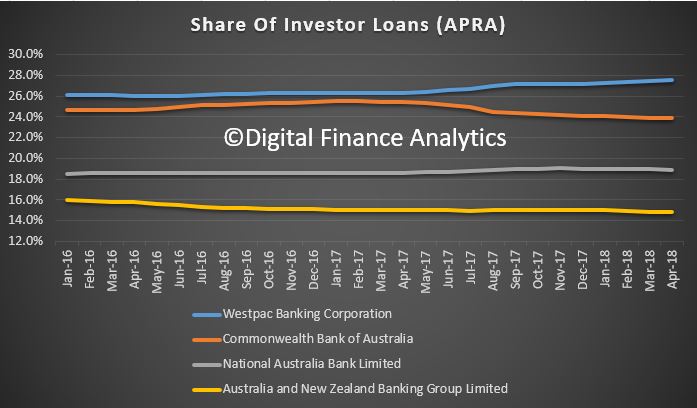

Turning to the individual market shares, at the aggregate level there was little change, other than Westpac’s share of investor loans grew to 27.6%, up from 26.1% in January 2016

Here is the trends from the big four. Westpac has continued to increase share of investor loans. CBA has fallen away the most significantly.

There has been almost no shift in owner occupied loan shares.

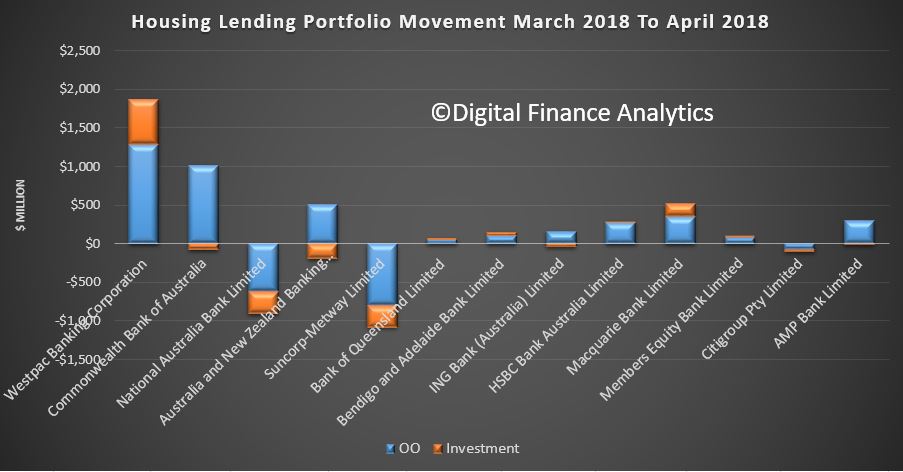

The monthly changes in value tell the story, with Westpac and Macquarie growing the value of their portfolios, across both owner occupied and investment lending. We see falls in net investor lending elsewhere.

We conclude that Westpac executed a different strategy in terms of mortgage origination compared with its competitors. They may be offering selective discounts to attract particular types of business, or they may have different lending standards, or both.

It is quite possible we will see other lenders trying to compete relative to Westpac in the investment loan domain ahead, as lending growth is needed to sustain profitability. But demand is also falling, so we expect lending momentum to continue to weaken, with the consequential impact on home prices and bank profitability. We are entering credit crunch territory!

When I last addressed this Committee, I outlined some of the many ways APRA is accountable to both the Parliament and the Australian people. These measures are crucial for APRA to maintain the trust of industry and the public as we aim to fulfil our mandate as a prudential regulator, promoting financial safety and thereby protecting the interests of bank depositors, insurance policyholders and superannuation members.

The core of APRA’s mission is safety and soundness. Clearly, some of the revelations emerging from the Royal Commission have been disturbing and go to the heart of whether financial institutions treat their customers fairly. However, while institutions have a great deal of work to do to restore trust, I want to emphasise that Australians can be reassured that the industry is financially sound, and that the financial system is stable. That reflects considerable policy reform and hands-on supervision, over a long period of time, designed to build strength and resilience. We don’t know when the next period of adversity will arrive or what will trigger it, but when it does arrive we need to have done what we could to strengthen the financial system so that it can continue to provide its essential services to the Australian community when they are needed most.

The importance of accountability has been one of our key themes this year, and was front and centre with the release in April of our review of executive remuneration practices in large financial institutions. Incentives and accountability can play an important role in driving positive outcomes such as growth, innovation and productivity, and also in deterring behaviours or decisions that produce poor risk-taking and damaging results. Our review found that while policies and processes existed within institutions to align remuneration with sound risk outcomes, their practical application was often weak. We have indicated that we are minded to strengthen the prudential framework to give better effect to the principles we want to see followed – less rewards based on narrow and mechanical shareholder metrics, and greater exercise of Board discretion to judge senior executive performance more holistically. But we have also urged institutions to push ahead with their own improvements, notwithstanding some investor opposition, in light of the long-term commercial benefits that can flow from better remuneration practices.

A lack of accountability for poor outcomes was a theme that also emerged in the Final Report of the Prudential Inquiry into the Commonwealth Bank of Australia, which was released earlier this month. The Report is clear and comprehensive, and provides a strong message – not just to CBA but to the entire financial services industry – about the importance of cultivating a robust risk culture, especially when it comes to non-financial risks. We are keen that the Report will be seen not just a road map for CBA, but a useful guide for all institutions in relation to strengthening governance, culture and accountability.

Residential mortgage lending is another area where APRA has been lifting industry standards. Although there remains more to do before we are ready to significantly dial back our supervisory intensity, there has been a lift in industry lending practices. As a result, last month we announced we would remove the 10 per cent investor growth benchmark for those lenders who could provide a range of assurances as to the quality of their lending standards and practices now and into the future.

Superannuation is an area where APRA consistently emphasises the need for trustees, regardless of size or ownership structure, to go beyond compliance with minimum regulatory requirements and aim to deliver the best possible outcomes for members. In this vein, we have just released the results of two thematic reviews of superannuation licensees; on board governance and the management of related parties. Both reviews noted improvements in industry practices in recent years, but also found more work was needed to address some longstanding weaknesses, including finding ways to bring fresh ideas, perspectives and skills onto trustee boards. Our post-implementation review of 2013’s Stronger Super reforms, launched last week, should also provide us additional insights on how the prudential framework is performing, and whether any adjustments would help to better achieve our objectives. Many of the findings in the Productivity Commission report into superannuation released this week are consistent with APRA’s approach to supervising RSE licensees. In particular, they align with APRA’s focus on enhancing the delivery of member outcomes through our engagement with trustees with “outlier” underperforming funds and products.

Technology is rapidly changing the way financial institutions operate. In all likelihood, the financial system will look very different in five years’ time relative to the way it looks today. Much of that change will bring benefits to the community, in the form of new competitors, products and ways of access. But it will also bring risks, and the accelerating threat of cyber-attacks to regulated entities has prompted APRA to recently propose its first prudential standard on information security. Industry consultation is ongoing, but we hope to implement the new cross-industry standard from 1 July next year. This is an issue which is only going to grow in importance.

Continuing to look ahead, APRA’s preparations are well advanced for the commencement of the Banking Executive Accountability Regime (BEAR), which will begin in just over a month. The BEAR largely strengthens APRA’s existing powers to identify and address the prudential risks arising from poor governance, weak culture, or ineffective risk management. However, I have made the point previously that while important, the BEAR alone will not remedy perceived weakness in financial sector accountability, and we have encouraged all regulated entities – not just ADIs – to use the new regime as a trigger to genuinely improve systems of governance, responsibility and accountability.

Finally, APRA is continuing to provide relevant information to the Royal Commission to help it in its inquiries. In addition, APRA and the Australian financial system more broadly, will be subject to intensive scrutiny from the International Monetary Fund in the weeks ahead as part of its 2018 Financial Sector Assessment Program (FSAP). The FSAP will examine in quite some detail financial sector vulnerabilities and the quality of regulatory oversight arrangements in Australia. As ever, APRA will fully cooperate with our international reviewers, and look forward to their report card, including any recommendations on how we could perform our role more effectively in the future.

With those opening remarks, we would now be happy to answer the Committee’s questions.

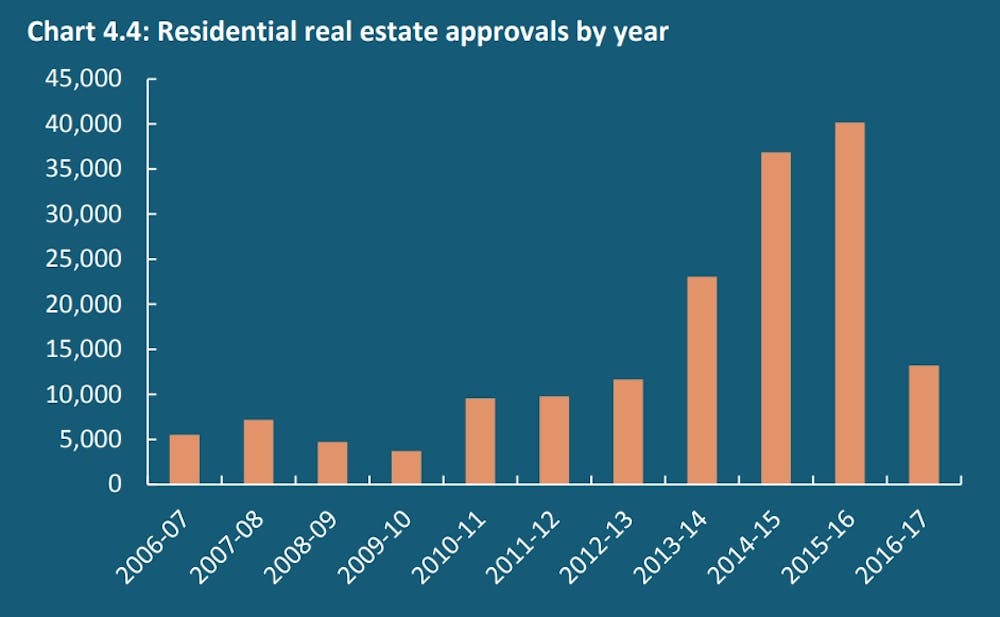

Australia’s Foreign Investment Review Board (FIRB) reported this week that foreign residential real estate approvals dropped significantly in the 2016-17 period.

Whereas 2015-16 saw 40,149 approvals granted, totalling A$72.4 billion, the figure for the following year was just 13,198 approvals, totalling A$25.2 billion. On these numbers, the foreign property investment boom looks to be over.

This is bad news for the property and financial industries, who are already feeling the pressure of weak household income growth, tighter lending restrictions on local borrowers, and a slowing in housing market activity in key Australian cities.

FIRB suggests that declining demand from China is a factor in the overall decline in overseas approvals. Chinese demand may have been weakened by a range of factors, including the new FIRB application fees, Chinese overseas direct investment capital controls, and the changing global economy.

But if the cycle is moving from boom towards bust, we have learned several things along the way.

Lesson 1: We still need more data

In 2014 the House of Representatives Standing Committee on Economics undertook an inquiry into foreign investment in residential real estate. It acknowledged the growing public disquiet about the level of this foreign investment, adding that:

…there is no accurate or timely data that tracks foreign investment in residential real estate. No one really knows how much foreign investment there is in residential real estate, nor where that investment comes from.

Four years on, FIRB is still flagging the limitations of data collection and analysis. Without fine-grained data, it’s hard to forecast how much, if at all, the injection of foreign capital can push up local house prices.

The latest figures come with a caveat. The approvals data represent potential investment, rather than actual investment. There are key differences between the two. Potential investors might, for example, seek approval for multiple properties while only intending to buy one of them.

We need the government to collect more extensive and detailed data on individual foreign real estate investment, and make it publicly available. This needs to cover more than approvals data at the city level, but data on investment levels in neighbourhoods or even individual housing developments.

Lesson 2: People on the property ladder are less hostile to foreign buyers

Data from Sydney reveals widespread concern about foreign investment. Almost 56% of Sydneysiders believed foreign investors should not be allowed to buy residential real estate in Sydney. Only 17% of respondents in our study thought the government’s regulation of foreign housing investment was effective.

Just over half of Sydneysiders say they would not want Chinese investors buying properties in their suburb. And 78% thought foreign investment was driving up housing prices in greater Sydney.

Yet those who have real estate investments were more likely to support foreign investment than those who don’t. This suggests that Sydneysiders with equity in the housing market, such as homeowners or investors, might view foreign buyers pushing up housing values as positive. And they might fear that the new decline in foreign investment might depress their assets.

Lesson 3: Housing is built with specific buyers in mind

When Chinese real estate investment started to rise significantly in 2013-14, property developers scrambled to model this new emerging market. The real estate media rushed to map out where Chinese investors were keenest to buy, and how best to design and market property developments to this new foreign client base.

The growing numbers of Chinese and Indian migrants in Australia means property investors need to consider the cultural sensitivity of the residential property they purchase to ensure they maximise the resell value.

Between 2013 and 2017, property developers, both local and foreign, regularly contacted me to ask if I had any up-to-date research on foreign investors’ consumer preferences and market forecasts. I did not. But there was no shortage of advice out there, covering everything from feng shui-informed housing design to the key needs of foreign university students.

Some global real estate agents suggested to their clients that they could buy an Australian home to accommodate their child while they were studying at an Australian university, and then use the capital gain from the property sale to pay back the tuition fees.

Many property developers were formulating medium- to long-term development pipelines that included the foreign capital and consumer preferences of foreign investors. It is unclear, now, whether much of this housing stock will ever be built. If it is, will it suit the changing future needs of our cities, or address our ongoing housing affordability problems?

In other words, what sorts of properties will be left as the legacy of the recent foreign real estate investment mania?

Lesson 4: Racialised housing debates are simplistic and harmful

We need to take care not to conflate domestic Chinese-Australian buyers with international Chinese investors. Much of the media coverage of the new report features stereotyped images of Asian families buying an Australian home. But given the foreign investment rules and logistics involved, these pictures are far more likely to depict Chinese-Australians than foreigners.

Understanding the long-term migration and education plans of the investors is important too. Different investor groups will interact with the city in different ways, and their impact on society can be vastly different too. For example, super-rich absentee investors will have a different impact on neighbourhood life compared with that of middle-class migrants or international students.

If the federal government wants to court foreign investment, then better education about the possible risks and benefits of individual foreign real estate investment is needed. Our research suggests that the government’s pro-foreign investment stance must be accompanied with strategies to protect intercultural community relations in Australia.

…fluctuation in property prices recorded for Sydney have been caused by the forces linking the city to the Australian economy and to the remainder of the world.

Daly charted the influx of foreign people and capital into Sydney between 1850 until 1981, as wealth was channelled through the financial services sector and into urban real estate. Along the way, he observed that one “group to attract the abuse of the general population were the Chinese”.

Domestic and foreign real estate investment have long been connected to the financial services industries, and the built environment is central to creating and storing surplus capital. Australian cities continue to be heavily influenced by global money today.

A key lesson is that domestic and foreign housing booms, bubbles and busts are thus better understood as cycles within our housing and financial system, rather than as a set of short-term ruptures to this system.

We need to think about the collective impacts of domestic and foreign real estate investment over the long-term in our cities if we are serious about addressing housing inequality.

Author: Dallas Rogers, Program Director, Master of Urbanism. School of Architecture, Design and Planning, University of Sydney

At first blush the news at home and abroad appears to be steering us towards our most risky – scenario 4 outcome, where global financial markets are disrupted and home prices fall by 20-40 percent or more as confidence wains.

Some would call this GFC 2.0. So let’s looks at the evidence.

In Australia, as we predicted, a massive class action lawsuit is being planned on behalf of “Australian bank customers that have entered into mortgage finance agreements with banks since 2012”.

Law firm Chamberlains has been appointed to act in the planned class action lawsuit, which has been instructed by Roger Donald Brown of MortgageDeception.com in the action that aims to represent various Australian bank customers that are “incurring financial losses as a result of entering into mortgage loan contracts with banks since 2012”.

As the AFR put it – Lawyers’ representing up to 300,000 litigants are planning an $80 billion action against mortgage lenders, mortgage brokers and financial regulators in a class action that would dwarf previous actions. Roger Brown, a former Lloyds of London insurance broker, said he already has about 200,000 borrowers ready to join the action and has $75 million backing from UK and European investors. There has been a scam, he said about mortgage lending to Australian property buyers. “But the train has hit the buffers and there needs to be recompense.

As we discussed before, if loans made were “unsuitable” as defined by the credit legislation, there is potential recourse. This could be a significant risk to the major players if it gains momentum. And more will likely join up if home prices fall further and mortgage repayments get more difficult. But we think individuals must take some responsibility too!

Next, we now see a number of the major media outlets starting to blame the Royal Commission for the falls in home prices, tighter lending standards and even damage to the broader economy. Talk about shoot the messenger. The fact is we have had years of poor lending practice, and poor regulation. But the industry and regulators kept stumn preferring to enjoy the fruits of over generous lending. The Royal Commission is doing a great job of exposing what has been going on. In fact, the reaction appears to be that what had been hidden is now in the sunshine, and it is true the sunlight is the best disinfectant. Structural malpractice is being exposed, some of which may be illegal, and some of which certainly falls below community expectations. But let’s be clear, it’s the poor behaviour of the banks and the regulators which have placed us in this difficult position. Hoping bad lending remans hidden is a crazy path to resolution. At least if the issues are in the open they stand a chance of being addressed.

But it is also true that just a lax lending allowed households to get bigger mortgages than they should, and bid home prices higher, to be benefit of the banks, and the GDP out-turn, the reverse is also true. Tighter lending will lead to less credit being available, which in turn will translate to lower home prices, and less book growth for the banks. But do not lay this at the door of the Royal Commission. They are actually doing Australia a great service, in a most professional manner.

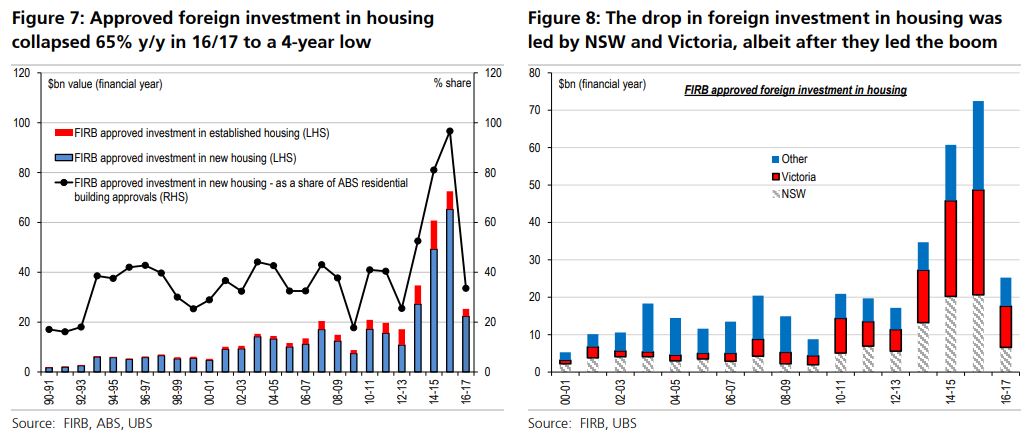

But that does not stop the rot. UBS came out today with an update saying that the housing market is slowing, with house prices falling and credit conditions tightening. Given the number of headwinds the market is facing; many investors are now questioning whether the housing correction could become disorderly. We expect credit growth to slow sharply and believe the risk of a Credit Crunch is rising.

They walk through the main areas, including tighter lending, interest only loans and foreign buyers. Specifically, they highlight that approved foreign investment in housing is down -65%. The Foreign Investment Review Board just released data for 16/17. The value of approvals to buy residential housing collapsed 65% y/y to $25bn in 16/17, the lowest level since 12/13, and mostly reversing the prior ‘super boom’. The fall was across both new (-66% to $22bn) and established housing (-59% to $3bn) – led by total falls in NSW (-66% to $7bn) and Victoria (-61% to $11bn.

They say that the collapse in 16/17 may be overstated because of the introduction of application fees in Dec-15 – meaning the fall in transactions is less pronounced. But, there is still likely to have been a drop in transactions, reflecting more structural factors including – the lift in taxes on foreigners; domestic lenders tightening standards for foreign buyers (effectively no longer lending against foreign sources of income or collateral); as well as tighter capital controls especially from China.

Their base case is for a small fall in prices ahead, and assumes house prices fall by 5%+ over the coming year and that bad and doubtful debts increase only modestly given the current very benign credit environment. but they also talk about a downside scenario which reflects a more disorderly correction in the housing market (ie a Credit Crunch) and could result in approximately 40% reduction in major bank share prices. This is likely due to credit growth falling more substantially, by ~2-3% compound and credit impairment charges rising significantly as the credit cycle turns. This scenario would put pressure on bank NIMs. Litigation risk from class actions for mortgage misselling is also a tail risk. Dividends would need to be cut in this scenario. Given the leverage in the banking system, accurately predicting the extent of a downturn is very difficult, as was seen in 2008.

And the reason they still hold to their milder view is the expectation that the Government will step in to assist, and slow the implementation of recommendations from the Royal Commission. To quote Scott Morrison on 2GB radio on 23d March.

If banks stop lending, then what do people think that is going to mean for people starting businesses or getting loans or getting jobs or all of this. In the budget papers, the Treasury have actually highlighted this as a bit of a risk with the process we are going through. We have got to be very careful. These stories are heartbreaking, I agree, but we have to be also very cautious about, well, how do we respond to that. What is the right reaction to that? Is it to just throw more regulation there which basically constipates the banking and financial industry which means that people can’t start businesses and people can’t get jobs, people can’t get home loans. Or do we want to move to a smarter way of how this is all done and I think in the era of financial technology in particular there are some real opportunities there. We are going to continue to listen and carefully respect the royal commission, not prejudge the findings, but be very careful about any responses that are made because this can determine how strong an economy we live in over the next ten years and whether people get jobs and start businesses.

But in essence, expect some unnatural acts from the Government to try to keep the bubble going a little longer. All bets are off the other side of the election.

And the third risk, and the one which takes us closest to GFC 2.0 is what is happening in Italy. I am not going to go back over the history, but after months of wrangling, Italy’s political crisis has a hit an impasse, with new elections now increasingly likely. The country faces an institutional crisis without precedent in the history of the Italian republic. Its implications extend well beyond Italy, to the European Union as a whole.

Since an election on March 4, there have been endless vain attempts to form a government – with the likely outcome changing every 24 hours. By mid-May, the Five Star Movement (M5S) and the League, both populist parties, had come together to draft a programme for government featuring tax cuts and spending plans. But it sent shivers down the spines of those contemplating Italy’s public debt – running at over 130% of GDP – and threatened the stability of the eurozone.

The appointment of Carlo Cottarelli, a former official from the International Monetary Fund, as prime minister on May 28 was merely a stop-gap measure until fresh elections in the autumn. His government will almost certainly fail to win the necessary vote of confidence required of all incoming governments upon taking office. This means that it will be unable to undertake any legislative initiatives that go beyond day-to-day administration.

ITALY’S president, Sergio Mattarella had originally planned to put a former IMF economist, Carlo Cottarelli, at the head of a government of technocrats, tasked with steering the country back to the polls after the summer. But Mr Mattarella was reportedly considering changing tack after meeting Mr Cottarelli on May 29th amid growing evidence of support in parliament for an earlier vote. Not a single big party has declared its readiness to back Mr Cottarelli’s proposed administration in a necessary vote of confidence.

So the president is expected to decide on May 30th whether to call a snap election as early as July in an effort to resolve a rapidly deepening political and economic crisis that has sent tremors through global financial markets. There was also concern that the populist parties could win a bigger parliamentary majority in the new election, creating a bigger risk for the future of the eurozone.

In a sign of investors’ concern, the yield gap between Italian and German benchmark government bonds soared from 190 basis points on May 28th to more than 300. The governor of the Bank of Italy, Ignazio Visco, warned his compatriots not to “forget that we are only ever a few steps away from the very serious risk of losing the irreplaceable asset of trust.”

The yield on two-year debt has risen from below zero to close to 2% and Italy’s 10-year bond yields, which is a measure of the country’s sovereign borrowing costs, breached 3 per cent on Tuesday, the highest in four years. At the start of the month they were just 1.8 per cent. Italy’s sovereign debt pile of €2.3 trillion is the largest in the eurozone

The Italian stock market was also down 3 per cent on Tuesday, and has lost around 13 per cent of its value this month.

But these movements need to be put in some context. The Italian stock market is still only back to its levels of last July, after experiencing a strong bull run since later 2016.

In 2011 and 2012 Italian bond breached 7 per cent and threatened a fiscal crisis for the government in Rome. Yields are still some distance from those extreme distress levels.

George Soros was quoted in the FT:

The EU is in an existential crisis. Everything that could go wrong has gone wrong,” he said. To escape the crisis, “it needs to reinvent itself.” Mr Soros said tackling the European migration crisis “may be the best place to start,” but stressed the importance of not forcing European countries to accept set quotas of refugees. He said the Dublin regulation — which decides which nation is responsible for processing a refugee’s asylum status, largely based on which country the individual first enters — had put an “unfair burden” on Italy and other Mediterranean countries, “with disastrous political implications.” While austerity policies appeared initially to have been working, said Mr Soros, the “addiction to austerity” had harmed the euro and was now worsening the European crisis. US president Donald Trump’s exit from the nuclear arms deal with Iran and the uncertainty over tariffs that threaten transatlantic trade will harm European economies, particularly Germany’s, he said, while a strong dollar was prompting “flight” from emerging market economies. “We may be heading for another major financial crisis,” he said. Meanwhile, years of austerity policies had led working people to feel “excluded and ignored,” sentiment that had been exploited by populist and nationalistic politicians, said Mr Soros. He called for greater emphasis on grassroots organisations to meaningfully engage with citizens.

To play devil’s advocate, if Italy were to leave the Eurozone, the Lira would drop, hard. Most probably Italy would default on debt, and this would hit the Eurozone banks hard, especially those in German and French banks will be hit hard and they are saddled with about half the outstanding debt. Just like in the GFC a decade back, global counter-party bank risk will rise, and this time sovereign are involved, so it may go higher. The US Dollar will run hot, and there will be a flight to quality, tightening the capital markets, lifting rates and causing global stocks and commodities to crash, possibly a recession will follow.

In Australia, the dollar would slide significantly, fuelling stock market falls and a further drop in home prices, leading to higher levels of default, and recession, despite the Reserve Bank cutting rates and even trying QE.

Now the financial situation in Italy at the moment, a far cry from the height of the eurozone crisis in 2012, when it really did look possible that weaker member states would be imminently forced to default and the single currency would collapse. Then, that situation was finally defused when the head of the European Central Bank, Mario Draghi, announced he would do “whatever it takes” to stop this break up happening, unveiling an emergency programme of backstop bond buying by the central bank. This reassured private investor that they would, at least, get their money back and bond yields in countries like Italy and Spain fell back to earth, ending the risk of a destructive debt spiral.

But the latest deadlock in Rome is nevertheless the biggest crisis in the eurozone since Greece last threatened to leave in 2015. And Italy is a much larger economy than Greece. If the third largest country in the bloc exited the euro, it is doubtful the single currency would survive.

Falling bank shares dragged down Europe’s main share markets. At the close the UK’s FTSE 100 fell almost 1.3%, while Germany’s Dax was down 1.5% and France’s Cac 1.3% lower. “It’s a market that is totally in panic”, said a fund manager at Anthilia Capital Partners, who noted “a total lack of confidence in the outlook for Italian public finances”. And the chief economic adviser at Allianz in the US said: “If the political situation in Italy worsens, the longer-term spill overs would be felt in the US via a stronger dollar and lower European growth.”

So whether you look locally or globally its risk on at the moment, and we are it seems to me teetering on the edge of our Scenario 4. This will not be pretty and it will not be quick. I see that slow moving train wreck still grinding down the tracks, with no way out.

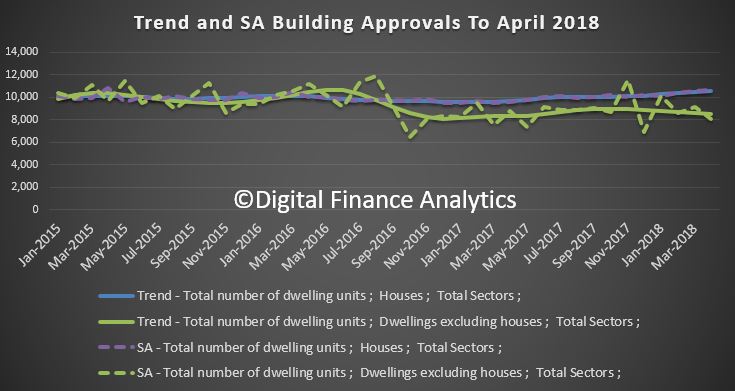

The ABS reports that the number of dwellings approved in Australia fell by 0.1 per cent in April 2018 in trend terms. We see a fall in units, somewhat offset by a rise in houses approved. The seasonally adjusted numbers show a more significant drop.

“The total dwellings series has been relatively stable for the past eight months, with around 19,000 dwellings approved per month,” said Justin Lokhorst, Director of Construction Statistics at the ABS. “The strength in approvals for houses is being offset by weakness in semi-detached and attached dwelling approvals.”

Among the states and territories, dwelling approvals fell in April in Tasmania (3.7 per cent), Victoria (2.3 per cent) and Western Australia (2.2 per cent) in trend terms.

Dwelling approvals rose in trend terms in the Australian Capital Territory (14.8 per cent), the Northern Territory (6.7 per cent), South Australia (1.7 per cent), New South Wales (0.9 per cent) and Queensland (0.7 per cent).

In trend terms, approvals for private sector houses rose 0.9 per cent in April. Private sector house approvals rose in Queensland (1.6 per cent), Victoria (1.5 per cent) and New South Wales (0.6 per cent), but fell in Western Australia (0.9 per cent) and South Australia (0.4 per cent).

In seasonally adjusted terms, total dwellings fell by 5.0 per cent in April, driven by a 11.5 per cent decrease in private sector dwellings excluding houses. Private sector houses rose 0.1 per cent in seasonally adjusted terms.

The value of total building approved fell 0.7 per cent in April, in trend terms, and has fallen for six months. The value of residential building fell 0.5 per cent while non-residential building fell 1.0 per cent.

The HIA managed to put a positive spin on the results saying “Detached House Approvals Strongest in 15 Years”.

The performance of the detached house building market is remarkable. The volume of house approvals during the three months to April was 9.9 per cent higher than a year ago – a time when it was already elevated,” said Shane Garrett, HIA’s Senior Economist.

Strong demand for new houses is being sustained by healthy rates of population growth – itself a product of robust labour markets in Australia’s largest cities. While it’s a virtuous circle for detached house building at the moment, there are risks on the horizon.

As we predicted, a massive class action lawsuit is being planned on behalf of “Australian bank customers that have entered into mortgage finance agreements with banks since 2012”.

If loans made were “unsuitable” as defined by the legislation, there is potential recourse. This could be a significant risk to the major players if it gains momentum. But we think individuals must take some responsibility too!

As the AFR put it –

Lawyers’ representing up to 300,000 litigants are planning an $80 billion action against mortgage lenders, mortgage brokers and financial regulators in a class action that would dwarf previous actions.

…Roger Brown, a former Lloyds of London insurance broker, said he already has about 200,000 borrowers ready to join the action and has $75 million backing from UK and European investors.

“There has been a scam,” he said about mortgage lending to Australian property buyers. “But the train has hit the buffers and there needs to be recompense,” he said.

Law firm Chamberlains has been appointed to act in the planned class action lawsuit, which has been instructed by Roger Donald Brown of MortgageDeception.com in the action that aims to represent various Australian bank customers that are “incurring financial losses as a result of entering into mortgage loan contracts with banks since 2012”.

The law firm is currently calling on bank customers to join the class action, led by Stipe Vuleta, if they have “incurred financial losses due to irresponsible lending practices”.

The MortgageDeception site says:

Those who have entered into loans with banks to purchase residential properties since 2011 are about to encounter difficulties. Since 1995, banks in the United Kingdom, Ireland, Australia and New Zealand have been making massive and obscene profits from providing finance to property purchasers. These banks have cared little about the lending practices adopted by them, and reckless lending has brought about huge and unsustainable increases in property prices.

These lending practices are now leading to problems for both intending buyers and existing owners of property.

We believe that the banking industry and its regulators have intentionally turned a blind eye to the irresponsible lending that has been taking place.”

For Australian bank customers that have entered into mortgage finance agreements with banks since 2012, we have appointed the leading Canberra-based law firm of Chamberlains, www.chamberlains.com.au, to act in the planned class action lawsuit. The partner in charge is Mr Stipe Vuleta.

The New Zealand Reserve Bank has issued their latest financial stability report. They say that New Zealand’s financial system remains sound. Household debt is firmly in the frame as the biggest potential risk!

The banking system holds sufficient capital and liquidity buffers, guided by our prudential regulatory requirements. These buffers reduce New Zealand banks’ exposure to adverse shocks.An ongoing driver of financial soundness is the conduct and culture of banks and insurance companies. These features are being jointly reviewed by the Financial Markets Authority and ourselves, and we will report our findings over coming months. The financial system vulnerabilities are much the same as we discussed in our previous Financial Stability Report.

Household mortgage debt remains high. However, financial risk has lessened with both lending and house price growth slowing in the last 12 months – in part due to our imposition of loan-to-value (LVR) ratio restrictions. This more subdued lending growth needs to be further sustained before we gain sufficient confidence to again ease the LVR restrictions.

However, the banks says the high level and concentration of household sector debt in New Zealand is the largest single vulnerability of the financial system. Some households are vulnerable to developments that reduce their debt servicing capacity, such as higher interest rates or a change in financial circumstances. Households with severe debt servicing problems could default on their loans, creating losses for lenders. If debt servicing problems were widespread, weaker consumption and investment could reduce incomes and contribute to an economic downturn. This could threaten financial stability by causing households and businesses to default, and by reducing the value of assets against which banks have lent, such as houses.

The high level and concentration of household sector debt in New Zealand is the largest single vulnerability of the financial system. Some households are vulnerable to developments that reduce their debt servicing capacity, such as higher interest rates or a change in financial circumstances. Households with severe debt servicing problems could default on their loans, creating losses for lenders. If debt servicing problems were widespread, weaker consumption and investment could reduce incomes and contribute to an economic downturn. This could threaten financial stability by causing households and businesses to default, and by reducing the value of assets against which banks have lent, such as houses.

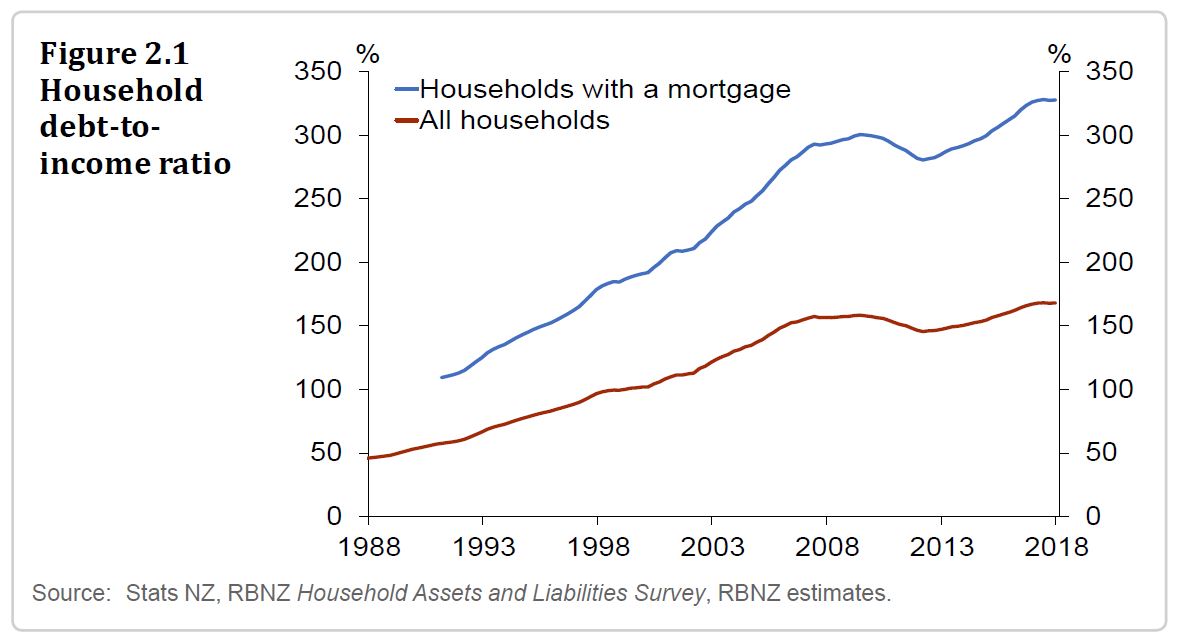

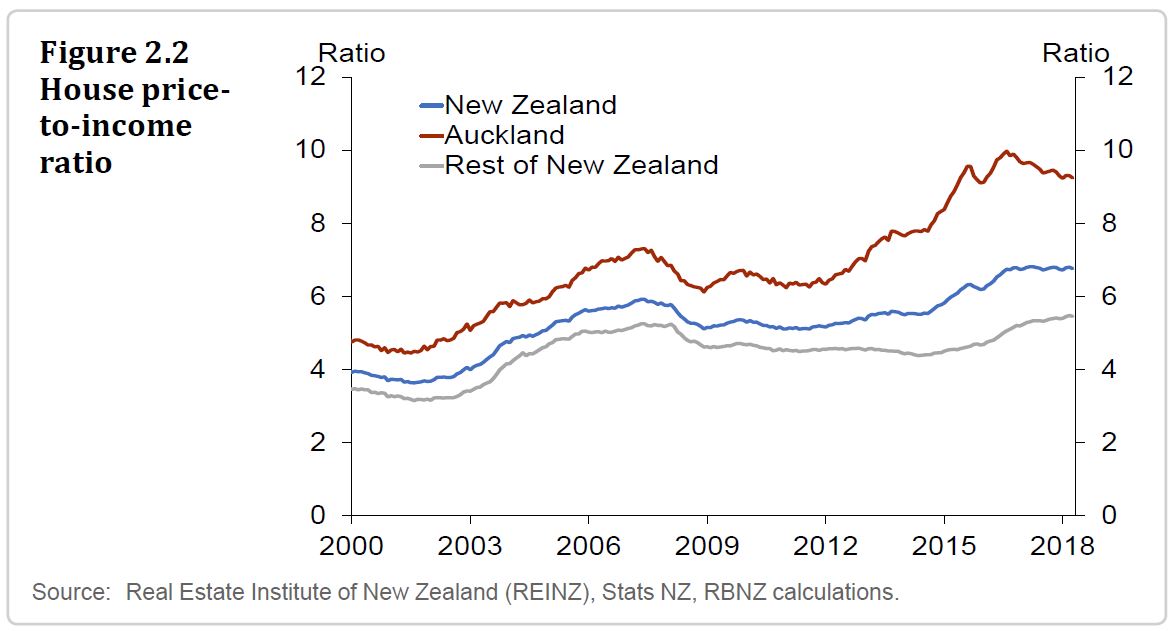

The rise in household debt since 2012 has coincided with a sharp rise in house prices, particularly in Auckland (figure 2.2). The simultaneous rise in household debt and house prices could partly reflect a self-reinforcing cycle, where bank lending has boosted house prices and, in turn, higher house prices have supported more bank lending, by increasing the value of homeowners’ collateral. But this cycle can also operate in reverse, driving down bank lending and house prices. This negative interaction can amplify the financial stability impact of a household income shock, by lowering collateral values and reducing households’ ability to service their existing debts by increasing their borrowing.

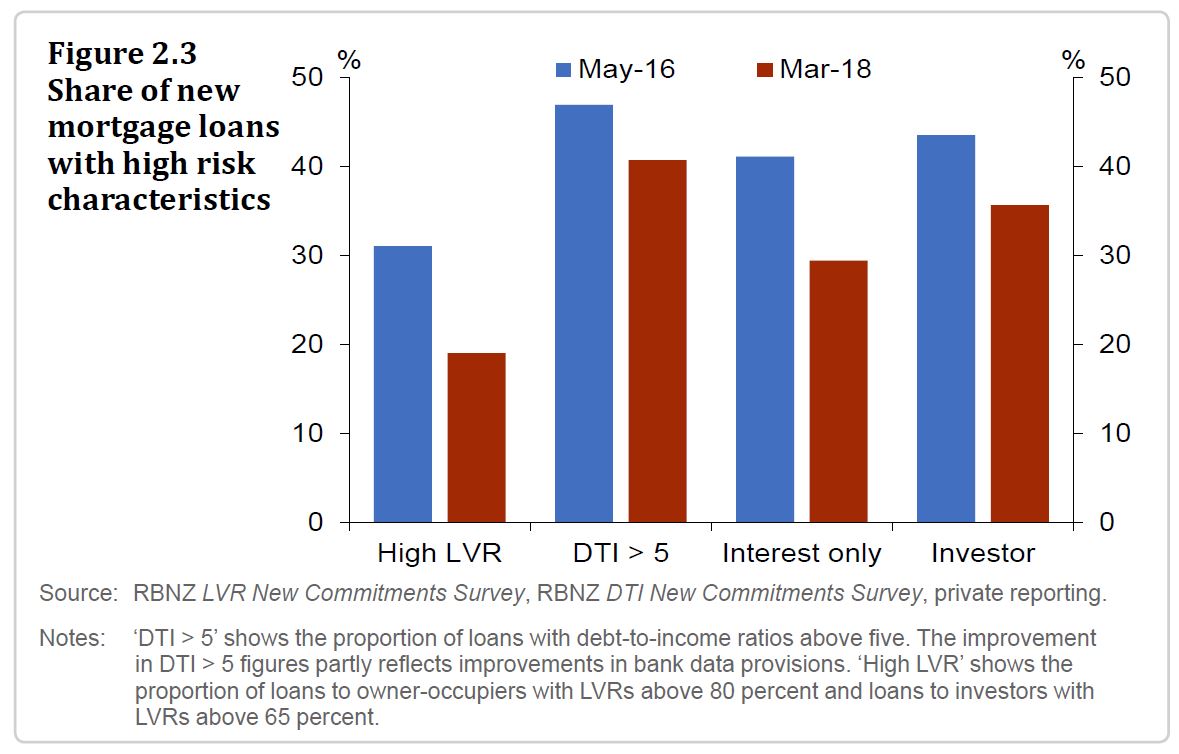

In the past two years, concerns about vulnerabilities in the household sector have caused a tightening in bank lending standards to the sector. This is partly the result of the Reserve Bank tightening its restrictions on new mortgage lending, particularly to investors, at high loan-tovalue ratios (LVRs) in October 2016.1 It also reflects actions by banks to tighten lending standards, such as the use of higher household living cost assumptions when assessing borrowers’ ability to service loans. As a result, a lower proportion of banks’ new mortgage loans have high risk characteristics than in 2016.

However, the share of new lending with high risk characteristics is still concerning. The proportion of new mortgage lending to borrowers with debt-to-income ratios above five is high compared to international peers, such as the UK. Households with this level of indebtedness are

particularly vulnerable to even modest changes in income or interest rates.

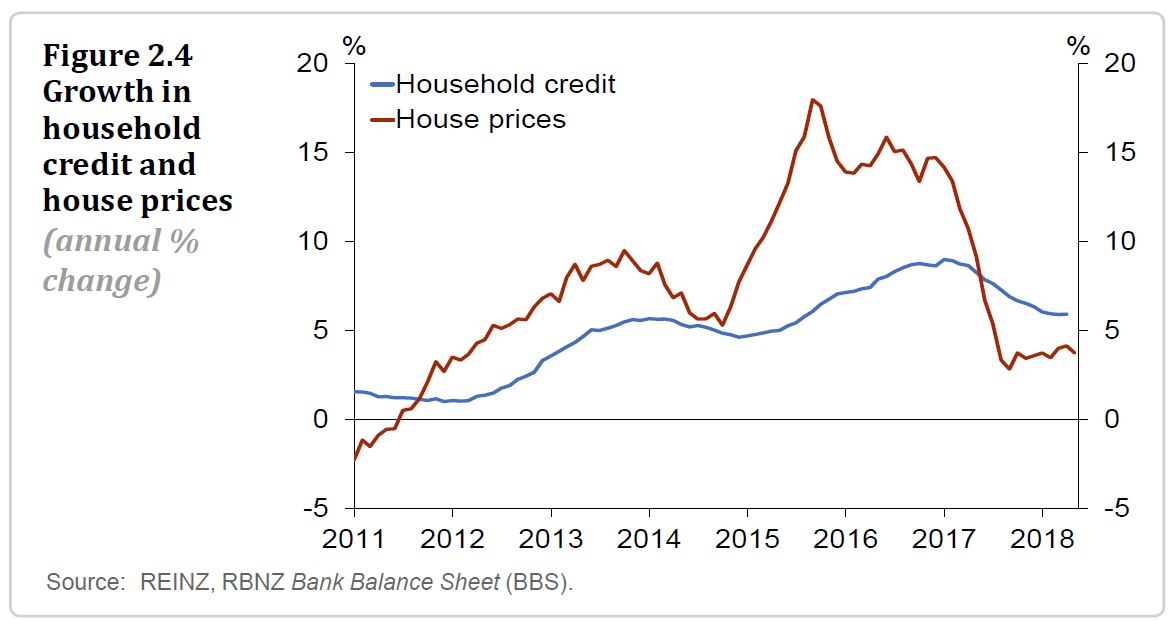

The tightening in lending standards has contributed to the annual growth rate of household credit slowing to 6 percent, slightly above the rate of income growth (figure 2.4). This has coincided with a slowdown in national house price growth, to 4 percent in the year to April. The

decline in house price inflation partly reflects the announcement and implementation of government policies (such as KiwiBuild, the extension of the bright-line test and plans for ‘loss ring-fencing’). But low mortgage rates and high net migration continue to support house prices.

The growth rates of household debt and house prices have been fairly stable over the past six months. Combined with tighter bank lending standards, this suggests the financial system’s vulnerability to household debt has not changed materially since the previous Report.

Ultimately, continued stabilisation, or a further reduction, in the growth rates of household debt and house prices, will be required before the risk to the financial system is normalised. Bank lending standards will have an influence over both. Currently, banks expect to keep their lending standards relatively tight for the rest of 2018.

In a similar vein, the dairy farming sector remains highly indebted. Most dairy farms are currently cash-flow positive, but remain vulnerable to any possible downturn in dairy prices and agriculture shocks. Reducing this bank lending concentration risk requires more prudent lending practices.

The high dairy-farm indebtedness, and the fact that LVRs were necessary, reflects that banks’ allocative efficiency – eg deciding how much to lend to whom – can be impaired due to the pursuit of short-term, rather than longer-term, profits.

The report also commented on the Australia Economy:

The Australian economy is growing steadily. But vulnerabilities have risen in recent years, particularly in the household sector, which carries a relatively high level of debt. House prices also appear stretched in some cities. Regulators have responded in a number of ways, including by requiring banks to conduct more rigorous loan serviceability assessments. These changes, coupled with a broader improvement in lending standards and an easing in housing market conditions, have improved the outlook for risks in the Australian household sector. But the Australian financial system remains vulnerable to developments that could weaken households’ ability to service their debts.