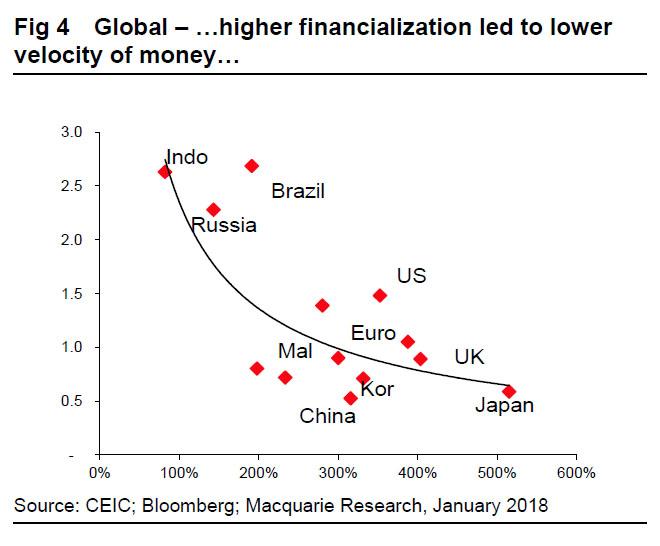

Investors are currently residing in a surreal world of low volatilities and spreads, ignoring potentially radical shifts in monetary and fiscal policies and unwinding of extraordinary measures of the last decade. Even as Central Banks (CBs) are worried about lack of volatility and excessive risk-taking, investors seem convinced that either strength of economic recovery, or return to liquidity and cost of capital supports, will ensure that volatilities are kept under control. Thus, either way, investors seem to expect that spreads would stay low and elevated valuations of various asset classes remain a permanent feature of an investment landscape.

Do we agree? In our view, financial markets have been for years drifting away from real economies. Not only is the value of financial assets at least five-to-ten times larger than the underlying economies, but also this ‘financial cloud’ is now managed by computer trading, algorithms, AI and passive investments.

This is potentially a highly destabilizing mix.

CBs are aware of dangers; hence the warnings by IMF and BIS to be ‘mindful’ of gaps between economic growth and asset bubbles. In our view, CBs and financial supervisory bodies have essentially morphed from masters of the universe into slaves of grotesquely swollen financial markets.

The key to monetary policy is no longer to guide real economies, but to avoid a collapse of the financial cloud, out of fear of what a return to traditional price discovery and volatilities might imply for wealth creation and asset prices. Over the last three decades, real economies (everything from personal savings to fixed-asset investment) have become far more tightly intertwined with asset values than with wages or productivity.

In this surreal world of complete dominance of financial assets, conventional economic rules break down and financialization and avoidance of sharp asset price contractions becomes the paramount policy objective. In our view, this implies that liquidity supports cannot be withdrawn and cost of capital (holistically defined) can never rise.

Only a return to private sector dominance and accelerating productivity (rather than recoveries driven by liquidity and/or stimulus) can ensure ‘beautiful deleveraging’. We maintain that this remains a low-probability event.

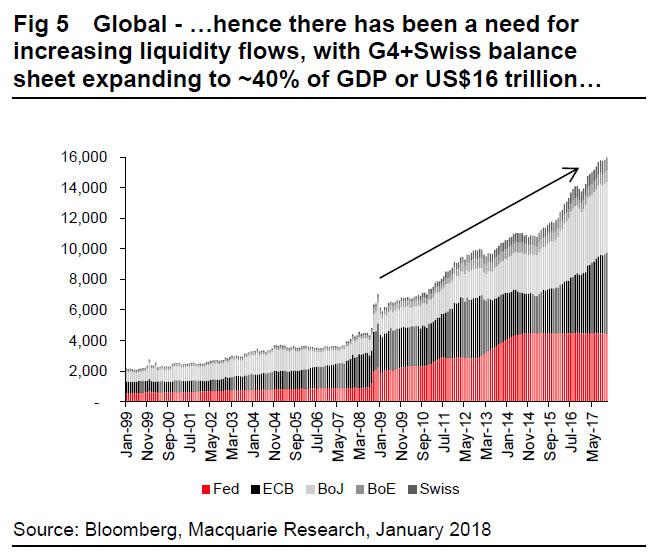

Far more likely is that the latest two-year-old recovery was due to a mix of unique and to some extent unsustainable factors, such as massive liquidity injections by key CBs (US$3.5 trillion – Mar’16 and Dec’17), coordinated monetary policies (since Feb’16) and as always, China’s stimulus.

The question therefore is what would happen to values and volatilities, if these three supports are gradually withdrawn. For example, CBs’ liquidity injection in ’18 is likely to be only ~US$0.7 trillion (turning negative in ’19) or growth of ~5%, barely enough to cover global nominal GDP (~6%).

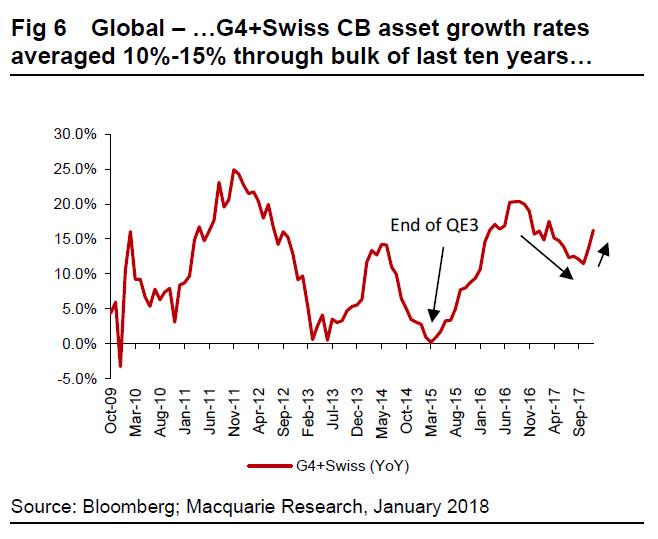

Similarly, CBs are likely to make repeated attempts to raise cost of capital, despite likely inability to do so while China is tightening, and if history is any guide, it would more than likely over-tighten. This should raise volatilities. Even if assume that recovery is indeed more sustainable, CBs (uncomfortable as they are with current excessive valuations and low volatilities) would be happy to see volatilities rise and return to some form of price discovery. The 64-dollar dollar question is whether ‘patient is sufficiently healthy to withstand pressure’.

Thus, one way or another, it seems volatilities are likely to rise at some point in ’18, and as always ‘canary’ in the coalmine would be high yield, FX and EM markets.

CBA says Matt Comyn will be the new Chief Executive Officer of the Commonwealth Bank of Australia (CBA), effective 9 April 2018, replacing Ian Narev, who announced in August that he would retire before the end of this financial year, after more than six years in the role.

An internal appointment, Matt Comyn has nearly 20 years’ experience in banking across business, institutional, retail and wealth management.

He joined the Commonwealth Bank Group in 1999 where he has held a number of senior leadership roles. In 2012 he was appointed Group Executive Retail Banking Services, which now accounts for half of the Group’s profit and also leads the development of digital products and services on behalf of the Group.

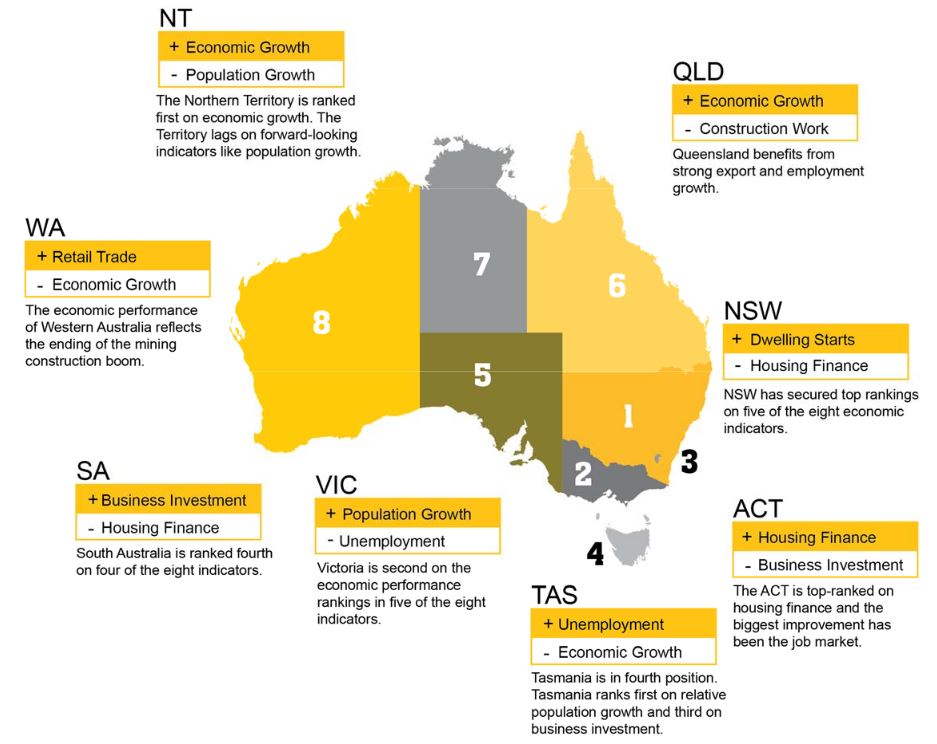

Commsec released their latest state of the state report, calculated from eight key indicators: economic growth; retail spending; business investment; unemployment; construction work done; population growth; housing finance and dwelling commencements. Housing finance and construction therefore drive the index hard.

They say that Australia’s economies are in good shape but with some differences in relative performance. NSW remains solidly on top of the economic performance rankings from Victoria while the ACT holds down third spot. Then there is a gap to Tasmania, South Australia and Queensland, and then a gap to the Northern Territory and Western Australia.

NSW has secured top rankings on five of the eight economic indicators: retail trade, dwelling starts, equipment investment, construction work and unemployment. NSW is second on economic growth and in third spot on population growth and housing finance.

Victoria is second on the economic performance rankings for five of the eight indicators: retail trade, housing finance, population growth, construction work done and equipment investment. The lowest ranking is fifth on the unemployment rate.

The ACT held on to third spot on the rankings. The biggest improvement has been the job market, with annual employment growth now the strongest in almost a decade. The ACT is top-ranked on housing finance.

There is little to separate three of the next economies with a further gap to Northern Territory and Western Australia. Tasmania has lifted from fifth to fourth position. Tasmania now is top-ranked on relative population growth and is third-placed on equipment investment and unemployment. Population growth is the strongest in 6½ years.

South Australia has eased from fourth to fifth on the performance rankings. South Australia is ranked fourth on four of the eight indicators.

Queensland remains in sixth position. But the outlook is promising with annual employment growth the fastest in the nation and just off the fastest for the state in over a decade.

The Northern Territory retains its seventh position on the economic performance rankings. The Territory is top ranked on economic growth but now lags all other economies on six of the eight indicators. Employment is now lower than a year ago in trend terms. The good news is that exports are growing strongly, up 35 per cent on a year ago.

The economic performance of Western Australia continues to reflect the ending of the mining construction boom. But employment growth was just off the strongest levels seen in five years. And annual population growth has lifted for the past four quarters.

We get a steady flow of questions from those who read our research, or follow our posts, but one question, more than any other we get asked is – Should I Buy Property Now? Many cite the real estate industry claims that now is a great time to buy – but is it really? Today we are going to explore this question, but with a caveat. This is NOT financial advice, and is simply my opinion, based our own research and surveys. Your mileage may vary. The market is different across states and locations.

Watch the video or read the transcript.

But it is an important question given that home prices appear to have reached something of a peak, and may be sliding in some areas; housing is Australia is unaffordable, as the recent Demographia report showed; banks are tightening their lending standards under regulatory pressure; net rental streams are looking pretty stressed; many households are under severe financial pressure, and mortgage interest rates are likely to rise.

In fact, we have a generation of home buyers and prospective home buyers who have only ever seen home values rise, and if you are in the property owning system, is has become a significant source of wealth creation, amplified if you are a property investor, and assisted by ultra-low interest rates, tax breaks and other incentives. But will the good times continue to roll? Not necessarily.

So to decide if now is a good time to buy, consider these questions.

First, why do you want to buy a property? Up until recently, our surveys have shown the number one reason to buy was capital appreciation and wealth building, with finding somewhere to live a poor second. But now, if you are wanting to buy to grow wealth, we say be careful, as the market dynamics are changing, and its likely prices will slide. Also there may be changes to negative gearing under a Labor government, and property investment mortgage rates are likely to rise, while rental streams are not, so more investment properties, on a cash flow basis will be under water. At the moment there are much better returns from the buoyant stock market, though of course that may change. Remember that prices crashed by 40% in Ireland, 35% in the USA and 25% in UK after the GFC. Prices can go down as well as up. Property is not a one-way bet!

But, if you are seeking to buy, for somewhere to live, and capital growth is less important to you, then it may still be a good time to transact. Prices are already down, and many sellers are accepting deeper discounts off the asking price to make a deal. In addition, if you are a first time buyer, there are state incentives and really low mortgage rates available. But remember you are still buying into a highly unaffordable market, and the capital value of your property may fall. This could turn into a paper loss, and indeed should you need to sell, a real financial hit. The way a mortgage works is you put in a deposit, and the bank lends the rest. But in a falling market, it is your deposit which is eroded. After the GFC many households in the northern hemisphere ended up in negative equity, meaning the value of their mortgage was larger than the market value of their property. As a result, people were stuck living in their properties unable to move, hoping the market would rise again. In fact, it did over the next 10 years, so now many are no longer in negative equity. But it can be a long and winding road.

Next, if you do decide to buy, do the work. First look around at property available, and recent sales, to get a sense of the market. Also look in different areas, and even different states. Often locations a little further from public transport are cheaper – but then is the trade-off worth it? Also compare new builds with existing property. Often newly constructed homes carry a premium, which just like a new car, on first use falls away. On the other hand, there are some desperate builders out there, with big projects, and few buyers, especially in the high-rise belts of Brisbane, Melbourne and Sydney, so they may do a deal. We are seeing a steady stream of people who sign up for off the plan builds, but then when it comes to getting a mortgage, they cannot find one, so cannot complete. So read the small print on these contracts. Ask yourself, what happens if you cannot complete the transaction.

It is also harder to add any value to a new property, whereas an older one may offer more potential for investment and upgrade, and this can be a way of helping to preserve value. There is an old adage – buy the worst property on the best street. This is still true, with caveats – you should check the condition of the property so you know what you are up for.

Also, do the work when it comes to a mortgage. Our research shows you can often get better mortgage rates from some of the smaller customer owned lender, as opposed to the big four by going direct to them. So shop around. Whilst using a broker may help, again we find that some of the best rates are found by borrowers who do the work themselves. Many brokers will do the right thing, and really help, but there is a risk that the commission and ownership structure of broker firms may mean they do not have access to the best rates, and they may not always be working in your best interests, so be careful.

There is more work to do also, on affordability. A lender will make an offer of a mortgage, based on your financial details as contained in the application, and supporting evidence. Remember lenders want to make a loan – it is the only game in town in terms of their profitability – but there is evidence that some lenders will offer a bigger loan, by using more aggressive living expenses, and income assumptions. That said, the industry is getting more conservative, with lower allowable loan to value ratios, and some income categories now reduced.

Just because the lender says you can have a loan, does not mean you should get the loan. The lender is looking at risk of loss from their perspective, not yours. If you have a large deposit, then the bank can assume that capital is available on default to recover their mortgage. Remember in Australia, you cannot just walk away and return the keys, the liability stays with you. So, ask the lender, not just about repayments at current interest rates, but also what happens if they rise. A good rule of thumb is catering for a 3% rise in rates. Get the lender to tell you what the revised repayments would be at this higher rate, and ask yourself if you could still make the repayments. This is important, as incomes are not growing in real terms and mortgage rates may well rise. If you cannot make the repayments at 3% high, get a smaller loan, and buy a smaller place.

You may need to build your own cash flow to test what is affordable – again do not rely on the bank for this – remember they are concerned about risk of loss to their shareholders, not to you. ASIC’s MoneySmart Budget Planner is a good starting point. Also, remember to include the transaction and stamp duty costs in your calculations.

Another area is the deposit you will need. These days you are likely to need a bigger deposit. 20% would be a good target, as this then avoids having to pay for expensive Lenders Mortgage Insurance. Above that, you will need this facility – which to be clear, protects the bank, not you!

More prospective borrowers are turning to the Bank of Mum and Dad, for help, but there are also risks attached to this arrangement – see our earlier Video Blog on the Bank of Mum and Dad. Some buyers are clubbing together to purchase, but there are risks attached to these arrangements too.

Finally, if you do buy, work on the assumption you will need to hold the property for some time – say a minimum of 3-5 years. The old trick of flicking after a year or so will not work if, as we expect prices fall. Remember too that there are additional costs to owning a property from council rates, running costs – such as electricity – and maintenance costs. Owning property is an expensive business. Make sure these costs are included in your cash flows.

So what’s the bottom line? If you are wanting to buy to put shelter over your family’s head, and can afford the mortgage, and are willing to accept a risk of loss of capital, then do the work, and it might be the right thing to do. A capital gain is by no means certain in the current climate!

But, if you are looking at property as a wealth building tool, I think you might do better to hold off, as prices are likely to slide, and the costs of an investment mortgage are on the rise. At very least look in areas around Hobart and Adelaide where value is better at the moment.

In fact, though, the only reason I can see to transact in this case is to lock in a negative gearing arrangement now, before the next Federal election. But then, that seems to me to be a long bow, and our modelling suggests that the removal of negative gearing will have only a minor impact on the market. There are a bunch of other more compelling reasons to think the market will fall.

So in summary, whatever type of borrower you are, do the work and be very careful. Prices may rise, but they can also certainly fall, and a mortgage could just be a noose around your neck.

If you found this useful, do like the post, leave a comment, and subscribe to receive future updates. Keep an eye out for our upcoming special post on Cryptocurrencies and Bit Coin.

Housing in Australia is severely unaffordable, and despite the growth in jobs, unemployment in some centres is rising. We look at the evidence. Welcome the Property Imperative Weekly to 27th January 2018.

Thanks to checking out this week’s edition of our property and finance digest. Watch the video or read the transcript.

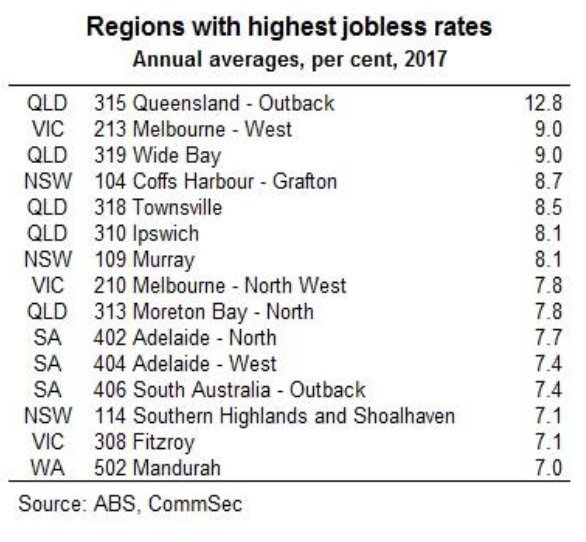

Today we start with employment data. CommSec looked at employment across regions over the last year. Despite the boom in jobs, the regional variations are quite stark, with some areas showing higher rates of unemployment, and difficult economic conditions. Unemployment has increased in several Queensland regional centres in recent years. Queensland’s coastal regional centres such as Bundaberg, Gympie, Bundaberg and Hervey Bay, known more broadly as Wide Bay (average 9.0 per cent), together with Townsville (albeit lower at 8.5 per cent) have elevated jobless rates. Unemployment also increased along the suburban fringes and city ‘spines’ such as Ipswich (8.1 per cent) in Brisbane and the western suburbs of Melbourne (9.0 per cent). In Western Australia, Mandurah, south of Perth, experienced a significant decline in the jobless rate to an average of 7.0 per cent in December from 11.2 per cent a year ago. Higher income metropolitan areas, especially in Sydney’s coastal suburbs, dominate the regions with the lowest unemployment rates. However, the corridor between Broken Hill and Dubbo has Australia’s lowest regional unemployment rate at 2.9 per cent, benefitting from agricultural, tourism and mining-related jobs growth. You will find there is a strong correlation with mortgage stress, as we will discuss next week.

The Victorian Government has reaffirmed their intent to shortly accept applications for its shared equity scheme known as HomesVic from up to 400 applicants. We do not think such schemes help affordability, they simply lift prices higher, but looks good politically. This was first announced in March 2017. The $50-million pilot initiative aims to make it easier for first-home buyers to enter the market by reducing the size of their loan, hence reducing the amount they need to save for a deposit. The initiative targets single first-home buyers earning an annual income of less than $75,000 and couples earning less than $95,000. Eligible applicants must buy in so-called “priority areas” which include 85 Melbourne suburbs, seven fringe towns and 130 regional towns and suburbs. In Melbourne, the list includes suburbs around Box Hill, Broadmeadows, Dandenong, Epping, Fishermen’s Bend, Footscray, Fountain Gate, Frankston, LaTrobe, Monash, Pakenham, Parkville, Ringwood, Sunshine and Werribee. Regional centres on the list include Ballarat, Bendigo, Castlemaine, Geelong, La Trobe, Mildura, Seymour, Shepparton, Wangaratta, Warrnambool and Wodonga. The state government said the locations were chosen in growth areas where there was a high demand for housing and access to employment and public transport. Some of these locations are where mortgage stress, on our modelling is highest – we will release the January results next week. The scheme is not available in most of Melbourne’s bayside suburbs, the leafy inner eastern suburbs or some pockets of the inner north.

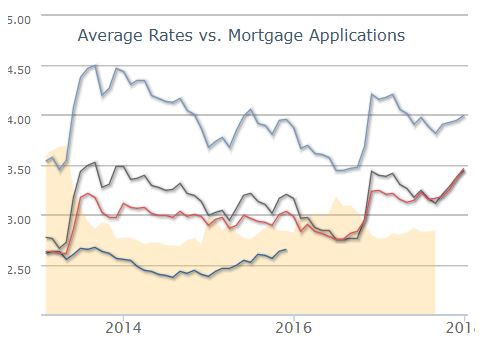

Overseas, the US Mortgage Rates continue to rise, heading back to the worst levels in more than 9 months. Rates have risen an eighth of a percentage point since last week, a quarter of a point from 2 weeks ago, and 3/8ths of a point since mid-December. That makes this the worst run since the abrupt spike following 2016’s presidential election. While this doesn’t necessarily mean that rates will continue a linear trend higher in the coming months, the trajectory is up, reflecting movements in the capital markets, and putting more pressure on funding costs globally.

The Bank for International Settlements (BIS) has published an important report “Structural changes in banking after the crisis“. The report highlights a “new normal” world of lower bank profitability, and warns that banks may be tempted to take more risks, and leverage harder in an attempt to bolster profitability. This however, should be resisted. They also underscore the issues of banking concentration and the asset growth, two issues which are highly relevant to Australia. The report says that in some countries the 2007 banking crisis brought about the end of a period of fast and excessive growth in domestic banking sectors. Worth noting the substantial growth in Australia, relative to some other markets and of particular note has been the dramatic expansion of the Chinese banking system, which grew from about 230% to 310% of GDP over 2010–16 to become the largest in the world, accounting for 27% of aggregate bank assets.

Back home, an ASIC review of financial advice provided by the five biggest vertically integrated financial institutions (the big four banks and AMP) has identified areas where improvements are needed to the management of conflicts of interest. 68% of clients’ funds were invested in in-house products. ASIC also examined a sample of files to test whether advice to switch to in-house products satisfied the ‘best interests’ requirements. ASIC found that in 75% of the advice files reviewed the advisers did not demonstrate compliance with the duty to act in the best interests of their clients. Further, 10% of the advice reviewed was likely to leave the customer in a significantly worse financial position. This highlights the problems in vertically integrated firms, something which the Productivity Commission is also looking at. The real problem is commission related remuneration, and cultural norms which put interest of customers well down the list of priorities.

The Financial Services Royal Commission has called for submissions, demonstrating poor behaviour and misconduct. It will hold an initial public hearing in Melbourne on Monday 12 February 2018. The not-for-profit consumer organisation, the Consumer Action Law Centre (CALC) said the number of Aussie households facing mortgage stress has “soared” nearly 20 per cent in the last six months, and argued that lenders are to blame. Referencing Digital Finance Analytics’ prediction that homes facing mortgage stress will top 1 million by 2019, CALC said older Australians are at particular risk. The organisation explained: “Irresponsible mortgage lending can have severe consequences, including the loss of the security of a home. “Consumer Action’s experience is that older people are at significant risk, particularly where they agree to mortgage or refinance their home for the benefit of third parties. This can be family members or someone who holds their trust.” Continuing, CALC said a “common situation” features adult children persuading an older relative to enter into a loan contract as the borrower, assuring them that they will execute all the repayments. “[However] the lack of appropriate inquiries into the suitability of a loan only comes to light when the adult child defaults on loan repayments and the bank commences proceedings for possession of the loan in order to discharge the debt,” CALC said. We think poor lending practice should be on the Commissions Agenda, and we will be making our own submission shortly.

The latest 14th edition of the Annual Demographia International Housing Affordability Survey: 2018, continues to demonstrate the fact that we have major issues here in Australia. There are no affordable or moderately affordable markets in Australia. NONE! Sydney is second worst globally in terms of affordability after Hong Kong, with Melbourne, Sunshine Coast, Gold Coast, Geelong, Adelaide, Brisbane, Hobart, Perth, Cains and Canberra all near the top of the list. You can watch our separate video where we discuss the findings and listen to our discussion with Ben Fordham on 2GB. When this report comes out each year, we get the normal responses from industry, such as Australia is different or the calculations are flawed. I would simply say, the trends over time show the relative collapse in affordability, and actually the metrics are well researched.

Fitch Ratings published its Global Home Prices report. They say price growth is expected to slow in most markets and risks are growing as the prospect of gradually rising mortgage rates comes into view this year. Their data on Australia makes interesting reading. Fitch expects Sydney and Melbourne HPI to stabilise in 2018, due to low interest rates, falling rental yields, increasing supply, limited investment alternatives and growing dwelling completions, partially offset by high population growth. Fitch expects the increase in FTB to be temporary; low income growth, tighter underwriting and rising living costs will maintain pressure on affordability for FTB. As mortgage rates are currently low, any material rate rise will weigh further on mortgage affordability and serviceability. The rising cost of living and sluggish wage growth are likely to increase pressure on recent borrowers who have little disposable income. Fitch expects mortgage lending growth to slow to around 4% in 2018, based on continued record low interest rates and stable unemployment. This will once again be offset by continued underemployment, reduced investor demand and tougher lending practices.

Finally, the latest weekly data from CoreLogic underscores the weakness in the property market. First prices are drifting lower, with Sydney down 0.4% in the past week and Melbourne down 0.1%. The indicator of mortgage activity is also down, suggesting demand is easing as lending rules tighten. But then we always have a decline over the summer break. The question is, are we seeing a temporary blip, over the holiday season, or something more structural? We think the latter is more likely, but time will tell.

So that’s the Property Imperative Weekly to 27th January 2018. If you found this useful, do like the post, add a comment and subscribe to receive future editions. Many thanks for taking the time to watch.

Despite the boom in jobs, the regional variations are quite stark, with some areas showing higher rates of unemployment, and difficult economic conditions

There is also a correlation between employment and mortgage stress, more on this when we release our latest monthly stress update next week.

CommSec says:

Generally people in metropolitan areas earn higher incomes than their cousins in the country, but employment outcomes vary considerably.

Unemployment has increased in several Queensland regional centres in recent years. Outback Queensland, which includes western and far north areas of the state, has the worst unemployment rate in the country. That said, Cairns’ average unemployment rate has improved to 5.9 per cent in 2017 from 7.8 per cent a year ago.

Queensland’s coastal regional centres such as Bundaberg, Maryborough, Gympie, Bundaberg and Hervey Bay, known more broadly as Wide Bay (average 9.0 per cent), together with Townsville (albeit lower at 8.5 per cent) have elevated jobless rates. Manufacturing jobs in Wide Bay have declined by 1,306 between 2010 and 2016 according to Regional Development Australia.

The average unemployment rate in Coffs Harbour-Grafton on the NSW Mid-North Coast deteriorated to 8.7 per cent over 2017. Pleasingly, the actual unemployment rate fell to 6.1 per cent by year-end. Construction jobs have increased, underpinned by the $3.3 billion Pacific Highway upgrade between Port Macquarie and Coffs Harbour. A further 2,970 workers are expected to be employed on the $4.36 billion Woolgoolga to Ballina road upgrade.

Unemployment also increased along the suburban fringes and city ‘spines’ such as Ipswich (8.1 per cent) in Brisbane and the western suburbs of Melbourne (9.0 per cent). Around 950 jobs were lost at Holden’s Elizabeth factory in Adelaide’s north in October, pushing up the area’s unemployment rate to 7.7 per cent.

Higher income metropolitan areas, especially in Sydney’s coastal suburbs, dominate the regions with the lowest unemployment rates. However, the corridor between Broken Hill and Dubbo has Australia’s lowest regional unemployment rate at 2.9 per cent, benefitting from agricultural, tourism and mining-related jobs growth.

Melbourne satellite city Ballarat has experienced faster and younger population growth than its regional Victorian peers, supporting jobs growth. The unemployment rate in Ballarat has fallen to 4.1 per cent from 5.3 per cent over the year to December.

In Western Australia, Mandurah, south of Perth, experienced a significant decline in the jobless rate to an average of 7.0 per cent in December from 11.2 per cent a year ago. Mandurah has benefited from job-creating projects such as the Dwellingup National Trails Centre and Quambie Park aged care expansion.

The U.S. Securities and Exchange Commission Chairman Jay Clayton spoke at Stanford University’s Stanford Rock Center for Corporate Governance and discussed his first eight months at the SEC and his enforcement, examination, market, and capital formation priorities. His comments on cryptocurriences were revealing.

SEC is clearly monitoring Initial Coin Offers (ICO) , and is concerned about the lack of protection for investors. There is significant risk of price manipulation, yet the underlying blockchain technologies offer significant opportunity.

“What I see happening in the ICO market today is ‘let me have all of the disclosure freedom of a private placement and all of the secondary activity and ability to market this of a public offering. We decided in 1934: that [having both of these at once] led to a lot of problems.”

“I think we can say that wherever the date is, it’s passed,” he said when asked whether his commission has made ICO rules clear enough yet.

“There are a lot of protections in the way stock trades on exchanges… these platforms that you’re seeing where people are trading cryptocurrencies — there are none of these rules… The opportunity for price manipulation is at orders of magnitude.”

“Blockchain, distributed ledger tech — I don’t think any of us think it’s a fad… it clearly has a applications that are gonna add efficiencies.”

“If this market continues as it is, this will not be the last enforcement actions that we take,” he said of the three ICOs the S.E.C. has moved against so far.

“Some of the offerings that we’re seeing, if the lawyers are telling them it’s OK, they’re just plain wrong,” he said, adding that taking action against lawyers knowing giving advice to ICO issuers that is against current laws is a possibility.

The world is currently witnessing a new backlash against economic globalisation. Supporters of the UK’s exit from the European Union seek to “take back control” from Brussels, while Donald Trump’s economic ethno-nationalism has promised to put “America first”.

Trump arrives at the 2018 World Economic Forum in Davos after his administration claimed that US support for China joining the World Trade Organisation (WTO) in 2001 was a mistake and having just announced large tariffs on imported solar panels. It is remarkable that the backlash that he represents emerged from the right of the political spectrum, in countries long recognised as the chief architects and beneficiaries of economic globalisation.

At the turn of the millennium, the primary opposition to globalisation was concerned with its impacts in the Global South. Joseph Stiglitz, former chief economist at the World Bank, wrote in his 2006 book Making Globalization Work that “the rules of the game have been largely set by the advanced industrial countries”, who unsurprisingly “shaped globalisation to further their own interests.” Their political influence was represented through dominant roles in organisations such as the World Bank, International Monetary Fund and WTO, and the corporate dominance of their multinationals.

In the 1990s the anti-globalisation movement opposed neoliberal economic integration from a range of perspectives, with a particular emphasis on the Global South. The movement was populated by activists, non-governmental organisations and groups with a variety of concerns: peace, climate change, conservation, indigenous rights, fair trade, debt relief, organised labour, sweatshops, and the AIDS pandemic.

The big switch

Economic globalisation in the 21st century has evolved in ways that neither its extreme proponents nor its most vocal critics predicted. A big switch has occurred, and today’s backlash against globalisation emerged from concerns about its impacts in the Global North.

In the aftermath of the Brexit vote, UK prime minister Theresa May offered a sceptical assessment at the 2017 World Economic Forum at Davos, arguing that “talk of greater globalisation can make people fearful. For many, it means their jobs being outsourced and wages undercut. It means having to sit back as they watch their communities change around them.” The US, under Trump, subsequently began renegotiating NAFTA and withdrew from the Trans-Pacific Partnership.

The polling company YouGov, in a 2016 survey of people across 19 countries, found that France, the US and the UK were the places where the fewest people believe that “globalisation has been a force for good”. In contrast, the survey found the most enthusiasm for globalisation in East and Southeast Asia, where over 70% in all countries believed it has been a force for good. The highest approval, 91%, was in Vietnam.

Most notably, China took a very different stance on globalisation than the US and the UK at the 2017 Davos gathering. China’s president, Xi Jinping, said that his country will assume the leadership of 21st century globalisation. Defending the current economic order, Xi said that China was committed to make globalisation work for everyone, which was its responsibility as “leaders of our times”.

It feels like the opposite of globalisation is happening. The negative impact of this kind of mindset and wrong priorities cannot be considered less dangerous than climate change or terrorism.

What drove the switch?

Significant proportions of the US and other countries in the Global North have experienced limited, if any, income gains in the most recent era of globalisation. Leading global inequality expert Branko Milanovic has explored changes in real incomes between 1988 and 2008 to show who particularly lost out on relative gains in income. He found two groups lost most: the global upper middle class – those between the 75th and 90th percentiles on the global income distribution, of whom 86% were from advanced economies – and the poorest 5% of the world population.

A different picture emerges in the Global South. People living in Asia accounted for the vast majority of those who experienced relative income gains from 1988 to 2008. In comparison with the 1990s, the Global South now earns a much larger share of world GDP, has more middle-income countries, more middle-class people, less dependency on foreign aid, considerably greater life expectancy, and lower child and maternal mortality.

Emerging evidence indicates that increased global trade has played a role in economic stagnation or decline for people in the north, especially in the US. MIT economist David Autor and his colleagues suggest that the “China shock” has had major redistributive effects in the US, leading to declines in manufacturing employment.

Economists had previously argued that the “losers” from trade could be compensated by transfers of wealth. Autor and his colleagues found that while there have been increases in welfare payments to regions of the US hardest hit by the trade shock, they fall far short of compensating for the income loss.

Not just globalisation

Not all of the stagnation and decline experienced in the Global North can be attributed to economic globalisation. Technological change is a big factor and national policy choices around taxation and social welfare have also played key roles in shaping inequality patterns within countries. In such a context, “globalisation” has been deployed as a scapegoat by some governments, invoking external blame for economic problems made at home.

The current backlash is not just about economic globalisation. It has involved ethno-nationalist and anti-immigrant components, for example among supporters of Trump and Brexit.

Neither does less of a backlash in the Global South necessarily mean support for neoliberal globalisation – and the optimism in countries such as Vietnam may paradoxically be a result of an earlier rejection of it. China, in particular, has not followed the same approach to economic globalisation as that which was encouraged by the US and organisations such as the IMF and World Bank in the late 20th century.

Meanwhile, many of the world’s poorest in the Global South have seen very little improvement in quality of life in recent years, yet are much more marginal and less well positioned to express their frustrations than the “losers” in countries such as the US and UK. They must not be forgotten.

A key lesson from the late 20th century is to be wary of wholesale attacks on, and sweeping defences of, 21st century economic globalisation. In light of the difficulties of establishing solidarity between “losers” in different parts of the world, the challenge of our times is for an alter-globalisation movement which addresses all of them.

Authors: Rory Horner, Lecturer, Global Development Institute, University of Manchester; Daniel Haberly, Lecturer In Human Geography, University of Sussex; Seth Schindler, Lecturer, Department of Geography, University of Sheffield; Yuko Aoyama, Professor of Economic Geography, Clark University

The Victorian Government has reaffirmed their intent to shortly accept applications for its shared equity scheme known as HomesVic from up to 400 applicants. This was first announced in March 2017.

As we said at the time:

… our analysis not only here but overseas is that they simply lifts prices by the same amount. It is a zero sum game.

Whilst we understand the political agenda, this move is unlikely to improve housing affordability and access to property.

Of course many will highlight that fact that buyers will be entering the market as prices being to go south, and might even suggest this is a further attempt to keep the property market afloat.

The scheme will allow young people to purchase a home with the state government providing up to 25 percent of the purchase price – reducing the size of the mortgage that must be taken out. When the house is sold, the government recoups its share of the proceeds.

The $50-million initiative aims to make it easier for first-home buyers to enter the market by reducing the size of their loan, hence reducing the amount they need to save for a deposit.

The initiative targets single first-home buyers earning an annual income of less than $75,000 and couples earning less than $95,000.

Eligible applicants must buy in so-called “priority areas” which include 85 Melbourne suburbs, seven fringe towns and 130 regional towns and suburbs.

In Melbourne, the list includes suburbs around Box Hill, Broadmeadows, Dandenong, Epping, Fishermen’s Bend, Footscray, Fountain Gate, Frankston, LaTrobe, Monash, Pakenham, Parkville, Ringwood, Sunshine and Werribee.

The scheme is not available in most of Melbourne’s bayside suburbs, the leafy inner eastern suburbs or some pockets of the inner north.

The state government said the locations were chosen in growth areas where there was a high demand for housing and access to employment and public transport.

Regional centres on the list include Ballarat, Bendigo, Castlemaine, Geelong, La Trobe, Mildura, Seymour, Shepparton, Wangaratta, Warrnambool and Wodonga.

Some of the locations are where mortgage stress, on our modeling is highest – we will release the January results next week.

The move was welcomed by HIA – “it is a positive scheme that addresses the rising problem of housing affordability and will help see young people achieve the Aussie dream of owning their own home faster,” senior spokesperson for HIA Kristen Brookfield said.

“HIA figures show that the typical stamp duty bill on homes in Victoria has risen by 4,000 percent since 1982. With the median price of a Melbourne dwelling at $720,417, this makes buying a house a pipe dream for so many low income young people.

“Buying a house gives an individual a sense of great pride and security. Although the HomesVic scheme is currently only open to 400 applicants, it is still a good start and we will watch its progress with keen interest,” Kristin Brookfield concluded.

After taking just one day off from the prevailing move higher, mortgage rateswere back at it today, heading back to the worst levels in more than 9 months. The average lender is now back in line with the highs seen 2 days ago on Monday afternoon. Over slightly longer time-frames, rates have risen an eighth of a percentage point since last week, a quarter of a point from 2 weeks ago, and 3/8ths of a point since mid December. That makes this the worst run since the abrupt spike following 2016’s presidential election.

Unfortunately, this trend won’t necessarily stop simply because things have “gotten bad.” While it’s true that the economic effects of higher and higher rates will eventually have a self-righting effect, that could take months–even years to play out. While this doesn’t necessarily mean that rates will continue a linear trend higher in the coming months, it does mean the current trend is not our friend, and that it would take some huge changes in bond market trading levels before it made sense to lower our defenses.