The enhanced focus on mortgage lending serviceability means that a consideration of the loan to income ratio or LTI is ever more important.

In the UK, where LTI calculations are the norm, the Bank of England first introduced limits on high LTI mortgages in 2014. These measures meant that no more than 15 per cent of mortgages issued should exceed a loan-to-income ratio of 4.5. The actions were not retrospective and few British lenders were impacted by the curbs.

The UK’s 4.5 LTI cap on 85 per cent of new lending is still in place. In June last year, Bank of England governor Mark Carney announced that the 4.5 ratio “insurance measures” will become “structural features of the UK housing market.

Last month, APRA, the prudential regulator announced that it would remove its 10 per cent benchmark on investor loan growth for banks that could confirm that their policies and practices meet a range of expectations.

But one of APRA’s expectations for banks is a commitment to develop

internal risk appetite limits on the proportion of new lending at very high debt-to-income levels (where debt is greater than six times a borrower’s income) and policy limits on maximum debt-to-income levels for individual borrowers.

So, it should be of no surprise to note that the Commonwealth Bank of Australia has announced that it has brought in its new debt-to-income measurement for borrowers.

CBA, who is the largest owner occupied mortgage lender in Australia has disclosed that it will now “monitor” loan applications with a debt-to-income ratio higher than 4.5 and will also bring in a new e-learning requirement for brokers that have not settled a CBA loan for more than a year. Applications with a DTI higher than 7.0 will be subject to a manual credit approval check.

The new measure will reportedly help the bank get a clearer picture of what its book looks like and to understand trends. Speaking of the decision, Daniel Huggins, CBA’s executive general manager, home buying, said:

At the Commonwealth Bank, we constantly review and monitor our home loan processes and policies to ensure we are maintaining our prudent lending standards and meeting our customers’ home buying needs. Our decision to implement a new debt-to-income measure is just another example of our ongoing commitment to responsible lending and meeting our regulatory commitments.

Last year, NAB introduced an LTI ratio calculation of 8 for all home loan applications. In February, this year, it was reduced to 7 a still generous 7 times.

The bank said at the time.

NAB is committed to lending responsibly and ensuring our customers can meet their home loan repayments today and into the future.

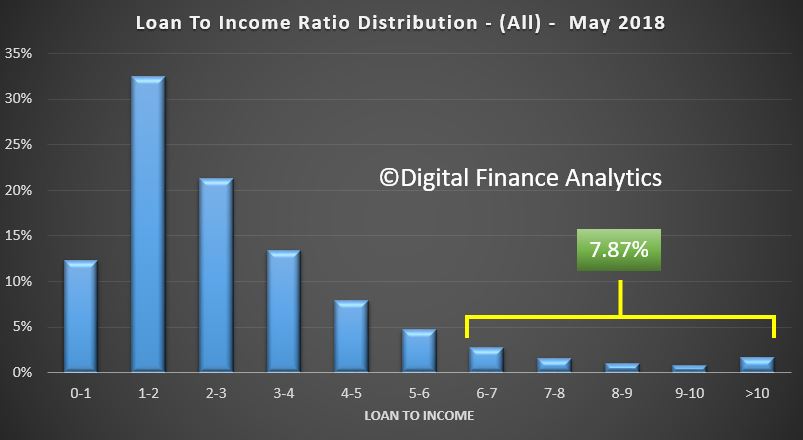

Now we have been looking at the current portfolio view of all mortgages in Australia from an LTI perspective using data from our core market model. This is based on our rolling survey of 52,000 households each year.

The relative distribution across the LTI bands highlights relative risks in the system.

We took a cut off of 6 times, in line with the APRA guidelines. On an all portfolio basis, across the country around 7.9% of all loans have a current loan to income ratio of 6 times or more. This is based on current loan values and current incomes, not those considered at the inception of the loan.

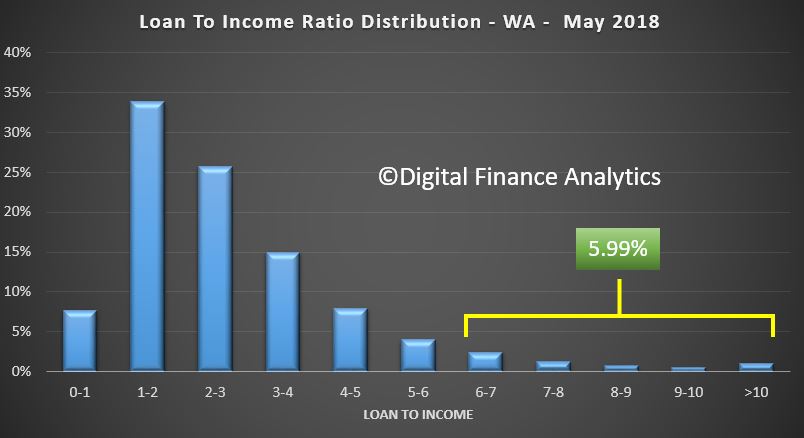

But there are some significant state variations, for example, loans in Western Australia have 6% of loans with an LTI of 6 or above. In the west the proportion is rising as incomes remain constrained, despite loans growing a little. This is thanks partly to capital being released via refinancing.

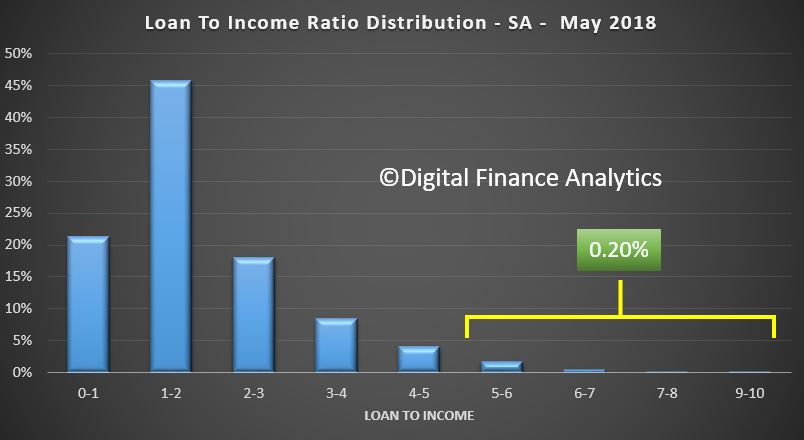

In South Australia, only a very small proportion of loans have a loan to income of 6 times or more.

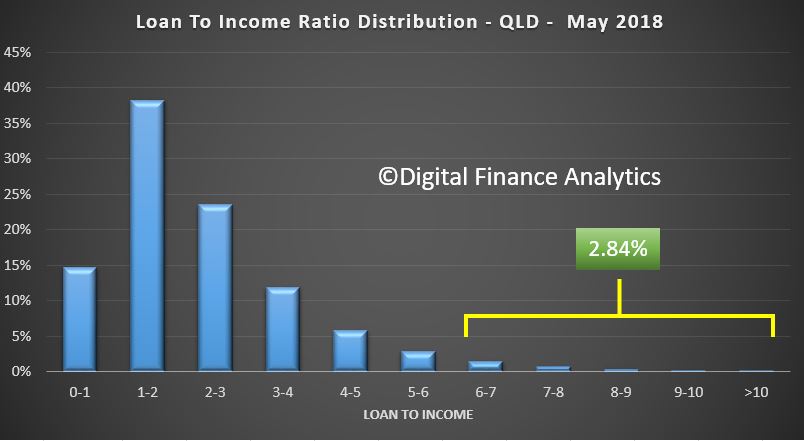

In Queensland, the total proportion above 6 times is 2.8%.

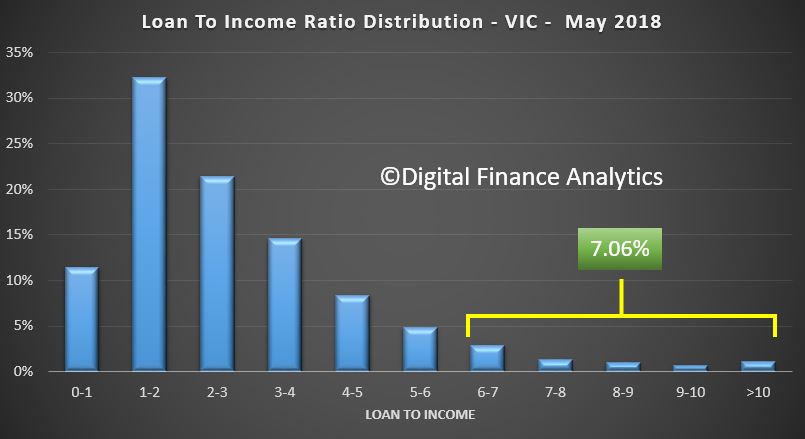

However things get more interesting in the eastern states, with 7.1% of households in Victoria holding a loan to income ratio of 6 times or higher.

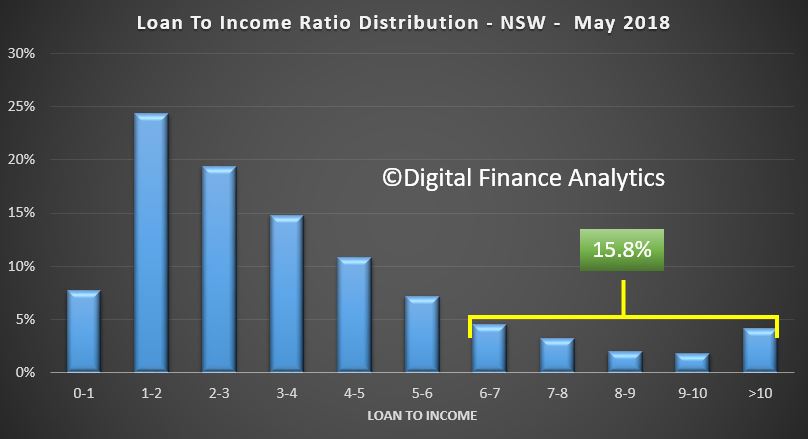

But the prize goes to New South Wales with a massive 15.8% of households currently holding loans with a loan to income ratio of 6 or more. This is of course explained by the high prices, big mortgages, and lose lending standards.

This analysis provides some insights into the pressures on households, as this higher multiples are indicative of larger payments being made to service the loan.

Thus we conclude the most severe issues will be found in NSW, where of course house prices are now firmly on the slide.

We will publish our latest mortgage stress data, to the end of May early next week. Finally, consider this, when I was a banker, the rule of thumb was 3 times one income plus 1 time the second. How the world has changed!

In Australia, lending conditions are tightening and we are already seeing the housing market slow in major cities. It is tricky to determine the extent of any fall ahead, and most predictions will of course be wrong. But the more significant factor in play is the significant change in the atmospherics around the housing sector. More are going negative. And when the largest lender in Australia signals they expect a fall, even mild, this is significant.

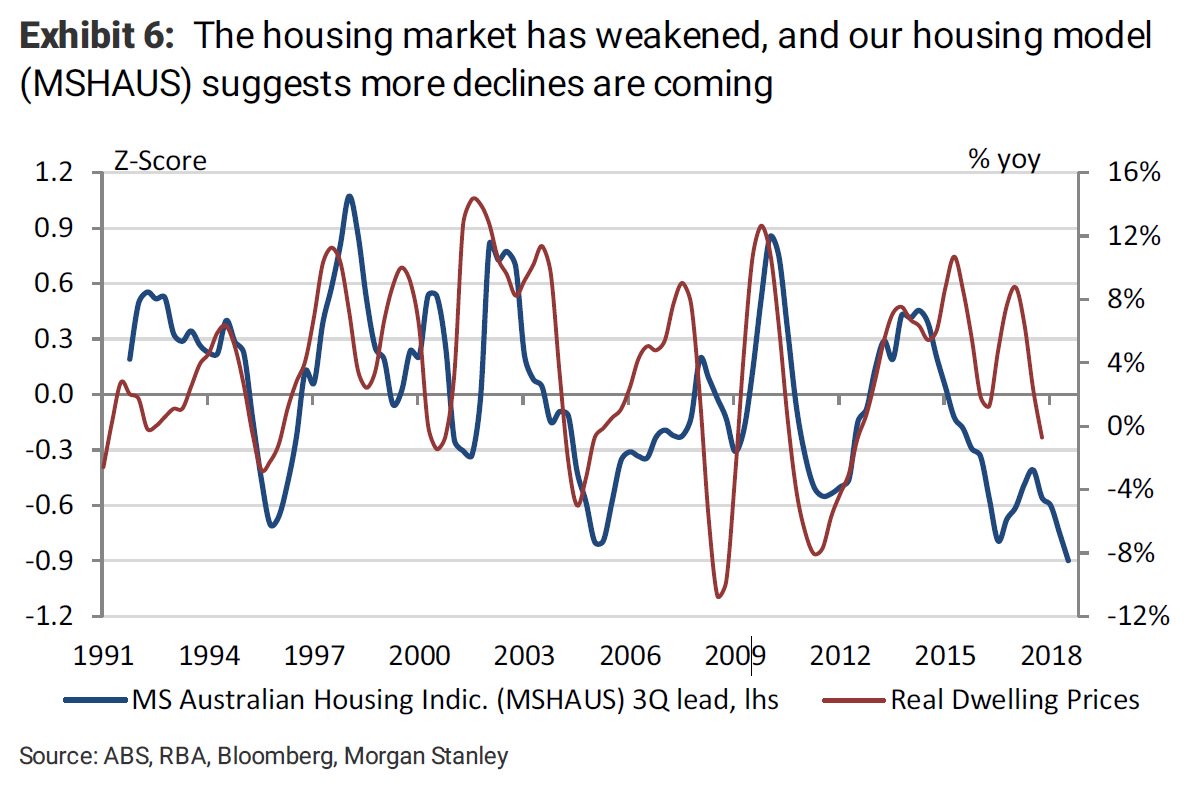

Recently Morgan Stanley said it is predicting property prices could fall by about 8% in 2018, and lending by more than a third.

Morgan Stanley suggests there’ll not only be further price weakness in the months ahead, but also the likelihood of renewed softening in building approvals. It says these two factors will likely weigh on household consumption and building activity, seeing Australian economic growth decelerate, rather than accelerate, this year.

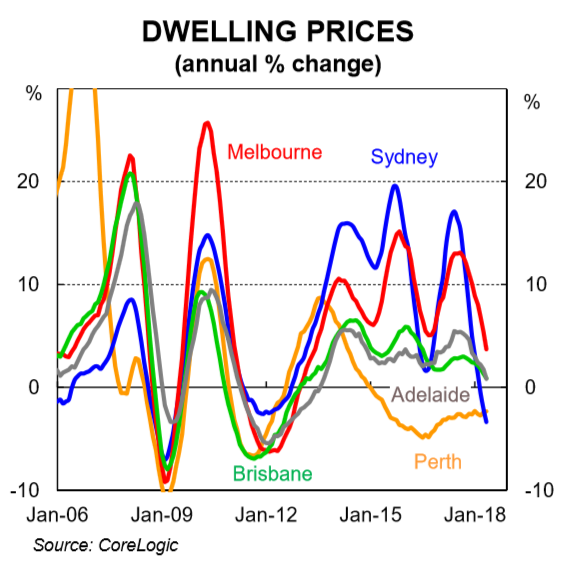

CBA has also gone negative on housing, now forecasting a mild correction. Gareth Aird, senior economist at CBA says that Australian residential property prices have fallen over the past six months. Additional declines appear likely over the next 1½ years due to a further tightening in lending standards, a continued lift in supply, potentially higher mortgage rates and more rational price expectations from would-be buyers. But he says a hard landing, however, looks unlikely and “is not our central scenario”.

Stepping through the argument he posits first dwelling prices go through both long-run super cycles as well as shorter-term cyclical trends. The recent evidence suggests that Australia’s latest residential property short-run cycle has come to an end. After a little over five years of incredibly strong property price growth, driven by Sydney and Melbourne, dwelling prices have been deflating.

It is our view that prices will to continue to deflate over the next 1½ years. Credit standards are likely to be further tightened, supply will continue to lift, mortgage rates are more likely to go up than down and buyer expectations have adjusted downwards from exuberance to more rational levels. We do not expect a hard landing, however. Population growth, driven by net immigration, is expected to remain strong. And rental growth is still positive, which ensures yields look reasonable in a low interest rate world. We also expect the unemployment rate to gradually drift lower, which means that the risk of default is low.

Author and economist Harry Dent thinks property prices could fall even more. Harry is the editor of Harry Dent Daily and has been recently touring around Australia.

And, as he told Australian Property Investor recently, ‘the real estate bubble is like a popcorn popper with different markets frothing over and peaking at different times, but all will burst ultimately.’

We can consider ourselves lucky if the property market corrects by only 10–20%. He has consistently been negative on Australian property.

“Your problem is you’ve got the second highest real estate costs compared to income in the world. I see Australia as the best house in a bad neighbourhood, but you can’t escape a global crisis.

“I think this time your real estate will come back 20, 30, 40, 50 per cent. That’s good. When young people have to pay 12 times their incomes for a house, that’s not good, so this is where the reset needs to come. I think you will have a recession this time.”

The Commonwealth Bank has agreed to sell its 37.5 per cent stake in Chinese insurer BoComm Life Insurance to a Japanese firm as reported in InvestorDaily.

CBA will sell its stake in BoComm Life Insurance Company to Japanese firm Mitsui Sumitomo Insurance Co for $688 million.

The sale will satisfy one of the conditions included in the sale of the CBA’s Australian and New Zealand insurance businesses to AIA.

CBA chief executive Matt Comyn said the transaction would be a further step in “simplifying and focusing” the bank’s portfolio.

“It follows the announcement of the proposed sale of the group’s life insurance businesses in Australia and New Zealand to AIA Group, and the strategic review of the group’s life insurance business in Indonesia,” Mr Comyn said.

The sale will be subject to the China Banking and Insurance Regulatory Commission’s regulatory approval process as well as Chinese merger clearance.

BoComm Life also plans to undertake a capital raise prior to the sale, to which the Commonwealth Bank’s pro rata contribution will be $235 million; however, this “will be separately reimbursed in full” by Mitsui Sumitomo upon completion of the sale, said CBA in a statement.

Commonwealth Bank (CBA) announces it has reached an in-principle agreement with the Australian Securities and Investments Commission (ASIC) to settle the legal proceedings in relation to claims of manipulation of the Bank Bill Swap Rate (BBSW).

As part of the in-principle settlement, CBA will acknowledge that, in the course of trading on the BBSW market in Australia on five occasions between February and June 2012, CBA attempted to engage in unconscionable conduct in breach of the ASIC Act. CBA will also acknowledge it did not have adequate policies and systems in place to monitor the trading and communications of its staff in order to prevent that conduct from occurring.

Subject to Federal Court approval of the settlement, CBA has agreed to pay a $5 million penalty, a payment of $15 million to a financial consumer protection fund and a $5 million payment towards ASIC’s costs of the litigation and its investigation. The impact of this settlement will be reflected in CBA’s 2018 Financial Year results.

CBA has also agreed to enter into an enforceable undertaking with ASIC, under which an independent expert will be appointed to review controls, policies, training and monitoring in relation to its BBSW business.

CBA and ASIC will make an application to the Federal Court for approval of the settlement

CBA released their 3Q18 trading update today. They announced an unaudited statutory net profit of approximately $2.30bn, in the quarter and unaudited cash net profit of approximately $2.35bn in the quarter. This is down 9% on an underlying basis compared with 1H18.

We see some signs of rising consumer arrears, and a flat NIM (stark contrast to WBC earlier in the week!). Expenses were higher due to provisions for regulatory and compliance.

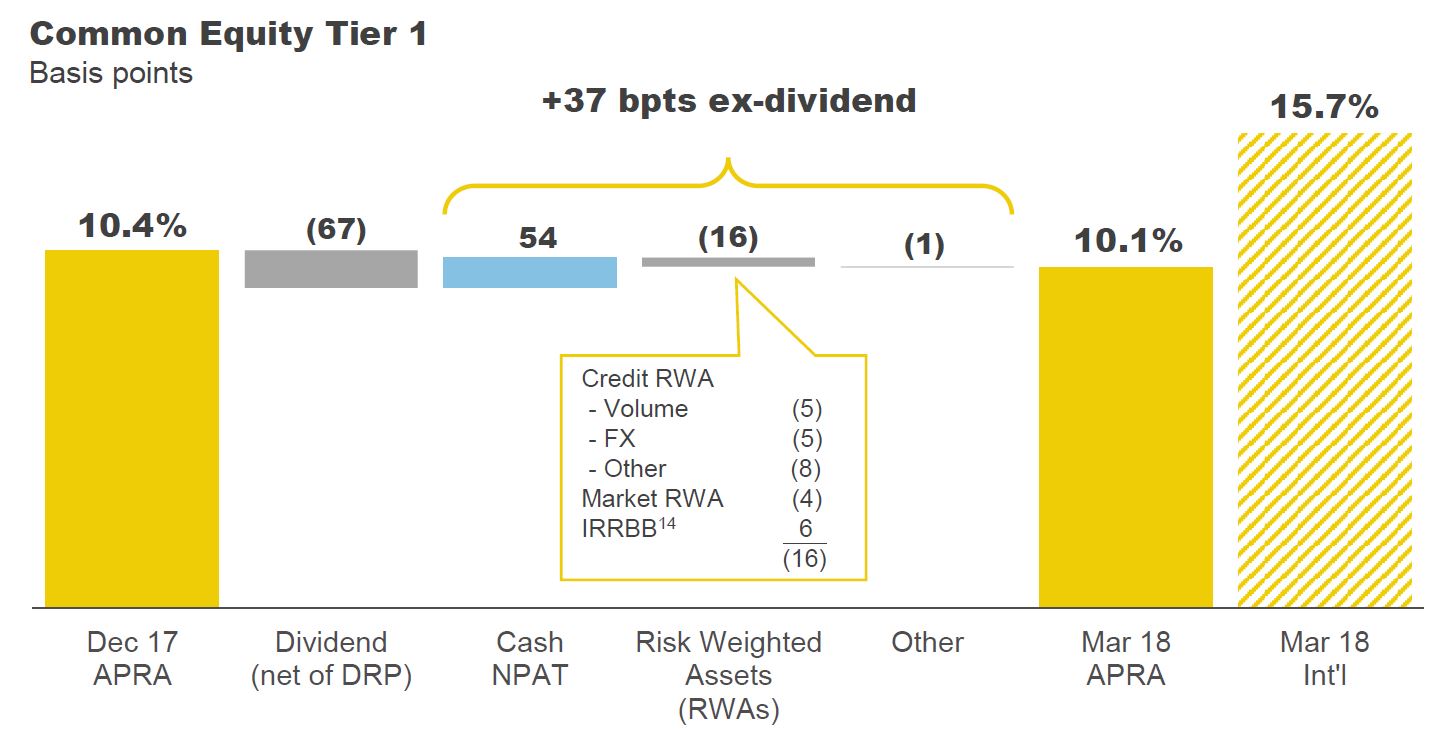

The APRA imposed increase Operational Risk regulatory capital by $1 billion (RWA of $12.5 billion) was effective 30 April 2018 and the pro-forma impact on the CET1 ratio as at 31 March 2018 is a decrease of 27 basis points, to 9.8%.

Underlying operating income decreased by 4%. Excluding the impact of two fewer days in the quarter (approximately $100m), net interest income was broadly flat. Volume growth was offset by a slight decline in Group Net Interest Margin due to customer switching from interest only to principal and interest home loans, as well as higher basis risk. Other banking income was lower driven by lower treasury and trading performance, and seasonally lower card fee income.

Underlying operating expense increased by 3%, driven by increased provisions for regulatory and compliance project spend.

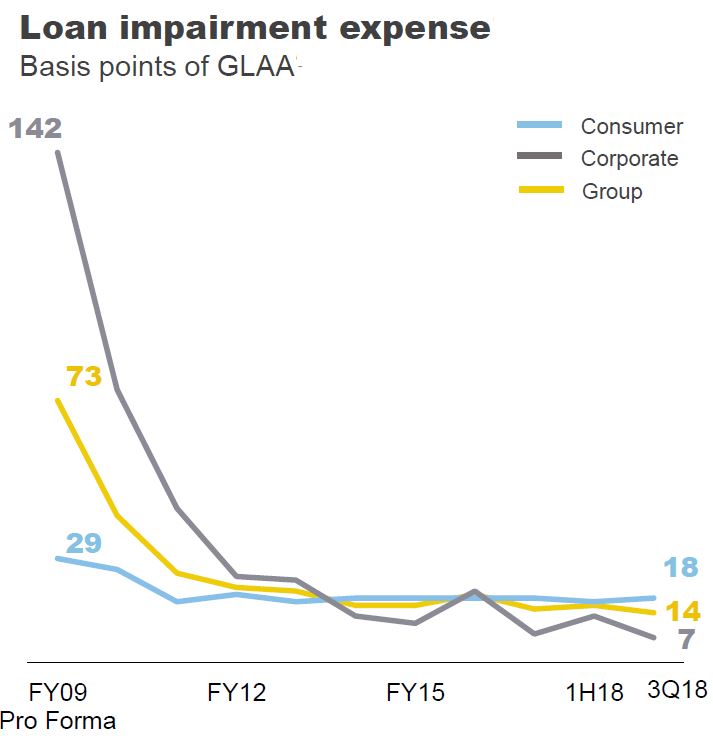

CBA says the credit quality of the Group’s lending portfolios remained sound. Loan Impairment Expense of $261 million in the quarter equated to 14 basis points of Gross Loans and Acceptances, compared to 16 basis points in 1H18.

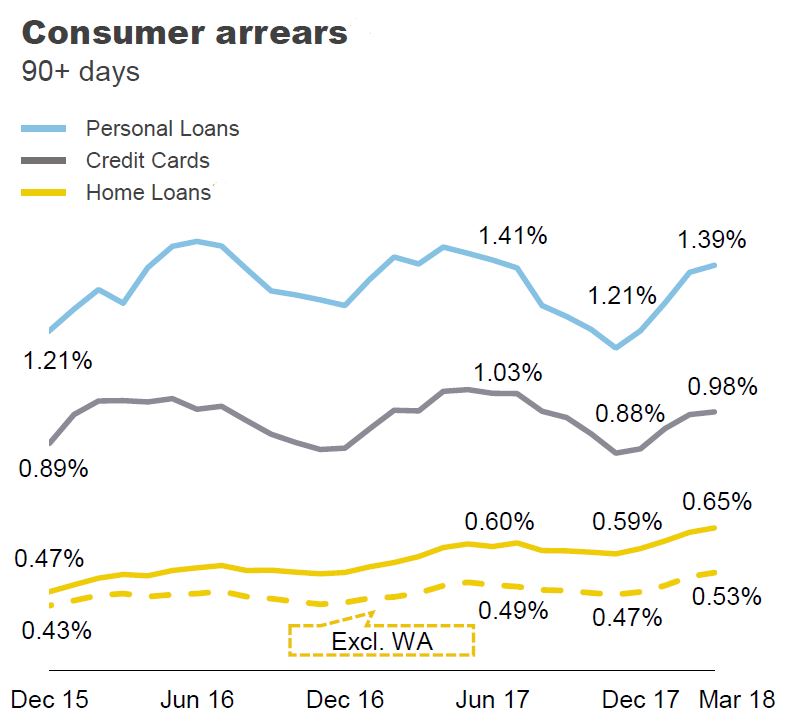

Consumer arrears were seasonally higher in the quarter. There has been an uptick in home loan arrears, influenced by a small number of customers experiencing difficulties with rising essential costs and limited income growth.

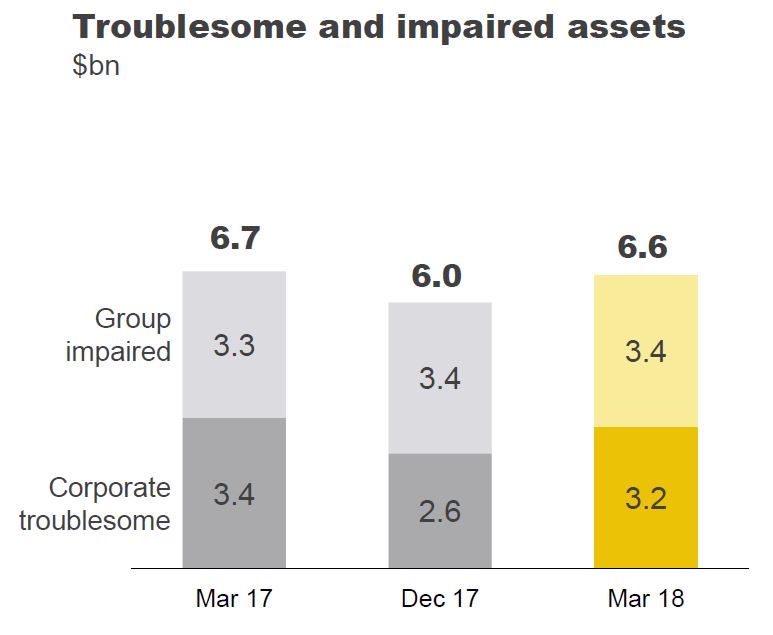

Troublesome and impaired assets increased to $6.6 billion. A small number of credits drove the increase in troublesome exposures over the quarter, with impaired assets stable.

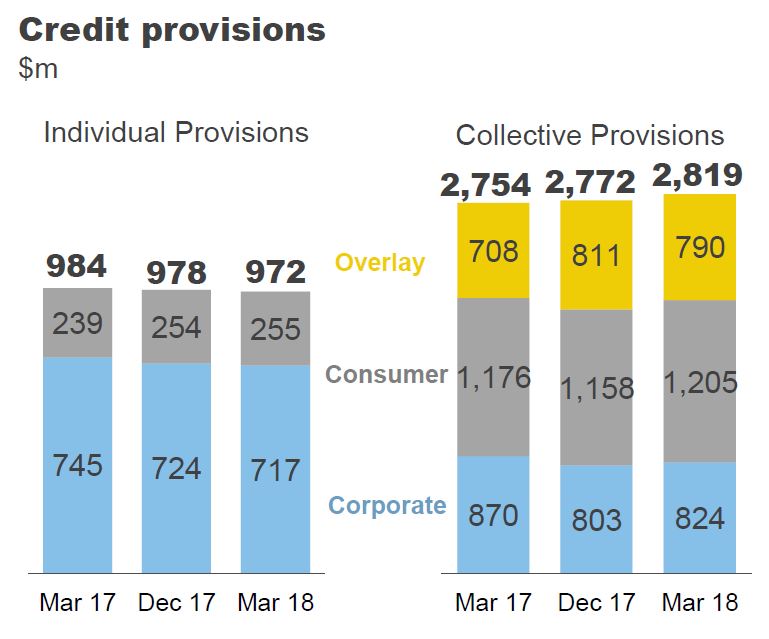

Prudent levels of credit provisioning were maintained, with Total Provisions at approximately $3.8 billion. Overall collective provisions rose.

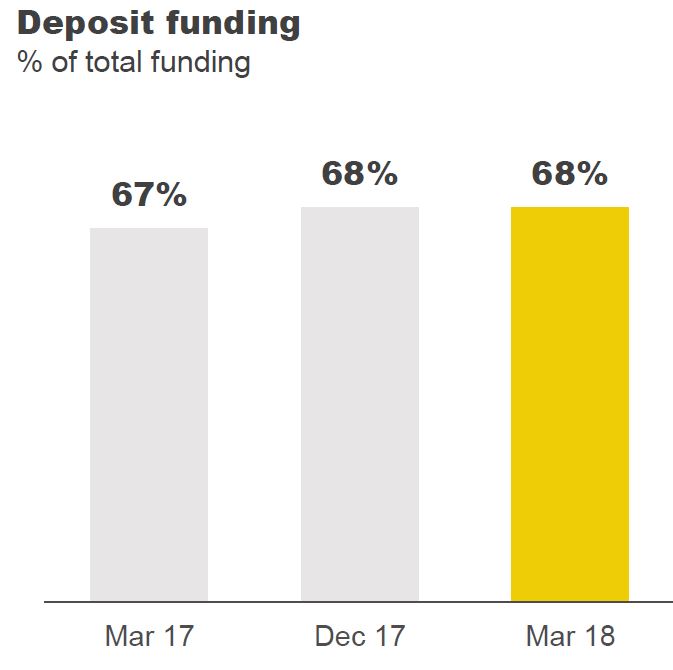

Funding and liquidity positions remained strong, with customer deposit funding at 68%

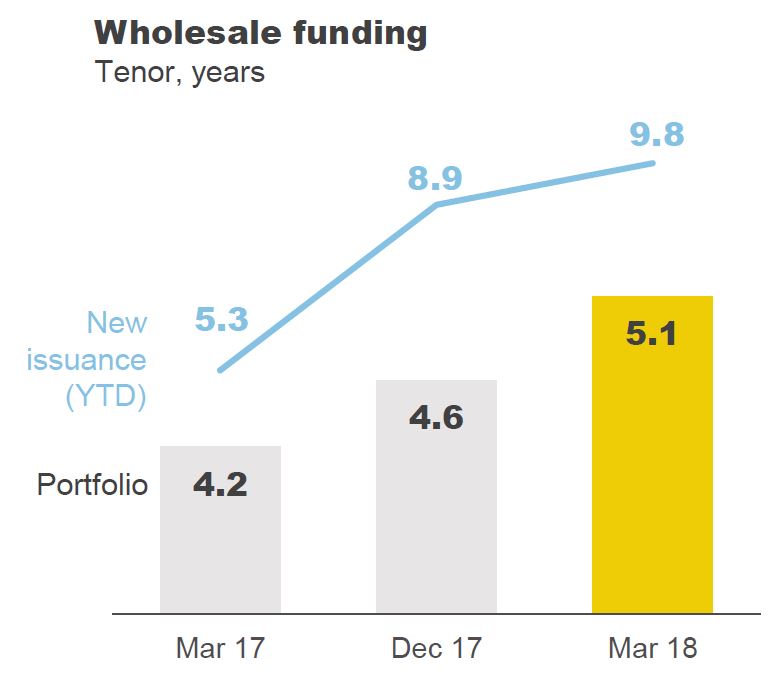

The average tenor of the long term wholesale funding portfolio at 5.1 years. The Group issued $10.2 billion of long term funding in the quarter.

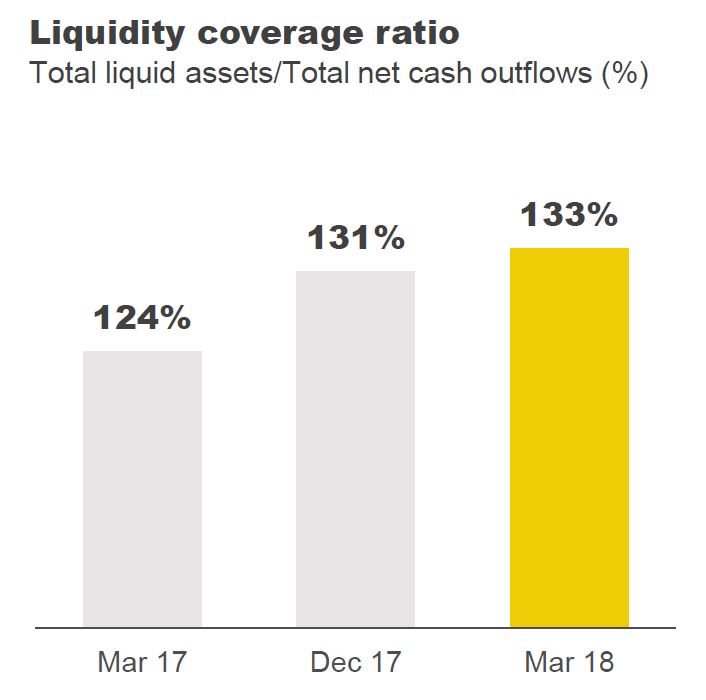

The Net Stable Funding Ratio (NSFR) was 111% at March 2018, up from 110% at December 2017. The Liquidity Coverage Ratio (LCR) increased to 133% as at March 2018, driven by higher liquid assets (up approximately $5 billion in the quarter to $144 billion13).

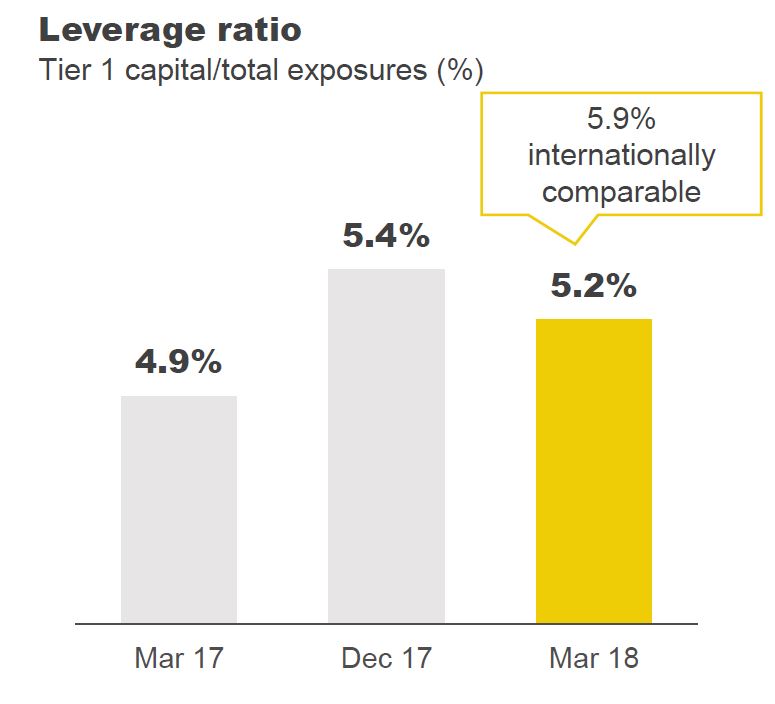

The Group’s Leverage Ratio was 5.2% on an APRA basis and 5.9% on an internationally comparable basis, 20 basis points lower than December 2017, primarily reflecting the impact of the 2018 interim dividend.

CET1 (APRA) ratio at 10.1%, up 37 bpts since Dec 17 after allowing for payment of the 2018 interim dividend

After allowing for the impact of the 2018 interim dividend (which included the issuance of shares in respect of the Dividend Reinvestment Plan), CET1 increased 37 basis points in the quarter. This was driven by capital generated from earnings, partially offset by higher Risk Weighted Assets.

Credit Risk Weighted Assets were higher in the quarter (-18 basis points), reflecting a combination of volume and foreign exchange movements, credit quality and regulatory changes.

The final tranche of Colonial debt ($315m) is due to mature in the June 2018 quarter, with an estimated CET1 impact of -7 basis points.

The Group will adopt AASB 9 on 1 July 2018. The impact will be recognised in opening retained earnings. The Group’s estimate of the pro-forma impact of AASB 9 as at 1 January 2018 is an increase in collective provisions of approximately $1,050 million (before tax) and a reduction in the CET1 ratio of approximately 26 basis points. This reflects the revised treatment of the General Reserve for Credit Losses as advised by APRA.

On 1 May 2018, APRA released the findings of the Prudential Inquiry into CBA. APRA requires CBA to increase Operational Risk regulatory capital by $1 billion (RWA of $12.5 billion). This adjustment is effective 30 April 2018, being the date the Group entered into an Enforceable Undertaking with APRA which states that CBA may apply for the removal of the adjustment only on meeting certain conditions. The pro-forma impact on the CET1 ratio as at 31 March 2018 is a decrease of 27 basis points, to 9.8%.

The sale of the Group’s Australian and New Zealand life insurance operations is expected to be completed in the December 2018 half year (subject to regulatory approvals) resulting in an uplift to the CET1 ratio of approximately +70 basis points.

Welcome to our latest digest of finance and property news to 5th May 2018.

Read the transcript, or watch the video.

We continue to be bombarded with news of more issues in the banking sector. CBA admitted that they have “lost” customer data contained on two tapes relating to almost 20 million accounts. The event happened in 2016, and they decided not to inform customers, as the data “most likely” had been destroyed. This is likely the largest data breach for a bank in Australia and goes again to the question of trust. So much customer data in a single tape drive, and passed to a third party for destruction. But there was no record of the tape arriving, and the data has not been recovered. Angus Sullivan Head of Retail at CBA said, an investigation suggests the tape were destroyed, and they chose not to inform customers at the time, despite discussing with the regulators.

We think they had a duty of care to disclose this to customers at this time, but they chose not to, because they did not put customers first. Such rich transaction data would be very valuable to criminals. I have a CBA account, and I feel uncomfortable. Why should I trust them with my data?

And of course CBA featured in the report which was published this week following a review into their culture. We discussed this in detail in a separate video “CBA’s World of Pain and The Regulators’ Wet Lettuce response”. The report says CBA’s continued financial success dulled the institution’s senses to signals that might have otherwise alerted the Board and senior executives to a deterioration in CBA’s risk profile. APRA has applied a $1 billion add-in to CBA’s minimum capital requirement.

Over the past six months, the Panel examined the underlying reasons behind a series of incidents at CBA that have significantly damaged its reputation and public standing. It found there was a complex interplay of organisational and cultural factors at work, but that a common theme from the Panel’s analysis and review was that CBA’s continued financial success dulled the institution’s senses to signals that might have otherwise alerted the Board and senior executives to a deterioration in CBA’s risk profile. This dulling was particularly apparent in CBA’s management of non-financial risks, i.e. its operational, compliance and conduct risks. These risks were neither clearly understood nor owned, the frameworks for managing them were cumbersome and incomplete, and senior leadership was slow to recognise, and address, emerging threats to CBA’s reputation. The consequences of this slowness were not grasped. So CBA agreed to put a plan in place to address the issues raised, and circulated the report to their top 500 executives, and other banks and corporates should also read the report in detail. The core message is simple, a fixation on superior financial performance at all costs, can destroy the business and customer confidence. Oh, and APRA’s $1bn capital add-in is little more than a light slap to the face.

We got results this week from Macquarie Bank who managed to lift their profitability yet again, mainly thanks to significant growth in their Capital Markets Business, plus ANZ and NAB who both revealed pressures on margin and higher mortgage loan delinquencies. They are literally banking on home loans and warned that if funding costs continue to rise they will need to lift rates. NAB’s profit was down 16% on the prior comparable period. We discussed their mortgage delinquency trends as part of our video on Mortgage Stress “More On Mortgage Stress and Defaults”. Both banks are seeking to reduce their exposure to the wealth management sector, and focus more on selling more mortgages. Interesting timing, given the Royal Commission, and tighter lending standards.

And Genworth, the Lenders Mortgage Insurer, who underwrites loans about 80% (or 70%) in some cases also reported higher losses again. The delinquency rate increased slightly from 0.48% in 1Q17 to 0.49% in 1Q18, driven mainly by Western Australia and New South Wales (NSW). Delinquencies in mining areas are showing signs of improving. In non-mining regions there are indications of a softening in cure rates, in particular in NSW and Western Australia.

Our own latest research showed that across Australia, more than 963,000 households are estimated to be now in mortgage stress (last month 956,000). This equates to 30.1% of owner occupied borrowing households. In addition, more than 21,600 of these are in severe stress, up 500 from last month. We estimate that more than 55,600 households risk 30-day default in the next 12 months. We expect bank portfolio losses to be around 2.8 basis points, though losses in WA are higher at 5 basis points. We continue to see the impact of flat wages growth, rising living costs and higher real mortgage rates.

But there was one item in the NAB results which peaked my interest. They included this slide on the gross income distribution of households in their mortgage portfolio. Gross income is defined as total pre-tax unshaded income for the application. This can include business income, income of multiple applicants and other income sources, such as family trust income. And it relates to draw-downs from Oct 17 – Mar 18. ~35% of transactions have income over 200K for owner occupied loans, and ~47% for investment loans. Now, I recognise that NAB has a skewed demographic in their customers, but, the proportion of high income households looked odd to me. So I pulled the household income data from our surveys, including only mortgaged households. We also ask for income on a similar basis, gross from all sources. And we plotted the results. The blue bars are the household gross income across the country for mortgaged households. The next two are a replication of the NAB data sets above. Either they are very, very good at targetting high income customers, or incomes in their system are being overstated. We discussed this in a separate video “Mortgage Distribution By Income Bands”.

AMP published a 28 page response to the issues raised by the Royal Commission. They made the point that the fees for no service issue is old news. In addition, they down played the preparation of a Clayton Utz report into the issue and the firms misleading representations to ASIC. They did unreservedly apologise for their financial advice failings relating to service delivery to customers and spoke about extensive action aims to ensure these issues “never happen again.” But I am not sure they have really understood the implications for their business of the findings, despite the Chairman Catherine Brenner, following the CEO out of the door. And I am not sure they have clarity around their strategy.

But they also announced that David Murray, a well-respected financial services insider to take over the Chairman’s role. He of course was the CEO at CBA during its massive expansion into Wealth Management, and significant vertical integration – the very issues which are at the heart of the Royal Commission Inquiry. And He led the Financial Systems Inquiry, which forced capital ratios higher, but which was also very light on customer centricity. So he will be a safe pair of hands, but we wonder if he can truly transform AMP to a customer focussed business. They have a massive amount to do to deal with potential fines, repair the damaged brand and chart a path ahead. But there are in my mind some critical questions about the role and shape of the board, and how they truly inject a customer first focus. This question should be occupying the minds of all CEO’s and Boards in the sector, not just AMP.

And I have a suggestion. I think the financial services companies should have a customer board – a group of customers of the bank, who would be engaged and involved in the operations and strategic direction of the business. A strong customer Board would be able to ensure the voice of the customer is heard and the priority of customer centricity placed firmly on the agenda. And remember, there is strong evidence that companies who truly put their customers first can create superior and sustainable value for shareholders too.

Of course there are structural options too. I think is likely that the financial services sector will see a bevy of break-ups and sell-offs. NAB, for example will be selling off their MLC wealth management business, marking the end of their mass-market wealth experiment. They will retain their upper end JBWere business as part of their Private Bank, for the most affluent customers. Other players are also divesting wealth businesses, partly because they never really generated the value expected, (and frittered away shareholder funds in the process) and because of the higher risks thanks to the FOFA “Best Interests” requirement. So it raises the question of whether financial advice will be available to the masses, even via robots, and indeed whether they really need it anyway. For most people generally the approach would be pretty simple (but your mileage may vary, so this is not Financial Advice). Pay down the mortgage as fast as you can. Make sure you have adequate insurance. Don’t use consumer credit and save via an appropriate industry fund. Hardly need to pay fees to an adviser for that guidance I would have thought. Financial Advice has been over-hyped, which is why the fees grabbed by the sector are so high. Mostly it’s an unnecessary expense, in my view.

Another option to fix the Banking System would be to bring in a Glass-Steagall type regime. Glass-Steagall emerged in the USA in 1993, after a banking crisis, where banks lent loans for a long period, but funded them from short term, money market instruments. Things went pear shaped when short and long term rates got out of kilter. So The Glass-Steagall Act was brought in to separate the “speculative” aspects of banking from the core business of taking deposits and making loans. Down the track in 1999, the Act was revoked, and many say this was one of the elements which created the last crisis in the USA in 2007.

Now the Citizens Electoral Council of Australia CEC (an Australian Political Party) has drafted an Australian version of the Glass-Steagall act, and Bob Katter has announced that he will try to bring the legislation as a Private Member’s Bill called The Banking System Reform (Separation of Banks) Bill 2018. And Bob Katter has form here, in taking the lead in Parliament on Glass-Steagall, as he did on the need for a Royal Commission into the banks in 2017.

The 21st Century Glass-Steagall Act has been updated to prohibit commercial banks from speculating in the specific financial products that caused the 2008 global financial crisis, which didn’t exist in 1933, such as financial derivatives. These updates are reflected in the Australian bill. Aside from specific practices, the overriding lesson of the 2008 crash is that commercial banks should not mix with other financial activities such as speculative investment banking, hedge funds and private equity funds, insurance, stock broking, financial advice and funds management. The banks have gone far beyond traditional banking, into other financial services and speculating in derivatives and mortgage-backed securities. Consequently, they have built up a housing bubble, which is heading towards a crash and an Australian financial crisis.

The bill also addresses the question of the role and function of APRA, the financial regulator, which we believe has a myopic fixation on financial stability at all costs, never might the impact on customers, as the recent Productivity Commission review called out.

Two points. First there is merit in the Glass Steagall reforms, and I recommend getting behind the initiative, despite the fact that it will not fix the current problem of the massive debt households have. Banks were able to create loans thanks to funding being available from the capital markets, and so bid prices up. Turn that off, and their ability to lend will be curtailed ahead, which is a good thing, but the existing debts will remain. Second, some are concerned about the CEC, and its motives. The CEC, is an Australian federally registered political party which was established in 1988. From 1992 onward the CEC joined with Lyndon H. LaRouche and you can read about his policies and philosophy here. But my point is, if you need a horse, and a horse appears, ride the horse and worry less about which stable it came from. I applaud the CEC for driving the Glass Stegall agenda.

But to deal with the debt burden we have, there are some other things to consider. For example, at the moment the standard mortgage contract gives banks full recourse — if you default the bank can not only sell the property, but also get a court judgment to go after your other assets and even send you bankrupt. In the USA some states have non-recourse loans, and recent research showed that borrowers in these non-recourse states are 32 per cent more likely to default than borrowers in recourse states. This is because if the outcome of missing your mortgage payments is losing pretty much everything you own and being declared bankrupt, you will do just about anything possible to keep paying your home loan. And banks will be more likely to make riskier loans when they have full recourse. So I wonder if we should consider changes to the recourse settings in Australia, which appear to me to favour the banks over customers, and encourage more sporty lending.

Then finally, there is the idea of changing the fundamental basis of bank funding, using the Chicago Plan. You can watch our video “Popping The Housing Affordability Myth” where we discuss this in more detail and “It’s Time for An Alternative Finance Narrative” where we go into more details. Essentially, the idea is to limit bank lending to deposits they hold, and it offers a workout strategy to deal with the high debt in the system and remove the boom and bust cycles. This is not a mainstream idea at the moment, but I think the ideas are worthy of further exploration. This is something I plan to do in a later video and look at how a transition would work.

But my broader point is that we need some fresh thinking to break out of our current dysfunctional banking models. Today, they may support GDP results as they inflate home prices more, but we are at the point where households a “full of debt”. So we see higher risks in the system as the latest RBA Statement On Monetary Policy, which we discussed in our video “The RBA Sees Cake – Tomorrow”. They called out risks relating to the amount of debt in the household sector, and the prospect of higher funding costs, a credit crunch, and lower consumption should home prices fall. And the latest data shows that prices are falling in the major centres now, and auction results continue lower. I believe that the RBA’s business as usual approach will lead us further up the debt blind alley. Which is why we need more radical reform in the banking system and the regulators if we are to chart a path ahead.

On Tuesday, the Australian Prudential Regulation Authority (APRA) released the results of its prudential inquiry into Commonwealth Bank of Australia, which cited its concerns about the bank’s management of non-financial risks and made recommendations to address those issues. APRA also will apply a capital adjustment by adding AUD1 billion to CBA’s operational risk capital requirement until it is satisfied that CBA has addressed the recommendations. APRA’s inquiry results are credit negative for CBA because it exposes the bank to reputational damage and costs associated with addressing its shortcomings. Additionally, the capital adjustment will lower CBA’s Common Equity Tier 1 ratio to a pro forma 10.1% as of year-end 2017 from an actual 10.4%.

APRA’s report noted that CBA’s continued financial success negatively affected the bank’s ability to manage its operational, compliance and conduct risks. In particular, the report highlighted the board and its committees’ inadequate oversight of emerging non-financial risks; unclear accountabilities, starting with a lack of ownership of key risks; weaknesses in how issues, incidents and risks were identified and escalated and overly complex and bureaucratic decision-making processes. The report cited an operational risk-management framework that worked better on paper than in practice, supported by an immature and under-resourced compliance function. In addition, APRA criticized the bank’s remuneration framework, which before the prudential inquiry began in August 2017, had few consequences for senior management for poor risk management and compliance performance.

The report made 35 recommendations to strengthen the bank’s governance, accountability and culture, and gave the bank 60 days to provide a remedial action plan to APRA. An independent reviewer will be appointed to provide quarterly updates to APRA on CBA’s progress. The recommendations are focused on five key areas: more rigorous board- and executive-committee-level governance of non-financial risks; exacting accountability standards reinforced by remuneration practices; a substantial upgrade of the authority and capability of the operational risk management and compliance functions; questioning the appropriateness of all dealings with and decisions on customers; and cultural changes that aim for best practices in risk identification and remediation.

APRA began the inquiry after a number of incidents that have negatively affected the bank’s reputation. In August 2017, the Australian Transaction Reports and Analysis Centre began proceedings against CBA for non-compliance of the Anti-Money Laundering and Counter-Terrorism Financing Act. The same month, the Australian Securities and Investments Commission (ASIC) announced that CBA would refund more than 65,000 customers a total of approximately AUD10 million after selling them unsuitable consumer credit insurance. In March 2016, the bank’s life insurance business, CommInsure, was accused of deliberately avoiding or delaying paying claims to its customers (ASIC cleared CommInsure of any breaches of the law in March 2017). In 2014, CBA announced a review into the poor quality of advice and compliance breaches by its financial planning businesses.

The report comes against a backdrop of the ongoing Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry, which has identified conduct and culture challenges at some of Australia’s largest financial institutions. We note that the franchise dominance of Australia’s major banks and their exceptionally low credit costs during an extended period of low interest rates may have elevated the risk of complacency in their approach to operational and governance risks.

More bad news relating to CBA. They have confirmed the loss of data relating to almost 20 million accounts. The event happened in 2016, and they decided not to inform customers, as the data “most likely” had been destroyed.

The Commonwealth Bank has confirmed it lost the historical financial statements of almost 20 million accounts, but insists its customers’ information has not been compromised.

The statements, containing customers’ names, addresses, account numbers and transaction details from 2000 to 2016, were stored on two magnetic tapes which were lost by sub-contractor Fuji-Xerox last year.

When the bank became aware of the incident, it said, it ordered an independent “forensic” investigation to figure out what had happened and informed the Office of the Australian Information Commissioner (OAIC).

The inquiry, conducted by KPMG, determined the tapes had most likely been disposed of.

Commonwealth Bank’s Angus Sullivan described the incident as “unacceptable” but said the tapes did not contain any passwords or PINs that could compromise customers’ accounts.

CBA said:

Following recent media reports detailing an incident in May 2016, we want to reassure you there is no evidence of your information being compromised and you do not need to take any action.

Here is what you need to know:

There is no evidence that any customer information was compromised.

In May 2016 we were unable to confirm the scheduled destruction of two magnetic tapes used by a supplier to print bank statements. These tapes contained information including customer names, addresses, account numbers and transaction details.

They did not contain passwords or PINs which could enable fraud.

We deployed enhanced reporting and ongoing monitoring of customer accounts to ensure customers were protected. These protections are still in place today.

This was not cyber-related. CommBank’s technology platforms, systems, services, apps and websites were not compromised.

CommBank offers you a 100% security guarantee against fraud for all your accounts, where you are not at fault. We cover any loss should someone make an unauthorised transaction.

A report on the Commonwealth Bank’s governance, culture and accountability has stripped away the bank’s delusion that it is well run and a model of good governance.

The report by the Australian Prudential Regulation Authority (APRA) is a damning indictment of every aspect of CBA management, from the board of directors to executive management and even the lower levels of the bank. However, APRA has done little more than rap CBA on the knuckles.

Responsibility for fixing up CBA has been turned over to the bank itself. More could have been done, including placing conditions on CBA’s banking licence and removing board members and executives.

APRA has applied a A$1 billion add-on to CBA’s minimum capital requirement. These are the financial assets that the Commonwealth Bank is required to hold to ensure a stable banking system.

APRA has also accepted an enforceable undertaking from the CBA. This is essentially an agreement under which CBA accepts the report’s findings (but does not expressly agree with them) and promises to prepare a plan to respond to its recommendations.

There are indications in the APRA report that there will be further investigations of the conduct of bank employees.

What penalties?

The A$1 billion add-on to CBA’s capital requirements is not a penalty, despite commentary to that effect. APRA can and does require top-ups of this kind from time to time under the Banking Act to ensure security and confidence in the banking sector.

Given the Commonwealth Bank’s size and leading role in the sector, the additional capital requirement is prudent but hardly controversial. The funds will be returned to CBA when it completes the actions proposed by the enforceable undertaking.

That leaves the CBA enforceable undertaking as the principal outcome from the APRA report.

The enforceable undertaking is mostly a procedural document. For instance, CBA must submit its remedial action plan by June 30 2018.

It must have a clear and measurable set of responses and a timetable for each response, and must nominate a person responsible from the CBA executive team. CBA must also appoint an independent reviewer, approved by APRA, to report to APRA on compliance with the enforceable undertaking and the completion of items in the plan. CBA must report separately on executive pay issues.

In essence APRA has handed over the responsibility for cleaning up the management mess found at the CBA to the bank itself, despite finding that it is culturally unfit to properly manage itself.

Why should anyone take comfort from that arrangement?

APRA’s report also makes clear that the problems at the Commonwealth Bank do not stem from one specific issue. The problems affect the whole organisation of more than 45,000 employees with A$967 billion in assets.

An independent reviewer will vet what is being done and report on its success or otherwise to APRA. But that report will be made to APRA, not to the general public. We may never know what measures the bank implements as APRA has no obligation to disclose anything.

What else could have been done?

An enforceable undertaking can save the regulator the time, cost and uncertainty of taking legal action, as well as enable it to craft specific remedial actions to fit the circumstances.

But there is very little tailoring in the Commonwealth Bank’s enforceable undertaking. APRA has opted to wait and see what remedial action the bank comes up with. The regulatory touch is so light that even describing it as featherweight would be an exaggeration.

APRA could have done much more than it did. Banks require a licence and APRA is empowered by Banking Act to place conditions on these licences that restrict or limit how banks can operate.

APRA could have used this power to place immediate restrictions on CBA’s business practices, including on the size and calculation of executive compensation. One of the major findings of APRA’s report is that CBA executive compensation schemes did not provide sufficient incentives for senior executives to account for risk in their decision-making. Certainly, the criticisms of CBA management in the APRA report are sufficient to warrant this kind of action.

APRA should have queried whether these changes were sufficient. Perhaps this is part of the wait-and-see approach implied in the enforceable undertaking.

The APRA report highlights systemic problems in Australia’s leading company and premier bank, including a culture of complacency, defensiveness, insularity and overconfidence. But for all of that, and despite the financial and emotional costs borne by the Australia community, APRA’s response appears to be no more than “wait and see”.

Author: Helen Bird, Course Director, Master of Corporate Governance & Research Fellow, Swinburne Law School, Swinburne University of Technology

Commonwealth Bank of Australia (CBA) today confirmed it will implement all the recommendations contained in the Report of the Prudential Inquiry released this morning by the Australian Prudential Regulation Authority (APRA).

The Capital “hit” is 29 basis points, and reduces CBA’s 31 December 2017 CET1 ratio from 10.4% to 10.1%.

CBA Chairman Catherine Livingstone said: “Addressing the findings of the Report is a key focus for the Board and management to ensure that our governance, culture and accountability frameworks and practices are significantly improved and meet the high standards expected of us.

“Changes have been underway throughout 2017 at Board and operational levels, and have continued this year, helping to rebuild customer and community trust. This includes the process of Board renewal. Together they represent a significant change program and the APRA Report provides us with a clear roadmap for the hard work still ahead of us.

“The Board will now oversee a comprehensive response to APRA, using the Report to assess the adequacy of steps already underway, and to address the additional improvements needed to implement all its recommendations. We will also appoint an agreed, independent reviewer to report to APRA on our progress.

“We understand the scale of change which is necessary and its seriousness in order for us to become a better, stronger bank for our customers, staff, regulators and shareholders.”

CBA Chief Executive Officer Matt Comyn said: “We have embraced the Report as a critical but fair assessment of the issues facing us and we will act on its recommendations, and the requirements of the Enforceable Undertaking, in an open, transparent and timely way.

“Our current change priorities are consistent with the Report’s recommendations. We now have a detailed roadmap for ongoing change and we will work with APRA to ensure we implement all of the Report’s 35 recommendations.”

APRA Prudential Inquiry into CBA: Overview of Recommendations and CBA Change Priorities

APRA Levers of Change*

CBA Change Priorities

· More rigorous Board, Executive Committee level governance of non-financial risks.

· Development of exacting accountability standards reinforced by remuneration practices.

· Undertaking a substantial upgrading of authority and capability of the operational risk management and compliance functions.

· Injection into CBA’s DNA of the “should we” question in relation to all dealings with and decisions on customers.

· Cultural change that moves the dial from reactive and complacent to empowered, challenging, striving for best practice in risk identification and remediation.

· Strengthening the governance and management of non-financial risks at the Board and executive level.

· Changes to remuneration policies and practices to ensure greater accountability for risk, compliance and customer outcomes.

· Strengthening capability in operational risk and compliance throughout the Group supported by positive, transparent regulatory relationships.

· Renewed focus on listening to customers and improved systems and procedures for reporting and resolving customer complaints.

· Empowering staff with the tools and processes they need to manage risk better including embedding three lines of accountability as a consistent operating model.

* APRA Prudential Inquiry into CBA, p4. The full APRA Prudential Inquiry Report can be found at www.apra.gov.au.

In response to the Report, Commonwealth Bank has also entered into an Enforceable Undertaking (EU) with APRA. The key terms of the EU involve:

1. Remedial Action Plan

· Establishing an APRA-agreed remedial action plan within 60 days with clear and measurable responses to each of the Report’s recommendations supported by a timeline and executive accountabilities for completing each remedial action.

· Appointing an independent reviewer, approved by APRA, to report to APRA every three months commencing 30 September 2018, on compliance with the EU and on those items in the remedial action plan that CBA considers are nearing completion.

2. Remuneration

· Reporting to APRA by 30 June 2018 on how the findings of the Report have been reflected in remuneration outcomes for current and past executives.

· Ensuring accountability for completing items in the remedial action plan is given significant weight in the performance scorecards of the senior executive team and other staff as relevant.

3. Capital Adjustment

· APRA will apply a capital adjustment to CBA’s minimum capital requirement by adding $1 billion to the Bank’s operational risk capital requirement. The effect of this adjustment equates to 29 basis points of Common Equity Tier 1 capital and reduces CBA’s 31 December 2017 CET1 ratio from 10.4% to 10.1%.

· CBA may apply for removal of all or part of the capital adjustment when it believes it can demonstrate compliance, to APRA’s satisfaction, with the specific EU undertakings and the commitments in the remedial action plan.

Mr Comyn said: “Change starts with acknowledging mistakes. I apologise to the Bank’s customers and staff, our regulators, our shareholders and the Australian community for letting them down.

“We will make the necessary changes to become a better bank and we will be transparent about our progress. This includes establishing a much higher level of accountability and consequence for our actions and the impact we have on customers. This starts with me.”

CBA will release its Third Quarter Trading Update on 9 May 2018. In early July, subject to finalisation with APRA, CBA will provide a public update on its agreed remediation plan. An estimate of the expected financial cost of this program for the 2019 financial year will be disclosed as part of CBA’s Annual Results announcement on 8 August 2018.

CBA will report on its progress in addressing the recommendations of the Prudential Inquiry’s report. The form of this public reporting is subject to agreement with APRA on reporting mechanisms.

Commonwealth Bank remains in a strong financial position as acknowledged by the APRA Report which notes: “the undoubted financial strength and acumen of CBA, its global standing and avowed commitment of staff to servicing customers.”

Since it was announced in August 2017, APRA’s Prudential Inquiry into CBA has received the Bank’s full co-operation and active support.

The UK’s 4.5 LTI cap on 85 per cent of new lending is still in place. In June last year, Bank of England governor Mark Carney announced that the 4.5 ratio “insurance measures” will become “structural features of the UK housing market.

The UK’s 4.5 LTI cap on 85 per cent of new lending is still in place. In June last year, Bank of England governor Mark Carney announced that the 4.5 ratio “insurance measures” will become “structural features of the UK housing market.

But there are some significant state variations, for example, loans in Western Australia have 6% of loans with an LTI of 6 or above. In the west the proportion is rising as incomes remain constrained, despite loans growing a little. This is thanks partly to capital being released via refinancing.

But there are some significant state variations, for example, loans in Western Australia have 6% of loans with an LTI of 6 or above. In the west the proportion is rising as incomes remain constrained, despite loans growing a little. This is thanks partly to capital being released via refinancing. In South Australia, only a very small proportion of loans have a loan to income of 6 times or more.

In South Australia, only a very small proportion of loans have a loan to income of 6 times or more. In Queensland, the total proportion above 6 times is 2.8%.

In Queensland, the total proportion above 6 times is 2.8%. However things get more interesting in the eastern states, with 7.1% of households in Victoria holding a loan to income ratio of 6 times or higher.

However things get more interesting in the eastern states, with 7.1% of households in Victoria holding a loan to income ratio of 6 times or higher. But the prize goes to New South Wales with a massive 15.8% of households currently holding loans with a loan to income ratio of 6 or more. This is of course explained by the high prices, big mortgages, and lose lending standards.

But the prize goes to New South Wales with a massive 15.8% of households currently holding loans with a loan to income ratio of 6 or more. This is of course explained by the high prices, big mortgages, and lose lending standards. This analysis provides some insights into the pressures on households, as this higher multiples are indicative of larger payments being made to service the loan.

This analysis provides some insights into the pressures on households, as this higher multiples are indicative of larger payments being made to service the loan.